Diploma of Finance and Mortgage Broking - Financial Services

VerifiedAdded on 2022/08/18

|24

|3757

|14

Homework Assignment

AI Summary

This document presents a detailed solution for a Diploma of Finance and Mortgage Broking assignment. It covers a range of topics, including the influence of external factors on interest rates, the role of financial services sectors like banking and corporate sectors, and the Australian Financial Complaints Authority (AFCA). The assignment explores communication strategies related to AFCA, the impact of the Comprehensive Credit Reporting (CCR), and the implications of credit representative appointments. It also addresses aspects such as ABN/ACN, GST, performance objectives, training requirements, and role-modeling within the finance and mortgage broking context. The document includes various tasks and questions providing a comprehensive overview of the financial services landscape, relevant legislation, and compliance requirements.

Running head: DIPLOMA OF FINANCE AND MORTGAGE BROKING

Diploma of Finance and Mortgage Broking

Name of the Student

Name of the University

Author Note

Diploma of Finance and Mortgage Broking

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1DIPLOMA OF FINANCE AND MORTGAGE BROKING

Table of Contents

Task 1...............................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................4

Task 2...........................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................6

Task 3...........................................................................................................................................7

Question 1....................................................................................................................................7

Question 2....................................................................................................................................7

Question 3....................................................................................................................................7

Task 4...........................................................................................................................................8

Question 1....................................................................................................................................8

Question 2....................................................................................................................................9

Question 3....................................................................................................................................9

Task 5.........................................................................................................................................10

Question 1..................................................................................................................................10

Question 2..................................................................................................................................11

Question 3..................................................................................................................................11

Question 4..................................................................................................................................12

Table of Contents

Task 1...............................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................4

Task 2...........................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................6

Task 3...........................................................................................................................................7

Question 1....................................................................................................................................7

Question 2....................................................................................................................................7

Question 3....................................................................................................................................7

Task 4...........................................................................................................................................8

Question 1....................................................................................................................................8

Question 2....................................................................................................................................9

Question 3....................................................................................................................................9

Task 5.........................................................................................................................................10

Question 1..................................................................................................................................10

Question 2..................................................................................................................................11

Question 3..................................................................................................................................11

Question 4..................................................................................................................................12

2DIPLOMA OF FINANCE AND MORTGAGE BROKING

Question 5..................................................................................................................................13

Question 6..................................................................................................................................13

Question 7..................................................................................................................................13

Question 8..................................................................................................................................14

Question 9..................................................................................................................................14

Task 6.........................................................................................................................................14

Question 1..................................................................................................................................14

Question 2..................................................................................................................................15

Question 3..................................................................................................................................16

Task 7.........................................................................................................................................16

Question 1..................................................................................................................................16

Question 2..................................................................................................................................16

Question 3..................................................................................................................................17

Task 8.........................................................................................................................................17

Question 1..................................................................................................................................17

Question 2..................................................................................................................................18

Question 3..................................................................................................................................20

Question 4..................................................................................................................................20

Sustainability goal......................................................................................................................20

Economic outcome/s..................................................................................................................20

Question 5..................................................................................................................................13

Question 6..................................................................................................................................13

Question 7..................................................................................................................................13

Question 8..................................................................................................................................14

Question 9..................................................................................................................................14

Task 6.........................................................................................................................................14

Question 1..................................................................................................................................14

Question 2..................................................................................................................................15

Question 3..................................................................................................................................16

Task 7.........................................................................................................................................16

Question 1..................................................................................................................................16

Question 2..................................................................................................................................16

Question 3..................................................................................................................................17

Task 8.........................................................................................................................................17

Question 1..................................................................................................................................17

Question 2..................................................................................................................................18

Question 3..................................................................................................................................20

Question 4..................................................................................................................................20

Sustainability goal......................................................................................................................20

Economic outcome/s..................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3DIPLOMA OF FINANCE AND MORTGAGE BROKING

Task 9.........................................................................................................................................21

Question 1..................................................................................................................................21

Question 2..................................................................................................................................21

Question 3..................................................................................................................................21

Question 4..................................................................................................................................21

Question 5..................................................................................................................................21

