Business and Management Assignment - Financial Planning Analysis

VerifiedAdded on 2022/08/17

|12

|3263

|17

Homework Assignment

AI Summary

This assignment, completed by a student, delves into various aspects of business and financial management. Part A focuses on personal finance, analyzing a balance sheet, exploring mortgage risks, and comparing savings and investment products based on their risk-return profiles. It also examines insurance premiums and adverse selection. Part B shifts to macroeconomic concepts, examining the supply and demand model, and applying it to the impact of Brexit on the UK property market. The analysis covers factors such as household income, material costs, and interest rates, illustrating how these elements influence demand and supply, and ultimately, property prices. The assignment demonstrates an understanding of financial planning, risk assessment, and market dynamics.

Running head: BUSINESS AND MANAGEMENT

Business and management

Name of the Student:

Name of the University:

Author note:

Part A

Question 1

Business and management

Name of the Student:

Name of the University:

Author note:

Part A

Question 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BUSINESS AND MANAGEMENT

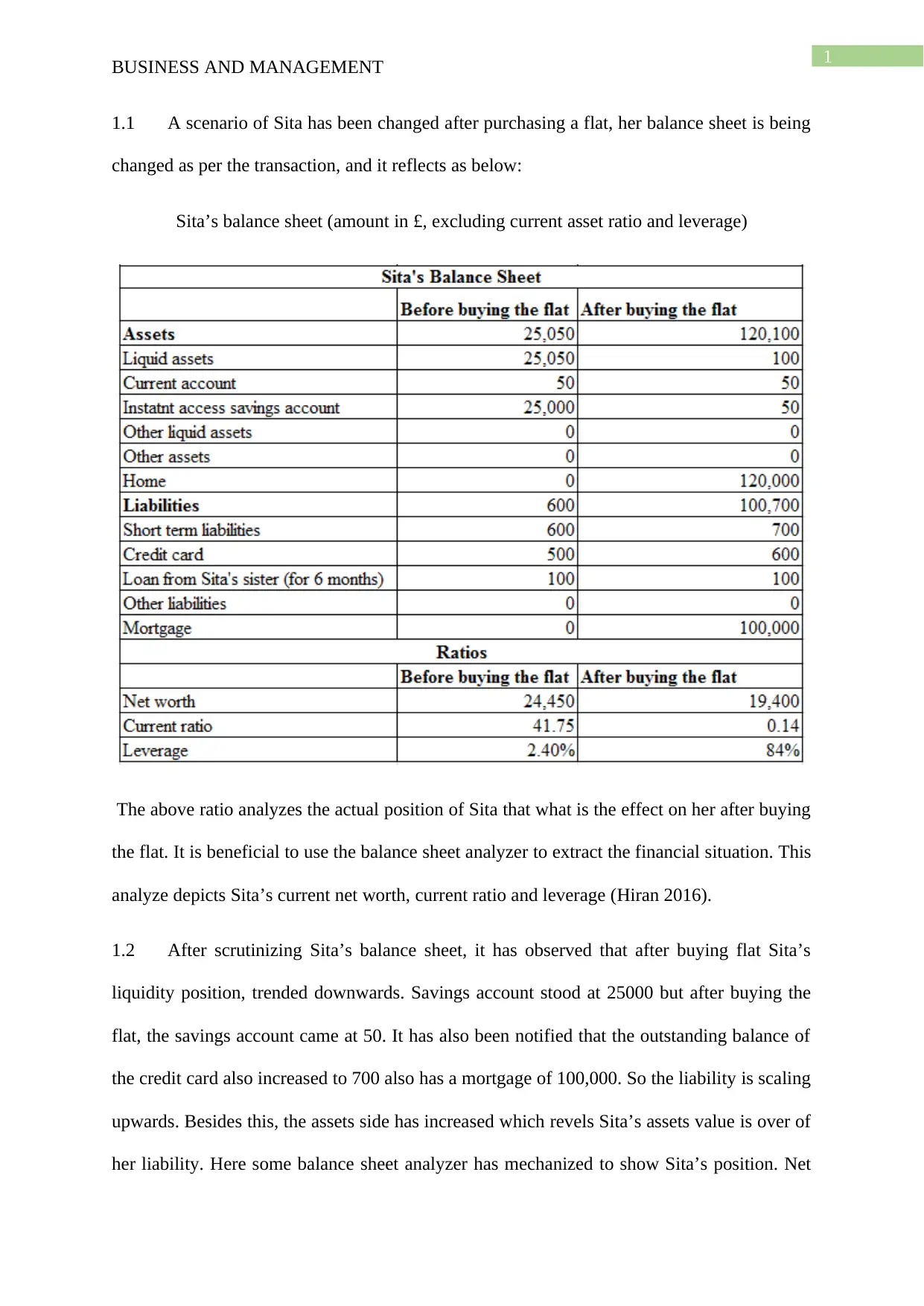

1.1 A scenario of Sita has been changed after purchasing a flat, her balance sheet is being

changed as per the transaction, and it reflects as below:

Sita’s balance sheet (amount in £, excluding current asset ratio and leverage)

The above ratio analyzes the actual position of Sita that what is the effect on her after buying

the flat. It is beneficial to use the balance sheet analyzer to extract the financial situation. This

analyze depicts Sita’s current net worth, current ratio and leverage (Hiran 2016).

