Financial Management Report: DMGT Risk and RN Financing Analysis

VerifiedAdded on 2021/10/14

|17

|4039

|38

Report

AI Summary

This report provides a detailed analysis of financial management, focusing on two key areas: risk assessment at DMGT and financing options for RN Plc. The first part of the report examines DMGT's classification of risks, distinguishing between strategic and operational risks. It identifies increasing risk factors like portfolio management, economic uncertainty, talent risk, and information security breaches, providing in-depth descriptions and mitigation plans for each. The second part delves into RN Plc's financial situation, analyzing its term to exhaustion under normal and stressed conditions and exploring various financing arrangements. It discusses equity and debt financing options available during the construction and operation phases of a shopping center, including equity capital, mortgage loans, lines of credit, and potential government support, offering insights into their advantages and disadvantages. The report provides a comprehensive overview of financial management principles and practical applications in real-world scenarios.

TAM 01: Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question-1 (a)

DMGT classifies the risks into two major categories such as strategic risk and operational

risk. The strategic risk implies that risk which emanate from the business strategy formulated by

the management of the company. The management is involved in formulating strategies for day

to day operations as well as for long term plans and objectives (Aven, 2016). There is the risk

that management may formulate a strategy which might not work out for the company’s well

being. Thus, the risk of failure of the management’s strategy is called the strategic risk. The

board of directors and the CEOs are the primary driver of the strategic risk. It is perceived that

the stronger the board of directors and CEOs, the lower will be the strategic risk. The company’s

with weak management at the top are more likely to trigger the strategic risk. The top

management’s inability to formulate focused, reliable and achievable business strategies is the

main cause of high strategic risk (Aven, 2016).

On the other hand, the operational risk is associated with the implementation of the

business strategies formulated by the top management in the desired manner (Teece, Peteraf, and

Leih, 2016). Thus, the risk of the failure on the part of the middle or tactical level of

management to executive the top management’s strategy and plans is called the operational risk.

The operational risk is more likely to arise due to breakdowns and flaws in the internal

procedures and systems of the company. Thus, the companies with weak internal control

procedures, more human interventions, and lesser technology and innovation are likely to face

high operational risk (Teece, Peteraf, and Leih, 2016).

The main difference between the strategic risk and the operational risk is the association

of two risks with different types of activities within an organization. One is associated with the

2

DMGT classifies the risks into two major categories such as strategic risk and operational

risk. The strategic risk implies that risk which emanate from the business strategy formulated by

the management of the company. The management is involved in formulating strategies for day

to day operations as well as for long term plans and objectives (Aven, 2016). There is the risk

that management may formulate a strategy which might not work out for the company’s well

being. Thus, the risk of failure of the management’s strategy is called the strategic risk. The

board of directors and the CEOs are the primary driver of the strategic risk. It is perceived that

the stronger the board of directors and CEOs, the lower will be the strategic risk. The company’s

with weak management at the top are more likely to trigger the strategic risk. The top

management’s inability to formulate focused, reliable and achievable business strategies is the

main cause of high strategic risk (Aven, 2016).

On the other hand, the operational risk is associated with the implementation of the

business strategies formulated by the top management in the desired manner (Teece, Peteraf, and

Leih, 2016). Thus, the risk of the failure on the part of the middle or tactical level of

management to executive the top management’s strategy and plans is called the operational risk.

The operational risk is more likely to arise due to breakdowns and flaws in the internal

procedures and systems of the company. Thus, the companies with weak internal control

procedures, more human interventions, and lesser technology and innovation are likely to face

high operational risk (Teece, Peteraf, and Leih, 2016).

The main difference between the strategic risk and the operational risk is the association

of two risks with different types of activities within an organization. One is associated with the

2

activities of the top management and another is associated with the activities of middle or tactical

level management. It would also be said that the operational risk arises as a consequence of the

strategic level risk (Teece, Peteraf, and Leih, 2016).

Question-1 (b)

There are many risks being identified by DMGT, out of which some has increased, some

has remained stagnant, and a few have declined during the year. Among the strategic risk

category, the risk factors such as portfolio management, economical and geographical

uncertainty, and Talent shows increase in the risk during the year. Further, among the operational

risk category, one risk factor such as information security breach or cyber attack has been found

to be increasing (DMGT, 2017). Out of the above identified increasing risk factors three risk

factors have been discussed as below:

Portfolio Management risk

Risk description: The portfolio management risk implies the risk associated with the failure of

the investment and divestment strategies of management. DMGT is focused on increasing the

investment portfolio as the management considers this as the key to success for the group as a

whole. However, with the high rate of success, there is associated high level of risk as well. The

group is exposed to the risk of not achieving the desired objective by adopting changes in the

portfolio of investment. During the current year, the management of DMGT estimates the

portfolio risk as high due to increased number of transactions and reduction in Euro money

holdings (DMGT, 2017).

Mitigation plan: In order to mitigate the portfolio risk, the management of DMGT has taken

various positive steps which involve enhancing the controlling and monitoring of the investment

3

level management. It would also be said that the operational risk arises as a consequence of the

strategic level risk (Teece, Peteraf, and Leih, 2016).

Question-1 (b)

There are many risks being identified by DMGT, out of which some has increased, some

has remained stagnant, and a few have declined during the year. Among the strategic risk

category, the risk factors such as portfolio management, economical and geographical

uncertainty, and Talent shows increase in the risk during the year. Further, among the operational

risk category, one risk factor such as information security breach or cyber attack has been found

to be increasing (DMGT, 2017). Out of the above identified increasing risk factors three risk

factors have been discussed as below:

Portfolio Management risk

Risk description: The portfolio management risk implies the risk associated with the failure of

the investment and divestment strategies of management. DMGT is focused on increasing the

investment portfolio as the management considers this as the key to success for the group as a

whole. However, with the high rate of success, there is associated high level of risk as well. The

group is exposed to the risk of not achieving the desired objective by adopting changes in the

portfolio of investment. During the current year, the management of DMGT estimates the

portfolio risk as high due to increased number of transactions and reduction in Euro money

holdings (DMGT, 2017).