Question 6..................................................................................................................................22

Question 7..................................................................................................................................22

Question 8..................................................................................................................................22

Bibliography...............................................................................................................................23

Task 9.........................................................................................................................................21

Question 1..................................................................................................................................21

Question 2..................................................................................................................................21

Question 3..................................................................................................................................21

Question 4..................................................................................................................................21

Question 5..................................................................................................................................21

Question 6..................................................................................................................................22

Question 7..................................................................................................................................22

Question 8..................................................................................................................................22

Bibliography...............................................................................................................................23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4DIPLOMA OF FINANCE AND MORTGAGE BROKING

Task 1

Question 1

The three external factors which could influence the movement in the interest rates and

also dictate the economic and political climate are the level of inflation, growth in the wage rates

and the level of job security in the country. In case of low inflation, the consumers choose to

spend more which results in the lower interest rates. If the rate of inflation is high, then the

government increases the interest rates to compensate the consumers for sacrificing their

consumption. Similarly, growth of wages also positively impacts the interest rates as there is a

growth in the income available for saving. The job insecurity results in a decrease in the interest

rates as investors prefer to save more than they spend in these situations. Hence, the incentive to

save becomes lower due to lower interest rates. In these cases, the interest rates not only affect

the Central bank but they also effect the investment choices of the financial and other sectors in

the economy.

Question 2

The two financial services sectors that are involved in influencing the interest rates

prevalent in the economy are the banking sector and the corporate sector. The banking sector

determines the interest rates prevalent in the economy and they change the interest rates

according to the conditions existing in the market. The corporate giants determine the interest

rates by purchasing bonds from the markets and injecting the funds into the banks to fund their

business operations in the short term and the long run.

Task 1

Question 1

The three external factors which could influence the movement in the interest rates and

also dictate the economic and political climate are the level of inflation, growth in the wage rates

and the level of job security in the country. In case of low inflation, the consumers choose to

spend more which results in the lower interest rates. If the rate of inflation is high, then the

government increases the interest rates to compensate the consumers for sacrificing their

consumption. Similarly, growth of wages also positively impacts the interest rates as there is a

growth in the income available for saving. The job insecurity results in a decrease in the interest

rates as investors prefer to save more than they spend in these situations. Hence, the incentive to

save becomes lower due to lower interest rates. In these cases, the interest rates not only affect

the Central bank but they also effect the investment choices of the financial and other sectors in

the economy.

Question 2

The two financial services sectors that are involved in influencing the interest rates

prevalent in the economy are the banking sector and the corporate sector. The banking sector

determines the interest rates prevalent in the economy and they change the interest rates

according to the conditions existing in the market. The corporate giants determine the interest

rates by purchasing bonds from the markets and injecting the funds into the banks to fund their

business operations in the short term and the long run.

5DIPLOMA OF FINANCE AND MORTGAGE BROKING

Task 2

Question 1

Dear Colleagues,

The Australian Financial Complaints Authority is an Australian external dispute

resolution scheme which intends to resolve the complaints of the consumers with their member

financial organisations. Based on the ASIC Regulatory Guide RG 165, various bodies like the

Australian financial services licensees, credit licensees and authorised credit representatives are

all required to be members of AFCA. The main advantage of having the membership of AFCA is

that most of its members do not have any complaint lodged against them. This is because of the

fair, independent and effective solutions provided by the experienced and professional staff

operating within the organisation. Other benefits of the membership of AFCA include the

expertise, professional development, knowledge and security provided by the scheme. It also

ensures that the firms registering with it are complying with the guidelines of ASIC.

The key points that are needed to be considered in communicating to the customers are

the purpose of AFCA and its basic nature. As the purpose of it is to settle complaints from

consumers and small businesses, it saves a huge amount of time and resources for the same.

