University Financial Accounting Report: Accounts, Revenue, Errors

VerifiedAdded on 2023/01/17

|11

|1957

|79

Report

AI Summary

This report provides a detailed analysis of various financial accounting topics. Part I focuses on accounts receivable and inventories using Burberry's annual report, examining topics such as trade receivables and inventory valuation. Part II delves into long-term revenue recognition, applying the percentage of completion method to a construction project. Part III investigates financial statement errors, identifying their impact on assets, liabilities, and retained earnings. Finally, Part IV explores accruals and earnings management, analyzing scenarios involving unearned revenue and unethical accounting practices. The report includes calculations, explanations, and references to relevant accounting literature and the Burberry annual report.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Table of Contents

Part I: Accounts Receivable and Inventories – Burberry...........................................................3

Question 1:.............................................................................................................................3

Question 2:.............................................................................................................................3

Question 3:.............................................................................................................................4

Question 4:.............................................................................................................................4

Question 5:.............................................................................................................................4

Question 6:.............................................................................................................................4

Part II: Long-term revenue recognition......................................................................................5

Question 1:.............................................................................................................................5

Question 2:.............................................................................................................................5

Question 3:.............................................................................................................................6

Question 4:.............................................................................................................................6

Part III: Financial Statement Errors...........................................................................................6

Question 1:.............................................................................................................................6

Question 2:.............................................................................................................................7

Question 3:.............................................................................................................................7

Part IV: Accruals and Earnings Management............................................................................8

Question 1:.............................................................................................................................8

Question 2:.............................................................................................................................8

Question 3:.............................................................................................................................9

Table of Contents

Part I: Accounts Receivable and Inventories – Burberry...........................................................3

Question 1:.............................................................................................................................3

Question 2:.............................................................................................................................3

Question 3:.............................................................................................................................4

Question 4:.............................................................................................................................4

Question 5:.............................................................................................................................4

Question 6:.............................................................................................................................4

Part II: Long-term revenue recognition......................................................................................5

Question 1:.............................................................................................................................5

Question 2:.............................................................................................................................5

Question 3:.............................................................................................................................6

Question 4:.............................................................................................................................6

Part III: Financial Statement Errors...........................................................................................6

Question 1:.............................................................................................................................6

Question 2:.............................................................................................................................7

Question 3:.............................................................................................................................7

Part IV: Accruals and Earnings Management............................................................................8

Question 1:.............................................................................................................................8

Question 2:.............................................................................................................................8

Question 3:.............................................................................................................................9

2FINANCIAL ACCOUNTING

References and Bibliographies:................................................................................................10

References and Bibliographies:................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

Part I: Accounts Receivable and Inventories – Burberry

Question 1:

