Wilmar International: Financial Risk Exposure and Hedging Strategies

VerifiedAdded on 2022/03/03

|28

|4590

|27

Report

AI Summary

This report provides an overview of the financial risks faced by Wilmar International Limited, a leading agribusiness company. It identifies key risks including equity price risk (S&P 500, FTSE 100), exchange rate risk (USD, Euro, AUD), and interest rate risk (variable rate loans, commercial papers, and bank accepted bills). The report recommends hedging strategies, including partial hedging of equity risks, full hedging of commercial papers for interest rate and currency risks, and the use of derivative instruments like futures and options contracts offered by CME Group to minimize potential losses. Option combination strategies, such as bear put spreads and long straddles, are also proposed to hedge against specific risks, like those associated with Sterling Equities. The report concludes with detailed analyses and recommendations to mitigate financial vulnerabilities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report is served to display an overview of the exposure of financial risks faced by Wilmar

International Limited. Appropriate hedging strategies are then proposed to suit the company.

There will be three sections of the report. In the first section, identified financial risks will be

explained in detail, which are interest rate risks, equity risks, and also foreign exchange risks.

Next, the recommendations suggested for Wilmar are to hedge partially on equity risks, hedging

fully on the commercial papers for interest rate risks and currency risks, but not hedging on BAB

and variable rate loans.

In the second section, Wilmar is recommended to utilize the derivative instruments provided by

CME Group such as futures contracts to hedge equity and interest rate risks, while options

contract is used to hedge the exchange rate risks. By utilizing the hedge, Wilmar can reduce the

potential losses to a minimum level. Besides, an analysis table is provided to indicate how the

company hedges against the risk faced for hedging fully on the commercial papers.

In the last section, option combination strategies provided are recommended to Wilmar. Wilmar

is suggested to hedge against the risk of Sterling Equities of £700 million with the bear put

spread strategy and also the long straddle strategy.

2

The report is served to display an overview of the exposure of financial risks faced by Wilmar

International Limited. Appropriate hedging strategies are then proposed to suit the company.

There will be three sections of the report. In the first section, identified financial risks will be

explained in detail, which are interest rate risks, equity risks, and also foreign exchange risks.

Next, the recommendations suggested for Wilmar are to hedge partially on equity risks, hedging

fully on the commercial papers for interest rate risks and currency risks, but not hedging on BAB

and variable rate loans.

In the second section, Wilmar is recommended to utilize the derivative instruments provided by

CME Group such as futures contracts to hedge equity and interest rate risks, while options

contract is used to hedge the exchange rate risks. By utilizing the hedge, Wilmar can reduce the

potential losses to a minimum level. Besides, an analysis table is provided to indicate how the

company hedges against the risk faced for hedging fully on the commercial papers.

In the last section, option combination strategies provided are recommended to Wilmar. Wilmar

is suggested to hedge against the risk of Sterling Equities of £700 million with the bear put

spread strategy and also the long straddle strategy.

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Wilmar International Limited, one of the largest leading agribusiness companies in Asia. The

company is founded and headquartered in Singapore. This study will be focusing on the exposed

financial risks in the operation of the business cultivating palm oil across Asia and Africa. This

report aims to identify all potentially relevant financial risks and suggest appropriate hedging

techniques to the company to minimize the chances of making potential losses. Future contracts,

forward contracts, or option contracts will be used as the derivative instruments for the hedging

techniques. The data used for the derivative instruments like futures prices and option prices are

retrieved from the website of CME Group and Barchart.com to ensure the reliability and

accuracy of the report.

4

Wilmar International Limited, one of the largest leading agribusiness companies in Asia. The

company is founded and headquartered in Singapore. This study will be focusing on the exposed

financial risks in the operation of the business cultivating palm oil across Asia and Africa. This

report aims to identify all potentially relevant financial risks and suggest appropriate hedging

techniques to the company to minimize the chances of making potential losses. Future contracts,

forward contracts, or option contracts will be used as the derivative instruments for the hedging

techniques. The data used for the derivative instruments like futures prices and option prices are

retrieved from the website of CME Group and Barchart.com to ensure the reliability and

accuracy of the report.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section I

(A) Financial Risk Exposures

Equity Price Risk

Wilmar is exposed to equity price risks as the investment portfolio displayed a significant

amount invested in the S&P 500 and FTSE 100. The portfolio beta of a particular stock shows

the comparison between the volatility of the stock and the volatility of the market (Lemke 2020).