Apart from it, the fact related to it being made mandatory by the ASIC should also be explained

to the consumers. However, it should also be mentioned that it is not a company or a government

department to avoid confusion about its nature and the bodies governing it. It also provides

certain confidence to the consumers before investing in the same. The application fees and the

basis of its calculation also need to be explained to the consumers. The range of complaints

which are covered by the scheme including credit, financial, loan, banking deposits and

Task 2

Question 1

Dear Colleagues,

The Australian Financial Complaints Authority is an Australian external dispute

resolution scheme which intends to resolve the complaints of the consumers with their member

financial organisations. Based on the ASIC Regulatory Guide RG 165, various bodies like the

Australian financial services licensees, credit licensees and authorised credit representatives are

all required to be members of AFCA. The main advantage of having the membership of AFCA is

that most of its members do not have any complaint lodged against them. This is because of the

fair, independent and effective solutions provided by the experienced and professional staff

operating within the organisation. Other benefits of the membership of AFCA include the

expertise, professional development, knowledge and security provided by the scheme. It also

ensures that the firms registering with it are complying with the guidelines of ASIC.

The key points that are needed to be considered in communicating to the customers are

the purpose of AFCA and its basic nature. As the purpose of it is to settle complaints from

consumers and small businesses, it saves a huge amount of time and resources for the same.

Apart from it, the fact related to it being made mandatory by the ASIC should also be explained

to the consumers. However, it should also be mentioned that it is not a company or a government

department to avoid confusion about its nature and the bodies governing it. It also provides

certain confidence to the consumers before investing in the same. The application fees and the

basis of its calculation also need to be explained to the consumers. The range of complaints

which are covered by the scheme including credit, financial, loan, banking deposits and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6DIPLOMA OF FINANCE AND MORTGAGE BROKING

insurance complaints all need to be taken into consideration. The range of firms which are

registered and the mandatory nature of the scheme should also be explained to the consumers.

The nature of remedies like compensation for losses and the other solutions provided by the

same should be clearly stated. The aspects which are supported by the scheme and how they

benefit the consumers need to be explained. Similarly, the codes and other related aspects which

are administered by the firm also need to taken into consideration.

The AFCA Code Compliance team supports the financial firms to strengthen their

relationship with the customers, improve the complaints handing from customers and also reduce

the number of disputes arising from customers through improved service delivery. Some of the

aspects administered by it include the Code of Banking Practice, General Insurance Code of

Practice, Insurance Brokers Code of Practice, and Customer owned Banking Code of Practice

and the Life Insurance Code of Practice.

Question 2

The key points that need to be kept in mind while communicating information about

AFCA to the customers are as follows:

ASIC Regulatory Guide 165

Form 5 Information Statement

Form 9 Information Statement

Form 17 Information Statement

Other relevant information like final response letters, delay letters and credit guide are

all important aspects to consider in explaining the same to the consumers.

insurance complaints all need to be taken into consideration. The range of firms which are

registered and the mandatory nature of the scheme should also be explained to the consumers.

The nature of remedies like compensation for losses and the other solutions provided by the

same should be clearly stated. The aspects which are supported by the scheme and how they

benefit the consumers need to be explained. Similarly, the codes and other related aspects which

are administered by the firm also need to taken into consideration.

The AFCA Code Compliance team supports the financial firms to strengthen their

relationship with the customers, improve the complaints handing from customers and also reduce

the number of disputes arising from customers through improved service delivery. Some of the

aspects administered by it include the Code of Banking Practice, General Insurance Code of

Practice, Insurance Brokers Code of Practice, and Customer owned Banking Code of Practice

and the Life Insurance Code of Practice.

Question 2

The key points that need to be kept in mind while communicating information about

AFCA to the customers are as follows:

ASIC Regulatory Guide 165

Form 5 Information Statement

Form 9 Information Statement

Form 17 Information Statement

Other relevant information like final response letters, delay letters and credit guide are

all important aspects to consider in explaining the same to the consumers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7DIPLOMA OF FINANCE AND MORTGAGE BROKING

Task 3

Question 1

The main change will be related to the manner in which the creditworthiness of the

consumers is determined. Instead of only looking at the negative aspects of a consumer, the CCR

also allows the organisation to operate more efficiently and maintain and develop a good

relationship with the consumers.

Question 2

The usage of the Equifax website and connecting it to the industry on which information

is required is a good way of ensuring that regular updates are received with regards to the

changes in the CCR or any other related regulations.