Mitigation plan: In order to mitigate the portfolio risk, the management of DMGT has taken

various positive steps which involve enhancing the controlling and monitoring of the investment

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and divestment transactions. The executive committee has been entrusted with the job of

evaluating the growth prospects of the individual businesses and allocating the funds according

to such evaluation. Further, the investment and divestment decisions have been subjected to

approval of the investment and finance committee. It will reduce the risk of imprudent

investment and divestment decisions. The management has mandated a rigorous due diligence

before the acquisition decision is finalized (DMGT, 2017).

Talent risk

Risk description: Talent risk is associated with the hiring and recruitment strategy of the

management. DMGT considers that attracting, retaining and developing right talent in the

company is the key to group’s success (Acharya, Pagano, and Volpin, 2016). DMGT exposes to

the risk of losing the good talent in the current year. These apprehensions of the management are

due to the reasons of reorganizational changes implemented during the current year (DMGT,

2017).

Mitigation plan: There are several steps being undertaken by DMGT for stabilizing and

controlling the risk of losing good talent. Firstly, DMGT has established a group of experts

having specialization in human resource recruitment and management. The executive

management from the top would also involve in hiring and recruitment for the leadership roles in

the group companies. The top management would focus more on retaining the key managerial

personnel in the group companies. The employee engagement initiatives have been planned by

the group so that good talent could be persuaded to stay in the company for longer run (DMGT,

2017).

Risk of information security breach or cyber attack

4

evaluating the growth prospects of the individual businesses and allocating the funds according

to such evaluation. Further, the investment and divestment decisions have been subjected to

approval of the investment and finance committee. It will reduce the risk of imprudent

investment and divestment decisions. The management has mandated a rigorous due diligence

before the acquisition decision is finalized (DMGT, 2017).

Talent risk

Risk description: Talent risk is associated with the hiring and recruitment strategy of the

management. DMGT considers that attracting, retaining and developing right talent in the

company is the key to group’s success (Acharya, Pagano, and Volpin, 2016). DMGT exposes to

the risk of losing the good talent in the current year. These apprehensions of the management are

due to the reasons of reorganizational changes implemented during the current year (DMGT,

2017).

Mitigation plan: There are several steps being undertaken by DMGT for stabilizing and

controlling the risk of losing good talent. Firstly, DMGT has established a group of experts

having specialization in human resource recruitment and management. The executive

management from the top would also involve in hiring and recruitment for the leadership roles in

the group companies. The top management would focus more on retaining the key managerial

personnel in the group companies. The employee engagement initiatives have been planned by

the group so that good talent could be persuaded to stay in the company for longer run (DMGT,

2017).

Risk of information security breach or cyber attack

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk description: The risk of information security breach or cyber attack implies the risk

emanating from the lack of stringent information security controls. The risk of information

security breach exposes the organization to the data loss, financial loss or damage to the

organizational reputation (Bromiley, McShane, Nair, and Rustambekov, 2015). Further, the risk

of information security breach could also result in group facing legal consequences. The group

may be liable to penalties and prosecutions due to cyber security breaches. DMGT has assessed

that the risk of information security breach would be high in the current year. The reason for

such apprehensions of the group is the increase in the inherent threat to the cyber security

(DMGT, 2017).

Mitigation plan: Considering the severe consequences of the cyber security breach, the

management of the company has laid out plan to implement stringent controls. For this purpose,

a committee to be called information security steering committee would be established under the

leadership of the CEO. The committee will review the information security controls and suggest

the improvement areas. Further, the review of information security controls has been brought

under the scope of internal audit. The group has also taken cyber insurance plan to transfer the

risk of information security breaches (DMGT, 2017).