Hence, a stock is said to have higher volatility than the market when the portfolio beta is greater

than 1.0. According to the investment portfolio, the S&P 500 shows a portfolio beta of 1.5, while

FTSE100 shows a portfolio beta of 1.0. It means that the stock price for the S&P 500 is 50%

more volatile than the market index. On the other hand, the stock price from FTSE100 shows the

same volatility as the market index. In this situation, the S&P 500 investment has a high price

fluctuation which incurs potential risks for Wilmar to lose money from this investment. For

FTSE100, the beta value of 1.0 suggests that the stock price activity is strongly correlated to the

market. Hence, there are only systematic risks for the stock. Investing in a stock with a portfolio

beta of 1.0 will not bring risks to the investment portfolio. However, the likelihood of the stock

providing an excess return is also minimum. Onali (2020) claims that the constantly increasing

cases of the COVID-19 pandemic had triggered the high volatility in stock prices, which triggers

the possibility of stock prices falling in the future. The uncertainties arising from the pandemic

recently may affect the stock market further, causing a constant falling of prices (Dillon 2020).

The stock price of the S&P 500 and FTSE100 is expected to fall soon, which means that the

value in the future will be lesser. Even though the risks for FTSE100 are comparatively lower,

the stock price still follows the market trend of falling. Hence, potential losses are expected for

both equity investments.

Exchange Rate Risks

The risks caused by the exchange rate fluctuations will directly affect the profit and loss of

overseas trade and investment. Currency risks may incur losses when the movement of the

exchange rate is adverse (Chen 2020). For Wilmar, investments of relatively huge amounts in

5

(A) Financial Risk Exposures

Equity Price Risk

Wilmar is exposed to equity price risks as the investment portfolio displayed a significant

amount invested in the S&P 500 and FTSE 100. The portfolio beta of a particular stock shows

the comparison between the volatility of the stock and the volatility of the market (Lemke 2020).

Hence, a stock is said to have higher volatility than the market when the portfolio beta is greater

than 1.0. According to the investment portfolio, the S&P 500 shows a portfolio beta of 1.5, while

FTSE100 shows a portfolio beta of 1.0. It means that the stock price for the S&P 500 is 50%

more volatile than the market index. On the other hand, the stock price from FTSE100 shows the

same volatility as the market index. In this situation, the S&P 500 investment has a high price

fluctuation which incurs potential risks for Wilmar to lose money from this investment. For

FTSE100, the beta value of 1.0 suggests that the stock price activity is strongly correlated to the

market. Hence, there are only systematic risks for the stock. Investing in a stock with a portfolio

beta of 1.0 will not bring risks to the investment portfolio. However, the likelihood of the stock

providing an excess return is also minimum. Onali (2020) claims that the constantly increasing

cases of the COVID-19 pandemic had triggered the high volatility in stock prices, which triggers

the possibility of stock prices falling in the future. The uncertainties arising from the pandemic

recently may affect the stock market further, causing a constant falling of prices (Dillon 2020).

The stock price of the S&P 500 and FTSE100 is expected to fall soon, which means that the

value in the future will be lesser. Even though the risks for FTSE100 are comparatively lower,

the stock price still follows the market trend of falling. Hence, potential losses are expected for

both equity investments.

Exchange Rate Risks

The risks caused by the exchange rate fluctuations will directly affect the profit and loss of

overseas trade and investment. Currency risks may incur losses when the movement of the

exchange rate is adverse (Chen 2020). For Wilmar, investments of relatively huge amounts in

5

Commercial notes of US dollars and Eurodollars. If any of the currencies depreciate, there are

potential risks for exchange losses as the value Wilmar invested may turn out less in the future.

As for the Bank accepted bills, the Australian dollars can also be affected by the fluctuations in

the exchange rate of Australian dollars. The COVID-19 pandemic had created a huge impact that

the European Commission had forecasted that the public debt and deficit in the budget of the

Eurozone will be increasing exponentially and further cause economic contraction (Essex 2020).

These factors provide an insight into the potential exchange rate risks. The forecast from the

Economy Forecast Agency stated that the depreciation of the Euro against US dollars is expected

(Appendix 1). On the other hand, the exchange rate of Australian dollars against US dollars is

expected to appreciate due to the restrain of speculative activities controlled by the Reserve Bank

of Australia (Appendix 1). Hence, there are not likely exchange rate risks for the bank accepted

bills. The potential exchange risks Wilmar is exposed to is mainly the commercial notes

invested.

