Business Planning: Financial Statement Analysis and Performance

VerifiedAdded on 2023/06/12

|16

|3107

|171

Report

AI Summary

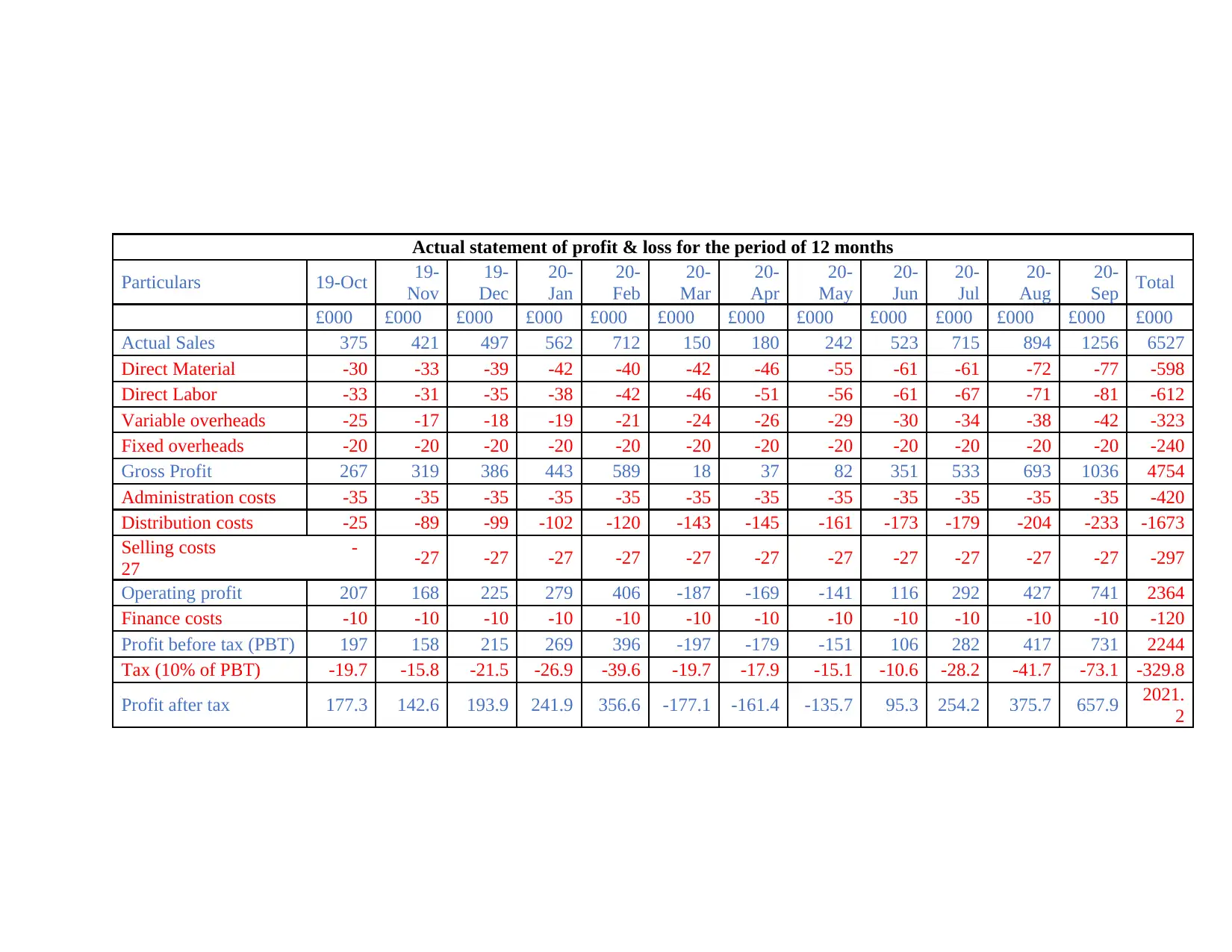

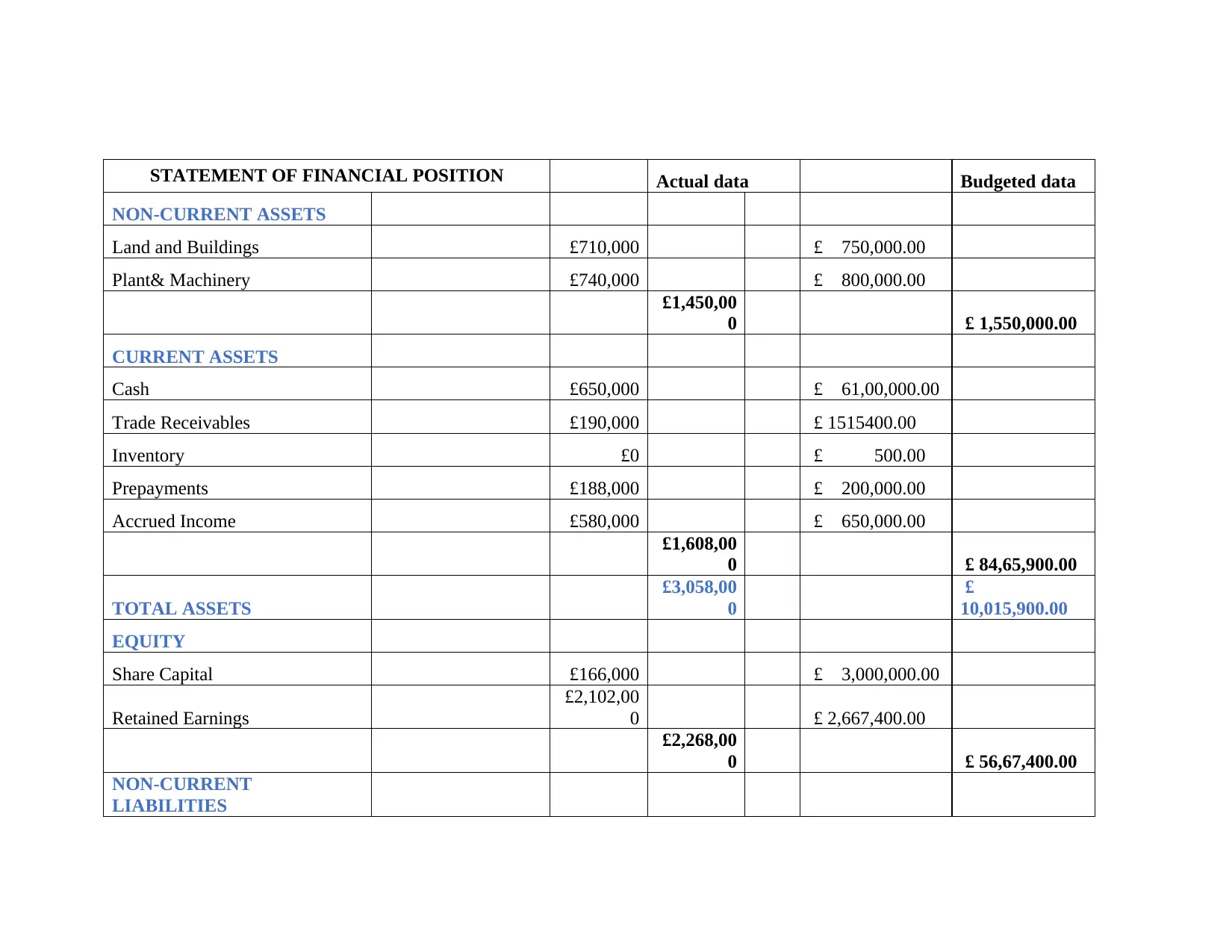