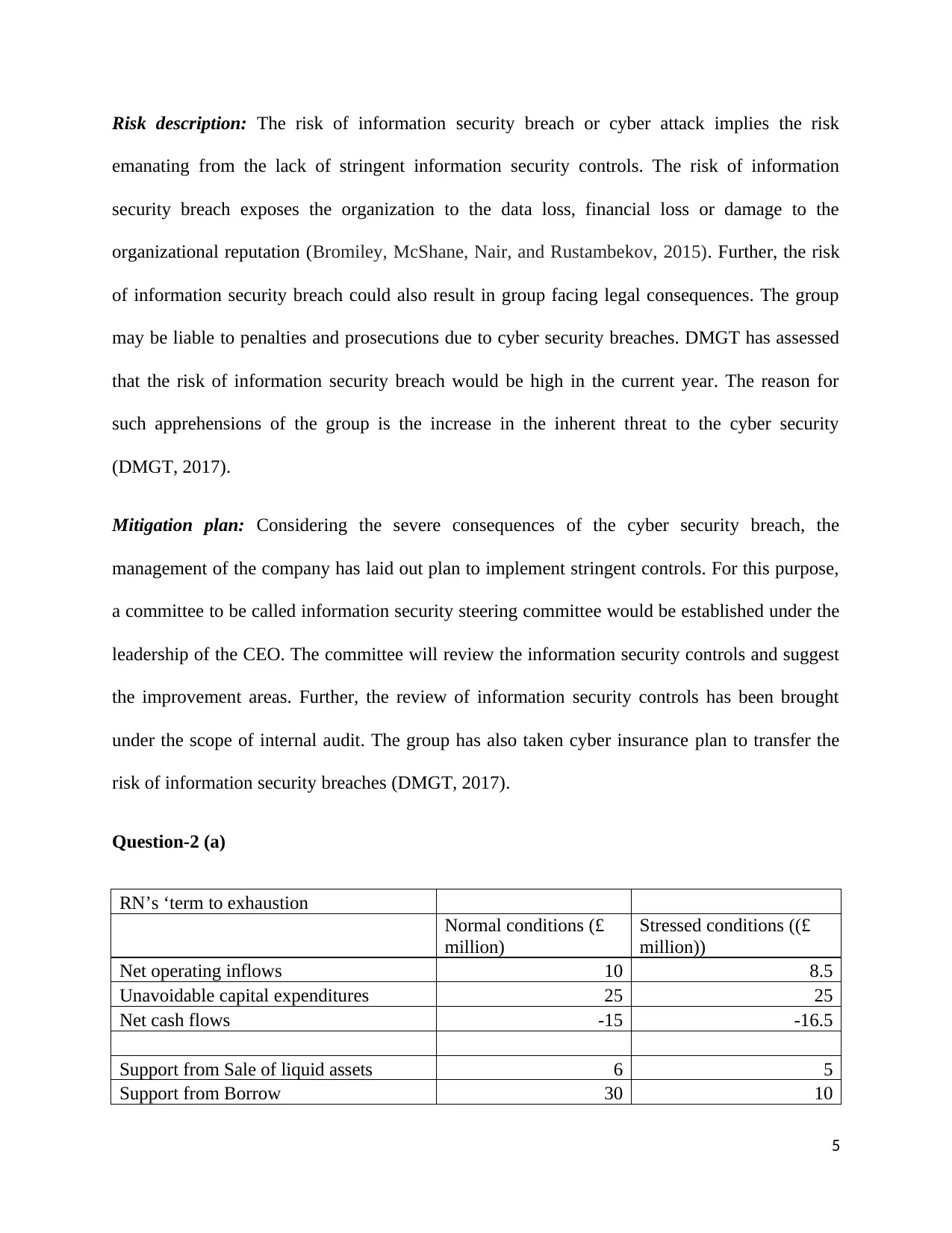

Question-2 (a)

RN’s ‘term to exhaustion

Normal conditions (£

million)

Stressed conditions ((£

million))

Net operating inflows 10 8.5

Unavoidable capital expenditures 25 25

Net cash flows -15 -16.5

Support from Sale of liquid assets 6 5

Support from Borrow 30 10

5

emanating from the lack of stringent information security controls. The risk of information

security breach exposes the organization to the data loss, financial loss or damage to the

organizational reputation (Bromiley, McShane, Nair, and Rustambekov, 2015). Further, the risk

of information security breach could also result in group facing legal consequences. The group

may be liable to penalties and prosecutions due to cyber security breaches. DMGT has assessed

that the risk of information security breach would be high in the current year. The reason for

such apprehensions of the group is the increase in the inherent threat to the cyber security

(DMGT, 2017).

Mitigation plan: Considering the severe consequences of the cyber security breach, the

management of the company has laid out plan to implement stringent controls. For this purpose,

a committee to be called information security steering committee would be established under the

leadership of the CEO. The committee will review the information security controls and suggest

the improvement areas. Further, the review of information security controls has been brought

under the scope of internal audit. The group has also taken cyber insurance plan to transfer the

risk of information security breaches (DMGT, 2017).

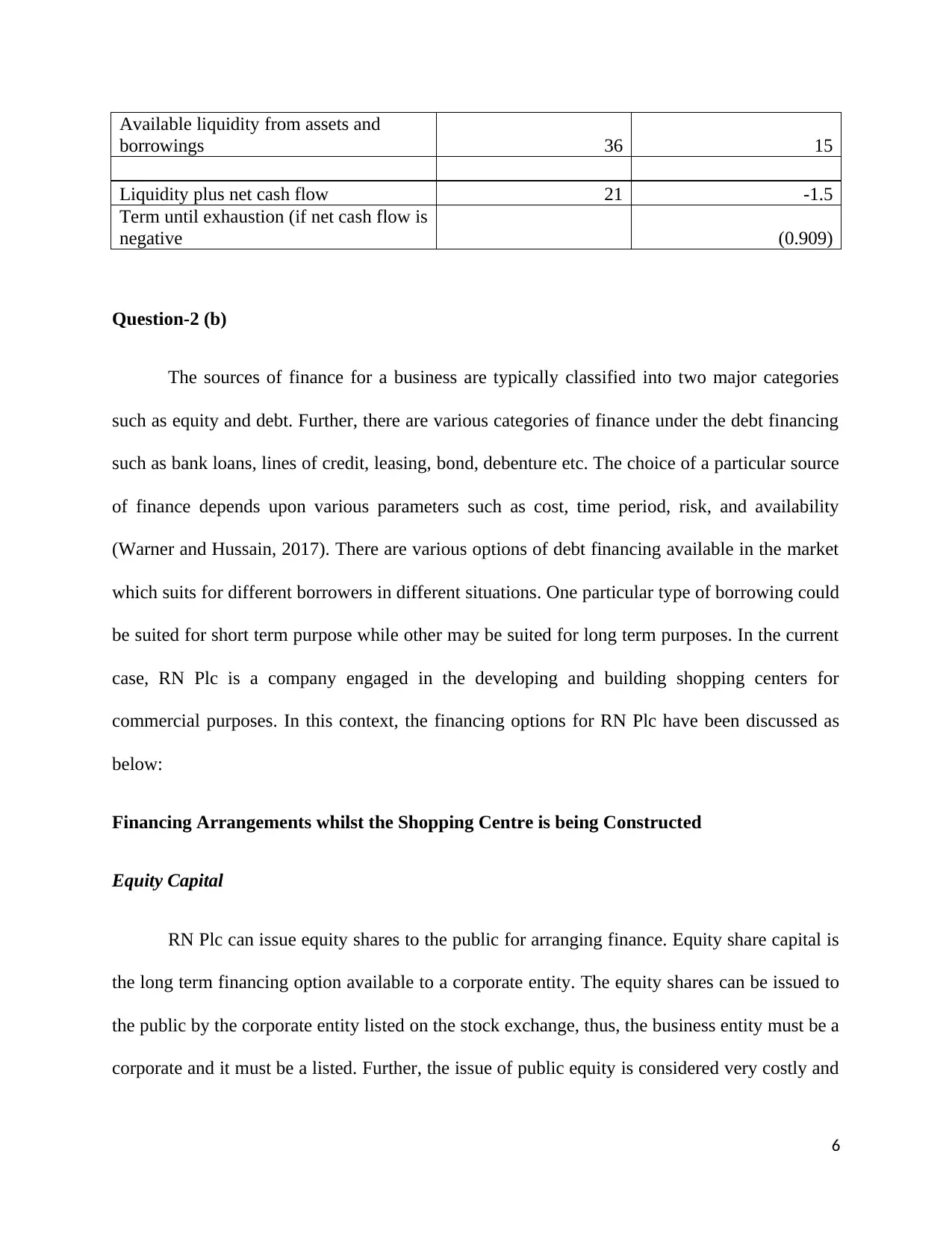

Question-2 (a)

RN’s ‘term to exhaustion

Normal conditions (£

million)