1.2 After scrutinizing Sita’s balance sheet, it has observed that after buying flat Sita’s

liquidity position, trended downwards. Savings account stood at 25000 but after buying the

flat, the savings account came at 50. It has also been notified that the outstanding balance of

the credit card also increased to 700 also has a mortgage of 100,000. So the liability is scaling

upwards. Besides this, the assets side has increased which revels Sita’s assets value is over of

her liability. Here some balance sheet analyzer has mechanized to show Sita’s position. Net

BUSINESS AND MANAGEMENT

1.1 A scenario of Sita has been changed after purchasing a flat, her balance sheet is being

changed as per the transaction, and it reflects as below:

Sita’s balance sheet (amount in £, excluding current asset ratio and leverage)

The above ratio analyzes the actual position of Sita that what is the effect on her after buying

the flat. It is beneficial to use the balance sheet analyzer to extract the financial situation. This

analyze depicts Sita’s current net worth, current ratio and leverage (Hiran 2016).

1.2 After scrutinizing Sita’s balance sheet, it has observed that after buying flat Sita’s

liquidity position, trended downwards. Savings account stood at 25000 but after buying the

flat, the savings account came at 50. It has also been notified that the outstanding balance of

the credit card also increased to 700 also has a mortgage of 100,000. So the liability is scaling

upwards. Besides this, the assets side has increased which revels Sita’s assets value is over of

her liability. Here some balance sheet analyzer has mechanized to show Sita’s position. Net

2

BUSINESS AND MANAGEMENT

worth was 24450 pound but after buying the flat, her net worth is getting low and shows

19400 pounds. Now a question usually raised why Sita’s net worth is getting low even if she

has purchased an asset for her. It is simply because she has increased her liability. Therefore,

the net worth of Sita is poor. Measuring the position of liquidity her current ratio draws

attention to that inferior current ratio she is carrying after buying the flat, from 41.75 to only

0.14. She has utilized her savings account in the context of purchasing flat. Therefore, in

short, it can say Sita’s liquidity position is very low. Now the leverage indicates a high

percentage because of her increasing debt. After buying the flat, it stood at 84% (Keown

2019).

1.3

a. Sita’s mortgage is 100,000 pounds, and she needs to repay the amount in 25 years of

the term along with 2.91% interest. Now the mortgage calculator suggests her monthly

payment during the first two years is $469.54, which is 360.98 pounds (Hamilton, Huebner

and Griffiths 2016).

b. In the context of risk by taking a mortgage, Sita should be aware of her mortgage.

There are two such risks that Sita may face, interest rate risk and credit risk.

Interest rate risk

The interest rate is 2.91% in a year on Sita’s mortgage. If, in any circumstances, this

rate increases then Sita will have to pay more to the lender. It could be unaffordable to Sita,

which may force Sita into default. In that case, it is necessary to foreclose the property

(Bretscher et al 2015).

Credit risk

BUSINESS AND MANAGEMENT

worth was 24450 pound but after buying the flat, her net worth is getting low and shows

19400 pounds. Now a question usually raised why Sita’s net worth is getting low even if she

has purchased an asset for her. It is simply because she has increased her liability. Therefore,

the net worth of Sita is poor. Measuring the position of liquidity her current ratio draws

attention to that inferior current ratio she is carrying after buying the flat, from 41.75 to only

0.14. She has utilized her savings account in the context of purchasing flat. Therefore, in

short, it can say Sita’s liquidity position is very low. Now the leverage indicates a high

percentage because of her increasing debt. After buying the flat, it stood at 84% (Keown

2019).

1.3

a. Sita’s mortgage is 100,000 pounds, and she needs to repay the amount in 25 years of

the term along with 2.91% interest. Now the mortgage calculator suggests her monthly

payment during the first two years is $469.54, which is 360.98 pounds (Hamilton, Huebner

and Griffiths 2016).

b. In the context of risk by taking a mortgage, Sita should be aware of her mortgage.

There are two such risks that Sita may face, interest rate risk and credit risk.

Interest rate risk

The interest rate is 2.91% in a year on Sita’s mortgage. If, in any circumstances, this

rate increases then Sita will have to pay more to the lender. It could be unaffordable to Sita,

which may force Sita into default. In that case, it is necessary to foreclose the property

(Bretscher et al 2015).

Credit risk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BUSINESS AND MANAGEMENT

Credit risk is the default risk on the debt. This debt arises from a borrower failing to

make required payments. In that case, to reduce the lender’s risk, Sita may perform the credit

check. If credit checks would be weak for Sita, then higher risk and higher risk will lead to a

higher interest rate that Sita needs to pay. Such type of risk can arise if Sita will be unable to

pay her dues (Bluhm, Overbeck and Wagner 2016).

It would suggest to Sita that she should keep her financial liquidity position available.

Question 2

2.1

a. In terms of savings, an “Annual Equivalent Rate” is a rate in which an investor gets

on fixed deposits for year on year basis. AER is a standard measure of the interest rate, which

recognizes when the interest was credited. It allows a comparison of different account’s

return. Interest is used to calculate for getting the returns. Returns receive by adding the

interest on the original deposited amount and compounded annually. (finder.com 2019).

b. Choosing the different savings account, AER is essential. Because of AER shows the

return on the separate account. Depending on the AER, it can calculate which savings product

will give a better performance.

