Financial Accounting Report: Regulations, Statements, and Ratios

VerifiedAdded on 2020/02/05

|23

|4466

|207

Report

AI Summary

This report delves into the core concepts of financial accounting, providing a comprehensive overview of its principles and practices. It begins by identifying the diverse users of financial statements and their respective information needs, emphasizing the importance of financial stability and growth indicators. The report then explores the legal and regulatory influences on financial statements, including key legislation like the Companies Act 2006, and accounting standards such as IFRS and GAAP, highlighting their implications for users. Furthermore, the report examines the role of regulatory bodies and how different laws and regulations shape accounting and reporting standards. The report also provides a practical application of accounting principles through the preparation of financial statements from a trial balance and addresses the preparation of financial statements from incomplete records. Finally, the report concludes with an analysis of accounting ratios to assess the performance and position of a business, offering valuable insights into financial statement analysis.

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................3

Task 1.........................................................................................................................................3

1.1 Different users of financial statements and their needs...................................................3

1.2 Legal and regulatory influences on financial statements.................................................4

1.3 Implications for users of regulatory bodies.....................................................................5

1.4 Different laws and regulations deals with accounting and reporting standards..............5

3.1 Information needs of different user group vary...............................................................6

3.2 Preparation of financial statement...................................................................................7

TASK 2......................................................................................................................................8

2.1 Preparing financial statements for the variety of business from a trail balance..............8

2.2 Preparing financial statements from incomplete records..............................................15

2.3 Consolidated balance sheet and p&L a/c.......................................................................17

TASK 4....................................................................................................................................20

4.1 Calculation of accounting ratios to assess the performance and position of a business20

4.2 Interpretations................................................................................................................20

Conclusion................................................................................................................................21

references..................................................................................................................................22

Introduction................................................................................................................................3

Task 1.........................................................................................................................................3

1.1 Different users of financial statements and their needs...................................................3

1.2 Legal and regulatory influences on financial statements.................................................4

1.3 Implications for users of regulatory bodies.....................................................................5

1.4 Different laws and regulations deals with accounting and reporting standards..............5

3.1 Information needs of different user group vary...............................................................6

3.2 Preparation of financial statement...................................................................................7

TASK 2......................................................................................................................................8

2.1 Preparing financial statements for the variety of business from a trail balance..............8

2.2 Preparing financial statements from incomplete records..............................................15

2.3 Consolidated balance sheet and p&L a/c.......................................................................17

TASK 4....................................................................................................................................20

4.1 Calculation of accounting ratios to assess the performance and position of a business20

4.2 Interpretations................................................................................................................20

Conclusion................................................................................................................................21

references..................................................................................................................................22

INTRODUCTION

Financial accounting is the cornerstone of the work of an accountant and preparing

accounts is the reporting mechanism for all the organization of different sectors of business.

This case will help to develop the framework for financial accounting and enable the reader

to understand various practical scenarios,which includes case study that integrates the various

aspects of financial accounting (Edwards, 2013). Financial accounting basically keeps

records of a company's financial transactions which follows set of rules which are explained

in accounting standard or accounting principals. Apart form this financial reporting includes

the annual report of company to its stockholder and securities and exchange commission

(Stickney and et.al., 2009).

TASK 1

1.1 Different users of financial statements and their needs

There are many users of financial statements who needs the information for various

purposes. Financial statements of the company shows the financial stability and growth of the

company over a fixed period of time (Porter and Norton, 2012). Different users like both

internal and external are their who will be affected by financial statements of the company

and needs the information for their own purposes.

Company management

The management team of the business needs the information to understand the

profitability,liquidity and cash flows to make decisions on operational and financing activities

of the business.

Employees

A company needs to give financial statement to their employees to increase the

involvement level of employees in business and make them comfortable to understand the

environment of the business so that company's growth can be maximized.

Government

Government needs the information of financial statements to find out whether the

company is meeting with their legal liabilities and provisions like payment of tax and other

(Warren, Reeve and Duchac, 2011). Therefore, government set some legislation and acts for

each kind of business.

Lenders

Financial accounting is the cornerstone of the work of an accountant and preparing

accounts is the reporting mechanism for all the organization of different sectors of business.

This case will help to develop the framework for financial accounting and enable the reader

to understand various practical scenarios,which includes case study that integrates the various

aspects of financial accounting (Edwards, 2013). Financial accounting basically keeps

records of a company's financial transactions which follows set of rules which are explained

in accounting standard or accounting principals. Apart form this financial reporting includes

the annual report of company to its stockholder and securities and exchange commission

(Stickney and et.al., 2009).

TASK 1

1.1 Different users of financial statements and their needs

There are many users of financial statements who needs the information for various

purposes. Financial statements of the company shows the financial stability and growth of the

company over a fixed period of time (Porter and Norton, 2012). Different users like both

internal and external are their who will be affected by financial statements of the company

and needs the information for their own purposes.

Company management

The management team of the business needs the information to understand the

profitability,liquidity and cash flows to make decisions on operational and financing activities

of the business.

Employees

A company needs to give financial statement to their employees to increase the

involvement level of employees in business and make them comfortable to understand the

environment of the business so that company's growth can be maximized.

Government

Government needs the information of financial statements to find out whether the

company is meeting with their legal liabilities and provisions like payment of tax and other

(Warren, Reeve and Duchac, 2011). Therefore, government set some legislation and acts for

each kind of business.

Lenders

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A lender who give loans to an organization needs the information to determine the

ability of the borrower to pay back the loan and charges which are applied on that. Lender

need to take complete details of borrower if in case he don't pay back the amount.

Suppliers

Suppliers needs the information of financial statement to find out the credit

worthiness of the company that whether it is safe to extend credit to the organization. It is

very important for suppliers to follow all legal acts and provisions.

