Semester 1 2018 UUAC5300 Assignment 2: Accounting and Finance Solution

VerifiedAdded on 2021/05/31

|15

|3222

|20

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting and finance assignment, focusing on financial statement analysis, ratio analysis, and budgeting. The solution begins with an evaluation of financial statements, including implications of various ratios like current ratio, quick ratio, asset turnover ratio, cash debt coverage, profit and earnings per share, to assess a company's financial health and debt worthiness. It then covers the calculation and significance of key ratios such as debt-equity ratio, interest coverage ratio, and debt ratio. Furthermore, the solution includes a horizontal analysis of net sales and profit after tax, providing insights into sales and profitability trends. It also presents a detailed ratio analysis of profitability, financial stability, and asset utilization, using data from New Zealand Post Group's annual reports. The assignment also includes a budgeting section with a schedule of expected cash receipts and a cash budget. The document offers valuable insights into financial statement analysis and management accounting tools for business decision-making.

1

Accounting and Finance for Executives – UUAC5300

Assignment - 2

Semester 1 - 2018

Accounting and Finance for Executives – UUAC5300

Assignment - 2

Semester 1 - 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Solution 1: Evaluation of financial statements and reporting findings

Answer 1.1:

A:

Following are implications of the ratio provided for the lending decision:

Current ratio: Current ratio reflects the ability of company to pay the short term

liabilities. In year 2016, the current ratio was 3.1 times whereas it was reduced to 2.1

times in year 2017. It indicates that short term solvency position of Borrower’s company

has been reduced in the current year as compared with previous year. The current ratio of

2.1 times in current year shows that company has enough assets to pay the current

liabilities as it arises.

Quick Ratio: Quick ratio is also an important indicator of liquidity position of the

company as it takes it into account only those assets those are capable of converting into

cash and cash equivalent very rapidly. Quick ratio of Borrowers Company has increased

in year 2017 as compared to previous year that shows improvement in quick assets and

company has now more assets to pay the short term liabilities.

Asset Turnover Ratio: This ratio indicates how frequently company uses total assets to

earn the revenue. This ratio has been decreased in year 2017 as compared to year 2016

that indicated company efficiency to use the assets to produce the revenue has been

decreased in current year (Damodaran, 2011).

Cash Debt Coverage: This ratio shows level of operating cash flows as against the debt

liabilities of the company. As this ratio is less than 1 it indicates that company has very

less cash flow to pay back the debt capital. Although, there has been rise in this ratio that

indicates increase in flow net cash flow from the operating activity.

Profit and Earning per share: Profit of company has been decreased in current year by

8% as compared with previous reflect the poor profitability position. The EPS of

Borrowers Company has also reduced from $3.30 to $2.50 that indicates poor position of

the company in the market in current year.

Although above ratios shows Company has stable liquidity position but poor profitability

position in the current year as compared to previous year made the financial position of the

Solution 1: Evaluation of financial statements and reporting findings

Answer 1.1:

A:

Following are implications of the ratio provided for the lending decision:

Current ratio: Current ratio reflects the ability of company to pay the short term

liabilities. In year 2016, the current ratio was 3.1 times whereas it was reduced to 2.1

times in year 2017. It indicates that short term solvency position of Borrower’s company

has been reduced in the current year as compared with previous year. The current ratio of

2.1 times in current year shows that company has enough assets to pay the current

liabilities as it arises.

Quick Ratio: Quick ratio is also an important indicator of liquidity position of the

company as it takes it into account only those assets those are capable of converting into

cash and cash equivalent very rapidly. Quick ratio of Borrowers Company has increased

in year 2017 as compared to previous year that shows improvement in quick assets and

company has now more assets to pay the short term liabilities.

Asset Turnover Ratio: This ratio indicates how frequently company uses total assets to

earn the revenue. This ratio has been decreased in year 2017 as compared to year 2016

that indicated company efficiency to use the assets to produce the revenue has been

decreased in current year (Damodaran, 2011).

Cash Debt Coverage: This ratio shows level of operating cash flows as against the debt

liabilities of the company. As this ratio is less than 1 it indicates that company has very

less cash flow to pay back the debt capital. Although, there has been rise in this ratio that

indicates increase in flow net cash flow from the operating activity.

Profit and Earning per share: Profit of company has been decreased in current year by

8% as compared with previous reflect the poor profitability position. The EPS of

Borrowers Company has also reduced from $3.30 to $2.50 that indicates poor position of

the company in the market in current year.

Although above ratios shows Company has stable liquidity position but poor profitability

position in the current year as compared to previous year made the financial position of the

3

company unfavorable. These ratios are not relevant for evaluating the debt worthiness of the

company.

B:

The three ratios that need to be calculated for analyzing the decision of the debt

worthiness are as follows:

Debt Equity Ratio: This ratio helps to know the level of debt against the shareholder

equity capital of the company. It will provide current level of debt and also shows

increase in debt level will change the capital structure to make it leveraged firm or not.

Interest Coverage Ratio: This ratio tells times the company can pay interest expenses on

the debt capital it is charge on the profitability of the company. This ratio will guide

whether company has enough profitability position to bear the increase in interest

expenses (Davies and Crawford, 2011).

Debt ratio: This ratio will provide information on level of debt capital used to finance

the total assets of the company.

C:

There are some drawbacks associated with the use of financial ratio analysis that limits

the application of technique in investing and credit decisions. The most significant limitation

associated with the use of ratio analysis technique is that it is not suitable to be used on a stand-

alone basis and the results obtained need to be benchmarked against some specific criteria such

as industry norm, aggregate economy and past performance. Also, it is not regarded to be a

useful technique for carrying out comparison of the financial performance of the companies that

differ on the basis of size and also belongs to different industry groups. The ratio analysis

sometimes does not provide an actual depiction of the financial performance of a company as the

financial statements are subjected to distortion by the economic and seasonal factors. In addition

to this, the use of different accounting methods and policies can provide uneven comparison of

the companies that belong to even same sectors. Also, there may be some good and some weak

financial ratios which make it difficult for investors to predict the future growth potential of the

company (Tracy, 2012).

company unfavorable. These ratios are not relevant for evaluating the debt worthiness of the

company.

B:

The three ratios that need to be calculated for analyzing the decision of the debt

worthiness are as follows:

Debt Equity Ratio: This ratio helps to know the level of debt against the shareholder

equity capital of the company. It will provide current level of debt and also shows

increase in debt level will change the capital structure to make it leveraged firm or not.

