Financial Statement Analysis Report for Kingston Wharves Limited

VerifiedAdded on 2023/02/01

|23

|3618

|82

Report

AI Summary

This report provides a comprehensive financial analysis of Kingston Wharves Limited, evaluating its financial performance and position over a two-year period. The analysis includes an assessment of the company's financial status, capital structure, and liquidity, revealing improvements in its financial position. The report examines the company's revenue growth, cost management, asset utilization, and profitability ratios, highlighting strong net and gross profit margins. Furthermore, it assesses the value created for shareholders by analyzing earnings per share and the valuation of the company's shares in the market. The report also covers the company's cash management, including the impact of operations on cash flow and other sources and uses of cash, providing a detailed overview of the company's financial health and performance.

Accounting Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Part 1..........................................................................................................................................4

Part 2..........................................................................................................................................6

1. An assessment of the financial status of the company including.......................................6

a. The company’s financial position as at the reporting date.............................................6

b. The capital structure of the company.............................................................................6

c. The liquidity of the company.........................................................................................8

2. An assessment of the financial performance of the company over the last 2 years

including...............................................................................................................................11

a. The company’s revenue growth...................................................................................11

b. The company’s management of its different category of cost and capital. The

company’s efficient use of its assets................................................................................12

3. An assessment of the value created by the company for its shareholders over the last two

years including.....................................................................................................................13

a. The earnings returned on each share............................................................................13

b. The earnings paid to shareholders on each share.........................................................13

c. The valuation of the company’s shares in the market..................................................14

4. An assessment of the company’s cash management including........................................16

a. The impact of the company’s operations on its cash flow...........................................16

b. The company’s other sources and uses of cash............................................................17

Part 3........................................................................................................................................18

Conclusion................................................................................................................................21

References................................................................................................................................22

Introduction................................................................................................................................3

Part 1..........................................................................................................................................4

Part 2..........................................................................................................................................6

1. An assessment of the financial status of the company including.......................................6

a. The company’s financial position as at the reporting date.............................................6

b. The capital structure of the company.............................................................................6

c. The liquidity of the company.........................................................................................8

2. An assessment of the financial performance of the company over the last 2 years

including...............................................................................................................................11

a. The company’s revenue growth...................................................................................11

b. The company’s management of its different category of cost and capital. The

company’s efficient use of its assets................................................................................12

3. An assessment of the value created by the company for its shareholders over the last two

years including.....................................................................................................................13

a. The earnings returned on each share............................................................................13

b. The earnings paid to shareholders on each share.........................................................13

c. The valuation of the company’s shares in the market..................................................14

4. An assessment of the company’s cash management including........................................16

a. The impact of the company’s operations on its cash flow...........................................16

b. The company’s other sources and uses of cash............................................................17

Part 3........................................................................................................................................18

Conclusion................................................................................................................................21

References................................................................................................................................22

Introduction

One of the most effective method of evaluating financial performance and financial position

of a company is with the help of financial statement analysis. Conclusions made with the help

of financial statement analysis are accurate and relevant as search conclusions are based on

accurate data provided in financial statements at the end of every year (Morden, 2016).

Financial statement analysis a can be very helpful in evaluating internal growth of a company

by comparing financial position of the company at the end of different financial year. Main

purpose of this report is to evaluate different financial aspects of Kingston Wharves Limited

which is the business organization operating in Jamaica. Primary financial aspects that will be

under consideration in this financial statement analysis report are profitability, liquidity,

efficiency and solvency. It is also provided that to shareholders of the company expects a

return of 10% from this business organization and this report will evaluate the whether

company has been able to achieve search expectation by analysing return on capital assets

(Hill, Jones & Schilling, 2014).

One of the most effective method of evaluating financial performance and financial position

of a company is with the help of financial statement analysis. Conclusions made with the help

of financial statement analysis are accurate and relevant as search conclusions are based on

accurate data provided in financial statements at the end of every year (Morden, 2016).

Financial statement analysis a can be very helpful in evaluating internal growth of a company

by comparing financial position of the company at the end of different financial year. Main

purpose of this report is to evaluate different financial aspects of Kingston Wharves Limited

which is the business organization operating in Jamaica. Primary financial aspects that will be

under consideration in this financial statement analysis report are profitability, liquidity,

efficiency and solvency. It is also provided that to shareholders of the company expects a

return of 10% from this business organization and this report will evaluate the whether

company has been able to achieve search expectation by analysing return on capital assets

(Hill, Jones & Schilling, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1

Long term security can be defined as the securities that cannot be converted into cash before

12 months of its issue date. Management of the company should make investment in this type

of security if liquidity position of the company is already strong and they want to earn extra

income on additional cash available with the company. This is due to the fact that interest

available on long-term securities is higher as compared to short term securities (Hoesli &

MacGregor, 2014). Following are some of the long term securities available in financial

market along with their advantages and disadvantages-

Investment in subsidiaries- Investment can be made by Business organizations in other

business organizations for long period of time. It is important that such securities should not

be categorised as "held for trading purposes". Such investments will be considered as a short

term securities if categorised as held for trading purposes. Primary advantage of such

investment is that it will help in merger and acquisition decision to be made in future.

Disadvantage of this method is that profitability on investment is totally dependent on

operational efficiency of subsidiaries and probability of loss in this type of investment are

very high.

