Financial Accounting Report: Analysis of Dandy's Financial Statements

VerifiedAdded on 2021/02/19

|12

|2602

|62

Report

AI Summary

This financial accounting report analyzes a retail business's financial performance, focusing on the preparation and interpretation of financial statements. The report begins with an introduction to financial accounting, covering the recording, summarizing, and reporting of financial transactions. It then delves into a detailed explanation of various financial events, including trial balances, sales accounts, purchase accounts, and cash flow statements. The report includes an analysis of transactions, such as sales and purchase day books, and ledger accounts. Finally, it addresses the principle of prudence in accounting, emphasizing the importance of recognizing potential losses and ensuring accurate financial reporting. The report concludes with financial statements, including an income statement and a balance sheet, and provides insights into the company's financial position.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

1) Short explanation of the events........................................................................................................3

2). Transactions and records....................................................................................................................5

3). Principle of prudency.......................................................................................................................10

CONCLUSION........................................................................................................................................11

REFERENCES........................................................................................................................................12

INTRODUCTION.....................................................................................................................................3

1) Short explanation of the events........................................................................................................3

2). Transactions and records....................................................................................................................5

3). Principle of prudency.......................................................................................................................10

CONCLUSION........................................................................................................................................11

REFERENCES........................................................................................................................................12

INTRODUCTION

Financial accounting is a wider concept having number of activities comprising of recording,

summarizing and reposting the results to the users of such information. The transactions included

are of financial nature (Weil, Schipper and Francis, 2013). These are used to prepare financial

statements such as balance sheet, income statement and cash flow statement for disclosing the

position and performance of the company for a particular time period which is normally

annually. The main aim is to present these reports to the shareholders as their money are invested

in the organization (May, 2013). This report is based on a company which is having retail

business and it covers the detail understanding of the various events which taken place in the

month as specified, preparation of accurate and reliable accounts, trial balance, income statement

and balance sheet which can be relied upon and principle of prudence in maintaining the

authenticity of such reports.

1) Short explanation of the events

Trial balance- It is a bookkeeping worksheet which includes all the amounts of the ledgers

accounts. Two columns are drawn for debit and credit amounts which are made equal in order to

check the accuracy (Meaning of Trial Balance, 2019). An organization prepares it mainly at the

end of a particular reporting period. The main purpose is to attain the fact that each and every

entry in the books are mathematically correct. The trial balance of Dandy’s shows that sales are

of 301,000, purchases are of 154,840. Apart from this, there were genuine expenses such as

wages, electricity, rent which are fixed. Furthermore, it made purchases of equipment for

170,000 on which a depreciation of 34,000 was received. The amount available as capital as on

1st June is 205,000 which can be utilized wisely for multiplying the profit.

Sales Account- This account includes every transactions related to sales. There is no

exclusion of cash or credit sales. In other words, sales in the nature of credit as well as cash are

included. Furthermore, it is then teamed up with all the sales returns and allowances account in

order to ascertain the net sales (Meaning of sales account, 2019). It is the actual sales which is

mentioned in the income statement. In the context of Dandy’s business, the account depicts that

sales made in the month of June is 10,360 which includes cash sales of 6,820 whereas the sales

returns are 2,700 and the net sales is 315,480.

Financial accounting is a wider concept having number of activities comprising of recording,

summarizing and reposting the results to the users of such information. The transactions included

are of financial nature (Weil, Schipper and Francis, 2013). These are used to prepare financial

statements such as balance sheet, income statement and cash flow statement for disclosing the

position and performance of the company for a particular time period which is normally

annually. The main aim is to present these reports to the shareholders as their money are invested

in the organization (May, 2013). This report is based on a company which is having retail

business and it covers the detail understanding of the various events which taken place in the

month as specified, preparation of accurate and reliable accounts, trial balance, income statement

and balance sheet which can be relied upon and principle of prudence in maintaining the

authenticity of such reports.

1) Short explanation of the events

Trial balance- It is a bookkeeping worksheet which includes all the amounts of the ledgers

accounts. Two columns are drawn for debit and credit amounts which are made equal in order to

check the accuracy (Meaning of Trial Balance, 2019). An organization prepares it mainly at the

end of a particular reporting period. The main purpose is to attain the fact that each and every

entry in the books are mathematically correct. The trial balance of Dandy’s shows that sales are

of 301,000, purchases are of 154,840. Apart from this, there were genuine expenses such as

wages, electricity, rent which are fixed. Furthermore, it made purchases of equipment for

170,000 on which a depreciation of 34,000 was received. The amount available as capital as on

1st June is 205,000 which can be utilized wisely for multiplying the profit.

Sales Account- This account includes every transactions related to sales. There is no

exclusion of cash or credit sales. In other words, sales in the nature of credit as well as cash are

included. Furthermore, it is then teamed up with all the sales returns and allowances account in

order to ascertain the net sales (Meaning of sales account, 2019). It is the actual sales which is

mentioned in the income statement. In the context of Dandy’s business, the account depicts that

sales made in the month of June is 10,360 which includes cash sales of 6,820 whereas the sales

returns are 2,700 and the net sales is 315,480.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