Interest Coverage Ratio: This ratio tells times the company can pay interest expenses on

the debt capital it is charge on the profitability of the company. This ratio will guide

whether company has enough profitability position to bear the increase in interest

expenses (Davies and Crawford, 2011).

Debt ratio: This ratio will provide information on level of debt capital used to finance

the total assets of the company.

C:

There are some drawbacks associated with the use of financial ratio analysis that limits

the application of technique in investing and credit decisions. The most significant limitation

associated with the use of ratio analysis technique is that it is not suitable to be used on a stand-

alone basis and the results obtained need to be benchmarked against some specific criteria such

as industry norm, aggregate economy and past performance. Also, it is not regarded to be a

useful technique for carrying out comparison of the financial performance of the companies that

differ on the basis of size and also belongs to different industry groups. The ratio analysis

sometimes does not provide an actual depiction of the financial performance of a company as the

financial statements are subjected to distortion by the economic and seasonal factors. In addition

to this, the use of different accounting methods and policies can provide uneven comparison of

the companies that belong to even same sectors. Also, there may be some good and some weak

financial ratios which make it difficult for investors to predict the future growth potential of the

company (Tracy, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

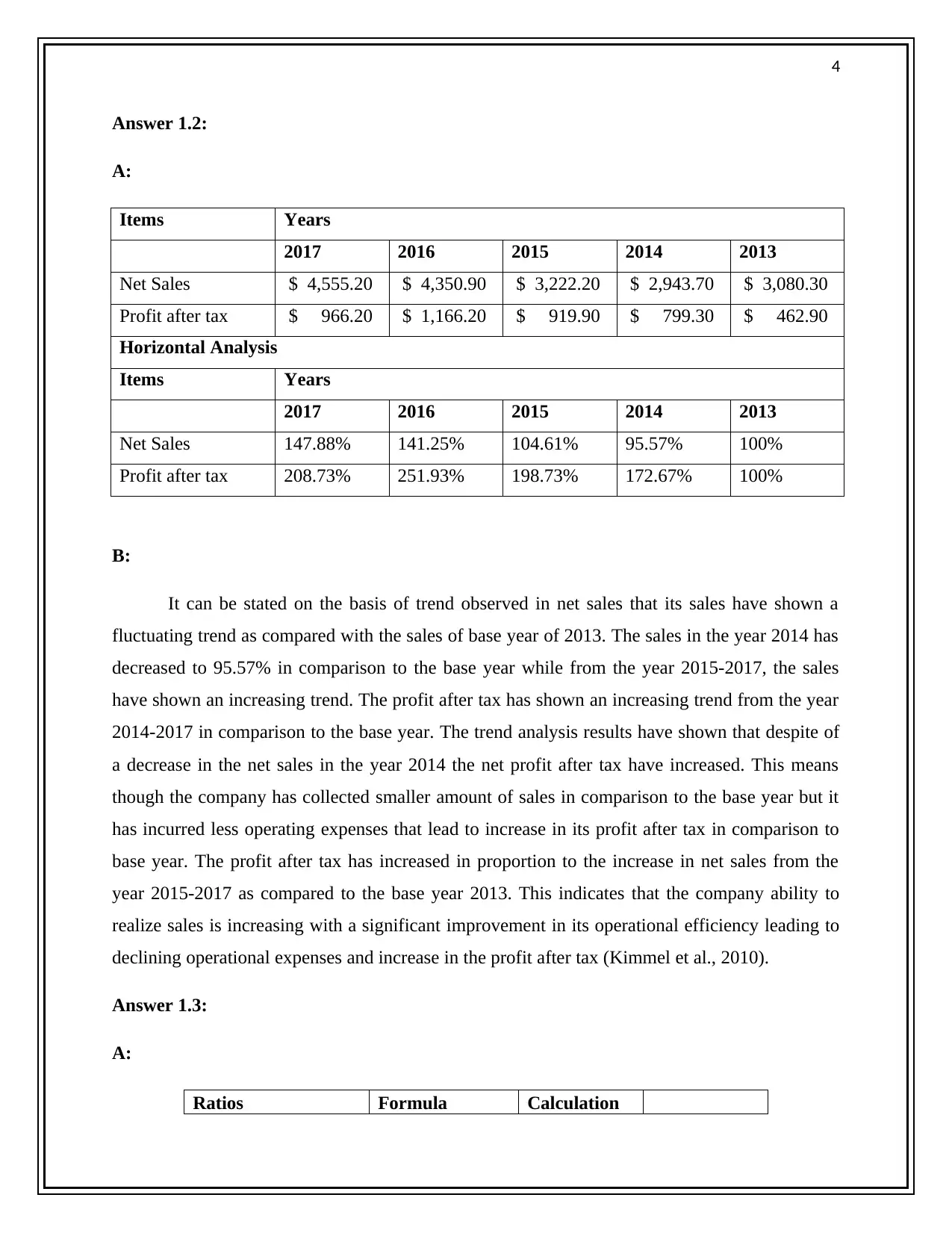

Answer 1.2:

A:

Items Years

2017 2016 2015 2014 2013

Net Sales $ 4,555.20 $ 4,350.90 $ 3,222.20 $ 2,943.70 $ 3,080.30

Profit after tax $ 966.20 $ 1,166.20 $ 919.90 $ 799.30 $ 462.90

Horizontal Analysis

Items Years

2017 2016 2015 2014 2013

Net Sales 147.88% 141.25% 104.61% 95.57% 100%

Profit after tax 208.73% 251.93% 198.73% 172.67% 100%

B:

It can be stated on the basis of trend observed in net sales that its sales have shown a

fluctuating trend as compared with the sales of base year of 2013. The sales in the year 2014 has

decreased to 95.57% in comparison to the base year while from the year 2015-2017, the sales

have shown an increasing trend. The profit after tax has shown an increasing trend from the year

2014-2017 in comparison to the base year. The trend analysis results have shown that despite of

a decrease in the net sales in the year 2014 the net profit after tax have increased. This means

though the company has collected smaller amount of sales in comparison to the base year but it

has incurred less operating expenses that lead to increase in its profit after tax in comparison to

base year. The profit after tax has increased in proportion to the increase in net sales from the

year 2015-2017 as compared to the base year 2013. This indicates that the company ability to

realize sales is increasing with a significant improvement in its operational efficiency leading to

declining operational expenses and increase in the profit after tax (Kimmel et al., 2010).