Interest Rate Risks

Interest Rate risks will bring potential losses to a company’s interest-bearing debt, for instance,

the loan. It is usually caused by a change in interest rate. The increase in interest rate will

contribute to the increased cost of borrowing and also increasing the return of the depositors. The

Federal Reserve will maintain the interest rate and lending rate of 3.25% for the year 2020 due to

the global economic downturn caused by the COVID-19 pandemic (Payne 2020). Wilmar having

a variable rate loan of US$10,000 million will be exposed to the interest rate risk when adverse

changes in the interest rate occur. Thus, the US economy is not likely to achieve an optimistic V-

shaped recovery due to the catastrophic effects and uncertainties given the current situation of

the pandemic. Employment situations had also contributed to the difficult recovery of the

economy causing the increased length of time needed to achieve (Winck 2020). Hence, it is safe

to assume that the interest rate for the variable rate loan will not increase in the recent future.

The Eurodollar rate referred to as London Interbank Offered Rate (LIBOR) is predicted by The

Economy Forecast Agency (2020) that it will gradually decline over the second half of 2020.

Hence, the commercial papers invested at $11,500 million are exposed to interest rate risks as the

6

potential risks for exchange losses as the value Wilmar invested may turn out less in the future.

As for the Bank accepted bills, the Australian dollars can also be affected by the fluctuations in

the exchange rate of Australian dollars. The COVID-19 pandemic had created a huge impact that

the European Commission had forecasted that the public debt and deficit in the budget of the

Eurozone will be increasing exponentially and further cause economic contraction (Essex 2020).

These factors provide an insight into the potential exchange rate risks. The forecast from the

Economy Forecast Agency stated that the depreciation of the Euro against US dollars is expected

(Appendix 1). On the other hand, the exchange rate of Australian dollars against US dollars is

expected to appreciate due to the restrain of speculative activities controlled by the Reserve Bank

of Australia (Appendix 1). Hence, there are not likely exchange rate risks for the bank accepted

bills. The potential exchange risks Wilmar is exposed to is mainly the commercial notes

invested.

Interest Rate Risks

Interest Rate risks will bring potential losses to a company’s interest-bearing debt, for instance,

the loan. It is usually caused by a change in interest rate. The increase in interest rate will

contribute to the increased cost of borrowing and also increasing the return of the depositors. The

Federal Reserve will maintain the interest rate and lending rate of 3.25% for the year 2020 due to

the global economic downturn caused by the COVID-19 pandemic (Payne 2020). Wilmar having

a variable rate loan of US$10,000 million will be exposed to the interest rate risk when adverse

changes in the interest rate occur. Thus, the US economy is not likely to achieve an optimistic V-

shaped recovery due to the catastrophic effects and uncertainties given the current situation of

the pandemic. Employment situations had also contributed to the difficult recovery of the

economy causing the increased length of time needed to achieve (Winck 2020). Hence, it is safe

to assume that the interest rate for the variable rate loan will not increase in the recent future.

The Eurodollar rate referred to as London Interbank Offered Rate (LIBOR) is predicted by The

Economy Forecast Agency (2020) that it will gradually decline over the second half of 2020.

Hence, the commercial papers invested at $11,500 million are exposed to interest rate risks as the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decreased interest rate will contribute to the increase in settlement price. The interest Wilmar

earned from the commercial papers will be comparatively lesser, as the difference between the

value invested and value received by investors had decreased.

The bank accepted bills (BAB) are also exposed to the same risks as it shares the concept with

the commercial paper, but only varies on the interest rate as it follows the rate from Australia.

The RBA intends to maintain the cash rate of 0.1% for November and December and raise back

to 0.25% in 2021 and further maintain until there are high chances of inflation where the rate can

be raised and maintained within the range of 2% to 3%, and hopefully achieving the natural rate

of unemployment.

(B) Recommendations on Hedging

Equity Price Risks

As the stock market is still filled with uncertainties due to the pandemic, it is unlikely that the

stock market will be recovering in the first half of 2021 or even the end of 2020. Hence, Wilmar

is suggested to hedge 60% of the portfolio value of both the S&P500 and the FTSE100 against

the equity risk. Due to the unstoppable outbreak of the pandemic, there are no guidelines in

predicting the accurate economic recovery time. The stock prices fluctuate widely every single

day and may suddenly boost to a new level someday. It is not recommended for Wilmar to hedge

100% of the invested portfolio value by entering a futures contract, this is because if the market

is outperformed, there will be a loss out. If the stock prices increase, Wilmar will incur losses

and further trigger margin calls on losing the futures position. Therefore, partial hedging will

allow gaining in the stock market when there are favorable movements in the stock prices.

