Financial Accounting Report: Statement Analysis and Project Evaluation

VerifiedAdded on 2023/06/18

|15

|2355

|61

Report

AI Summary

This report provides a comprehensive financial analysis, starting with the preparation of a statement of profit and loss and a statement of financial position for Peter Baker as of September 2019. It includes calculations of depreciation using both the straight-line and sum-of-digits methods, along with arguments for and against each method. Furthermore, the report computes and interprets key financial ratios such as the current ratio, debt-equity ratio, return on equity, and gross profit ratio for the years 2018 and 2019. It also identifies two users of financial statements. Finally, the report assesses two projects using the payback period and net present value methods, advising the director based on the findings and discussing the advantages and limitations of each method.

Accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Q1. ...................................................................................................................................................3

a) Statement of profit & loss for the year ended September 2019...............................................3

b) Statement of financial position for the year 2019....................................................................3

Q2. ...................................................................................................................................................4

a) Calculation of depreciation using Straight line method...........................................................4

b) Computation of depreciation using Sum of digit method........................................................5

c) Arguments made for and against two methods........................................................................5

Q3.....................................................................................................................................................7

a) Computation of current ratio with its measure and interpretation for 2018 & 2019 year.......7

b) Calculation of debt equity ratio with measure and interpretation for the period 2018 & 2019

......................................................................................................................................................7

c) Determination of return on equity with its measures and interpretation.................................8

d) Calculation of gross profit ratio by considering its measures and interpretation for period

2018 & 2019................................................................................................................................8

e) Two users of financial statement.............................................................................................9

Q4. ...................................................................................................................................................9

a) Access of following projects using two methods:...................................................................9

b) Pay back period method..........................................................................................................9

c) Net present value method......................................................................................................10

b) Advise to the director............................................................................................................11

c) Advantages and limitations of two methods.........................................................................11

REFERENCES..............................................................................................................................13

Q1. ...................................................................................................................................................3

a) Statement of profit & loss for the year ended September 2019...............................................3

b) Statement of financial position for the year 2019....................................................................3

Q2. ...................................................................................................................................................4

a) Calculation of depreciation using Straight line method...........................................................4

b) Computation of depreciation using Sum of digit method........................................................5

c) Arguments made for and against two methods........................................................................5

Q3.....................................................................................................................................................7

a) Computation of current ratio with its measure and interpretation for 2018 & 2019 year.......7

b) Calculation of debt equity ratio with measure and interpretation for the period 2018 & 2019

......................................................................................................................................................7

c) Determination of return on equity with its measures and interpretation.................................8

d) Calculation of gross profit ratio by considering its measures and interpretation for period

2018 & 2019................................................................................................................................8

e) Two users of financial statement.............................................................................................9

Q4. ...................................................................................................................................................9

a) Access of following projects using two methods:...................................................................9

b) Pay back period method..........................................................................................................9

c) Net present value method......................................................................................................10

b) Advise to the director............................................................................................................11

c) Advantages and limitations of two methods.........................................................................11

REFERENCES..............................................................................................................................13

Q1.