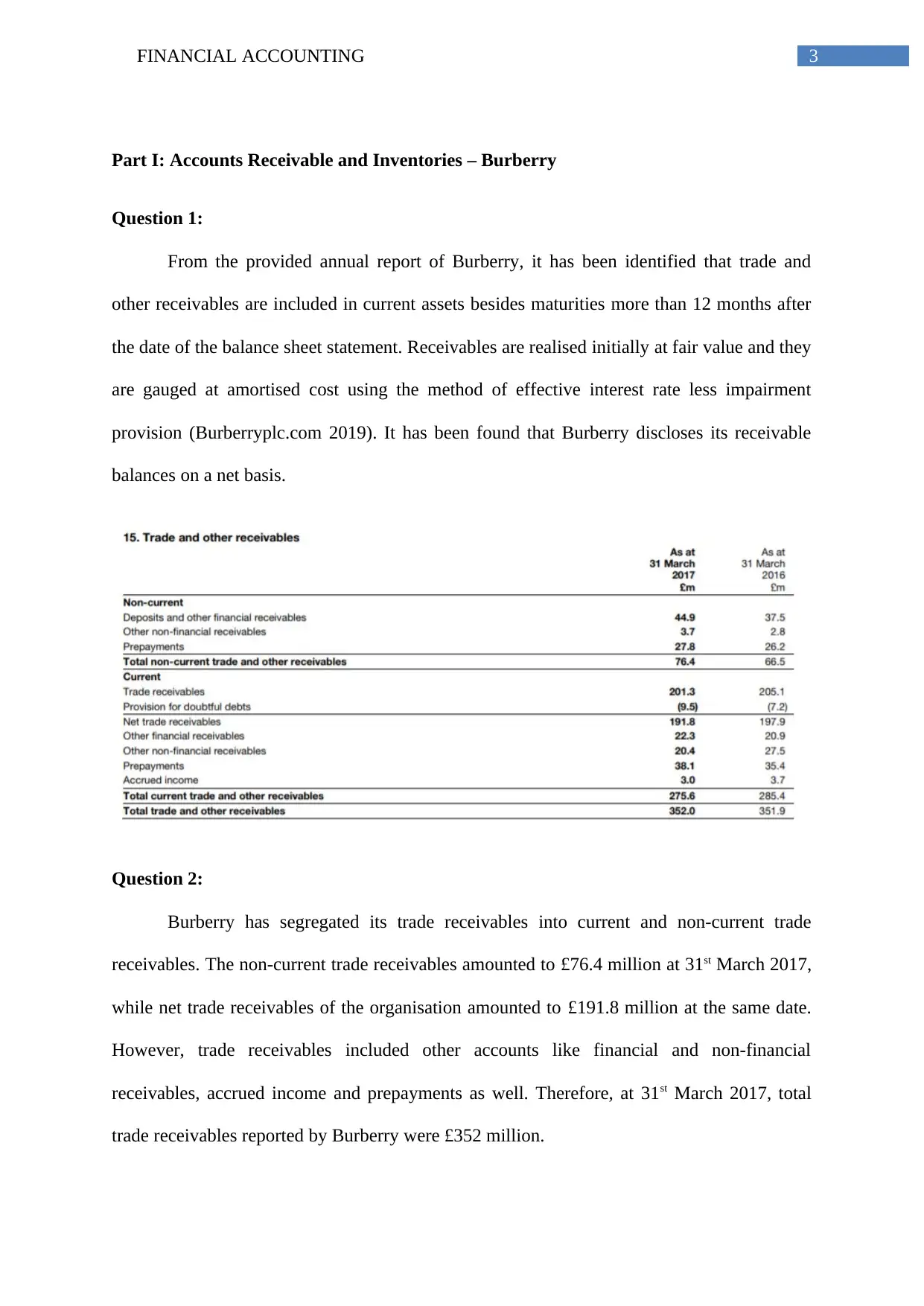

From the provided annual report of Burberry, it has been identified that trade and

other receivables are included in current assets besides maturities more than 12 months after

the date of the balance sheet statement. Receivables are realised initially at fair value and they

are gauged at amortised cost using the method of effective interest rate less impairment

provision (Burberryplc.com 2019). It has been found that Burberry discloses its receivable

balances on a net basis.

Question 2:

Burberry has segregated its trade receivables into current and non-current trade

receivables. The non-current trade receivables amounted to £76.4 million at 31st March 2017,

while net trade receivables of the organisation amounted to £191.8 million at the same date.

However, trade receivables included other accounts like financial and non-financial

receivables, accrued income and prepayments as well. Therefore, at 31st March 2017, total

trade receivables reported by Burberry were £352 million.

Part I: Accounts Receivable and Inventories – Burberry

Question 1:

From the provided annual report of Burberry, it has been identified that trade and

other receivables are included in current assets besides maturities more than 12 months after

the date of the balance sheet statement. Receivables are realised initially at fair value and they

are gauged at amortised cost using the method of effective interest rate less impairment

provision (Burberryplc.com 2019). It has been found that Burberry discloses its receivable

balances on a net basis.

Question 2:

Burberry has segregated its trade receivables into current and non-current trade

receivables. The non-current trade receivables amounted to £76.4 million at 31st March 2017,

while net trade receivables of the organisation amounted to £191.8 million at the same date.

However, trade receivables included other accounts like financial and non-financial

receivables, accrued income and prepayments as well. Therefore, at 31st March 2017, total

trade receivables reported by Burberry were £352 million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

Question 3:

From the segmental analysis disclosed in the 2017 annual report of Burberry, the

product division of the organisation mainly includes accessories, women’s clothing, men’s

clothing, children and other clothing and beauty products. Out of these four products, beauty

products of the organisation witnessed a decline from £202.5 million in 2015/16 to £184.4

million in 2016/17.