Exchange Rate Risks

Based on the forecast of currencies, the Euro and US Dollars are expected to depreciate

in the future. The fluctuation of exchange rates will incur losses to Wilmar. Hence, it is

recommended for Wilmar to hedge 100% on the commercial papers to avoid losses. However,

7

earned from the commercial papers will be comparatively lesser, as the difference between the

value invested and value received by investors had decreased.

The bank accepted bills (BAB) are also exposed to the same risks as it shares the concept with

the commercial paper, but only varies on the interest rate as it follows the rate from Australia.

The RBA intends to maintain the cash rate of 0.1% for November and December and raise back

to 0.25% in 2021 and further maintain until there are high chances of inflation where the rate can

be raised and maintained within the range of 2% to 3%, and hopefully achieving the natural rate

of unemployment.

(B) Recommendations on Hedging

Equity Price Risks

As the stock market is still filled with uncertainties due to the pandemic, it is unlikely that the

stock market will be recovering in the first half of 2021 or even the end of 2020. Hence, Wilmar

is suggested to hedge 60% of the portfolio value of both the S&P500 and the FTSE100 against

the equity risk. Due to the unstoppable outbreak of the pandemic, there are no guidelines in

predicting the accurate economic recovery time. The stock prices fluctuate widely every single

day and may suddenly boost to a new level someday. It is not recommended for Wilmar to hedge

100% of the invested portfolio value by entering a futures contract, this is because if the market

is outperformed, there will be a loss out. If the stock prices increase, Wilmar will incur losses

and further trigger margin calls on losing the futures position. Therefore, partial hedging will

allow gaining in the stock market when there are favorable movements in the stock prices.

Exchange Rate Risks

Based on the forecast of currencies, the Euro and US Dollars are expected to depreciate

in the future. The fluctuation of exchange rates will incur losses to Wilmar. Hence, it is

recommended for Wilmar to hedge 100% on the commercial papers to avoid losses. However,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the bank acceptable bills should not be hedged because Australian dollars are expected to

appreciate. Meaning the possibility of risks occurring in the bank acceptable bills is minimum.

Interest Rate Risk

According to Payne (2020), the current bank lending rate of 3.25% is at a rock-bottom

level yet it is expected to maintain for a comparatively long period. Hence, hedging is not

necessary for the variable rate loan as Wilmar is not exposed to the interest rate risks and can

benefit from the low rate for the time being. As for the commercial papers, Wilmar is

recommended to hedge completely since the LIBOR rate is very much possible to fall sharply to

a new level. On the other hand, the bank accepted bills should not be hedged as well because the

interest rate in Australia will be steadily maintained at 0.1% for November and December due to

the pandemic and prediction to rise back to 0.25% in 2021 (Appendix 2).

Section II

(C) Recommendations on Derivative Instrument

Commodity Price Risk

Wilmar is a corporation mainly engaged in the operations of the production of palm oil

throughout Asia and Africa. If crude palm oil prices collapse, Wilmar shall make less profit.

Thus, by locking up the crude palm oil at a fixed price in the future, Wilmar could enter the short

future to avoid adverse price adjustments but if crude palm oil prices rise in the future, Wilmar

will be unable to earn an additional profit, but then Wilmar will reduce the losses if prices

decrease in the future as expected. Furthermore, Wilmar can hedge commodity price risk with an

option contract since Wilmar is concerned with the decline in prices for crude palm oil, and they

may use the put option to ensure that Wilmar can continue to sell crude palm oil at its current

strike price in the future. Yet, Wilmar would be required to pay an advance premium. The date of

maturity is one of the reasons which will raise the premium rates because Wilmar will hedge the

8

appreciate. Meaning the possibility of risks occurring in the bank acceptable bills is minimum.

