Financial Performance Analysis: Tesco and Sainsbury Comparison

VerifiedAdded on 2019/12/03

|12

|2806

|110

Report

AI Summary

This report presents a financial analysis of Tesco and Sainsbury, two major retail companies. It examines their financial statements, including income statements and balance sheets, to assess their profitability, liquidity, efficiency, and solvency. The analysis involves calculating and interpreting various financial ratios such as gross profit ratio, operating profit ratio, current ratio, quick ratio, total assets turnover ratio, inventory turnover ratio, debt-equity ratio, and times interest ratio. The report compares the financial performance of both companies over a period of time, highlighting trends and providing insights into how different users of financial statements, including managers, shareholders, employees, government, financial institutions, and investors, might interpret the results. The report concludes with a summary of the key findings and their implications for the stakeholders. This analysis helps understand the financial health and performance of Tesco and Sainsbury, offering valuable information for decision-making.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................1

Users of financial statements............................................................................................1

Analysis of financial statements of Sainsbury for different users....................................2

Analysis of financial statements of Tesco for different users...........................................6

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

INTRODUCTION................................................................................................................................1

Users of financial statements............................................................................................1

Analysis of financial statements of Sainsbury for different users....................................2

Analysis of financial statements of Tesco for different users...........................................6

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

INDEX OF TABLES

Table 1: Financial statements - Sainsbury...........................................................................................2

Table 2: Ratio Analysis- Tesco............................................................................................................4

Table 1: Financial statements - Sainsbury...........................................................................................2

Table 2: Ratio Analysis- Tesco............................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every organization prepares its financial statements in the form of income statements and

balance sheet. Income statement shows the profitability of business whereas balance sheet shows the

financial position of it (Scott, 2014). There are different users of financial statements such as

customers, employees, managers, government and investors. Moreover, their needs about the

financial information of company also tend to vary. Therefore, financial statements should satisfy

the needs of different users by providing useful information to them. In addition to it, it can also be

used for the analysis purpose between two or more companies. In this report, the financial

statements of Tesco and Sainsbury will be discussed as both are retail sector companies and explain

the way in which organization’s financial statements satisfy its users.

Users of financial statements

The objective of financial statements is to provide information about the financial position

as well as performance of organization. The information is considered to be useful for the users in

making economic decisions (Schroeder, Clark and Cathey, 2011). There are mainly two groups of

users, that is, internal as well as external.

Internal Users: Internal users are the part of company’s operating activities such as

managers, owners and employees.

Managers: They require financial statements so as to increase the profitability as well as

financial position of business. In Tesco and Sainsbury, management includes board of directors,

operating board and the committees. Board of directors are responsible to create long term

sustainable value for its shareholders by an effective and strategic planning (Edwards, 2013).

However, operating board is responsible to manage day to day operating activities of company.

Owners: Shareholders are the owners of organization. They make investment in the form of

shares with an objective of high return and capital appreciation. Tesco and Sainsbury collect its

funds by issuing the share capital. They need financial information to know the profitability of

business and to take necessary decisions about their invested funds.

Employees: Employees are very much concerned about the job security, high salary and

their employment terms (Ibson, 2008). Therefore, they want to know Tesco and Sainsbury’s

stability and profitability position.

External Users: External users are considered as the outsiders for organization such as

government, financial institutions and investors (Stickney and et.al., 2009)

Government: Government needs the accounting information of both companies for the

purpose of economic growth. They want to know the correctness of tax declared by Tesco and

1 | P a g e

Every organization prepares its financial statements in the form of income statements and

balance sheet. Income statement shows the profitability of business whereas balance sheet shows the

financial position of it (Scott, 2014). There are different users of financial statements such as

customers, employees, managers, government and investors. Moreover, their needs about the

financial information of company also tend to vary. Therefore, financial statements should satisfy

the needs of different users by providing useful information to them. In addition to it, it can also be

used for the analysis purpose between two or more companies. In this report, the financial

statements of Tesco and Sainsbury will be discussed as both are retail sector companies and explain

the way in which organization’s financial statements satisfy its users.

Users of financial statements

The objective of financial statements is to provide information about the financial position

as well as performance of organization. The information is considered to be useful for the users in

making economic decisions (Schroeder, Clark and Cathey, 2011). There are mainly two groups of

users, that is, internal as well as external.

Internal Users: Internal users are the part of company’s operating activities such as

managers, owners and employees.

Managers: They require financial statements so as to increase the profitability as well as

financial position of business. In Tesco and Sainsbury, management includes board of directors,

operating board and the committees. Board of directors are responsible to create long term

sustainable value for its shareholders by an effective and strategic planning (Edwards, 2013).

However, operating board is responsible to manage day to day operating activities of company.

Owners: Shareholders are the owners of organization. They make investment in the form of

shares with an objective of high return and capital appreciation. Tesco and Sainsbury collect its

funds by issuing the share capital. They need financial information to know the profitability of

business and to take necessary decisions about their invested funds.

Employees: Employees are very much concerned about the job security, high salary and

their employment terms (Ibson, 2008). Therefore, they want to know Tesco and Sainsbury’s

stability and profitability position.

External Users: External users are considered as the outsiders for organization such as

government, financial institutions and investors (Stickney and et.al., 2009)

Government: Government needs the accounting information of both companies for the

purpose of economic growth. They want to know the correctness of tax declared by Tesco and

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sainsbury in the tax return. Government also tracks economic progress by analyzing the financial

statements of different sectors of economy.