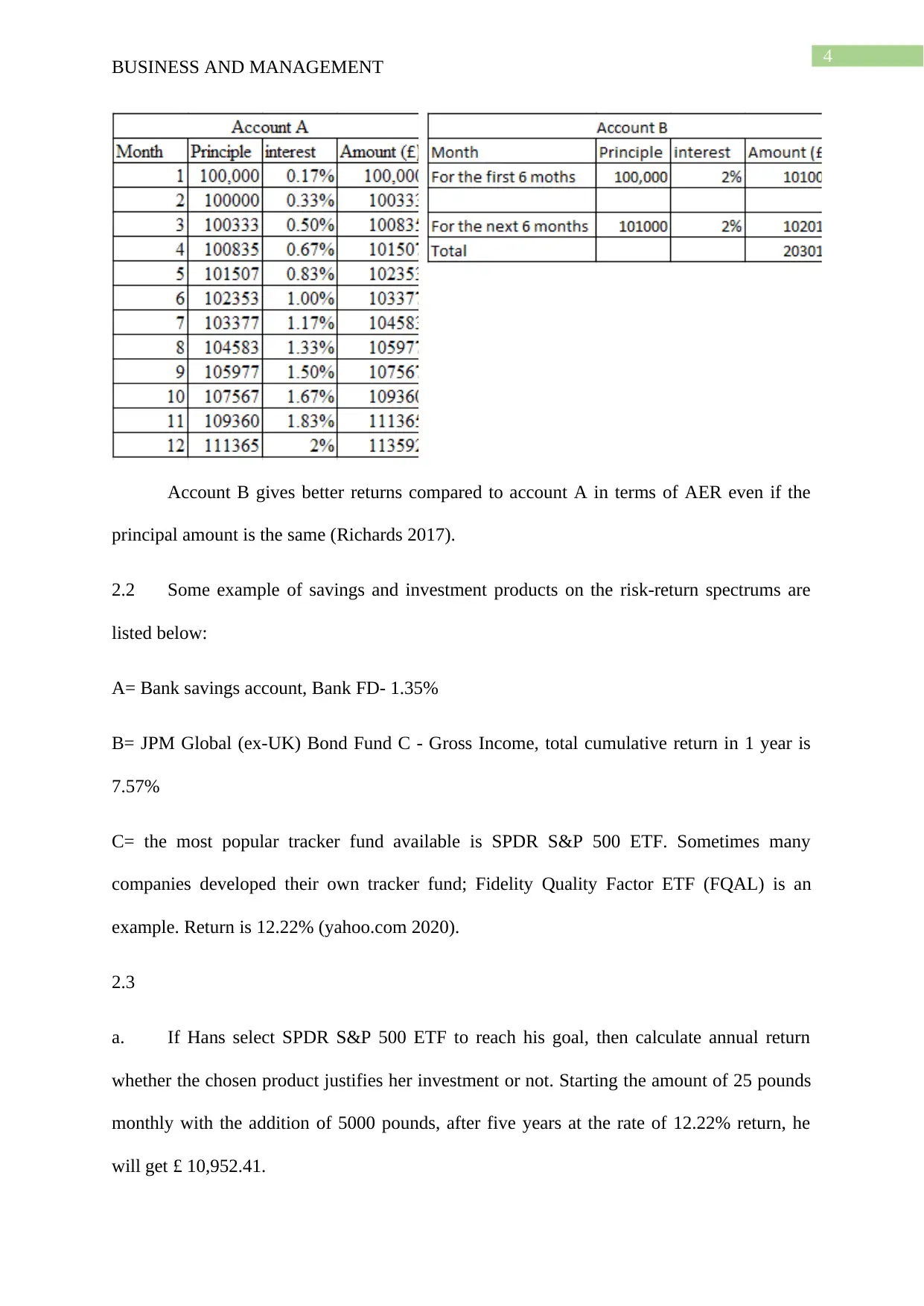

Assuming 100,000 pounds has invested in two different accounts like A and B.

AER= 2%

Account “A” pays interest every month

Account “B” pays interest every six months

BUSINESS AND MANAGEMENT

Credit risk is the default risk on the debt. This debt arises from a borrower failing to

make required payments. In that case, to reduce the lender’s risk, Sita may perform the credit

check. If credit checks would be weak for Sita, then higher risk and higher risk will lead to a

higher interest rate that Sita needs to pay. Such type of risk can arise if Sita will be unable to

pay her dues (Bluhm, Overbeck and Wagner 2016).

It would suggest to Sita that she should keep her financial liquidity position available.

Question 2

2.1

a. In terms of savings, an “Annual Equivalent Rate” is a rate in which an investor gets

on fixed deposits for year on year basis. AER is a standard measure of the interest rate, which

recognizes when the interest was credited. It allows a comparison of different account’s

return. Interest is used to calculate for getting the returns. Returns receive by adding the

interest on the original deposited amount and compounded annually. (finder.com 2019).

b. Choosing the different savings account, AER is essential. Because of AER shows the

return on the separate account. Depending on the AER, it can calculate which savings product

will give a better performance.