Stressed conditions ((£

million))

Net operating inflows 10 8.5

Unavoidable capital expenditures 25 25

Net cash flows -15 -16.5

Support from Sale of liquid assets 6 5

Support from Borrow 30 10

5

Available liquidity from assets and

borrowings 36 15

Liquidity plus net cash flow 21 -1.5

Term until exhaustion (if net cash flow is

negative (0.909)

Question-2 (b)

The sources of finance for a business are typically classified into two major categories

such as equity and debt. Further, there are various categories of finance under the debt financing

such as bank loans, lines of credit, leasing, bond, debenture etc. The choice of a particular source

of finance depends upon various parameters such as cost, time period, risk, and availability

(Warner and Hussain, 2017). There are various options of debt financing available in the market

which suits for different borrowers in different situations. One particular type of borrowing could

be suited for short term purpose while other may be suited for long term purposes. In the current

case, RN Plc is a company engaged in the developing and building shopping centers for

commercial purposes. In this context, the financing options for RN Plc have been discussed as

below:

Financing Arrangements whilst the Shopping Centre is being Constructed

Equity Capital

RN Plc can issue equity shares to the public for arranging finance. Equity share capital is

the long term financing option available to a corporate entity. The equity shares can be issued to

the public by the corporate entity listed on the stock exchange, thus, the business entity must be a

corporate and it must be a listed. Further, the issue of public equity is considered very costly and

6

borrowings 36 15

Liquidity plus net cash flow 21 -1.5

Term until exhaustion (if net cash flow is

negative (0.909)

Question-2 (b)

The sources of finance for a business are typically classified into two major categories

such as equity and debt. Further, there are various categories of finance under the debt financing

such as bank loans, lines of credit, leasing, bond, debenture etc. The choice of a particular source

of finance depends upon various parameters such as cost, time period, risk, and availability

(Warner and Hussain, 2017). There are various options of debt financing available in the market

which suits for different borrowers in different situations. One particular type of borrowing could

be suited for short term purpose while other may be suited for long term purposes. In the current

case, RN Plc is a company engaged in the developing and building shopping centers for

commercial purposes. In this context, the financing options for RN Plc have been discussed as

below:

Financing Arrangements whilst the Shopping Centre is being Constructed

Equity Capital

RN Plc can issue equity shares to the public for arranging finance. Equity share capital is

the long term financing option available to a corporate entity. The equity shares can be issued to

the public by the corporate entity listed on the stock exchange, thus, the business entity must be a

corporate and it must be a listed. Further, the issue of public equity is considered very costly and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time consuming (DAILY, KIEFF, and WILMARTH JR, 2014). The public issues takes time of 2

to 3 months in concluding as there is lengthy legal processes the compliance of which is

necessary. Further, various middle agents are involved in the public issues such as underwriters,

merchant brokers, and stock brokers. The commission and fees paid to the middle agents makes

the public issues costly financing arrangement option. Apart from this, the risk of dilution of the

control would also arise upon issuing equity to the public. However, there are various benefits of

issuing equity. The biggest advantage is that the company can arrange large amount of funds by

issuing equity. Further, the company’s not able to arrange debt funds due to weak market

reputation or no collateral assets being available to put as pledge against debt funding could also

take advantage of equity issues.

Further, there have been innovations in the equity financing as well. RN Plc can consider

going for venture capital or issuing equity to the Angel investors (Colombo, Cumming, and

Vismara, 2016). The venture capitalists provide finance for the projects having high growth

potential. The venture capitalists get equity shares in the company against the money lent.

However, financing though this option is little difficult to get because the venture capitalists

invest in the selected projects having high growth prospects only.

Debt Funding

RN Plc can opt for various debt funding options such as mortgage loan, line of credit,

term loan etc. Apart from this, the company can also opt for issuing bond or debentures to the

public through the stock exchange.

Mortgage loan is financed against the property. RN Plc can get the mortgage loan against

the property being constructed. The banks could finance easily upto 90% of the value of

7

to 3 months in concluding as there is lengthy legal processes the compliance of which is

necessary. Further, various middle agents are involved in the public issues such as underwriters,

merchant brokers, and stock brokers. The commission and fees paid to the middle agents makes

the public issues costly financing arrangement option. Apart from this, the risk of dilution of the

control would also arise upon issuing equity to the public. However, there are various benefits of

issuing equity. The biggest advantage is that the company can arrange large amount of funds by

issuing equity. Further, the company’s not able to arrange debt funds due to weak market

reputation or no collateral assets being available to put as pledge against debt funding could also

take advantage of equity issues.

Further, there have been innovations in the equity financing as well. RN Plc can consider

going for venture capital or issuing equity to the Angel investors (Colombo, Cumming, and

Vismara, 2016). The venture capitalists provide finance for the projects having high growth

potential. The venture capitalists get equity shares in the company against the money lent.

However, financing though this option is little difficult to get because the venture capitalists

invest in the selected projects having high growth prospects only.

Debt Funding

RN Plc can opt for various debt funding options such as mortgage loan, line of credit,

term loan etc. Apart from this, the company can also opt for issuing bond or debentures to the

public through the stock exchange.

Mortgage loan is financed against the property. RN Plc can get the mortgage loan against

the property being constructed. The banks could finance easily upto 90% of the value of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mortgage property. Further, the land and building is the permanent establishment carrying less

risk, thus, the banks and even the private lenders would be very much willing to lend funds. The

company can arrange huge amount of long term funds through mortgage loans (Rostamkalaei

and Freel, 2016). However, arranging money through mortgage loans more than the capacity to

repay gives rise to the solvency risk.

There is line of credit available to the business entities being offered by various banks

and financial institutions. The line of credit provides good source of finance for working capital

purposes. RN Plc can go for line of credit to arrange funds for short term purposes. The banks

provide line of credit against the borrower’s pledge of stocks and debtors (Rostamkalaei and

Freel, 2016). Thus, the amount of funds that could be arranged through line of credit is limited.

Further, the lending against the working capital of the business is also considered riskier from the

lenders view point. Thus, the banks normally keep big margin while lending against working

capital. The interest rates are also generally higher as compared to the term loan and mortgage

loans. Basically, the financing through line of credit also suffers from the reputation and status of

the borrower in the market. The companies having weak market reputation are less likely to get

finance through line of credit facility (Rostamkalaei and Freel, 2016).