Answer 1.3:

A:

Ratios Formula Calculation

Answer 1.2:

A:

Items Years

2017 2016 2015 2014 2013

Net Sales $ 4,555.20 $ 4,350.90 $ 3,222.20 $ 2,943.70 $ 3,080.30

Profit after tax $ 966.20 $ 1,166.20 $ 919.90 $ 799.30 $ 462.90

Horizontal Analysis

Items Years

2017 2016 2015 2014 2013

Net Sales 147.88% 141.25% 104.61% 95.57% 100%

Profit after tax 208.73% 251.93% 198.73% 172.67% 100%

B:

It can be stated on the basis of trend observed in net sales that its sales have shown a

fluctuating trend as compared with the sales of base year of 2013. The sales in the year 2014 has

decreased to 95.57% in comparison to the base year while from the year 2015-2017, the sales

have shown an increasing trend. The profit after tax has shown an increasing trend from the year

2014-2017 in comparison to the base year. The trend analysis results have shown that despite of

a decrease in the net sales in the year 2014 the net profit after tax have increased. This means

though the company has collected smaller amount of sales in comparison to the base year but it

has incurred less operating expenses that lead to increase in its profit after tax in comparison to

base year. The profit after tax has increased in proportion to the increase in net sales from the

year 2015-2017 as compared to the base year 2013. This indicates that the company ability to

realize sales is increasing with a significant improvement in its operational efficiency leading to

declining operational expenses and increase in the profit after tax (Kimmel et al., 2010).

Answer 1.3:

A:

Ratios Formula Calculation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

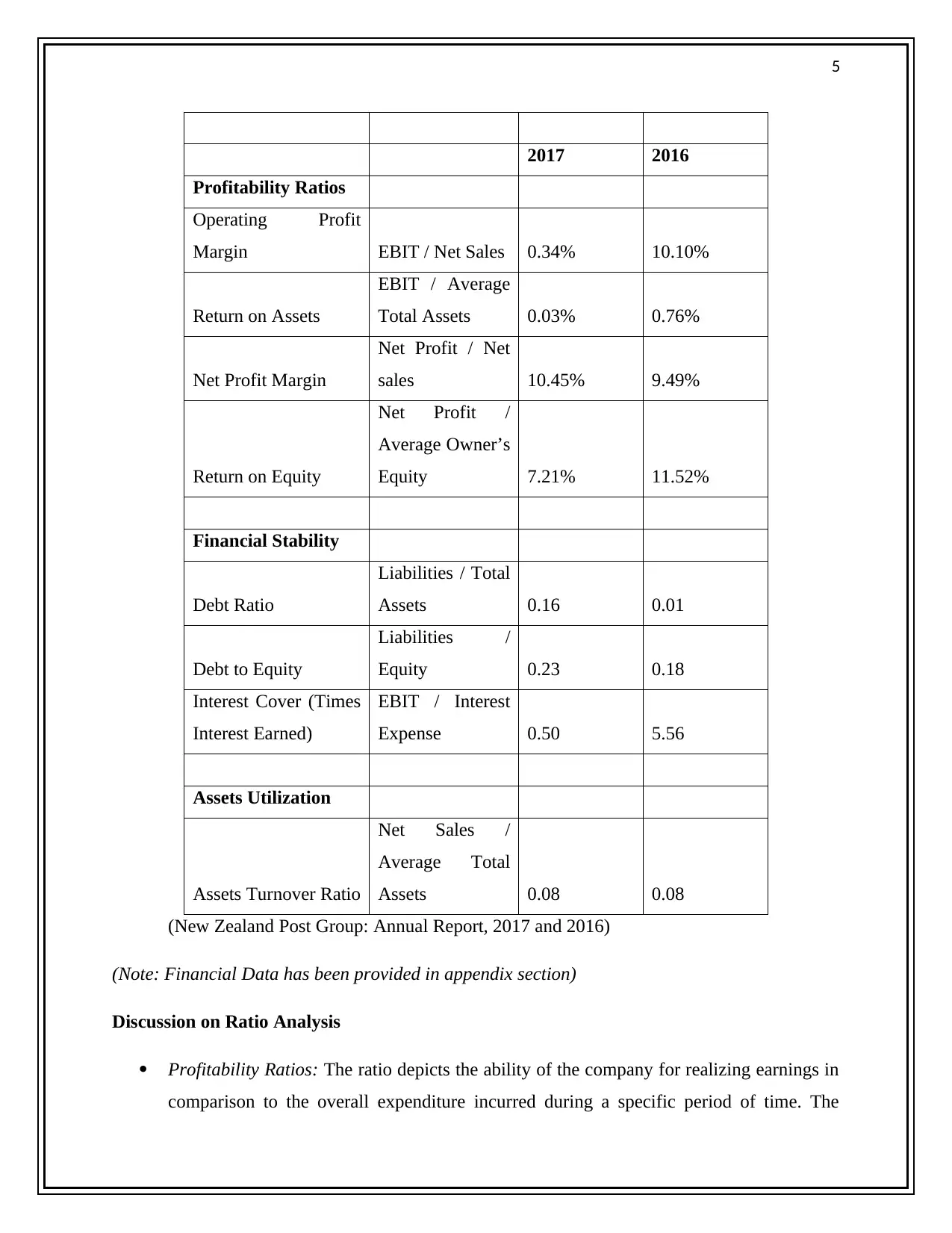

2017 2016

Profitability Ratios

Operating Profit

Margin EBIT / Net Sales 0.34% 10.10%

Return on Assets

EBIT / Average

Total Assets 0.03% 0.76%

Net Profit Margin

Net Profit / Net

sales 10.45% 9.49%

Return on Equity

Net Profit /

Average Owner’s

Equity 7.21% 11.52%

Financial Stability

Debt Ratio

Liabilities / Total

Assets 0.16 0.01

Debt to Equity

Liabilities /

Equity 0.23 0.18

Interest Cover (Times

Interest Earned)

EBIT / Interest

Expense 0.50 5.56

Assets Utilization

Assets Turnover Ratio

Net Sales /

Average Total

Assets 0.08 0.08

(New Zealand Post Group: Annual Report, 2017 and 2016)

(Note: Financial Data has been provided in appendix section)

Discussion on Ratio Analysis

Profitability Ratios: The ratio depicts the ability of the company for realizing earnings in

comparison to the overall expenditure incurred during a specific period of time. The

