Financial Risk Management: Comparative Analysis of HSBC and Lloyd Bank

VerifiedAdded on 2021/12/13

|18

|3518

|26

Report

AI Summary

This report provides a comprehensive analysis of financial risk management within the banking sector, specifically focusing on HSBC and Lloyd Bank. The study employs a quantitative approach, utilizing financial data from 2011 to 2017, to assess the banks' performance through various financial ratios, including efficiency, profitability, liquidity, share performance, management capacity, and capital structure. The research methodology involves a descriptive research design and deductive approach, with data sourced from the annual reports of both companies. The analysis includes liquidity, profitability, and management capacity ratios, revealing the banks' ability to manage short-term obligations, generate returns, and utilize assets effectively. The findings highlight the relative variability in financial operations and asset utilization between the two banks, despite their overall strong performance. The report concludes by discussing the implications of these findings for effective risk management practices within the banking industry and providing insights into the financial health and stability of HSBC and Lloyd Bank.

0

Running head: BANK FINANCIAL RISK MANAGEMENT

BANK FINANCIAL RISK MANAGEMENT

Name of the Student

Name of the University

Author’s Note

Running head: BANK FINANCIAL RISK MANAGEMENT

BANK FINANCIAL RISK MANAGEMENT

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BANK FINANCIAL RISK MANAGEMENT

Abstract

The objective of the paper is to delve into the aspects of risk management through

covering the process of effective examination upon the financial performance of the considered

two banks which are HSBC bank and Lloyd bank. Quantitative analysis is being executed upon

the obtained financial data from 2011 till 2017 for the two banks and the respective results are

interpreted and compared. The involved ratios that were being undertaken for conducting the

financial ratio analysis are the efficiency ratio, profitability ratio, liquidity ratio, share

performance, management capacity and capital structure of the two banking firms. Descriptive

statistical analysis was then implemented to rank the financial performance of the firms followed

by revealing the existing banking scenario in terms of its overall stability and measure of

dispersion from the performance expected. The major finding reflected that both of the banks

performed substantially well though relative variability was been found in their financial

operation and way of asset utilization.

Keywords: HSBC, Lloyd Bank, Financial Ratios Analysis, Performance Measurement

Abstract

The objective of the paper is to delve into the aspects of risk management through

covering the process of effective examination upon the financial performance of the considered

two banks which are HSBC bank and Lloyd bank. Quantitative analysis is being executed upon

the obtained financial data from 2011 till 2017 for the two banks and the respective results are

interpreted and compared. The involved ratios that were being undertaken for conducting the

financial ratio analysis are the efficiency ratio, profitability ratio, liquidity ratio, share

performance, management capacity and capital structure of the two banking firms. Descriptive

statistical analysis was then implemented to rank the financial performance of the firms followed

by revealing the existing banking scenario in terms of its overall stability and measure of

dispersion from the performance expected. The major finding reflected that both of the banks

performed substantially well though relative variability was been found in their financial

operation and way of asset utilization.

Keywords: HSBC, Lloyd Bank, Financial Ratios Analysis, Performance Measurement

2BANK FINANCIAL RISK MANAGEMENT

Table of Contents

Abstract............................................................................................................................................1

Introduction......................................................................................................................................3

Background Information..................................................................................................................3

Research Objective..........................................................................................................................4

Research Methodology....................................................................................................................4

Literature Review............................................................................................................................4

Financial Ratio Analysis..................................................................................................................5

Liquidity Analysis......................................................................................................................6

Profitability Ratios.......................................................................................................................8

Management Capacity Ratios....................................................................................................10

Capital Structure Ratios.............................................................................................................12

Growth Ratios............................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

Table of Contents

Abstract............................................................................................................................................1

Introduction......................................................................................................................................3

Background Information..................................................................................................................3

Research Objective..........................................................................................................................4

Research Methodology....................................................................................................................4

Literature Review............................................................................................................................4

Financial Ratio Analysis..................................................................................................................5

Liquidity Analysis......................................................................................................................6

Profitability Ratios.......................................................................................................................8

Management Capacity Ratios....................................................................................................10

Capital Structure Ratios.............................................................................................................12

Growth Ratios............................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BANK FINANCIAL RISK MANAGEMENT

Introduction

It is important to understand the existing state of financial health of the banks based on

which a bank undertakes its future actions. The financial reports helps to track the financial

statements of HSBC and Lloyds bank based on which the financial standings of the firms from

2011 till 2017 is being assessed (Schürmann. 2016). The purpose of risk management in case of

these banks is to detect the core issues related to financial problems before they takes place in

order to handle the uncertainties that exists in the industry and invoke a strategic approach that

will mitigate adverse impacts yet will be able to optimize the objectives of the firms. Financial

ratios help the banks to examine the state of efficiency, liquidity as well as gaps in financial

performance of the banks and in segments where it can improve its functionality. The study

delves into these issues in case of Lloyds & HSBC bank followed by interpreting their financial

ratios and revealing about the degree of sophistication required for practicing effective risk

management in those banks.

Background Information

Being a multinational company HSBC bank is the 7th largest banking and financial

service group that was established in 1865 in British Hong Kong. After that the company

expanded its business worldwide and currently have its presence in 73 countries. With more than

6100 offices and its global headquarter in London, HSBC encompasses nearby 216000

shareholders possessing 228687 employees. The bank have a market capitalization of 182 billion

US dollars by 2017 followed by having a total number of assets of $ 2.521 trillion, total equity of

190.24 billion US dollars. The operating income of the company is close to $ 14.792 billion and

the net income is of $ 11.879 billion by 2017. HSBC is involved in retail banking, mortgage

loans, insurance, wealth management, private banking, investment as well as corporate banking

Introduction

It is important to understand the existing state of financial health of the banks based on

which a bank undertakes its future actions. The financial reports helps to track the financial

statements of HSBC and Lloyds bank based on which the financial standings of the firms from

2011 till 2017 is being assessed (Schürmann. 2016). The purpose of risk management in case of

these banks is to detect the core issues related to financial problems before they takes place in

order to handle the uncertainties that exists in the industry and invoke a strategic approach that

will mitigate adverse impacts yet will be able to optimize the objectives of the firms. Financial

ratios help the banks to examine the state of efficiency, liquidity as well as gaps in financial

performance of the banks and in segments where it can improve its functionality. The study

delves into these issues in case of Lloyds & HSBC bank followed by interpreting their financial

ratios and revealing about the degree of sophistication required for practicing effective risk

management in those banks.