Financial Institutions: Banks provide credit facility to Tesco and Sainsbury for various

purposes. Hence, they use financial statement to know the financial health of business and take

effective decision for lending purpose (Lebas and Stolowy, 2006).

Investors: Investors make investment in company with the purpose of generating high

return. They predict expected dividend and the risk factor associated with the investment (Wantao

and Ramanathan, 2008). Hence, they need financial statements of Tesco and Sainsbury to know the

profitability and also the fluctuations in profits.

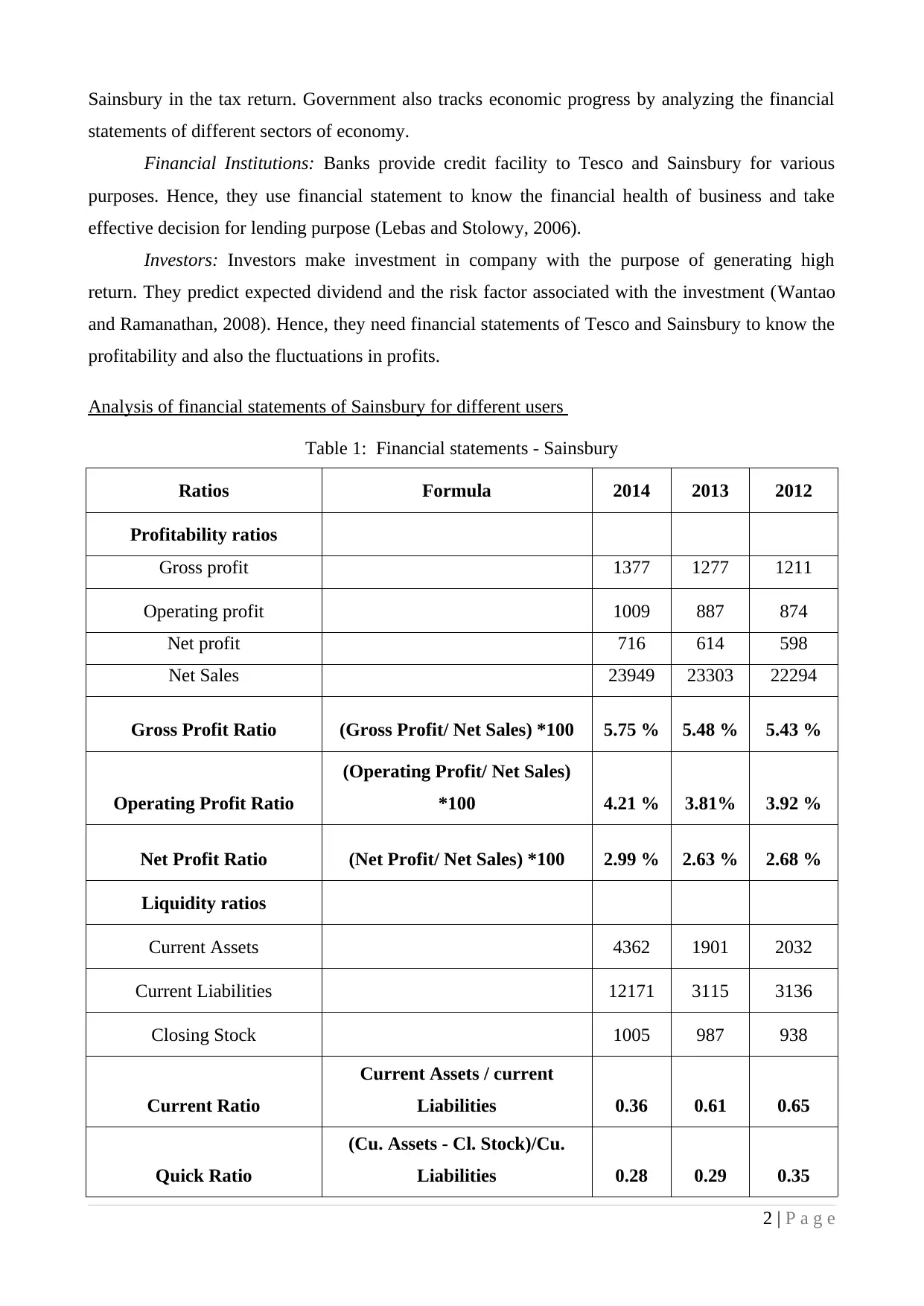

Analysis of financial statements of Sainsbury for different users

Table 1: Financial statements - Sainsbury

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 1377 1277 1211

Operating profit 1009 887 874

Net profit 716 614 598

Net Sales 23949 23303 22294

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 % 5.43 %

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 4.21 % 3.81% 3.92 %

Net Profit Ratio (Net Profit/ Net Sales) *100 2.99 % 2.63 % 2.68 %

Liquidity ratios

Current Assets 4362 1901 2032

Current Liabilities 12171 3115 3136

Closing Stock 1005 987 938

Current Ratio

Current Assets / current

Liabilities 0.36 0.61 0.65

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29 0.35

2 | P a g e

statements of different sectors of economy.

Financial Institutions: Banks provide credit facility to Tesco and Sainsbury for various

purposes. Hence, they use financial statement to know the financial health of business and take

effective decision for lending purpose (Lebas and Stolowy, 2006).