Investors

Investors need the information of financial statement to find out the growth of the

business and to determine their part of profit in the organization. Financial statement gives a

detailed idea of profits or loss of the company over a given period of time.

1.2 Legal and regulatory influences on financial statements

Every organization needs to maintain their financial statement for various purpose. To

maintain the financial statement properly government has formed some rules and regulation

according to which the financial statements have to be maintained by each organization

(Wild, 2010). For this some laws and accounting standards are their like companies Act 2006,

IFRS, GAAP, ISBA etc..

Companies Act 2006

Under companies act there is no specific statutory requirement for sole proprietor and

limited company. If they are registered for Value added Tax than they have to keep adequate

records in their financial statements (Frank, Lynch and Rego, 2009). This act deals with the

entire activities of business regarding finance and a company must have to keep record of

daily financial transactions. According to companies act those companies which are which

are dealing in stocks have to keep report on total purchases and sales in the financial year.

Companies Act 2006 that are applied on both sole proprietor and limited company

IFRS(International financial reporting system)

IFRS has had a positive impact on the business entities as it widens the financial and

regulatory duties of the company. It is the improved form of domestic accounting standards

and also improved international image (Fülbier, and Weller, 2011). A single set of accounts

are developed for international transactions. Apart from this they extended the adoption of

common ratios which are used in GAAP.

ability of the borrower to pay back the loan and charges which are applied on that. Lender

need to take complete details of borrower if in case he don't pay back the amount.

Suppliers

Suppliers needs the information of financial statement to find out the credit

worthiness of the company that whether it is safe to extend credit to the organization. It is

very important for suppliers to follow all legal acts and provisions.

Investors

Investors need the information of financial statement to find out the growth of the

business and to determine their part of profit in the organization. Financial statement gives a

detailed idea of profits or loss of the company over a given period of time.

1.2 Legal and regulatory influences on financial statements

Every organization needs to maintain their financial statement for various purpose. To

maintain the financial statement properly government has formed some rules and regulation

according to which the financial statements have to be maintained by each organization

(Wild, 2010). For this some laws and accounting standards are their like companies Act 2006,

IFRS, GAAP, ISBA etc..

Companies Act 2006

Under companies act there is no specific statutory requirement for sole proprietor and

limited company. If they are registered for Value added Tax than they have to keep adequate

records in their financial statements (Frank, Lynch and Rego, 2009). This act deals with the

entire activities of business regarding finance and a company must have to keep record of

daily financial transactions. According to companies act those companies which are which

are dealing in stocks have to keep report on total purchases and sales in the financial year.

Companies Act 2006 that are applied on both sole proprietor and limited company

IFRS(International financial reporting system)

IFRS has had a positive impact on the business entities as it widens the financial and

regulatory duties of the company. It is the improved form of domestic accounting standards

and also improved international image (Fülbier, and Weller, 2011). A single set of accounts

are developed for international transactions. Apart from this they extended the adoption of

common ratios which are used in GAAP.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

GAAP(Generally accepted accounting principles)

GAAP is the generally accepted accounting principles according to which an business

entity have to maintain their accounts. It includes the rules,regulations and convention of

accounts. It basically deals with the domestic accounting principle not like international

accounting principals of IFRS.

IASB(International accounting standards boards)

The IASB has full control over developing and setting its own agenda this will

focuses on making better statements (Pratt, 2013). Some new standards for lease and revenue

recognition are their for lease and other related services. On the other side it focuses to record

better financial statements.

1.3 Implications for users of regulatory bodies

Different regulatory bodies deals with the different companies to which proper

accounts should be maintained and all the entities have to make statements according to their

rules and regulations (Schroeder, Clark, and Cathey, 2011). GAAP deals with domestic

entities in which no specific rules are their for sole proprietor and limited company. IFRS

have some better and different rules for each company that focus on true and fair view of

statements of accounts by the companies. IFRS adoption will be beneficial to the investors

and other users because it reduces the cost of comparing alternative investment and also

increases the quality of information which is provided by the companies (Gassen and

Schwedler, 2010). Entities which have higher level of international activities will be

benefited by adoption of IFRS. On the other side IASB is a independent accounting standard

which is setting body of IFRS. Single set of accounts are developed for the business who

does overseas business transactions. According to companies act each and every transaction

have to be maintained separately. Apart from this financial company who holds 51% shares

have to prepare a consolidated financial statement otherwise default officers will be

penalized. Every account should be maintained according to set of regulations of companies

act. Different companies have to manages accounts separately but after IFRS there is a lot of

improvement in accounts and the reliability of its data (Henderson and et.al., 2013).

1.4 Different laws and regulations deals with accounting and reporting standards

As per the regulatory framework of UK all the business entities have to manage their

accounts as per the provisions of regulatory bodies (Schroeder, Clark and Cathey, 2013).

Companies Act,2006

GAAP is the generally accepted accounting principles according to which an business

entity have to maintain their accounts. It includes the rules,regulations and convention of

accounts. It basically deals with the domestic accounting principle not like international

accounting principals of IFRS.

IASB(International accounting standards boards)

The IASB has full control over developing and setting its own agenda this will

focuses on making better statements (Pratt, 2013). Some new standards for lease and revenue

recognition are their for lease and other related services. On the other side it focuses to record

better financial statements.

