Comparative Financial Risk Analysis: HSBC and Lloyds Bank Report

VerifiedAdded on 2021/12/13

|17

|1792

|65

Report

AI Summary

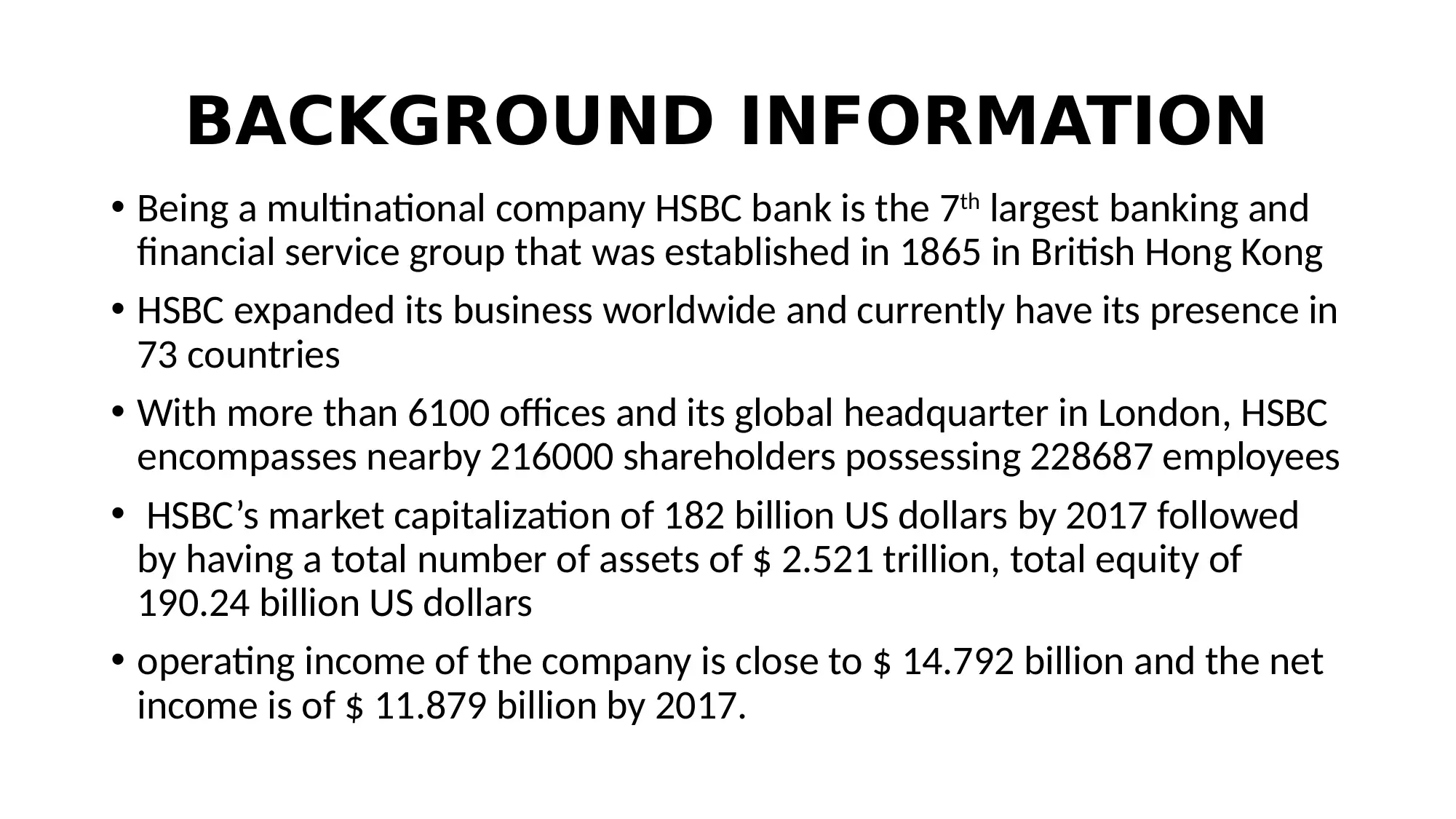

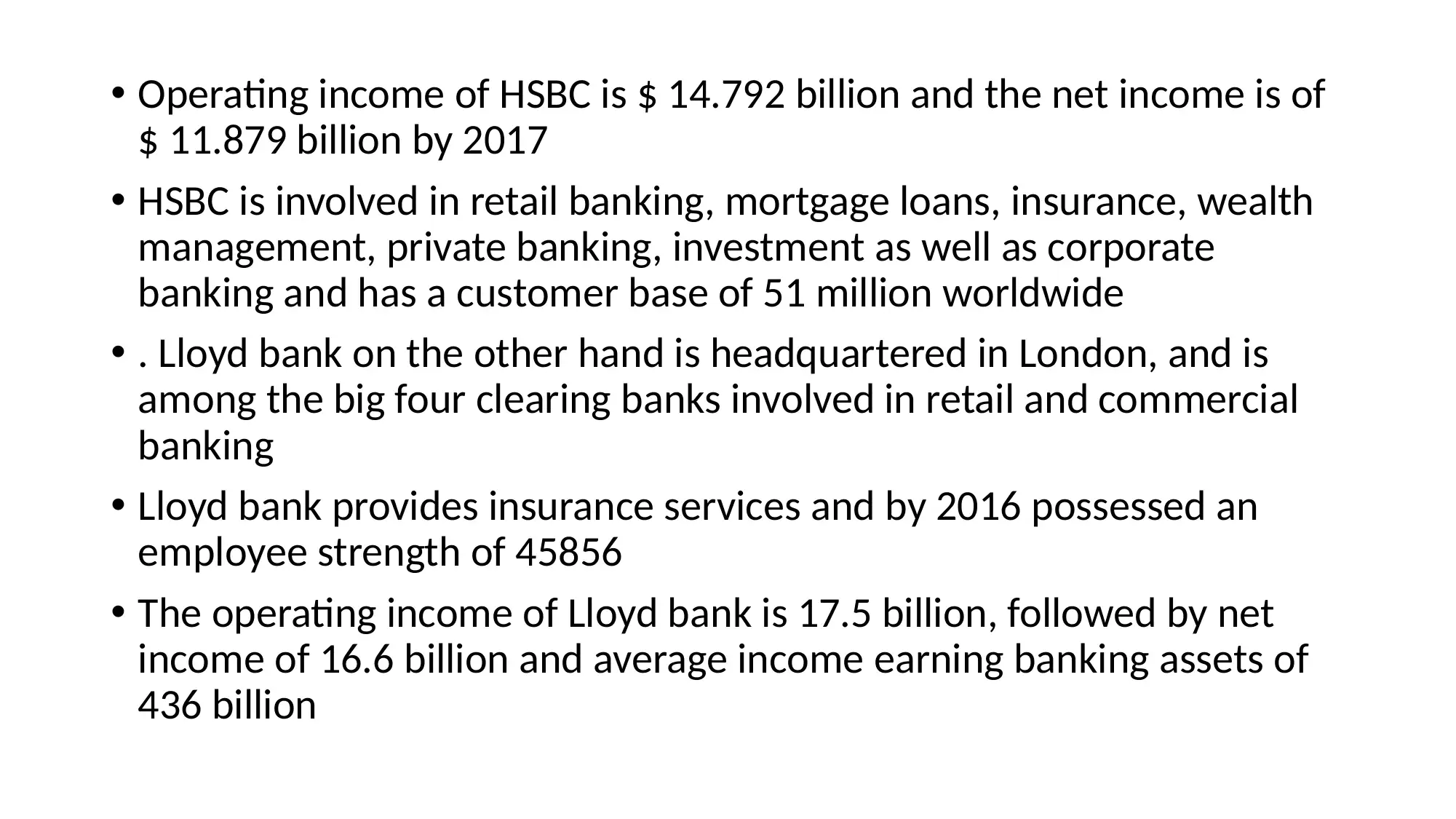