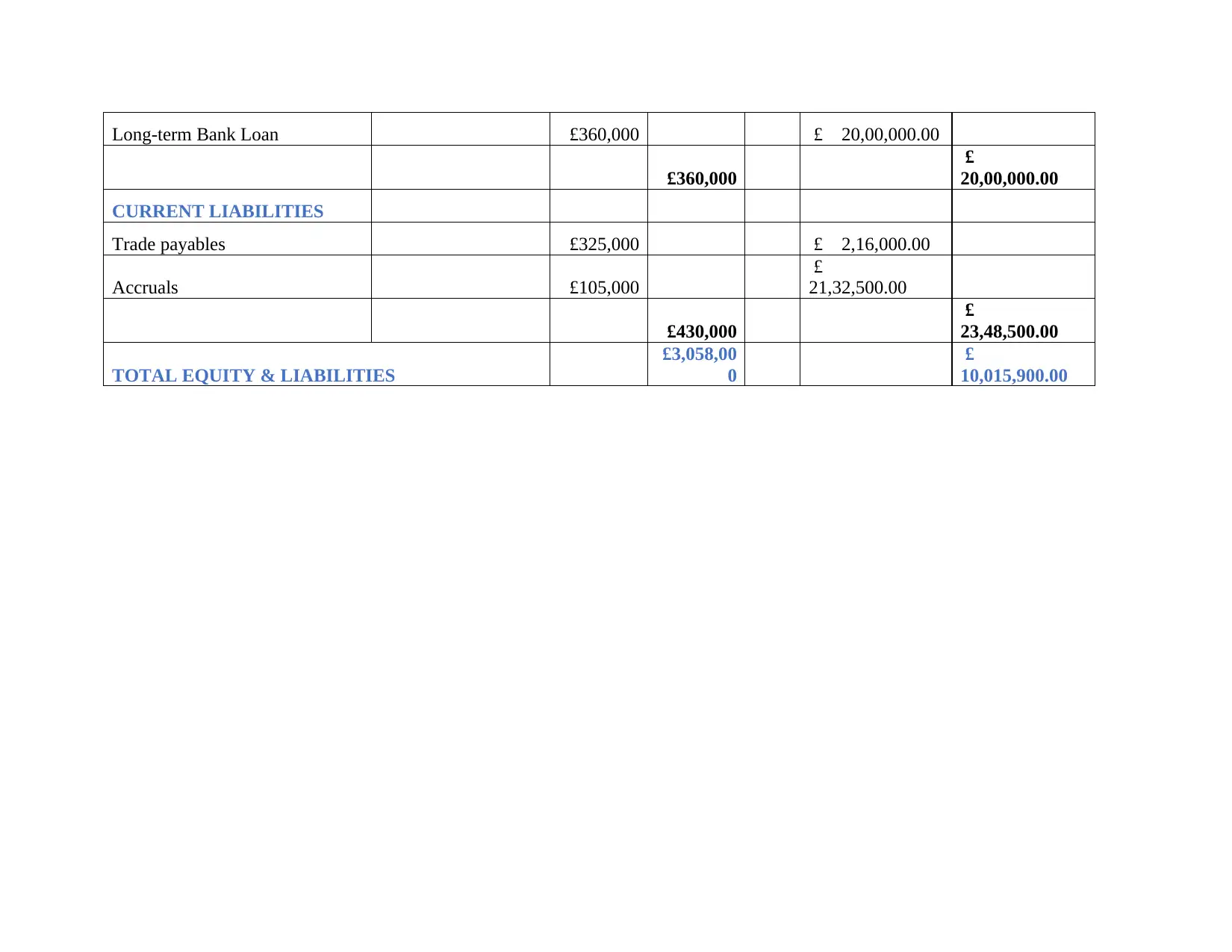

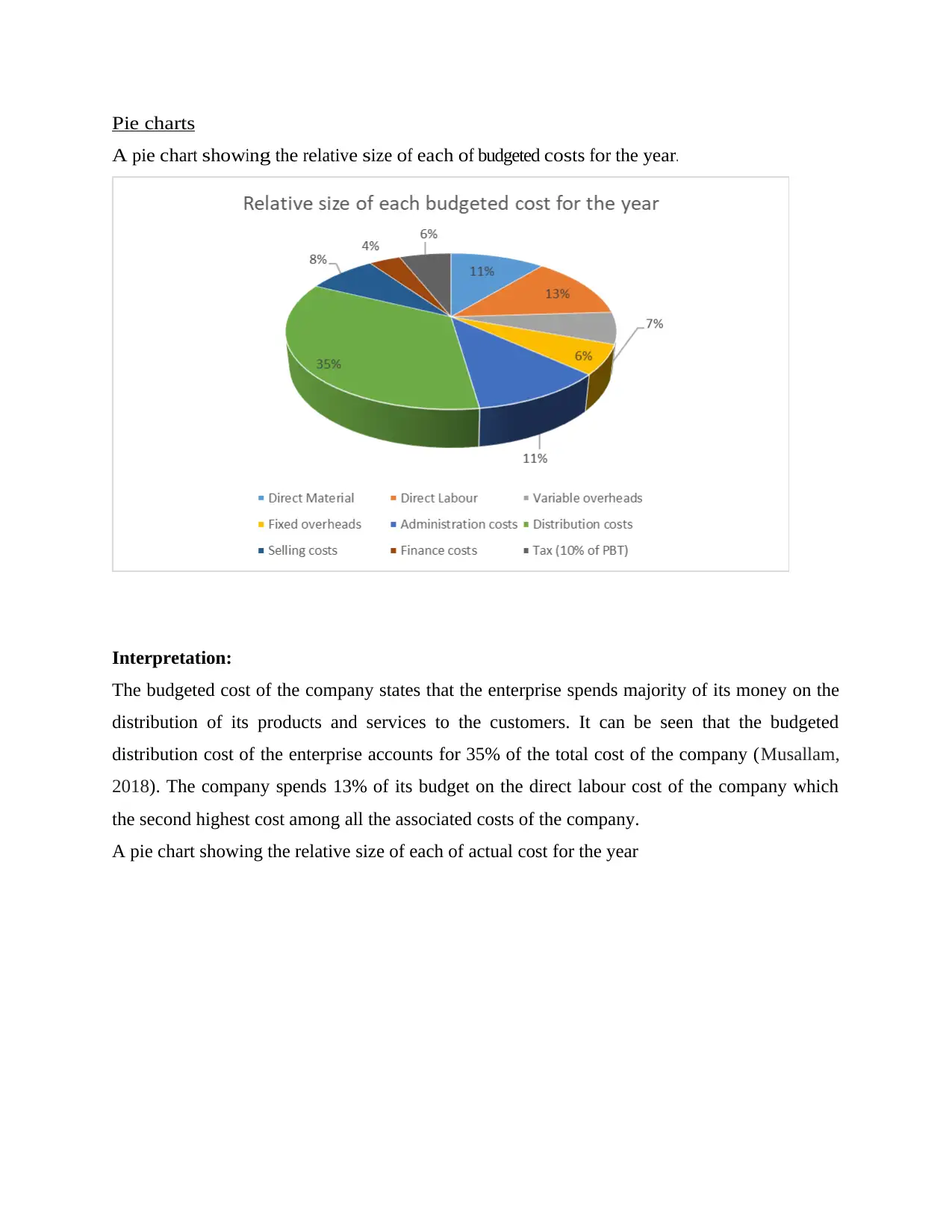

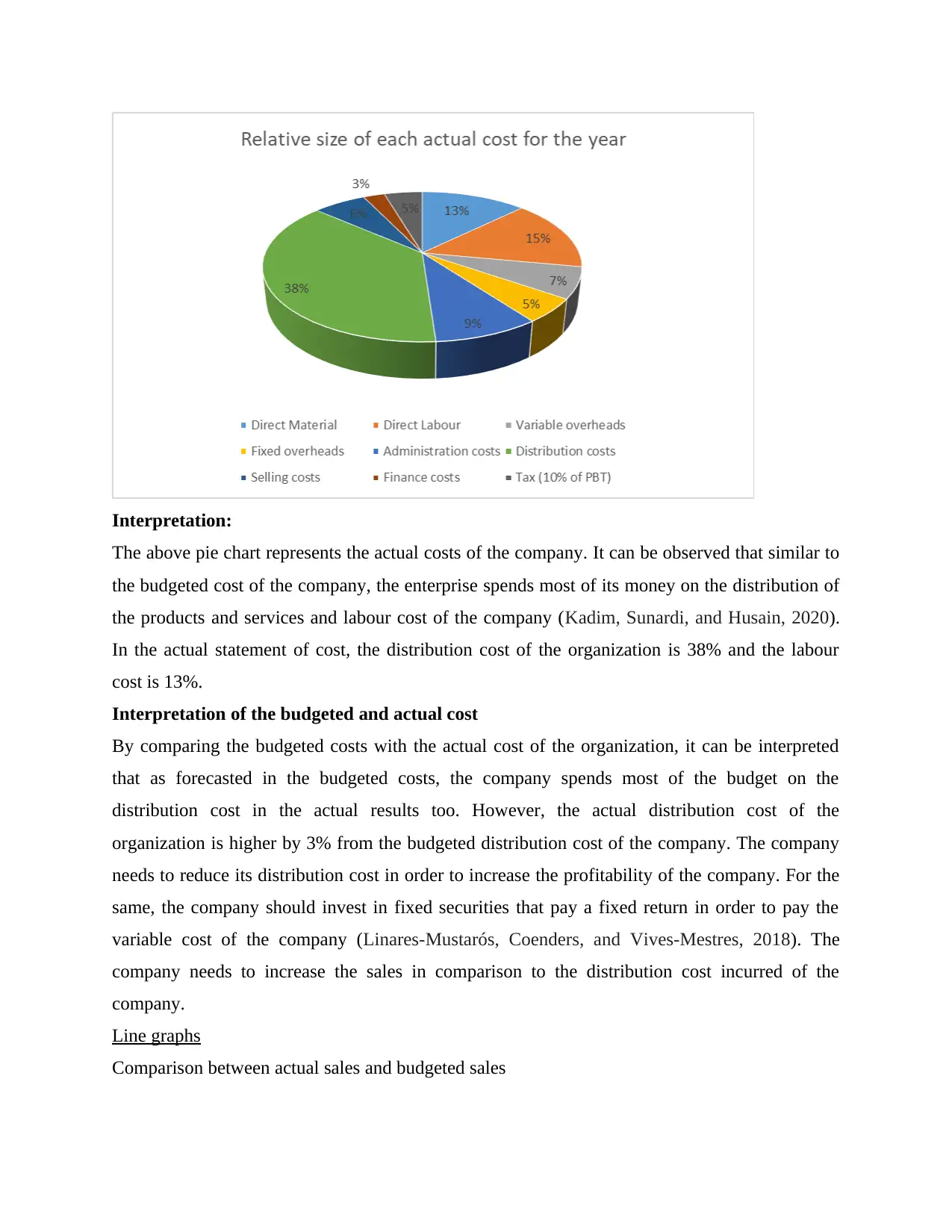

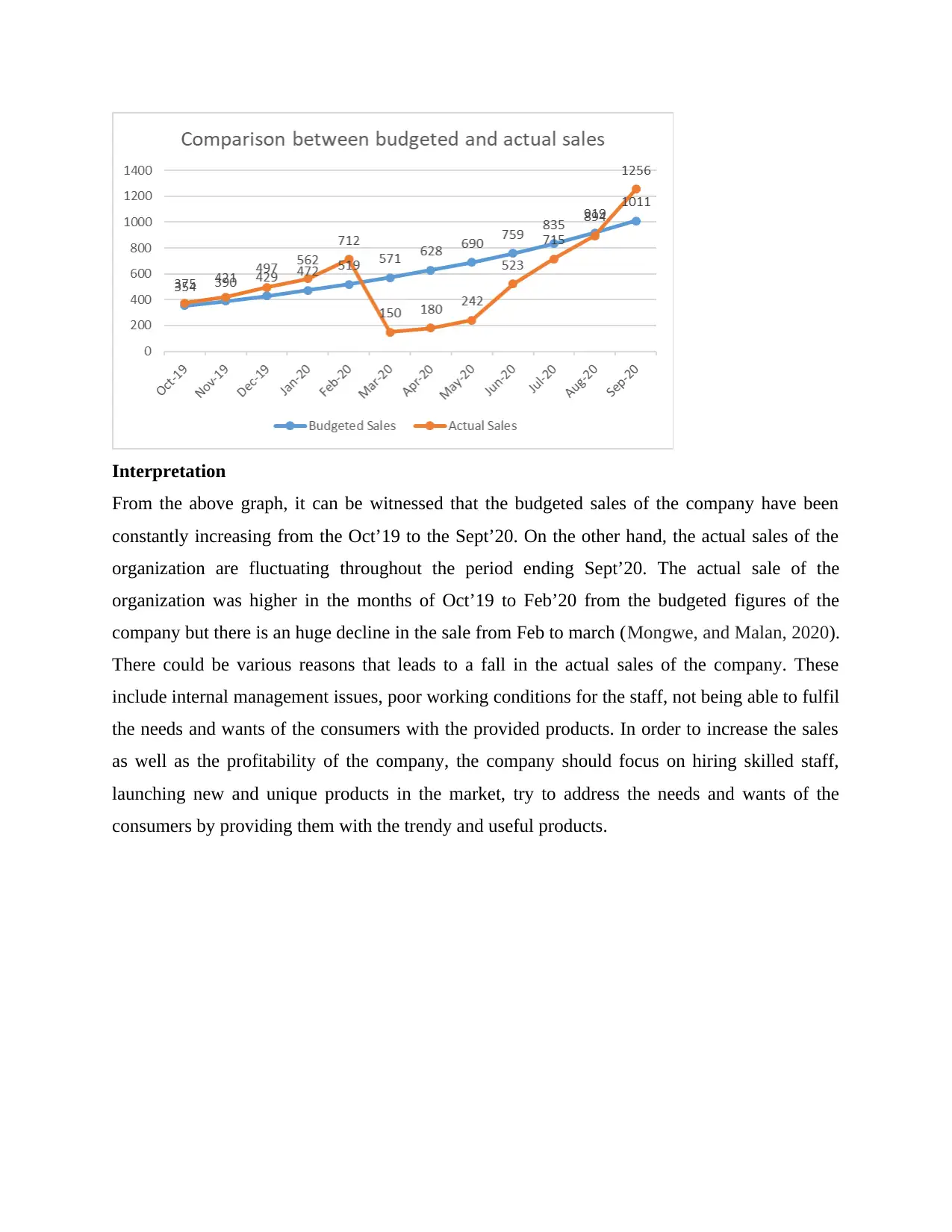

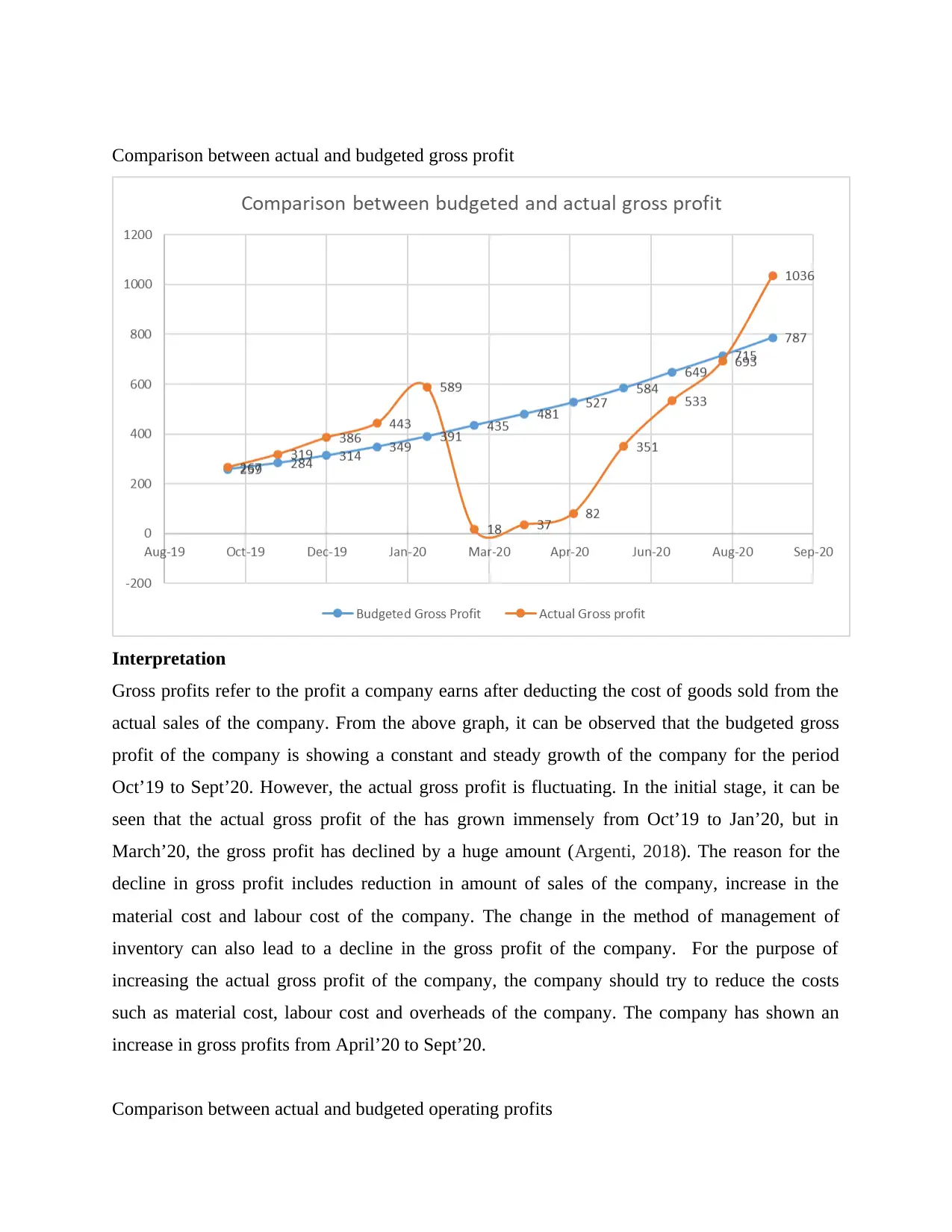