Assuming 100,000 pounds has invested in two different accounts like A and B.

AER= 2%

Account “A” pays interest every month

Account “B” pays interest every six months

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

BUSINESS AND MANAGEMENT

Account B gives better returns compared to account A in terms of AER even if the

principal amount is the same (Richards 2017).

2.2 Some example of savings and investment products on the risk-return spectrums are

listed below:

A= Bank savings account, Bank FD- 1.35%

B= JPM Global (ex-UK) Bond Fund C - Gross Income, total cumulative return in 1 year is

7.57%

C= the most popular tracker fund available is SPDR S&P 500 ETF. Sometimes many

companies developed their own tracker fund; Fidelity Quality Factor ETF (FQAL) is an

example. Return is 12.22% (yahoo.com 2020).

2.3

a. If Hans select SPDR S&P 500 ETF to reach his goal, then calculate annual return

whether the chosen product justifies her investment or not. Starting the amount of 25 pounds

monthly with the addition of 5000 pounds, after five years at the rate of 12.22% return, he

will get £ 10,952.41.

BUSINESS AND MANAGEMENT

Account B gives better returns compared to account A in terms of AER even if the

principal amount is the same (Richards 2017).

2.2 Some example of savings and investment products on the risk-return spectrums are

listed below:

A= Bank savings account, Bank FD- 1.35%

B= JPM Global (ex-UK) Bond Fund C - Gross Income, total cumulative return in 1 year is

7.57%

C= the most popular tracker fund available is SPDR S&P 500 ETF. Sometimes many

companies developed their own tracker fund; Fidelity Quality Factor ETF (FQAL) is an

example. Return is 12.22% (yahoo.com 2020).

2.3

a. If Hans select SPDR S&P 500 ETF to reach his goal, then calculate annual return

whether the chosen product justifies her investment or not. Starting the amount of 25 pounds

monthly with the addition of 5000 pounds, after five years at the rate of 12.22% return, he

will get £ 10,952.41.

5

BUSINESS AND MANAGEMENT

b. “SPDR S&P ETF” would be suitable for Hans, which helps to reach his financial

goal. In the case of risk-return trade-off, (Adrian, Crump and Vogt 2019) one thing needs to

understand that an investment associated with high risk gives high returns and low risk can

provide a low return. In the case of ETF, it offers high performance and returns with taking

high risk compared to the other two investments listed in the graph.

c. If Hans would not be willing to take many risks, then he could save in a bank account

for some more years. It can be suggested, that Hans should go for any safe investment like

bank savings or bank fixed deposit, which is not market-oriented if he is risk-averse.

