Financial Analysis: Risk and Return for Market Index and Two Shares

VerifiedAdded on 2020/04/07

|3

|720

|40

Report

AI Summary

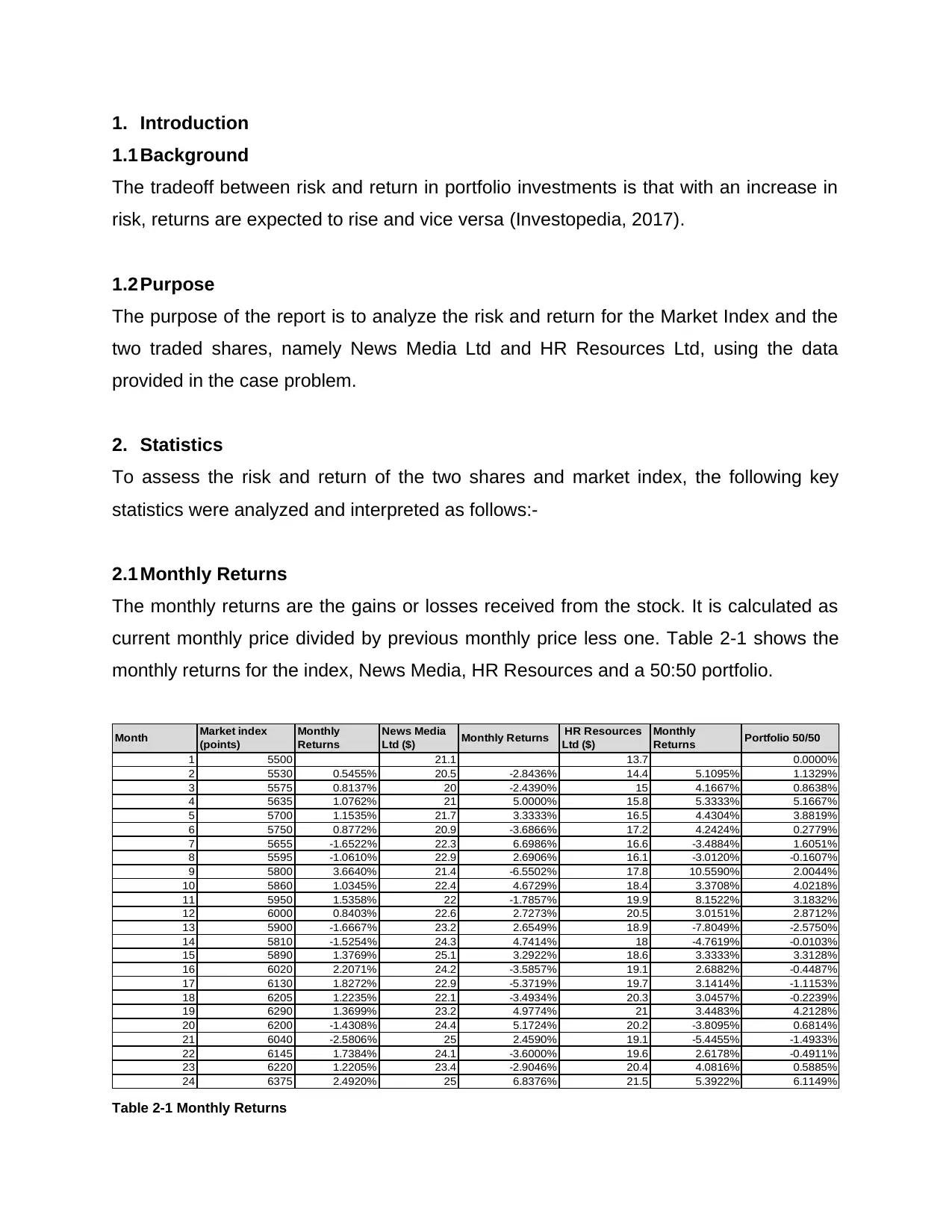

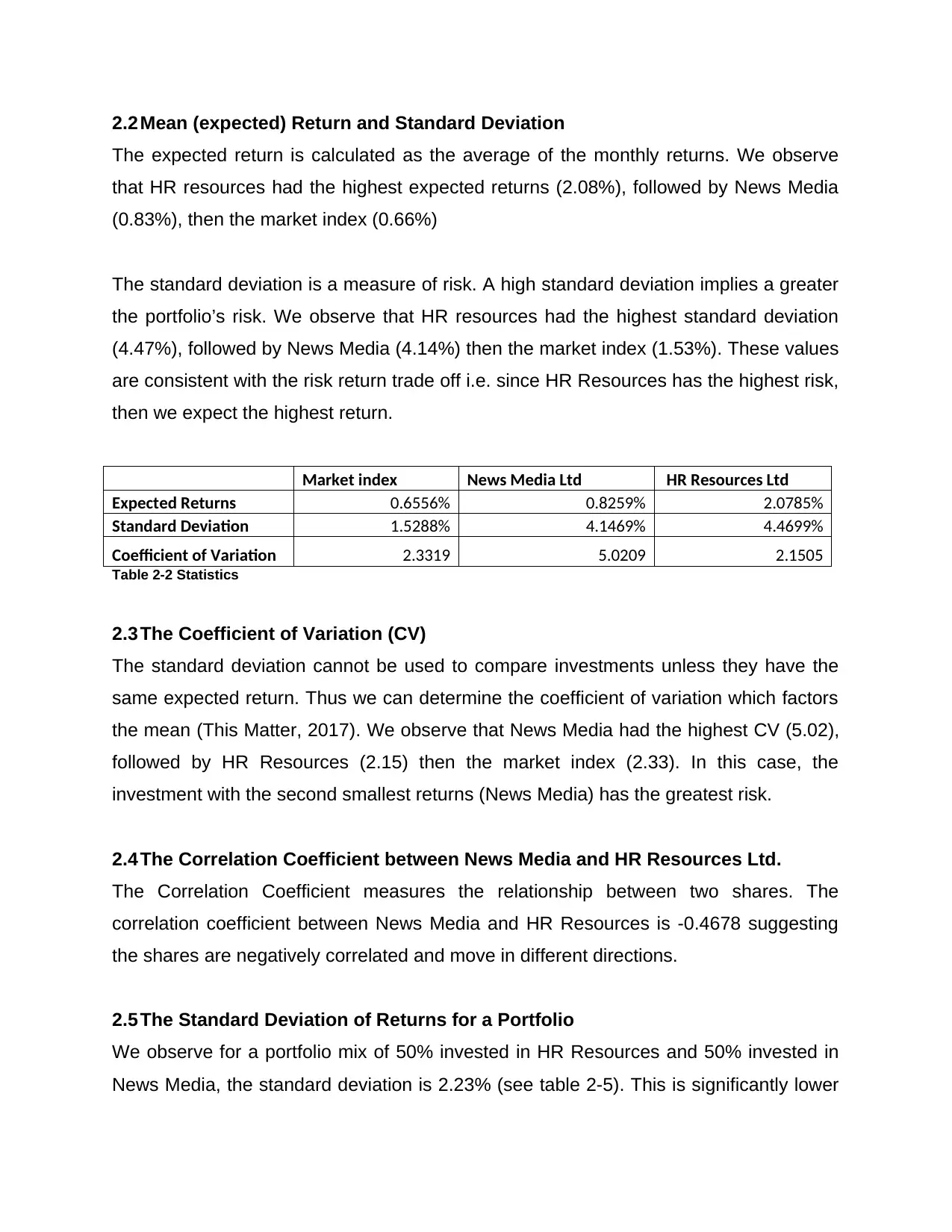

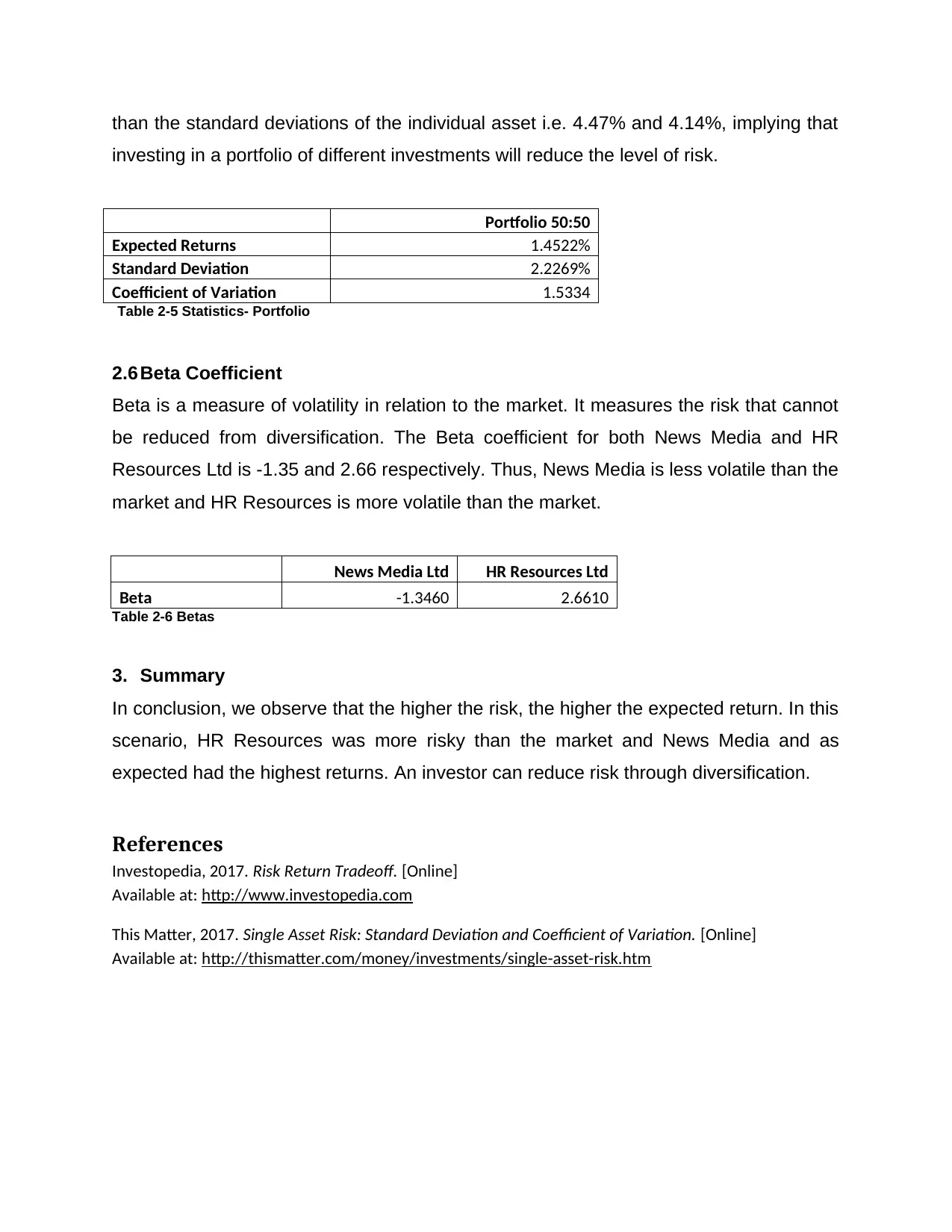

This report analyzes the risk and return of the Market Index, News Media Ltd, and HR Resources Ltd. It examines key financial statistics like monthly returns, expected returns, standard deviation, coefficient of variation, correlation coefficients, and beta coefficients to assess investment risk. The analysis reveals that HR Resources, with the highest standard deviation, also has the highest expected returns, supporting the risk-return tradeoff. The report also highlights how diversification through a 50:50 portfolio of HR Resources and News Media can reduce overall risk. The beta coefficients further illustrate the volatility of each share relative to the market. The report concludes that higher risk investments can provide higher returns and that diversification is a useful tool to manage risk.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.