Question 4:

For measuring inventories, Burberry discloses them at lower of net realisable value or

lower of cost. The costs comprise of all purchase costs, conversion costs, design costs and

other costs spent on transferring the inventories to their current condition and location (Beatty

and Liao 2014). In case of inventories associated with the beauty product division including

finished products and raw materials, weighted average method is used for cost measurement.

In case of other product divisions, the determination of inventory cost is made by using First-

In-First-Out method by considering the fashion seasons for which there has been inventory

offer. During necessity, there is creation of provision for minimising cost to below or equal to

net realisable value in relation to condition and nature of inventory along with estimated

utilisation and saleability.

Question 5:

At 31st March 2017, the total inventory balance of inventory has been £505.3 million

out of which finished goods have amounted to £470.8 million. Therefore, the fraction of

finished goods in inventory has been 93.17% in 2017.

Question 6:

From the annual report of Burberry in 2017, it could be said that Burberry is a global

luxury brand based on UK involved in selling its products through wholesale and retail

Question 3:

From the segmental analysis disclosed in the 2017 annual report of Burberry, the

product division of the organisation mainly includes accessories, women’s clothing, men’s

clothing, children and other clothing and beauty products. Out of these four products, beauty

products of the organisation witnessed a decline from £202.5 million in 2015/16 to £184.4

million in 2016/17.

Question 4:

For measuring inventories, Burberry discloses them at lower of net realisable value or

lower of cost. The costs comprise of all purchase costs, conversion costs, design costs and

other costs spent on transferring the inventories to their current condition and location (Beatty

and Liao 2014). In case of inventories associated with the beauty product division including

finished products and raw materials, weighted average method is used for cost measurement.

In case of other product divisions, the determination of inventory cost is made by using First-

In-First-Out method by considering the fashion seasons for which there has been inventory

offer. During necessity, there is creation of provision for minimising cost to below or equal to

net realisable value in relation to condition and nature of inventory along with estimated

utilisation and saleability.

Question 5:

At 31st March 2017, the total inventory balance of inventory has been £505.3 million

out of which finished goods have amounted to £470.8 million. Therefore, the fraction of

finished goods in inventory has been 93.17% in 2017.

Question 6:

From the annual report of Burberry in 2017, it could be said that Burberry is a global

luxury brand based on UK involved in selling its products through wholesale and retail

5FINANCIAL ACCOUNTING

channels. For 2016/17, the organisation has accounted for 77% of sales revenue in retail and

22% in wholesale. In addition, it provides licensing agreements, which is 1% of total revenue

leveraging the technological expertise of the license partners.

Part II: Long-term revenue recognition

Question 1:

From the provided information, the cost incurred in 2016 by Balfour Beatty has been

£80 million. The estimated total cost of the project has been £240 million, while the price of

construction is £400 million. However, there has been no previous recognition of revenue.

Therefore, the revenue to be recognised from the contract in 2016 could be computed by

using the following formula:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £80/£240 x £400

Revenue = £133.33 million

Question 2:

By considering the above-formula, the revenue to be recognised in 2017 is calculated

as follows:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £ (80 + 60)/£260 x £400

Revenue = £215.38 million

channels. For 2016/17, the organisation has accounted for 77% of sales revenue in retail and

22% in wholesale. In addition, it provides licensing agreements, which is 1% of total revenue

leveraging the technological expertise of the license partners.

Part II: Long-term revenue recognition

Question 1:

From the provided information, the cost incurred in 2016 by Balfour Beatty has been

£80 million. The estimated total cost of the project has been £240 million, while the price of

construction is £400 million. However, there has been no previous recognition of revenue.

Therefore, the revenue to be recognised from the contract in 2016 could be computed by

using the following formula:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £80/£240 x £400

Revenue = £133.33 million

Question 2:

By considering the above-formula, the revenue to be recognised in 2017 is calculated

as follows:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £ (80 + 60)/£260 x £400

Revenue = £215.38 million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Question 3:

The same formula is used for calculating revenue recognition from the contract in

2019 or total:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £ (80 + 60 + 130)/£260 x £400

Revenue = £261.54 million

Question 4:

If Balfour Beatty uses the complete contract method rather than percentage of

completion method for revenue recognition, the total net income would be £130 million

(£400 million - $80 million - $60 million - $130 million), which is lower by £131.54 million

compared to the percentage of completion method.