Bonds

Bonds can be defined as fixed interest securities that are issued as debt component by

business organizations for other investors. Bonds are generally issued by government

organizations rather than business organizations. Primary advantage of investment in this

type of security is that there is no risk associated with investment and interest will be

provided at regular interval of time. Disadvantage of investment in this security is that returns

available are very low (Chandra, 2017). In addition to that there is a lock-in period before

which investors cannot realise their investment into cash.

Preference shares

This security can be defined as a combination of debt and equity component as it has

properties of both these type securities. Fixed rate of interest is available on preference shares

issued by Business organizations to their investors and certain rights are available to

preference shareholders that are similar to equity shareholders (DeFusco, McLeavey, Pinto,

Anson & Runkle, 2015). Advantage of investing in preference share is that interest available

Long term security can be defined as the securities that cannot be converted into cash before

12 months of its issue date. Management of the company should make investment in this type

of security if liquidity position of the company is already strong and they want to earn extra

income on additional cash available with the company. This is due to the fact that interest

available on long-term securities is higher as compared to short term securities (Hoesli &

MacGregor, 2014). Following are some of the long term securities available in financial

market along with their advantages and disadvantages-

Investment in subsidiaries- Investment can be made by Business organizations in other

business organizations for long period of time. It is important that such securities should not

be categorised as "held for trading purposes". Such investments will be considered as a short

term securities if categorised as held for trading purposes. Primary advantage of such

investment is that it will help in merger and acquisition decision to be made in future.

Disadvantage of this method is that profitability on investment is totally dependent on

operational efficiency of subsidiaries and probability of loss in this type of investment are

very high.

Bonds

Bonds can be defined as fixed interest securities that are issued as debt component by

business organizations for other investors. Bonds are generally issued by government

organizations rather than business organizations. Primary advantage of investment in this

type of security is that there is no risk associated with investment and interest will be

provided at regular interval of time. Disadvantage of investment in this security is that returns

available are very low (Chandra, 2017). In addition to that there is a lock-in period before

which investors cannot realise their investment into cash.

Preference shares

This security can be defined as a combination of debt and equity component as it has

properties of both these type securities. Fixed rate of interest is available on preference shares

issued by Business organizations to their investors and certain rights are available to

preference shareholders that are similar to equity shareholders (DeFusco, McLeavey, Pinto,

Anson & Runkle, 2015). Advantage of investing in preference share is that interest available

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on preference shares is higher as compared to bonds and risk free returns available in market.

In addition to that certain rights are also available to equity shareholders in the company by

which such securities are issued. Disadvantage of investing and preference share is that

principal amount will be received back by the investor after the term for which preference

share are issued will end (Szegö, 2014).

In addition to that certain rights are also available to equity shareholders in the company by

which such securities are issued. Disadvantage of investing and preference share is that

principal amount will be received back by the investor after the term for which preference

share are issued will end (Szegö, 2014).

Part 2

1. An assessment of the financial status of the company including

a. The company’s financial position as at the reporting date

Financial position of a company can be identified with the help of a total assets available in

the organization on the reporting date of balance sheet. Total Assets of this organization has

increased from $29475959000 in the year 2017 to $31456820000 in the year 2018. On the

basis of this evaluation it can be said that to financial position of the company has improved

by 6.72 percent in the one year of operation. In addition to that total revenue generated by the

company in the year 20 18 has also improved by 13% as compared to 2017 (Robinson,

Henry, Pirie & Broihahn, 2015). Therefore it can be said that there has been an improvement

in financial position and performance of the company in the one year of operation.