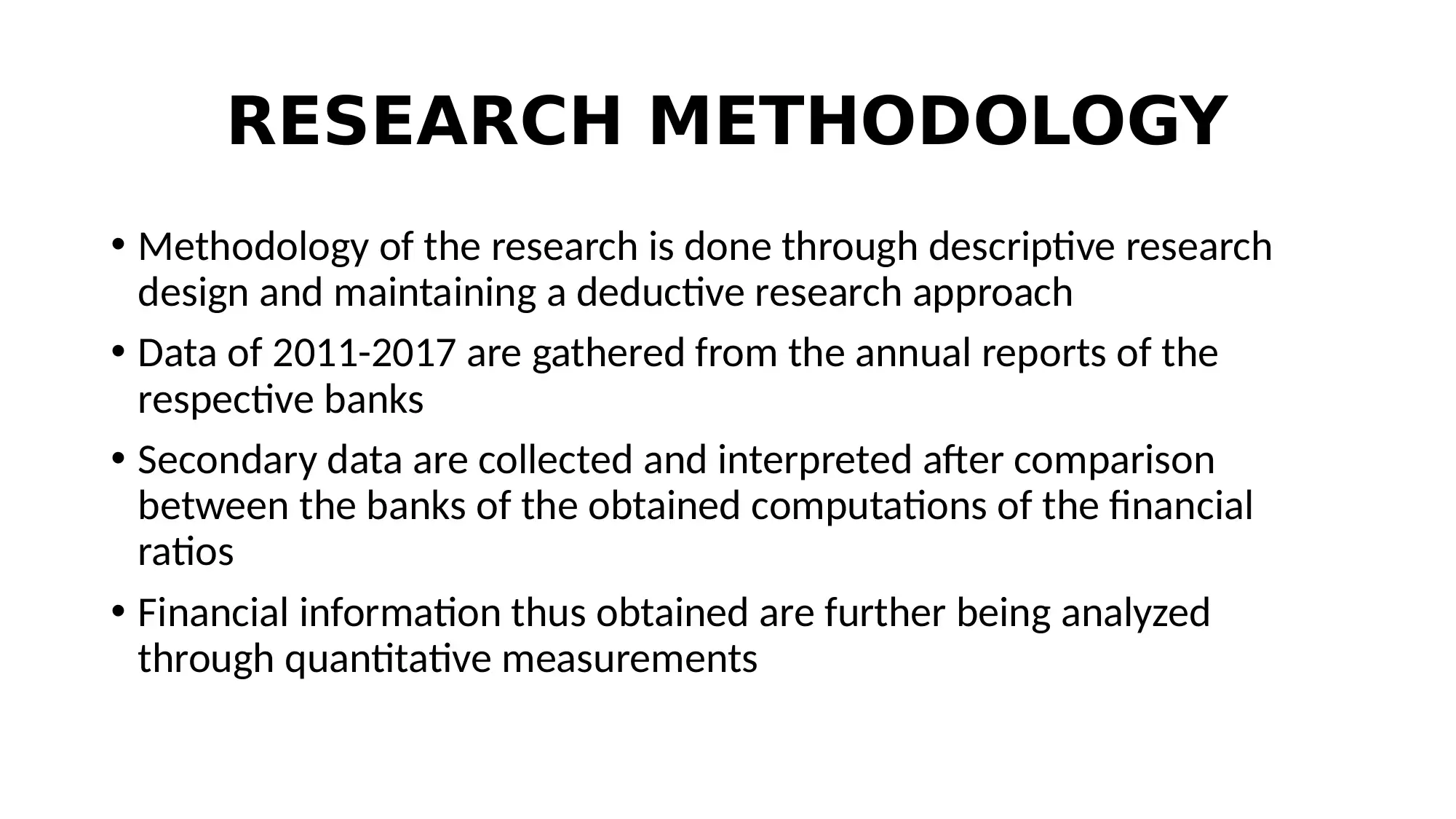

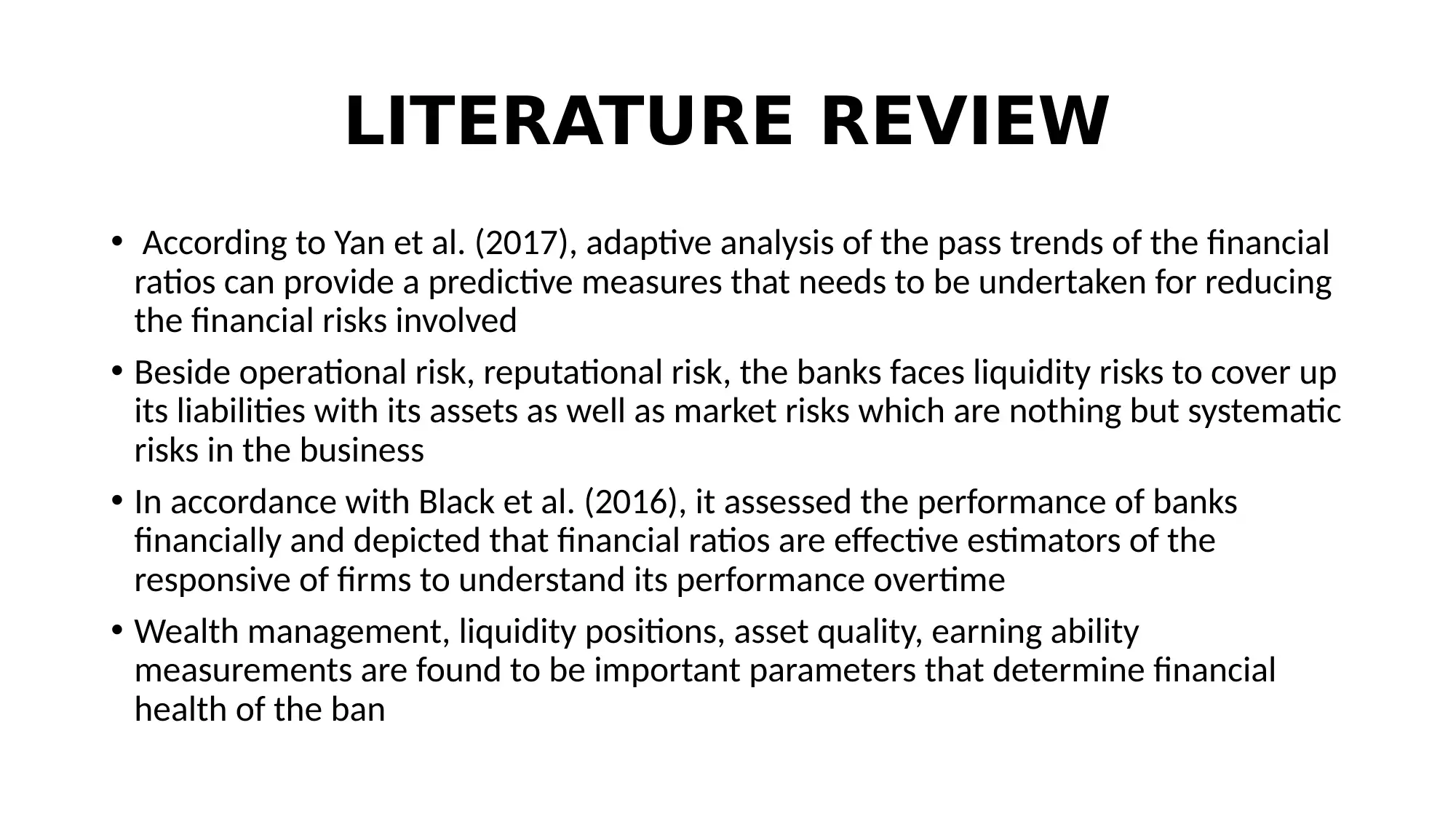

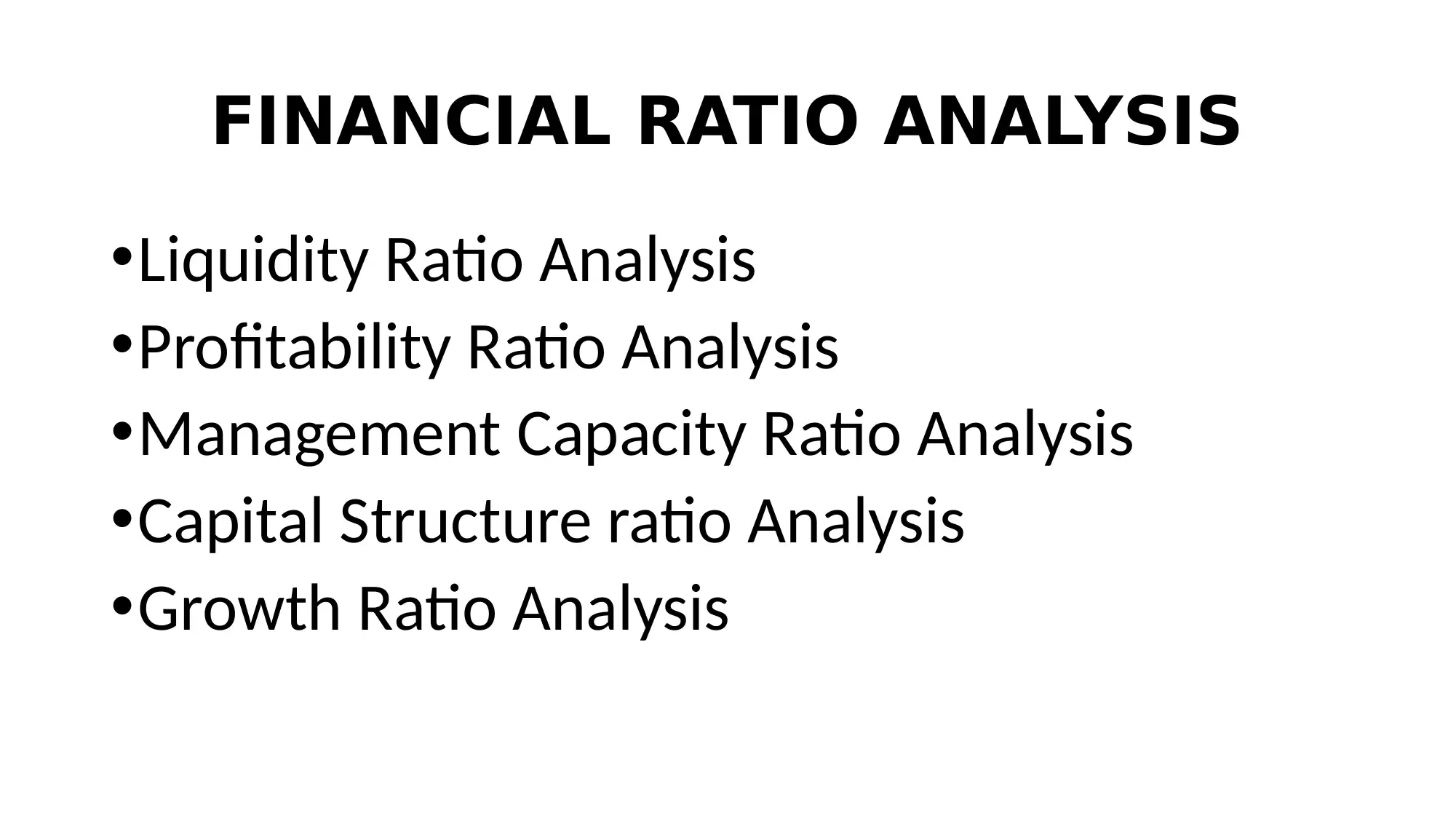

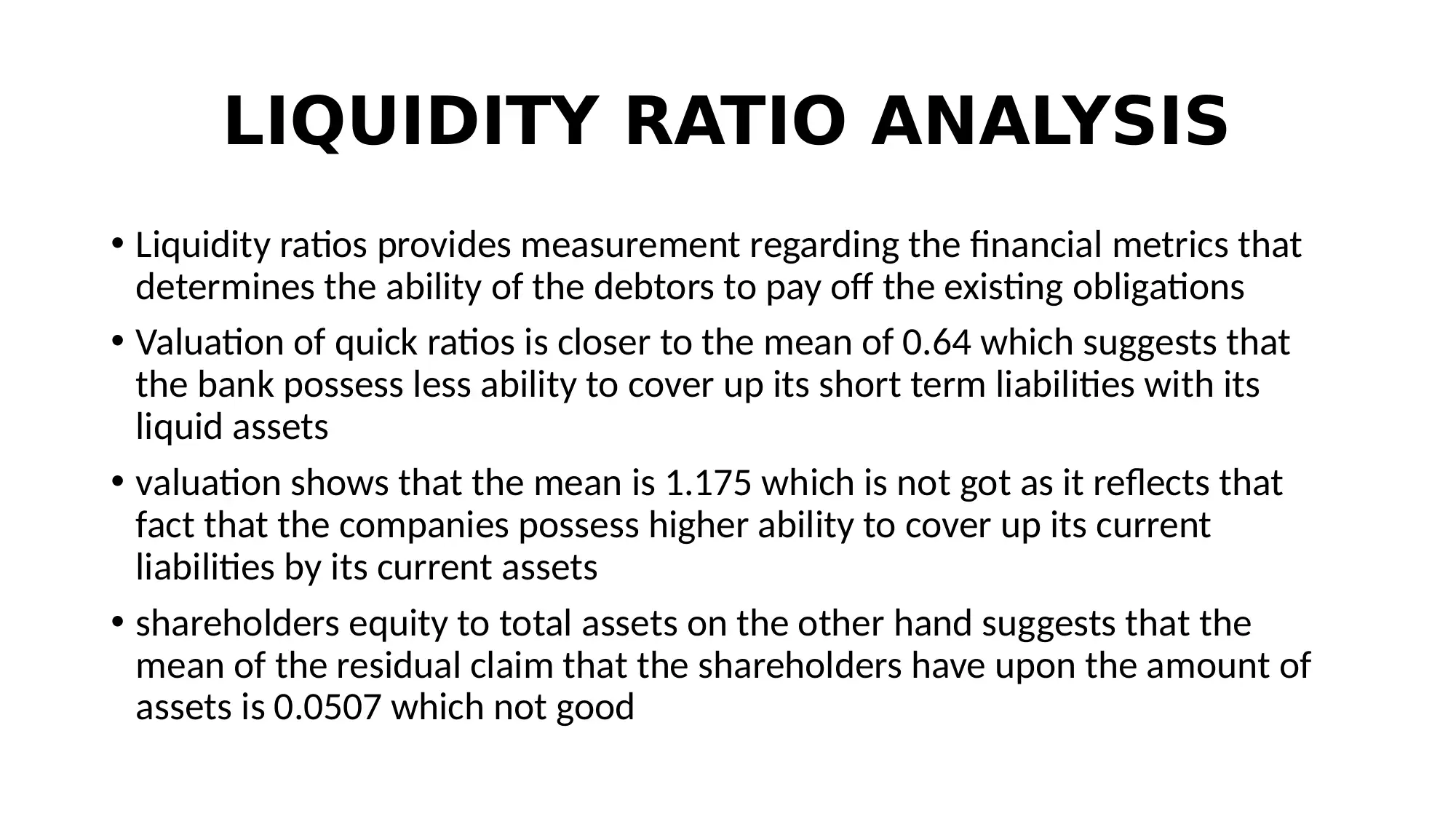

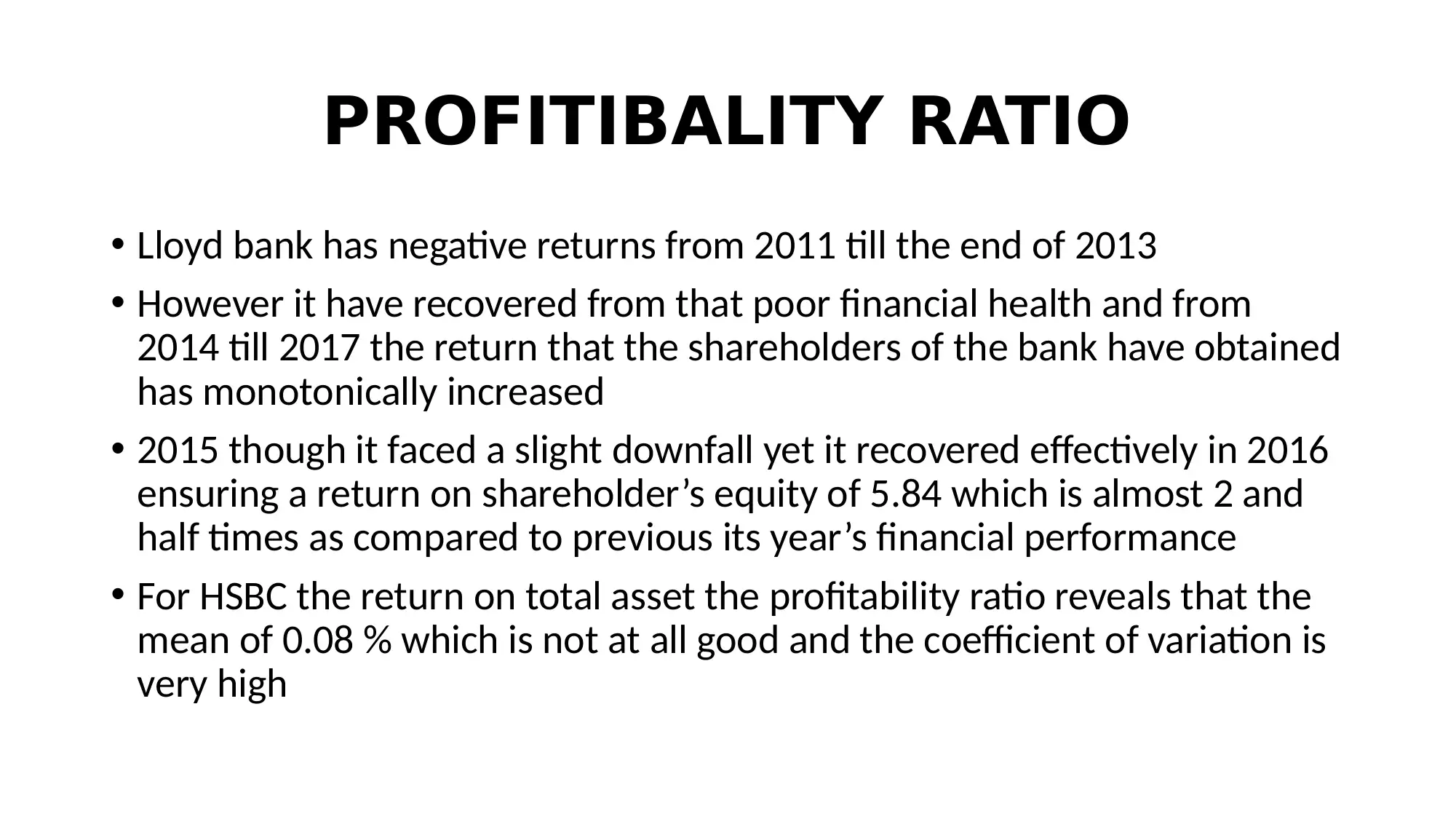

