Financial Accounting Report: Final Accounts and Reconciliation

VerifiedAdded on 2020/10/22

|13

|2049

|448

Report

AI Summary

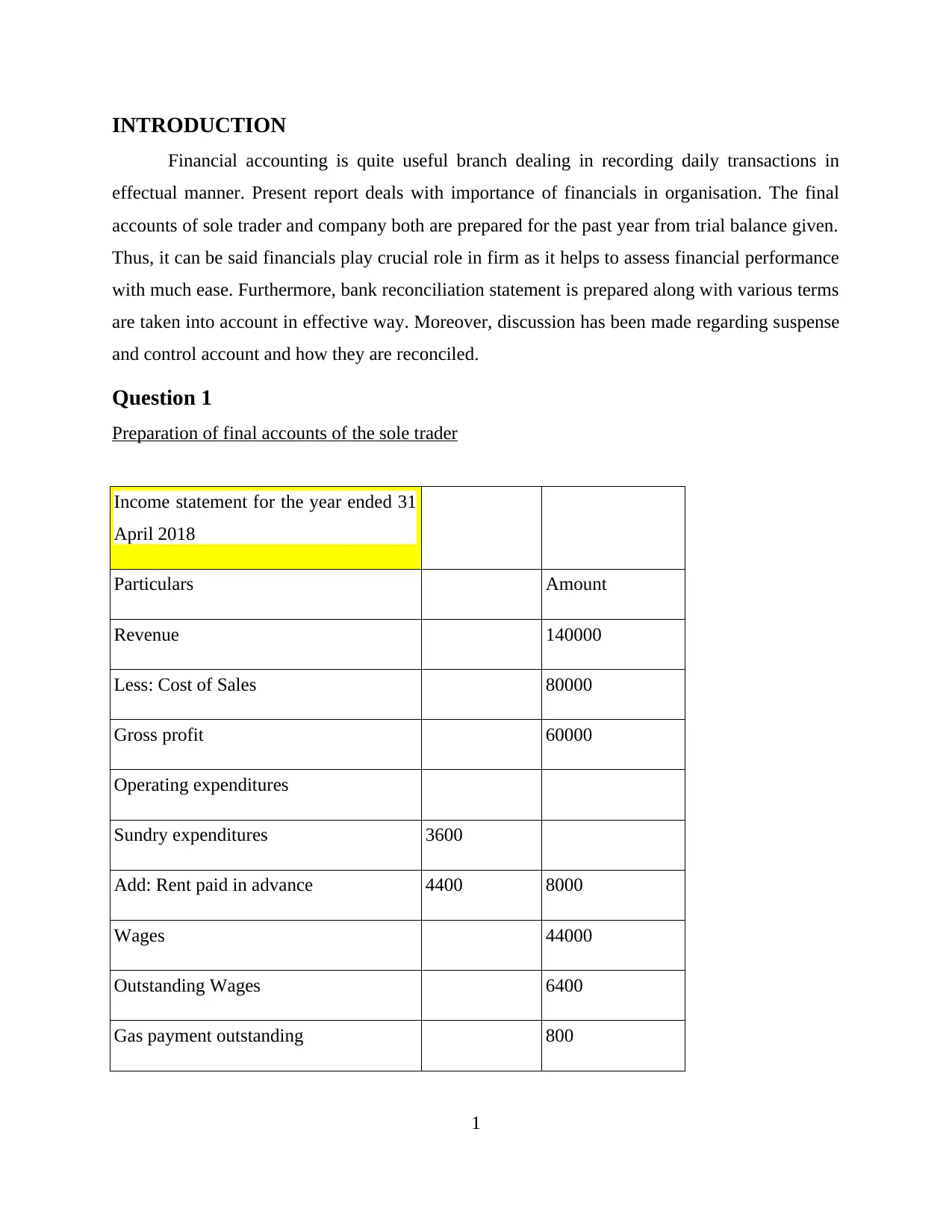

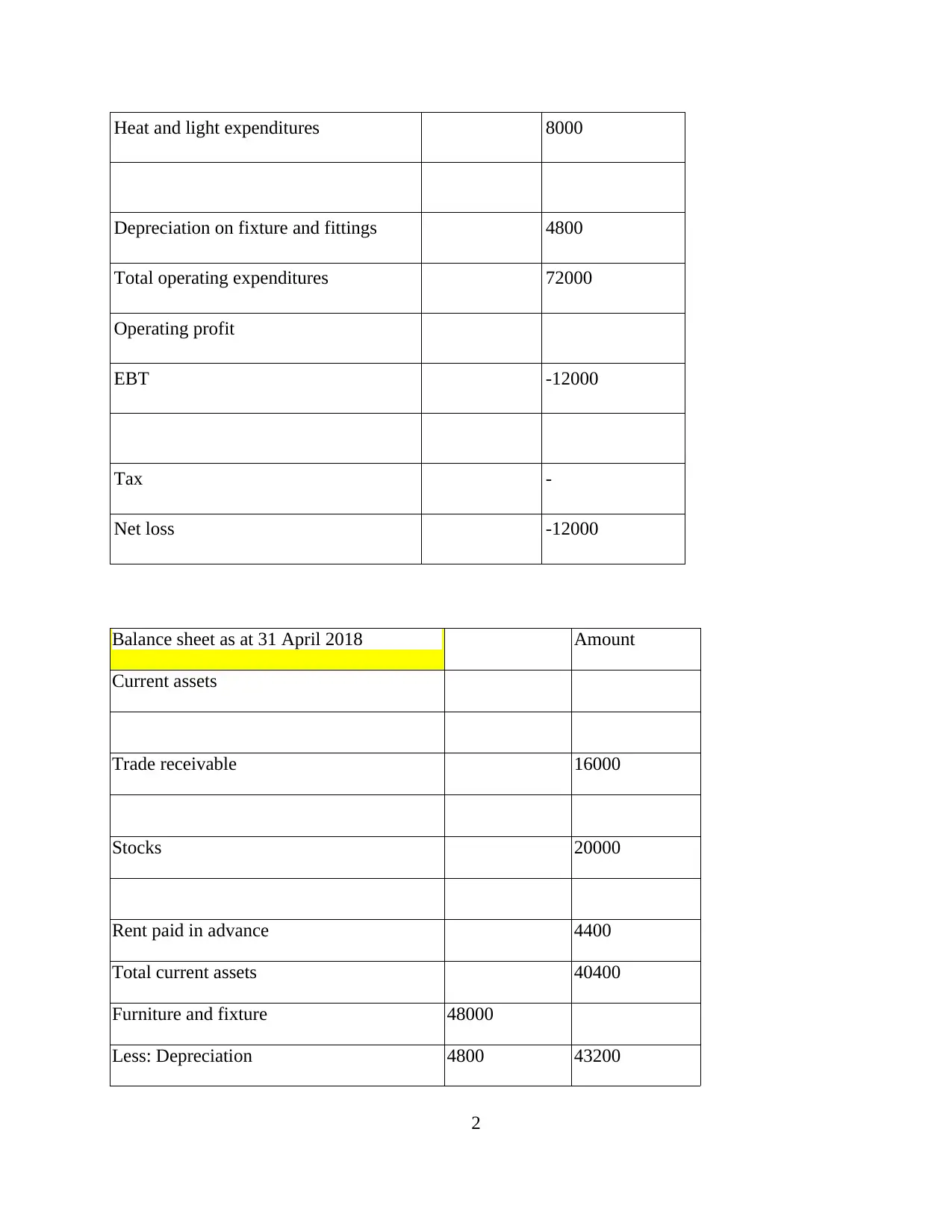