2017 2016

Profitability Ratios

Operating Profit

Margin EBIT / Net Sales 0.34% 10.10%

Return on Assets

EBIT / Average

Total Assets 0.03% 0.76%

Net Profit Margin

Net Profit / Net

sales 10.45% 9.49%

Return on Equity

Net Profit /

Average Owner’s

Equity 7.21% 11.52%

Financial Stability

Debt Ratio

Liabilities / Total

Assets 0.16 0.01

Debt to Equity

Liabilities /

Equity 0.23 0.18

Interest Cover (Times

Interest Earned)

EBIT / Interest

Expense 0.50 5.56

Assets Utilization

Assets Turnover Ratio

Net Sales /

Average Total

Assets 0.08 0.08

(New Zealand Post Group: Annual Report, 2017 and 2016)

(Note: Financial Data has been provided in appendix section)

Discussion on Ratio Analysis

Profitability Ratios: The ratio depicts the ability of the company for realizing earnings in

comparison to the overall expenditure incurred during a specific period of time. The

6

profitability position of New Zealand Post has been examined with the calculation of

following ratios:

Operating Profit Margin: It indicates the profit realized by the company after meeting its

variable cost of production. It is depicted from the calculation of the ratio from the above

table that its operating profit margin has decreased from 2016 to 2017 to a large extent.

Return on Assets: The return on assets ratio of the company has also comparatively

declined from 0.76% to 0.03% from the year 2016 to 2017 which depicts that its ability to

realize revenue from assets have decreased significantly (Lumby and Jones, 2007).

Net Profit Margin: Its net profit margin has increased significantly from 9.49% to 10.45%

in the year 206 to 2017. Thus, it indicates that the efficiency of New Zealand Post to

reduce its operational expenses has increased and this increases the percentage of revenue

available for the company after meeting all the significant expenses.

Return on Equity: The return on equity ratio of the company has decreased significantly

from 2016 to 2017 from 11.52% to 7.21%. This indicates that the ability of the company

to generate returns for the shareholders have reduced to a large extent (Tracy, 2012).

Financial Stability

Debt Ratio: The debt ratio of the company has increased from the year 2016 to 2017 as

depicted in the above table. This indicates that financial leverage on the company is

increasing.

Debt to Equity Ratio: The debt-equity ratio of the company has also increased over the

time period of 2016-2017 as presented in the above table. This indicates that company is

incorporating more debt in comparison to equity in the year 2017 as compared to the year

2016 (Moles and Kidwekk, 2011).

Interest Cover: The interest coverage ratio of the company has reduced to a large extent

from the year 2016 to 2017 as depicted in the above table. This indicates that the ability

of the company to meet its interest expenses on outstanding dent has reduced

(Szydlowska, 2018).

Assets Utilization

profitability position of New Zealand Post has been examined with the calculation of

following ratios:

Operating Profit Margin: It indicates the profit realized by the company after meeting its

variable cost of production. It is depicted from the calculation of the ratio from the above

table that its operating profit margin has decreased from 2016 to 2017 to a large extent.

Return on Assets: The return on assets ratio of the company has also comparatively

declined from 0.76% to 0.03% from the year 2016 to 2017 which depicts that its ability to

realize revenue from assets have decreased significantly (Lumby and Jones, 2007).

Net Profit Margin: Its net profit margin has increased significantly from 9.49% to 10.45%

in the year 206 to 2017. Thus, it indicates that the efficiency of New Zealand Post to

reduce its operational expenses has increased and this increases the percentage of revenue

available for the company after meeting all the significant expenses.

Return on Equity: The return on equity ratio of the company has decreased significantly

from 2016 to 2017 from 11.52% to 7.21%. This indicates that the ability of the company

to generate returns for the shareholders have reduced to a large extent (Tracy, 2012).

Financial Stability

Debt Ratio: The debt ratio of the company has increased from the year 2016 to 2017 as

depicted in the above table. This indicates that financial leverage on the company is

increasing.

Debt to Equity Ratio: The debt-equity ratio of the company has also increased over the

time period of 2016-2017 as presented in the above table. This indicates that company is

incorporating more debt in comparison to equity in the year 2017 as compared to the year

2016 (Moles and Kidwekk, 2011).

Interest Cover: The interest coverage ratio of the company has reduced to a large extent

from the year 2016 to 2017 as depicted in the above table. This indicates that the ability

of the company to meet its interest expenses on outstanding dent has reduced

(Szydlowska, 2018).

Assets Utilization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Asset Turnover ratio: The company have maintained a steady growth rate over the year

2016-2017 in relation to asset turnover as depicted in the above table. This indicates that

the value of its sales in relation to the value of its assets has remained steady (Ross, Jaffe

and Kakani, 2008).

Thus, it can be stated on the basis of profitability analysis of the company that its profit

earning capacity has reduced in the year 2017 as compared to the year 2016. In addition to this,

the financial stability ratios have indicated that it is adopting more use of debt in its capital

structure which is not a good sign for the future growth of the company. Also, it is not able to

improve its efficiency of generating sales from asset utilization. This all indicates that the

financial health of the company has deteriorated in the year 2017 as compared to the year 2016.

This is also not indicative of good sign of potential growth of the company (Papadopoulos,

2011).

B:

Cash flow from operating activity ratio provides an overall assessment of the liquidity

position of a company. It is calculated by dividing the cash flow from operations by the current

liabilities that need to be repaid by the company within 1 year and is represented in the balance

sheet. Thus, if the operating cash flow ratio is greater than 1, it indicates that the company is

generating more cash from its business operations for meeting adequately its current liabilities in

the specified period and vice-versa. On the other hand, the earnings figure reflects the net profit

that indicates the actual profit that has been realized after meeting all the significant expenses of

operation, interest and taxes. Thus, if the cash flow from operations is less than the earnings

figure then the company might have a poor financial health. This is because it is not having

sufficient liquidity for meeting its current obligations although its accrued profit level might be

good (Weston and Brigham, 2015). This may indicate that the company is not highly effective in

meeting its current obligations due to its inefficiency in collecting its accounts receivables. The

business companies adopt the use of accrual basis of accounting and thus the earning figure

indicates the net profit to be realized by the company by taking into account the amount of

accounts receivables. Thus, if the cash flow from operations is less than the earning figure then

the company financial condition cannot be regarded as good as there is possibility of default o its

part as its credit obligations become due (White, 2014).