Question 3

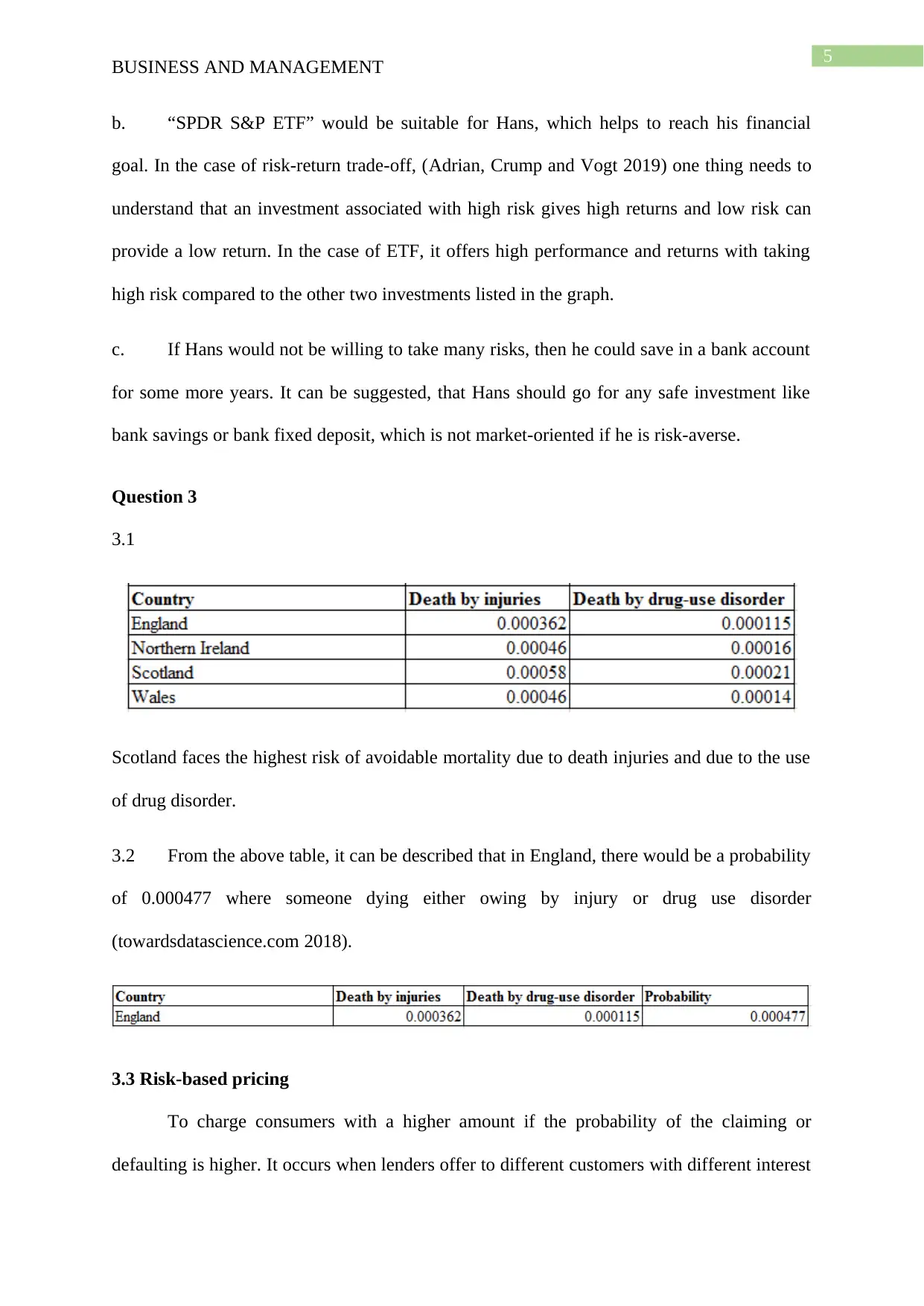

3.1

Scotland faces the highest risk of avoidable mortality due to death injuries and due to the use

of drug disorder.

3.2 From the above table, it can be described that in England, there would be a probability

of 0.000477 where someone dying either owing by injury or drug use disorder

(towardsdatascience.com 2018).

3.3 Risk-based pricing

To charge consumers with a higher amount if the probability of the claiming or

defaulting is higher. It occurs when lenders offer to different customers with different interest

BUSINESS AND MANAGEMENT

b. “SPDR S&P ETF” would be suitable for Hans, which helps to reach his financial

goal. In the case of risk-return trade-off, (Adrian, Crump and Vogt 2019) one thing needs to

understand that an investment associated with high risk gives high returns and low risk can

provide a low return. In the case of ETF, it offers high performance and returns with taking

high risk compared to the other two investments listed in the graph.

c. If Hans would not be willing to take many risks, then he could save in a bank account

for some more years. It can be suggested, that Hans should go for any safe investment like

bank savings or bank fixed deposit, which is not market-oriented if he is risk-averse.

Question 3

3.1

Scotland faces the highest risk of avoidable mortality due to death injuries and due to the use

of drug disorder.

3.2 From the above table, it can be described that in England, there would be a probability

of 0.000477 where someone dying either owing by injury or drug use disorder

(towardsdatascience.com 2018).

3.3 Risk-based pricing

To charge consumers with a higher amount if the probability of the claiming or

defaulting is higher. It occurs when lenders offer to different customers with different interest

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BUSINESS AND MANAGEMENT

rates or other loan terms. It is based on the assumed risk that the consumers will fail to pay

back their loans. Now the actuaries will utilize the data mentioned in the question. A person

who is an expert in the fields of economics, statistics and mathematics and who also helps

tom assess the risk assessment and estimation of the premiums etc. for insurance business are

called an actuary. So taking this data, actuaries will evaluate all the probable risk of death due

to injuries and drug use disorder and set the insurance premiums in the UK (Walke, Fullerton

and Tokle 2018).

3.4 Adverse selection is generally those situations where people have a higher chance of

facing an event from which they will suffer and claim insurance to a greater extent than other

people. As far as the insurance concern, adverse selection is the tendency of those people

whose jobs in danger or high-risk lifestyles. In the range of “adverse situations”, the

insurance company reduces the exposure to broad claims by limiting the coverage or raising

premiums (Handel, Hendel and Whinston 2015).

There are several ways to avoid adverse selection is firstly; government regulations

prevent health insurers from using this “adverse selection” method. Most of the health

insurance companies employ medical underwriting to avoid adverse selection.

Part B

According to the English economist, Alfred Marshall published how demand and

supply model works for the first time in his work “Principles of Economics.” Today the

model of supply and demand is one of the primary concepts in economics. The price of the

good is determined at that point where the market equals amount. To comprehend the

demand and supply model consider the following case (Goodwin 2019).

This case refers to the Brexit deal, an impact on the UK property market. The threat of

Brexit is the downgraded cause of the property market in the UK. It shows the fastest falling

BUSINESS AND MANAGEMENT

rates or other loan terms. It is based on the assumed risk that the consumers will fail to pay

back their loans. Now the actuaries will utilize the data mentioned in the question. A person

who is an expert in the fields of economics, statistics and mathematics and who also helps

tom assess the risk assessment and estimation of the premiums etc. for insurance business are

called an actuary. So taking this data, actuaries will evaluate all the probable risk of death due

to injuries and drug use disorder and set the insurance premiums in the UK (Walke, Fullerton

and Tokle 2018).

3.4 Adverse selection is generally those situations where people have a higher chance of

facing an event from which they will suffer and claim insurance to a greater extent than other

people. As far as the insurance concern, adverse selection is the tendency of those people

whose jobs in danger or high-risk lifestyles. In the range of “adverse situations”, the

insurance company reduces the exposure to broad claims by limiting the coverage or raising

premiums (Handel, Hendel and Whinston 2015).