The government of the country makes efforts towards infrastructure funding. In that case,

the government may have introduced lending to the infrastructure development companies on

special liberalized terms. Further, the government also provides grants in certain cases, thus, RN

Plc can get advantages of it. Apart from this, the term loan is also an option available to RN Plc

(Arezki, Bolton, Peters, Samama, and Stiglitz, 2016). The banks and financial institutions

provide term loan for a specified period on the specified terms and conditions. The term loan is

8

risk, thus, the banks and even the private lenders would be very much willing to lend funds. The

company can arrange huge amount of long term funds through mortgage loans (Rostamkalaei

and Freel, 2016). However, arranging money through mortgage loans more than the capacity to

repay gives rise to the solvency risk.

There is line of credit available to the business entities being offered by various banks

and financial institutions. The line of credit provides good source of finance for working capital

purposes. RN Plc can go for line of credit to arrange funds for short term purposes. The banks

provide line of credit against the borrower’s pledge of stocks and debtors (Rostamkalaei and

Freel, 2016). Thus, the amount of funds that could be arranged through line of credit is limited.

Further, the lending against the working capital of the business is also considered riskier from the

lenders view point. Thus, the banks normally keep big margin while lending against working

capital. The interest rates are also generally higher as compared to the term loan and mortgage

loans. Basically, the financing through line of credit also suffers from the reputation and status of

the borrower in the market. The companies having weak market reputation are less likely to get

finance through line of credit facility (Rostamkalaei and Freel, 2016).

The government of the country makes efforts towards infrastructure funding. In that case,

the government may have introduced lending to the infrastructure development companies on

special liberalized terms. Further, the government also provides grants in certain cases, thus, RN

Plc can get advantages of it. Apart from this, the term loan is also an option available to RN Plc

(Arezki, Bolton, Peters, Samama, and Stiglitz, 2016). The banks and financial institutions

provide term loan for a specified period on the specified terms and conditions. The term loan is

8

usually sanctioned for the purchase of fixed assets like machinery and equipments. Thus, RN Plc

can have the machinery and equipments to be used in construction financed from banks.

Financing Arrangements when Shopping Centre is rented out

When the project is complete, RN Plc could consider discharging some of its mortgage

loans and term loans. Now, since the project is complete and commercial spaces in the building

are rented out, the company would get finance from the lease rentals. The leasing agreements

would be lessees would provide finance to the company to a greater extent. Further, the company

could also get finance against its debtors through debt securitization arrangement (Markham,

Gabilondo, and Hazen, 2017). Under the debt securitization arrangement, the company can sell

its debtors to a third party for arranging funds. Apart from this, the company can also enter into

contracts for brand endorsement and advertisements with other companies. This will also help

the company to arrange finance in terms of rentals for brand endorsements.

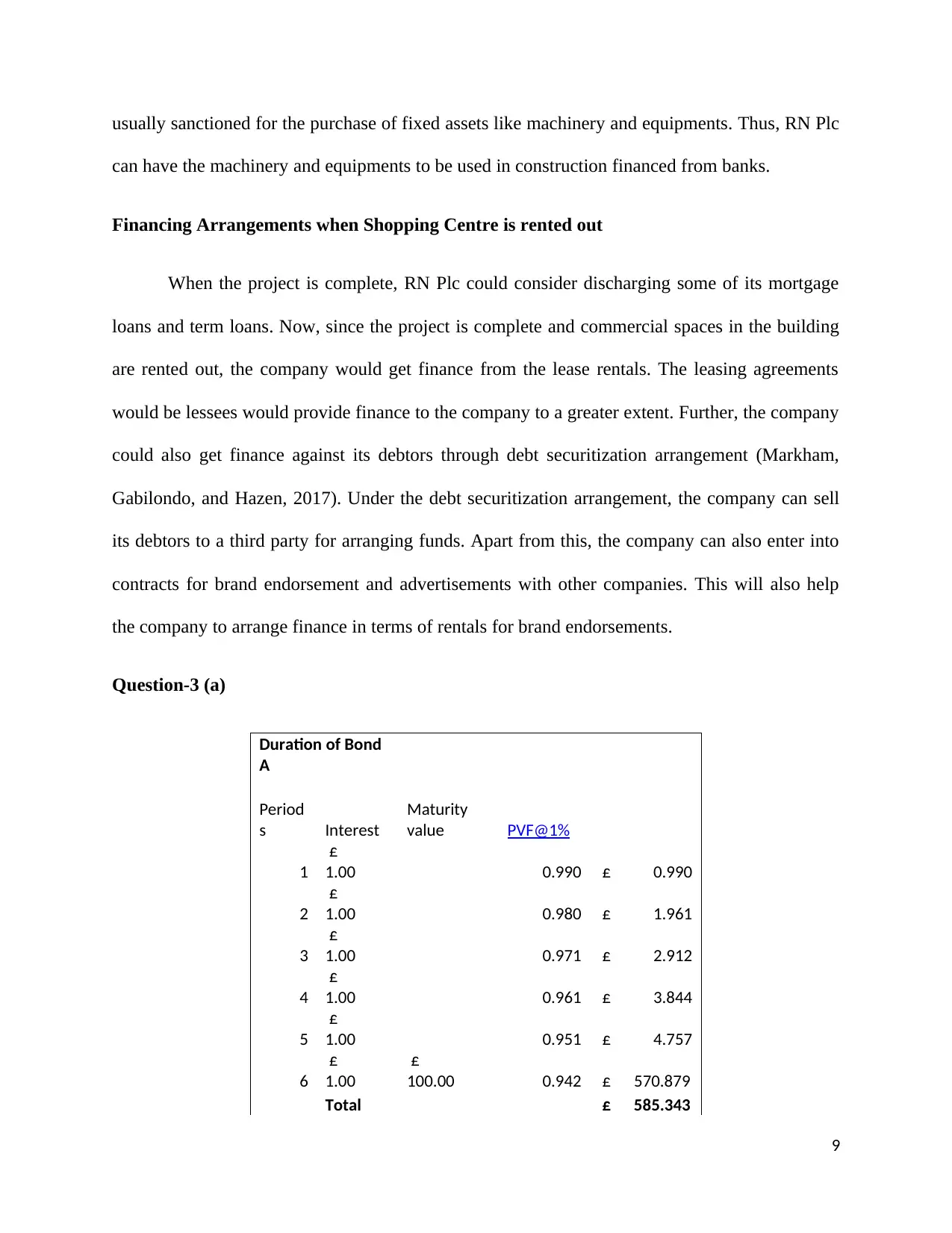

Question-3 (a)

