Financial Accounting and Costing Assignment Solution

VerifiedAdded on 2020/03/04

|10

|1170

|49

Homework Assignment

AI Summary

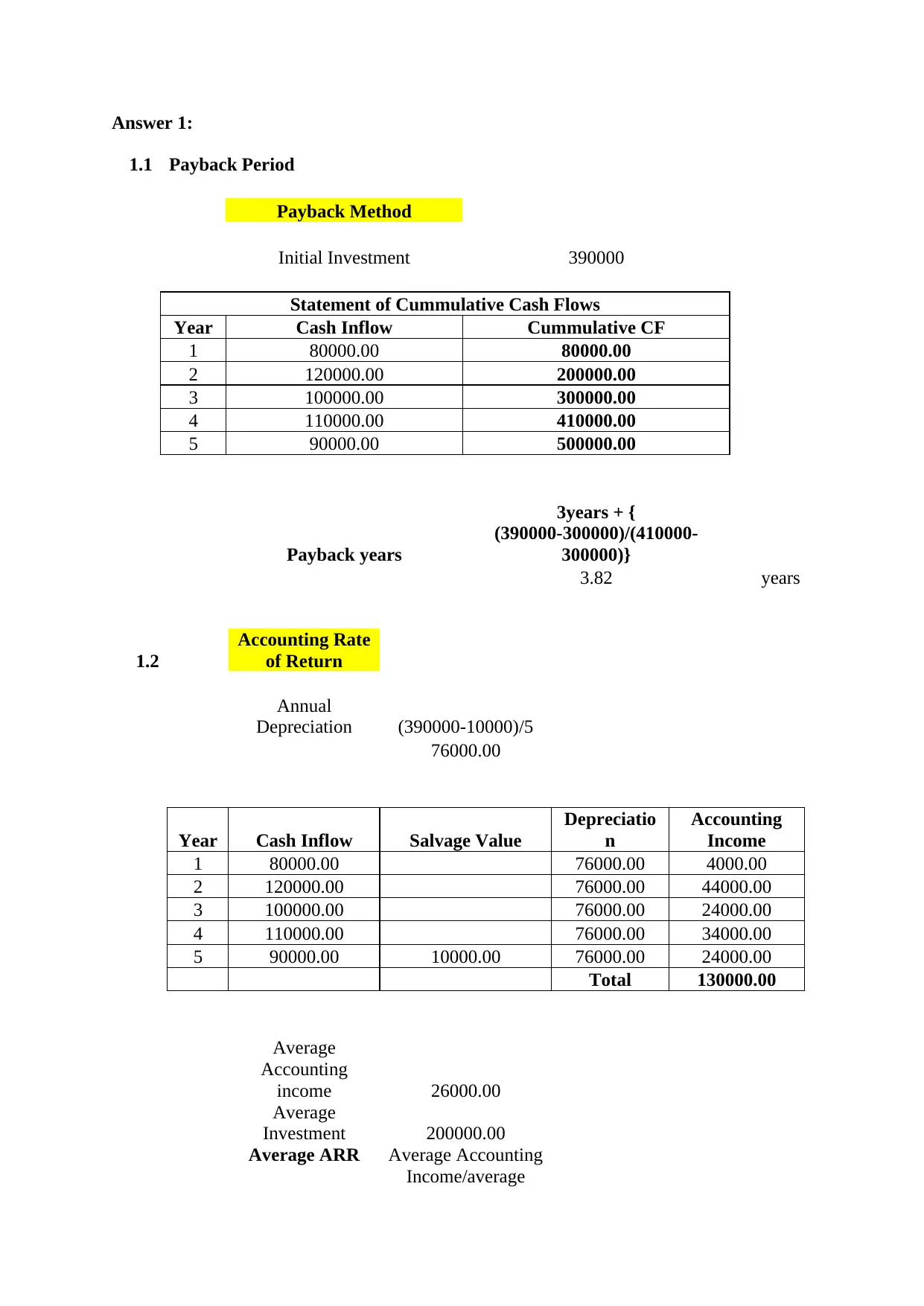