There are several ways to avoid adverse selection is firstly; government regulations

prevent health insurers from using this “adverse selection” method. Most of the health

insurance companies employ medical underwriting to avoid adverse selection.

Part B

According to the English economist, Alfred Marshall published how demand and

supply model works for the first time in his work “Principles of Economics.” Today the

model of supply and demand is one of the primary concepts in economics. The price of the

good is determined at that point where the market equals amount. To comprehend the

demand and supply model consider the following case (Goodwin 2019).

This case refers to the Brexit deal, an impact on the UK property market. The threat of

Brexit is the downgraded cause of the property market in the UK. It shows the fastest falling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUSINESS AND MANAGEMENT

in six years and sales have degraded in two decades. According to the Royal Institution of

Chartered Surveyors, sales expectations for the next three months will decrease. There was a

balance of a 28% difference between the number of anticipating increases and anticipating

decreases. The EY item club- an economic forecasting group warns that house price could

fall by up to 5% this year if the UK exit from EU without an agreement and if there would be

an agreement, then the cost could rise 2% over 2019. Many estate agents said in an interview

that the market in December is “tranquil” because of Christmas Eve and such uncertainty of

Brexit (Dhingra et al 2016). This deal could affect the lack of supply and affordability with

the stock levels, which may further cause the declining interest of the buyer. At the end of

2018, real household disposable income was 1500 pounds, which is remarkably lower than

the official budget. Such half of this income hit due to higher inflation. If household

disposable income hits in the economy inflation will take place for that people decrease their

demand and because of lacking the stock levels supply was also decreased, so the price will

be declined but the relativity strength of the demand is more than the supply. Material cost

may increase due to the Brexit deals, which fueled fears of slow growth for the contractors.

Some consultancy firms found that the cost of construction would increase by 5.3% in the

next year. Therefore, it is a fear of the subdued market. Demand will decrease in the

economy. If the Brexit comes with no deal, the inflation will infuse in the UK economy, and

then the Bank of England will forcefully raise the interest rate, and then demand the property

market will affect.

Extract 1 illustrates the price will fall due to supply, and demand has declined;

therefore, demand and supply curve will shift leftward. UK house price drop at the fastest

rate in six years because of Brexit. The outlook of the sales is very weakest in two decades,

according to Britain’s surveyors. As per the Royal Institute of Chartered Surveyors,suggests

the declining factors like several inquiries, agreed sales and new instructions will be shown in

BUSINESS AND MANAGEMENT

in six years and sales have degraded in two decades. According to the Royal Institution of

Chartered Surveyors, sales expectations for the next three months will decrease. There was a

balance of a 28% difference between the number of anticipating increases and anticipating

decreases. The EY item club- an economic forecasting group warns that house price could

fall by up to 5% this year if the UK exit from EU without an agreement and if there would be

an agreement, then the cost could rise 2% over 2019. Many estate agents said in an interview

that the market in December is “tranquil” because of Christmas Eve and such uncertainty of

Brexit (Dhingra et al 2016). This deal could affect the lack of supply and affordability with

the stock levels, which may further cause the declining interest of the buyer. At the end of

2018, real household disposable income was 1500 pounds, which is remarkably lower than

the official budget. Such half of this income hit due to higher inflation. If household

disposable income hits in the economy inflation will take place for that people decrease their

demand and because of lacking the stock levels supply was also decreased, so the price will

be declined but the relativity strength of the demand is more than the supply. Material cost

may increase due to the Brexit deals, which fueled fears of slow growth for the contractors.

Some consultancy firms found that the cost of construction would increase by 5.3% in the

next year. Therefore, it is a fear of the subdued market. Demand will decrease in the

economy. If the Brexit comes with no deal, the inflation will infuse in the UK economy, and

then the Bank of England will forcefully raise the interest rate, and then demand the property

market will affect.

Extract 1 illustrates the price will fall due to supply, and demand has declined;

therefore, demand and supply curve will shift leftward. UK house price drop at the fastest

rate in six years because of Brexit. The outlook of the sales is very weakest in two decades,

according to Britain’s surveyors. As per the Royal Institute of Chartered Surveyors,suggests

the declining factors like several inquiries, agreed sales and new instructions will be shown in

8

BUSINESS AND MANAGEMENT

December. Sales expectations were either negative or flat in every region of the UK from

January to March. As indicating declining sales, the aggregate demand in the economy will

decrease so that the individual demand curve will change negatively (Hunt and Wheeler

2017). Like added oil to the burning fire, EY Item Club further warns the economy by saying

that house prices could fall by up to 5 percent of UK exit from the EU without the agreement.

It means people will not demand further, additionally in December Christmas will be there,

so demanding of the people will get low. So changes of demand could see in the economy.

Surveyors also highlighted that a lack of supply and affordability would hit the stock levels.

Supply will suppress. The supply curve also changes negatively.

Extract 2 to 4, except price other factors, is changing as household income hit, cost of

materials is expected to raise, bank interest rate forced to grow, arise of inflation. For these,

demand as well as supply will reduce, so there is also a tendency of shifting leftwards for

demand and supply curve. It has seen, disposable income of 1500 pounds a year hit, it was

lower than projected. Half of the revenue was hit due to the higher inflation than forecasted.