Question 3

Who How By when

Finance Brokers Through an internal

document generated to all the

finance brokers

Within two weeks from the date

the guidelines were published

Consumers Through an additional

privacy form which is

generated to all the existing

and new customers and

provides information about

their credit worthiness and

the manner in which it was

Within a month to all the existing

forms and as a part of the business

process in relation to the new

customers.

Task 3

Question 1

The main change will be related to the manner in which the creditworthiness of the

consumers is determined. Instead of only looking at the negative aspects of a consumer, the CCR

also allows the organisation to operate more efficiently and maintain and develop a good

relationship with the consumers.

Question 2

The usage of the Equifax website and connecting it to the industry on which information

is required is a good way of ensuring that regular updates are received with regards to the

changes in the CCR or any other related regulations.

Question 3

Who How By when

Finance Brokers Through an internal

document generated to all the

finance brokers

Within two weeks from the date

the guidelines were published

Consumers Through an additional

privacy form which is

generated to all the existing

and new customers and

provides information about

their credit worthiness and

the manner in which it was

Within a month to all the existing

forms and as a part of the business

process in relation to the new

customers.

8DIPLOMA OF FINANCE AND MORTGAGE BROKING

determined.

Task 4

Question 1

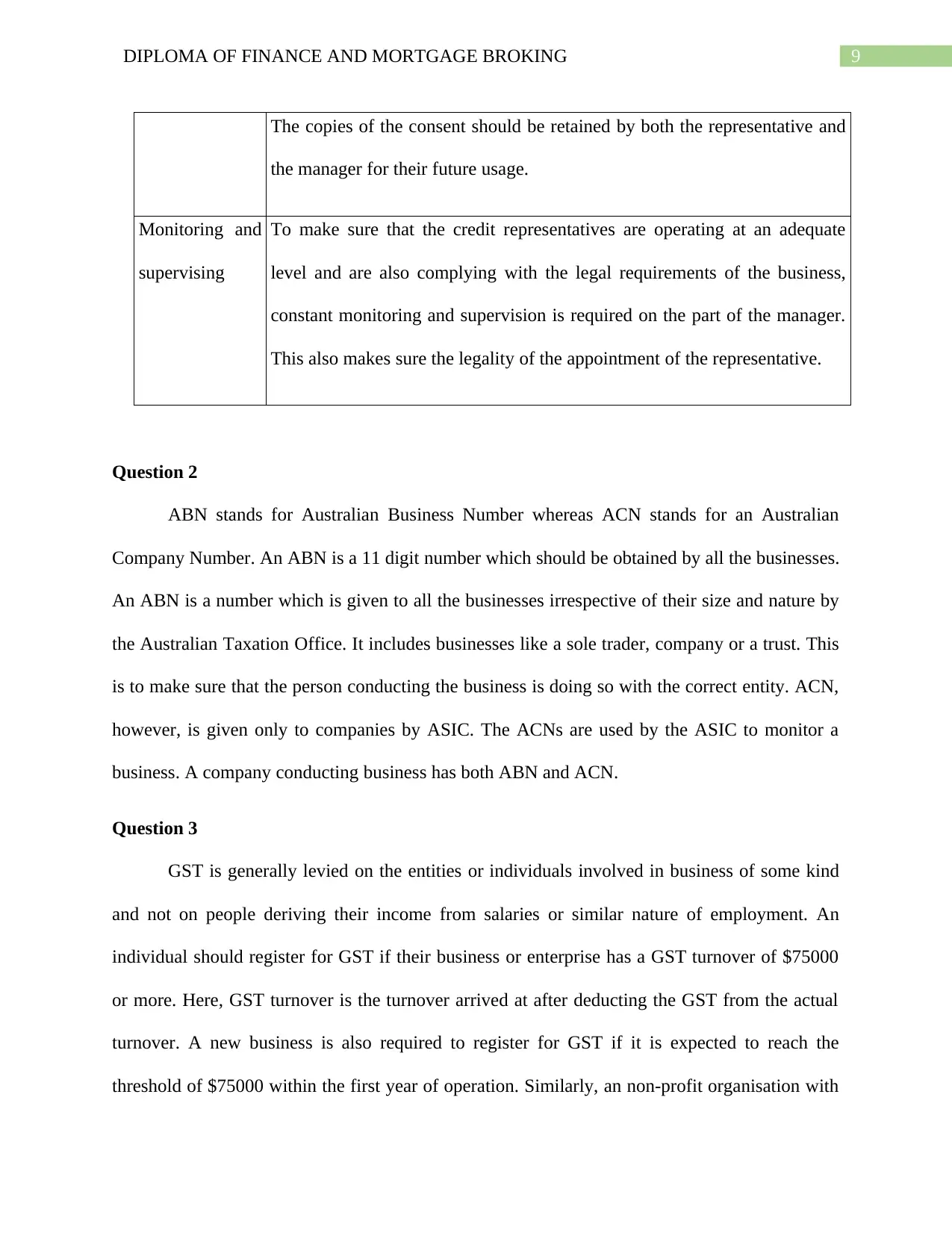

PROCESS IMPLICATION

Background

checks

This is to ensure that the representative undertakes only those activities

covered by their license and do not have any criminal record. This also

makes sure that they do not hire any people banned or disqualified from

being appointed as a representative. It ensures the legitimacy of the

appointment.

Training

requirements

This is to make sure that the credit representatives remain adequately trained

to act and perform their role competently. As the industry maintains certain

standards, the representatives are expected to carry out the operations at a

level accepted by the industry. This is also mandatory under the Regulatory

Guide 206.

Membership to

an EDR scheme

In order to ensure that the authorisation has an immediate effect, it is

necessary that the representative has a membership to an EDR scheme.

Otherwise, the authorisation will not have any effect on the appointment of

the representative.

Written consent To maintain adequate records and to serve as a proof for the appointment of

the representative, the licensee or the manager should give a written consent.

determined.

Task 4

Question 1

PROCESS IMPLICATION

Background

checks

This is to ensure that the representative undertakes only those activities