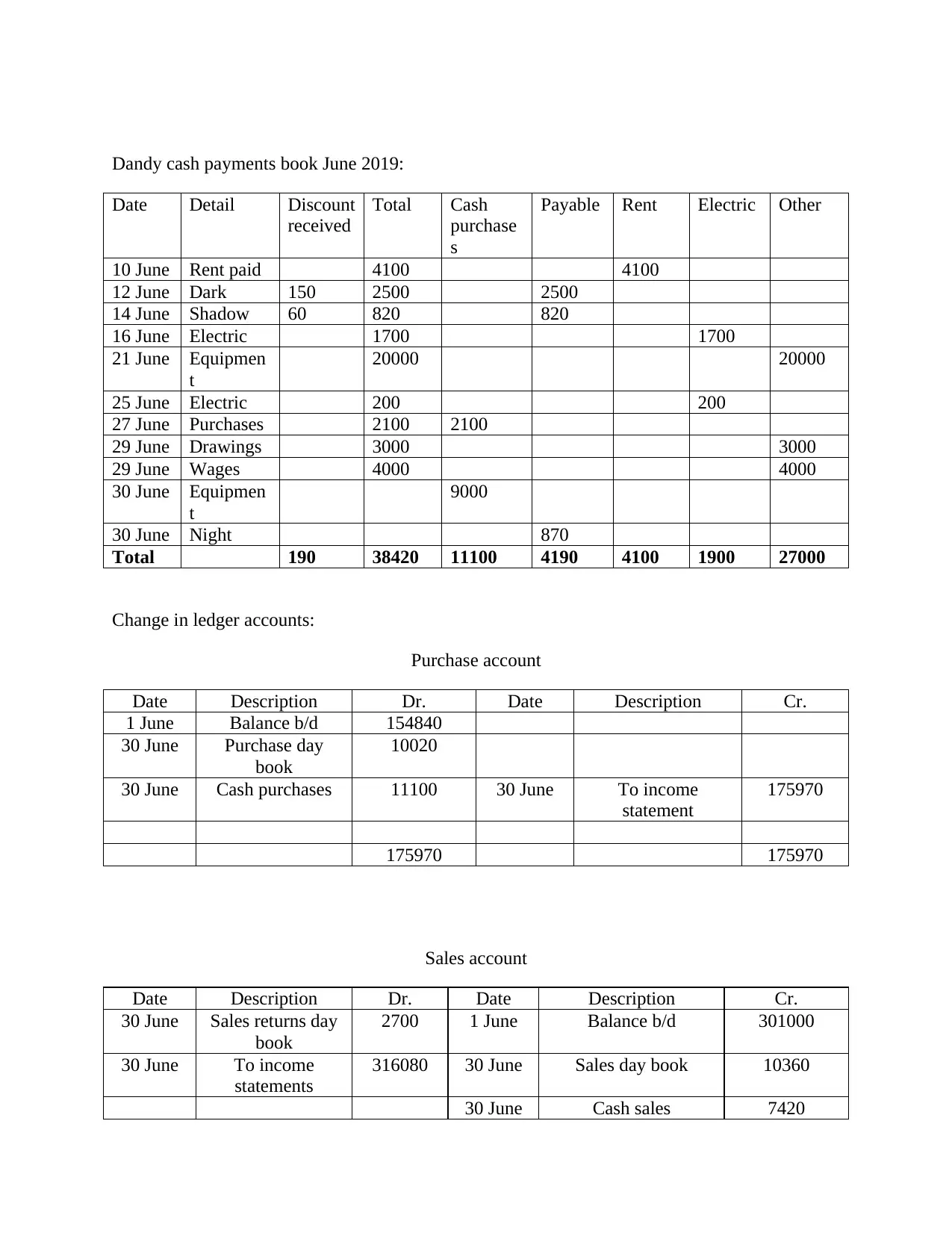

Purchase account- In this account, all the purchases are recorded which have occurred within

a period. Inventory is purchased for selling it by making a final product. It also includes

purchases made on credit and also on cash. This is to keep track of the raw material and other

assets in order to run the business successfully. Dandy made purchases of 10,020 in which cash

purchases on 2,100. In addition to this, the net purchases has a balance of 166,960 to be show in

the income statement as it is the net purchases made Dandy for the month of June. There were

purchase returns which amounted to 4,850 from two of its customers.

Carriage inwards account- The cost spent on transportation of the goods are included in this

account. It is paid by the purchaser. It is treated as the cost of the main product. These are the

direct expense which is taken into account while calculating cost of goods sold. In majority of

the cases it is made a part of the manufacturing of good to be sold to the customers. In Dandy’s

business, the total carriage inwards for the purchases made in the month of June is 1,300.

Cash receipts books- This is a book in which all the transactions happened in cash recorded.

It important to differentiate between cash and other dealings (Cash book, 2019). Apart from this,

discount which are allowed to a customer is also shown to find out the actual cash received by

the company at the end of the month. Dandy has made cash sales for 6,820 after providing a

discount of 500. The amount actually received by it is 5,900 on account of this book. These are

amounts which have been received by the company from the buyers to whom goods are sold.

Cash payments book- An entity also makes payments to buy different kinds of assets, raw

materials etc. It can be made on cash or credit. Hence, all the payments made by the company on

cash are shown in this book. Dandy has made a total payment of 38,420 which is divided among

rent, electric and other transactions. He also received a discount of 210 and paid 2100 in cash.

Wages Expense account- Every business organization hires employees for making them work in

order to complete the goals, and in return they are being paid. Hence, wages expense account

includes the amount given to the workers. It depicts that 56,890 is the amount which comprises

of wages paid and accrued wages also.