Asset Turnover ratio: The company have maintained a steady growth rate over the year

2016-2017 in relation to asset turnover as depicted in the above table. This indicates that

the value of its sales in relation to the value of its assets has remained steady (Ross, Jaffe

and Kakani, 2008).

Thus, it can be stated on the basis of profitability analysis of the company that its profit

earning capacity has reduced in the year 2017 as compared to the year 2016. In addition to this,

the financial stability ratios have indicated that it is adopting more use of debt in its capital

structure which is not a good sign for the future growth of the company. Also, it is not able to

improve its efficiency of generating sales from asset utilization. This all indicates that the

financial health of the company has deteriorated in the year 2017 as compared to the year 2016.

This is also not indicative of good sign of potential growth of the company (Papadopoulos,

2011).

B:

Cash flow from operating activity ratio provides an overall assessment of the liquidity

position of a company. It is calculated by dividing the cash flow from operations by the current

liabilities that need to be repaid by the company within 1 year and is represented in the balance

sheet. Thus, if the operating cash flow ratio is greater than 1, it indicates that the company is

generating more cash from its business operations for meeting adequately its current liabilities in

the specified period and vice-versa. On the other hand, the earnings figure reflects the net profit

that indicates the actual profit that has been realized after meeting all the significant expenses of

operation, interest and taxes. Thus, if the cash flow from operations is less than the earnings

figure then the company might have a poor financial health. This is because it is not having

sufficient liquidity for meeting its current obligations although its accrued profit level might be

good (Weston and Brigham, 2015). This may indicate that the company is not highly effective in

meeting its current obligations due to its inefficiency in collecting its accounts receivables. The

business companies adopt the use of accrual basis of accounting and thus the earning figure

indicates the net profit to be realized by the company by taking into account the amount of

accounts receivables. Thus, if the cash flow from operations is less than the earning figure then

the company financial condition cannot be regarded as good as there is possibility of default o its

part as its credit obligations become due (White, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

Solution 2: Application of management accounting tools to business decision making:

Budgeting

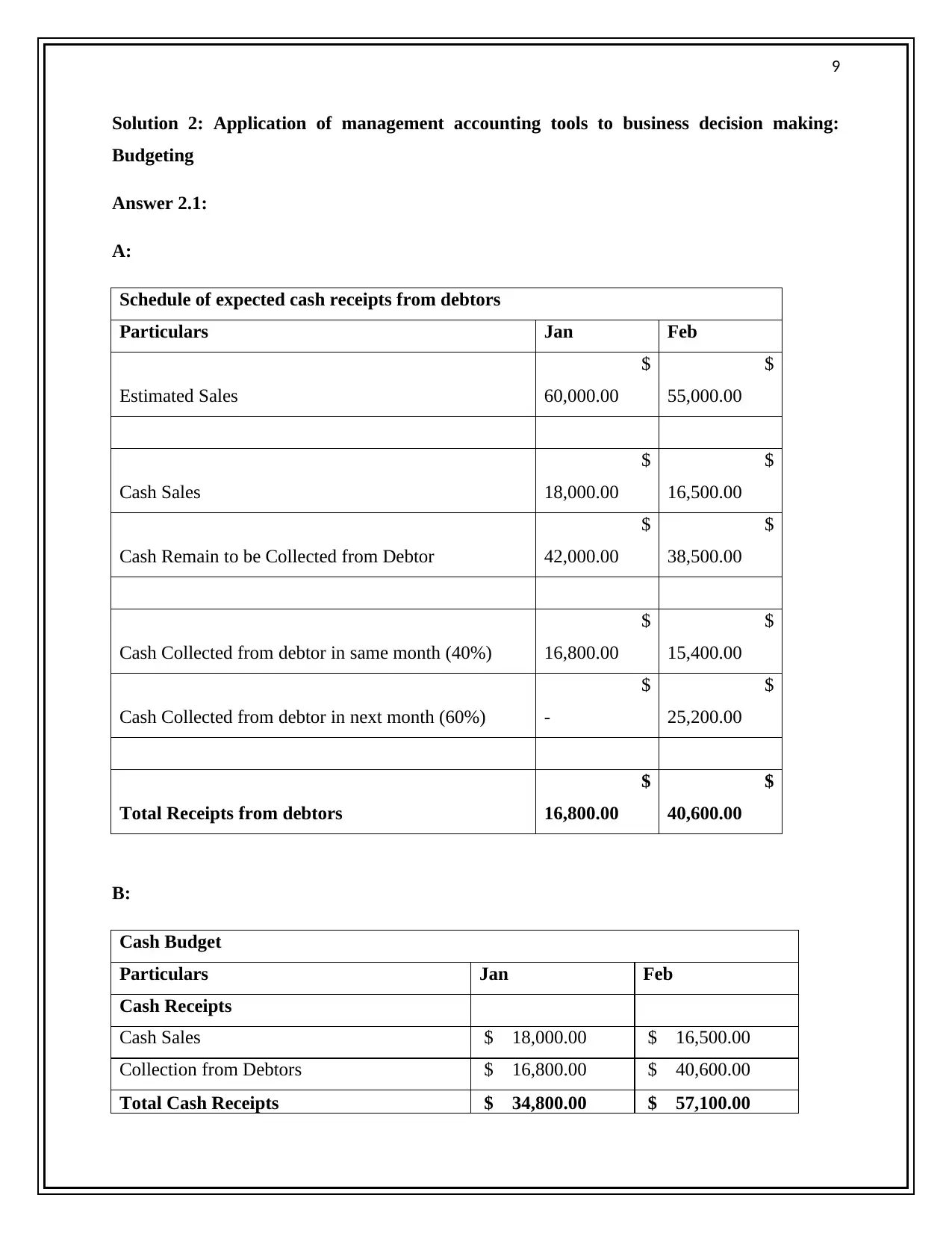

Answer 2.1:

A:

Schedule of expected cash receipts from debtors

Particulars Jan Feb

Estimated Sales

$

60,000.00

$

55,000.00

Cash Sales

$

18,000.00

$

16,500.00

Cash Remain to be Collected from Debtor

$

42,000.00

$

38,500.00

Cash Collected from debtor in same month (40%)

$

16,800.00

$

15,400.00

Cash Collected from debtor in next month (60%)

$

-

$

25,200.00

Total Receipts from debtors

$

16,800.00

$

40,600.00

B:

Cash Budget

Particulars Jan Feb

Cash Receipts

Cash Sales $ 18,000.00 $ 16,500.00

Collection from Debtors $ 16,800.00 $ 40,600.00

Total Cash Receipts $ 34,800.00 $ 57,100.00

Solution 2: Application of management accounting tools to business decision making:

Budgeting

Answer 2.1:

A:

Schedule of expected cash receipts from debtors

Particulars Jan Feb

Estimated Sales

$

60,000.00

$

55,000.00

Cash Sales

$

18,000.00

$

16,500.00

Cash Remain to be Collected from Debtor

$

42,000.00

$

38,500.00

Cash Collected from debtor in same month (40%)

$

16,800.00

$

15,400.00

Cash Collected from debtor in next month (60%)

$

-

$

25,200.00

Total Receipts from debtors

$

16,800.00

$

40,600.00

B:

Cash Budget

Particulars Jan Feb

Cash Receipts

Cash Sales $ 18,000.00 $ 16,500.00

Collection from Debtors $ 16,800.00 $ 40,600.00

Total Cash Receipts $ 34,800.00 $ 57,100.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

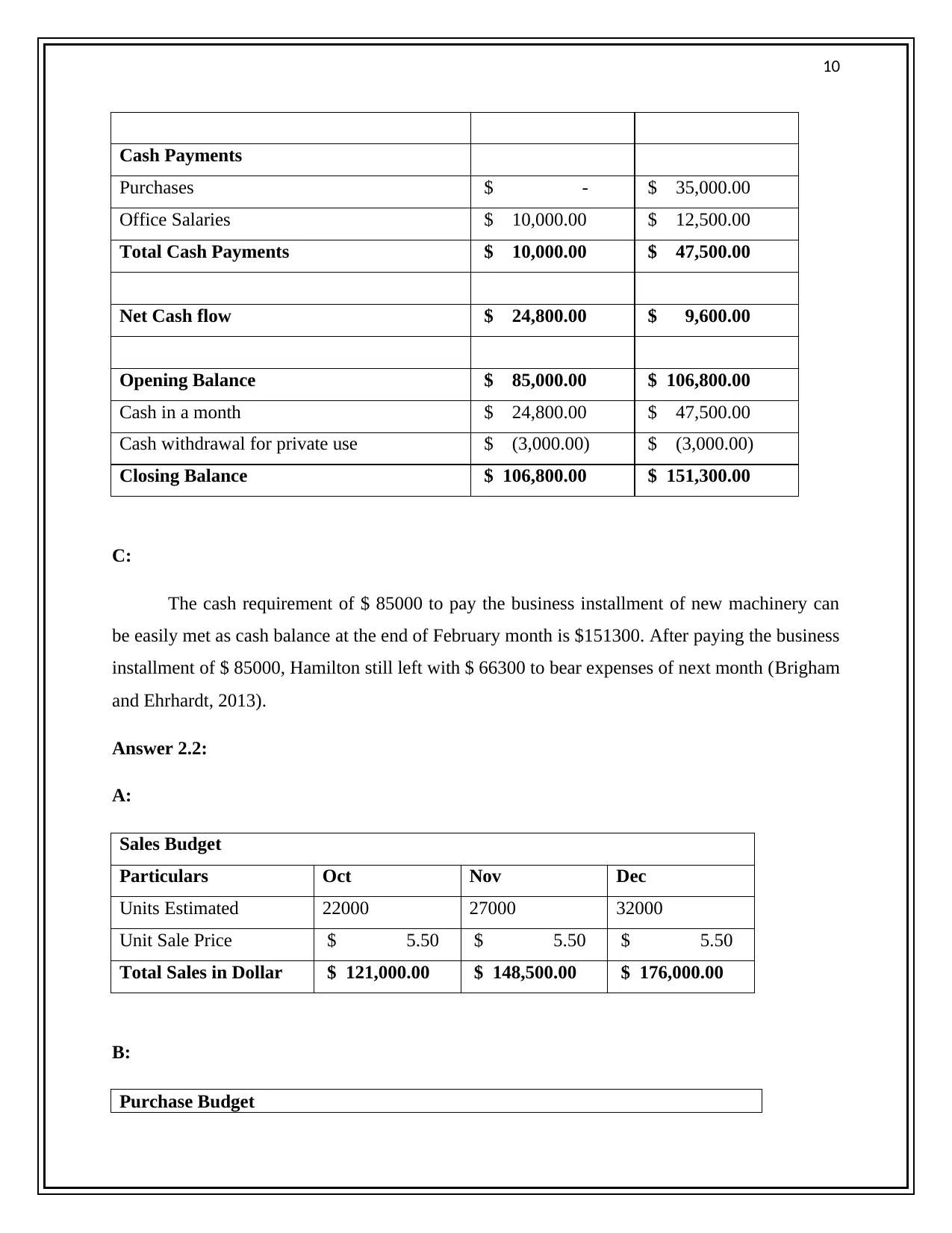

Cash Payments

Purchases $ - $ 35,000.00

Office Salaries $ 10,000.00 $ 12,500.00

Total Cash Payments $ 10,000.00 $ 47,500.00

Net Cash flow $ 24,800.00 $ 9,600.00

Opening Balance $ 85,000.00 $ 106,800.00

Cash in a month $ 24,800.00 $ 47,500.00

Cash withdrawal for private use $ (3,000.00) $ (3,000.00)

Closing Balance $ 106,800.00 $ 151,300.00

C:

The cash requirement of $ 85000 to pay the business installment of new machinery can

be easily met as cash balance at the end of February month is $151300. After paying the business

installment of $ 85000, Hamilton still left with $ 66300 to bear expenses of next month (Brigham

and Ehrhardt, 2013).