Investors: Investors make investment in company with the purpose of generating high

return. They predict expected dividend and the risk factor associated with the investment (Wantao

and Ramanathan, 2008). Hence, they need financial statements of Tesco and Sainsbury to know the

profitability and also the fluctuations in profits.

Analysis of financial statements of Sainsbury for different users

Table 1: Financial statements - Sainsbury

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 1377 1277 1211

Operating profit 1009 887 874

Net profit 716 614 598

Net Sales 23949 23303 22294

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 % 5.43 %

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 4.21 % 3.81% 3.92 %

Net Profit Ratio (Net Profit/ Net Sales) *100 2.99 % 2.63 % 2.68 %

Liquidity ratios

Current Assets 4362 1901 2032

Current Liabilities 12171 3115 3136

Closing Stock 1005 987 938

Current Ratio

Current Assets / current

Liabilities 0.36 0.61 0.65

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29 0.35

2 | P a g e

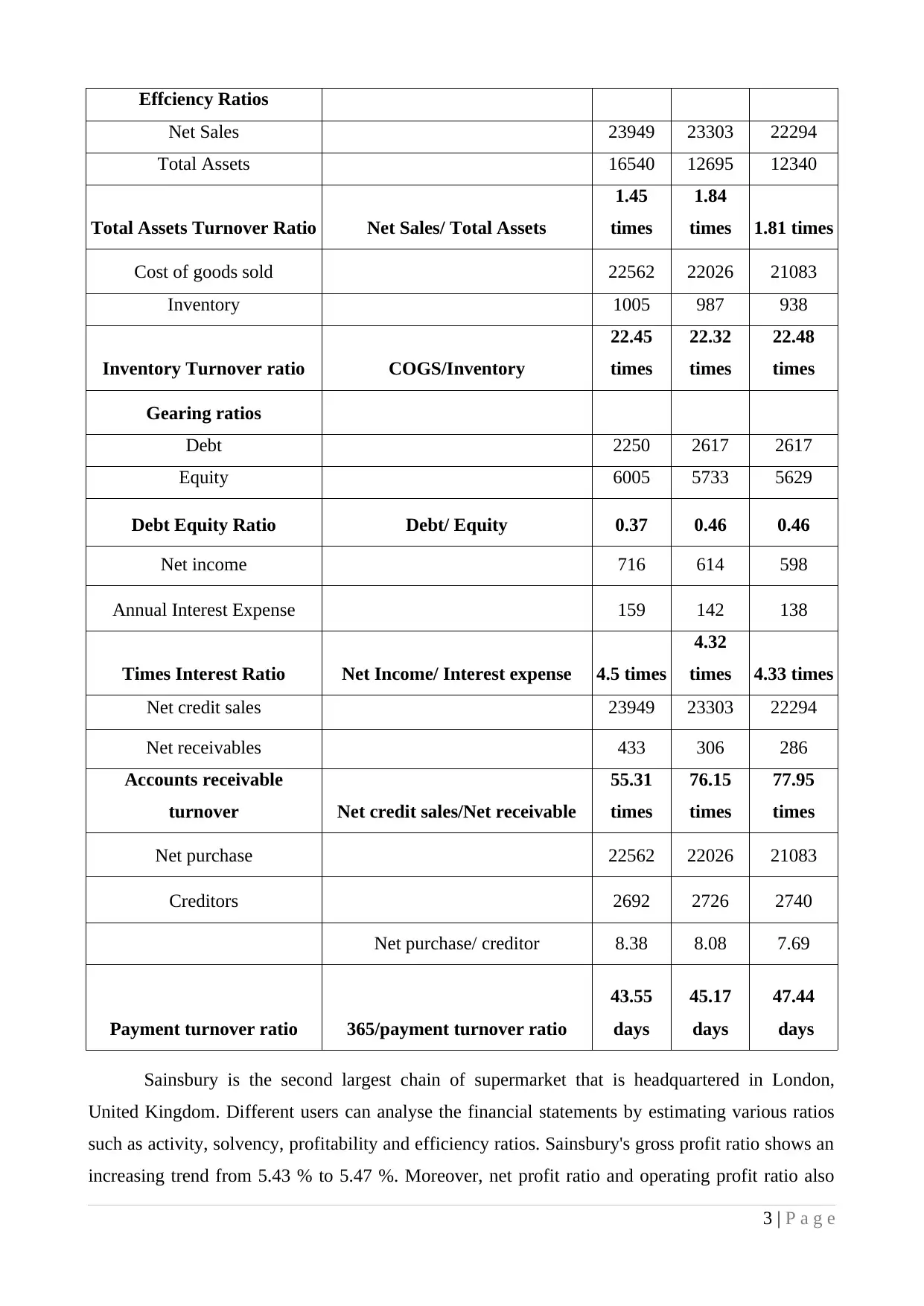

Effciency Ratios

Net Sales 23949 23303 22294

Total Assets 16540 12695 12340

Total Assets Turnover Ratio Net Sales/ Total Assets

1.45

times

1.84

times 1.81 times

Cost of goods sold 22562 22026 21083

Inventory 1005 987 938

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

22.48

times

Gearing ratios

Debt 2250 2617 2617

Equity 6005 5733 5629

Debt Equity Ratio Debt/ Equity 0.37 0.46 0.46

Net income 716 614 598

Annual Interest Expense 159 142 138

Times Interest Ratio Net Income/ Interest expense 4.5 times

4.32

times 4.33 times

Net credit sales 23949 23303 22294

Net receivables 433 306 286

Accounts receivable

turnover Net credit sales/Net receivable

55.31

times

76.15

times

77.95

times

Net purchase 22562 22026 21083

Creditors 2692 2726 2740

Net purchase/ creditor 8.38 8.08 7.69

Payment turnover ratio 365/payment turnover ratio

43.55

days

45.17

days

47.44

days

Sainsbury is the second largest chain of supermarket that is headquartered in London,