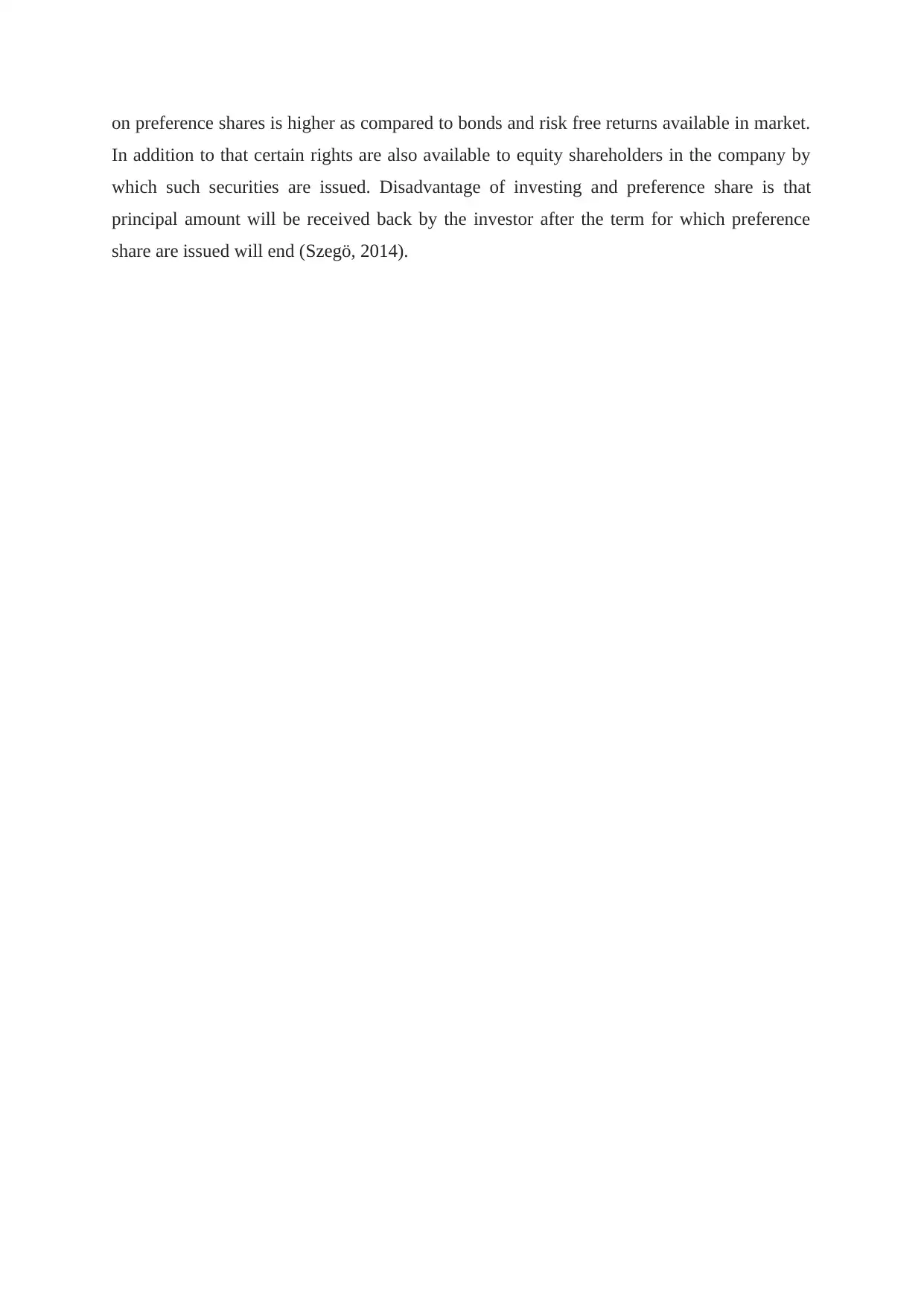

b. The capital structure of the company

Capital structure ratio 2018 2017

Total long term debt (A) 2273629 2385038

Total equity shareholders fund

(B) 24907132 23097317

Total assets '(C) 31456820 29475959

Debt Ratio (A/C) 0.072 0.081

Debt to equity ratio (A/B) 0.091 0.103

Capitalisation Ratio(A/(A+B)) 0.084 0.094

Capital Structure ratio

Effective and efficient capital structure in a business organization is defined by effective

balance between equity and debt component.

Debt Ratio (Total Debt to Total Assets): Total Debt ÷ Total Assets

1. An assessment of the financial status of the company including

a. The company’s financial position as at the reporting date

Financial position of a company can be identified with the help of a total assets available in

the organization on the reporting date of balance sheet. Total Assets of this organization has

increased from $29475959000 in the year 2017 to $31456820000 in the year 2018. On the

basis of this evaluation it can be said that to financial position of the company has improved

by 6.72 percent in the one year of operation. In addition to that total revenue generated by the

company in the year 20 18 has also improved by 13% as compared to 2017 (Robinson,

Henry, Pirie & Broihahn, 2015). Therefore it can be said that there has been an improvement

in financial position and performance of the company in the one year of operation.

b. The capital structure of the company

Capital structure ratio 2018 2017

Total long term debt (A) 2273629 2385038

Total equity shareholders fund

(B) 24907132 23097317

Total assets '(C) 31456820 29475959

Debt Ratio (A/C) 0.072 0.081

Debt to equity ratio (A/B) 0.091 0.103

Capitalisation Ratio(A/(A+B)) 0.084 0.094

Capital Structure ratio

Effective and efficient capital structure in a business organization is defined by effective

balance between equity and debt component.

Debt Ratio (Total Debt to Total Assets): Total Debt ÷ Total Assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