Background Information

Being a multinational company HSBC bank is the 7th largest banking and financial

service group that was established in 1865 in British Hong Kong. After that the company

expanded its business worldwide and currently have its presence in 73 countries. With more than

6100 offices and its global headquarter in London, HSBC encompasses nearby 216000

shareholders possessing 228687 employees. The bank have a market capitalization of 182 billion

US dollars by 2017 followed by having a total number of assets of $ 2.521 trillion, total equity of

190.24 billion US dollars. The operating income of the company is close to $ 14.792 billion and

the net income is of $ 11.879 billion by 2017. HSBC is involved in retail banking, mortgage

loans, insurance, wealth management, private banking, investment as well as corporate banking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BANK FINANCIAL RISK MANAGEMENT

and has a customer base of 51 million worldwide. Lloyd bank on the other hand is headquartered

in London, and is among the big four clearing banks involved in retail and commercial banking.

The firm provides insurance services and by 2016 possessed an employee strength of 45856 and

Lloyd bank was having an operating income of 17.5 billion, followed by net income of 16.6

billion and average income earning banking assets of 436 billion.

Research Objective

The objective of the research encompasses the aspect of determining the financial ratios

of HSBC and Lloyd banks based on which their financial development and ability to manage

financial risks for the period 2011-2017 are examined followed by a comparison between the

two banks.

Research Methodology

The methodology of the research is done through descriptive research design and

maintaining a deductive research approach. The data of 2011-2017 are gathered from the annual

reports of the respective companies and the financial information thus obtained are further being

analyzed through quantitative measurements.

Literature Review

According to Yan et al. (2017), financial positioning is quite dependent upon the

variations that are being taking place within the ability of the banking firms to mitigate risks

associated with their business. Adaptive analysis of the pass trends of the financial ratios can

provide a predictive measures that needs to be undertaken for reducing the financial risks

involved. The paper clearly put forth that beside operational risk, reputational risk, the banks

and has a customer base of 51 million worldwide. Lloyd bank on the other hand is headquartered

in London, and is among the big four clearing banks involved in retail and commercial banking.

The firm provides insurance services and by 2016 possessed an employee strength of 45856 and

Lloyd bank was having an operating income of 17.5 billion, followed by net income of 16.6

billion and average income earning banking assets of 436 billion.

Research Objective

The objective of the research encompasses the aspect of determining the financial ratios

of HSBC and Lloyd banks based on which their financial development and ability to manage

financial risks for the period 2011-2017 are examined followed by a comparison between the

two banks.

Research Methodology

The methodology of the research is done through descriptive research design and

maintaining a deductive research approach. The data of 2011-2017 are gathered from the annual

reports of the respective companies and the financial information thus obtained are further being

analyzed through quantitative measurements.

Literature Review

According to Yan et al. (2017), financial positioning is quite dependent upon the

variations that are being taking place within the ability of the banking firms to mitigate risks

associated with their business. Adaptive analysis of the pass trends of the financial ratios can

provide a predictive measures that needs to be undertaken for reducing the financial risks

involved. The paper clearly put forth that beside operational risk, reputational risk, the banks

5BANK FINANCIAL RISK MANAGEMENT

faces liquidity risks to cover up its liabilities with its assets as well as market risks which are

nothing but systematic risks in the business.

In accordance with Black et al. (2016), it assessed the performance of banks financially

and depicted that financial ratios are effective estimators of the responsive of firms to understand

its performance overtime. Measurement of the financial health based on the profitability ratios

and efficiency ratios gave that there exist statistically significant difference between the

performance levels of the banking firms.

Curi and Murgia (2018), investigated upon the influential factors that renders impact in

the long run upon the financial health of the banking sectors. Among them the wealth

management, liquidity positions, asset quality, earning ability measurements are found to be

important parameters that determine financial health of the banks.

Adelopo (2017), examined the financial anomalies of private and public banks and how

financial ratios helps to understand them. It was been reflected in the paper that the joint ventures

made by public and private banks are capable of strongly assessing the risk mitigation ability of

the banks by measurement of financial ratios. It was also revealed by the paper that ranking the

capital adequacy, return on assets, etc. renders adequate information about the existing capital

utilization and repayment ability of the banks of their debts.

Financial Ratio Analysis

The financial ratio analysis are done in order to understand the relationship between

various factors that boosts a firs ability to manage risks as well as ensure its success based on the

measurement of its past performance from the perspective of the investor as well as the bank.

faces liquidity risks to cover up its liabilities with its assets as well as market risks which are

nothing but systematic risks in the business.

In accordance with Black et al. (2016), it assessed the performance of banks financially

and depicted that financial ratios are effective estimators of the responsive of firms to understand

its performance overtime. Measurement of the financial health based on the profitability ratios

and efficiency ratios gave that there exist statistically significant difference between the

performance levels of the banking firms.

Curi and Murgia (2018), investigated upon the influential factors that renders impact in

the long run upon the financial health of the banking sectors. Among them the wealth

management, liquidity positions, asset quality, earning ability measurements are found to be

important parameters that determine financial health of the banks.

Adelopo (2017), examined the financial anomalies of private and public banks and how

financial ratios helps to understand them. It was been reflected in the paper that the joint ventures

made by public and private banks are capable of strongly assessing the risk mitigation ability of

the banks by measurement of financial ratios. It was also revealed by the paper that ranking the

capital adequacy, return on assets, etc. renders adequate information about the existing capital

utilization and repayment ability of the banks of their debts.