United Kingdom. Different users can analyse the financial statements by estimating various ratios

such as activity, solvency, profitability and efficiency ratios. Sainsbury's gross profit ratio shows an

increasing trend from 5.43 % to 5.47 %. Moreover, net profit ratio and operating profit ratio also

3 | P a g e

Net Sales 23949 23303 22294

Total Assets 16540 12695 12340

Total Assets Turnover Ratio Net Sales/ Total Assets

1.45

times

1.84

times 1.81 times

Cost of goods sold 22562 22026 21083

Inventory 1005 987 938

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

22.48

times

Gearing ratios

Debt 2250 2617 2617

Equity 6005 5733 5629

Debt Equity Ratio Debt/ Equity 0.37 0.46 0.46

Net income 716 614 598

Annual Interest Expense 159 142 138

Times Interest Ratio Net Income/ Interest expense 4.5 times

4.32

times 4.33 times

Net credit sales 23949 23303 22294

Net receivables 433 306 286

Accounts receivable

turnover Net credit sales/Net receivable

55.31

times

76.15

times

77.95

times

Net purchase 22562 22026 21083

Creditors 2692 2726 2740

Net purchase/ creditor 8.38 8.08 7.69

Payment turnover ratio 365/payment turnover ratio

43.55

days

45.17

days

47.44

days

Sainsbury is the second largest chain of supermarket that is headquartered in London,

United Kingdom. Different users can analyse the financial statements by estimating various ratios

such as activity, solvency, profitability and efficiency ratios. Sainsbury's gross profit ratio shows an

increasing trend from 5.43 % to 5.47 %. Moreover, net profit ratio and operating profit ratio also

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increases to 2.99% and 4.21% respectively. Therefore, it is favourable for various users such as

shareholders, managers and investors since the profitability is rising (Goyal and Goyal, 2012).

However, current ratio as well as quick ratio has decreased to 0.36 and 0.28 respectively. It shows

that less liquid assets are available to meet Sainsbury's short term requirement. Therefore, it will

have an adverse impact on the operations of business as well as users. On the contrary, total assets

and inventory turnover ratio decreased to 1.45 and 22.45 which shows that assets and inventory are

employed at less efficiency (Rajasekaran, 2011). Therefore, managers implement rules and

regulations strictly so as to increase the efficiency of assets. Debt equity ratio decreased to 0.37 and

time interest ratio increased to 4.50. It shows that Sainsbury is getting higher funds from lenders

and fewer amounts from shareholders. Time interest ratio increased to 4.50 which helps the

creditors and investors to evaluate that the creditworthiness of Sainsbury (Cotter and Hutchinson,

2011). However, accounts receivable and payable ratio decreased to 55.31 and 43.55 respectively. It

indicates quick collection from debtors and fast payment to creditors (Tulsian, 2002). Thus, it is

clear that managers have to take necessary steps to increase the liquidity and efficiency of assets.

Shareholders will be satisfied because earning per share of company has increased to 32.80p from

30.80p. Moreover, dividend per share has also increased from 16.70p to 17.30p. On the contrary,

financial institutions do not lend very much credit facility because of lowering the liquid position

and turnover ratio (Constantin, 2013).