Rent expense- The place where the business activities are being conducted may be taken on rent

by the owners. This is an expense which occurs every month and should be made within the right

time to avoid any late payment. Dandy has a place for which a fixed rent has to be paid. Also, it

a period. Inventory is purchased for selling it by making a final product. It also includes

purchases made on credit and also on cash. This is to keep track of the raw material and other

assets in order to run the business successfully. Dandy made purchases of 10,020 in which cash

purchases on 2,100. In addition to this, the net purchases has a balance of 166,960 to be show in

the income statement as it is the net purchases made Dandy for the month of June. There were

purchase returns which amounted to 4,850 from two of its customers.

Carriage inwards account- The cost spent on transportation of the goods are included in this

account. It is paid by the purchaser. It is treated as the cost of the main product. These are the

direct expense which is taken into account while calculating cost of goods sold. In majority of

the cases it is made a part of the manufacturing of good to be sold to the customers. In Dandy’s

business, the total carriage inwards for the purchases made in the month of June is 1,300.

Cash receipts books- This is a book in which all the transactions happened in cash recorded.

It important to differentiate between cash and other dealings (Cash book, 2019). Apart from this,

discount which are allowed to a customer is also shown to find out the actual cash received by

the company at the end of the month. Dandy has made cash sales for 6,820 after providing a

discount of 500. The amount actually received by it is 5,900 on account of this book. These are

amounts which have been received by the company from the buyers to whom goods are sold.

Cash payments book- An entity also makes payments to buy different kinds of assets, raw

materials etc. It can be made on cash or credit. Hence, all the payments made by the company on

cash are shown in this book. Dandy has made a total payment of 38,420 which is divided among

rent, electric and other transactions. He also received a discount of 210 and paid 2100 in cash.

Wages Expense account- Every business organization hires employees for making them work in

order to complete the goals, and in return they are being paid. Hence, wages expense account

includes the amount given to the workers. It depicts that 56,890 is the amount which comprises

of wages paid and accrued wages also.

Rent expense- The place where the business activities are being conducted may be taken on rent

by the owners. This is an expense which occurs every month and should be made within the right

time to avoid any late payment. Dandy has a place for which a fixed rent has to be paid. Also, it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

does not always include the rent of the property but any other things can also be rented.

Furthermore, it can also be paid in advance. In the case of Dandy the prepaid rent is 1,250 and

rent paid is 4,100.

Electricity expense account- The amount paid for consuming the electricity is shown in this

account. Dandy has paid an amount of 1900 on 30th June.

Income statement- It is prepared to have track of revenue and expenses during a particular

period. The alternative names for this are profit and loss statement or statement of revenue and

expense. It is helpful in calculating the profit after deducting all the expenses from the income. If

the answer is positive then it is net profit and if the answer is negative then it is the loss. Dandy

has earned a profit of 37,740.

