Financial Accounting Project: Sole Trader and Limited Companies

VerifiedAdded on 2020/10/22

|17

|1746

|80

Project

AI Summary

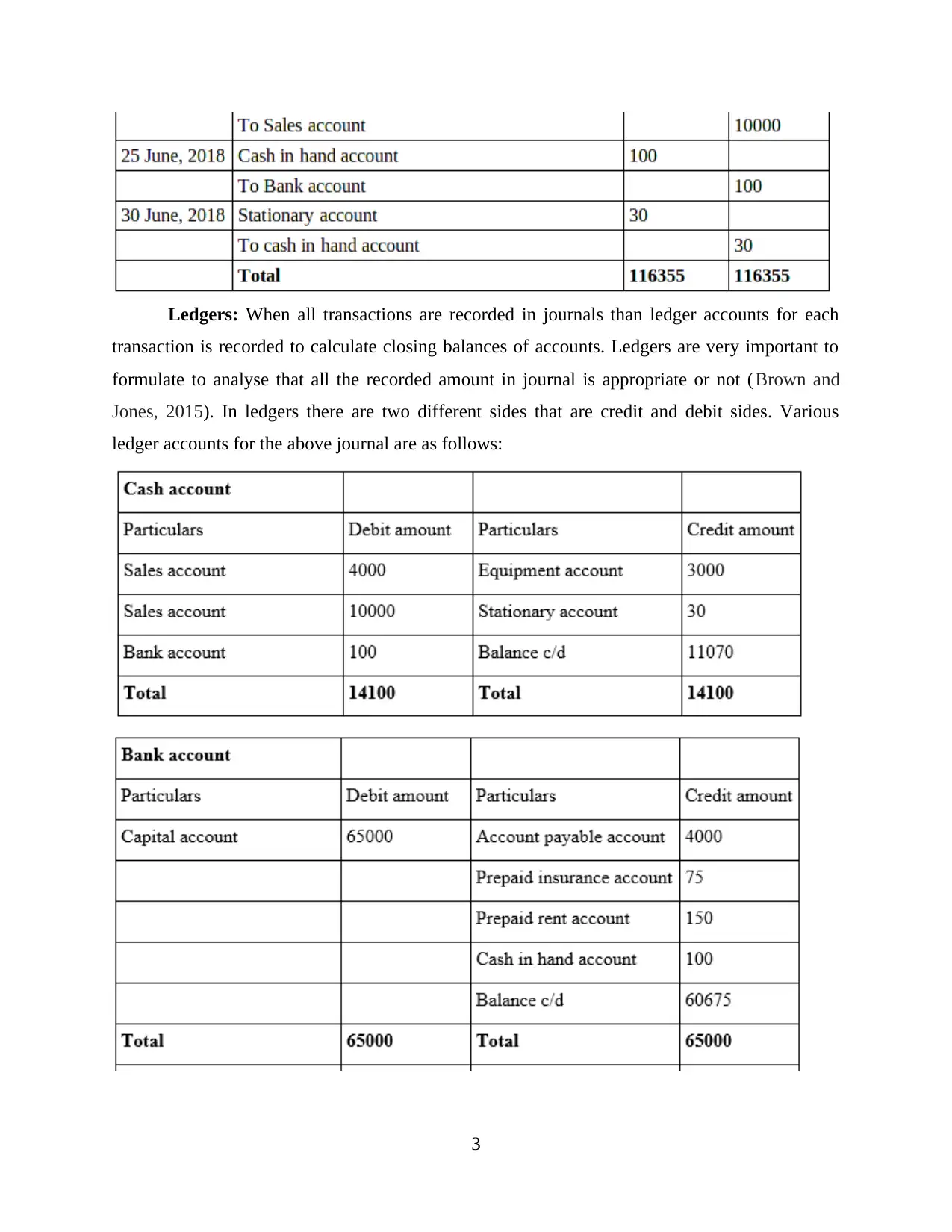