Duration of Bond

A

Period

s Interest

Maturity

value PVF@1%

1

£

1.00 0.990 £ 0.990

2

£

1.00 0.980 £ 1.961

3

£

1.00 0.971 £ 2.912

4

£

1.00 0.961 £ 3.844

5

£

1.00 0.951 £ 4.757

6

£

1.00

£

100.00 0.942 £ 570.879

Total £ 585.343

9

can have the machinery and equipments to be used in construction financed from banks.

Financing Arrangements when Shopping Centre is rented out

When the project is complete, RN Plc could consider discharging some of its mortgage

loans and term loans. Now, since the project is complete and commercial spaces in the building

are rented out, the company would get finance from the lease rentals. The leasing agreements

would be lessees would provide finance to the company to a greater extent. Further, the company

could also get finance against its debtors through debt securitization arrangement (Markham,

Gabilondo, and Hazen, 2017). Under the debt securitization arrangement, the company can sell

its debtors to a third party for arranging funds. Apart from this, the company can also enter into

contracts for brand endorsement and advertisements with other companies. This will also help

the company to arrange finance in terms of rentals for brand endorsements.

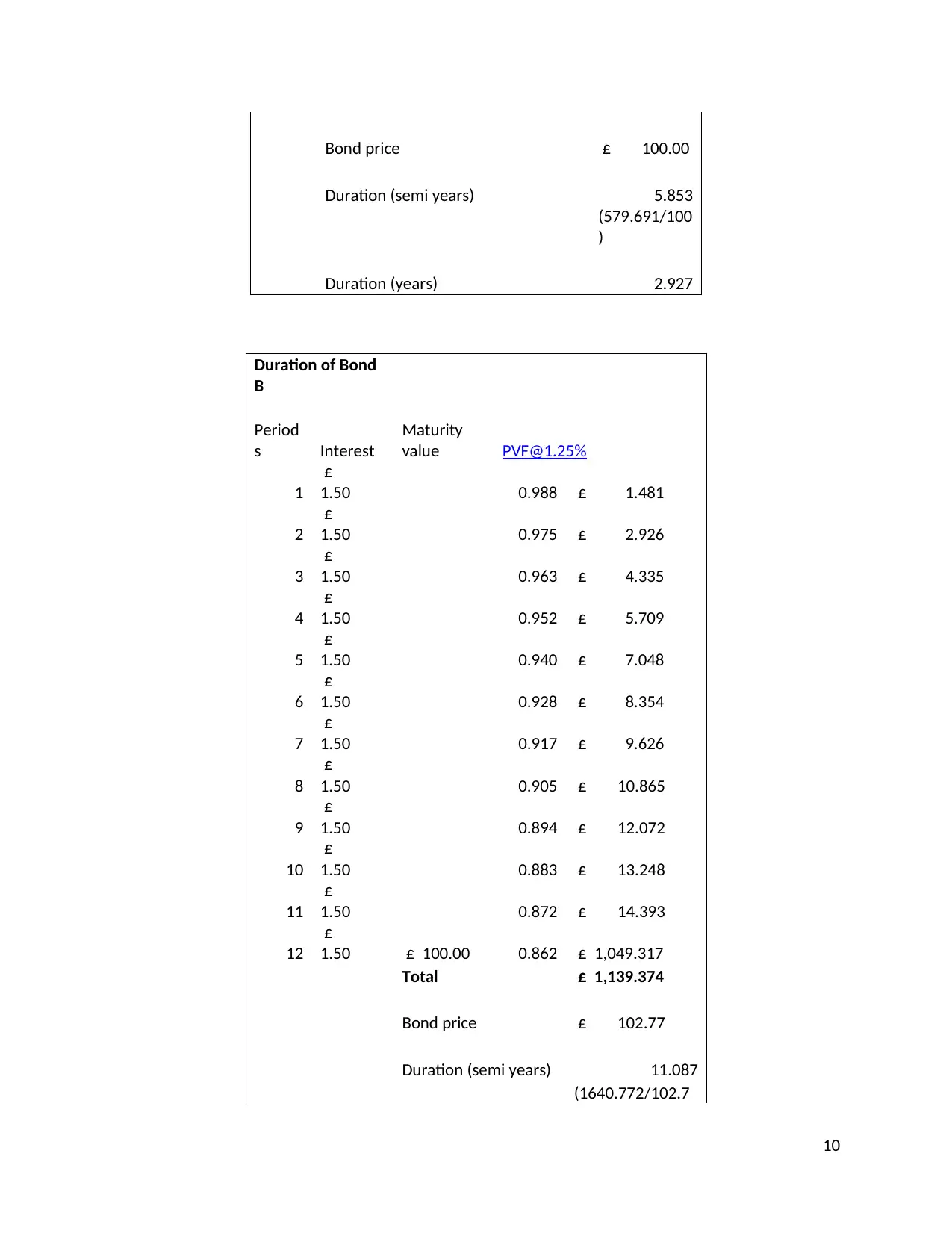

Question-3 (a)

Duration of Bond

A

Period

s Interest

Maturity

value PVF@1%

1

£

1.00 0.990 £ 0.990

2

£

1.00 0.980 £ 1.961

3

£

1.00 0.971 £ 2.912

4

£

1.00 0.961 £ 3.844

5

£

1.00 0.951 £ 4.757

6

£

1.00

£

100.00 0.942 £ 570.879

Total £ 585.343

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bond price £ 100.00

Duration (semi years) 5.853

(579.691/100

)