Interest Rate Risk

According to Payne (2020), the current bank lending rate of 3.25% is at a rock-bottom

level yet it is expected to maintain for a comparatively long period. Hence, hedging is not

necessary for the variable rate loan as Wilmar is not exposed to the interest rate risks and can

benefit from the low rate for the time being. As for the commercial papers, Wilmar is

recommended to hedge completely since the LIBOR rate is very much possible to fall sharply to

a new level. On the other hand, the bank accepted bills should not be hedged as well because the

interest rate in Australia will be steadily maintained at 0.1% for November and December due to

the pandemic and prediction to rise back to 0.25% in 2021 (Appendix 2).

Section II

(C) Recommendations on Derivative Instrument

Commodity Price Risk

Wilmar is a corporation mainly engaged in the operations of the production of palm oil

throughout Asia and Africa. If crude palm oil prices collapse, Wilmar shall make less profit.

Thus, by locking up the crude palm oil at a fixed price in the future, Wilmar could enter the short

future to avoid adverse price adjustments but if crude palm oil prices rise in the future, Wilmar

will be unable to earn an additional profit, but then Wilmar will reduce the losses if prices

decrease in the future as expected. Furthermore, Wilmar can hedge commodity price risk with an

option contract since Wilmar is concerned with the decline in prices for crude palm oil, and they

may use the put option to ensure that Wilmar can continue to sell crude palm oil at its current

strike price in the future. Yet, Wilmar would be required to pay an advance premium. The date of

maturity is one of the reasons which will raise the premium rates because Wilmar will hedge the

8

crude palm oil for the next six months and it will cost Wilmar an immense amount of premium.

Hence, Wilmar is not advised to enter into an option contract as Wilmar would have to pay a

high premium price for it.

Foreign Exchange Risk

Since Wilmar is an exporter, Wilmar has to concern itself when the home currency (SGD)

appreciates, since when exchanging the USD for the SGD, Wilmar becomes less home currency.

So, Wilmar can hedge the foreign currency risk by using a short foreign exchange forward

contract. Wilmar can be promised a fixed price of SGD by trading its USD to SGD at a specified

fixed price in the future.

Besides, the option contract also provides a feasible way for Wilmar to hedge the foreign

currency exchange rate risk. However, for the Singapore dollar, the Monetary Authority of

Singapore (MAS) runs a managed float regime which means the exchange weighted currency

can fluctuate within a policy band that is reported on the market semi-annually in its level and

direction. The band offers a tool for handling short-term currency volatility as well as stability in

exchange rate management (Monetary Authority of Singapore n.d.). Hence, it is not acceptable

for Wilmar to utilise the option to hedge the foreign exchange rate risk because Wilmar is

unlikely to recover the expenses of the premium it has paid.

Interest Rate Risk

Wilmar currently holds a Eurodollar commercial paper, an increase in the interest rate will

increase Wilmar’s interest earnings, vice versa. Therefore, by concluding a long future contract,

Wilmar is advised to hedge the interest rate risk as it is the greatest derivative option for Wilmar

because it has the right to buy a potential Eurodollar contract on the CME platform. As the

interest rate declines, Wilmar will reduce the losses that occur when the upcoming Eurodollar

contract closes at a better price in the future. Therefore, Wilmar should enter into a long futures

contract to lock in today's price at 99.775 (Appendix 3).

9

Hence, Wilmar is not advised to enter into an option contract as Wilmar would have to pay a

high premium price for it.

Foreign Exchange Risk

Since Wilmar is an exporter, Wilmar has to concern itself when the home currency (SGD)

appreciates, since when exchanging the USD for the SGD, Wilmar becomes less home currency.

So, Wilmar can hedge the foreign currency risk by using a short foreign exchange forward

contract. Wilmar can be promised a fixed price of SGD by trading its USD to SGD at a specified

fixed price in the future.

Besides, the option contract also provides a feasible way for Wilmar to hedge the foreign

currency exchange rate risk. However, for the Singapore dollar, the Monetary Authority of

Singapore (MAS) runs a managed float regime which means the exchange weighted currency

can fluctuate within a policy band that is reported on the market semi-annually in its level and

direction. The band offers a tool for handling short-term currency volatility as well as stability in

exchange rate management (Monetary Authority of Singapore n.d.). Hence, it is not acceptable

for Wilmar to utilise the option to hedge the foreign exchange rate risk because Wilmar is

unlikely to recover the expenses of the premium it has paid.