Financial Ratio Analysis

The financial ratio analysis are done in order to understand the relationship between

various factors that boosts a firs ability to manage risks as well as ensure its success based on the

measurement of its past performance from the perspective of the investor as well as the bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BANK FINANCIAL RISK MANAGEMENT

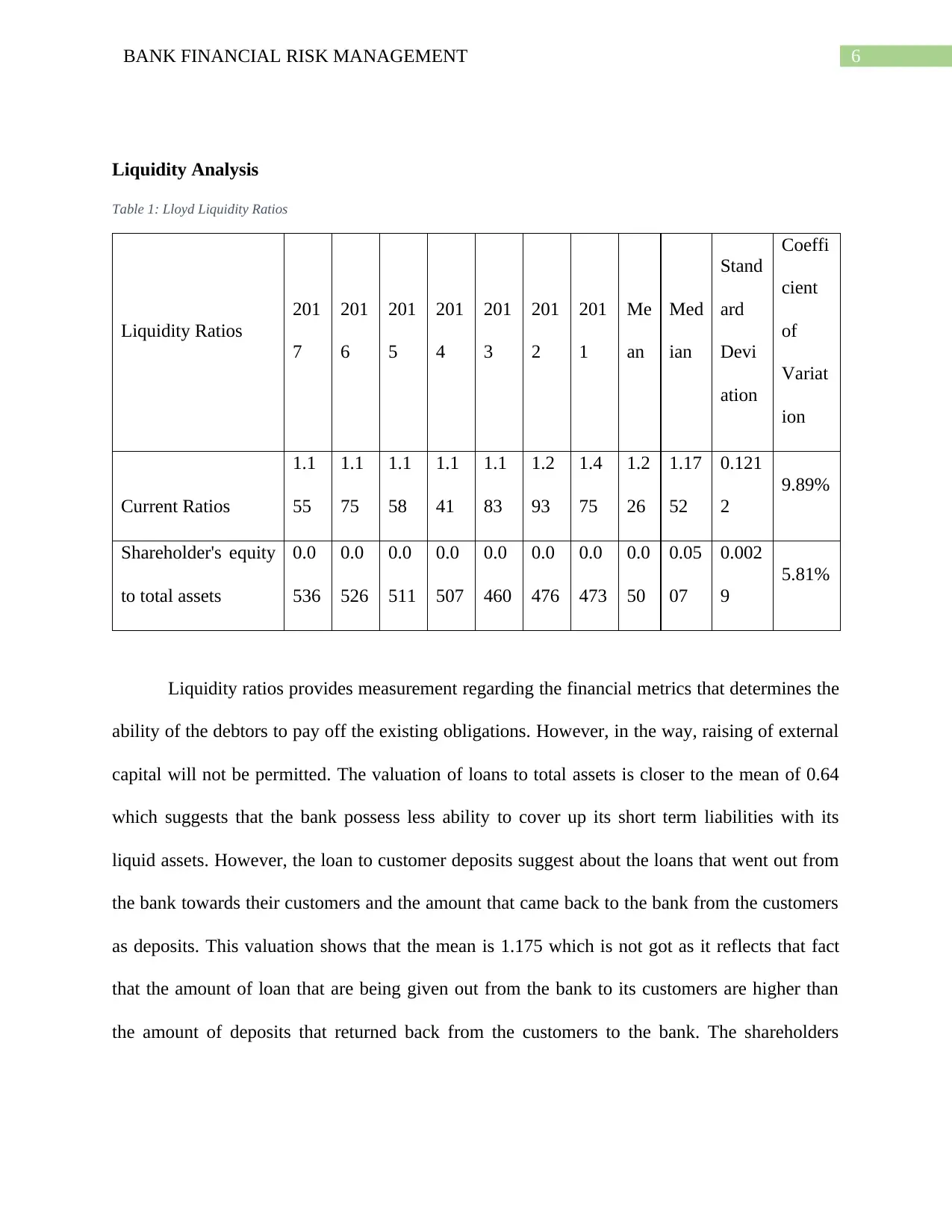

Liquidity Analysis

Table 1: Lloyd Liquidity Ratios

Liquidity Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Med

ian

Stand

ard

Devi

ation

Coeffi

cient

of

Variat

ion

Current Ratios

1.1

55

1.1

75

1.1

58

1.1

41

1.1

83

1.2

93

1.4

75

1.2

26

1.17

52

0.121

2

9.89%

Shareholder's equity

to total assets

0.0

536

0.0

526

0.0

511

0.0

507

0.0

460

0.0

476

0.0

473

0.0

50

0.05

07

0.002

9

5.81%

Liquidity ratios provides measurement regarding the financial metrics that determines the

ability of the debtors to pay off the existing obligations. However, in the way, raising of external

capital will not be permitted. The valuation of loans to total assets is closer to the mean of 0.64

which suggests that the bank possess less ability to cover up its short term liabilities with its

liquid assets. However, the loan to customer deposits suggest about the loans that went out from

the bank towards their customers and the amount that came back to the bank from the customers

as deposits. This valuation shows that the mean is 1.175 which is not got as it reflects that fact

that the amount of loan that are being given out from the bank to its customers are higher than

the amount of deposits that returned back from the customers to the bank. The shareholders

Liquidity Analysis

Table 1: Lloyd Liquidity Ratios

Liquidity Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Med

ian

Stand

ard

Devi

ation

Coeffi

cient

of

Variat

ion

Current Ratios

1.1

55

1.1

75

1.1

58

1.1

41

1.1

83

1.2

93

1.4

75

1.2

26

1.17

52

0.121

2

9.89%

Shareholder's equity

to total assets

0.0

536

0.0

526

0.0

511

0.0

507

0.0

460

0.0

476

0.0

473

0.0

50

0.05

07

0.002

9

5.81%

Liquidity ratios provides measurement regarding the financial metrics that determines the

ability of the debtors to pay off the existing obligations. However, in the way, raising of external

capital will not be permitted. The valuation of loans to total assets is closer to the mean of 0.64

which suggests that the bank possess less ability to cover up its short term liabilities with its

liquid assets. However, the loan to customer deposits suggest about the loans that went out from

the bank towards their customers and the amount that came back to the bank from the customers

as deposits. This valuation shows that the mean is 1.175 which is not got as it reflects that fact

that the amount of loan that are being given out from the bank to its customers are higher than

the amount of deposits that returned back from the customers to the bank. The shareholders

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BANK FINANCIAL RISK MANAGEMENT

equity to total assets on the other hand suggests that the mean of the residual claim that the

shareholders have upon the amount of assets is 0.0507 which not good.