Material cost expected to rise due to the “Brexit” as this create a fear of slow growth within

the contractors, as per the latest report of the market intelligence from Turner and Townsend.

The consultancy firm found that contractors are anticipated a rise of 5.3% of cost of

construction materials. Consequently, it subdued the market and economy will demand less.

If Brexit is cause to the house price crash, market will get inflated then the Bank of England

could raise the interest rate (Breinlich et al 2017). This will lead to some correction into the

property market; again, it would worry if other factor play in the economy like rise of interest

rate. By doing, this committee is somehow trying to manage the inflation but it would not

help because rising of interest rate will create less demand in the economy, and if demand

will less supply will also be less so the both the curve will shift negatively. Therefore, the

committee has to manage the monetary policy in other way to control the inflation. However,

BUSINESS AND MANAGEMENT

December. Sales expectations were either negative or flat in every region of the UK from

January to March. As indicating declining sales, the aggregate demand in the economy will

decrease so that the individual demand curve will change negatively (Hunt and Wheeler

2017). Like added oil to the burning fire, EY Item Club further warns the economy by saying

that house prices could fall by up to 5 percent of UK exit from the EU without the agreement.

It means people will not demand further, additionally in December Christmas will be there,

so demanding of the people will get low. So changes of demand could see in the economy.

Surveyors also highlighted that a lack of supply and affordability would hit the stock levels.

Supply will suppress. The supply curve also changes negatively.

Extract 2 to 4, except price other factors, is changing as household income hit, cost of

materials is expected to raise, bank interest rate forced to grow, arise of inflation. For these,

demand as well as supply will reduce, so there is also a tendency of shifting leftwards for

demand and supply curve. It has seen, disposable income of 1500 pounds a year hit, it was

lower than projected. Half of the revenue was hit due to the higher inflation than forecasted.

Material cost expected to rise due to the “Brexit” as this create a fear of slow growth within

the contractors, as per the latest report of the market intelligence from Turner and Townsend.

The consultancy firm found that contractors are anticipated a rise of 5.3% of cost of

construction materials. Consequently, it subdued the market and economy will demand less.

If Brexit is cause to the house price crash, market will get inflated then the Bank of England

could raise the interest rate (Breinlich et al 2017). This will lead to some correction into the

property market; again, it would worry if other factor play in the economy like rise of interest

rate. By doing, this committee is somehow trying to manage the inflation but it would not

help because rising of interest rate will create less demand in the economy, and if demand

will less supply will also be less so the both the curve will shift negatively. Therefore, the

committee has to manage the monetary policy in other way to control the inflation. However,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUSINESS AND MANAGEMENT

there was no expectation to reach the interest rate 5 to 7 percent in the next three years, if it is

happen then will have more to worry about housing crash. Therefore, it cannot say that there

will be a movement of the curve even if there will have a change of price; rather there will be

a shift of curve because other factors remain change except price.

Part C

Personal Development Planning PDP is one of the structured process. It will help to

achieve the goals and designs the achievements (McKenna, Baxter and Hainey 2017).

In the above section, I have used financial planning mechanism in terms of savings,

depending on different AER. Savings or investments in a proper product is very essential not

only to achieve personal finance but also for the career, life sustainability and personal goals.

Therefore, this area needs to develop.

I will make an agenda to invest my money in a regular manner and increase the

knowledge more on market, which will help foe selecting the product.

Market related factors are the only constraints because of fluctuations; any time is not good

for investing, so there will be a market related risk.

I will exercise more related to economics journal, business magazine, increase the

ability to critically analyze the company annual report and analyze various financial website.

It would be helpful towards my investment that can make it grow and return positively.

It will take just some week; I have to examine more on the market and choose

particular financial vehicle, which will cherish my goal. Therefore, after examine the market

related thing primarily and articulate the financial plan I will start progress in this area.

BUSINESS AND MANAGEMENT

there was no expectation to reach the interest rate 5 to 7 percent in the next three years, if it is

happen then will have more to worry about housing crash. Therefore, it cannot say that there

will be a movement of the curve even if there will have a change of price; rather there will be

a shift of curve because other factors remain change except price.

Part C

Personal Development Planning PDP is one of the structured process. It will help to

achieve the goals and designs the achievements (McKenna, Baxter and Hainey 2017).

In the above section, I have used financial planning mechanism in terms of savings,

depending on different AER. Savings or investments in a proper product is very essential not

only to achieve personal finance but also for the career, life sustainability and personal goals.

Therefore, this area needs to develop.

I will make an agenda to invest my money in a regular manner and increase the

knowledge more on market, which will help foe selecting the product.

Market related factors are the only constraints because of fluctuations; any time is not good

for investing, so there will be a market related risk.

I will exercise more related to economics journal, business magazine, increase the

ability to critically analyze the company annual report and analyze various financial website.

It would be helpful towards my investment that can make it grow and return positively.

It will take just some week; I have to examine more on the market and choose

particular financial vehicle, which will cherish my goal. Therefore, after examine the market

related thing primarily and articulate the financial plan I will start progress in this area.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUSINESS AND MANAGEMENT

Reference

Adrian, T., Crump, R.K. and Vogt, E., 2019. Nonlinearity and Flight‐to‐Safety in the Risk‐

Return Trade‐Off for Stocks and Bonds. The Journal of Finance, 74(4), pp.1931-1973.