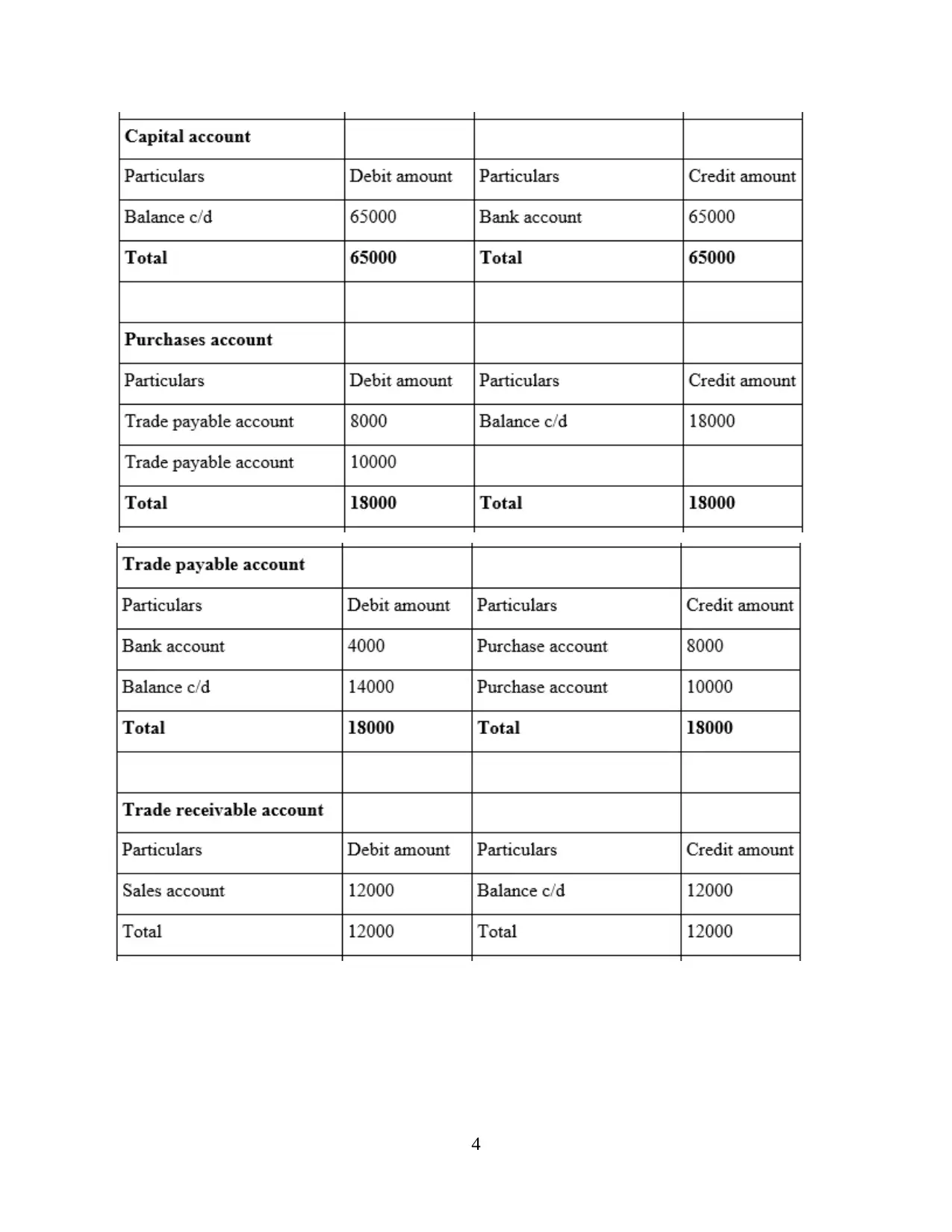

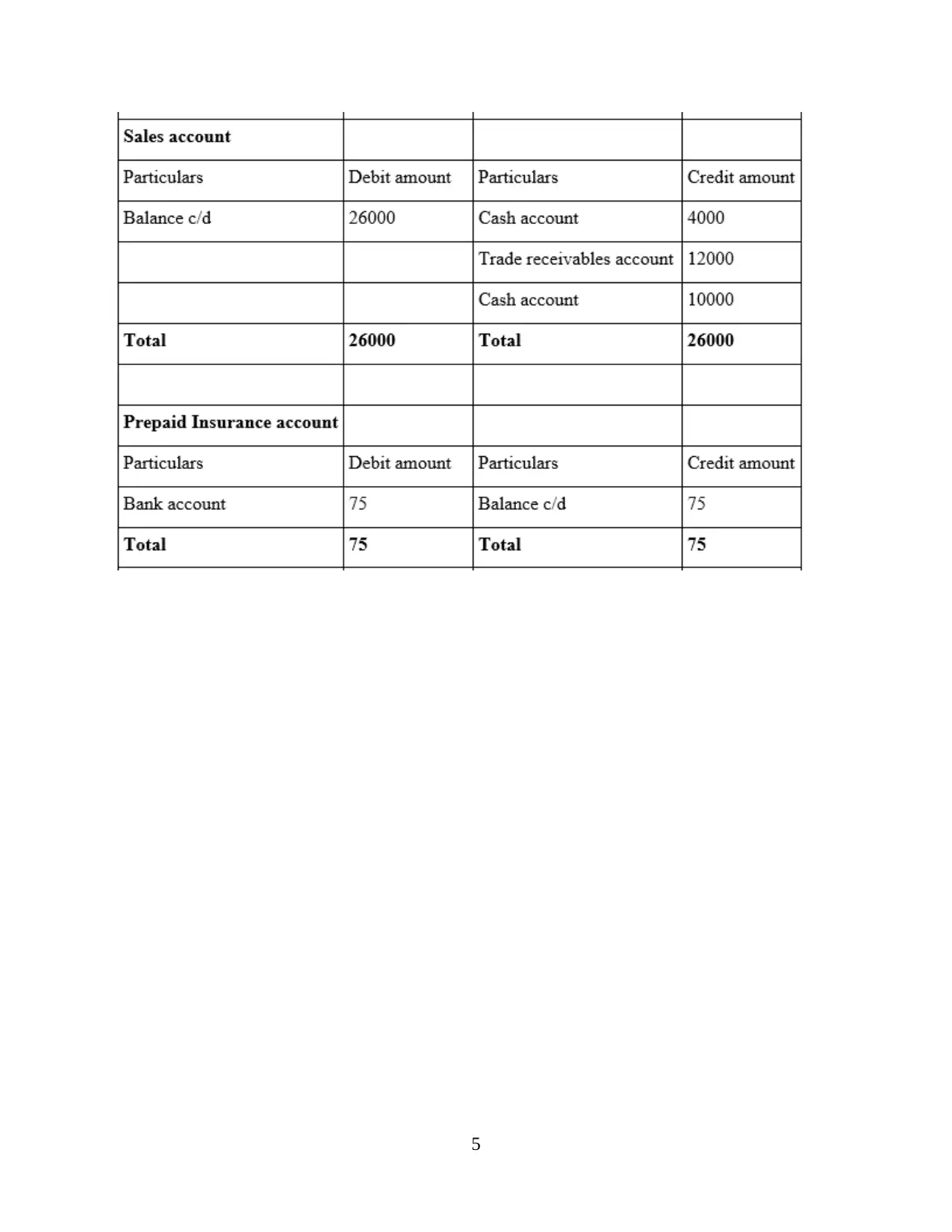

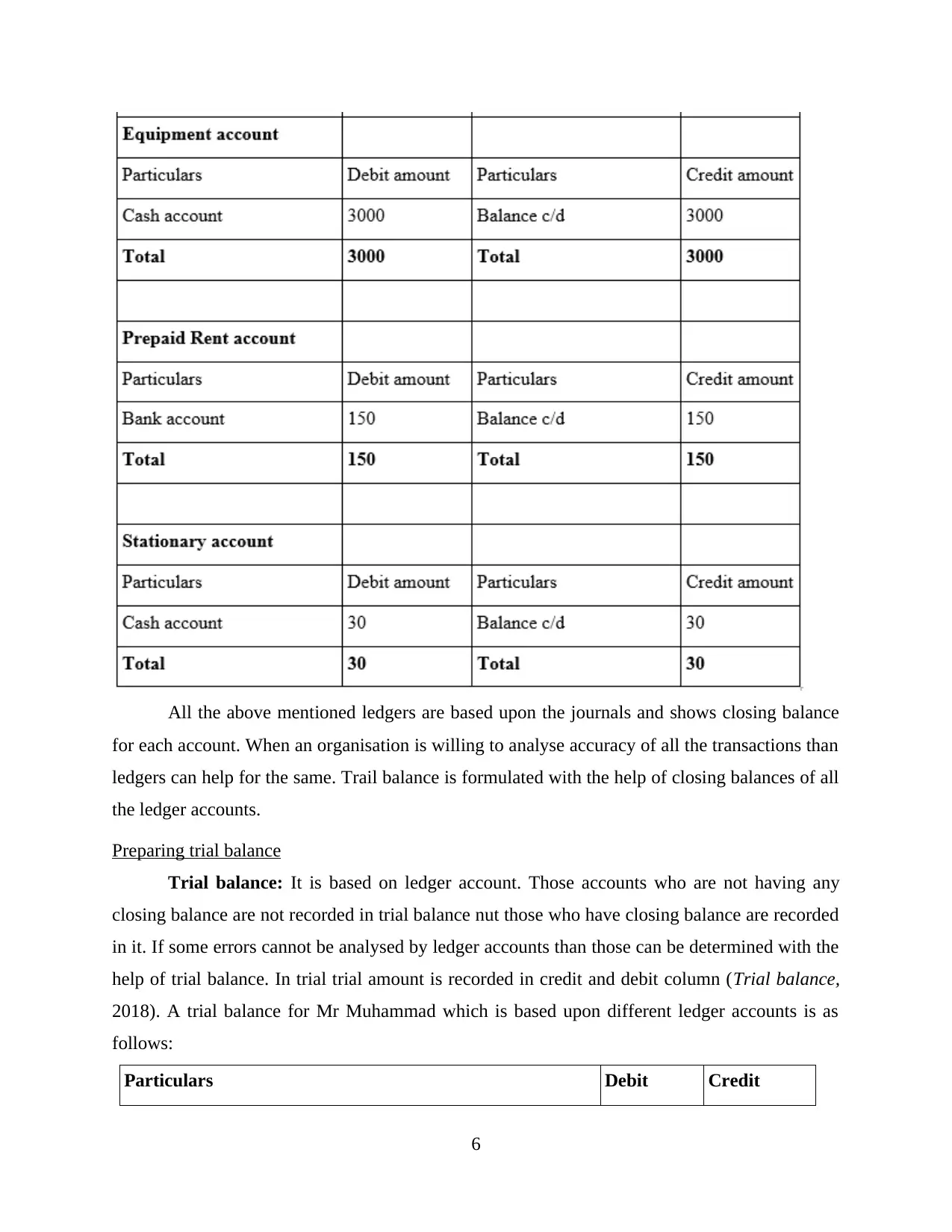

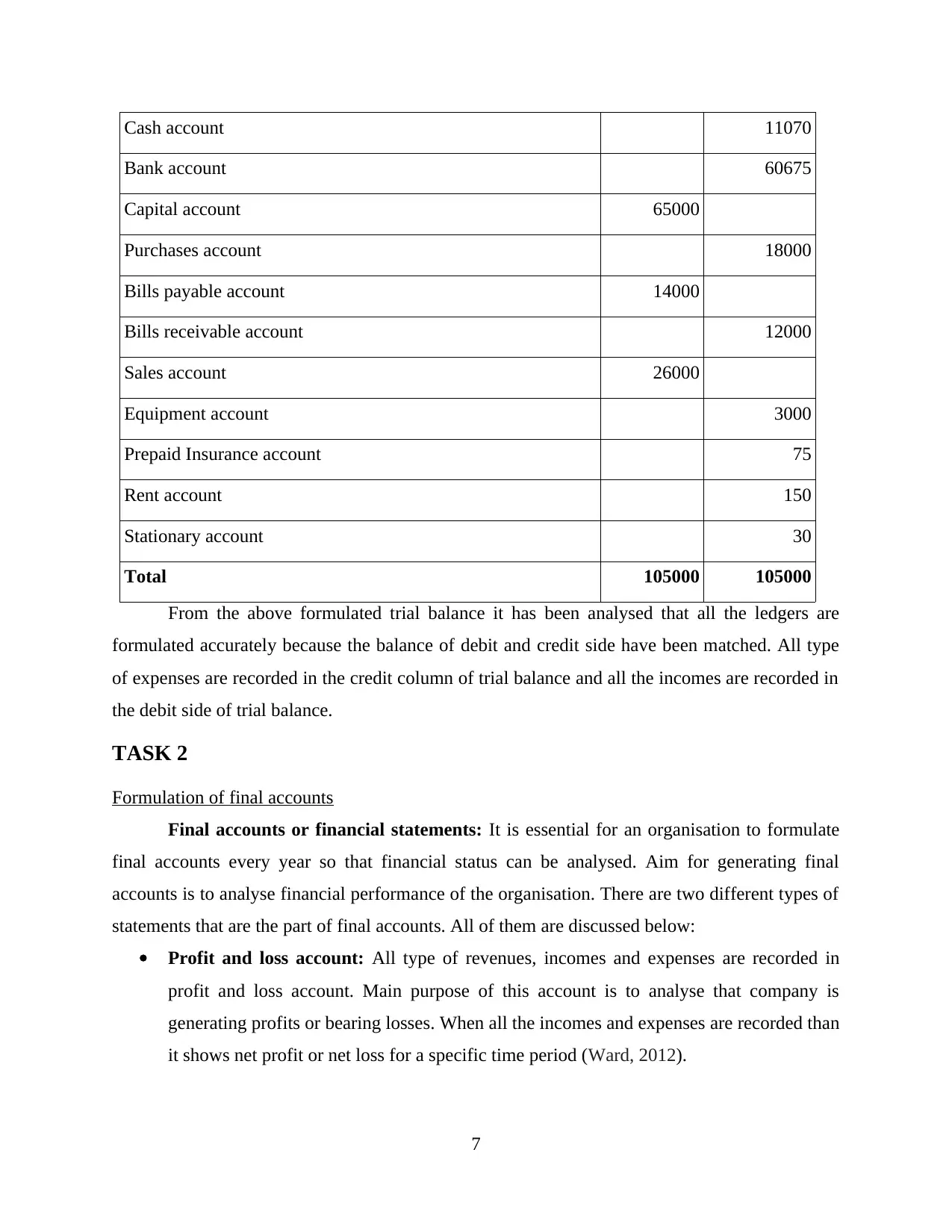