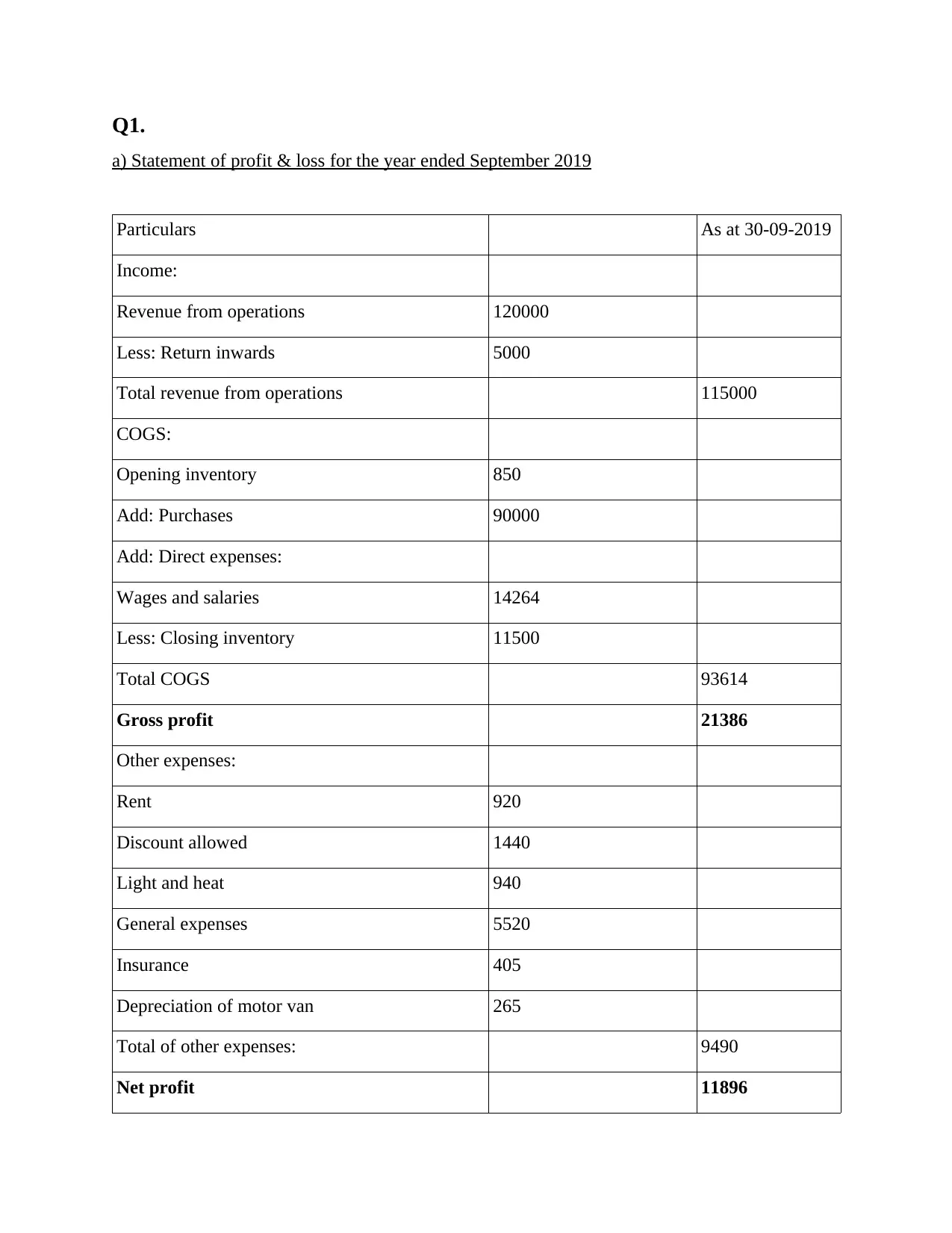

a) Statement of profit & loss for the year ended September 2019

Particulars As at 30-09-2019

Income:

Revenue from operations 120000

Less: Return inwards 5000

Total revenue from operations 115000

COGS:

Opening inventory 850

Add: Purchases 90000

Add: Direct expenses:

Wages and salaries 14264

Less: Closing inventory 11500

Total COGS 93614

Gross profit 21386

Other expenses:

Rent 920

Discount allowed 1440

Light and heat 940

General expenses 5520

Insurance 405

Depreciation of motor van 265

Total of other expenses: 9490

Net profit 11896

a) Statement of profit & loss for the year ended September 2019

Particulars As at 30-09-2019

Income:

Revenue from operations 120000

Less: Return inwards 5000

Total revenue from operations 115000

COGS:

Opening inventory 850

Add: Purchases 90000

Add: Direct expenses:

Wages and salaries 14264

Less: Closing inventory 11500

Total COGS 93614

Gross profit 21386

Other expenses:

Rent 920

Discount allowed 1440

Light and heat 940

General expenses 5520

Insurance 405

Depreciation of motor van 265

Total of other expenses: 9490

Net profit 11896

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

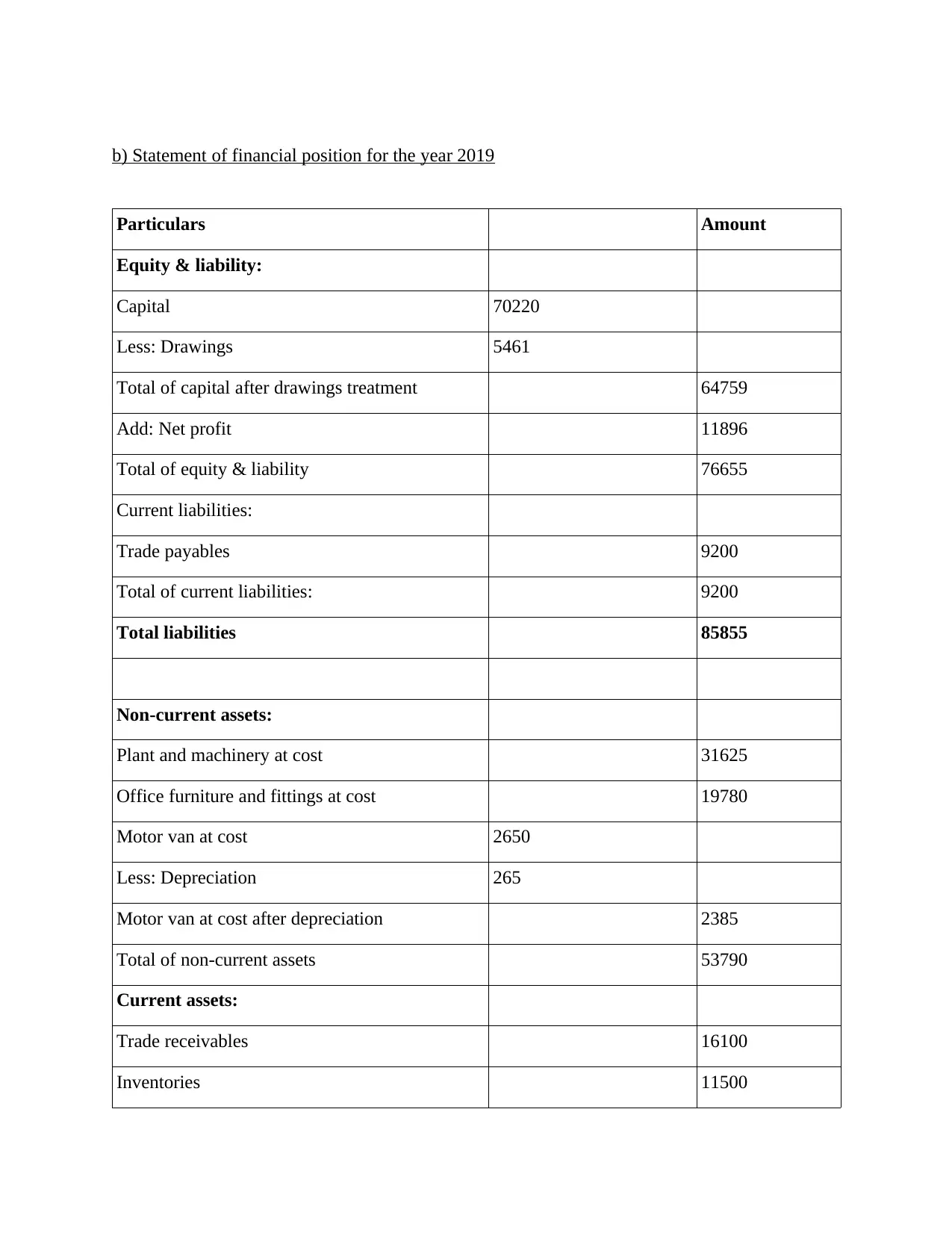

b) Statement of financial position for the year 2019

Particulars Amount

Equity & liability:

Capital 70220

Less: Drawings 5461

Total of capital after drawings treatment 64759

Add: Net profit 11896

Total of equity & liability 76655

Current liabilities:

Trade payables 9200

Total of current liabilities: 9200

Total liabilities 85855

Non-current assets:

Plant and machinery at cost 31625

Office furniture and fittings at cost 19780

Motor van at cost 2650

Less: Depreciation 265

Motor van at cost after depreciation 2385

Total of non-current assets 53790

Current assets:

Trade receivables 16100

Inventories 11500

Particulars Amount

Equity & liability:

Capital 70220

Less: Drawings 5461

Total of capital after drawings treatment 64759

Add: Net profit 11896

Total of equity & liability 76655

Current liabilities:

Trade payables 9200

Total of current liabilities: 9200

Total liabilities 85855

Non-current assets:

Plant and machinery at cost 31625

Office furniture and fittings at cost 19780

Motor van at cost 2650

Less: Depreciation 265

Motor van at cost after depreciation 2385

Total of non-current assets 53790

Current assets:

Trade receivables 16100

Inventories 11500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

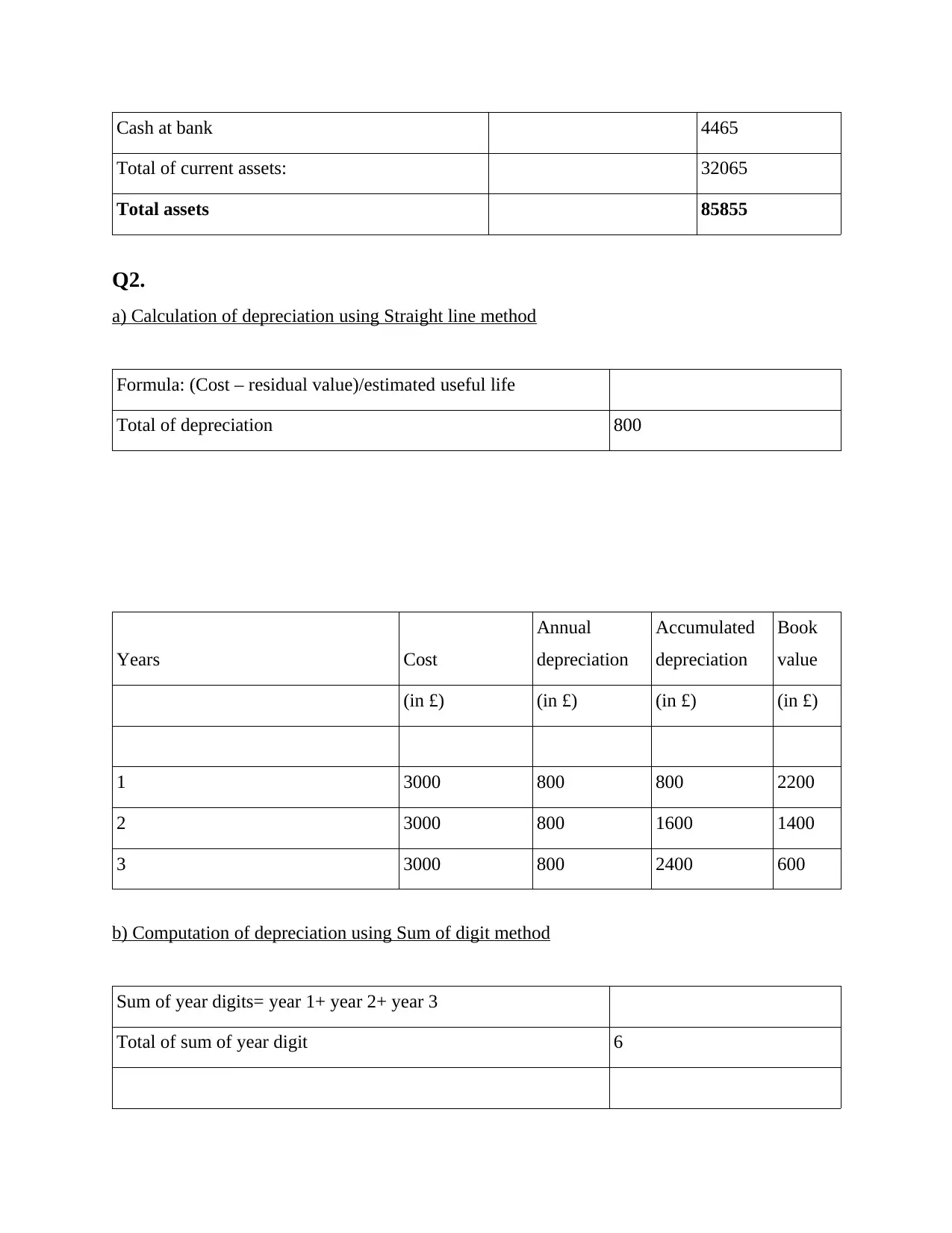

Cash at bank 4465

Total of current assets: 32065

Total assets 85855

Q2.

a) Calculation of depreciation using Straight line method

Formula: (Cost – residual value)/estimated useful life

Total of depreciation 800

Years Cost

Annual

depreciation

Accumulated

depreciation

Book

value

(in £) (in £) (in £) (in £)