covered by their license and do not have any criminal record. This also

makes sure that they do not hire any people banned or disqualified from

being appointed as a representative. It ensures the legitimacy of the

appointment.

Training

requirements

This is to make sure that the credit representatives remain adequately trained

to act and perform their role competently. As the industry maintains certain

standards, the representatives are expected to carry out the operations at a

level accepted by the industry. This is also mandatory under the Regulatory

Guide 206.

Membership to

an EDR scheme

In order to ensure that the authorisation has an immediate effect, it is

necessary that the representative has a membership to an EDR scheme.

Otherwise, the authorisation will not have any effect on the appointment of

the representative.

Written consent To maintain adequate records and to serve as a proof for the appointment of

the representative, the licensee or the manager should give a written consent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9DIPLOMA OF FINANCE AND MORTGAGE BROKING

The copies of the consent should be retained by both the representative and

the manager for their future usage.

Monitoring and

supervising

To make sure that the credit representatives are operating at an adequate

level and are also complying with the legal requirements of the business,

constant monitoring and supervision is required on the part of the manager.

This also makes sure the legality of the appointment of the representative.

Question 2

ABN stands for Australian Business Number whereas ACN stands for an Australian

Company Number. An ABN is a 11 digit number which should be obtained by all the businesses.

An ABN is a number which is given to all the businesses irrespective of their size and nature by

the Australian Taxation Office. It includes businesses like a sole trader, company or a trust. This

is to make sure that the person conducting the business is doing so with the correct entity. ACN,

however, is given only to companies by ASIC. The ACNs are used by the ASIC to monitor a

business. A company conducting business has both ABN and ACN.

Question 3

GST is generally levied on the entities or individuals involved in business of some kind

and not on people deriving their income from salaries or similar nature of employment. An

individual should register for GST if their business or enterprise has a GST turnover of $75000

or more. Here, GST turnover is the turnover arrived at after deducting the GST from the actual

turnover. A new business is also required to register for GST if it is expected to reach the

threshold of $75000 within the first year of operation. Similarly, an non-profit organisation with

The copies of the consent should be retained by both the representative and

the manager for their future usage.

