Financial Risk Management: Profitability Measures for Australian Banks

VerifiedAdded on 2023/06/08

|12

|2157

|323

Report

AI Summary

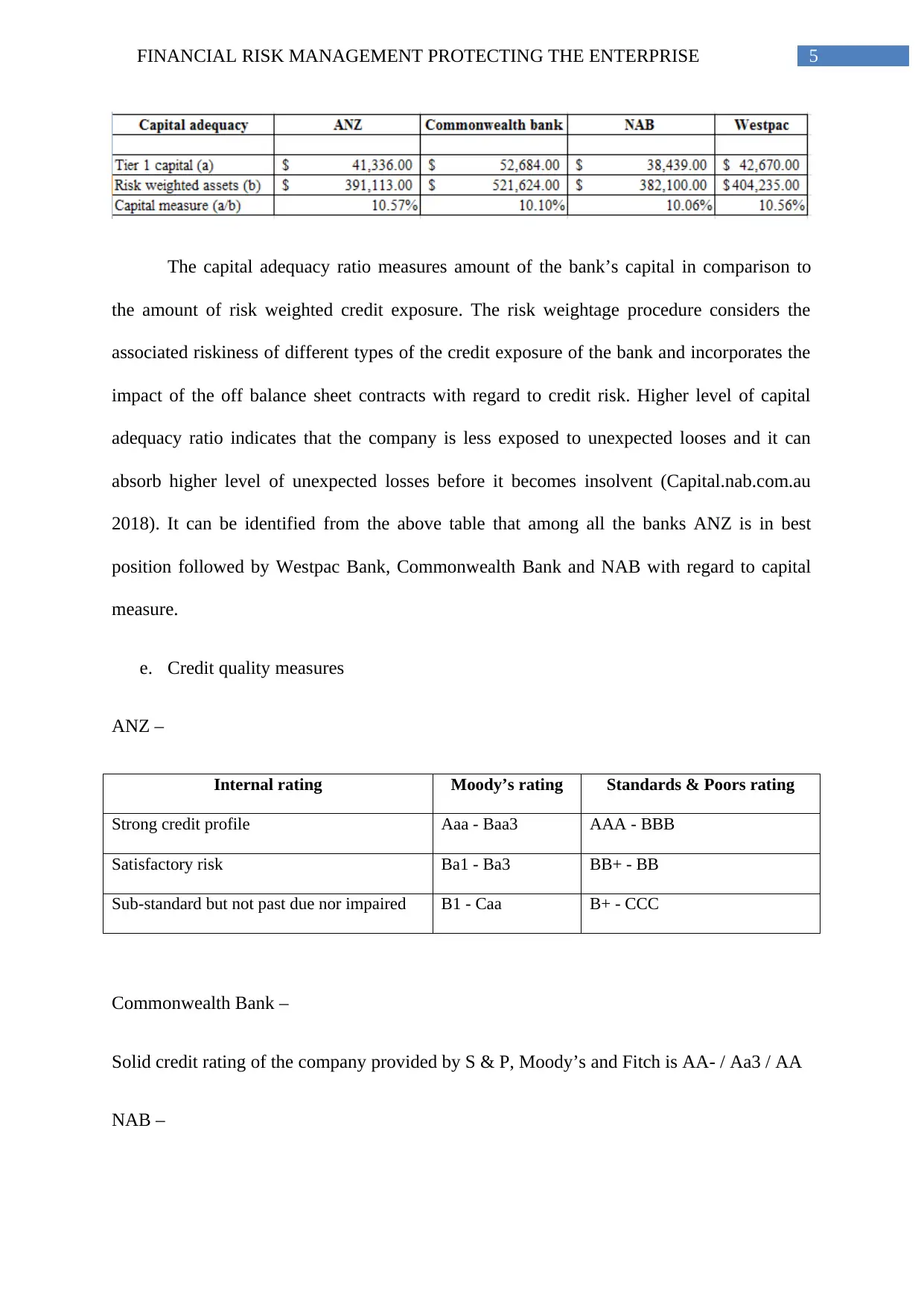

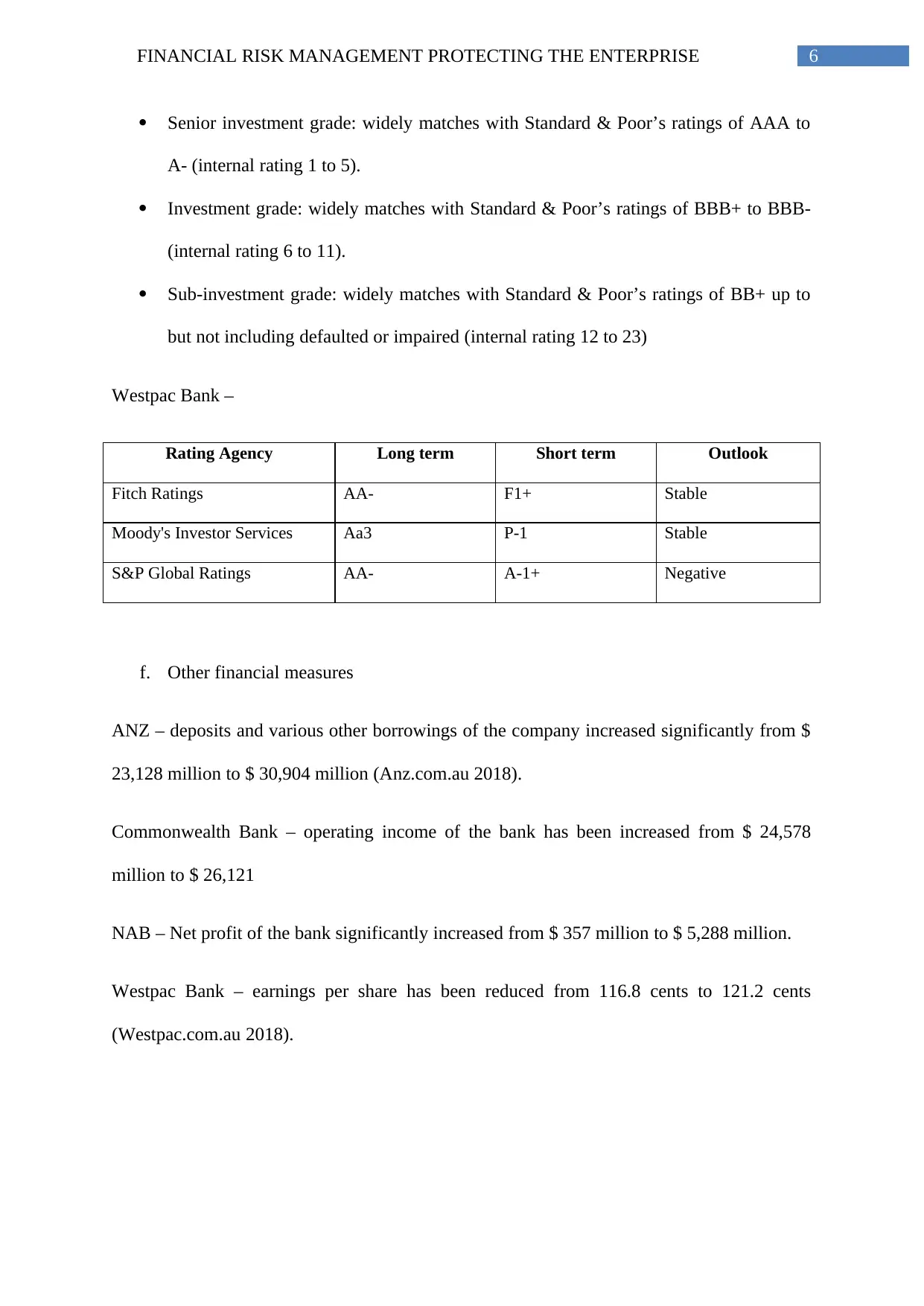

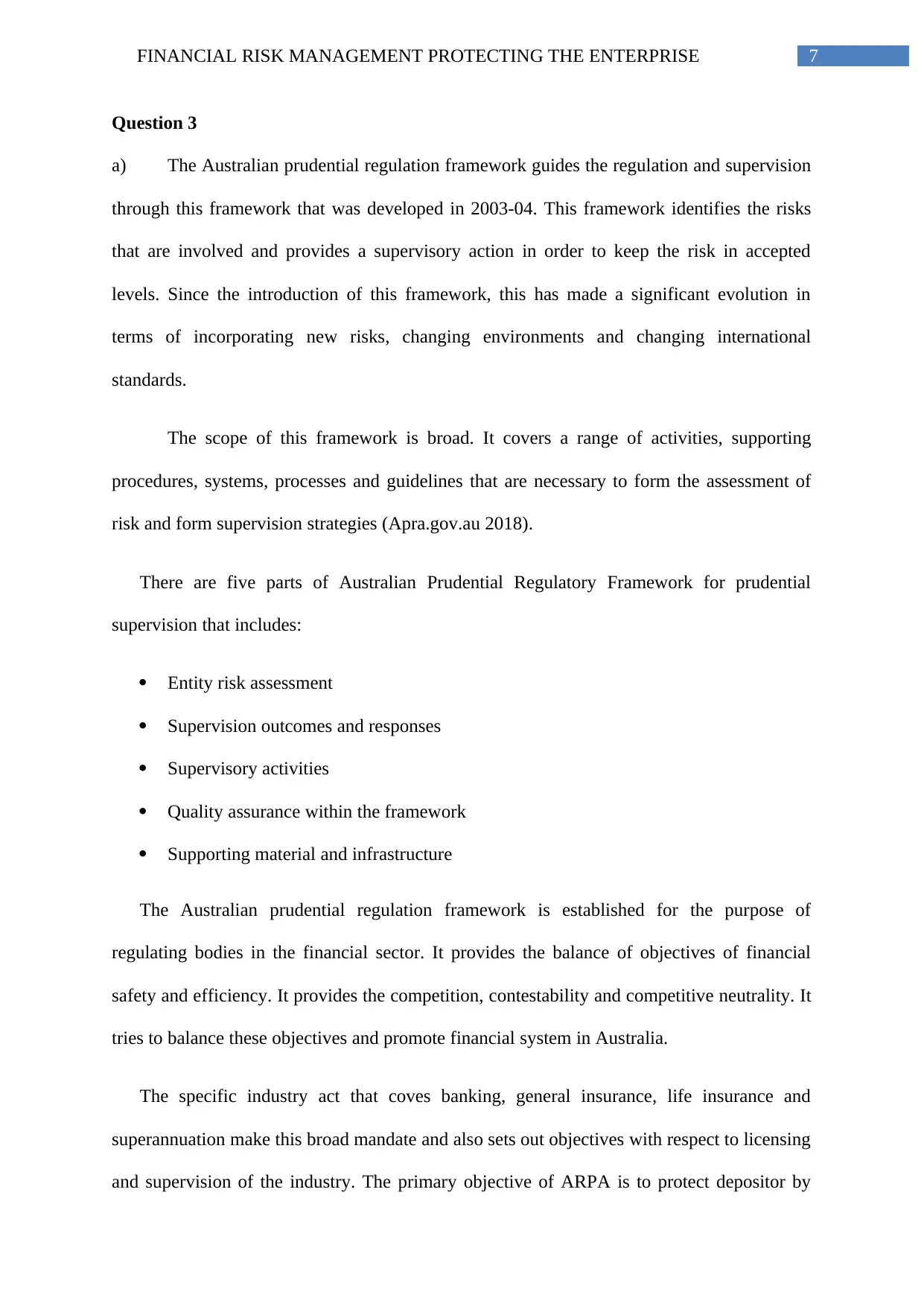

This report provides a comprehensive analysis of financial risk management within the Australian banking sector, focusing on the four major banks: Commonwealth Bank, ANZ, NAB, and Westpac. The report begins by identifying the primary sources and uses of funds for banks in Australia, supported by data from a selected bank's latest financial report. It then ranks the banks based on key metrics such as total assets, total equity, market capitalization, and profit before tax, followed by an in-depth examination of their financial performance using profitability ratios. The analysis extends to evaluating the banks' overall financial positions, including debt-equity ratios and capital adequacy, and assesses credit quality through internal and external ratings. Furthermore, the report explores various financial measures, including changes in deposits, operating income, net profit, and earnings per share. The report also discusses the Australian Prudential Regulation Framework (APRA), its role in guiding regulation and supervision, and its impact on the banking sector. Finally, the report calculates and interprets return on assets and return on equity to evaluate the banks' profitability and efficiency.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.