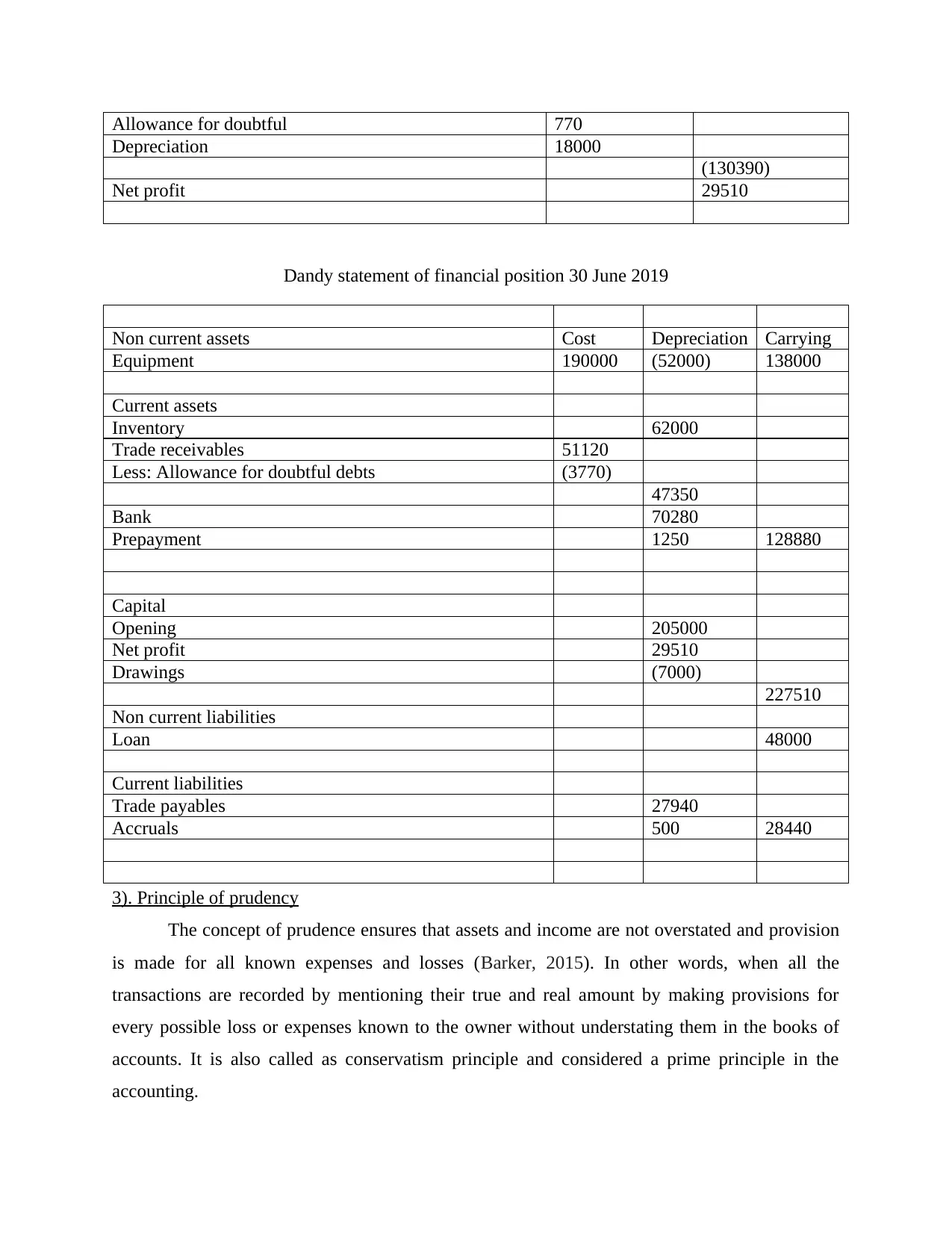

Balance sheet- It covers the assets and liabilities of a company for a particular period.

The main aim is to find out the financial position and soundness of the company (Reid, 2018). It

shows the performance and the findings are disclosed to the shareholders for making them invest

more into the company. In the current scenario of Dandy, the current assets are 133,780 and

fixed assets are 138,000. On the other hand, current liabilities is 28, 040 and non-current

liabilities are 48,000.

There are many different accounts having the amount which is important to determine in order to

have accurate entries in then accounts.

2). Transactions and records

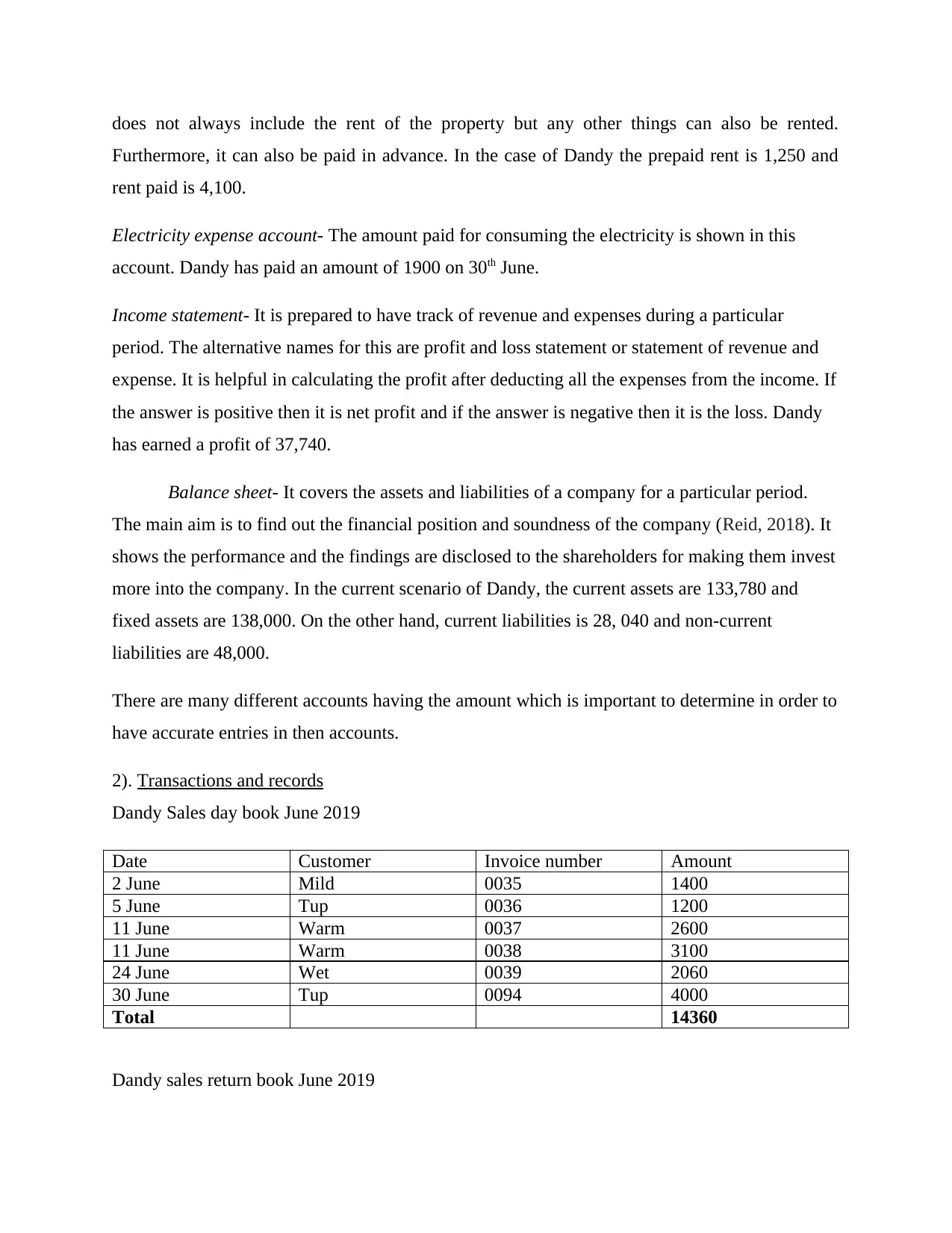

Dandy Sales day book June 2019

Date Customer Invoice number Amount

2 June Mild 0035 1400

5 June Tup 0036 1200

11 June Warm 0037 2600

11 June Warm 0038 3100

24 June Wet 0039 2060

30 June Tup 0094 4000

Total 14360

Dandy sales return book June 2019

Furthermore, it can also be paid in advance. In the case of Dandy the prepaid rent is 1,250 and

rent paid is 4,100.