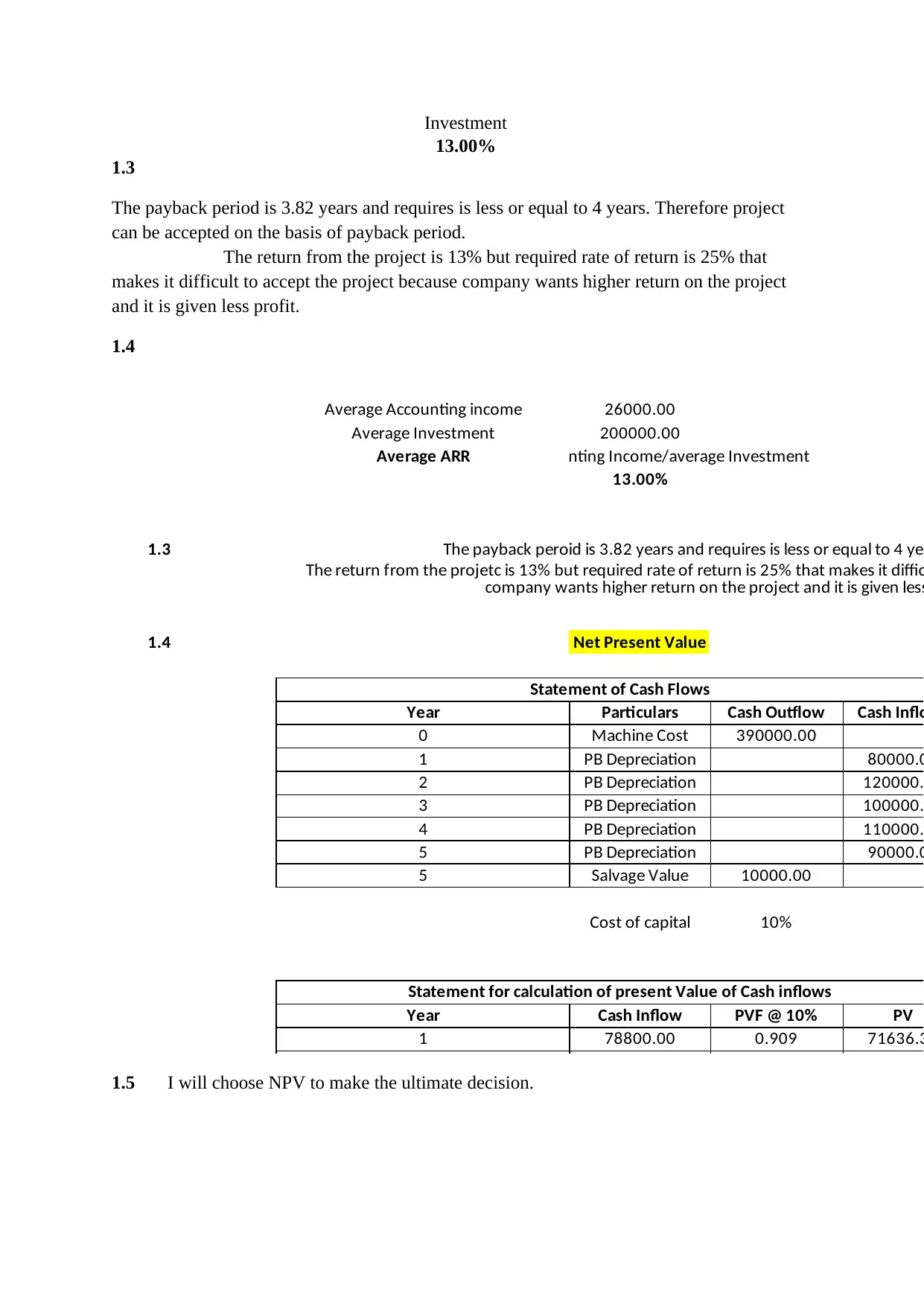

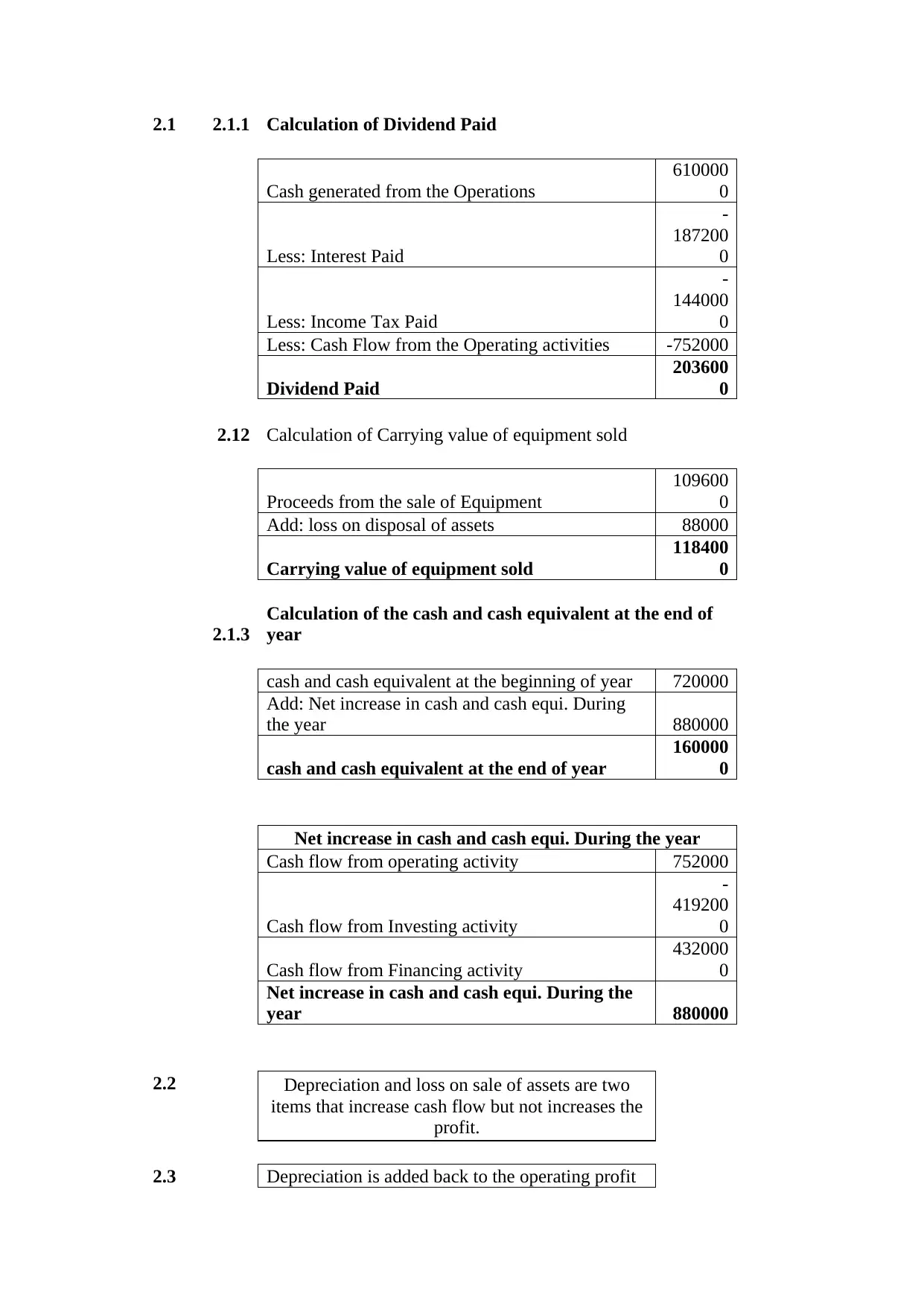

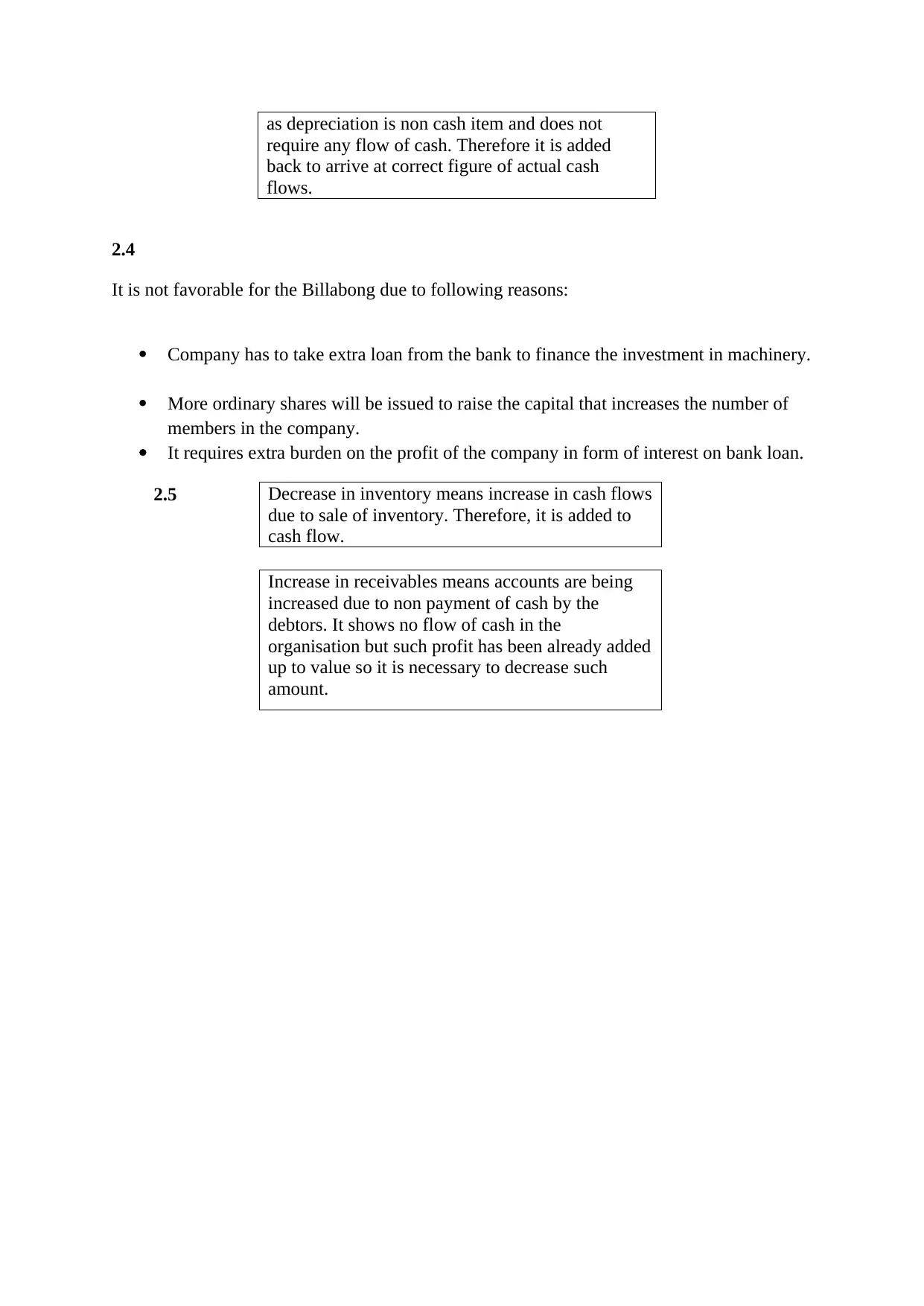

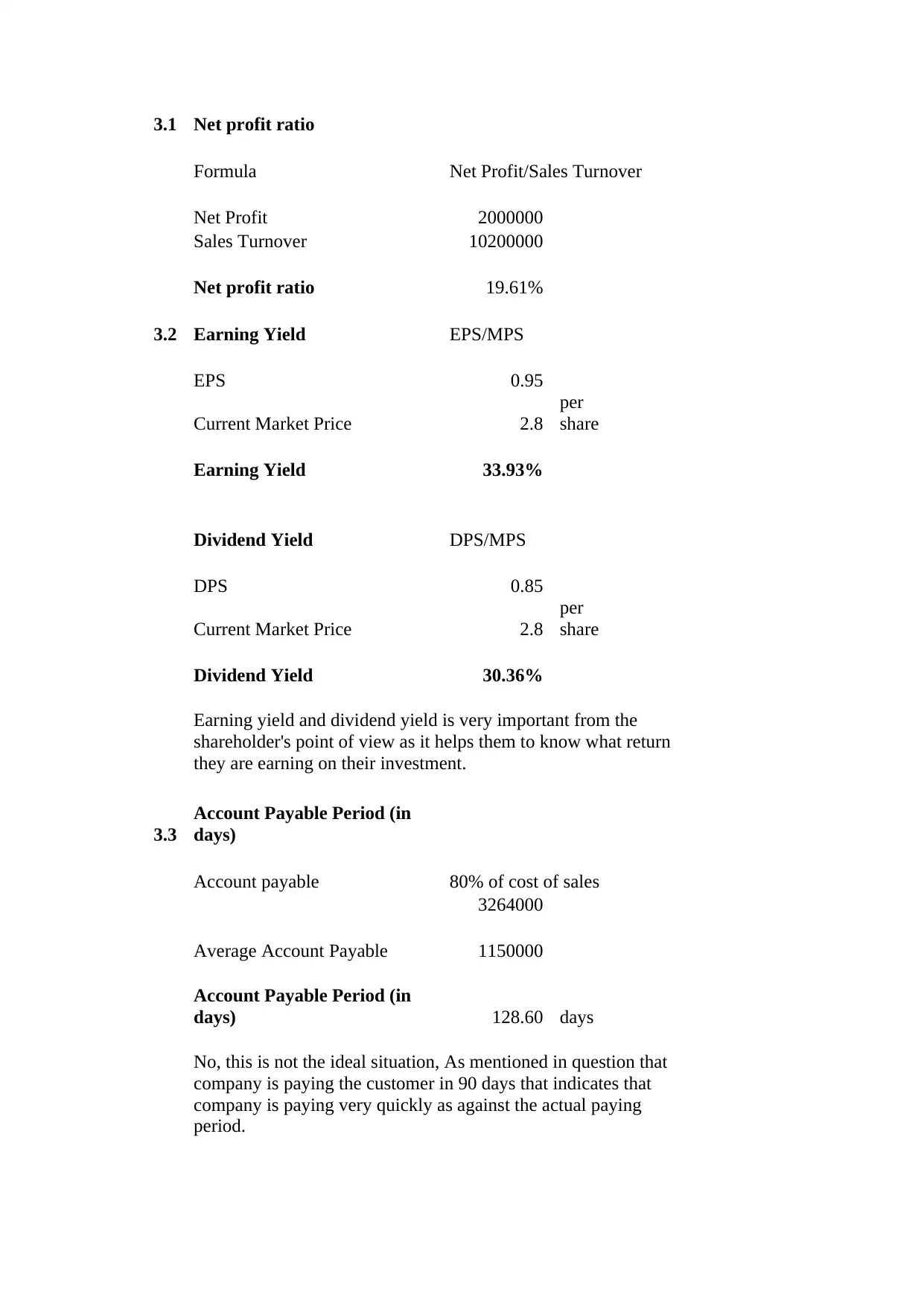