Monitoring and

supervising

To make sure that the credit representatives are operating at an adequate

level and are also complying with the legal requirements of the business,

constant monitoring and supervision is required on the part of the manager.

This also makes sure the legality of the appointment of the representative.

Question 2

ABN stands for Australian Business Number whereas ACN stands for an Australian

Company Number. An ABN is a 11 digit number which should be obtained by all the businesses.

An ABN is a number which is given to all the businesses irrespective of their size and nature by

the Australian Taxation Office. It includes businesses like a sole trader, company or a trust. This

is to make sure that the person conducting the business is doing so with the correct entity. ACN,

however, is given only to companies by ASIC. The ACNs are used by the ASIC to monitor a

business. A company conducting business has both ABN and ACN.

Question 3

GST is generally levied on the entities or individuals involved in business of some kind

and not on people deriving their income from salaries or similar nature of employment. An

individual should register for GST if their business or enterprise has a GST turnover of $75000

or more. Here, GST turnover is the turnover arrived at after deducting the GST from the actual

turnover. A new business is also required to register for GST if it is expected to reach the

threshold of $75000 within the first year of operation. Similarly, an non-profit organisation with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10DIPLOMA OF FINANCE AND MORTGAGE BROKING

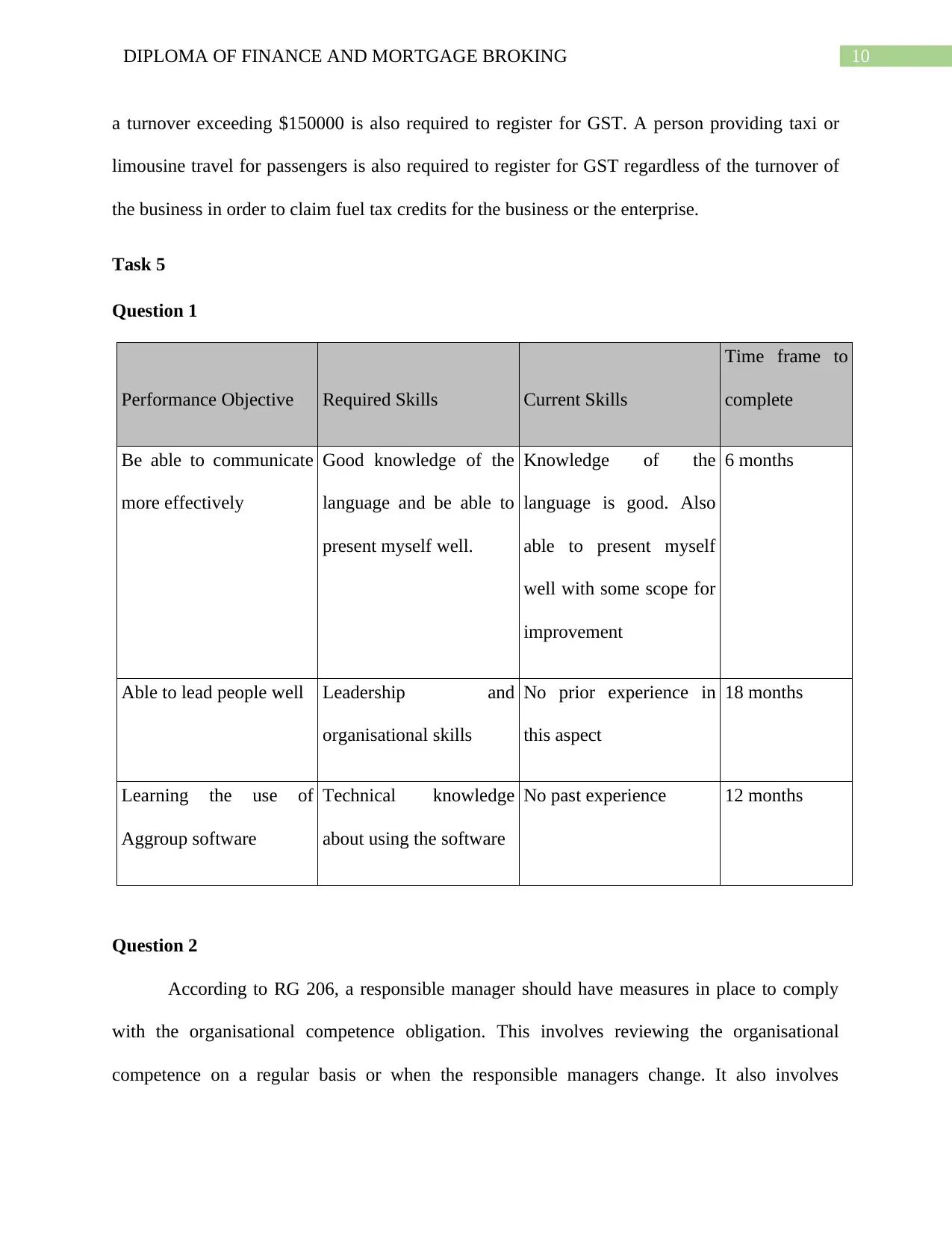

a turnover exceeding $150000 is also required to register for GST. A person providing taxi or

limousine travel for passengers is also required to register for GST regardless of the turnover of

the business in order to claim fuel tax credits for the business or the enterprise.