Electricity expense account- The amount paid for consuming the electricity is shown in this

account. Dandy has paid an amount of 1900 on 30th June.

Income statement- It is prepared to have track of revenue and expenses during a particular

period. The alternative names for this are profit and loss statement or statement of revenue and

expense. It is helpful in calculating the profit after deducting all the expenses from the income. If

the answer is positive then it is net profit and if the answer is negative then it is the loss. Dandy

has earned a profit of 37,740.

Balance sheet- It covers the assets and liabilities of a company for a particular period.

The main aim is to find out the financial position and soundness of the company (Reid, 2018). It

shows the performance and the findings are disclosed to the shareholders for making them invest

more into the company. In the current scenario of Dandy, the current assets are 133,780 and

fixed assets are 138,000. On the other hand, current liabilities is 28, 040 and non-current

liabilities are 48,000.

There are many different accounts having the amount which is important to determine in order to

have accurate entries in then accounts.

2). Transactions and records

Dandy Sales day book June 2019

Date Customer Invoice number Amount

2 June Mild 0035 1400

5 June Tup 0036 1200

11 June Warm 0037 2600

11 June Warm 0038 3100

24 June Wet 0039 2060

30 June Tup 0094 4000

Total 14360

Dandy sales return book June 2019

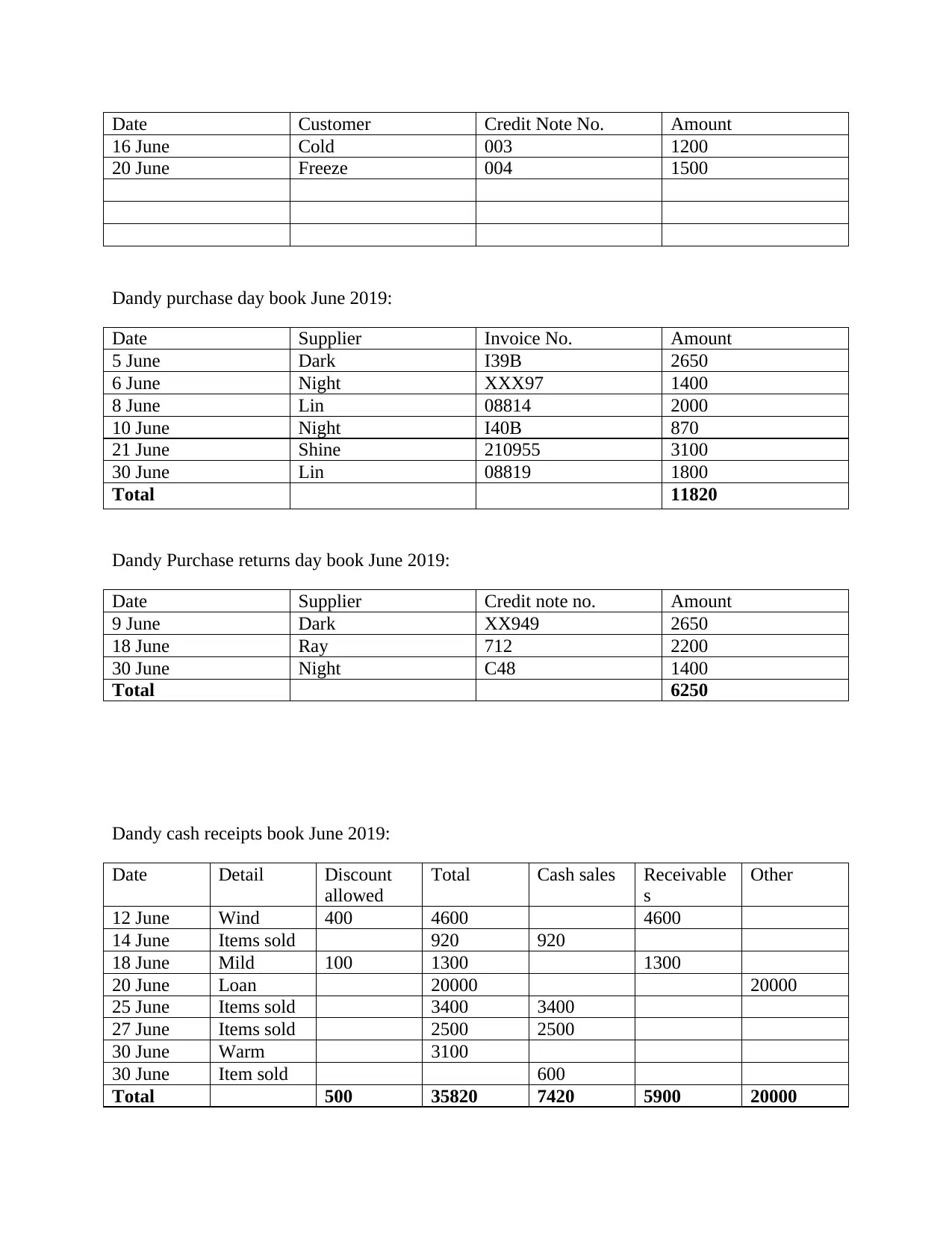

Date Customer Credit Note No. Amount

16 June Cold 003 1200

20 June Freeze 004 1500

Dandy purchase day book June 2019:

Date Supplier Invoice No. Amount

5 June Dark I39B 2650

6 June Night XXX97 1400

8 June Lin 08814 2000

10 June Night I40B 870

21 June Shine 210955 3100

30 June Lin 08819 1800

Total 11820

Dandy Purchase returns day book June 2019:

Date Supplier Credit note no. Amount

9 June Dark XX949 2650

18 June Ray 712 2200

30 June Night C48 1400

Total 6250

Dandy cash receipts book June 2019:

Date Detail Discount

allowed

Total Cash sales Receivable

s

Other

12 June Wind 400 4600 4600

14 June Items sold 920 920

18 June Mild 100 1300 1300

20 June Loan 20000 20000

25 June Items sold 3400 3400

27 June Items sold 2500 2500

30 June Warm 3100

30 June Item sold 600

Total 500 35820 7420 5900 20000

16 June Cold 003 1200

20 June Freeze 004 1500

Dandy purchase day book June 2019:

Date Supplier Invoice No. Amount

5 June Dark I39B 2650

6 June Night XXX97 1400

8 June Lin 08814 2000

10 June Night I40B 870

21 June Shine 210955 3100

30 June Lin 08819 1800

Total 11820

Dandy Purchase returns day book June 2019:

Date Supplier Credit note no. Amount

9 June Dark XX949 2650

18 June Ray 712 2200

30 June Night C48 1400

Total 6250

Dandy cash receipts book June 2019:

Date Detail Discount

allowed

Total Cash sales Receivable

s

Other

12 June Wind 400 4600 4600

14 June Items sold 920 920

18 June Mild 100 1300 1300

20 June Loan 20000 20000

25 June Items sold 3400 3400

27 June Items sold 2500 2500

30 June Warm 3100

30 June Item sold 600

Total 500 35820 7420 5900 20000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dandy cash payments book June 2019:

Date Detail Discount

received

Total Cash

purchase

s

Payable Rent Electric Other

10 June Rent paid 4100 4100

12 June Dark 150 2500 2500

14 June Shadow 60 820 820

16 June Electric 1700 1700

21 June Equipmen

t

20000 20000

25 June Electric 200 200

27 June Purchases 2100 2100

29 June Drawings 3000 3000

29 June Wages 4000 4000

30 June Equipmen

t

9000

30 June Night 870

Total 190 38420 11100 4190 4100 1900 27000

Change in ledger accounts:

Purchase account

Date Description Dr. Date Description Cr.

1 June Balance b/d 154840

30 June Purchase day

book

10020

30 June Cash purchases 11100 30 June To income

statement

175970

175970 175970

Sales account

Date Description Dr. Date Description Cr.

30 June Sales returns day

book

2700 1 June Balance b/d 301000

30 June To income

statements

316080 30 June Sales day book 10360

30 June Cash sales 7420

Date Detail Discount

received

Total Cash

purchase

s

Payable Rent Electric Other

10 June Rent paid 4100 4100

12 June Dark 150 2500 2500

14 June Shadow 60 820 820

16 June Electric 1700 1700

21 June Equipmen

t

20000 20000

25 June Electric 200 200

27 June Purchases 2100 2100

29 June Drawings 3000 3000

29 June Wages 4000 4000

30 June Equipmen

t

9000

30 June Night 870

Total 190 38420 11100 4190 4100 1900 27000

Change in ledger accounts:

Purchase account

Date Description Dr. Date Description Cr.

1 June Balance b/d 154840

30 June Purchase day

book

10020

30 June Cash purchases 11100 30 June To income

statement

175970

175970 175970

Sales account

Date Description Dr. Date Description Cr.