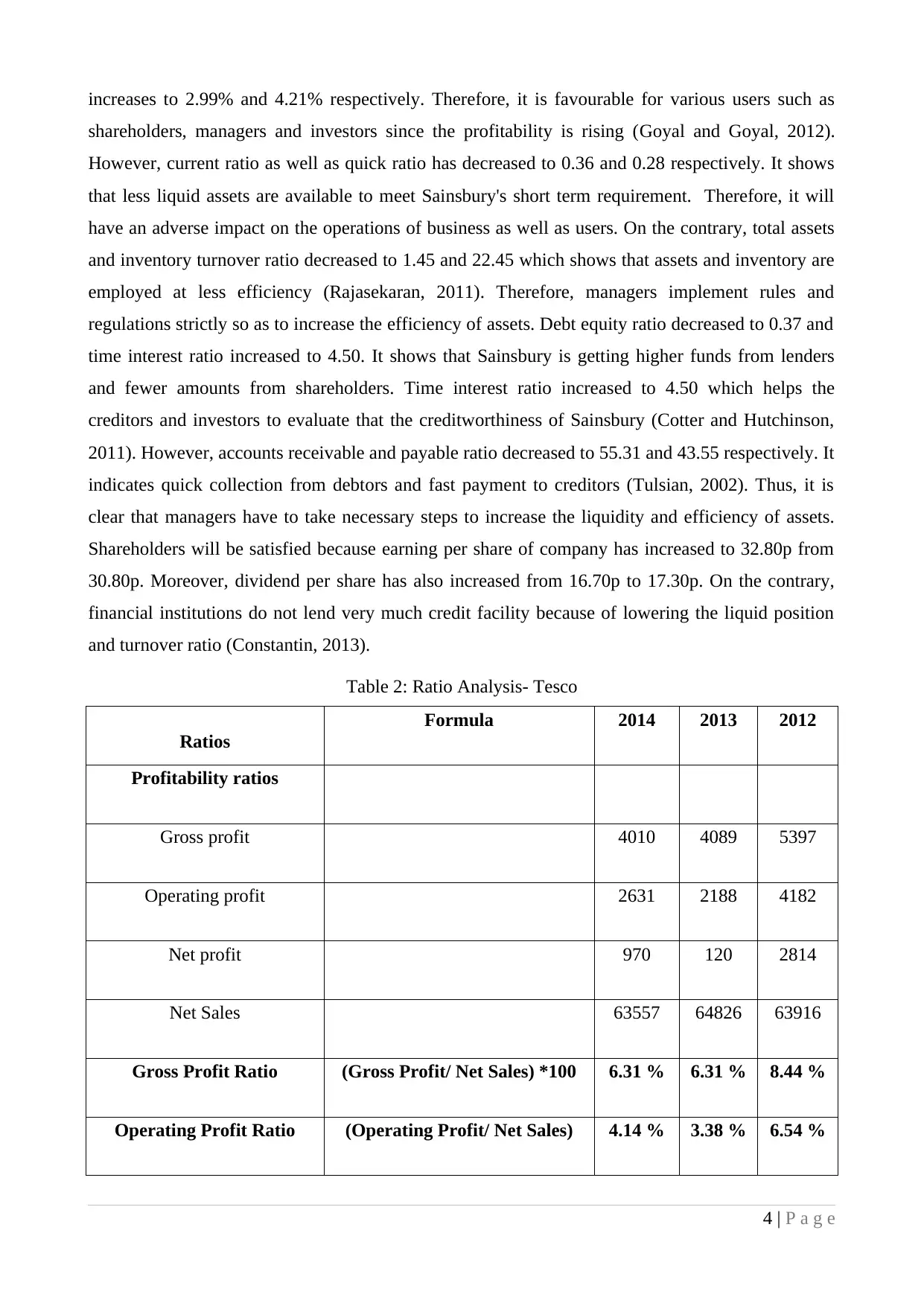

Table 2: Ratio Analysis- Tesco

Ratios

Formula 2014 2013 2012

Profitability ratios

Gross profit 4010 4089 5397

Operating profit 2631 2188 4182

Net profit 970 120 2814

Net Sales 63557 64826 63916

Gross Profit Ratio (Gross Profit/ Net Sales) *100 6.31 % 6.31 % 8.44 %

Operating Profit Ratio (Operating Profit/ Net Sales) 4.14 % 3.38 % 6.54 %

4 | P a g e

shareholders, managers and investors since the profitability is rising (Goyal and Goyal, 2012).

However, current ratio as well as quick ratio has decreased to 0.36 and 0.28 respectively. It shows

that less liquid assets are available to meet Sainsbury's short term requirement. Therefore, it will

have an adverse impact on the operations of business as well as users. On the contrary, total assets

and inventory turnover ratio decreased to 1.45 and 22.45 which shows that assets and inventory are

employed at less efficiency (Rajasekaran, 2011). Therefore, managers implement rules and

regulations strictly so as to increase the efficiency of assets. Debt equity ratio decreased to 0.37 and

time interest ratio increased to 4.50. It shows that Sainsbury is getting higher funds from lenders

and fewer amounts from shareholders. Time interest ratio increased to 4.50 which helps the

creditors and investors to evaluate that the creditworthiness of Sainsbury (Cotter and Hutchinson,

2011). However, accounts receivable and payable ratio decreased to 55.31 and 43.55 respectively. It

indicates quick collection from debtors and fast payment to creditors (Tulsian, 2002). Thus, it is

clear that managers have to take necessary steps to increase the liquidity and efficiency of assets.

Shareholders will be satisfied because earning per share of company has increased to 32.80p from

30.80p. Moreover, dividend per share has also increased from 16.70p to 17.30p. On the contrary,

financial institutions do not lend very much credit facility because of lowering the liquid position

and turnover ratio (Constantin, 2013).