Task 5

Question 1

Performance Objective Required Skills Current Skills

Time frame to

complete

Be able to communicate

more effectively

Good knowledge of the

language and be able to

present myself well.

Knowledge of the

language is good. Also

able to present myself

well with some scope for

improvement

6 months

Able to lead people well Leadership and

organisational skills

No prior experience in

this aspect

18 months

Learning the use of

Aggroup software

Technical knowledge

about using the software

No past experience 12 months

Question 2

According to RG 206, a responsible manager should have measures in place to comply

with the organisational competence obligation. This involves reviewing the organisational

competence on a regular basis or when the responsible managers change. It also involves

a turnover exceeding $150000 is also required to register for GST. A person providing taxi or

limousine travel for passengers is also required to register for GST regardless of the turnover of

the business in order to claim fuel tax credits for the business or the enterprise.

Task 5

Question 1

Performance Objective Required Skills Current Skills

Time frame to

complete

Be able to communicate

more effectively

Good knowledge of the

language and be able to

present myself well.

Knowledge of the

language is good. Also

able to present myself

well with some scope for

improvement

6 months

Able to lead people well Leadership and

organisational skills

No prior experience in

this aspect

18 months

Learning the use of

Aggroup software

Technical knowledge

about using the software

No past experience 12 months

Question 2

According to RG 206, a responsible manager should have measures in place to comply

with the organisational competence obligation. This involves reviewing the organisational

competence on a regular basis or when the responsible managers change. It also involves