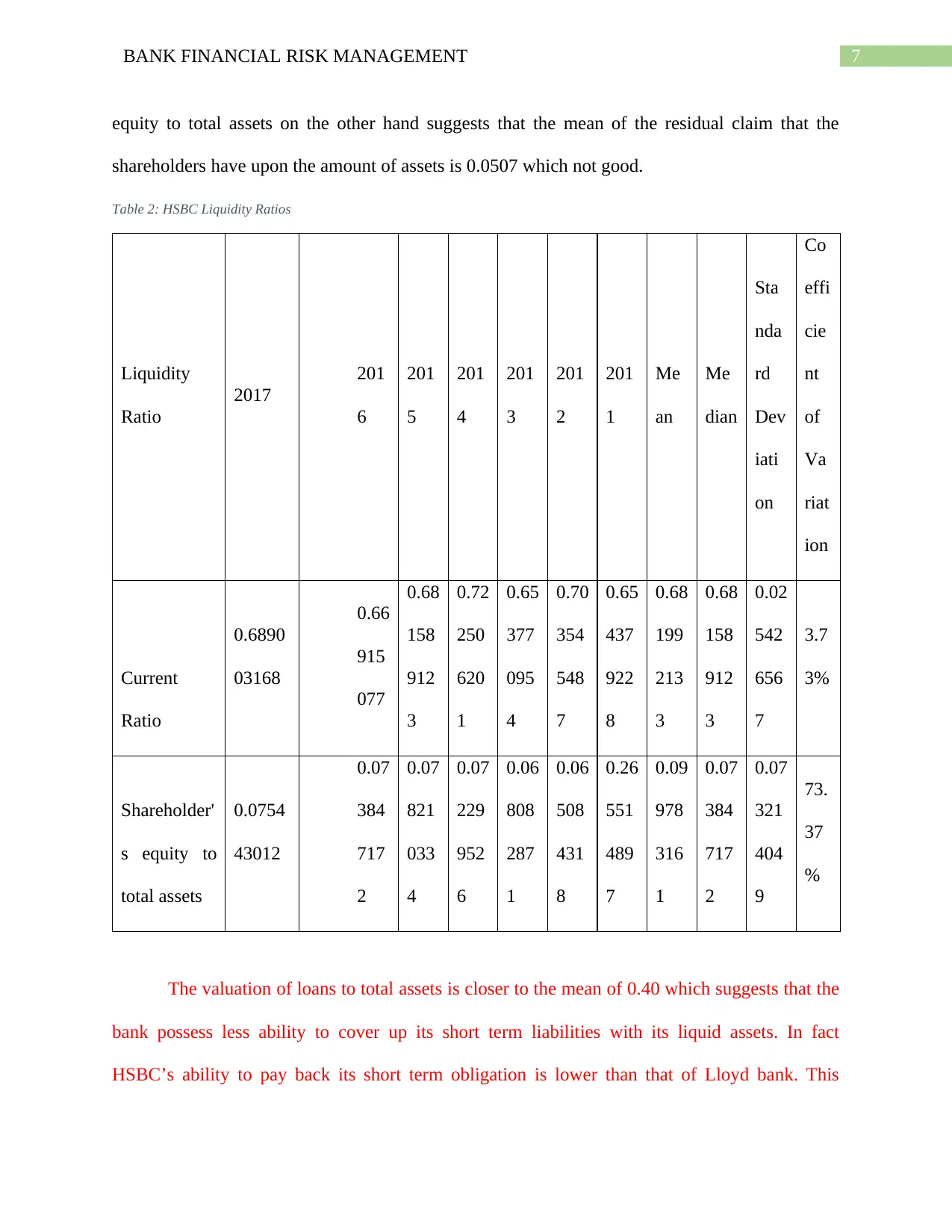

Table 2: HSBC Liquidity Ratios

Liquidity

Ratio

2017

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Me

dian

Sta

nda

rd

Dev

iati

on

Co

effi

cie

nt

of

Va

riat

ion

Current

Ratio

0.6890

03168

0.66

915

077

0.68

158

912

3

0.72

250

620

1

0.65

377

095

4

0.70

354

548

7

0.65

437

922

8

0.68

199

213

3

0.68

158

912

3

0.02

542

656

7

3.7

3%

Shareholder'

s equity to

total assets

0.0754

43012

0.07

384

717

2

0.07

821

033

4

0.07

229

952

6

0.06

808

287

1

0.06

508

431

8

0.26

551

489

7

0.09

978

316

1

0.07

384

717

2

0.07

321

404

9

73.

37

%

The valuation of loans to total assets is closer to the mean of 0.40 which suggests that the

bank possess less ability to cover up its short term liabilities with its liquid assets. In fact

HSBC’s ability to pay back its short term obligation is lower than that of Lloyd bank. This

equity to total assets on the other hand suggests that the mean of the residual claim that the

shareholders have upon the amount of assets is 0.0507 which not good.

Table 2: HSBC Liquidity Ratios

Liquidity

Ratio

2017

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Me

dian

Sta

nda

rd

Dev

iati

on

Co

effi

cie

nt

of

Va

riat

ion

Current

Ratio

0.6890

03168

0.66

915

077

0.68

158

912

3

0.72

250

620

1

0.65

377

095

4

0.70

354

548

7

0.65

437

922

8

0.68

199

213

3

0.68

158

912

3

0.02

542

656

7

3.7

3%

Shareholder'

s equity to

total assets

0.0754

43012

0.07

384

717

2

0.07

821

033

4

0.07

229

952

6

0.06

808

287

1

0.06

508

431

8

0.26

551

489

7

0.09

978

316

1

0.07

384

717

2

0.07

321

404

9

73.

37

%

The valuation of loans to total assets is closer to the mean of 0.40 which suggests that the

bank possess less ability to cover up its short term liabilities with its liquid assets. In fact

HSBC’s ability to pay back its short term obligation is lower than that of Lloyd bank. This

8BANK FINANCIAL RISK MANAGEMENT

incorporates a significant amount of risk which is necessary to be taken care of by not storing

case or non-cash assets rather by allowing for more loan opportunities for utilizing the market

value of the bank’s assets. However, the loan to customer deposits suggest about the loans that

went out from the bank towards their customers and the amount that came back to the bank from

the customers as deposits. This valuation shows that the mean is 0.68 which is well as it reflects

that fact that the amount of loan that are being given out from the bank to its customers are close

to the amount of deposits that returned back from the customers to the bank. The shareholders

equity to total assets on the other hand suggests that the mean of the residual claim that the

shareholders have upon the amount of assets is 0.0997. Notably the measure of dispersion

suggest that the variations in the HSBC bank is credible more than that of Lloyd bank.