Part III: Financial Statement Errors

Question 1:

Current Assets (O) 10,000 Long-term assets (U) 9,050

Current Liabilities NE Long-term liabilities (U)

Capital Stock NE Retained Earnings (O) 950

Explanation:

There is overstatement in current assets, since cash payment of $10,000 has not been

recorded that has resulted in overstatement of cash account and the entire current assets’

account. However, there is understatement in long-term assets, since the coffee machine

Question 3:

The same formula is used for calculating revenue recognition from the contract in

2019 or total:

Revenue = (Cost incurred until date/ Estimated total cost x Contract price) – Revenue

previously recognised

Revenue = £ (80 + 60 + 130)/£260 x £400

Revenue = £261.54 million

Question 4:

If Balfour Beatty uses the complete contract method rather than percentage of

completion method for revenue recognition, the total net income would be £130 million

(£400 million - $80 million - $60 million - $130 million), which is lower by £131.54 million

compared to the percentage of completion method.

Part III: Financial Statement Errors

Question 1:

Current Assets (O) 10,000 Long-term assets (U) 9,050

Current Liabilities NE Long-term liabilities (U)

Capital Stock NE Retained Earnings (O) 950

Explanation:

There is overstatement in current assets, since cash payment of $10,000 has not been

recorded that has resulted in overstatement of cash account and the entire current assets’

account. However, there is understatement in long-term assets, since the coffee machine

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

bought has not been recorded along with the depreciation incurred on it half-yearly. As a

result, this has caused understatement of long-term assets by $9,050. Moreover, due to non-

recording of depreciation expense, retained earnings have been overstated by $950.

Question 2:

Current Assets NE Long-term assets NE

Current Liabilities (U) $250,000 Long-term liabilities NE

Capital Stock NE Retained Earnings (O) $250,000

Explanation:

There has been understatement of current liabilities by $250,000, since out of

$750,000, 1/3rd of the amount has been for technical support. Due to the non-provision of

support in the year 2011, it would be adjudged as advance from the customer creating current

liabilities. Moreover, since technical support has not been provided in the past year, there

would be recognition of revenue in the period the services have been provided. Due to the

provision of service in the year 2012, there should be recognition of revenue in that year and

not in 2011.

Question 3:

Revenues NE

Expenses NE

Retained Earnings NE

Explanation:

bought has not been recorded along with the depreciation incurred on it half-yearly. As a

result, this has caused understatement of long-term assets by $9,050. Moreover, due to non-

recording of depreciation expense, retained earnings have been overstated by $950.

Question 2:

Current Assets NE Long-term assets NE

Current Liabilities (U) $250,000 Long-term liabilities NE

Capital Stock NE Retained Earnings (O) $250,000

Explanation:

There has been understatement of current liabilities by $250,000, since out of

$750,000, 1/3rd of the amount has been for technical support. Due to the non-provision of

support in the year 2011, it would be adjudged as advance from the customer creating current

liabilities. Moreover, since technical support has not been provided in the past year, there

would be recognition of revenue in the period the services have been provided. Due to the

provision of service in the year 2012, there should be recognition of revenue in that year and

not in 2011.

Question 3:

Revenues NE

Expenses NE

Retained Earnings NE

Explanation:

8FINANCIAL ACCOUNTING

According to the method of percentage completion, there would be realisation of

revenue in accordance with the percentage of project completion. Percentage completion is

computed by dividing period revenue by total project revenue (Henderson et al. 2015). In this

case, percentage completed is 66.67% (2/3 x 100) and thus, revenue recognised is 66.67 % of

£3 billion and the amount stands at £2 billion. This denotes the recognition of expenses as per

the actual figure. Therefore, there has been accurate recognition of expenses, revenues and

retained earnings.

Part IV: Accruals and Earnings Management

Question 1:

Service revenue of £8,000 is still unearned due to the non-completion of services until

January 2017. There has been improper record of sales amounting to £8,000. The

organisation has informed the accountant of not recording accrued salary of £12,000 along

with expired prepaid rent of £1,000. The non-recognition of these expenses has resulted in

excess revenue and ultimately, the impact is on net income.