Duration (years) 2.927

Duration of Bond

B

Period

s Interest

Maturity

value PVF@1.25%

1

£

1.50 0.988 £ 1.481

2

£

1.50 0.975 £ 2.926

3

£

1.50 0.963 £ 4.335

4

£

1.50 0.952 £ 5.709

5

£

1.50 0.940 £ 7.048

6

£

1.50 0.928 £ 8.354

7

£

1.50 0.917 £ 9.626

8

£

1.50 0.905 £ 10.865

9

£

1.50 0.894 £ 12.072

10

£

1.50 0.883 £ 13.248

11

£

1.50 0.872 £ 14.393

12

£

1.50 £ 100.00 0.862 £ 1,049.317

Total £ 1,139.374

Bond price £ 102.77

Duration (semi years) 11.087

(1640.772/102.7

10

Duration (semi years) 5.853

(579.691/100

)

Duration (years) 2.927

Duration of Bond

B

Period

s Interest

Maturity

value PVF@1.25%

1

£

1.50 0.988 £ 1.481

2

£

1.50 0.975 £ 2.926

3

£

1.50 0.963 £ 4.335

4

£

1.50 0.952 £ 5.709

5

£

1.50 0.940 £ 7.048

6

£

1.50 0.928 £ 8.354

7

£

1.50 0.917 £ 9.626

8

£

1.50 0.905 £ 10.865

9

£

1.50 0.894 £ 12.072

10

£

1.50 0.883 £ 13.248

11

£

1.50 0.872 £ 14.393

12

£

1.50 £ 100.00 0.862 £ 1,049.317

Total £ 1,139.374

Bond price £ 102.77

Duration (semi years) 11.087

(1640.772/102.7

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7)

Duration (years) 5.543

The duration of bond A is 2.927 years and that of bond B it is 5.543 years. The duration

of bond is linked to the volatility of the bond. This implies that higher the bond duration higher

will be the volatility. Thus, bond B has higher interest rate risk (volatility) as compared to bond

A.

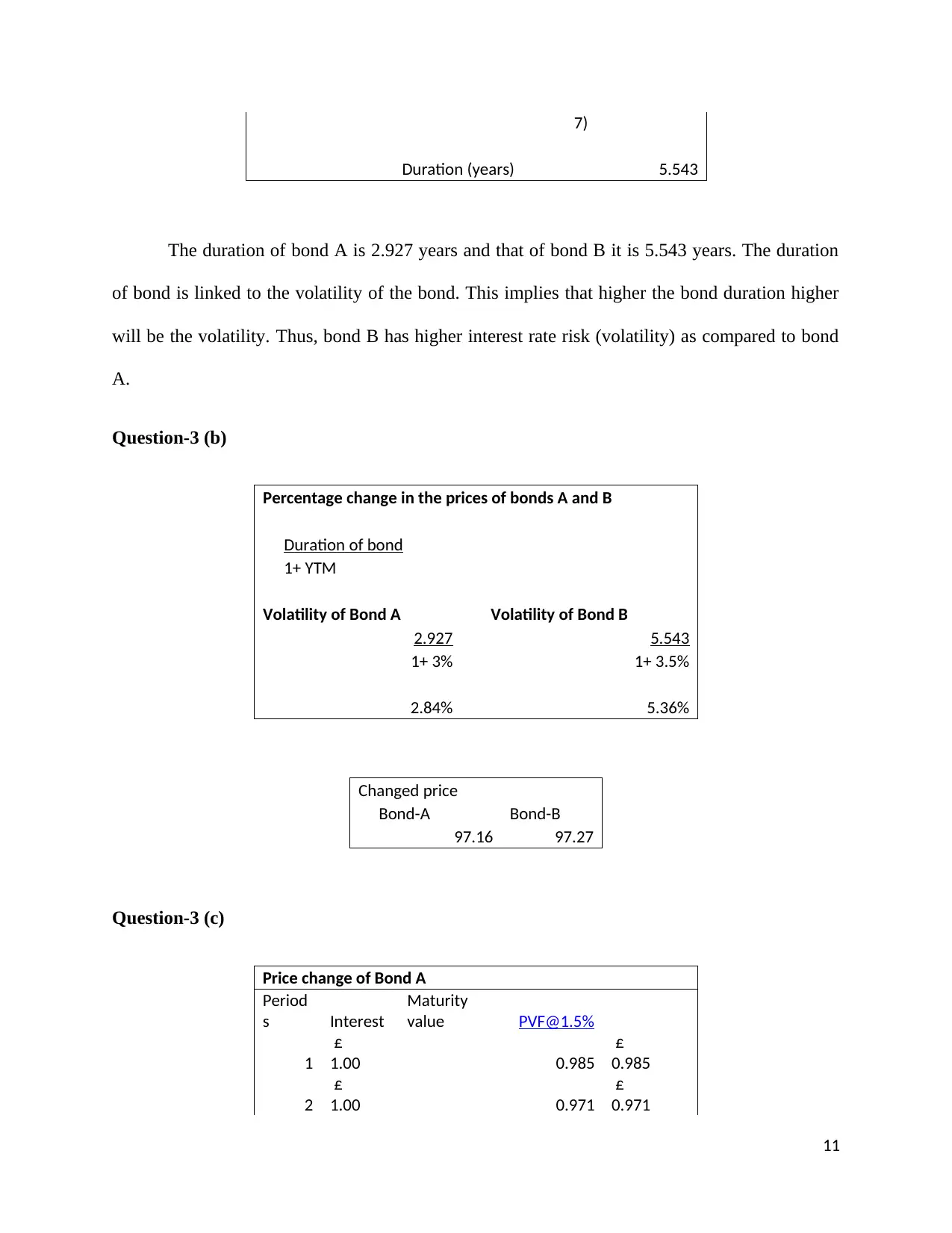

Question-3 (b)

Percentage change in the prices of bonds A and B

Duration of bond

1+ YTM

Volatility of Bond A Volatility of Bond B

2.927 5.543

1+ 3% 1+ 3.5%

2.84% 5.36%

Changed price

Bond-A Bond-B

97.16 97.27

Question-3 (c)

Price change of Bond A

Period

s Interest

Maturity

value PVF@1.5%

1

£

1.00 0.985

£

0.985

2

£

1.00 0.971

£

0.971

11

Duration (years) 5.543

The duration of bond A is 2.927 years and that of bond B it is 5.543 years. The duration

of bond is linked to the volatility of the bond. This implies that higher the bond duration higher

will be the volatility. Thus, bond B has higher interest rate risk (volatility) as compared to bond

A.