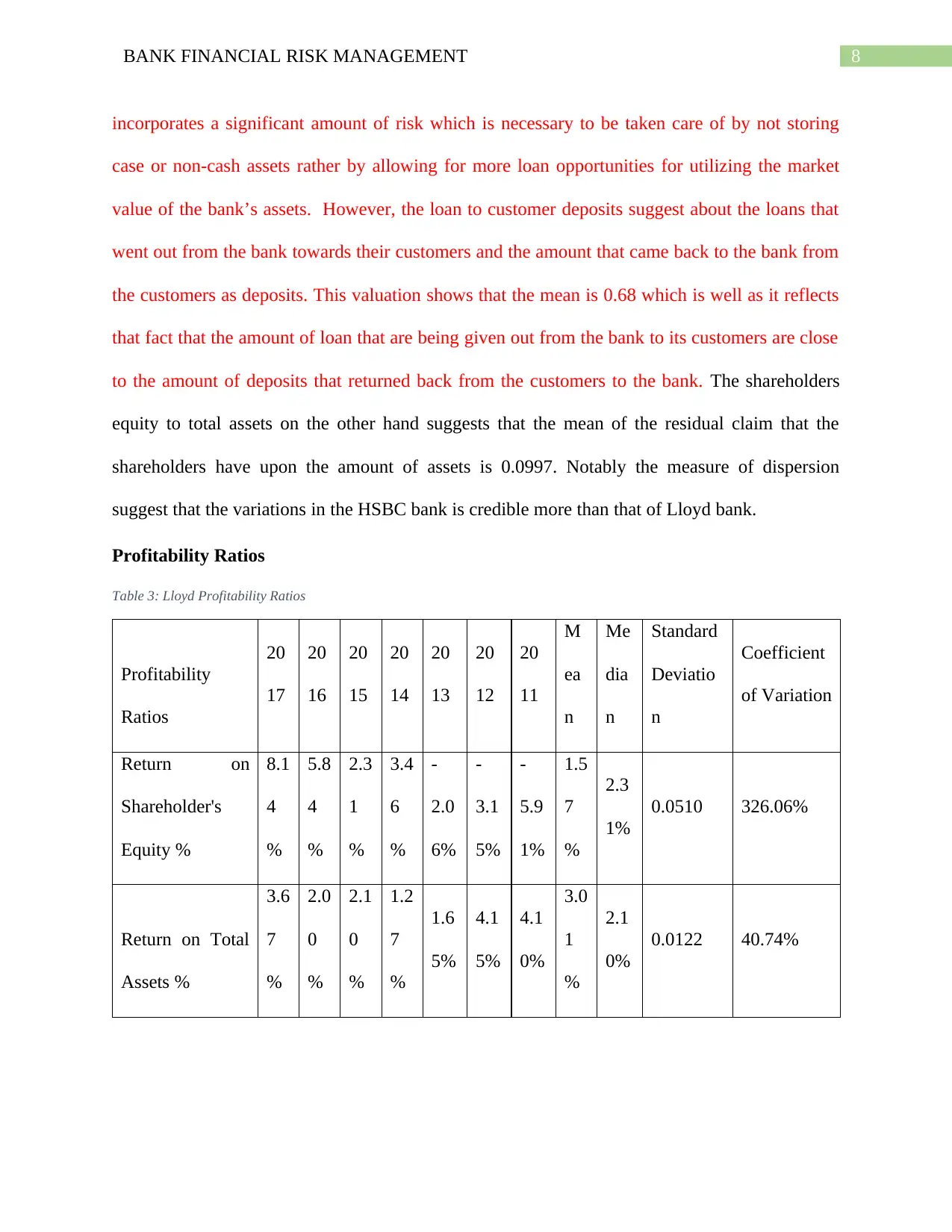

Profitability Ratios

Table 3: Lloyd Profitability Ratios

Profitability

Ratios

20

17

20

16

20

15

20

14

20

13

20

12

20

11

M

ea

n

Me

dia

n

Standard

Deviatio

n

Coefficient

of Variation

Return on

Shareholder's

Equity %

8.1

4

%

5.8

4

%

2.3

1

%

3.4

6

%

-

2.0

6%

-

3.1

5%

-

5.9

1%

1.5

7

%

2.3

1%

0.0510 326.06%

Return on Total

Assets %

3.6

7

%

2.0

0

%

2.1

0

%

1.2

7

%

1.6

5%

4.1

5%

4.1

0%

3.0

1

%

2.1

0%

0.0122 40.74%

incorporates a significant amount of risk which is necessary to be taken care of by not storing

case or non-cash assets rather by allowing for more loan opportunities for utilizing the market

value of the bank’s assets. However, the loan to customer deposits suggest about the loans that

went out from the bank towards their customers and the amount that came back to the bank from

the customers as deposits. This valuation shows that the mean is 0.68 which is well as it reflects

that fact that the amount of loan that are being given out from the bank to its customers are close

to the amount of deposits that returned back from the customers to the bank. The shareholders

equity to total assets on the other hand suggests that the mean of the residual claim that the

shareholders have upon the amount of assets is 0.0997. Notably the measure of dispersion

suggest that the variations in the HSBC bank is credible more than that of Lloyd bank.

Profitability Ratios

Table 3: Lloyd Profitability Ratios

Profitability

Ratios

20

17

20

16

20

15

20

14

20

13

20

12

20

11

M

ea

n

Me

dia

n

Standard

Deviatio

n

Coefficient

of Variation

Return on

Shareholder's

Equity %

8.1

4

%

5.8

4

%

2.3

1

%

3.4

6

%

-

2.0

6%

-

3.1

5%

-

5.9

1%

1.5

7

%

2.3

1%

0.0510 326.06%

Return on Total

Assets %

3.6

7

%

2.0

0

%

2.1

0

%

1.2

7

%

1.6

5%

4.1

5%

4.1

0%

3.0

1

%

2.1

0%

0.0122 40.74%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BANK FINANCIAL RISK MANAGEMENT

The profitability analysis suggests that in case of Lloyd bank the return that are being

obtained based on the investments that are being made by the shareholders of the firm was

negative from 2011 till the end of 2013. However the company have recovered from that poor

financial health and from 2014 till 2017 the return that the shareholders of the bank have

obtained has monotonically increased. After 2015 though it faced a slight downfall yet it

recovered effectively in 2016 ensuring a return on shareholder’s equity of 5.84 which is almost 2

and half times as compared to previous its year’s financial performance. Apart from that, the

return on total asset has a mean of 3.01 %.