1.3 Implications for users of regulatory bodies

Different regulatory bodies deals with the different companies to which proper

accounts should be maintained and all the entities have to make statements according to their

rules and regulations (Schroeder, Clark, and Cathey, 2011). GAAP deals with domestic

entities in which no specific rules are their for sole proprietor and limited company. IFRS

have some better and different rules for each company that focus on true and fair view of

statements of accounts by the companies. IFRS adoption will be beneficial to the investors

and other users because it reduces the cost of comparing alternative investment and also

increases the quality of information which is provided by the companies (Gassen and

Schwedler, 2010). Entities which have higher level of international activities will be

benefited by adoption of IFRS. On the other side IASB is a independent accounting standard

which is setting body of IFRS. Single set of accounts are developed for the business who

does overseas business transactions. According to companies act each and every transaction

have to be maintained separately. Apart from this financial company who holds 51% shares

have to prepare a consolidated financial statement otherwise default officers will be

penalized. Every account should be maintained according to set of regulations of companies

act. Different companies have to manages accounts separately but after IFRS there is a lot of

improvement in accounts and the reliability of its data (Henderson and et.al., 2013).

1.4 Different laws and regulations deals with accounting and reporting standards

As per the regulatory framework of UK all the business entities have to manage their

accounts as per the provisions of regulatory bodies (Schroeder, Clark and Cathey, 2013).

Companies Act,2006

This act deals with both pubic and private limited companies across the country.

Number of provision are their according to which the companies have to maintain their

accounts properly that must contain have true and reliable data in which every financial

transaction should be mentioned separately. Apart from this the accountant have to records

each business transaction. Other than this consolidates statements have to be prepared by the

parent company holding 51% shares or more than that.

UK GAAP

Generally accepted accounting principals are the basic accounting principles on the

base of which accounts of an entity has to be prepared. It has a set of rules,guidelines and

principals to which a business have to maintain their accounts. These principals bring

comparability in the statements (Kimmel, Weygandt, and Kieso, 2010).

IASB

It is an independent,private sector body that develops the international financial

reporting standards. It determines that how each and every business transaction have to be

reported in financial statements. Basically it guides on the reporting structures of financial

transactions.

IFRS

It is the international financial reporting system that deals with the global accounting

system which compare the overseas financial statements of an organization (May, 2013). It is

difficult to understand the structure of different countries for this IFRS improves the

accounting practices to make their users comfortable to understand and analyze the

performance of the business.

3.1 Information needs of different user group vary

For an organization different user groups are their who needs the information of the

business for their own purposes. A company has both internal and external groups who needs

the information of business. Internal groups are those which are directly in touch with the

organization says employees,managers etc. On the other side external groups includes the

customers,suppliers and investors.

Owners

Owner needs the information to determine the financial stability of the business in the

different changing situation. They analyze through the information whether the business is

Number of provision are their according to which the companies have to maintain their

accounts properly that must contain have true and reliable data in which every financial

transaction should be mentioned separately. Apart from this the accountant have to records

each business transaction. Other than this consolidates statements have to be prepared by the

parent company holding 51% shares or more than that.

UK GAAP

Generally accepted accounting principals are the basic accounting principles on the

base of which accounts of an entity has to be prepared. It has a set of rules,guidelines and

principals to which a business have to maintain their accounts. These principals bring

comparability in the statements (Kimmel, Weygandt, and Kieso, 2010).

IASB

It is an independent,private sector body that develops the international financial

reporting standards. It determines that how each and every business transaction have to be

reported in financial statements. Basically it guides on the reporting structures of financial

transactions.

IFRS

It is the international financial reporting system that deals with the global accounting

system which compare the overseas financial statements of an organization (May, 2013). It is

difficult to understand the structure of different countries for this IFRS improves the

accounting practices to make their users comfortable to understand and analyze the

performance of the business.

3.1 Information needs of different user group vary

For an organization different user groups are their who needs the information of the

business for their own purposes. A company has both internal and external groups who needs

the information of business. Internal groups are those which are directly in touch with the

organization says employees,managers etc. On the other side external groups includes the

customers,suppliers and investors.

Owners

Owner needs the information to determine the financial stability of the business in the

different changing situation. They analyze through the information whether the business is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profitable or not for them and on base of that they decides whether to continue ,improve or

drop it.

Customers

When the customer has a long term contract with the company, he needs the

information of stability of the company in the market and ability to provide better services

(Samphantharak and Townsend, 2010). Customer is always interested in information to

determine the changes in price of the product and find the best quality of the product.

General public

It includes the researchers, students, analysts which are interested in collecting the

information for their personal needs like market study or to compare the graph of the

companies to make a report on different organizations.

Trade creditors

Like lenders trade creditors are also interested in the ability of organization to pay the

obligations towards them at the time when they become due.

