Corporate Accounting Report: Ausnet Ltd Financial Analysis

VerifiedAdded on 2021/05/31

|13

|2813

|495

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, focusing on the financial statements of Ausnet Ltd. It begins with an examination of the cash flow statement, detailing the significant items within operating, investing, and financing activities. A comparative analysis of these three classifications over several years highlights trends and performance. The report then explores the comprehensive income statement, explaining items included in other comprehensive income, such as movements in hedge reserves and defined benefit funds, and their tax implications. The report also delves into the tax items of the business, including current tax paid, tax rates, and the treatment of deferred tax assets and liabilities. The analysis considers the differences between income tax expenses and income tax paid, along with the company's tax policies. The report utilizes the indirect method for preparing the cash flow statements. Overall, the report provides a detailed understanding of Ausnet Ltd's financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Cash Flow Statement.......................................................................................................................2

Significant Items of the Cash Flow Statement............................................................................2

Comparative Analysis of Three Classification of Cash Flow Statement....................................4

Comprehensive Income Statement..................................................................................................6

Items which are included in Other Comprehensive Income............................................................7

Understanding of Items shown under Comprehensive Income...................................................7

Reporting for Comprehensive Items................................................................................................7

Tax items of the Business................................................................................................................8

Current Tax Paid..........................................................................................................................8

Tax rate Charged by the business................................................................................................8

Deferred Tax Assets and Liabilities............................................................................................8

Current Tax Assets and Liabilities..............................................................................................9

Difference in Income tax expenses and Income Tax paid.........................................................10

Tax policy of the Company.......................................................................................................10

Reference.......................................................................................................................................11

CORPORATE ACCOUNTING

Table of Contents

Cash Flow Statement.......................................................................................................................2

Significant Items of the Cash Flow Statement............................................................................2

Comparative Analysis of Three Classification of Cash Flow Statement....................................4

Comprehensive Income Statement..................................................................................................6

Items which are included in Other Comprehensive Income............................................................7

Understanding of Items shown under Comprehensive Income...................................................7

Reporting for Comprehensive Items................................................................................................7

Tax items of the Business................................................................................................................8

Current Tax Paid..........................................................................................................................8

Tax rate Charged by the business................................................................................................8

Deferred Tax Assets and Liabilities............................................................................................8

Current Tax Assets and Liabilities..............................................................................................9

Difference in Income tax expenses and Income Tax paid.........................................................10

Tax policy of the Company.......................................................................................................10

Reference.......................................................................................................................................11

2

CORPORATE ACCOUNTING

Cash Flow Statement

Significant Items of the Cash Flow Statement

The cash flow statement depicts the cash flow of the business that is the cash inflows and

outflows of the business. The cash position of the business is depicted with the help of cash flow

statement as prepared by the business (Chang et al. 2014). The reason due to which cash flow

statement is prepared is to show the businesses liquidity position at the end of the financial year.

For the purpose of this assignment, Ausnet Ltd is selected which is engaged in energy generation

and distribution of the same.

The cash flow statement of Ausnet Ltd reveals that it is made up of cash from operating

activities, cash from investing activities and cash from financing activities

(Ausnetservices.com.au. 2018). The various cash inflows and outflows of the business is

recorded on the basis of the above mentioned three activities. The items which are shown in the

cash from operating activities of the business are shown to be working capital movement,

income tax which is paid by the business, the cash from investing activities of the business show

payments which are made for purchasing property, plant and equipment, sales of property, plants

and equipment, the cash from financing activities of the business includes dividends which are

paid by the business, borrowings which the business took during the year and the repayment of

loans. The cash from operations includes working capital movements which is shown to be $ 0.2

million in the cash flow statement. The cash flow statement is prepared following indirect

method and therefore items which are deductible from the net profit is deducted and the non-

deductible expenses are added back to the net profit to arrive at the cash flow from operations of

the business (Kaspina, Molotov and Kaspin 2015). The profit of the business for the year 2017 is

CORPORATE ACCOUNTING

Cash Flow Statement

Significant Items of the Cash Flow Statement

The cash flow statement depicts the cash flow of the business that is the cash inflows and

outflows of the business. The cash position of the business is depicted with the help of cash flow

statement as prepared by the business (Chang et al. 2014). The reason due to which cash flow

statement is prepared is to show the businesses liquidity position at the end of the financial year.