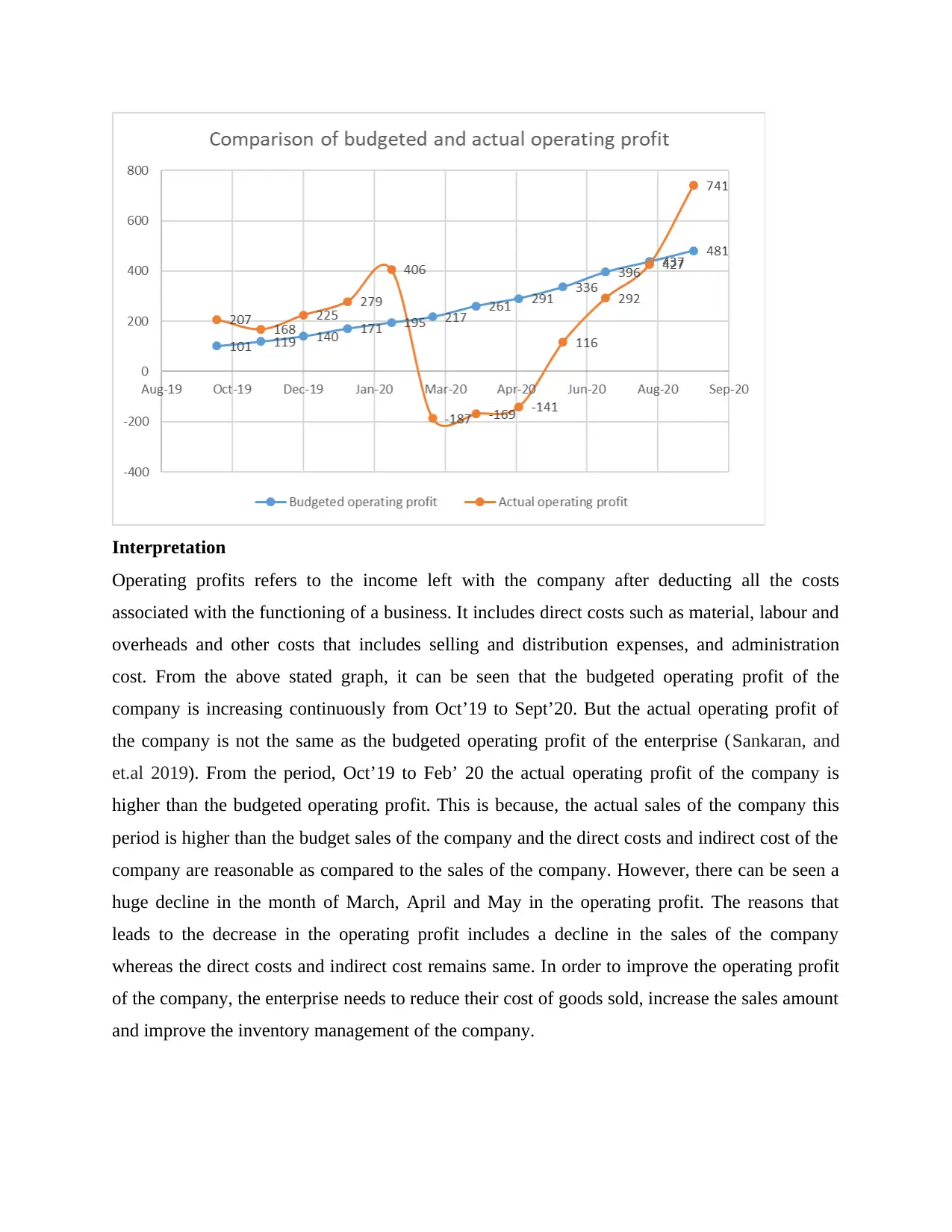

This report provides a comprehensive analysis of a company's business planning and financial performance. It includes a comparison of budgeted and actual financial statements, specifically the statement of profit and loss and the balance sheet, for the period of Oct’19 to Sept’20. The analysis identifies variances between budgeted and actual figures, highlighting areas of strong performance and areas needing improvement. Pie charts and line graphs are used to visually represent the data, comparing sales, gross profit, and operating profit. The report also calculates and interprets key liquidity and profitability ratios to assess the company's financial health. Key findings indicate that the company spends a significant portion of its budget on distribution costs, and sales fluctuated significantly during the year, particularly in March, April, and May. Recommendations include reducing distribution costs, improving sales strategies, and enhancing inventory management to increase profitability and overall financial stability. Desklib offers a variety of resources and tools to help students further understand business planning and financial analysis.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.