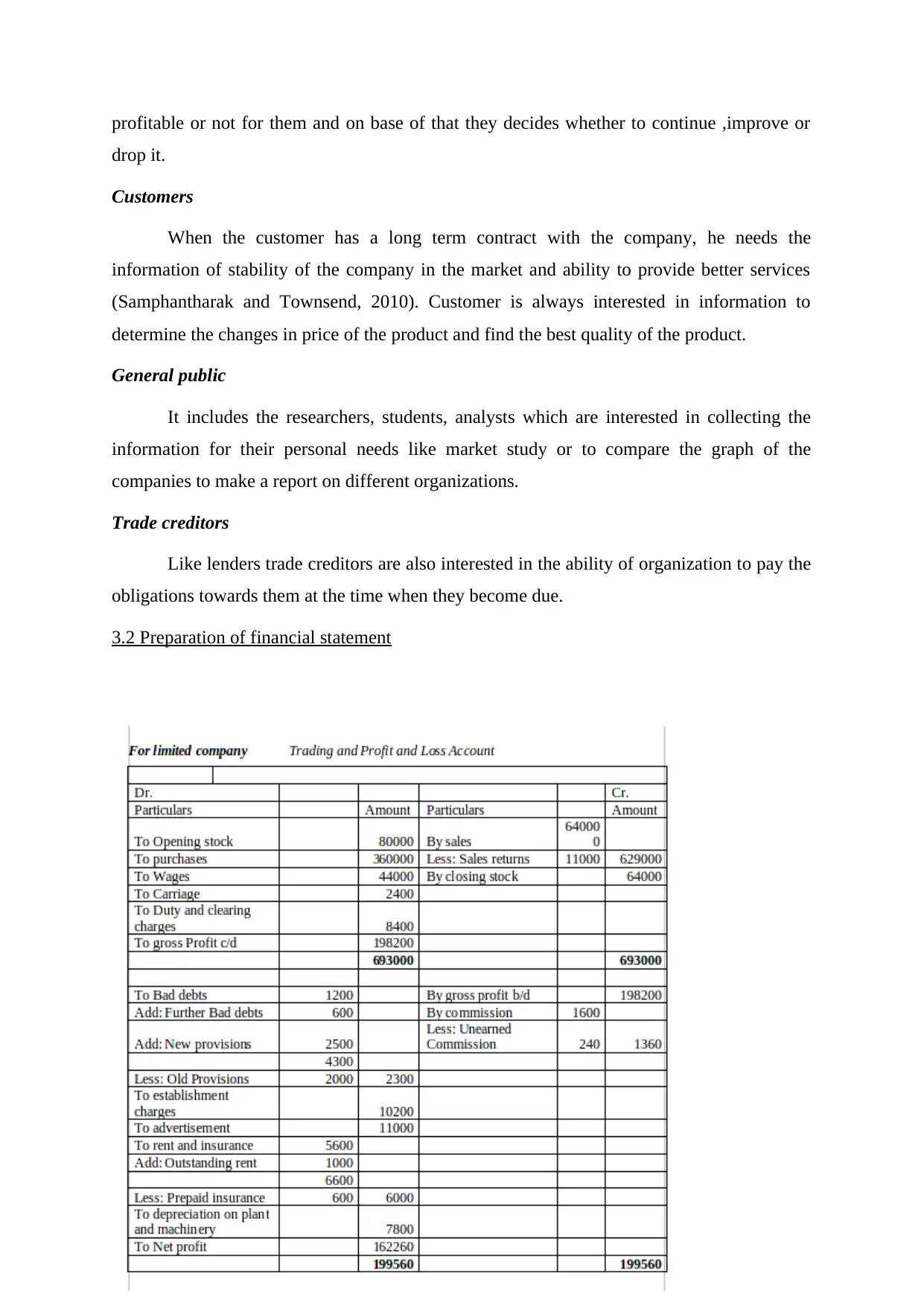

3.2 Preparation of financial statement

drop it.

Customers

When the customer has a long term contract with the company, he needs the

information of stability of the company in the market and ability to provide better services

(Samphantharak and Townsend, 2010). Customer is always interested in information to

determine the changes in price of the product and find the best quality of the product.

General public

It includes the researchers, students, analysts which are interested in collecting the

information for their personal needs like market study or to compare the graph of the

companies to make a report on different organizations.

Trade creditors

Like lenders trade creditors are also interested in the ability of organization to pay the

obligations towards them at the time when they become due.