Table 2: Ratio Analysis- Tesco

Ratios

Formula 2014 2013 2012

Profitability ratios

Gross profit 4010 4089 5397

Operating profit 2631 2188 4182

Net profit 970 120 2814

Net Sales 63557 64826 63916

Gross Profit Ratio (Gross Profit/ Net Sales) *100 6.31 % 6.31 % 8.44 %

Operating Profit Ratio (Operating Profit/ Net Sales) 4.14 % 3.38 % 6.54 %

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*100

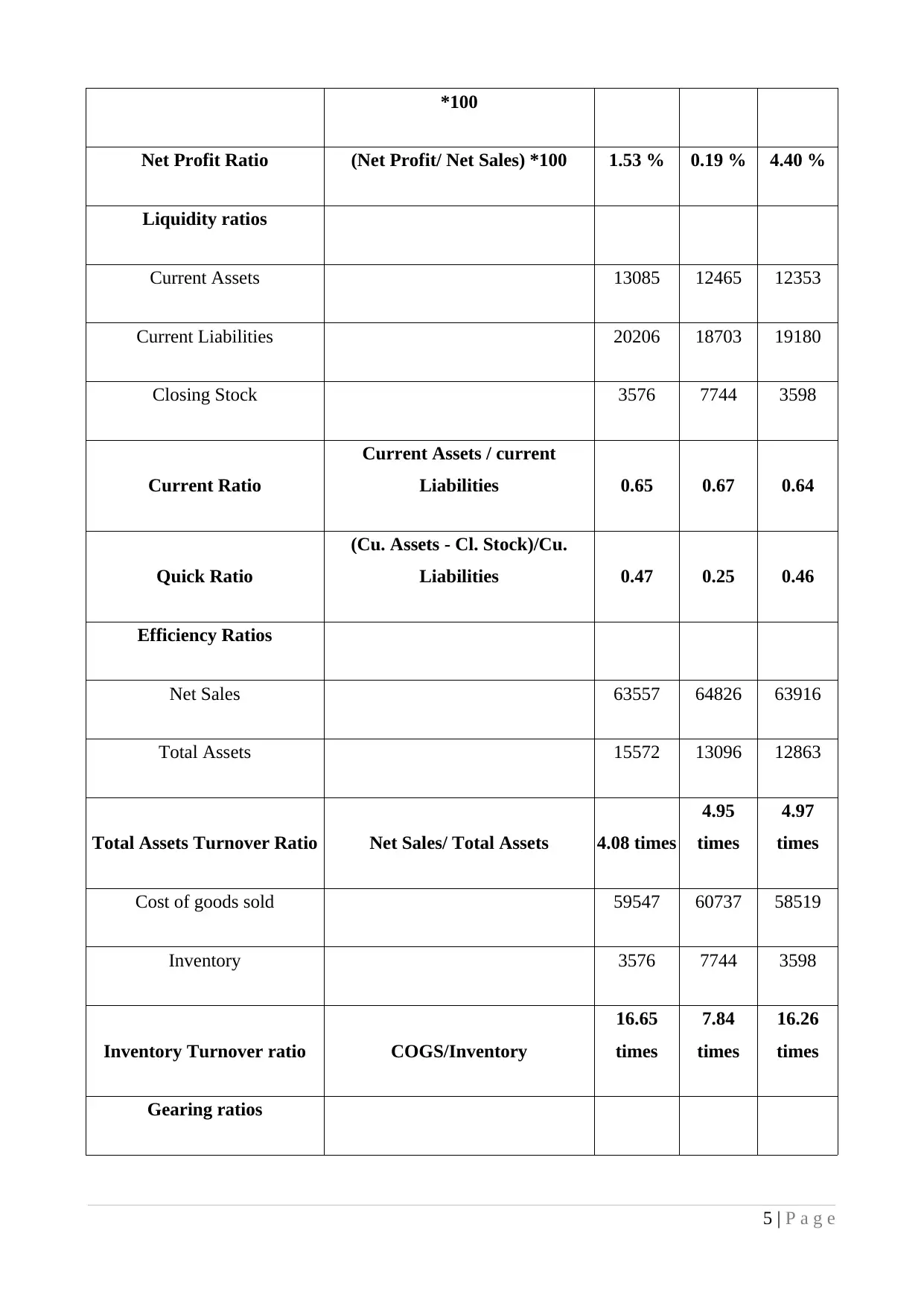

Net Profit Ratio (Net Profit/ Net Sales) *100 1.53 % 0.19 % 4.40 %

Liquidity ratios

Current Assets 13085 12465 12353

Current Liabilities 20206 18703 19180

Closing Stock 3576 7744 3598

Current Ratio

Current Assets / current

Liabilities 0.65 0.67 0.64

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.47 0.25 0.46

Efficiency Ratios

Net Sales 63557 64826 63916

Total Assets 15572 13096 12863

Total Assets Turnover Ratio Net Sales/ Total Assets 4.08 times

4.95

times

4.97

times

Cost of goods sold 59547 60737 58519

Inventory 3576 7744 3598

Inventory Turnover ratio COGS/Inventory

16.65

times

7.84

times

16.26

times

Gearing ratios

5 | P a g e

Net Profit Ratio (Net Profit/ Net Sales) *100 1.53 % 0.19 % 4.40 %

Liquidity ratios

Current Assets 13085 12465 12353

Current Liabilities 20206 18703 19180

Closing Stock 3576 7744 3598

Current Ratio

Current Assets / current

Liabilities 0.65 0.67 0.64

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.47 0.25 0.46

Efficiency Ratios

Net Sales 63557 64826 63916

Total Assets 15572 13096 12863

Total Assets Turnover Ratio Net Sales/ Total Assets 4.08 times

4.95

times

4.97

times

Cost of goods sold 59547 60737 58519

Inventory 3576 7744 3598

Inventory Turnover ratio COGS/Inventory

16.65

times

7.84

times

16.26

times

Gearing ratios

5 | P a g e

Debt 9303 10068 9911

Equity 14772 16661 17801

Debt Equity Ratio Debt/ Equity 0.63 0.60 0.56

Net income 970 120 2814

Annual Interest Expense 564 459 411

Times Interest Ratio Net Income/ Interest expense 1.72 times

0.26

times

6.85

times

Net credit sales 63557 64826 63916

Net receivables 2190 2525 2657

Accounts receivable turnover Net credit sales/Net receivable

29.021

times

25.67

times

24.06

times

Net purchase 59547 60735 58519

Creditors 10595 11094 11234

Net purchase/ creditor 5.62 5.47 5.21

Payment turnover ratio 365/payment turnover ratio

64.94

days

66.67

days

70.07

days

Analysis of financial statements of Tesco for different users

Tesco Plc is a British multinational and merchandise retail firm that is headquartered at