1 3000 800 800 2200

2 3000 800 1600 1400

3 3000 800 2400 600

b) Computation of depreciation using Sum of digit method

Sum of year digits= year 1+ year 2+ year 3

Total of sum of year digit 6

Total of current assets: 32065

Total assets 85855

Q2.

a) Calculation of depreciation using Straight line method

Formula: (Cost – residual value)/estimated useful life

Total of depreciation 800

Years Cost

Annual

depreciation

Accumulated

depreciation

Book

value

(in £) (in £) (in £) (in £)

1 3000 800 800 2200

2 3000 800 1600 1400

3 3000 800 2400 600

b) Computation of depreciation using Sum of digit method

Sum of year digits= year 1+ year 2+ year 3

Total of sum of year digit 6

Amount to be depreciated= Cost – residual value

Cost of the catering freezer 3000

Residual value 600

Total of amount to be depreciated 2400

Years

Amount to be

depreciated

Depreciation

factor

Depreciation

expense

(in £)

1 2400 0.50 1200

2 1200 0.33 400

3 800 0.17 133.33

c) Arguments made for and against two methods

Straight line method :

Arguments made for Straight line method of depreciation:

1) Simplicity: SLM is the simplest method for calculating depreciation and any normal

person can understand this method easily.

2) Asset are written off completely: Under straight line method depreciation is charged on

the cost of assets at constant rate over its estimated useful life i.e., charging takes place

till assets value comes to zero (Kumaat., Paendong and Lintong, 2021).

3) Suitable for small business: This method of depreciation is appropriate for small entity

because it is the easiest and simplest way to determine value of net assets for those

structure who has small business size.

Arguments made against Straight line method of depreciation:

1) Considered to be illogical: This way of computing depreciation value seems to be

illogical because charge is applied on original cost of asset irrespective of its declination

every year.

Cost of the catering freezer 3000

Residual value 600

Total of amount to be depreciated 2400

Years

Amount to be

depreciated

Depreciation

factor

Depreciation

expense

(in £)

1 2400 0.50 1200

2 1200 0.33 400

3 800 0.17 133.33

c) Arguments made for and against two methods

Straight line method :

Arguments made for Straight line method of depreciation:

1) Simplicity: SLM is the simplest method for calculating depreciation and any normal

person can understand this method easily.

2) Asset are written off completely: Under straight line method depreciation is charged on

the cost of assets at constant rate over its estimated useful life i.e., charging takes place

till assets value comes to zero (Kumaat., Paendong and Lintong, 2021).

3) Suitable for small business: This method of depreciation is appropriate for small entity

because it is the easiest and simplest way to determine value of net assets for those

structure who has small business size.

Arguments made against Straight line method of depreciation:

1) Considered to be illogical: This way of computing depreciation value seems to be

illogical because charge is applied on original cost of asset irrespective of its declination