3.2 Preparation of financial statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

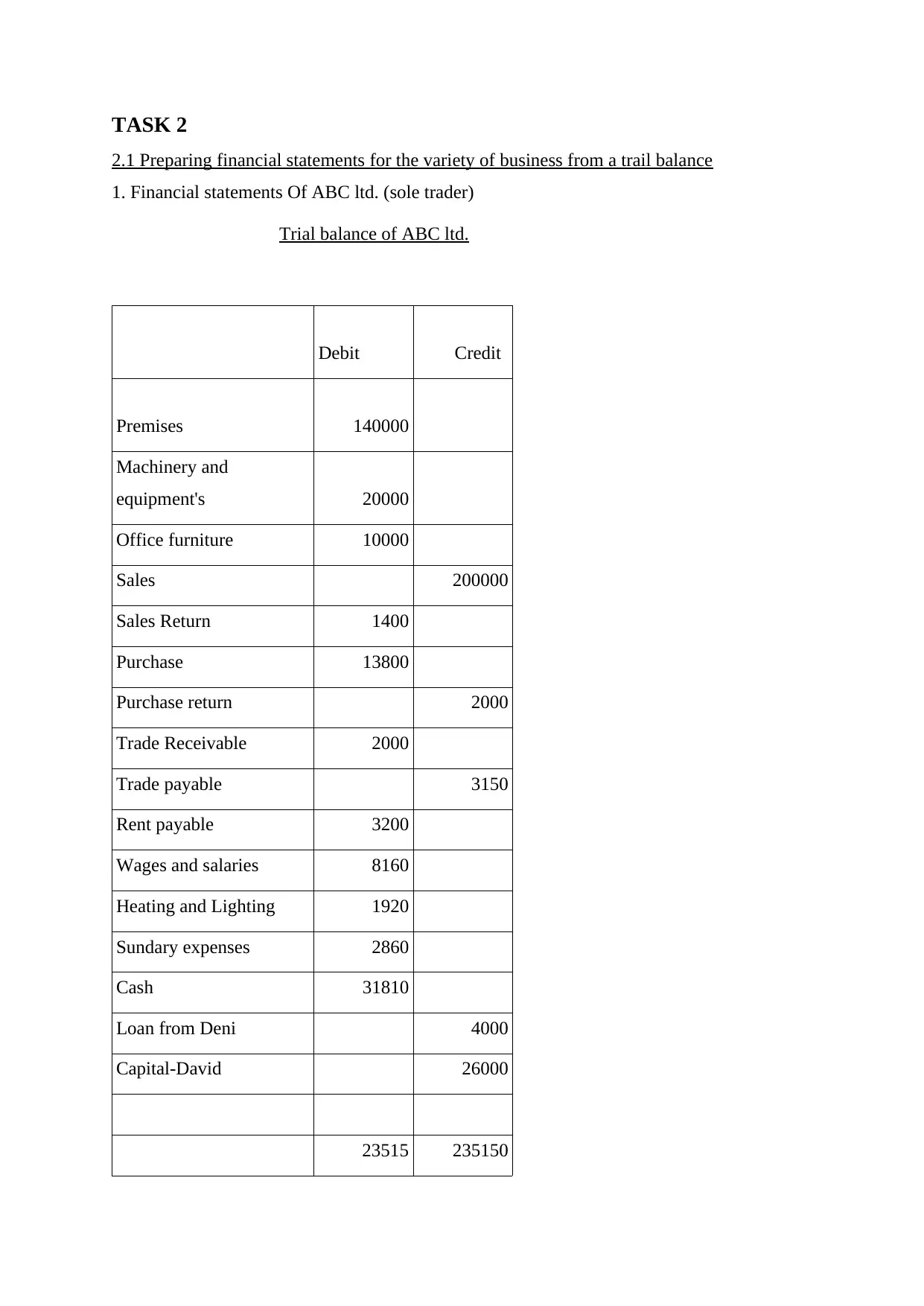

TASK 2

2.1 Preparing financial statements for the variety of business from a trail balance

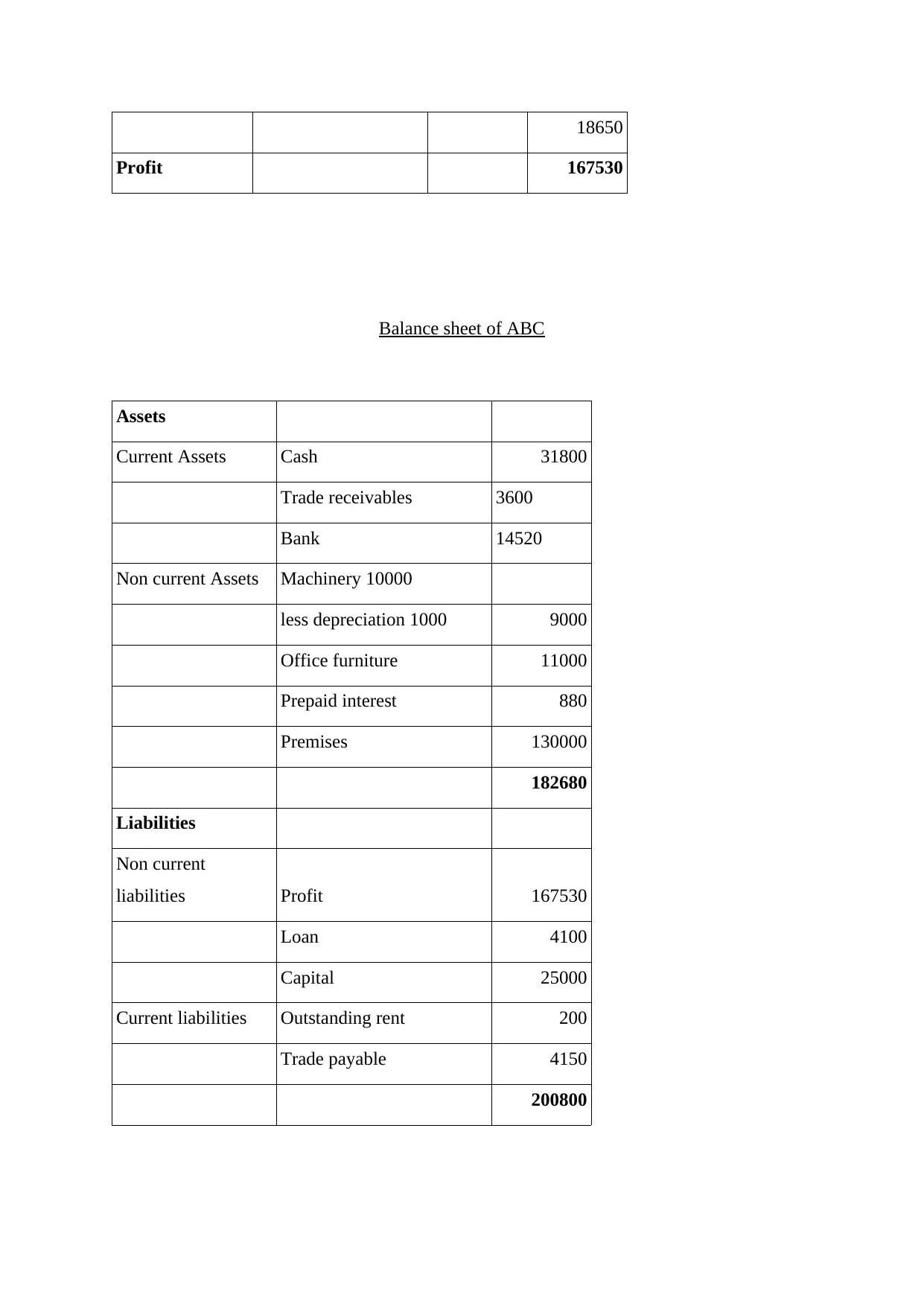

1. Financial statements Of ABC ltd. (sole trader)

Trial balance of ABC ltd.

