Financial Statement Analysis and Ratio Calculations - Accounting

VerifiedAdded on 2023/04/23

|10

|1309

|412

Homework Assignment

AI Summary

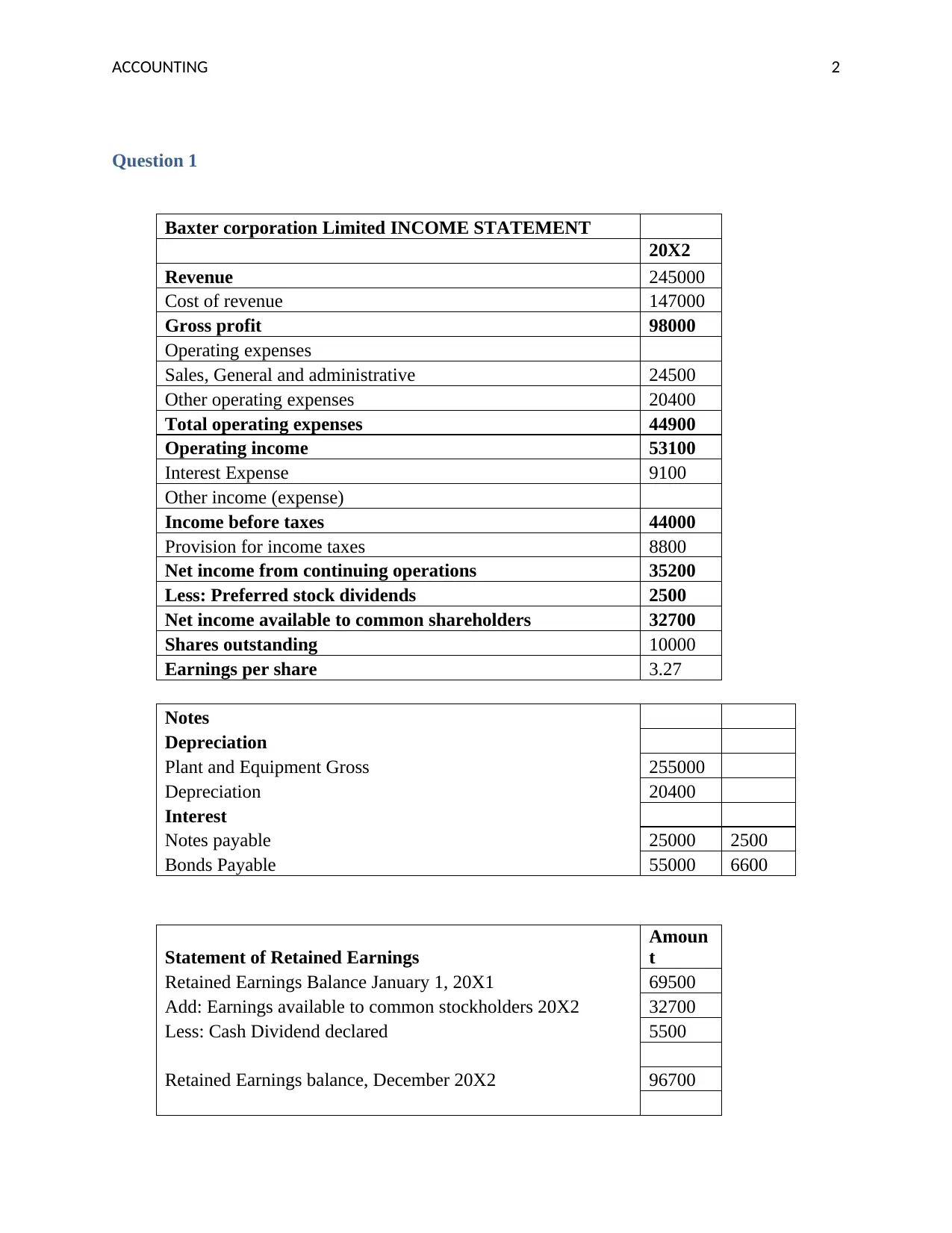

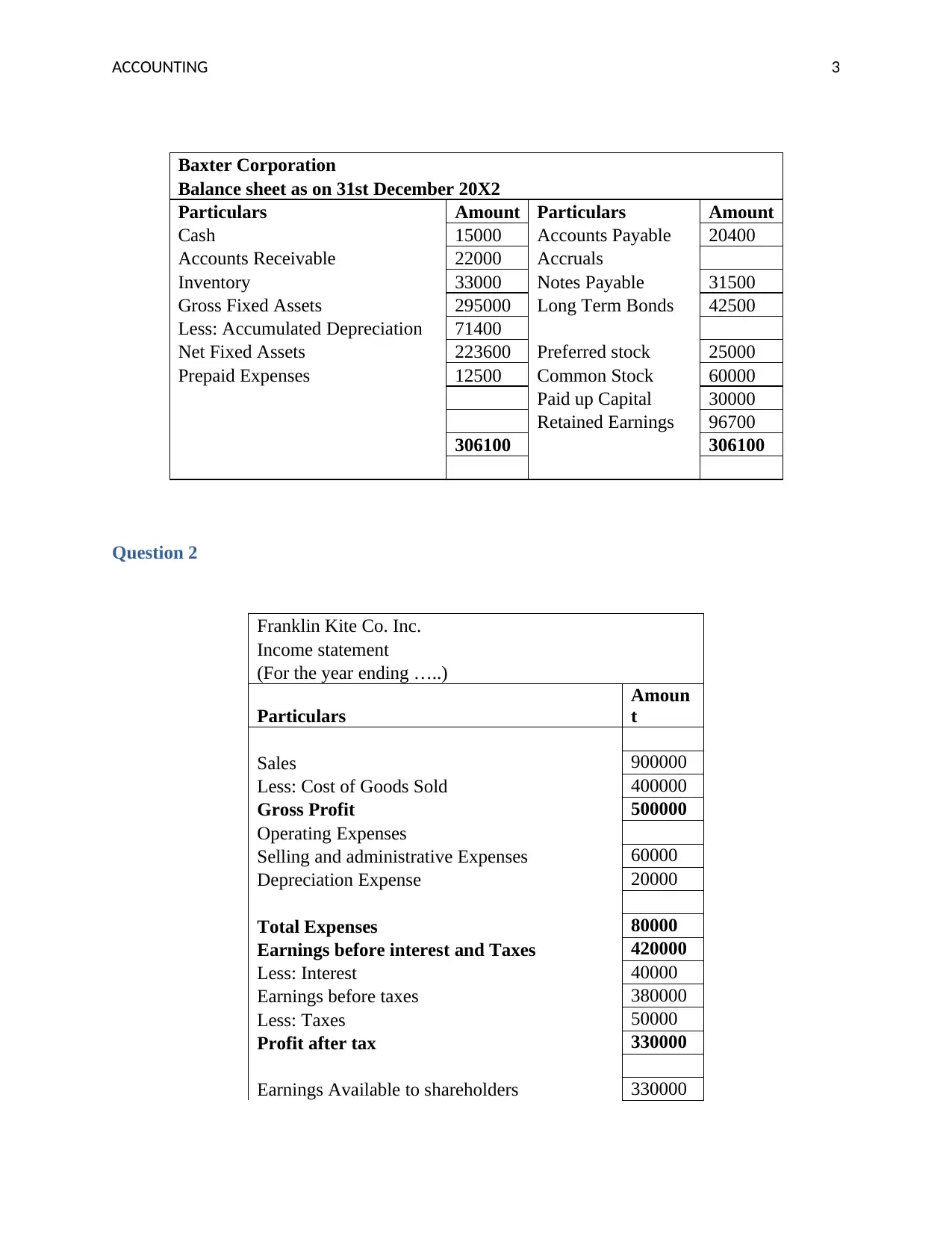

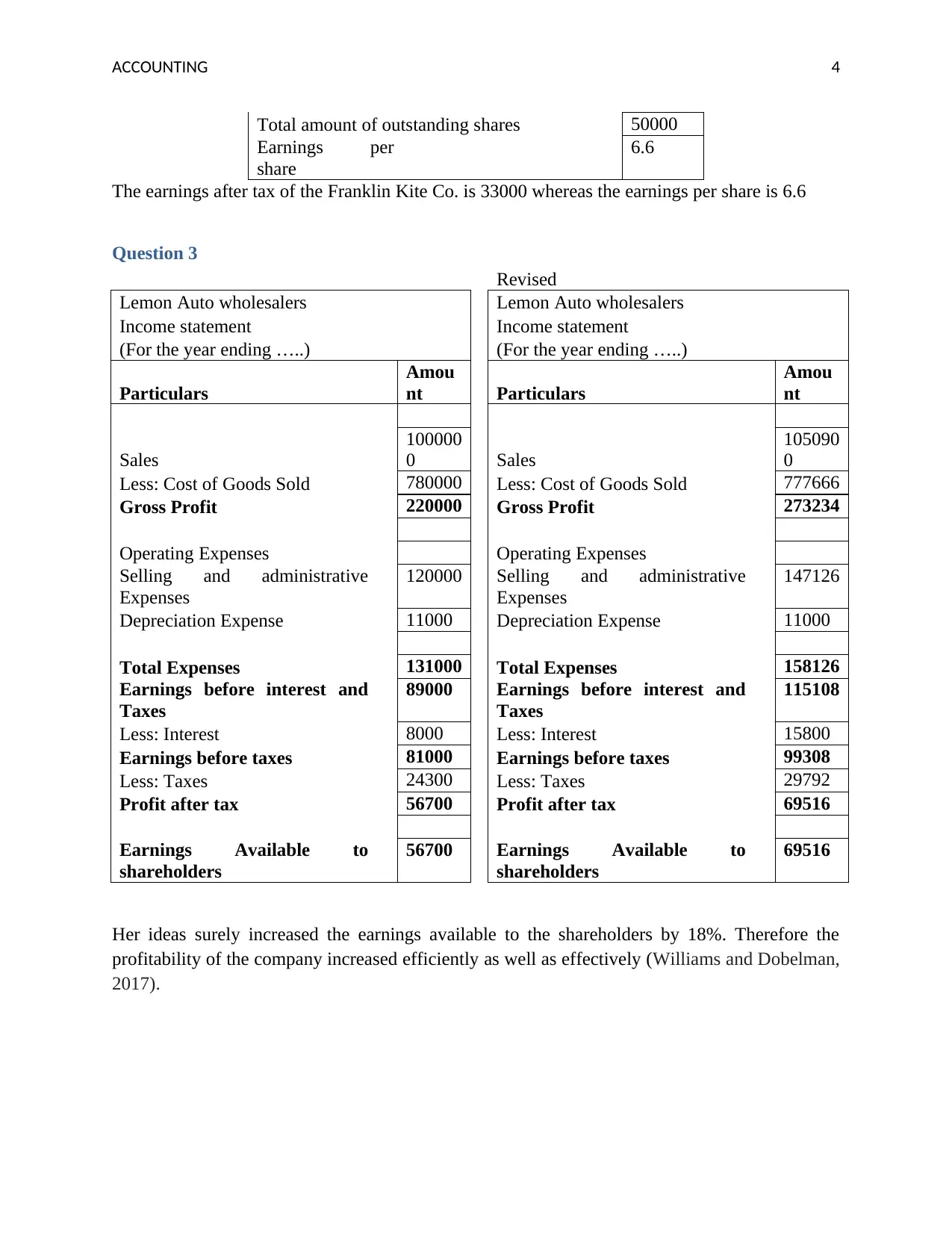