every year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

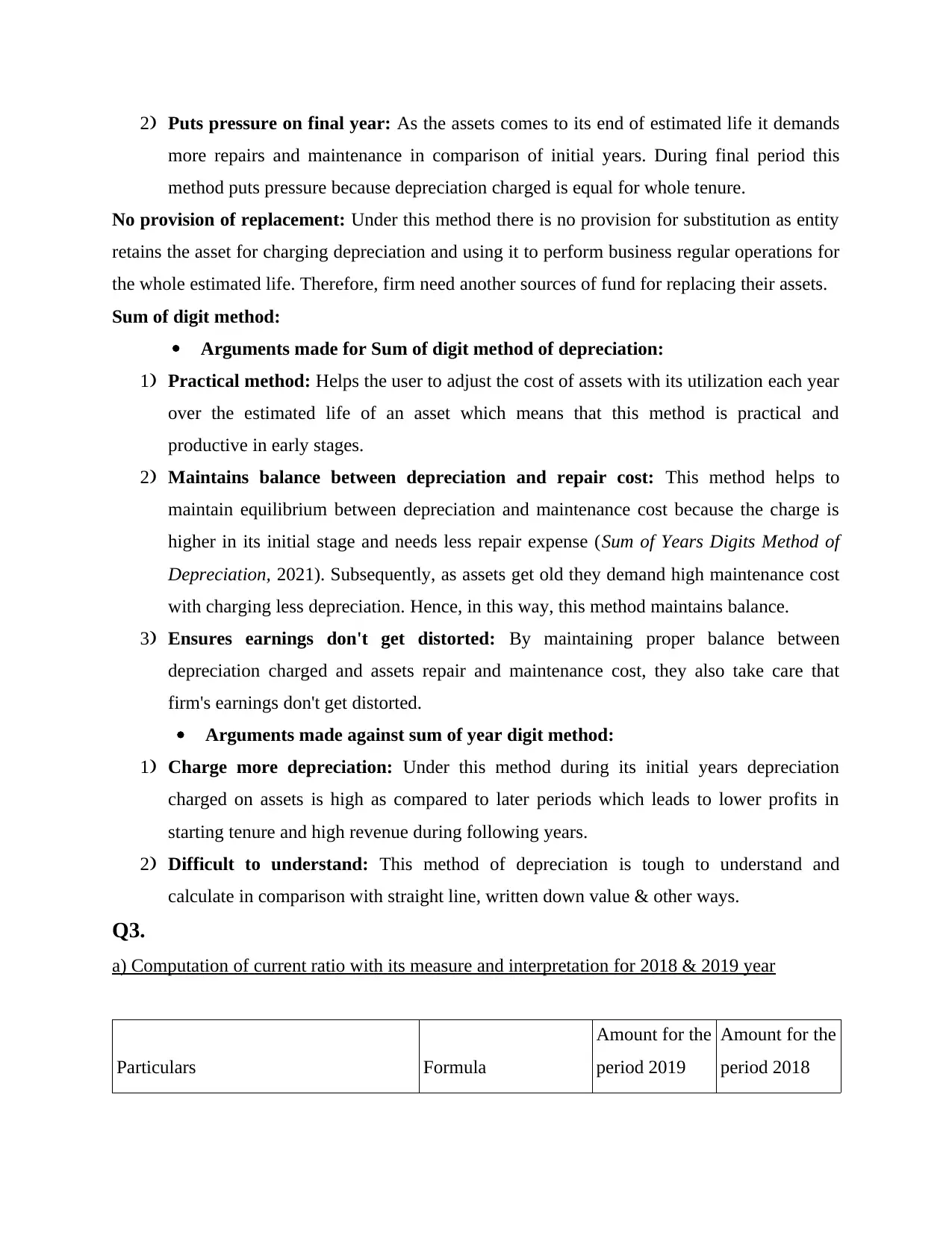

2) Puts pressure on final year: As the assets comes to its end of estimated life it demands

more repairs and maintenance in comparison of initial years. During final period this

method puts pressure because depreciation charged is equal for whole tenure.

No provision of replacement: Under this method there is no provision for substitution as entity

retains the asset for charging depreciation and using it to perform business regular operations for

the whole estimated life. Therefore, firm need another sources of fund for replacing their assets.

Sum of digit method:

Arguments made for Sum of digit method of depreciation:

1) Practical method: Helps the user to adjust the cost of assets with its utilization each year

over the estimated life of an asset which means that this method is practical and

productive in early stages.

2) Maintains balance between depreciation and repair cost: This method helps to

maintain equilibrium between depreciation and maintenance cost because the charge is

higher in its initial stage and needs less repair expense (Sum of Years Digits Method of

Depreciation, 2021). Subsequently, as assets get old they demand high maintenance cost

with charging less depreciation. Hence, in this way, this method maintains balance.

3) Ensures earnings don't get distorted: By maintaining proper balance between

depreciation charged and assets repair and maintenance cost, they also take care that

firm's earnings don't get distorted.

Arguments made against sum of year digit method:

1) Charge more depreciation: Under this method during its initial years depreciation

charged on assets is high as compared to later periods which leads to lower profits in

starting tenure and high revenue during following years.

2) Difficult to understand: This method of depreciation is tough to understand and

calculate in comparison with straight line, written down value & other ways.

Q3.

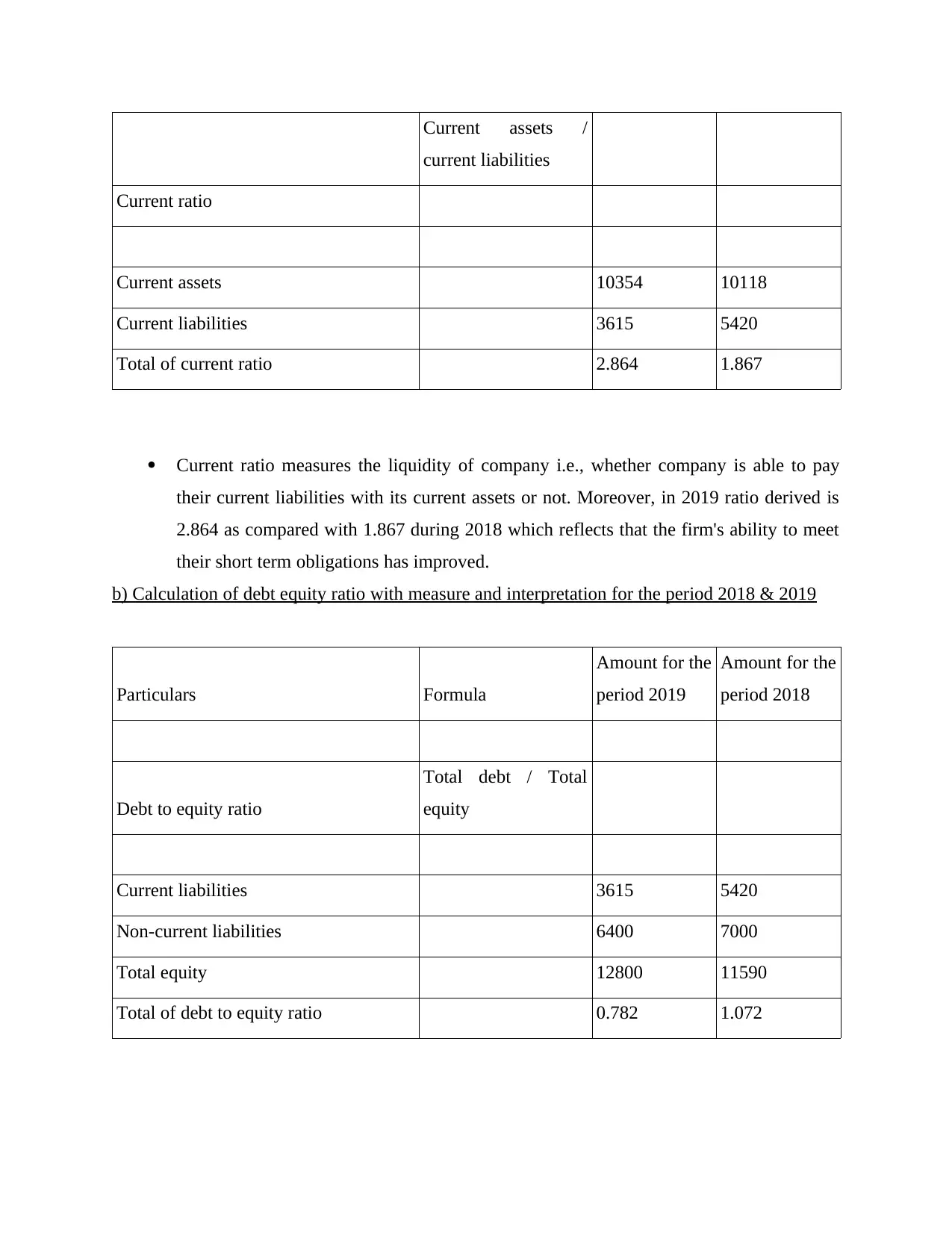

a) Computation of current ratio with its measure and interpretation for 2018 & 2019 year

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

more repairs and maintenance in comparison of initial years. During final period this

method puts pressure because depreciation charged is equal for whole tenure.