Debit Credit

Premises 140000

Machinery and

equipment's 20000

Office furniture 10000

Sales 200000

Sales Return 1400

Purchase 13800

Purchase return 2000

Trade Receivable 2000

Trade payable 3150

Rent payable 3200

Wages and salaries 8160

Heating and Lighting 1920

Sundary expenses 2860

Cash 31810

Loan from Deni 4000

Capital-David 26000

23515 235150

2.1 Preparing financial statements for the variety of business from a trail balance

1. Financial statements Of ABC ltd. (sole trader)

Trial balance of ABC ltd.

Debit Credit

Premises 140000

Machinery and

equipment's 20000

Office furniture 10000

Sales 200000

Sales Return 1400

Purchase 13800

Purchase return 2000

Trade Receivable 2000

Trade payable 3150

Rent payable 3200

Wages and salaries 8160

Heating and Lighting 1920

Sundary expenses 2860

Cash 31810

Loan from Deni 4000

Capital-David 26000

23515 235150

0

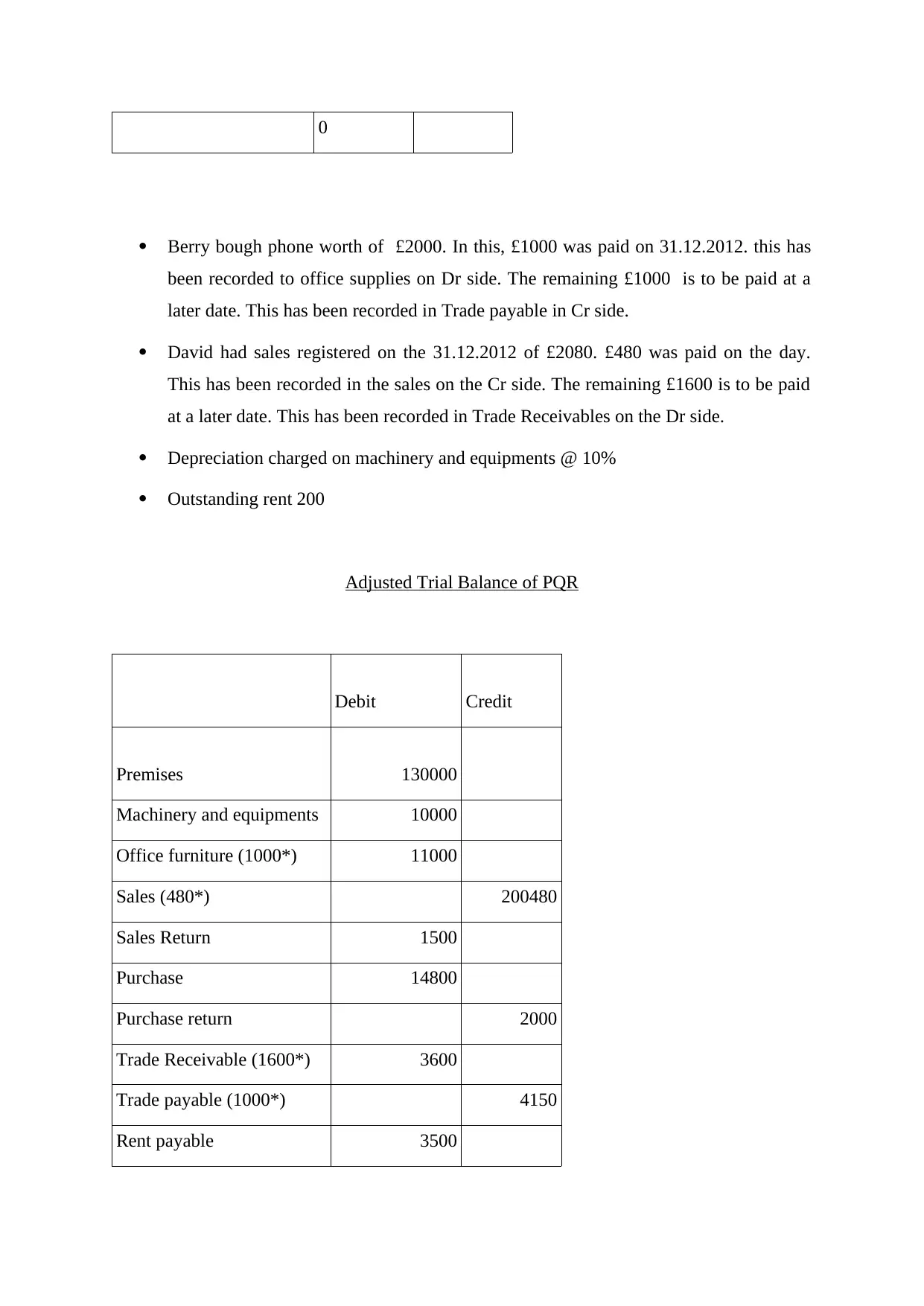

Berry bough phone worth of £2000. In this, £1000 was paid on 31.12.2012. this has

been recorded to office supplies on Dr side. The remaining £1000 is to be paid at a

later date. This has been recorded in Trade payable in Cr side.

David had sales registered on the 31.12.2012 of £2080. £480 was paid on the day.

This has been recorded in the sales on the Cr side. The remaining £1600 is to be paid

at a later date. This has been recorded in Trade Receivables on the Dr side.

Depreciation charged on machinery and equipments @ 10%

Outstanding rent 200

Adjusted Trial Balance of PQR

Debit Credit

Premises 130000

Machinery and equipments 10000

Office furniture (1000*) 11000

Sales (480*) 200480

Sales Return 1500

Purchase 14800

Purchase return 2000

Trade Receivable (1600*) 3600

Trade payable (1000*) 4150

Rent payable 3500

Berry bough phone worth of £2000. In this, £1000 was paid on 31.12.2012. this has

been recorded to office supplies on Dr side. The remaining £1000 is to be paid at a

later date. This has been recorded in Trade payable in Cr side.