11DIPLOMA OF FINANCE AND MORTGAGE BROKING

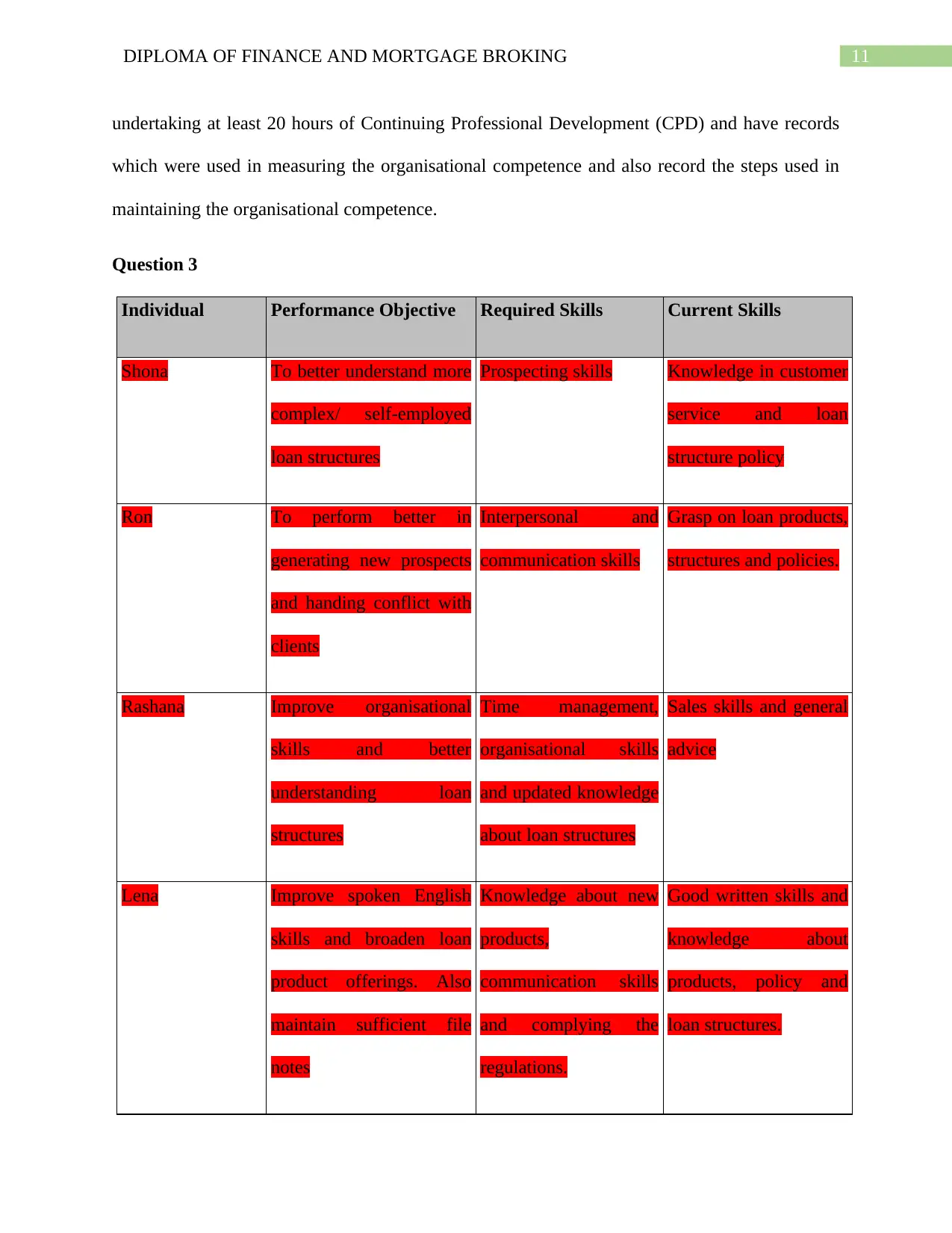

undertaking at least 20 hours of Continuing Professional Development (CPD) and have records

which were used in measuring the organisational competence and also record the steps used in

maintaining the organisational competence.

Question 3

Individual Performance Objective Required Skills Current Skills

Shona To better understand more

complex/ self-employed

loan structures

Prospecting skills Knowledge in customer

service and loan

structure policy

Ron To perform better in

generating new prospects

and handing conflict with

clients

Interpersonal and

communication skills

Grasp on loan products,

structures and policies.

Rashana Improve organisational

skills and better

understanding loan

structures

Time management,

organisational skills

and updated knowledge

about loan structures

Sales skills and general

advice

Lena Improve spoken English

skills and broaden loan

product offerings. Also

maintain sufficient file

notes

Knowledge about new

products,

communication skills

and complying the

regulations.

Good written skills and

knowledge about

products, policy and

loan structures.

undertaking at least 20 hours of Continuing Professional Development (CPD) and have records

which were used in measuring the organisational competence and also record the steps used in

maintaining the organisational competence.

Question 3

Individual Performance Objective Required Skills Current Skills

Shona To better understand more

complex/ self-employed

loan structures

Prospecting skills Knowledge in customer

service and loan

structure policy

Ron To perform better in

generating new prospects

and handing conflict with

clients

Interpersonal and

communication skills

Grasp on loan products,

structures and policies.

Rashana Improve organisational

skills and better

understanding loan

structures

Time management,

organisational skills

and updated knowledge

about loan structures

Sales skills and general

advice

Lena Improve spoken English

skills and broaden loan

product offerings. Also

maintain sufficient file

notes

Knowledge about new

products,

communication skills

and complying the

regulations.

Good written skills and

knowledge about

products, policy and

loan structures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.