Cheshnut, Hertfordshire, England in United Kingdom. The mission of company is to be the

champion for customers by providing better services to them. The profitability ratios of the

organization show a decreasing trend. Gross profit ratio of company has decreased to 6.31 from

8.44. Also, the net profit and operating profit ratio decreased to 4.14 and 1.53 respectively. It

indicates shareholders not to make investment in company because of decreasing profitability

6 | P a g e

Equity 14772 16661 17801

Debt Equity Ratio Debt/ Equity 0.63 0.60 0.56

Net income 970 120 2814

Annual Interest Expense 564 459 411

Times Interest Ratio Net Income/ Interest expense 1.72 times

0.26

times

6.85

times

Net credit sales 63557 64826 63916

Net receivables 2190 2525 2657

Accounts receivable turnover Net credit sales/Net receivable

29.021

times

25.67

times

24.06

times

Net purchase 59547 60735 58519

Creditors 10595 11094 11234

Net purchase/ creditor 5.62 5.47 5.21

Payment turnover ratio 365/payment turnover ratio

64.94

days

66.67

days

70.07

days

Analysis of financial statements of Tesco for different users

Tesco Plc is a British multinational and merchandise retail firm that is headquartered at

Cheshnut, Hertfordshire, England in United Kingdom. The mission of company is to be the

champion for customers by providing better services to them. The profitability ratios of the

organization show a decreasing trend. Gross profit ratio of company has decreased to 6.31 from

8.44. Also, the net profit and operating profit ratio decreased to 4.14 and 1.53 respectively. It

indicates shareholders not to make investment in company because of decreasing profitability

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Ahmad, 2008). Moreover, managers have to make efficient strategies on the ways in which profit

can be increased. However, current ratio decreased to 0.65 from 0.67 whereas quick ratio increased

to 0.47. It indicates that Tesco's liquidity position is increasing and now, company will be more able

to pay its short term liquidity. Assets turnover ratio is decreased from 4.97 to 4.08 which imply that

company is using its assets at less efficiency so its cash generation ability is decreasing (Georgiou,

2010). On the contrary, Tesco's inventory turnover ratio has increased to 16.65 which show that

company is using its inventory efficiently. Therefore, the managers should ensure that all the assets

should be used in an effective way. Debt equity ratio is increased to 0.63 whereas time interest ratio

decreased to 1.72. It indicates that Tesco's ability to pay interest on its debts has decreased.

Therefore, the loan providers and financial institutions will be affected badly and they do not lend

to company (Gray and et.al., 2011). Accounts receivable turnover ratio has increased to 29.021 and

payment turnover ratio has decreased to 64.94. It indicates that company is collecting its debts

earlier and later payments to creditors. Hence, from the above analysis, it is clear that managers,

employees, government and investors will be satisfied because of increase in profit percentage. In

addition to it, Tesco's financial statements affect loan providers’ adversely because of decrease in

the firm's time interest ratio and assets turnover ratio (Persons, 2011).

CONCLUSION

From the presented report, it is clear that every business needs to prepare financial

statements in order to know the profitability and its financial status. This statement also helps

different users by providing information according to their needs. Internal users aim at high

business growth whereas external users want high return on their investment (Minnis, 2011). In

addition to it, users can take effective decision through analysis of financial statements that are

produced by the firm. Moreover, government will be satisfied to find the business growth which in

turn helps the country's economic growth. It helps the organization to achieve their goals and

objectives by making strategic planning and controlling effectually (De Franco, Kothari and Verdi,

2011).

7 | P a g e

can be increased. However, current ratio decreased to 0.65 from 0.67 whereas quick ratio increased

to 0.47. It indicates that Tesco's liquidity position is increasing and now, company will be more able

to pay its short term liquidity. Assets turnover ratio is decreased from 4.97 to 4.08 which imply that

company is using its assets at less efficiency so its cash generation ability is decreasing (Georgiou,

2010). On the contrary, Tesco's inventory turnover ratio has increased to 16.65 which show that

company is using its inventory efficiently. Therefore, the managers should ensure that all the assets

should be used in an effective way. Debt equity ratio is increased to 0.63 whereas time interest ratio

decreased to 1.72. It indicates that Tesco's ability to pay interest on its debts has decreased.

Therefore, the loan providers and financial institutions will be affected badly and they do not lend

to company (Gray and et.al., 2011). Accounts receivable turnover ratio has increased to 29.021 and

payment turnover ratio has decreased to 64.94. It indicates that company is collecting its debts

earlier and later payments to creditors. Hence, from the above analysis, it is clear that managers,

employees, government and investors will be satisfied because of increase in profit percentage. In

addition to it, Tesco's financial statements affect loan providers’ adversely because of decrease in

the firm's time interest ratio and assets turnover ratio (Persons, 2011).