David had sales registered on the 31.12.2012 of £2080. £480 was paid on the day.

This has been recorded in the sales on the Cr side. The remaining £1600 is to be paid

at a later date. This has been recorded in Trade Receivables on the Dr side.

Depreciation charged on machinery and equipments @ 10%

Outstanding rent 200

Adjusted Trial Balance of PQR

Debit Credit

Premises 130000

Machinery and equipments 10000

Office furniture (1000*) 11000

Sales (480*) 200480

Sales Return 1500

Purchase 14800

Purchase return 2000

Trade Receivable (1600*) 3600

Trade payable (1000*) 4150

Rent payable 3500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wages and salaries 8200

Heating and Lighting 1900

Sundary expenses 2850

Cash 31800 12520

Loan from Sam 4100 4100

Capital 25000 25000

24825

0 248250

Profit and loss account of PQR

Sales

(- ) Sales return

200480

1500 198980

COGS

(Purchases)

(-) Purchase

return (14800-2000) 12800

186180

Expenses

Sundry 2850

Rent 3500

Add outstanding 200 3700

Wages 8200

Lighting and heat 1900

Depreciation 1000

Interest rate 1880

Less: Prepaid exp

(880) 1000

Heating and Lighting 1900

Sundary expenses 2850

Cash 31800 12520

Loan from Sam 4100 4100

Capital 25000 25000

24825

0 248250

Profit and loss account of PQR

Sales

(- ) Sales return

200480

1500 198980

COGS

(Purchases)