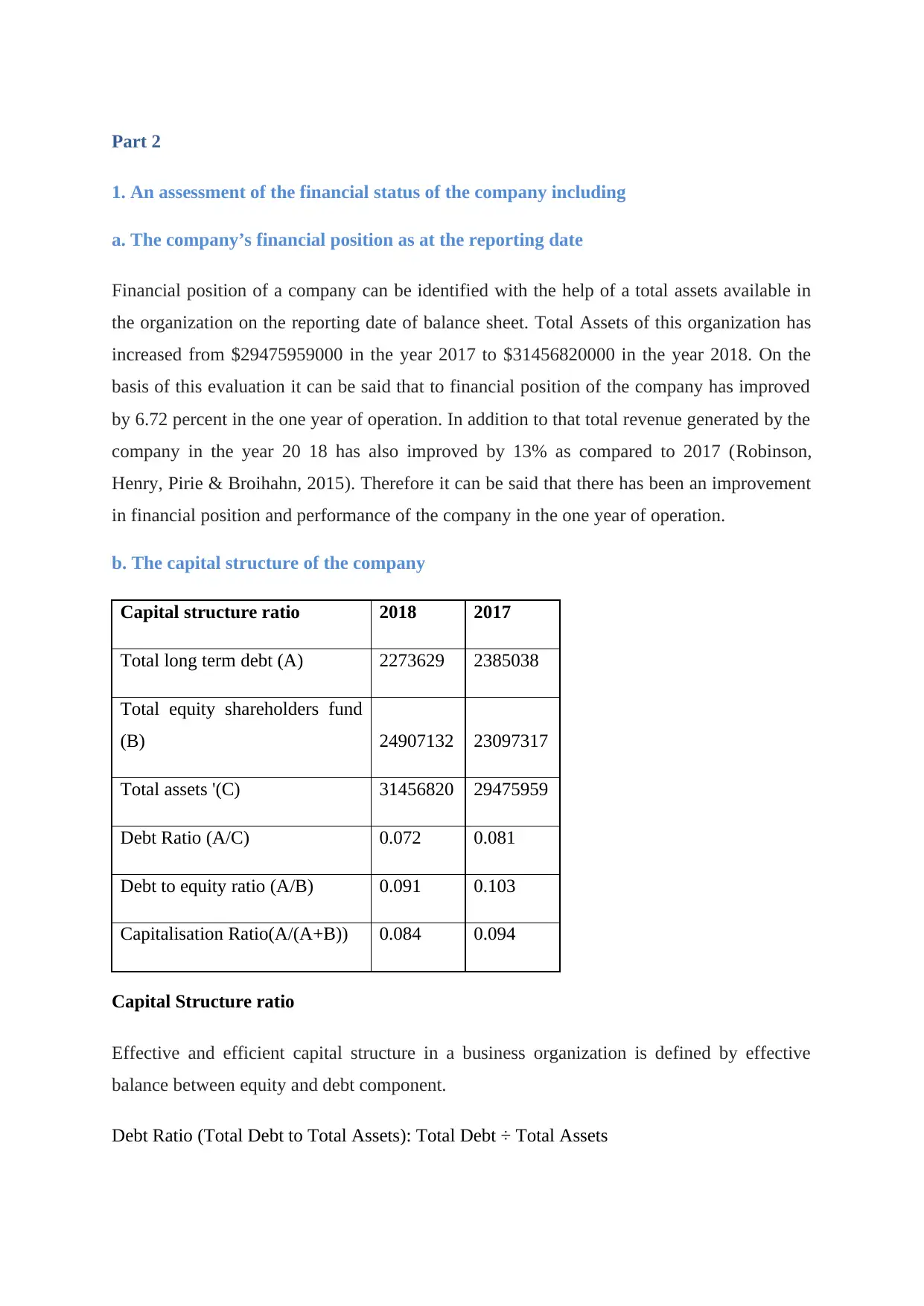

Debt to Equity Ratio: Total Debt ÷ Total shareholders fund

Capitalisation Ratio: Long-term debt ÷ long-term debt + shareholders' equity

Capitalisation Ratio: Long-term debt ÷ long-term debt + shareholders' equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

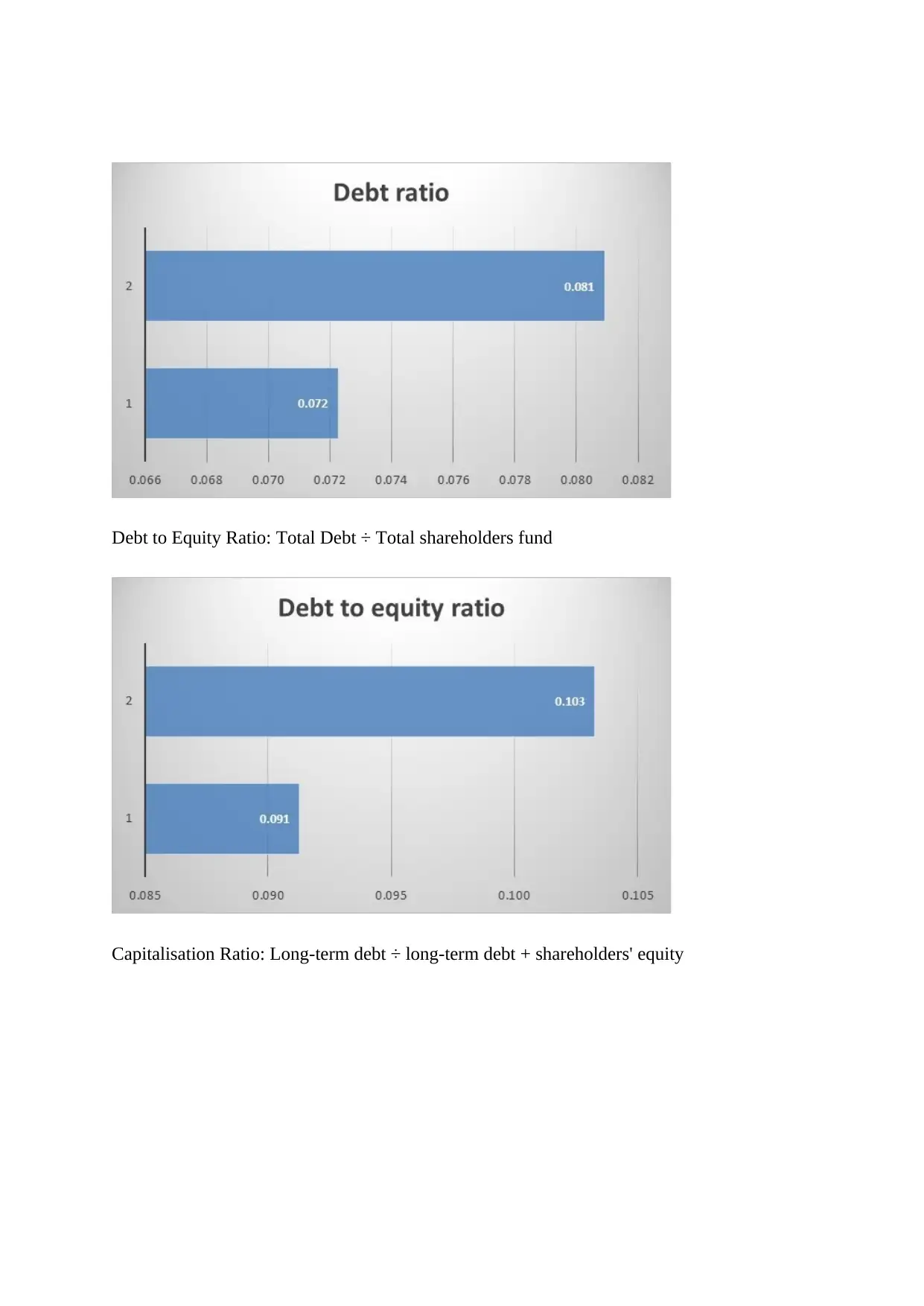

After analysing all the ratios listen to capital structure of the company it can be said that