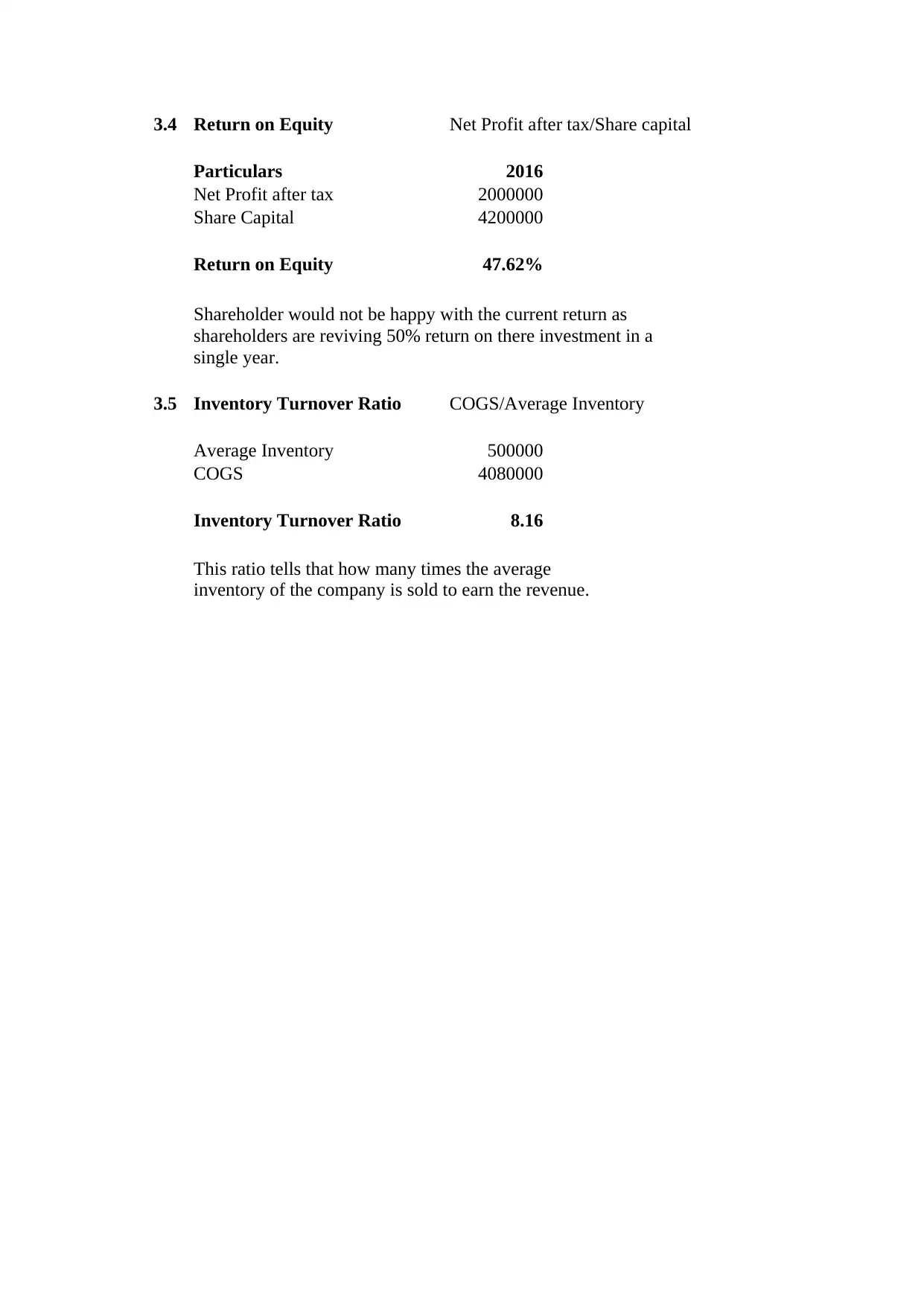

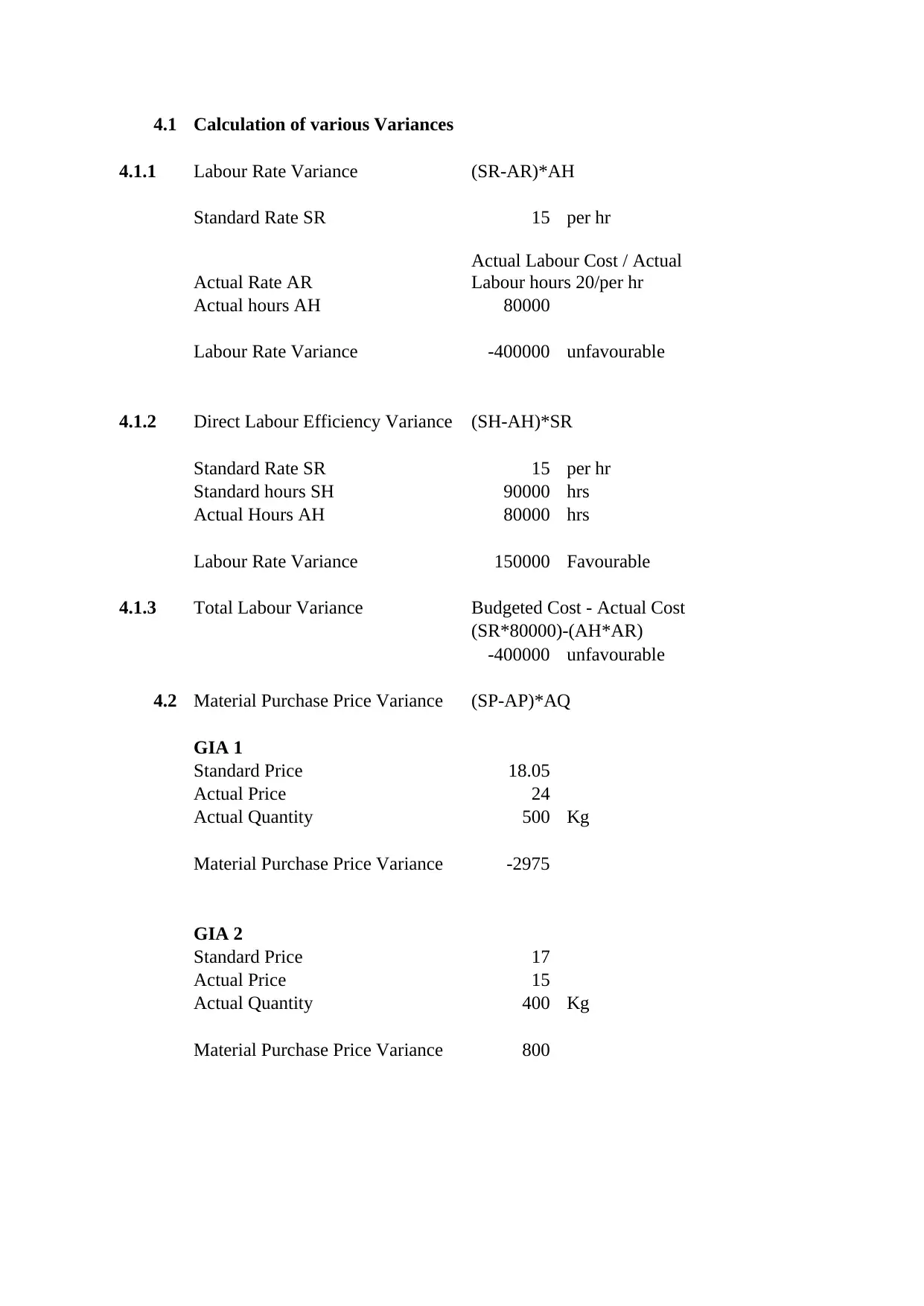

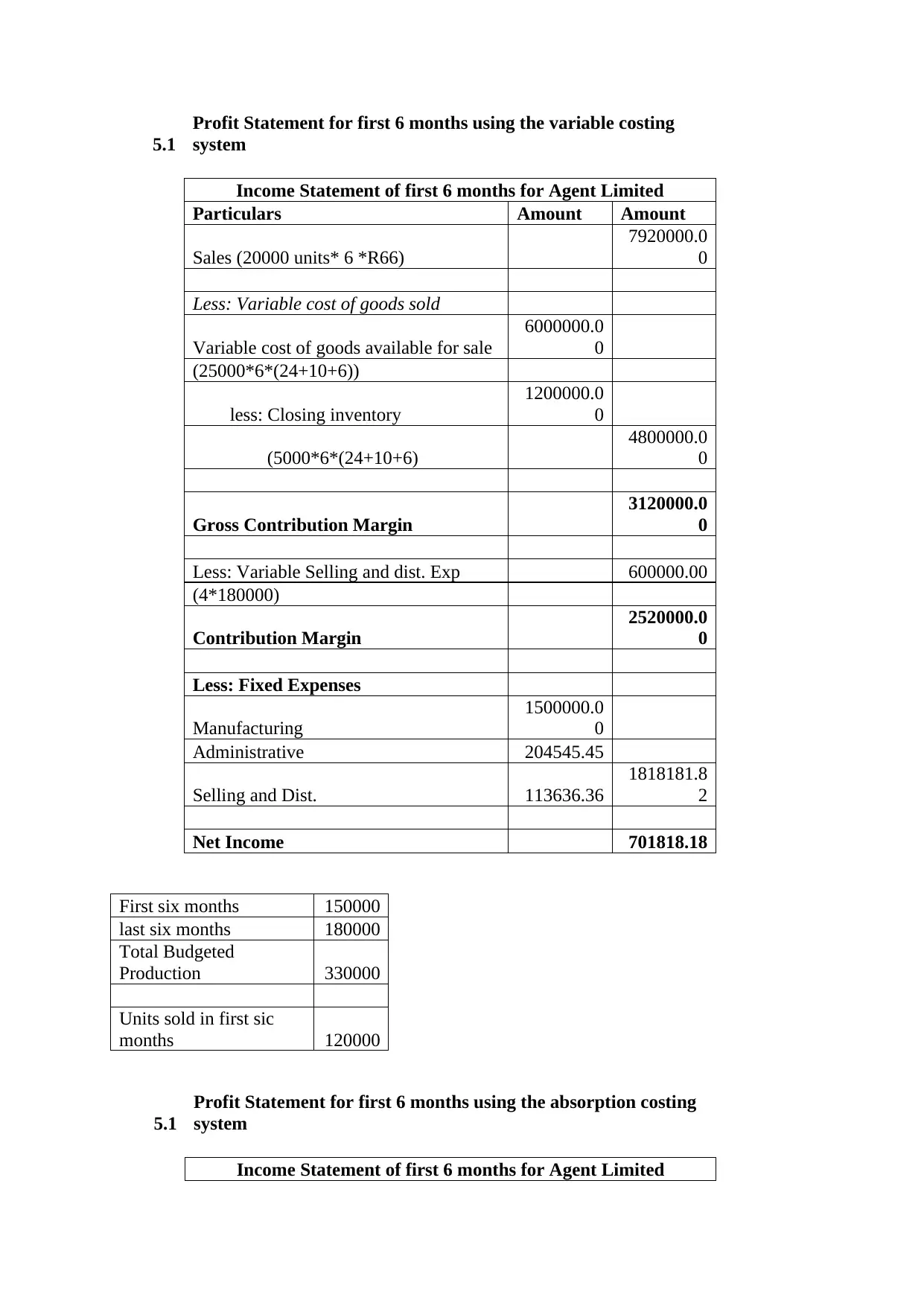