No provision of replacement: Under this method there is no provision for substitution as entity

retains the asset for charging depreciation and using it to perform business regular operations for

the whole estimated life. Therefore, firm need another sources of fund for replacing their assets.

Sum of digit method:

Arguments made for Sum of digit method of depreciation:

1) Practical method: Helps the user to adjust the cost of assets with its utilization each year

over the estimated life of an asset which means that this method is practical and

productive in early stages.

2) Maintains balance between depreciation and repair cost: This method helps to

maintain equilibrium between depreciation and maintenance cost because the charge is

higher in its initial stage and needs less repair expense (Sum of Years Digits Method of

Depreciation, 2021). Subsequently, as assets get old they demand high maintenance cost

with charging less depreciation. Hence, in this way, this method maintains balance.

3) Ensures earnings don't get distorted: By maintaining proper balance between

depreciation charged and assets repair and maintenance cost, they also take care that

firm's earnings don't get distorted.

Arguments made against sum of year digit method:

1) Charge more depreciation: Under this method during its initial years depreciation

charged on assets is high as compared to later periods which leads to lower profits in

starting tenure and high revenue during following years.

2) Difficult to understand: This method of depreciation is tough to understand and

calculate in comparison with straight line, written down value & other ways.

Q3.

a) Computation of current ratio with its measure and interpretation for 2018 & 2019 year

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current assets /

current liabilities

Current ratio

Current assets 10354 10118

Current liabilities 3615 5420

Total of current ratio 2.864 1.867

Current ratio measures the liquidity of company i.e., whether company is able to pay

their current liabilities with its current assets or not. Moreover, in 2019 ratio derived is

2.864 as compared with 1.867 during 2018 which reflects that the firm's ability to meet

their short term obligations has improved.

b) Calculation of debt equity ratio with measure and interpretation for the period 2018 & 2019

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

Debt to equity ratio

Total debt / Total

equity

Current liabilities 3615 5420

Non-current liabilities 6400 7000

Total equity 12800 11590

Total of debt to equity ratio 0.782 1.072

current liabilities

Current ratio

Current assets 10354 10118

Current liabilities 3615 5420

Total of current ratio 2.864 1.867

Current ratio measures the liquidity of company i.e., whether company is able to pay

their current liabilities with its current assets or not. Moreover, in 2019 ratio derived is

2.864 as compared with 1.867 during 2018 which reflects that the firm's ability to meet

their short term obligations has improved.

b) Calculation of debt equity ratio with measure and interpretation for the period 2018 & 2019

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

Debt to equity ratio

Total debt / Total

equity

Current liabilities 3615 5420

Non-current liabilities 6400 7000

Total equity 12800 11590

Total of debt to equity ratio 0.782 1.072

This ratio reflects the portion of equity and debt which company is using to fund its

assets. By looking at firm's ratio in the given case, it shows that firm's debt to equity

ratio has gone down in comparison to 2018 where it becomes 0.782 in 2019 from 1.072

during 2018. Therefore, financial risk for the company has reduced in 2019.

c) Determination of return on equity with its measures and interpretation

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

Return on equity ratio

Net income /

Shareholders equity

Net income

(revenue – cost of

sales – total

expenses) 3033 2025

Shareholders equity 12800 11590

Total of return on equity 23.70% 17.47%

Return on equity shows that whether the company is handling shareholders money

properly or not. Through a computation of such ratio we have seen that percentage is

increased by 6.23% in year 2019 i.e., it gives 23.70% from 17.47%. accordingly, it can

be said that the company's efficiency in using its shareholder's equity has improved.

d) Calculation of gross profit ratio by considering its measures and interpretation for period 2018

& 2019

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

assets. By looking at firm's ratio in the given case, it shows that firm's debt to equity

ratio has gone down in comparison to 2018 where it becomes 0.782 in 2019 from 1.072

during 2018. Therefore, financial risk for the company has reduced in 2019.

c) Determination of return on equity with its measures and interpretation

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

Return on equity ratio

Net income /

Shareholders equity

Net income

(revenue – cost of

sales – total

expenses) 3033 2025

Shareholders equity 12800 11590

Total of return on equity 23.70% 17.47%

Return on equity shows that whether the company is handling shareholders money

properly or not. Through a computation of such ratio we have seen that percentage is

increased by 6.23% in year 2019 i.e., it gives 23.70% from 17.47%. accordingly, it can

be said that the company's efficiency in using its shareholder's equity has improved.

d) Calculation of gross profit ratio by considering its measures and interpretation for period 2018

& 2019

Particulars Formula

Amount for the

period 2019

Amount for the

period 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit ratio

Gross profit / net

sales

Gross profit

(revenue – cost of

sales) 12188 10695

Net sales 18200 16481

Total of gross profit ratio 66.97% 64.89%

Gross profit ratio reflects the profitability of company i.e., how efficiently firm is

performing and generating good earnings over a particular period. Moreover, the above

quoted calculation has improved in 2019 i.e., entity is producing 66.97% profit from its

operations by comparing it with result generated during 2018 i.e., of 64.89%.

e) Two users of financial statement

1) Government: The stated authority uses such information to know whether firm has paid

appropriate amount of tax or not.