majority of capital in Kingston limited has been financed with the help of equity shares. Total

amount of shareholders fund is significantly higher as compared to long term debt. This type

of a capital structure is effective in short run but it can be harmful for solvency position of the

company in long run (Wahlen, Baginski & Bradshaw, 2014).

Business organization by this type of capital structure is very common in this industry but it

will have negative impact on solvency position of the company as management would be

required to pay higher amount of dividend on equity shares. In addition to that equity tax will

also increase over the period of time with the increase in number of equity shares. One of the

primary advantage of using debt component for sourcing capital is that interest paid on long

term date is fixed and tax deductible. management of the company can easily make

arrangements in advance for such type of payments but this type of management is very

difficult for payment of equity shares as expectations of equity shareholders with respect to

returns will increase over the period of time (Cao, Chychyla & Stewart, 2015).

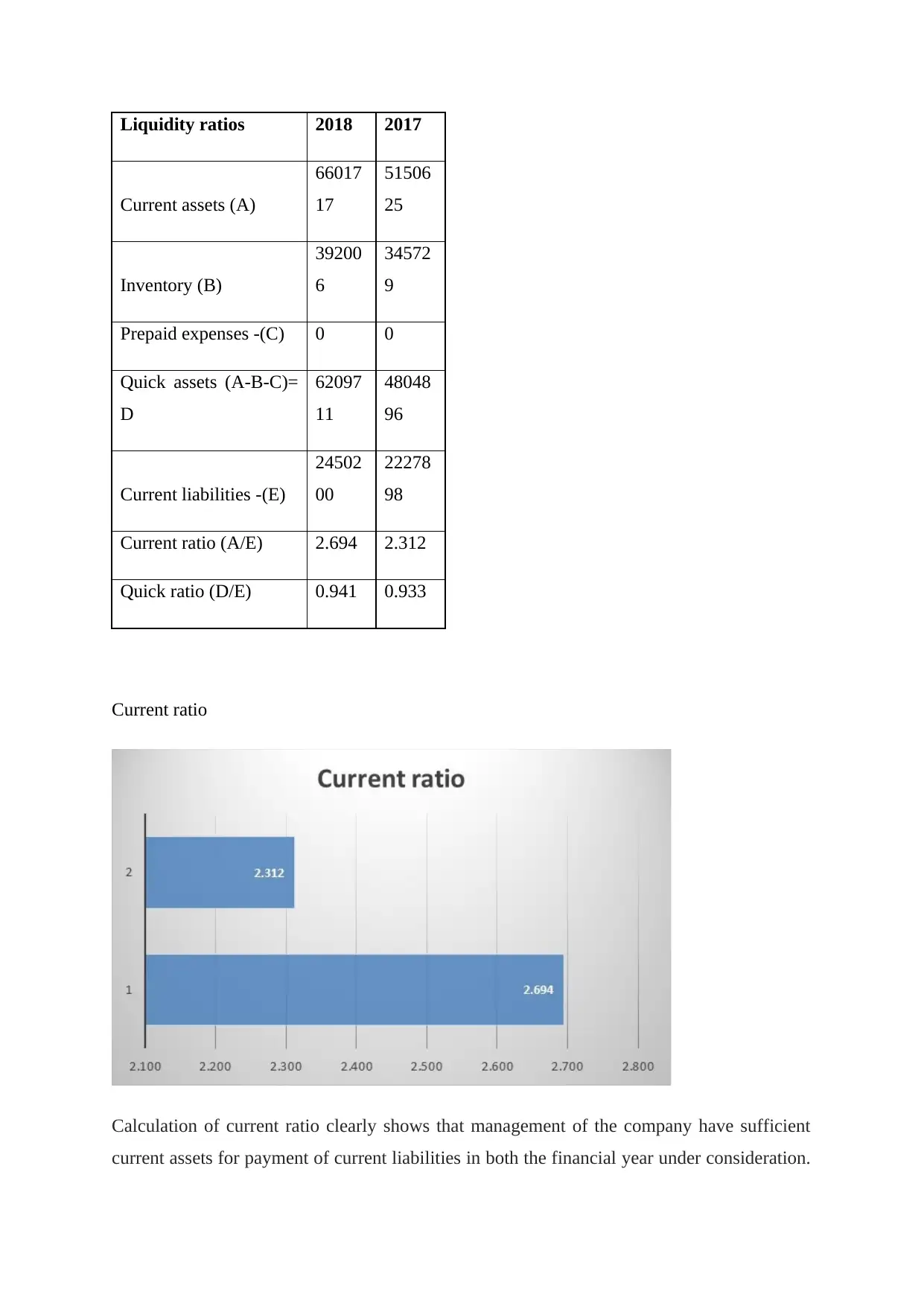

c. The liquidity of the company

Liquidity ratios

Short term liquidity position of a company can be identified by comparing current liabilities

with current assets i.e. management should have arranged payments in relation to current

liabilities by realising the amount from current assets. Optimum current ratio and acid test

ratio is 2 ratio 1 and 1 ratio 1 respectively (Brigham, Ehrhardt, Nason & Gessaroli, 2016).

majority of capital in Kingston limited has been financed with the help of equity shares. Total

amount of shareholders fund is significantly higher as compared to long term debt. This type

of a capital structure is effective in short run but it can be harmful for solvency position of the

company in long run (Wahlen, Baginski & Bradshaw, 2014).