30 June Sales returns day

book

2700 1 June Balance b/d 301000

30 June To income

statements

316080 30 June Sales day book 10360

30 June Cash sales 7420

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

318780 318780

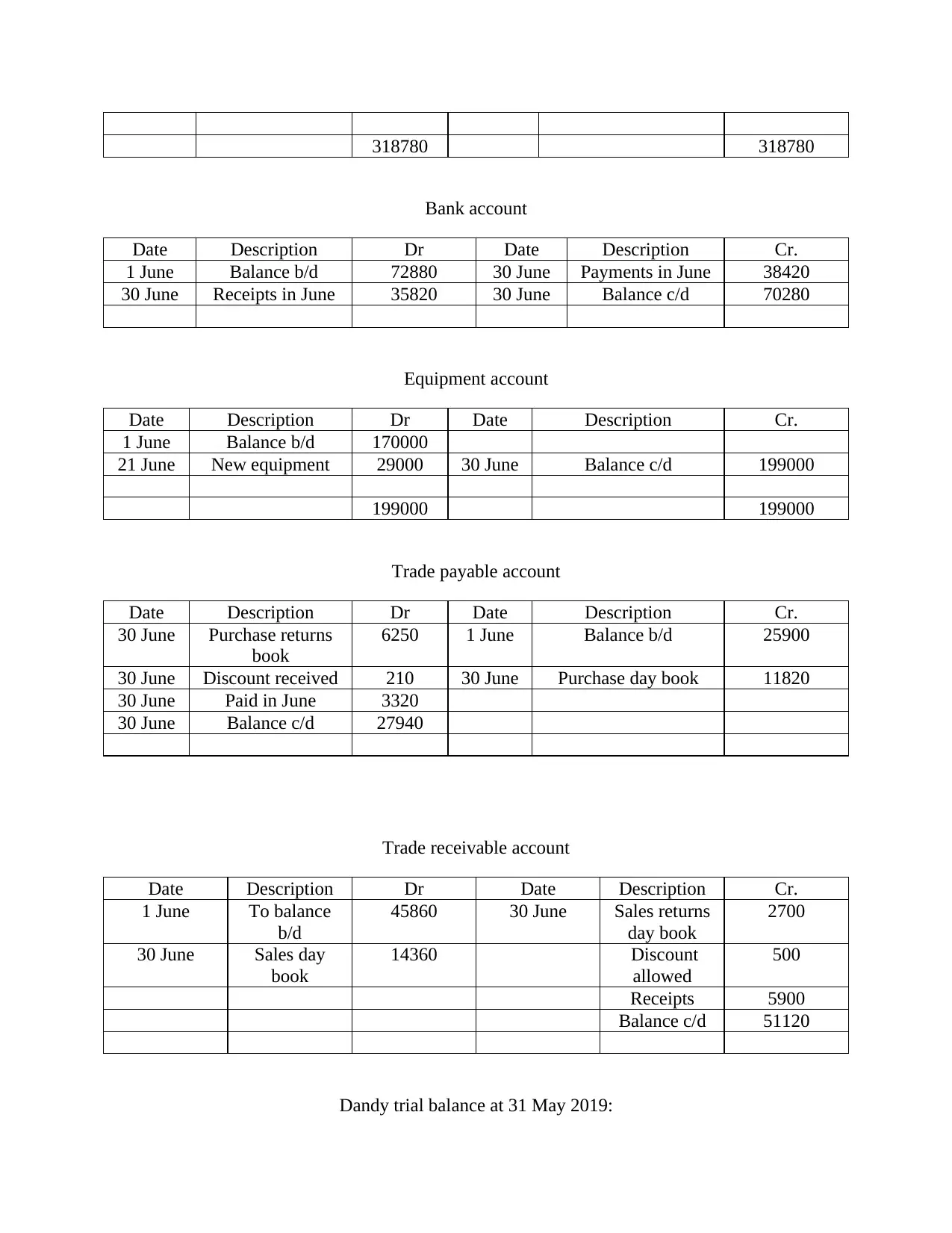

Bank account

Date Description Dr Date Description Cr.

1 June Balance b/d 72880 30 June Payments in June 38420

30 June Receipts in June 35820 30 June Balance c/d 70280

Equipment account

Date Description Dr Date Description Cr.

1 June Balance b/d 170000

21 June New equipment 29000 30 June Balance c/d 199000

199000 199000

Trade payable account

Date Description Dr Date Description Cr.

30 June Purchase returns

book

6250 1 June Balance b/d 25900

30 June Discount received 210 30 June Purchase day book 11820

30 June Paid in June 3320

30 June Balance c/d 27940

Trade receivable account

Date Description Dr Date Description Cr.

1 June To balance

b/d

45860 30 June Sales returns

day book

2700

30 June Sales day

book

14360 Discount

allowed

500

Receipts 5900

Balance c/d 51120

Dandy trial balance at 31 May 2019:

Bank account

Date Description Dr Date Description Cr.

1 June Balance b/d 72880 30 June Payments in June 38420

30 June Receipts in June 35820 30 June Balance c/d 70280

Equipment account

Date Description Dr Date Description Cr.

1 June Balance b/d 170000

21 June New equipment 29000 30 June Balance c/d 199000

199000 199000

Trade payable account

Date Description Dr Date Description Cr.

30 June Purchase returns

book

6250 1 June Balance b/d 25900

30 June Discount received 210 30 June Purchase day book 11820

30 June Paid in June 3320

30 June Balance c/d 27940

Trade receivable account

Date Description Dr Date Description Cr.

1 June To balance

b/d

45860 30 June Sales returns

day book

2700

30 June Sales day

book

14360 Discount

allowed

500

Receipts 5900

Balance c/d 51120

Dandy trial balance at 31 May 2019:

Dr. Cr.

Sales 316080

Purchase 175970

Carriage inward 1300

Return outwards 10300

Wages 56890

Rent 37230

Electricity 17000

Inventory 51600

Loans 50000

Trade receivables 51120

Discount allowed 500

Allowance for receivables 3770

Allowances for expenses 770

Trade payables 27940

Discount received 210

Equipments 190000

Provision for depreciation 52000

Depreciation 18000

Bank 70280

Drawings 7000

Capital 205000

Accruals 500

Prepayments 1250

665800 665800

Dandy income statement for year ending 30 June 2019:

Sales 316080

Opening inventory 51600

Purchase+ carriage- returns 166790

Less- Closing inventory (62000)

Cost of sales (156390)

Gross profit 159690

Discount received 210

159900

Expenses:

Wages 56890

Rent 37230

Electricity 17000

Discount allowed 500

Sales 316080

Purchase 175970

Carriage inward 1300

Return outwards 10300

Wages 56890

Rent 37230

Electricity 17000

Inventory 51600

Loans 50000

Trade receivables 51120

Discount allowed 500

Allowance for receivables 3770

Allowances for expenses 770

Trade payables 27940

Discount received 210

Equipments 190000

Provision for depreciation 52000

Depreciation 18000

Bank 70280

Drawings 7000

Capital 205000

Accruals 500

Prepayments 1250

665800 665800

Dandy income statement for year ending 30 June 2019:

Sales 316080

Opening inventory 51600

Purchase+ carriage- returns 166790

Less- Closing inventory (62000)

Cost of sales (156390)

Gross profit 159690

Discount received 210

159900

Expenses:

Wages 56890

Rent 37230

Electricity 17000

Discount allowed 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Allowance for doubtful 770

Depreciation 18000

(130390)

Net profit 29510

Dandy statement of financial position 30 June 2019

Non current assets Cost Depreciation Carrying

Equipment 190000 (52000) 138000

Current assets

Inventory 62000

Trade receivables 51120

Less: Allowance for doubtful debts (3770)

47350

Bank 70280

Prepayment 1250 128880

Capital

Opening 205000

Net profit 29510

Drawings (7000)

227510

Non current liabilities

Loan 48000

Current liabilities

Trade payables 27940

Accruals 500 28440

3). Principle of prudency

The concept of prudence ensures that assets and income are not overstated and provision

is made for all known expenses and losses (Barker, 2015). In other words, when all the

transactions are recorded by mentioning their true and real amount by making provisions for

every possible loss or expenses known to the owner without understating them in the books of

accounts. It is also called as conservatism principle and considered a prime principle in the

accounting.