Question-3 (b)

Percentage change in the prices of bonds A and B

Duration of bond

1+ YTM

Volatility of Bond A Volatility of Bond B

2.927 5.543

1+ 3% 1+ 3.5%

2.84% 5.36%

Changed price

Bond-A Bond-B

97.16 97.27

Question-3 (c)

Price change of Bond A

Period

s Interest

Maturity

value PVF@1.5%

1

£

1.00 0.985

£

0.985

2

£

1.00 0.971

£

0.971

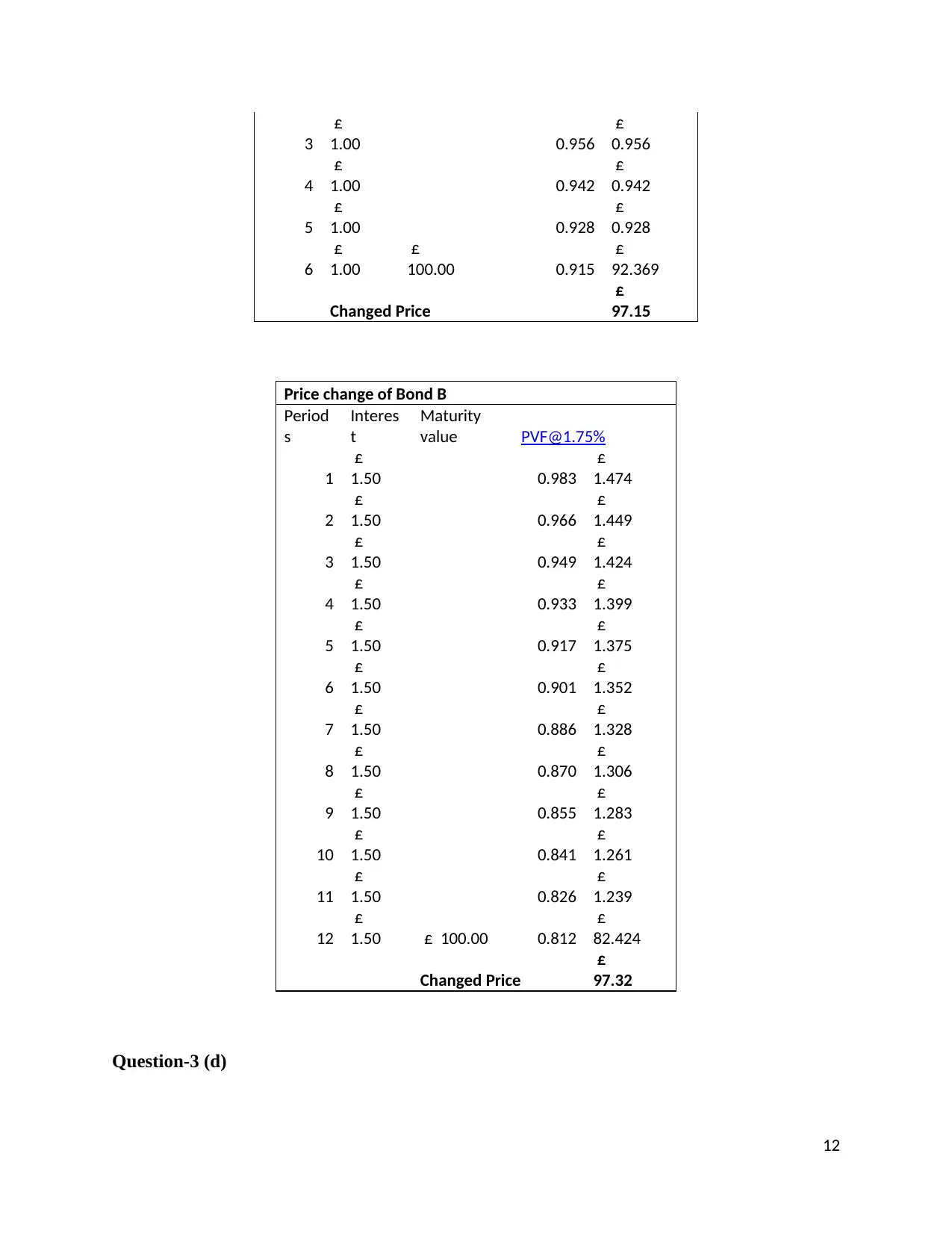

11

3

£

1.00 0.956

£

0.956

4

£

1.00 0.942

£

0.942

5

£

1.00 0.928

£

0.928

6

£

1.00

£

100.00 0.915

£

92.369

Changed Price

£

97.15

Price change of Bond B

Period

s

Interes

t

Maturity

value PVF@1.75%

1

£

1.50 0.983

£

1.474

2

£

1.50 0.966

£

1.449

3

£

1.50 0.949

£

1.424

4

£

1.50 0.933

£

1.399

5

£

1.50 0.917

£

1.375

6

£

1.50 0.901

£

1.352

7

£

1.50 0.886

£

1.328

8

£

1.50 0.870

£

1.306

9

£

1.50 0.855

£

1.283

10

£

1.50 0.841

£

1.261

11

£

1.50 0.826

£

1.239

12

£

1.50 £ 100.00 0.812

£

82.424

Changed Price

£

97.32

Question-3 (d)

12

£

1.00 0.956

£

0.956

4

£

1.00 0.942

£

0.942

5

£

1.00 0.928

£

0.928

6

£

1.00

£

100.00 0.915

£

92.369

Changed Price

£

97.15

Price change of Bond B

Period

s

Interes

t

Maturity

value PVF@1.75%

1

£

1.50 0.983

£

1.474

2

£

1.50 0.966

£

1.449

3

£

1.50 0.949

£

1.424

4

£

1.50 0.933

£

1.399

5

£

1.50 0.917

£

1.375

6

£

1.50 0.901

£

1.352

7

£

1.50 0.886

£

1.328

8

£

1.50 0.870

£

1.306

9

£

1.50 0.855

£

1.283

10

£

1.50 0.841

£

1.261

11

£

1.50 0.826

£

1.239

12

£

1.50 £ 100.00 0.812

£

82.424

Changed Price

£

97.32

Question-3 (d)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.