Business organization by this type of capital structure is very common in this industry but it

will have negative impact on solvency position of the company as management would be

required to pay higher amount of dividend on equity shares. In addition to that equity tax will

also increase over the period of time with the increase in number of equity shares. One of the

primary advantage of using debt component for sourcing capital is that interest paid on long

term date is fixed and tax deductible. management of the company can easily make

arrangements in advance for such type of payments but this type of management is very

difficult for payment of equity shares as expectations of equity shareholders with respect to

returns will increase over the period of time (Cao, Chychyla & Stewart, 2015).

c. The liquidity of the company

Liquidity ratios

Short term liquidity position of a company can be identified by comparing current liabilities

with current assets i.e. management should have arranged payments in relation to current

liabilities by realising the amount from current assets. Optimum current ratio and acid test

ratio is 2 ratio 1 and 1 ratio 1 respectively (Brigham, Ehrhardt, Nason & Gessaroli, 2016).

Liquidity ratios 2018 2017

Current assets (A)

66017

17

51506

25

Inventory (B)

39200

6

34572

9

Prepaid expenses -(C) 0 0

Quick assets (A-B-C)=

D

62097

11

48048

96

Current liabilities -(E)

24502

00

22278

98

Current ratio (A/E) 2.694 2.312

Quick ratio (D/E) 0.941 0.933

Current ratio

Calculation of current ratio clearly shows that management of the company have sufficient

current assets for payment of current liabilities in both the financial year under consideration.

Current assets (A)

66017

17

51506

25

Inventory (B)

39200

6

34572

9

Prepaid expenses -(C) 0 0

Quick assets (A-B-C)=

D

62097

11

48048

96

Current liabilities -(E)

24502

00

22278

98

Current ratio (A/E) 2.694 2.312

Quick ratio (D/E) 0.941 0.933

Current ratio

Calculation of current ratio clearly shows that management of the company have sufficient

current assets for payment of current liabilities in both the financial year under consideration.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