Interest Rate Risk

Wilmar currently holds a Eurodollar commercial paper, an increase in the interest rate will

increase Wilmar’s interest earnings, vice versa. Therefore, by concluding a long future contract,

Wilmar is advised to hedge the interest rate risk as it is the greatest derivative option for Wilmar

because it has the right to buy a potential Eurodollar contract on the CME platform. As the

interest rate declines, Wilmar will reduce the losses that occur when the upcoming Eurodollar

contract closes at a better price in the future. Therefore, Wilmar should enter into a long futures

contract to lock in today's price at 99.775 (Appendix 3).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stock Market Risk

Wilmar has an S&P 500 index of US Shares investment portfolio and FTSE 100 index of sterling

pound investment portfolio. So, if the equity index falls, Wilmar is earning less profit and might

lose. This is because the 1.5 and 1.0 portfolio beta imply that stock values are volatile and more

strongly compared to the share market value index. Options contracts are Wilmar's most

effective extract tool in this situation. For example, the value of a portfolio would decline by

15% if the market value index fell by 10%. It ensures that Wilmar will have limitless gains or

profits as an option holder if the option is practiced. Wilmar is thus encouraged to hedge market

risk with a long-put option contract so that Wilmar could sell the commodity portfolio with the

current strike price in the future. For instance, when the stock value falls in the future, Wilmar

shall have the right to sell the portfolio at a default strike price; while Wilmar could decide to

refrain from using the right and will have to pay the premium only if the stock price increases in

future.

10

Wilmar has an S&P 500 index of US Shares investment portfolio and FTSE 100 index of sterling

pound investment portfolio. So, if the equity index falls, Wilmar is earning less profit and might

lose. This is because the 1.5 and 1.0 portfolio beta imply that stock values are volatile and more

strongly compared to the share market value index. Options contracts are Wilmar's most

effective extract tool in this situation. For example, the value of a portfolio would decline by

15% if the market value index fell by 10%. It ensures that Wilmar will have limitless gains or

profits as an option holder if the option is practiced. Wilmar is thus encouraged to hedge market

risk with a long-put option contract so that Wilmar could sell the commodity portfolio with the

current strike price in the future. For instance, when the stock value falls in the future, Wilmar

shall have the right to sell the portfolio at a default strike price; while Wilmar could decide to

refrain from using the right and will have to pay the premium only if the stock price increases in