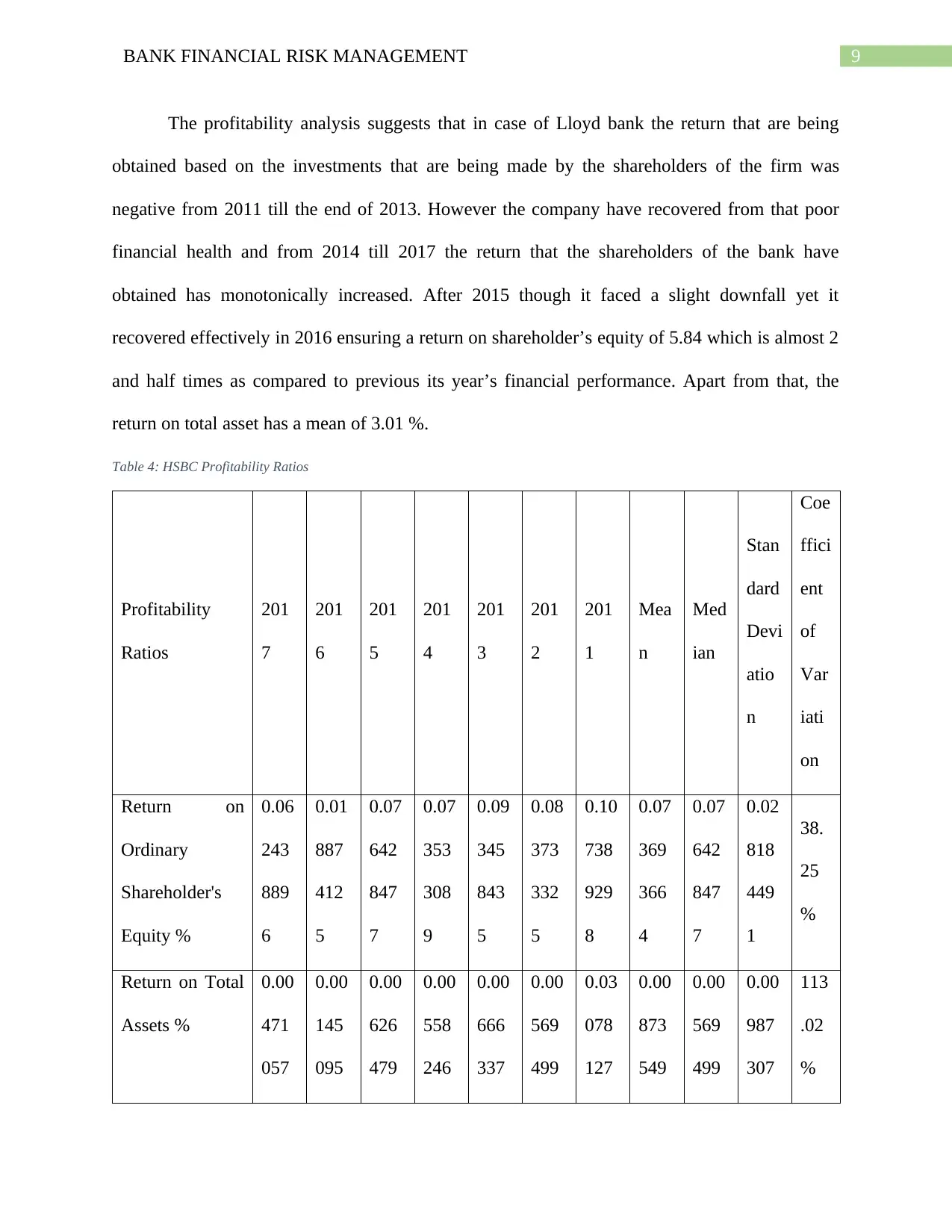

Table 4: HSBC Profitability Ratios

Profitability

Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Mea

n

Med

ian

Stan

dard

Devi

atio

n

Coe

ffici

ent

of

Var

iati

on

Return on

Ordinary

Shareholder's

Equity %

0.06

243

889

6

0.01

887

412

5

0.07

642

847

7

0.07

353

308

9

0.09

345

843

5

0.08

373

332

5

0.10

738

929

8

0.07

369

366

4

0.07

642

847

7

0.02

818

449

1

38.

25

%

Return on Total

Assets %

0.00

471

057

0.00

145

095

0.00

626

479

0.00

558

246

0.00

666

337

0.00

569

499

0.03

078

127

0.00

873

549

0.00

569

499

0.00

987

307

113

.02

%

The profitability analysis suggests that in case of Lloyd bank the return that are being

obtained based on the investments that are being made by the shareholders of the firm was

negative from 2011 till the end of 2013. However the company have recovered from that poor

financial health and from 2014 till 2017 the return that the shareholders of the bank have

obtained has monotonically increased. After 2015 though it faced a slight downfall yet it

recovered effectively in 2016 ensuring a return on shareholder’s equity of 5.84 which is almost 2

and half times as compared to previous its year’s financial performance. Apart from that, the

return on total asset has a mean of 3.01 %.

Table 4: HSBC Profitability Ratios

Profitability

Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Mea

n

Med

ian

Stan

dard

Devi

atio

n

Coe

ffici

ent

of

Var

iati

on

Return on

Ordinary

Shareholder's

Equity %

0.06

243

889

6

0.01

887

412

5

0.07

642

847

7

0.07

353

308

9

0.09

345

843

5

0.08

373

332

5

0.10

738

929

8

0.07

369

366

4

0.07

642

847

7

0.02

818

449

1

38.

25

%

Return on Total

Assets %

0.00

471

057

0.00

145

095

0.00

626

479

0.00

558

246

0.00

666

337

0.00

569

499

0.03

078

127

0.00

873

549

0.00

569

499

0.00

987

307

113

.02

%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BANK FINANCIAL RISK MANAGEMENT

8 6 5 9 7 9 6 3 9 1

The profitability analysis suggests that in case of HSBC bank, the company have a

moderate performance over its profitability yet the variation is low in its profitability. It has a

mean of 0.073 which is moderate. Apart from that, the return on total asset has a mean of 0.08 %

which is not at all good and the coefficient of variation is very high.