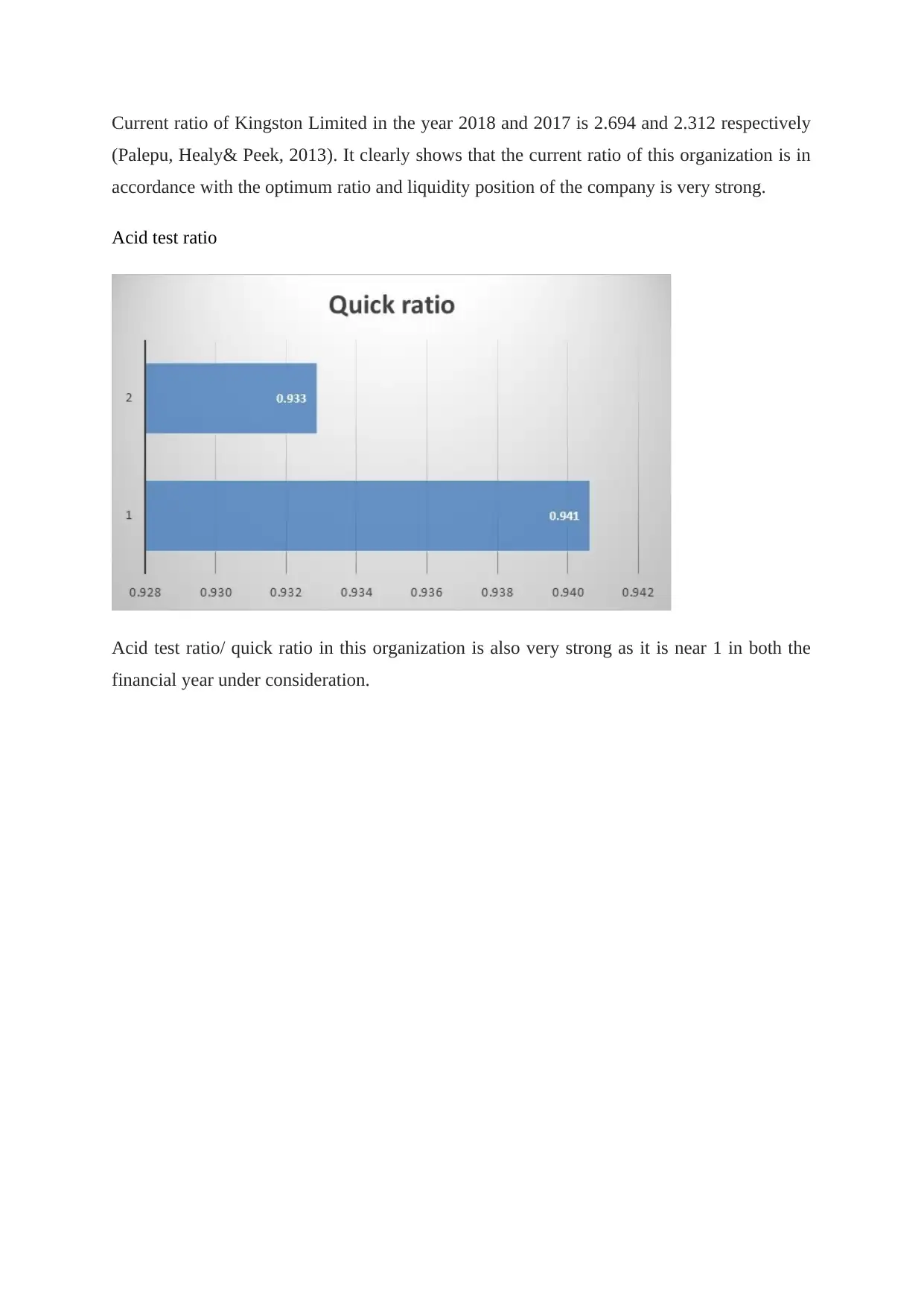

Current ratio of Kingston Limited in the year 2018 and 2017 is 2.694 and 2.312 respectively

(Palepu, Healy& Peek, 2013). It clearly shows that the current ratio of this organization is in

accordance with the optimum ratio and liquidity position of the company is very strong.

Acid test ratio

Acid test ratio/ quick ratio in this organization is also very strong as it is near 1 in both the

financial year under consideration.

(Palepu, Healy& Peek, 2013). It clearly shows that the current ratio of this organization is in

accordance with the optimum ratio and liquidity position of the company is very strong.

Acid test ratio

Acid test ratio/ quick ratio in this organization is also very strong as it is near 1 in both the

financial year under consideration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. An assessment of the financial performance of the company over the last 2 years

including

a. The company’s revenue growth

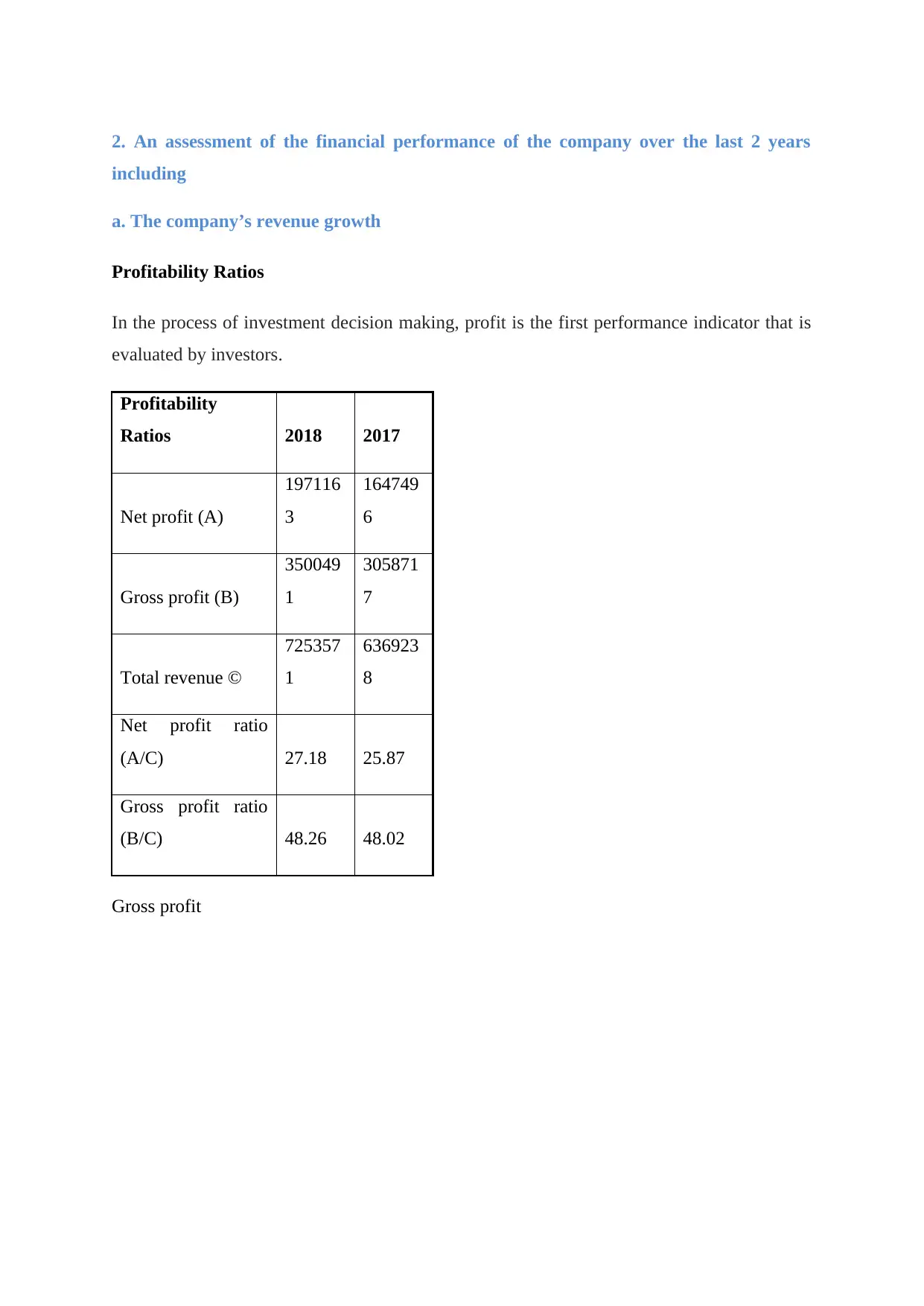

Profitability Ratios

In the process of investment decision making, profit is the first performance indicator that is

evaluated by investors.