Depreciation 18000

(130390)

Net profit 29510

Dandy statement of financial position 30 June 2019

Non current assets Cost Depreciation Carrying

Equipment 190000 (52000) 138000

Current assets

Inventory 62000

Trade receivables 51120

Less: Allowance for doubtful debts (3770)

47350

Bank 70280

Prepayment 1250 128880

Capital

Opening 205000

Net profit 29510

Drawings (7000)

227510

Non current liabilities

Loan 48000

Current liabilities

Trade payables 27940

Accruals 500 28440

3). Principle of prudency

The concept of prudence ensures that assets and income are not overstated and provision

is made for all known expenses and losses (Barker, 2015). In other words, when all the

transactions are recorded by mentioning their true and real amount by making provisions for

every possible loss or expenses known to the owner without understating them in the books of

accounts. It is also called as conservatism principle and considered a prime principle in the

accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The main focus is on taking all the losses into the consideration which may occur in

future. However, very little or zero consideration is given to prospective profits (Dennis, 2013).

This principle helps in bringing the information with enhanced realistic view depicting the actual

conditions of the company’s affairs. This principle can be applied in Dandy’s case which are as

follows:

1. Allowances for doubtful debts is provided which is the actual amount as shown in the

financial statement. It was likely that such a debt can be created in the future so Dandy

already took this into account.

2. It has provided the real amount which has been made in advance. The prepayments are

not overstated.

CONCLUSION

From the above report, it has been concluded that financial accounting is one of the

branches of accounting which deals with financial transactions. There is no inclusion of non-

financial records. Investors are more interested in financial activities as their money is utilized in

the operations of the company to make the money double. Every year financial statements are

prepared to ascertain the financial position of the organization and make decisions to improve the

working of the company. However, these can also be prepared on half year basis to develop short

term goals and strategies. Every account should be prepared by following number of accounting

principles so that accuracy and reliability of the financial information can be maintained. Since,

the shareholders and other stakeholders rely greatly on these documents, it should be taken into

that concept of prudence is abide by for avoiding any overstating the amounts in financial

statements.

future. However, very little or zero consideration is given to prospective profits (Dennis, 2013).

This principle helps in bringing the information with enhanced realistic view depicting the actual

conditions of the company’s affairs. This principle can be applied in Dandy’s case which are as

follows:

1. Allowances for doubtful debts is provided which is the actual amount as shown in the

financial statement. It was likely that such a debt can be created in the future so Dandy

already took this into account.

2. It has provided the real amount which has been made in advance. The prepayments are

not overstated.

CONCLUSION

From the above report, it has been concluded that financial accounting is one of the

branches of accounting which deals with financial transactions. There is no inclusion of non-

financial records. Investors are more interested in financial activities as their money is utilized in

the operations of the company to make the money double. Every year financial statements are

prepared to ascertain the financial position of the organization and make decisions to improve the

working of the company. However, these can also be prepared on half year basis to develop short

term goals and strategies. Every account should be prepared by following number of accounting

principles so that accuracy and reliability of the financial information can be maintained. Since,

the shareholders and other stakeholders rely greatly on these documents, it should be taken into

that concept of prudence is abide by for avoiding any overstating the amounts in financial

statements.

REFERENCES

Books & Journals:

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons. 28(2). pp.331-352.

Henderson, S., and et. Al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research. 45(4). pp.514-538.

Dennis, I., 2013. The nature of accounting regulation. Routledge.

Gheorghe, D., 2012. The accounting information quality concept. Economics, Management, and

Financial Markets. 7(4). pp.326-336.

Reid, W., 2018. The meaning of company accounts. Routledge.

Online:

Meaning of Trial Balance. 2019. [Online]. Available through :< https://accounting-

simplified.com/trial-balance.html>.

Meaning of sales account. 2019. [Online]. Available through :<

https://www.principlesofaccounting.com/account-types/>.

Cash book. 2019. [Online]. Available through :< https://www.investopedia.com/terms/c/cash-

book.asp>.

Books & Journals:

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons. 28(2). pp.331-352.

Henderson, S., and et. Al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research. 45(4). pp.514-538.

Dennis, I., 2013. The nature of accounting regulation. Routledge.

Gheorghe, D., 2012. The accounting information quality concept. Economics, Management, and

Financial Markets. 7(4). pp.326-336.

Reid, W., 2018. The meaning of company accounts. Routledge.

Online:

Meaning of Trial Balance. 2019. [Online]. Available through :< https://accounting-

simplified.com/trial-balance.html>.

Meaning of sales account. 2019. [Online]. Available through :<

https://www.principlesofaccounting.com/account-types/>.

Cash book. 2019. [Online]. Available through :< https://www.investopedia.com/terms/c/cash-

book.asp>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.