Management Capacity Ratios

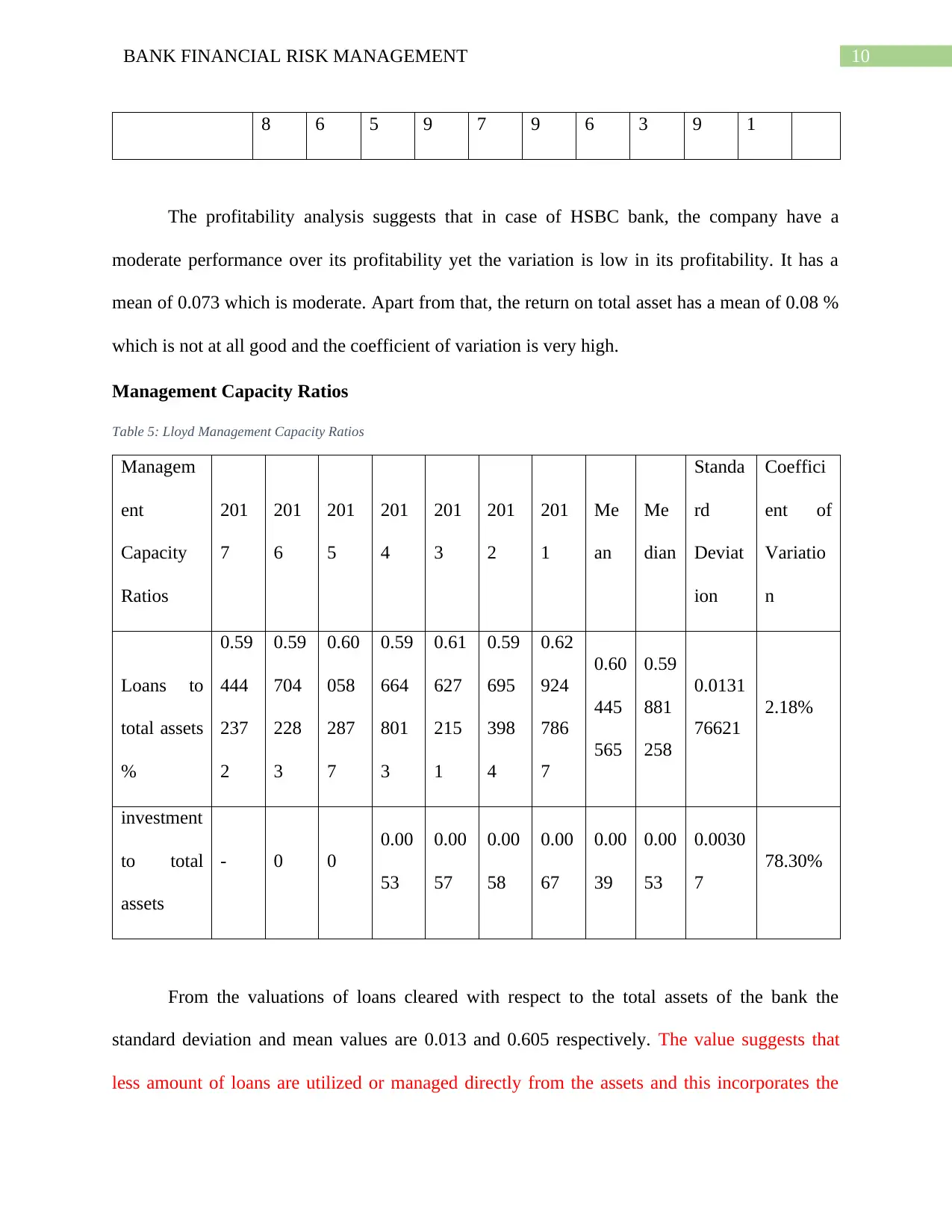

Table 5: Lloyd Management Capacity Ratios

Managem

ent

Capacity

Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Me

dian

Standa

rd

Deviat

ion

Coeffici

ent of

Variatio

n

Loans to

total assets

%

0.59

444

237

2

0.59

704

228

3

0.60

058

287

7

0.59

664

801

3

0.61

627

215

1

0.59

695

398

4

0.62

924

786

7

0.60

445

565

0.59

881

258

0.0131

76621

2.18%

investment

to total

assets

- 0 0

0.00

53

0.00

57

0.00

58

0.00

67

0.00

39

0.00

53

0.0030

7

78.30%

From the valuations of loans cleared with respect to the total assets of the bank the

standard deviation and mean values are 0.013 and 0.605 respectively. The value suggests that

less amount of loans are utilized or managed directly from the assets and this incorporates the

8 6 5 9 7 9 6 3 9 1

The profitability analysis suggests that in case of HSBC bank, the company have a

moderate performance over its profitability yet the variation is low in its profitability. It has a

mean of 0.073 which is moderate. Apart from that, the return on total asset has a mean of 0.08 %

which is not at all good and the coefficient of variation is very high.

Management Capacity Ratios

Table 5: Lloyd Management Capacity Ratios

Managem

ent

Capacity

Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Me

an

Me

dian

Standa

rd

Deviat

ion

Coeffici

ent of

Variatio

n

Loans to

total assets

%

0.59

444

237

2

0.59

704

228

3

0.60

058

287

7

0.59

664

801

3

0.61

627

215

1

0.59

695

398

4

0.62

924

786

7

0.60

445

565

0.59

881

258

0.0131

76621

2.18%

investment

to total

assets

- 0 0

0.00

53

0.00

57

0.00

58

0.00

67

0.00

39

0.00

53

0.0030

7

78.30%

From the valuations of loans cleared with respect to the total assets of the bank the

standard deviation and mean values are 0.013 and 0.605 respectively. The value suggests that

less amount of loans are utilized or managed directly from the assets and this incorporates the

11BANK FINANCIAL RISK MANAGEMENT

fact that from the perspective of risk less amount of risk is associated with the financial aspects

of the bank as the values are low. The lower value of it indicates lower risk. However, the

investment to total assets suggest that the assets that are being utilized to generate earnings is low

as its mean value is close to 0.0039 and moreover the standard deviation is low. The coefficient

of variation suggests that the degree of variation is 78 %.