(-) Purchase

return (14800-2000) 12800

186180

Expenses

Sundry 2850

Rent 3500

Add outstanding 200 3700

Wages 8200

Lighting and heat 1900

Depreciation 1000

Interest rate 1880

Less: Prepaid exp

(880) 1000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

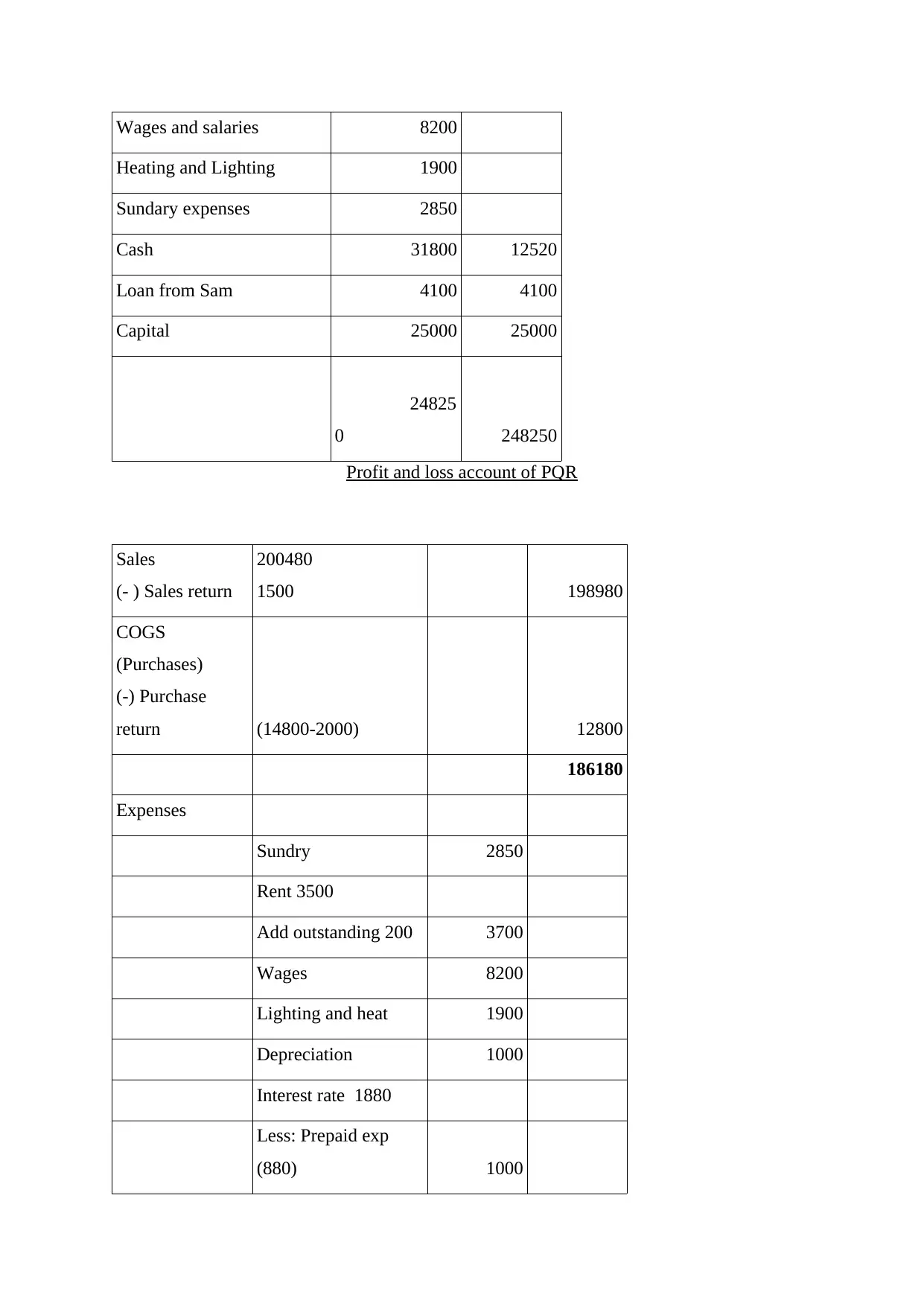

18650

Profit 167530

Balance sheet of ABC

Assets

Current Assets Cash 31800

Trade receivables 3600

Bank 14520

Non current Assets Machinery 10000

less depreciation 1000 9000

Office furniture 11000

Prepaid interest 880

Premises 130000

182680

Liabilities

Non current

liabilities Profit 167530

Loan 4100

Capital 25000

Current liabilities Outstanding rent 200

Trade payable 4150

200800

Profit 167530

Balance sheet of ABC

Assets

Current Assets Cash 31800

Trade receivables 3600

Bank 14520

Non current Assets Machinery 10000

less depreciation 1000 9000

Office furniture 11000

Prepaid interest 880

Premises 130000

182680

Liabilities

Non current

liabilities Profit 167530

Loan 4100

Capital 25000

Current liabilities Outstanding rent 200

Trade payable 4150

200800

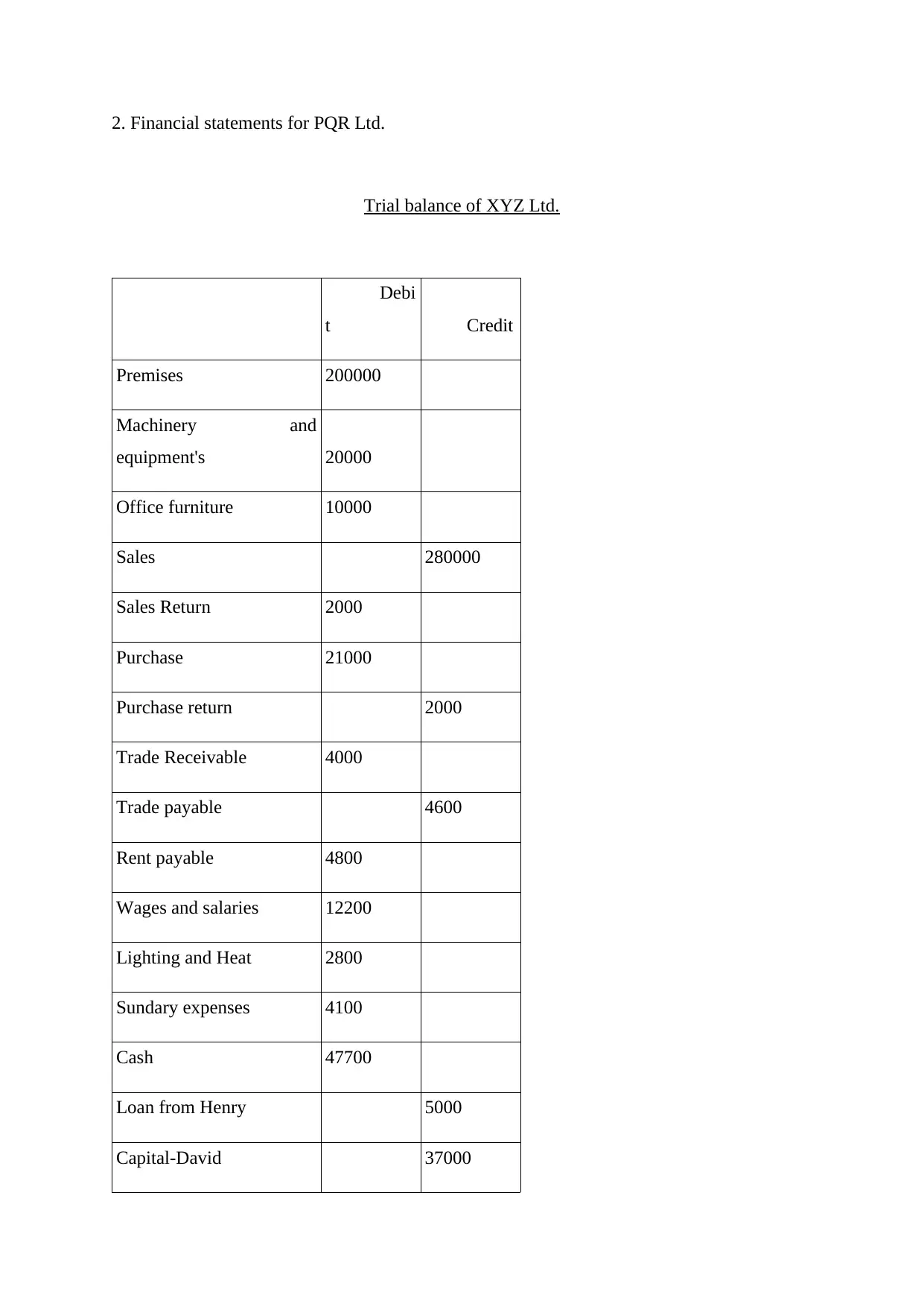

2. Financial statements for PQR Ltd.

Trial balance of XYZ Ltd.

Debi

t Credit

Premises 200000

Machinery and

equipment's 20000

Office furniture 10000

Sales 280000

Sales Return 2000

Purchase 21000

Purchase return 2000

Trade Receivable 4000

Trade payable 4600

Rent payable 4800

Wages and salaries 12200

Lighting and Heat 2800

Sundary expenses 4100

Cash 47700

Loan from Henry 5000

Capital-David 37000

Trial balance of XYZ Ltd.

Debi

t Credit

Premises 200000

Machinery and

equipment's 20000

Office furniture 10000

Sales 280000

Sales Return 2000

Purchase 21000

Purchase return 2000

Trade Receivable 4000

Trade payable 4600

Rent payable 4800

Wages and salaries 12200

Lighting and Heat 2800

Sundary expenses 4100

Cash 47700

Loan from Henry 5000

Capital-David 37000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.