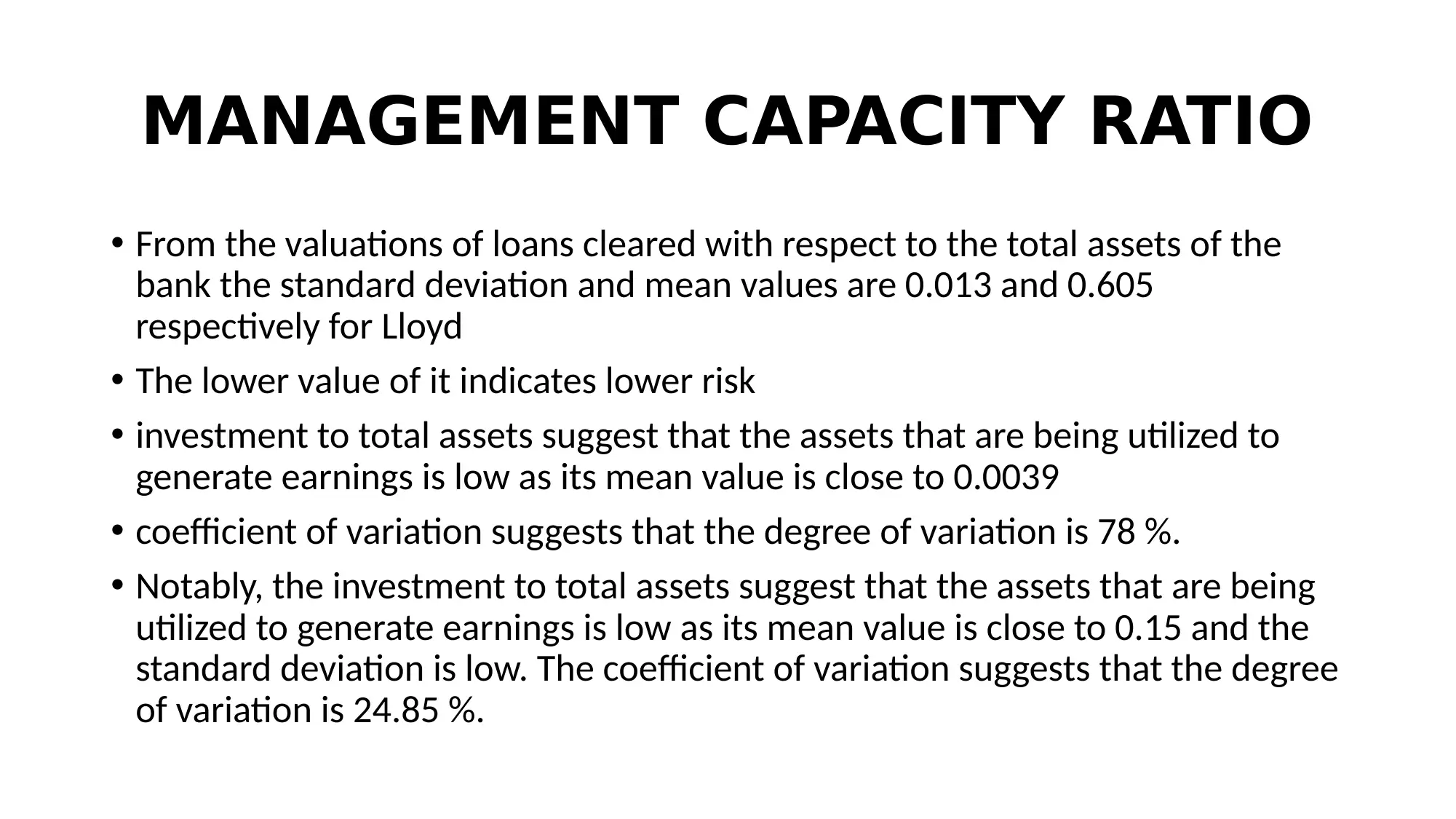

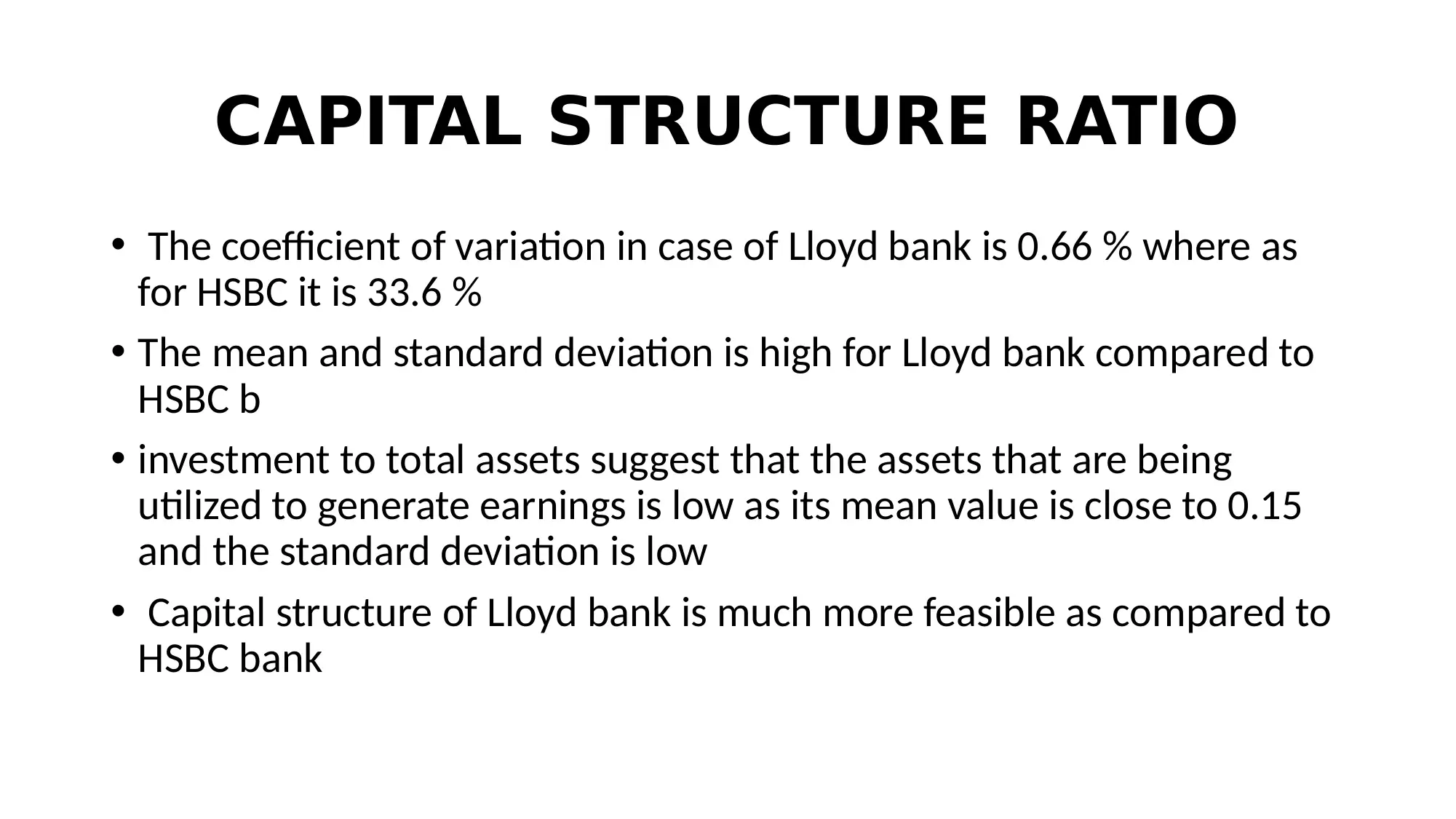

This report provides a comparative analysis of financial risk management in HSBC and Lloyds banks from 2011 to 2017. The study utilizes a descriptive research design and a deductive approach, analyzing secondary data from the banks' annual reports. Financial ratios, including liquidity, profitability, management capacity, capital structure, and growth ratios, are computed and compared. The analysis reveals that both banks face various financial risks, with HSBC demonstrating a stronger capital structure and better risk mitigation abilities compared to Lloyds Bank. The report highlights key findings on liquidity positions, asset quality, and earnings, offering insights into the banks' financial health and performance over the studied period. The conclusion emphasizes the variability in HSBC's financial metrics compared to Lloyds, suggesting a more credible dispersion in HSBC's performance. The study also incorporates a review of existing literature on financial risk, providing a comprehensive overview of the topic. The report concludes by summarizing the key differences in capital structure and relative variability between the two banks.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.