CONCLUSION

From the presented report, it is clear that every business needs to prepare financial

statements in order to know the profitability and its financial status. This statement also helps

different users by providing information according to their needs. Internal users aim at high

business growth whereas external users want high return on their investment (Minnis, 2011). In

addition to it, users can take effective decision through analysis of financial statements that are

produced by the firm. Moreover, government will be satisfied to find the business growth which in

turn helps the country's economic growth. It helps the organization to achieve their goals and

objectives by making strategic planning and controlling effectually (De Franco, Kothari and Verdi,

2011).

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ahmad, N., 2008. Financial Accounting. Atlantic publishers & Dist.

De Franco, G., Kothari, S. P. and Verdi, R. S., 2011. The benefits of financial statement

comparability. Journal of Accounting Research. 49(4). pp. 895-931.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Georgiou, G., 2010. The IASB standard-setting process: Participation and perceptions of financial

statement users. The British Accounting Review. 42(2). pp.103-118.

Goyal, K. V. and Goyal R., 2012. Financial Accounting. 4th edition. PHI Learning Pvt. Ltd.

Gray, G. L. and et. al., 2011. Perceptions and misperceptions regarding the unqualified auditor's

report by financial statement preparers, users, and auditors. Accounting Horizons. 25(4). pp.

659-684.

Ibson, C., 2008. Financial Reporting and Analysis: Using Accounting Information. 11th edition.

Cengage Learning.

Lebas, M. and Stolowy, H., 2006. Financial Accounting and Reporting: A Global Perspective.

Cengage Learning.

Minnis, M., 2011. The value of financial statement verification in debt financing: Evidence from

private US firms. Journal of Accounting Research. 49(2). pp. 457-506.

Persons, O. S., 2011. Using financial statement data to identify factors associated with fraudulent

financial reporting. Journal of Applied Business Research (JABR). 11(3). pp. 38-46.

Rajasekaran, V., 2011. Financial Accounting. Pearson Education India.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and analysis:

text and cases. John Wiley and Sons.

Scott, W. R., 2014. Financial accounting theory. Pearson Education Canada.

Stickney, C. and et. al., 2009. Financial accounting: an introduction to concepts, methods and uses.

Cengage Learning.

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

Wantao, Y. and Ramanathan, R., 2008. An assessment of operational efficiencies in the UK retail

sector. International Journal Of Retail And Distribution Management. 36(11). pp. 861-882.

Online

8 | P a g e

Books and Journals

Ahmad, N., 2008. Financial Accounting. Atlantic publishers & Dist.

De Franco, G., Kothari, S. P. and Verdi, R. S., 2011. The benefits of financial statement

comparability. Journal of Accounting Research. 49(4). pp. 895-931.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Georgiou, G., 2010. The IASB standard-setting process: Participation and perceptions of financial

statement users. The British Accounting Review. 42(2). pp.103-118.

Goyal, K. V. and Goyal R., 2012. Financial Accounting. 4th edition. PHI Learning Pvt. Ltd.

Gray, G. L. and et. al., 2011. Perceptions and misperceptions regarding the unqualified auditor's

report by financial statement preparers, users, and auditors. Accounting Horizons. 25(4). pp.

659-684.

Ibson, C., 2008. Financial Reporting and Analysis: Using Accounting Information. 11th edition.

Cengage Learning.

Lebas, M. and Stolowy, H., 2006. Financial Accounting and Reporting: A Global Perspective.

Cengage Learning.

Minnis, M., 2011. The value of financial statement verification in debt financing: Evidence from

private US firms. Journal of Accounting Research. 49(2). pp. 457-506.

Persons, O. S., 2011. Using financial statement data to identify factors associated with fraudulent

financial reporting. Journal of Applied Business Research (JABR). 11(3). pp. 38-46.

Rajasekaran, V., 2011. Financial Accounting. Pearson Education India.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and analysis:

text and cases. John Wiley and Sons.

Scott, W. R., 2014. Financial accounting theory. Pearson Education Canada.

Stickney, C. and et. al., 2009. Financial accounting: an introduction to concepts, methods and uses.

Cengage Learning.

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

Wantao, Y. and Ramanathan, R., 2008. An assessment of operational efficiencies in the UK retail

sector. International Journal Of Retail And Distribution Management. 36(11). pp. 861-882.

Online

8 | P a g e

Constantin, F. D., 2013. The users of accounting information and their needs. [PDF]. Available

through: <http://fse.tibiscus.ro/anale/lucrari2013/lucrari_vol_xix_2013_032.pdf>.

[Accessed on 2nd November 2015].

Cotter, J. and Hutchinson, W. R., 2011. The impact of accounting reporting techniques on earning

enhancement in the UK retailing sector. [Online]. Available through:

<http://www.tandfonline.com/doi/abs/10.1080/095939699342615>. [Accessed on 2nd

November 2015].

9 | P a g e

through: <http://fse.tibiscus.ro/anale/lucrari2013/lucrari_vol_xix_2013_032.pdf>.

[Accessed on 2nd November 2015].

Cotter, J. and Hutchinson, W. R., 2011. The impact of accounting reporting techniques on earning

enhancement in the UK retailing sector. [Online]. Available through:

<http://www.tandfonline.com/doi/abs/10.1080/095939699342615>. [Accessed on 2nd

November 2015].

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.