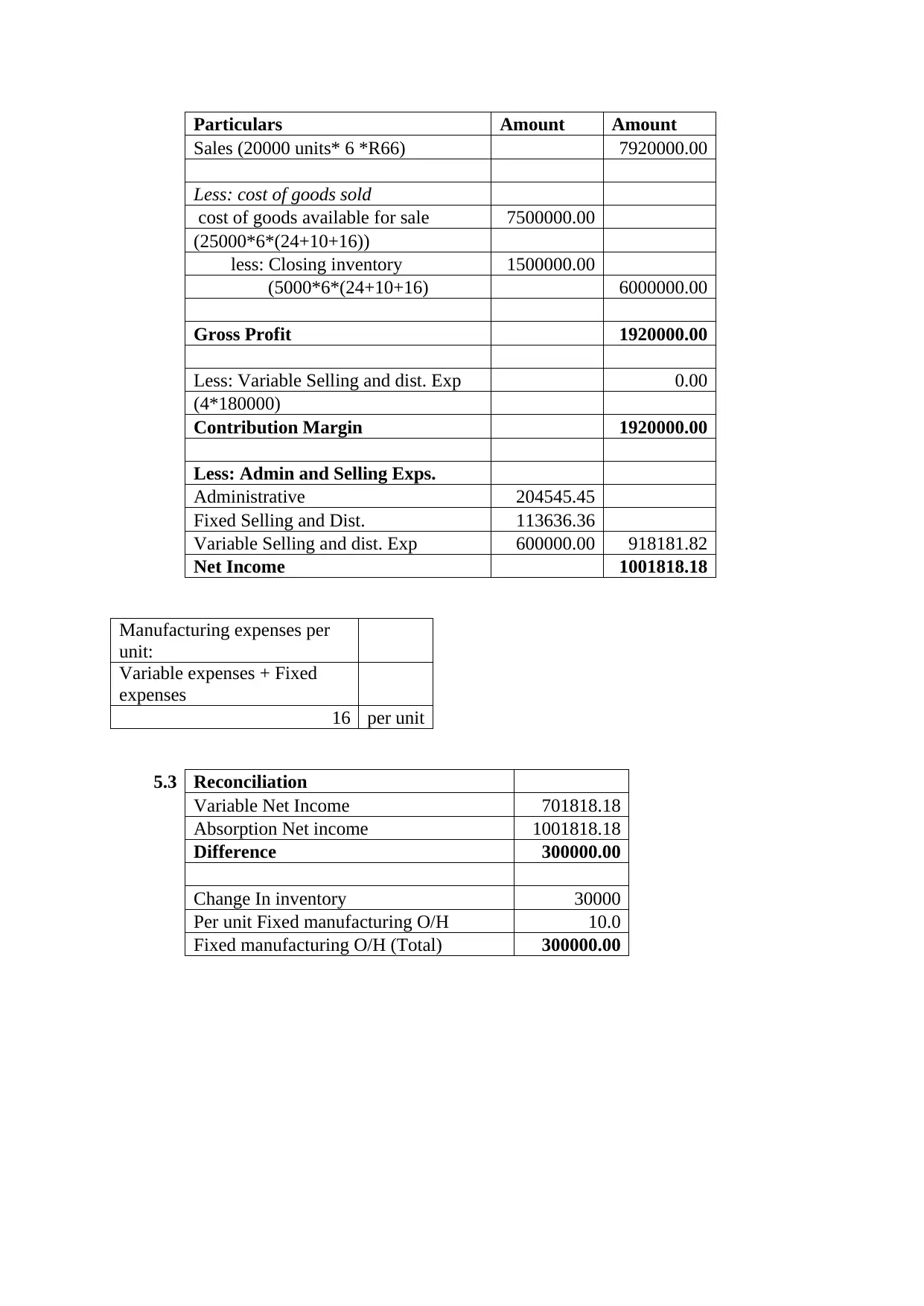

This finance assignment solution provides detailed answers to various financial analysis and accounting problems. It includes calculations and analysis of the payback period, accounting rate of return, and cash flow statements. The solution also covers financial ratio analysis, including net profit ratio, earning yield, dividend yield, and return on equity. Furthermore, it addresses variance analysis, including labor and material variances. Finally, the assignment explores variable and absorption costing methods and reconciles the differences in net income under these two approaches. The assignment demonstrates a comprehensive understanding of financial accounting and analysis techniques. The solution is provided by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.