Answer 2.2:

A:

Sales Budget

Particulars Oct Nov Dec

Units Estimated 22000 27000 32000

Unit Sale Price $ 5.50 $ 5.50 $ 5.50

Total Sales in Dollar $ 121,000.00 $ 148,500.00 $ 176,000.00

B:

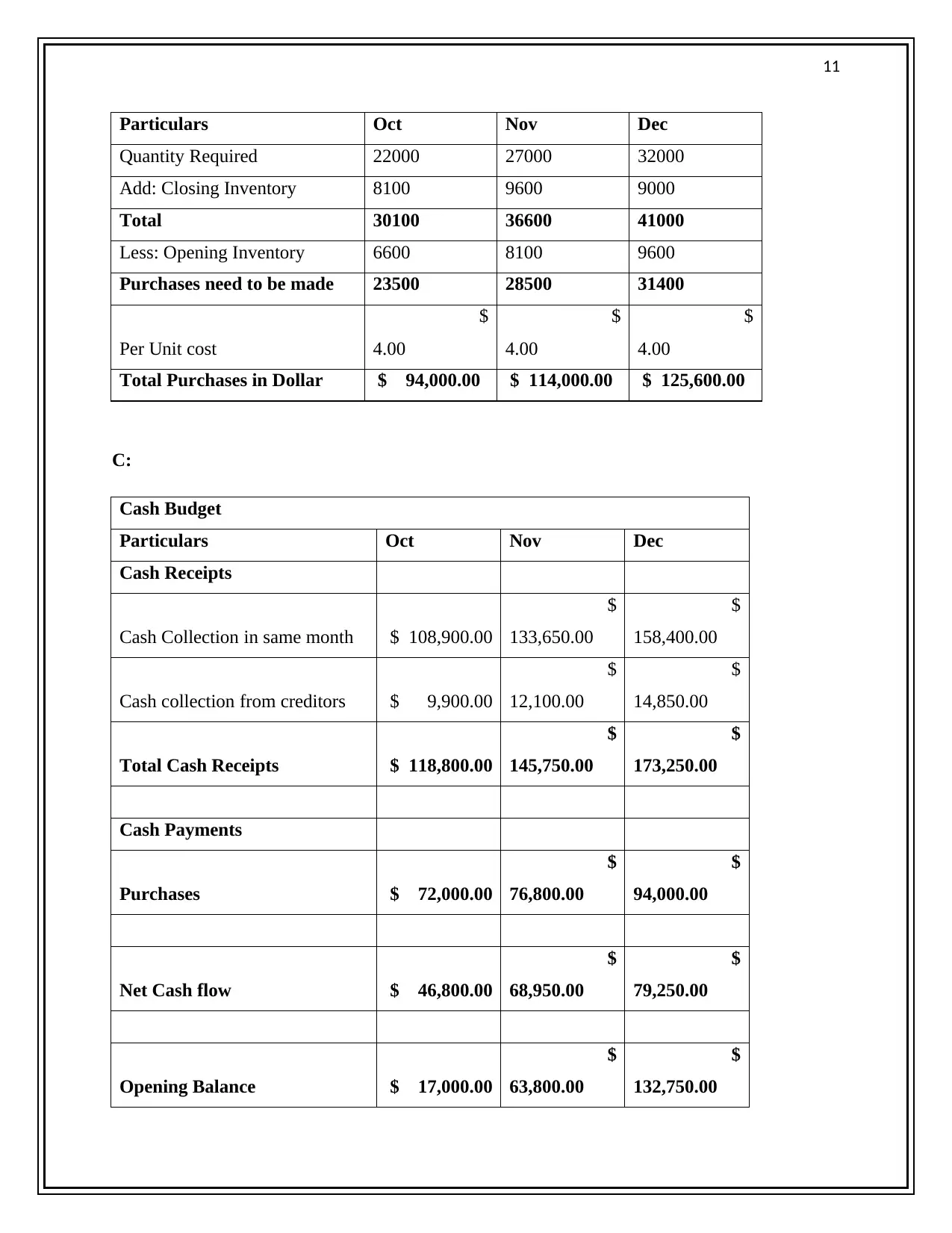

Purchase Budget

Cash Payments

Purchases $ - $ 35,000.00

Office Salaries $ 10,000.00 $ 12,500.00

Total Cash Payments $ 10,000.00 $ 47,500.00

Net Cash flow $ 24,800.00 $ 9,600.00

Opening Balance $ 85,000.00 $ 106,800.00

Cash in a month $ 24,800.00 $ 47,500.00

Cash withdrawal for private use $ (3,000.00) $ (3,000.00)

Closing Balance $ 106,800.00 $ 151,300.00

C:

The cash requirement of $ 85000 to pay the business installment of new machinery can

be easily met as cash balance at the end of February month is $151300. After paying the business

installment of $ 85000, Hamilton still left with $ 66300 to bear expenses of next month (Brigham

and Ehrhardt, 2013).

Answer 2.2:

A:

Sales Budget

Particulars Oct Nov Dec

Units Estimated 22000 27000 32000

Unit Sale Price $ 5.50 $ 5.50 $ 5.50

Total Sales in Dollar $ 121,000.00 $ 148,500.00 $ 176,000.00

B:

Purchase Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Particulars Oct Nov Dec

Quantity Required 22000 27000 32000

Add: Closing Inventory 8100 9600 9000

Total 30100 36600 41000

Less: Opening Inventory 6600 8100 9600

Purchases need to be made 23500 28500 31400

Per Unit cost

$

4.00

$

4.00

$

4.00

Total Purchases in Dollar $ 94,000.00 $ 114,000.00 $ 125,600.00

C:

Cash Budget

Particulars Oct Nov Dec

Cash Receipts

Cash Collection in same month $ 108,900.00

$

133,650.00

$

158,400.00

Cash collection from creditors $ 9,900.00

$

12,100.00

$

14,850.00

Total Cash Receipts $ 118,800.00

$

145,750.00

$

173,250.00

Cash Payments

Purchases $ 72,000.00

$

76,800.00

$

94,000.00

Net Cash flow $ 46,800.00

$

68,950.00

$

79,250.00

Opening Balance $ 17,000.00

$

63,800.00

$

132,750.00

Particulars Oct Nov Dec

Quantity Required 22000 27000 32000

Add: Closing Inventory 8100 9600 9000

Total 30100 36600 41000

Less: Opening Inventory 6600 8100 9600

Purchases need to be made 23500 28500 31400

Per Unit cost

$

4.00

$

4.00

$

4.00

Total Purchases in Dollar $ 94,000.00 $ 114,000.00 $ 125,600.00

C:

Cash Budget

Particulars Oct Nov Dec

Cash Receipts

Cash Collection in same month $ 108,900.00

$

133,650.00

$

158,400.00

Cash collection from creditors $ 9,900.00

$

12,100.00

$

14,850.00

Total Cash Receipts $ 118,800.00

$

145,750.00

$

173,250.00

Cash Payments

Purchases $ 72,000.00

$

76,800.00

$

94,000.00

Net Cash flow $ 46,800.00

$

68,950.00

$

79,250.00

Opening Balance $ 17,000.00

$

63,800.00

$

132,750.00

12

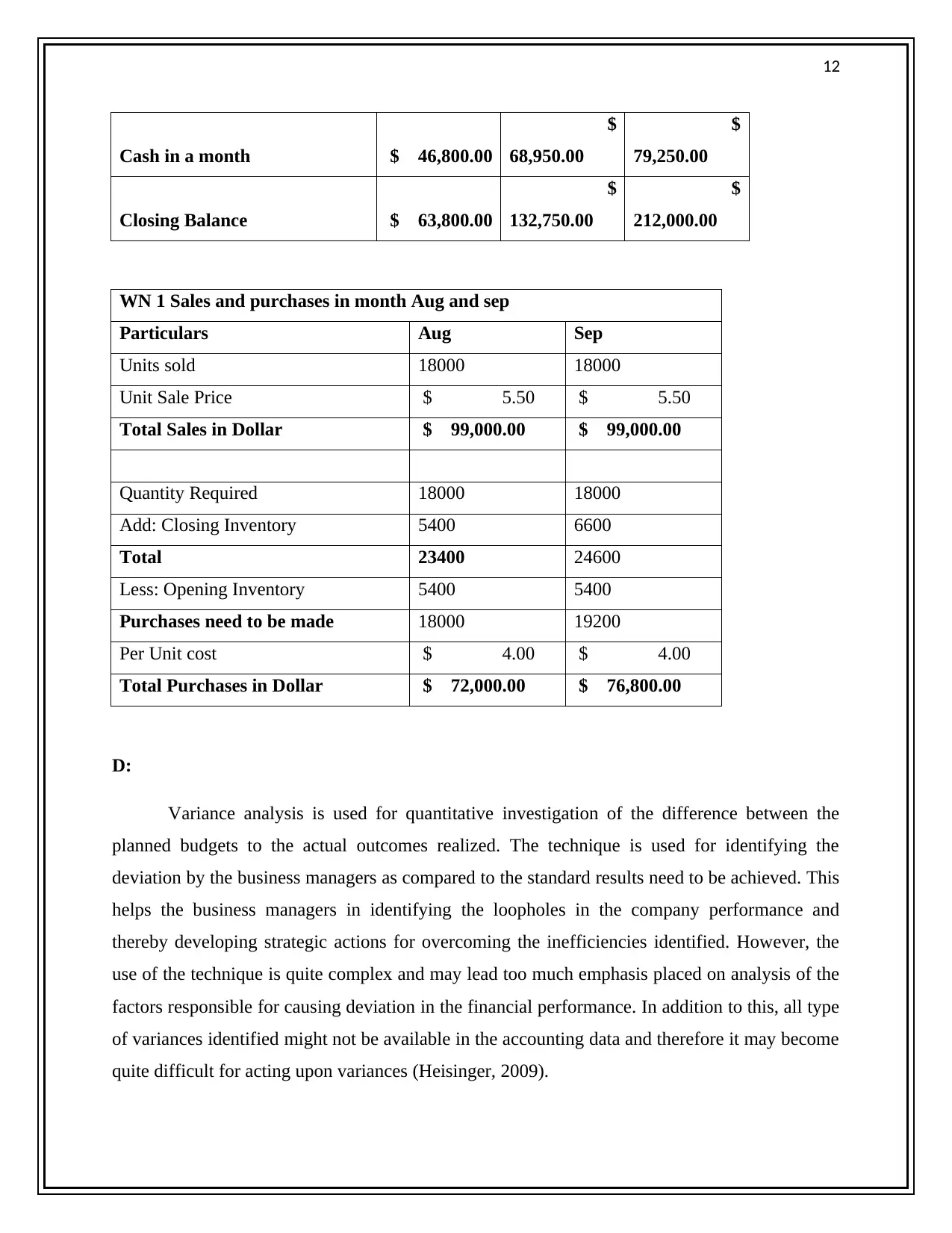

Cash in a month $ 46,800.00

$

68,950.00

$

79,250.00

Closing Balance $ 63,800.00

$

132,750.00

$

212,000.00

WN 1 Sales and purchases in month Aug and sep

Particulars Aug Sep

Units sold 18000 18000

Unit Sale Price $ 5.50 $ 5.50

Total Sales in Dollar $ 99,000.00 $ 99,000.00

Quantity Required 18000 18000

Add: Closing Inventory 5400 6600

Total 23400 24600

Less: Opening Inventory 5400 5400

Purchases need to be made 18000 19200

Per Unit cost $ 4.00 $ 4.00

Total Purchases in Dollar $ 72,000.00 $ 76,800.00

D:

Variance analysis is used for quantitative investigation of the difference between the

planned budgets to the actual outcomes realized. The technique is used for identifying the

deviation by the business managers as compared to the standard results need to be achieved. This

helps the business managers in identifying the loopholes in the company performance and

thereby developing strategic actions for overcoming the inefficiencies identified. However, the

use of the technique is quite complex and may lead too much emphasis placed on analysis of the

factors responsible for causing deviation in the financial performance. In addition to this, all type

of variances identified might not be available in the accounting data and therefore it may become

quite difficult for acting upon variances (Heisinger, 2009).

Cash in a month $ 46,800.00

$

68,950.00

$

79,250.00

Closing Balance $ 63,800.00

$

132,750.00

$

212,000.00

WN 1 Sales and purchases in month Aug and sep

Particulars Aug Sep

Units sold 18000 18000

Unit Sale Price $ 5.50 $ 5.50

Total Sales in Dollar $ 99,000.00 $ 99,000.00

Quantity Required 18000 18000

Add: Closing Inventory 5400 6600

Total 23400 24600

Less: Opening Inventory 5400 5400

Purchases need to be made 18000 19200

Per Unit cost $ 4.00 $ 4.00

Total Purchases in Dollar $ 72,000.00 $ 76,800.00

D:

Variance analysis is used for quantitative investigation of the difference between the

planned budgets to the actual outcomes realized. The technique is used for identifying the

deviation by the business managers as compared to the standard results need to be achieved. This

helps the business managers in identifying the loopholes in the company performance and

thereby developing strategic actions for overcoming the inefficiencies identified. However, the

use of the technique is quite complex and may lead too much emphasis placed on analysis of the

factors responsible for causing deviation in the financial performance. In addition to this, all type

of variances identified might not be available in the accounting data and therefore it may become

quite difficult for acting upon variances (Heisinger, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.