Profitability

Ratios 2018 2017

Net profit (A)

197116

3

164749

6

Gross profit (B)

350049

1

305871

7

Total revenue ©

725357

1

636923

8

Net profit ratio

(A/C) 27.18 25.87

Gross profit ratio

(B/C) 48.26 48.02

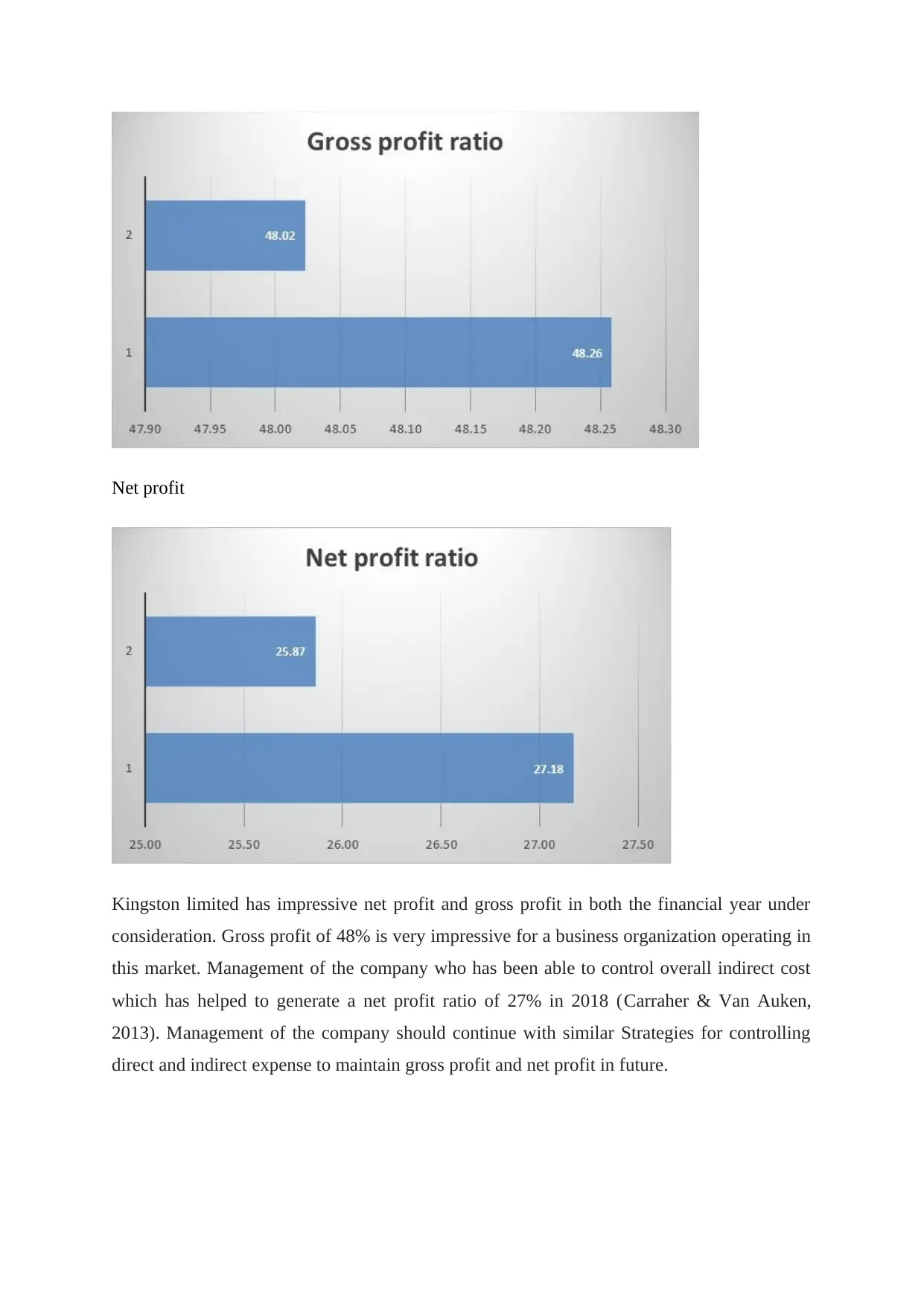

Gross profit

including

a. The company’s revenue growth

Profitability Ratios

In the process of investment decision making, profit is the first performance indicator that is

evaluated by investors.

Profitability

Ratios 2018 2017

Net profit (A)

197116

3

164749

6

Gross profit (B)

350049

1

305871

7

Total revenue ©

725357

1

636923

8

Net profit ratio

(A/C) 27.18 25.87

Gross profit ratio

(B/C) 48.26 48.02

Gross profit

Net profit

Kingston limited has impressive net profit and gross profit in both the financial year under

consideration. Gross profit of 48% is very impressive for a business organization operating in

this market. Management of the company who has been able to control overall indirect cost

which has helped to generate a net profit ratio of 27% in 2018 (Carraher & Van Auken,

2013). Management of the company should continue with similar Strategies for controlling

direct and indirect expense to maintain gross profit and net profit in future.

Kingston limited has impressive net profit and gross profit in both the financial year under

consideration. Gross profit of 48% is very impressive for a business organization operating in

this market. Management of the company who has been able to control overall indirect cost

which has helped to generate a net profit ratio of 27% in 2018 (Carraher & Van Auken,

2013). Management of the company should continue with similar Strategies for controlling

direct and indirect expense to maintain gross profit and net profit in future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.