future.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

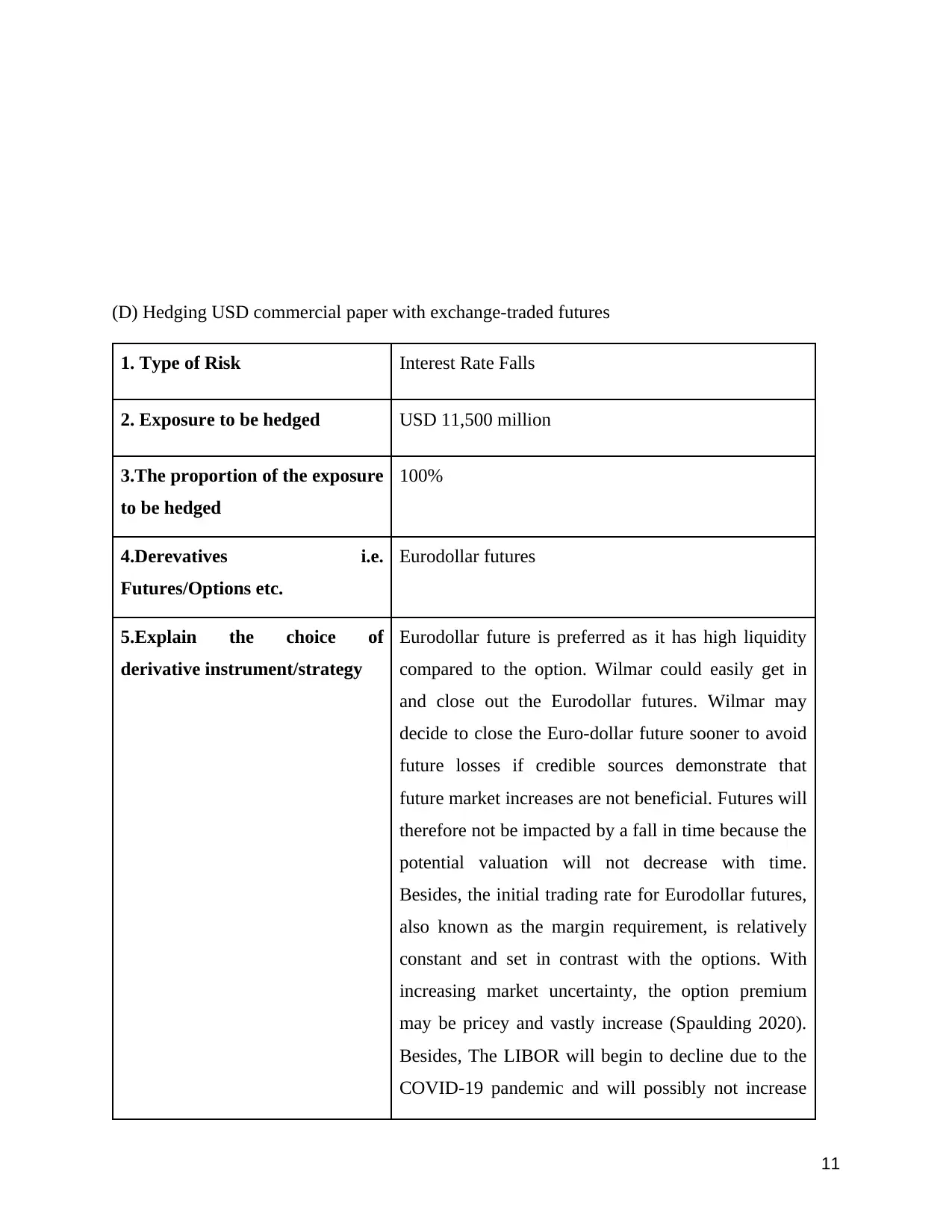

(D) Hedging USD commercial paper with exchange-traded futures

1. Type of Risk Interest Rate Falls

2. Exposure to be hedged USD 11,500 million

3.The proportion of the exposure

to be hedged

100%

4.Derevatives i.e.

Futures/Options etc.

Eurodollar futures

5.Explain the choice of

derivative instrument/strategy

Eurodollar future is preferred as it has high liquidity

compared to the option. Wilmar could easily get in

and close out the Eurodollar futures. Wilmar may

decide to close the Euro-dollar future sooner to avoid

future losses if credible sources demonstrate that

future market increases are not beneficial. Futures will

therefore not be impacted by a fall in time because the

potential valuation will not decrease with time.

Besides, the initial trading rate for Eurodollar futures,

also known as the margin requirement, is relatively

constant and set in contrast with the options. With

increasing market uncertainty, the option premium

may be pricey and vastly increase (Spaulding 2020).

Besides, The LIBOR will begin to decline due to the

COVID-19 pandemic and will possibly not increase

11

1. Type of Risk Interest Rate Falls

2. Exposure to be hedged USD 11,500 million

3.The proportion of the exposure

to be hedged

100%

4.Derevatives i.e.

Futures/Options etc.

Eurodollar futures

5.Explain the choice of

derivative instrument/strategy

Eurodollar future is preferred as it has high liquidity

compared to the option. Wilmar could easily get in

and close out the Eurodollar futures. Wilmar may

decide to close the Euro-dollar future sooner to avoid

future losses if credible sources demonstrate that

future market increases are not beneficial. Futures will

therefore not be impacted by a fall in time because the

potential valuation will not decrease with time.

Besides, the initial trading rate for Eurodollar futures,

also known as the margin requirement, is relatively

constant and set in contrast with the options. With

increasing market uncertainty, the option premium

may be pricey and vastly increase (Spaulding 2020).

Besides, The LIBOR will begin to decline due to the

COVID-19 pandemic and will possibly not increase

11

above the current LIBOR (McNamee, 2020). So,

when we're sure that interest rates will fall in the

future, futures are more suitable than options.

6.No. of Contracts (USD $11,500,000000 / USD $1,000,000) x 2 =

23,000 contracts

7.Contract Month used January 2021

8. Long/ Short/ Put/ Call Long

9. Strike Prices, Premiums/

Future Prices, etc.