2) Investors: They will require financial statements to know the firms position and for

understanding a performance of their investment.

Q4.

a) Assessement of following projects using two methods:

b) Pay back period method

Project 1:

Year Cash inflows Cumulative cash inflows

1 175000 175000

2 175000 350000

3 175000 525000

Gross profit / net

sales

Gross profit

(revenue – cost of

sales) 12188 10695

Net sales 18200 16481

Total of gross profit ratio 66.97% 64.89%

Gross profit ratio reflects the profitability of company i.e., how efficiently firm is

performing and generating good earnings over a particular period. Moreover, the above

quoted calculation has improved in 2019 i.e., entity is producing 66.97% profit from its

operations by comparing it with result generated during 2018 i.e., of 64.89%.

e) Two users of financial statement

1) Government: The stated authority uses such information to know whether firm has paid

appropriate amount of tax or not.

2) Investors: They will require financial statements to know the firms position and for

understanding a performance of their investment.

Q4.

a) Assessement of following projects using two methods:

b) Pay back period method

Project 1:

Year Cash inflows Cumulative cash inflows

1 175000 175000

2 175000 350000

3 175000 525000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

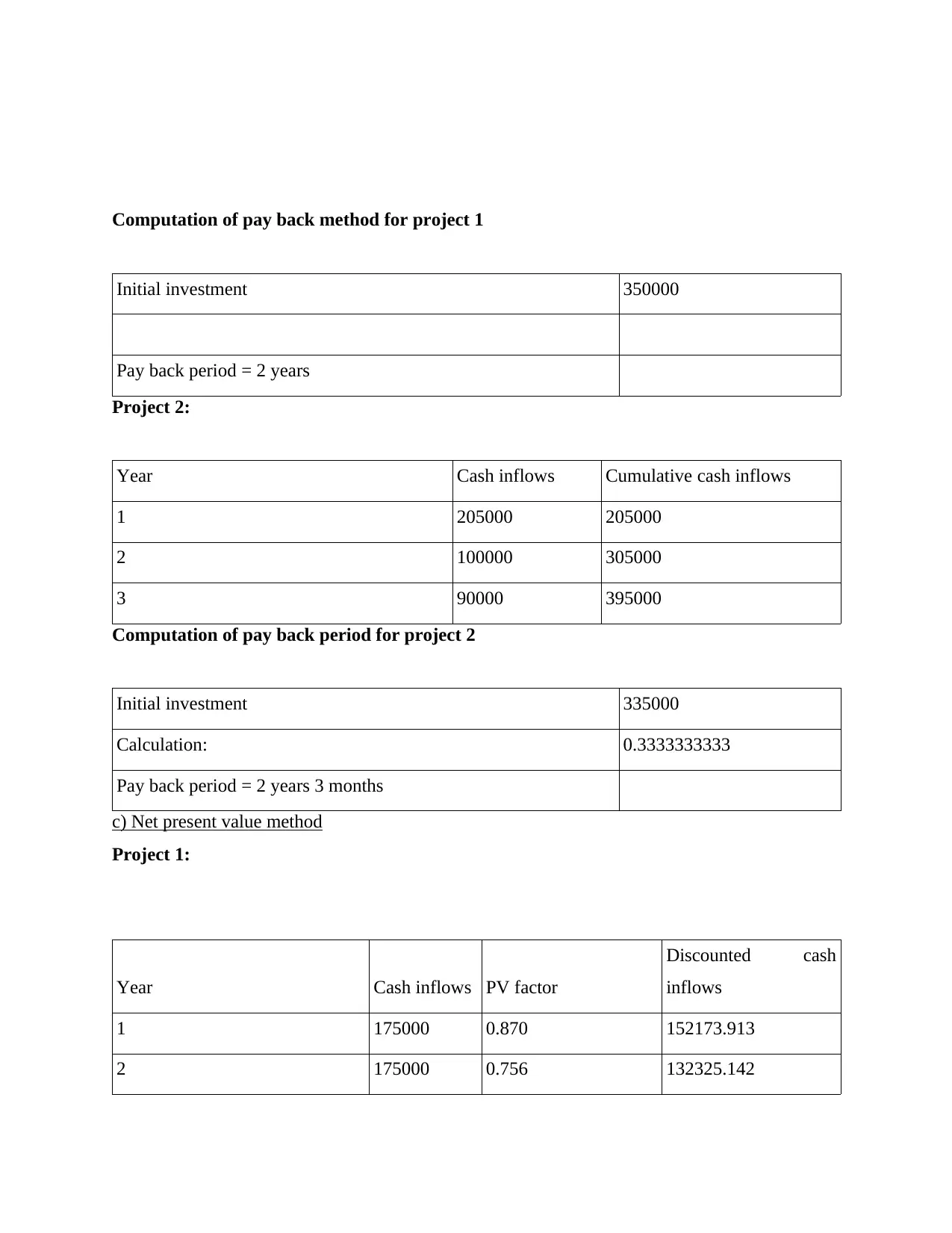

Computation of pay back method for project 1

Initial investment 350000

Pay back period = 2 years

Project 2:

Year Cash inflows Cumulative cash inflows

1 205000 205000

2 100000 305000

3 90000 395000

Computation of pay back period for project 2

Initial investment 335000

Calculation: 0.3333333333

Pay back period = 2 years 3 months

c) Net present value method

Project 1:

Year Cash inflows PV factor

Discounted cash

inflows

1 175000 0.870 152173.913

2 175000 0.756 132325.142

Initial investment 350000

Pay back period = 2 years

Project 2:

Year Cash inflows Cumulative cash inflows

1 205000 205000

2 100000 305000

3 90000 395000

Computation of pay back period for project 2

Initial investment 335000

Calculation: 0.3333333333

Pay back period = 2 years 3 months

c) Net present value method

Project 1:

Year Cash inflows PV factor

Discounted cash

inflows

1 175000 0.870 152173.913

2 175000 0.756 132325.142

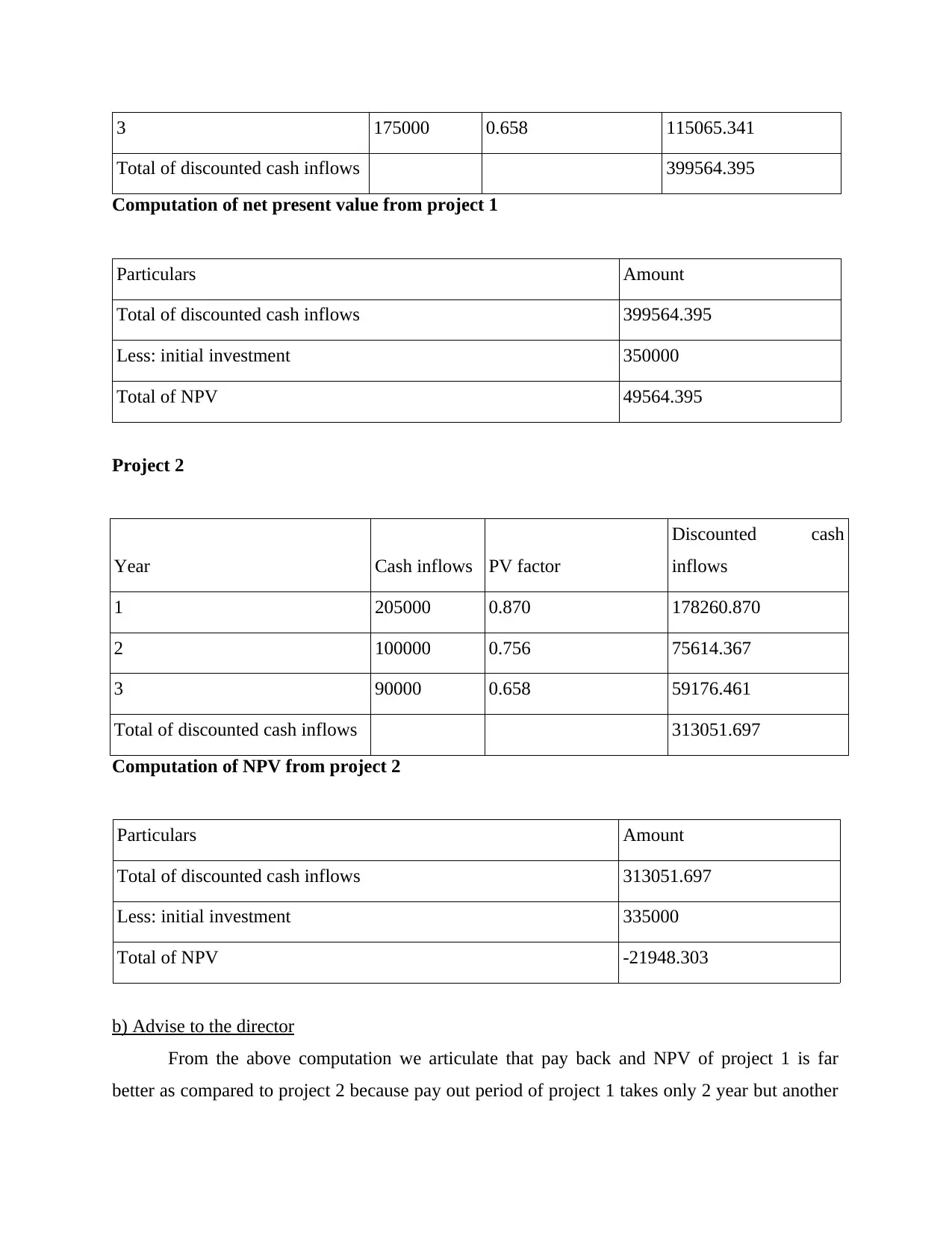

3 175000 0.658 115065.341

Total of discounted cash inflows 399564.395

Computation of net present value from project 1

Particulars Amount

Total of discounted cash inflows 399564.395

Less: initial investment 350000

Total of NPV 49564.395

Project 2

Year Cash inflows PV factor

Discounted cash

inflows

1 205000 0.870 178260.870

2 100000 0.756 75614.367

3 90000 0.658 59176.461

Total of discounted cash inflows 313051.697

Computation of NPV from project 2

Particulars Amount

Total of discounted cash inflows 313051.697

Less: initial investment 335000

Total of NPV -21948.303

b) Advise to the director

From the above computation we articulate that pay back and NPV of project 1 is far

better as compared to project 2 because pay out period of project 1 takes only 2 year but another

Total of discounted cash inflows 399564.395

Computation of net present value from project 1

Particulars Amount

Total of discounted cash inflows 399564.395

Less: initial investment 350000

Total of NPV 49564.395

Project 2

Year Cash inflows PV factor

Discounted cash

inflows

1 205000 0.870 178260.870

2 100000 0.756 75614.367

3 90000 0.658 59176.461

Total of discounted cash inflows 313051.697

Computation of NPV from project 2

Particulars Amount

Total of discounted cash inflows 313051.697

Less: initial investment 335000

Total of NPV -21948.303

b) Advise to the director

From the above computation we articulate that pay back and NPV of project 1 is far

better as compared to project 2 because pay out period of project 1 takes only 2 year but another

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.