Items Amount (in £)

Improper record of service revenue 8,000

Accrued salaries expense 12,000

Rent expense 1,000

Total overstated net profit 21,000

Question 2:

The carpenter has advised the accountant of not recording adjusting entries due to the

requirement of funds for the organisation along with enhanced income statement

According to the method of percentage completion, there would be realisation of

revenue in accordance with the percentage of project completion. Percentage completion is

computed by dividing period revenue by total project revenue (Henderson et al. 2015). In this

case, percentage completed is 66.67% (2/3 x 100) and thus, revenue recognised is 66.67 % of

£3 billion and the amount stands at £2 billion. This denotes the recognition of expenses as per

the actual figure. Therefore, there has been accurate recognition of expenses, revenues and

retained earnings.

Part IV: Accruals and Earnings Management

Question 1:

Service revenue of £8,000 is still unearned due to the non-completion of services until

January 2017. There has been improper record of sales amounting to £8,000. The

organisation has informed the accountant of not recording accrued salary of £12,000 along

with expired prepaid rent of £1,000. The non-recognition of these expenses has resulted in

excess revenue and ultimately, the impact is on net income.

Items Amount (in £)

Improper record of service revenue 8,000

Accrued salaries expense 12,000

Rent expense 1,000

Total overstated net profit 21,000

Question 2:

The carpenter has advised the accountant of not recording adjusting entries due to the

requirement of funds for the organisation along with enhanced income statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ACCOUNTING

performance. This action is unethical, as the organisation could obtain loan on cheaper

interest rate (De Waegenaere, Sansing and Wielhouwer 2015). In this situation, the banks

providing loans would be affected owing to wrong interpretation of figures in the income

statement. Moreover, there would be default risk on the banks due to the action of the

carpenter in hiding expenses. The effect would be on the investors as well for wrong

representation of net income, since they would invest in the organisation by seeing higher

income (Hoyle, Schaefer and Doupnik 2015). However, the situation is different, since the

organisation has lower income compared to the figure shown in the current income statement.

Question 3:

The accountants have to follow the code of conduct at the time of preparing financial

statements. They are liable to depict accurate figures for disclosing the actual performance of

the organisation (Warren and Jones 2018). Therefore, the accountant needs to refuse the

instructions of the carpenter to hide expenses and disclose unearned revenue in the form of

earned revenue. By conducting the same, there would no breach of the code of conduct on the

part of the accountant.

performance. This action is unethical, as the organisation could obtain loan on cheaper

interest rate (De Waegenaere, Sansing and Wielhouwer 2015). In this situation, the banks

providing loans would be affected owing to wrong interpretation of figures in the income

statement. Moreover, there would be default risk on the banks due to the action of the

carpenter in hiding expenses. The effect would be on the investors as well for wrong

representation of net income, since they would invest in the organisation by seeing higher

income (Hoyle, Schaefer and Doupnik 2015). However, the situation is different, since the

organisation has lower income compared to the figure shown in the current income statement.

Question 3:

The accountants have to follow the code of conduct at the time of preparing financial

statements. They are liable to depict accurate figures for disclosing the actual performance of

the organisation (Warren and Jones 2018). Therefore, the accountant needs to refuse the

instructions of the carpenter to hide expenses and disclose unearned revenue in the form of

earned revenue. By conducting the same, there would no breach of the code of conduct on the

part of the accountant.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ACCOUNTING

References and Bibliographies:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Burberryplc.com., 2019. [online] Available at:

https://www.burberryplc.com/content/dam/burberry/corporate/Investors/Results_Reports/

2017/AnnualReport/Burberry_AR_2016-17.pdf [Accessed 11 Apr. 2019].

De Waegenaere, A., Sansing, R. and Wielhouwer, J.L., 2015. Financial accounting effects of

tax aggressiveness: Contracting and measurement. Contemporary Accounting

Research, 32(1), pp.223-242.

Gassen, J., 2014. Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society, 39(7), pp.535-544.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder

Ready Version. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning

Pvt. Ltd.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

References and Bibliographies:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Burberryplc.com., 2019. [online] Available at:

https://www.burberryplc.com/content/dam/burberry/corporate/Investors/Results_Reports/

2017/AnnualReport/Burberry_AR_2016-17.pdf [Accessed 11 Apr. 2019].

De Waegenaere, A., Sansing, R. and Wielhouwer, J.L., 2015. Financial accounting effects of

tax aggressiveness: Contracting and measurement. Contemporary Accounting

Research, 32(1), pp.223-242.

Gassen, J., 2014. Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society, 39(7), pp.535-544.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder

Ready Version. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning

Pvt. Ltd.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.