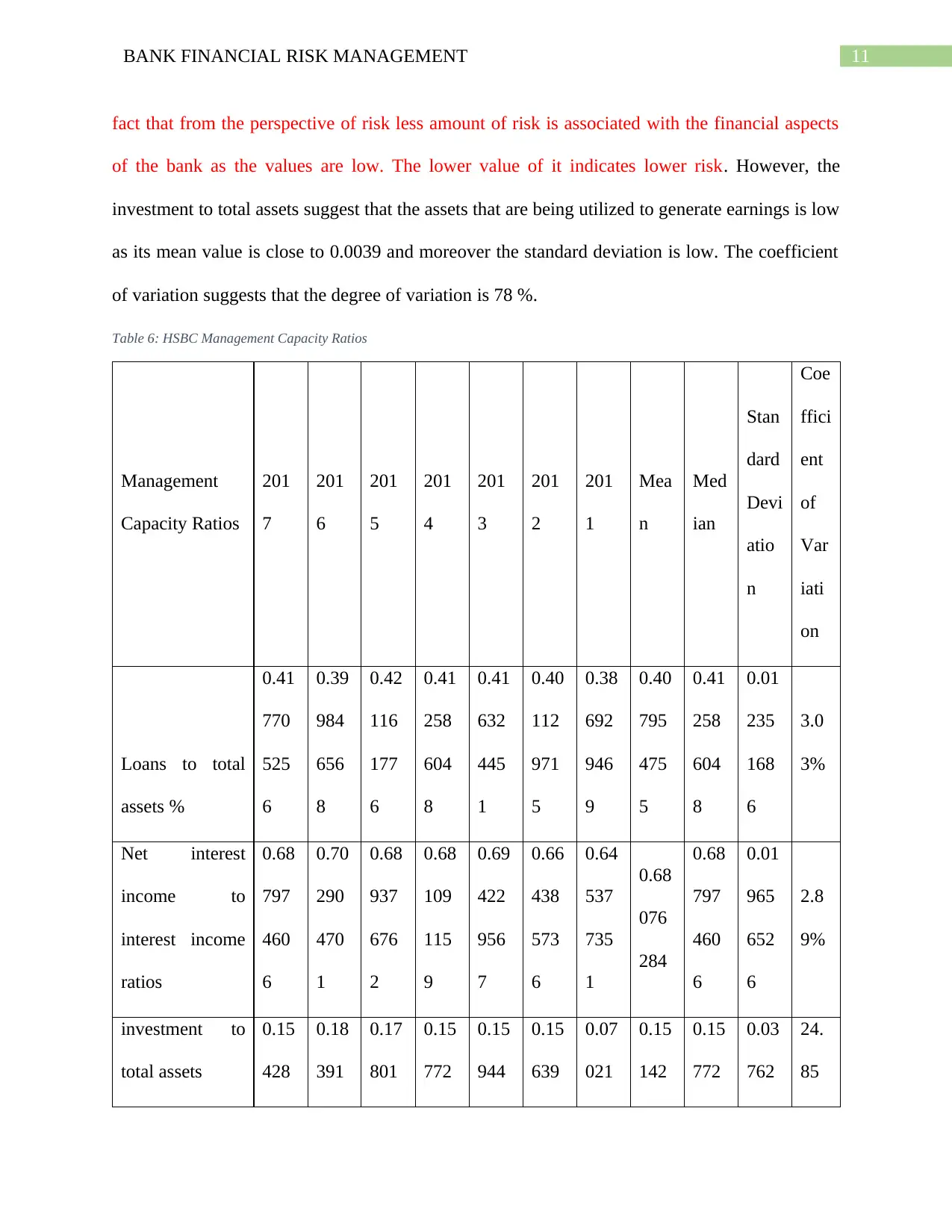

Table 6: HSBC Management Capacity Ratios

Management

Capacity Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Mea

n

Med

ian

Stan

dard

Devi

atio

n

Coe

ffici

ent

of

Var

iati

on

Loans to total

assets %

0.41

770

525

6

0.39

984

656

8

0.42

116

177

6

0.41

258

604

8

0.41

632

445

1

0.40

112

971

5

0.38

692

946

9

0.40

795

475

5

0.41

258

604

8

0.01

235

168

6

3.0

3%

Net interest

income to

interest income

ratios

0.68

797

460

6

0.70

290

470

1

0.68

937

676

2

0.68

109

115

9

0.69

422

956

7

0.66

438

573

6

0.64

537

735

1

0.68

076

284

0.68

797

460

6

0.01

965

652

6

2.8

9%

investment to

total assets

0.15

428

0.18

391

0.17

801

0.15

772

0.15

944

0.15

639

0.07

021

0.15

142

0.15

772

0.03

762

24.

85

fact that from the perspective of risk less amount of risk is associated with the financial aspects

of the bank as the values are low. The lower value of it indicates lower risk. However, the

investment to total assets suggest that the assets that are being utilized to generate earnings is low

as its mean value is close to 0.0039 and moreover the standard deviation is low. The coefficient

of variation suggests that the degree of variation is 78 %.

Table 6: HSBC Management Capacity Ratios

Management

Capacity Ratios

201

7

201

6

201

5

201

4

201

3

201

2

201

1

Mea

n

Med

ian

Stan

dard

Devi

atio

n

Coe

ffici

ent

of

Var

iati

on

Loans to total

assets %

0.41

770

525

6

0.39

984

656

8

0.42

116

177

6

0.41

258

604

8

0.41

632

445

1

0.40

112

971

5

0.38

692

946

9

0.40

795

475

5

0.41

258

604

8

0.01

235

168

6

3.0

3%

Net interest

income to

interest income

ratios

0.68

797

460

6

0.70

290

470

1

0.68

937

676

2

0.68

109

115

9

0.69

422

956

7

0.66

438

573

6

0.64

537

735

1

0.68

076

284

0.68

797

460

6

0.01

965

652

6

2.8

9%

investment to

total assets

0.15

428

0.18

391

0.17

801

0.15

772

0.15

944

0.15

639

0.07

021

0.15

142

0.15

772

0.03

762

24.

85

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.