Available at: Probability concepts explained: probability distributions introduction part 2018

https://towardsdatascience.com/probability-concepts-explained-probability-distributions-

introduction-part-3-4a5db81858dc (Accessed: 12 February 2020).

Available at: What Is Annual Equivalent Rate (AER)? - Finder UK 2019.

https://www.finder.com/uk/what-is-annual-equivalent-rate-aer (Accessed: 11 February 2020).

Available at: Yahoo is now a part of Verizon Media 2020.

https://in.finance.yahoo.com/quote/SPY?p=SPY&.tsrc=fin-srch (Accessed: 11 February

2020).

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling.

Chapman and Hall/CRC.

Breinlich, H., Leromain, E., Novy, D. and Sampson, T., 2017. The consequences of the

Brexit vote for UK inflation and living standards: first evidence. CEP Technical Report.

Bretscher, L., Mueller, P., Schmid, L. and Vedolin, A., 2015. Interest rate risk and corporate

hedging.

Dhingra, S., Ottaviano, G.I., Sampson, T. and Reenen, J.V., 2016. The consequences of

Brexit for UK trade and living standards.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2019. Principles of

economics in context. Routledge.

BUSINESS AND MANAGEMENT

Reference

Adrian, T., Crump, R.K. and Vogt, E., 2019. Nonlinearity and Flight‐to‐Safety in the Risk‐

Return Trade‐Off for Stocks and Bonds. The Journal of Finance, 74(4), pp.1931-1973.

Available at: Probability concepts explained: probability distributions introduction part 2018

https://towardsdatascience.com/probability-concepts-explained-probability-distributions-

introduction-part-3-4a5db81858dc (Accessed: 12 February 2020).

Available at: What Is Annual Equivalent Rate (AER)? - Finder UK 2019.

https://www.finder.com/uk/what-is-annual-equivalent-rate-aer (Accessed: 11 February 2020).

Available at: Yahoo is now a part of Verizon Media 2020.

https://in.finance.yahoo.com/quote/SPY?p=SPY&.tsrc=fin-srch (Accessed: 11 February

2020).

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling.

Chapman and Hall/CRC.

Breinlich, H., Leromain, E., Novy, D. and Sampson, T., 2017. The consequences of the

Brexit vote for UK inflation and living standards: first evidence. CEP Technical Report.

Bretscher, L., Mueller, P., Schmid, L. and Vedolin, A., 2015. Interest rate risk and corporate

hedging.

Dhingra, S., Ottaviano, G.I., Sampson, T. and Reenen, J.V., 2016. The consequences of

Brexit for UK trade and living standards.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2019. Principles of

economics in context. Routledge.

11

BUSINESS AND MANAGEMENT

Hamilton, I., Huebner, G. and Griffiths, R., 2016. Valuing energy performance in home

purchasing: an analysis of mortgage lending for sustainable buildings. Procedia

Engineering, 145, pp.319-326.

Handel, B., Hendel, I. and Whinston, M.D., 2015. Equilibria in health exchanges: Adverse

selection versus reclassification risk. Econometrica, 83(4), pp.1261-1313.

Hiran, S., 2016. Financial Performance Analysis of Indian Companies Belongs to

Automobile Industry with Special Reference to Liquidity & Leverage. International Journal

of Multidisciplinary and Current Research, 4, pp.39-51.

Hunt, A. and Wheeler, B., 2017. Brexit: All you need to know about the UK leaving the

EU. BBC News, 25. Richards, C., 2017. AER.

Keown, A.J., 2019. Personal finance. Pearson.

McKenna, G., Baxter, G. and Hainey, T., 2017. E-portfolios and personal development: a

higher educational perspective. Journal of Applied Research in Higher Education.

Walke, A.G., Fullerton Jr, T.M. and Tokle, R.J., 2018. Risk-based loan pricing consequences

for credit unions. Journal of Empirical Finance, 47, pp.105-119.

BUSINESS AND MANAGEMENT

Hamilton, I., Huebner, G. and Griffiths, R., 2016. Valuing energy performance in home

purchasing: an analysis of mortgage lending for sustainable buildings. Procedia

Engineering, 145, pp.319-326.

Handel, B., Hendel, I. and Whinston, M.D., 2015. Equilibria in health exchanges: Adverse

selection versus reclassification risk. Econometrica, 83(4), pp.1261-1313.

Hiran, S., 2016. Financial Performance Analysis of Indian Companies Belongs to

Automobile Industry with Special Reference to Liquidity & Leverage. International Journal

of Multidisciplinary and Current Research, 4, pp.39-51.

Hunt, A. and Wheeler, B., 2017. Brexit: All you need to know about the UK leaving the

EU. BBC News, 25. Richards, C., 2017. AER.

Keown, A.J., 2019. Personal finance. Pearson.

McKenna, G., Baxter, G. and Hainey, T., 2017. E-portfolios and personal development: a

higher educational perspective. Journal of Applied Research in Higher Education.

Walke, A.G., Fullerton Jr, T.M. and Tokle, R.J., 2018. Risk-based loan pricing consequences

for credit unions. Journal of Empirical Finance, 47, pp.105-119.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.