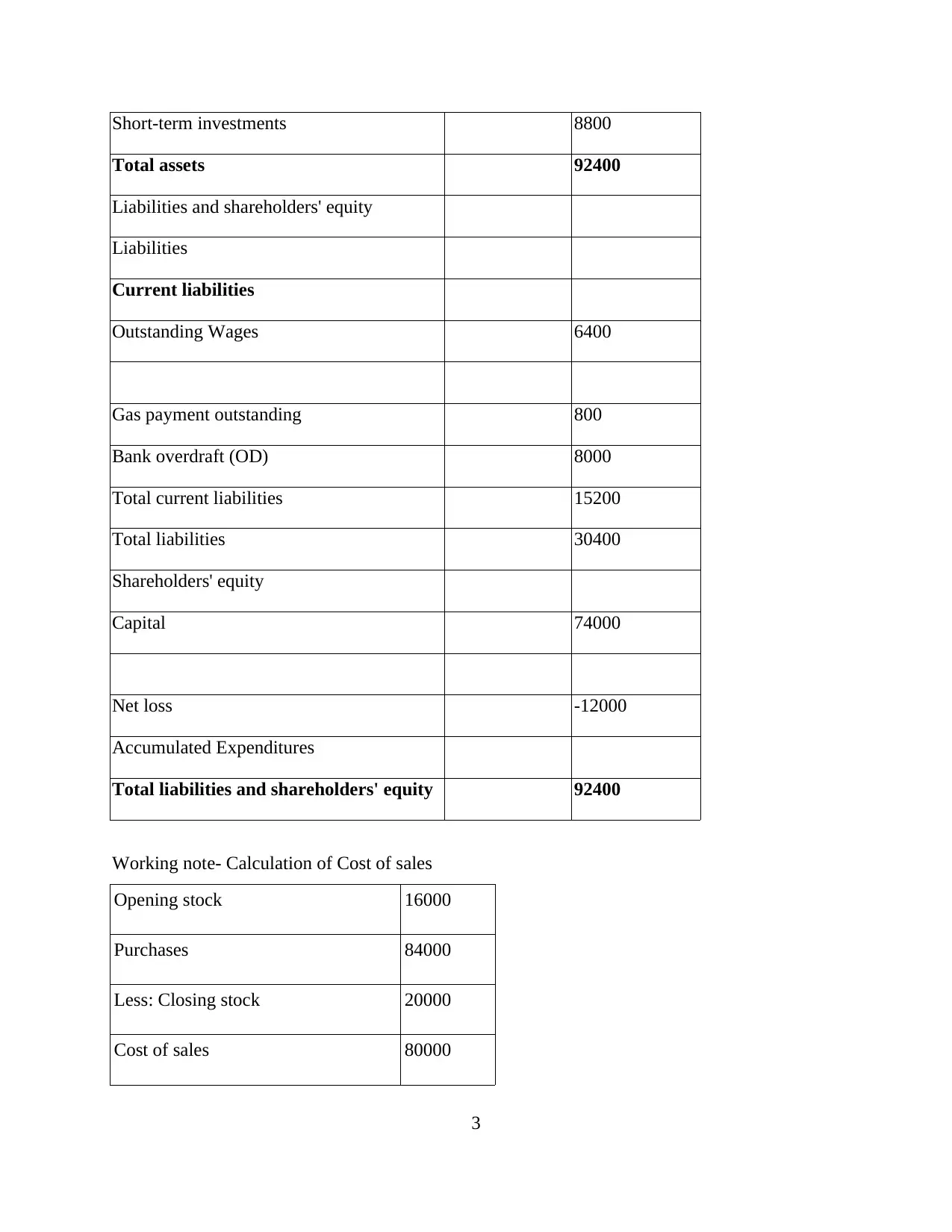

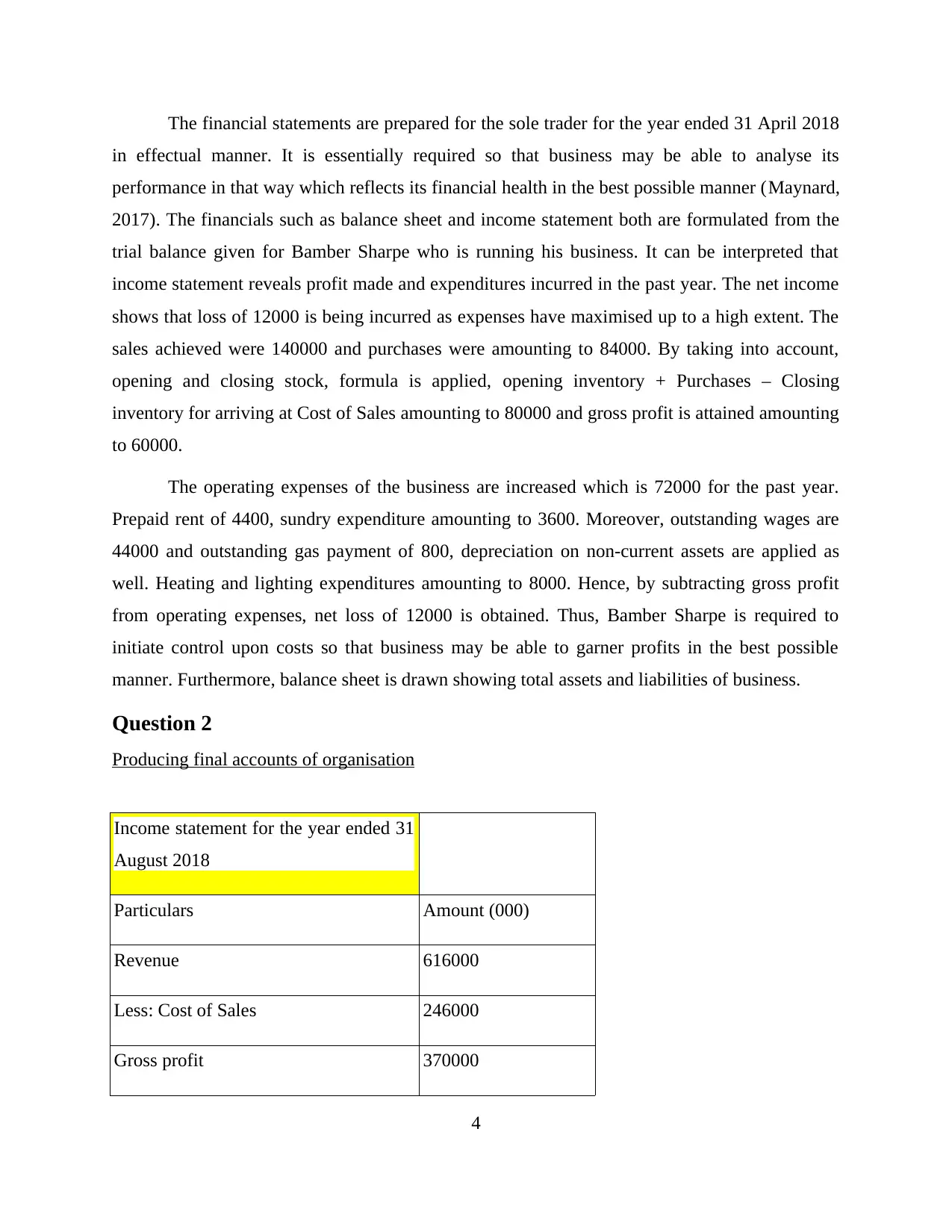

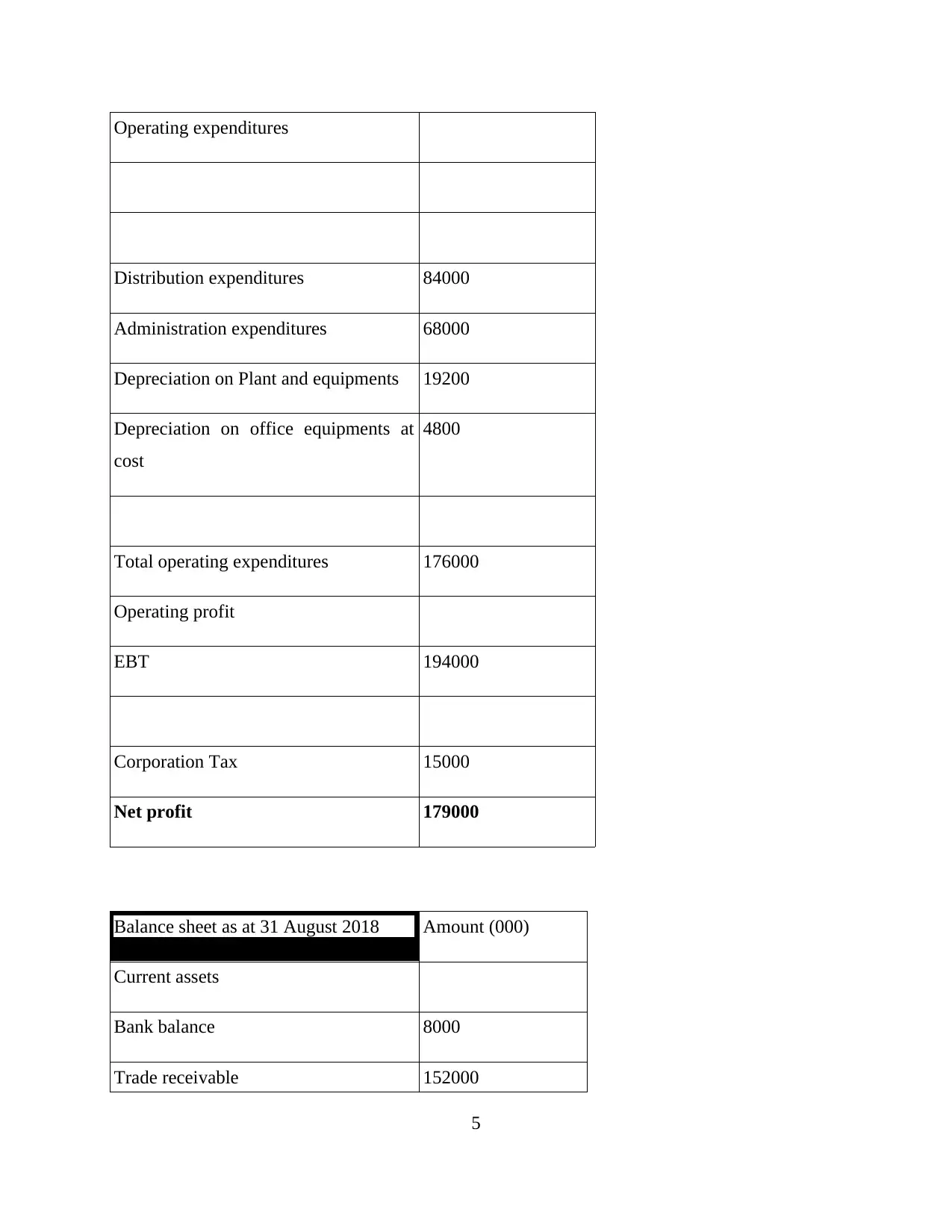

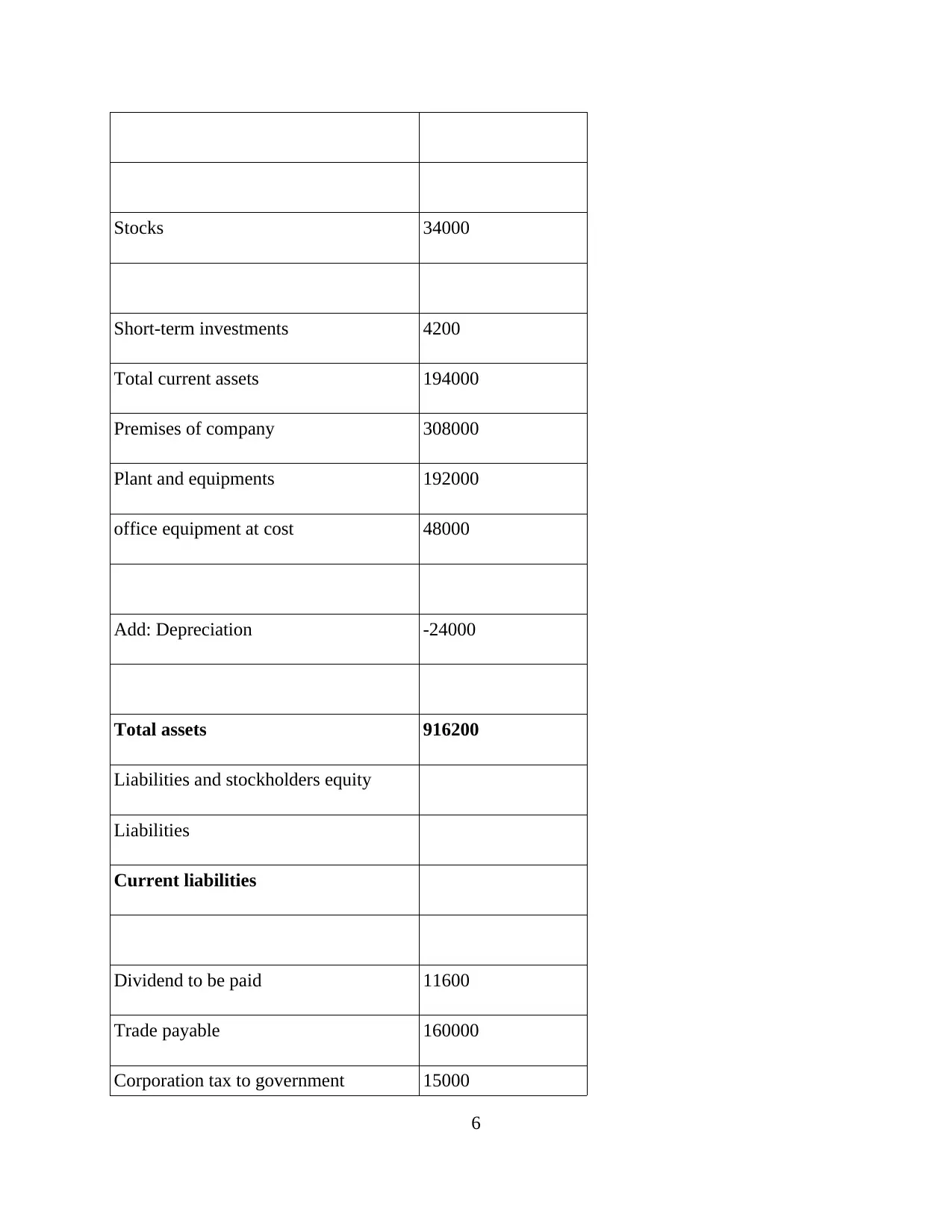

This report provides a comprehensive overview of financial accounting principles, focusing on the preparation and analysis of financial statements for both sole traders and companies. It begins by demonstrating the creation of income statements and balance sheets from trial balances, highlighting the importance of financial statements in assessing a business's financial health. The report then delves into bank reconciliation statements, explaining their purpose in rectifying discrepancies between a company's records and bank statements, along with key terms like deposits in transit and outstanding checks. Finally, it discusses the reconciliation of suspense and control accounts, emphasizing their roles in managing and classifying financial transactions, particularly in large organizations with numerous daily transactions. The report includes practical examples and working notes to illustrate the concepts discussed.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.