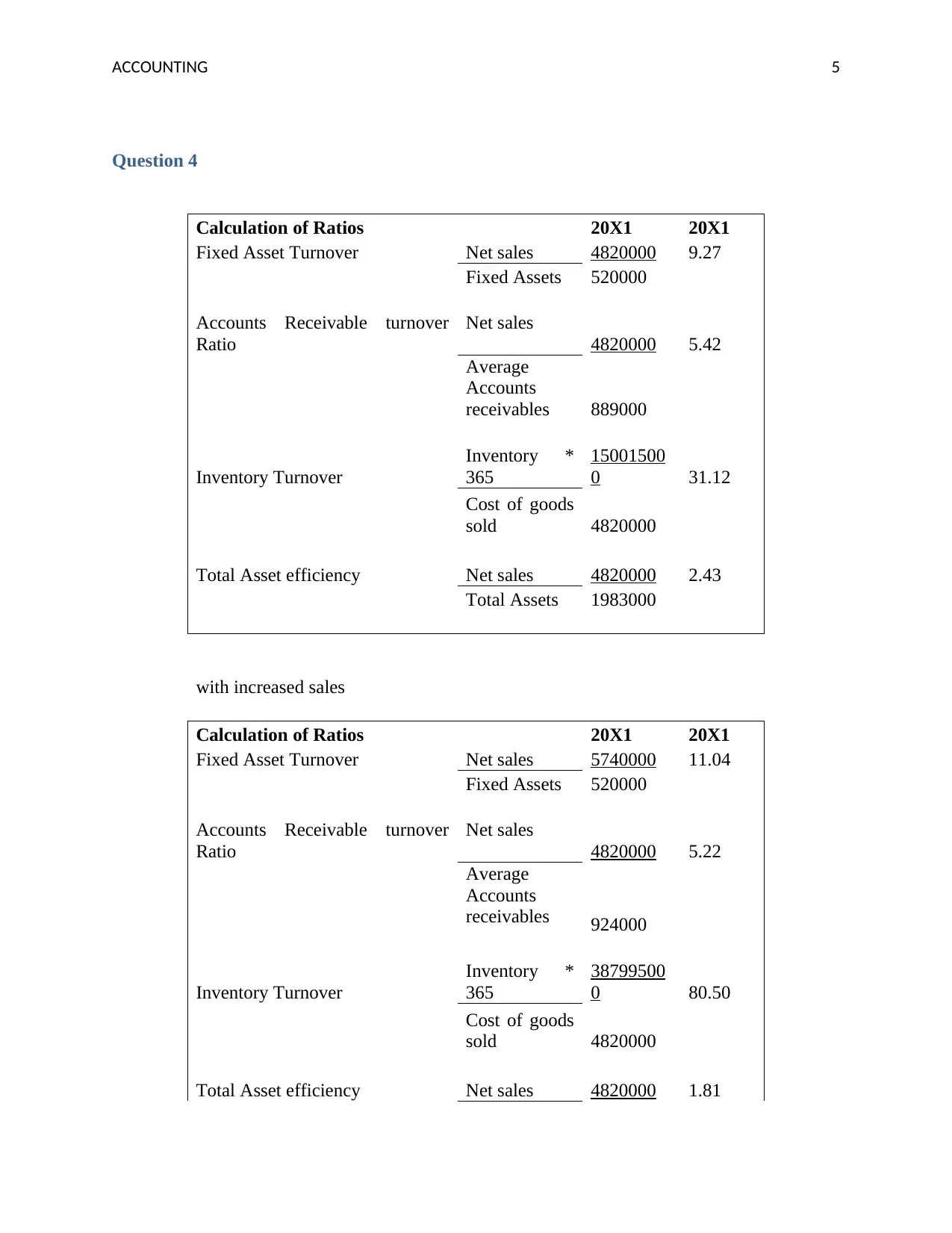

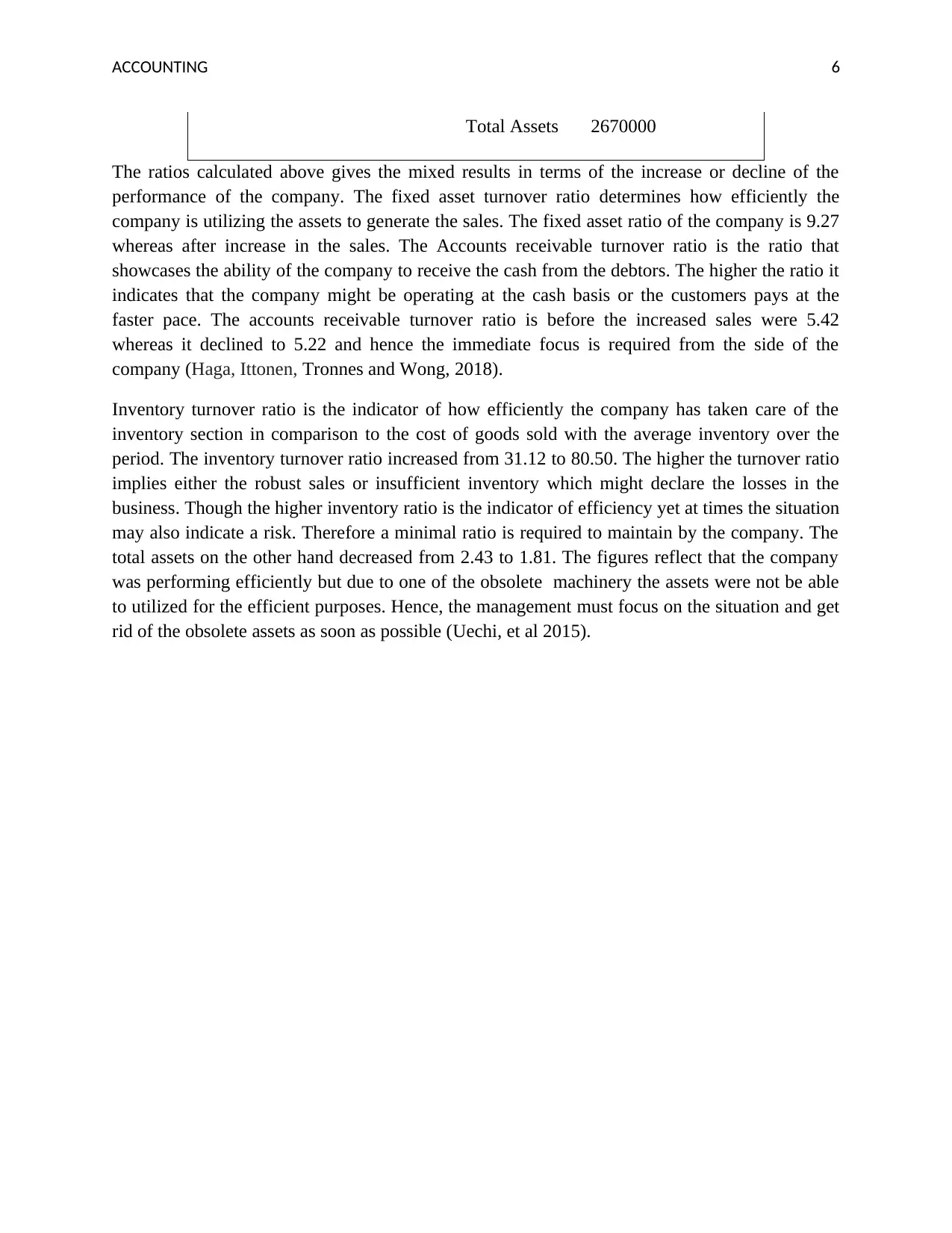

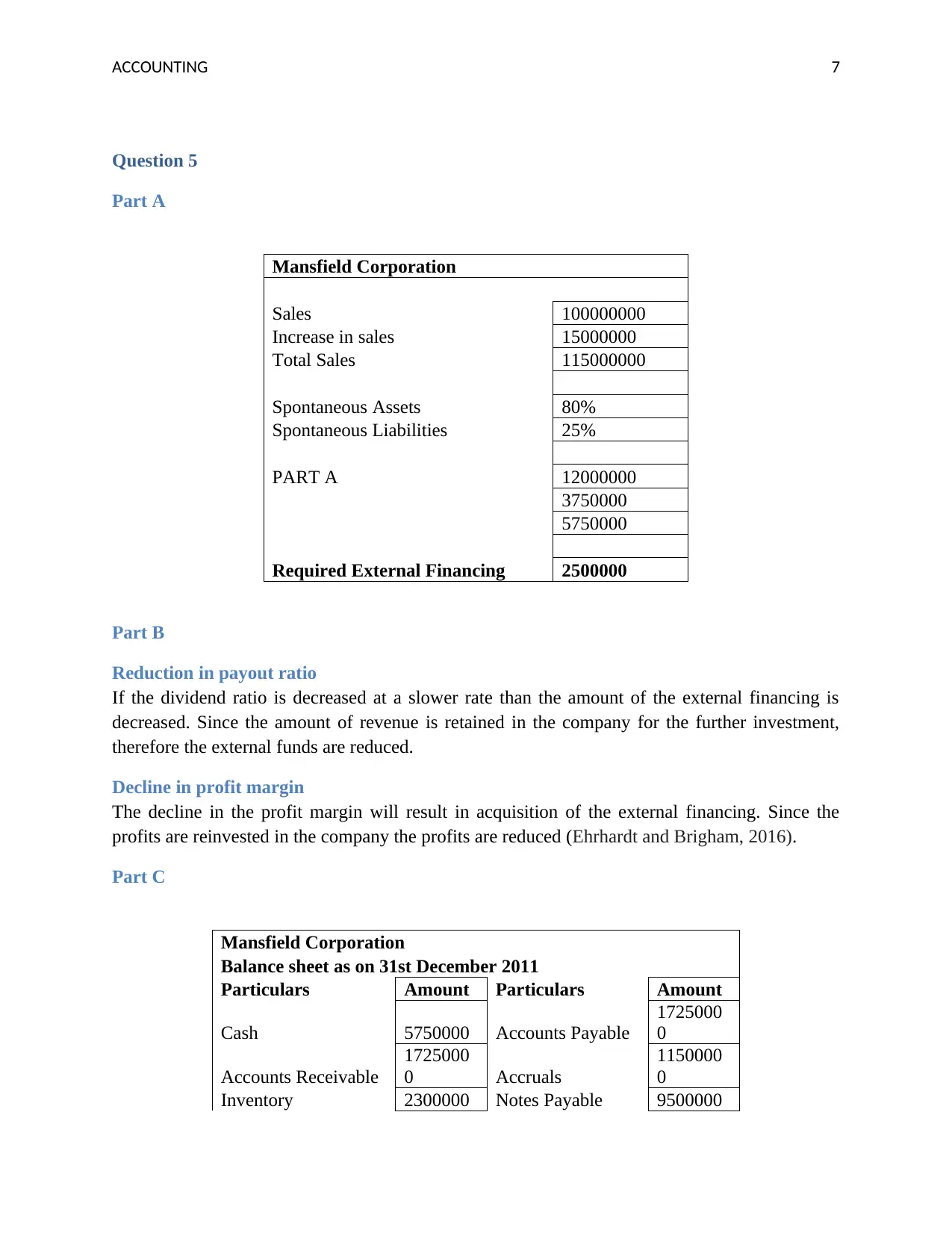

This accounting assignment provides comprehensive solutions to various financial analysis problems. It begins with the analysis of Baxter Corporation's financial statements, including the income statement, statement of retained earnings, and balance sheet for the year 20X2. The assignment then delves into the income statement and earnings per share calculations for Franklin Kite Co. Inc. The next section analyzes Lemon Auto wholesalers' income statements, comparing the results before and after implementing suggested changes. The core of the assignment involves the calculation and interpretation of key financial ratios, such as fixed asset turnover, accounts receivable turnover, inventory turnover, and total asset efficiency, for two different years. Further, the assignment explores the impact of changes in sales, spontaneous assets, and liabilities on external financing needs using the example of Mansfield Corporation. Finally, the assignment addresses the external financing requirements based on changes in sales and profit margin. The provided solution thoroughly addresses all the questions, demonstrating a strong understanding of accounting principles and financial statement analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.