99.775 (Appendix 3)

Section III

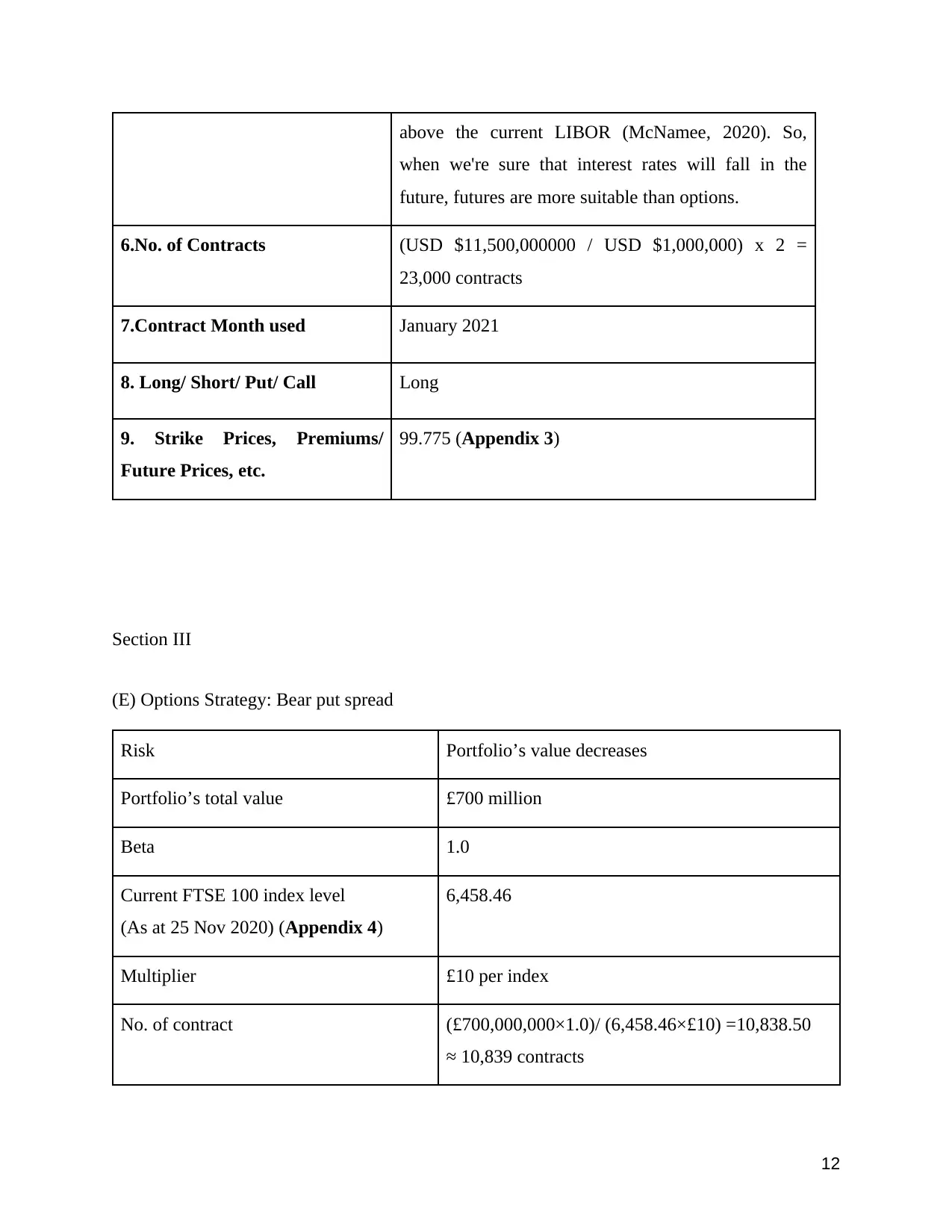

(E) Options Strategy: Bear put spread

Risk Portfolio’s value decreases

Portfolio’s total value £700 million

Beta 1.0

Current FTSE 100 index level

(As at 25 Nov 2020) (Appendix 4)

6,458.46

Multiplier £10 per index

No. of contract (£700,000,000×1.0)/ (6,458.46×£10) =10,838.50

≈ 10,839 contracts

12

when we're sure that interest rates will fall in the

future, futures are more suitable than options.

6.No. of Contracts (USD $11,500,000000 / USD $1,000,000) x 2 =

23,000 contracts

7.Contract Month used January 2021

8. Long/ Short/ Put/ Call Long

9. Strike Prices, Premiums/

Future Prices, etc.

99.775 (Appendix 3)

Section III

(E) Options Strategy: Bear put spread

Risk Portfolio’s value decreases

Portfolio’s total value £700 million

Beta 1.0

Current FTSE 100 index level

(As at 25 Nov 2020) (Appendix 4)

6,458.46

Multiplier £10 per index

No. of contract (£700,000,000×1.0)/ (6,458.46×£10) =10,838.50

≈ 10,839 contracts

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.