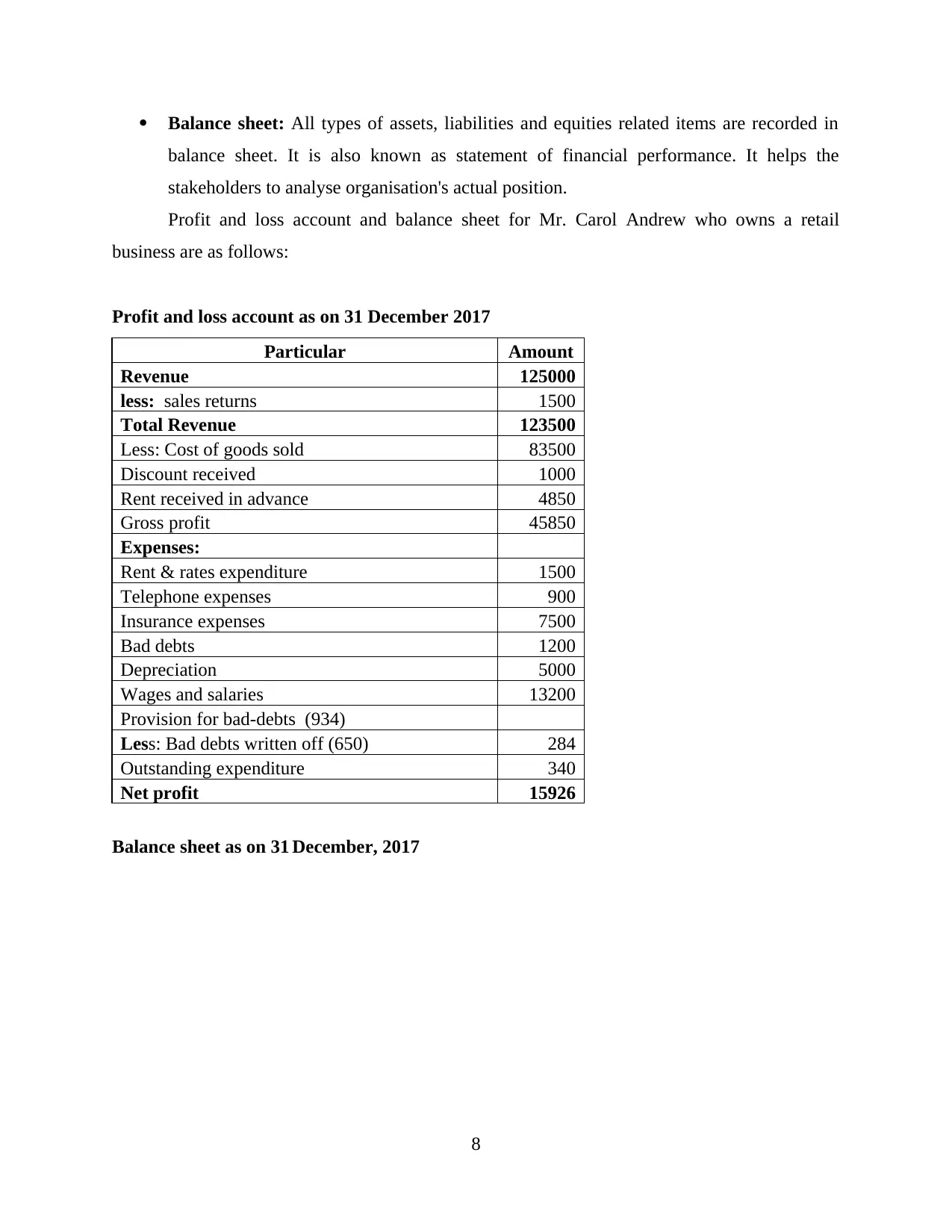

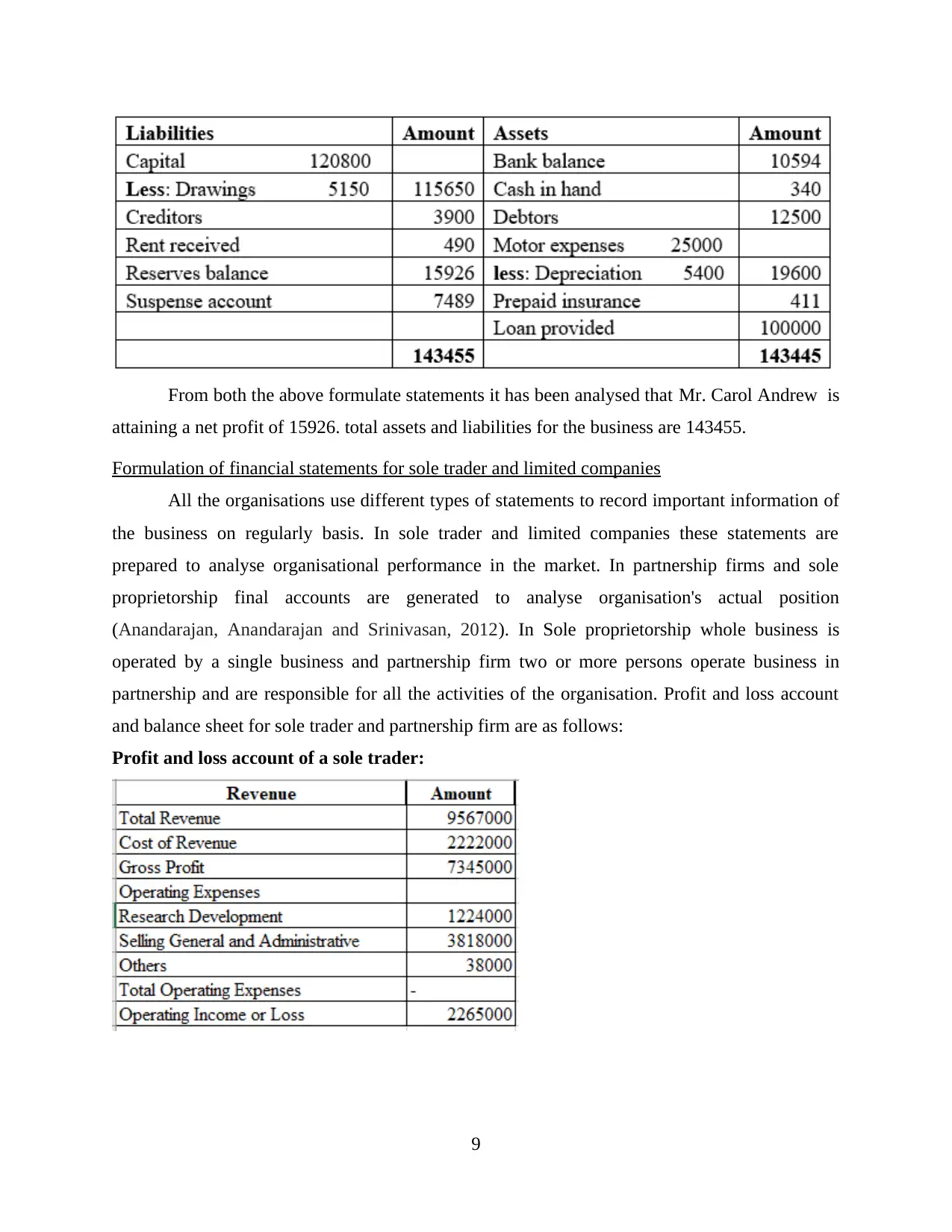

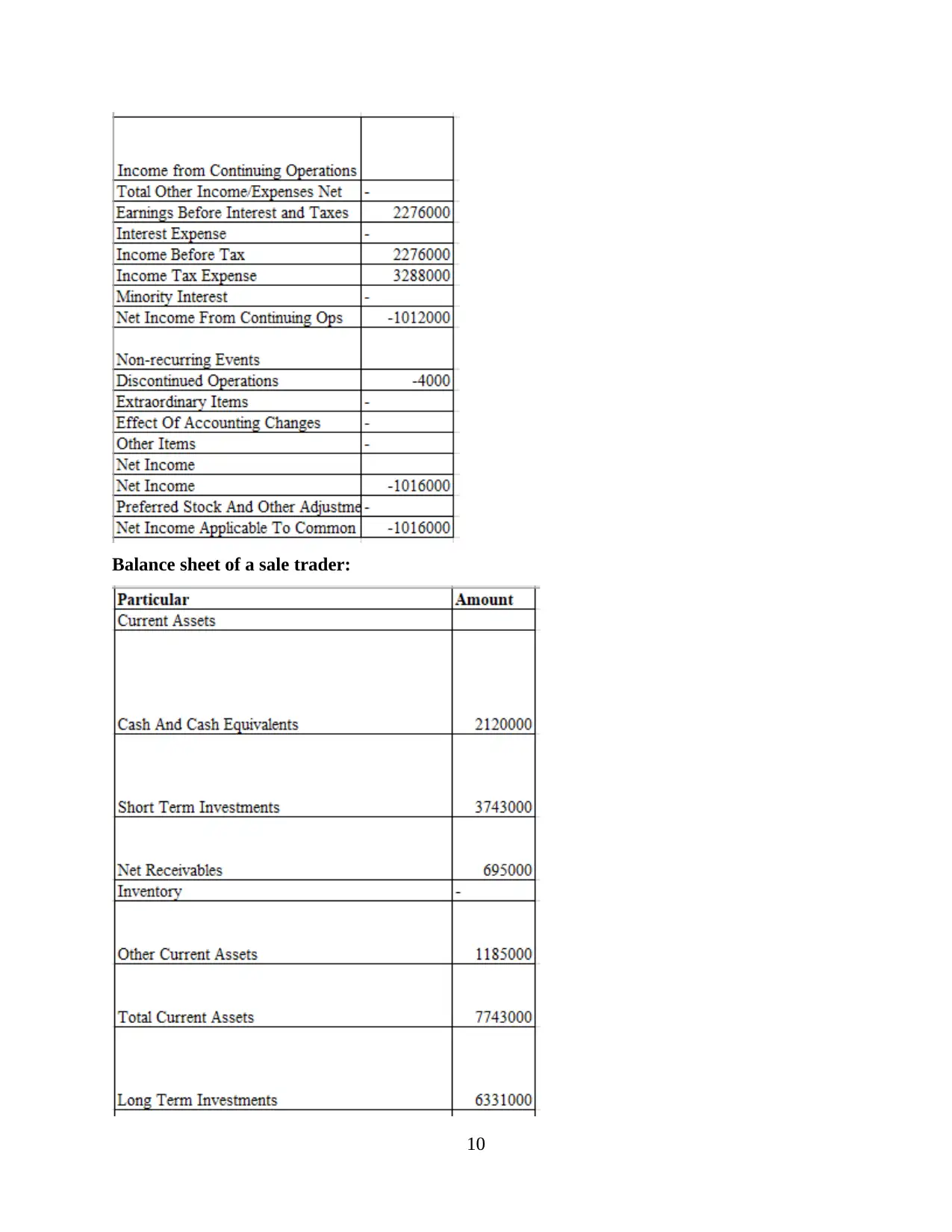

This project report delves into the core concepts of financial accounting, beginning with the double-entry bookkeeping system and its application in recording business transactions through journals and ledgers. It then proceeds to the preparation of a trial balance, ensuring the accuracy of recorded financial data. The project further explores the formulation of final accounts, including profit and loss accounts and balance sheets, crucial for assessing an organization's financial performance. The report contrasts financial statement preparation for sole traders and limited companies, highlighting the differences in accounting practices. It concludes by emphasizing the importance of accurate financial record-keeping for all types of businesses, providing a comprehensive overview of fundamental accounting principles and their practical application in financial statement analysis.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.