For the purpose of this assignment, Ausnet Ltd is selected which is engaged in energy generation

and distribution of the same.

The cash flow statement of Ausnet Ltd reveals that it is made up of cash from operating

activities, cash from investing activities and cash from financing activities

(Ausnetservices.com.au. 2018). The various cash inflows and outflows of the business is

recorded on the basis of the above mentioned three activities. The items which are shown in the

cash from operating activities of the business are shown to be working capital movement,

income tax which is paid by the business, the cash from investing activities of the business show

payments which are made for purchasing property, plant and equipment, sales of property, plants

and equipment, the cash from financing activities of the business includes dividends which are

paid by the business, borrowings which the business took during the year and the repayment of

loans. The cash from operations includes working capital movements which is shown to be $ 0.2

million in the cash flow statement. The cash flow statement is prepared following indirect

method and therefore items which are deductible from the net profit is deducted and the non-

deductible expenses are added back to the net profit to arrive at the cash flow from operations of

the business (Kaspina, Molotov and Kaspin 2015). The profit of the business for the year 2017 is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

shown to be $ 255.1 million which has significantly increased from previous year 2016 which is

shown to be $ 489.3 million. This shows that the business has significantly improved from

previous year and the operations of the business has also improved in a similar manner. The cash

from operations also show income tax which is actually paid by the business and the same is

shown to be $ 49.4 million and another significant item which is included under the head cash

from operating activities is net interest paid by the business (Radhakrishnan and Wu 2014). The

net interest of the company for the year 2017 is shown to be $ 285.3 million which has reduced

from the previous year which was shown to be $ 296.9 million as per the cash flow statement of

the business. The non-cash item which is shown in the cash flow statement is depreciation,

interest and tax is added back to profit figure and the same is shown to be $ 818.2 million for the

year 2017.

The cash from investing activities show proceeds which are received from the sale of

property, plant an d equipment which is shown to be $ 4.3 million which has increased from the

previous year. The company has also purchased property during the year for which the same is

shown in the cash flow statement is $ 888.2 million which has significantly increased from the

previous year. The major portion of the cash from investing activities is made up of the items

which are shown above.

The cash from financing activities show that the company has paid a dividend which is a

cash outflow for the business which is shown to be $ 211.9 million which has increased from

previous year’s estimate. This suggest that the business’s profitability has increased from the

previous year’s estimates. The company has taken a loan during the year which is shown to be $

987.8 million and the same is shown to be $ 1100 million. The repayment of debt which is

shown to be $ 756.2 million during the year is shown in the cash flow statement of the business.

CORPORATE ACCOUNTING

shown to be $ 255.1 million which has significantly increased from previous year 2016 which is

shown to be $ 489.3 million. This shows that the business has significantly improved from

previous year and the operations of the business has also improved in a similar manner. The cash

from operations also show income tax which is actually paid by the business and the same is

shown to be $ 49.4 million and another significant item which is included under the head cash

from operating activities is net interest paid by the business (Radhakrishnan and Wu 2014). The

net interest of the company for the year 2017 is shown to be $ 285.3 million which has reduced

from the previous year which was shown to be $ 296.9 million as per the cash flow statement of

the business. The non-cash item which is shown in the cash flow statement is depreciation,

interest and tax is added back to profit figure and the same is shown to be $ 818.2 million for the

year 2017.

The cash from investing activities show proceeds which are received from the sale of

property, plant an d equipment which is shown to be $ 4.3 million which has increased from the

previous year. The company has also purchased property during the year for which the same is

shown in the cash flow statement is $ 888.2 million which has significantly increased from the

previous year. The major portion of the cash from investing activities is made up of the items

which are shown above.

The cash from financing activities show that the company has paid a dividend which is a

cash outflow for the business which is shown to be $ 211.9 million which has increased from

previous year’s estimate. This suggest that the business’s profitability has increased from the

previous year’s estimates. The company has taken a loan during the year which is shown to be $

987.8 million and the same is shown to be $ 1100 million. The repayment of debt which is

shown to be $ 756.2 million during the year is shown in the cash flow statement of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

The business also had repaid a significant amount of loan in the previous year 2016 which is

shown to be $ 1373.4

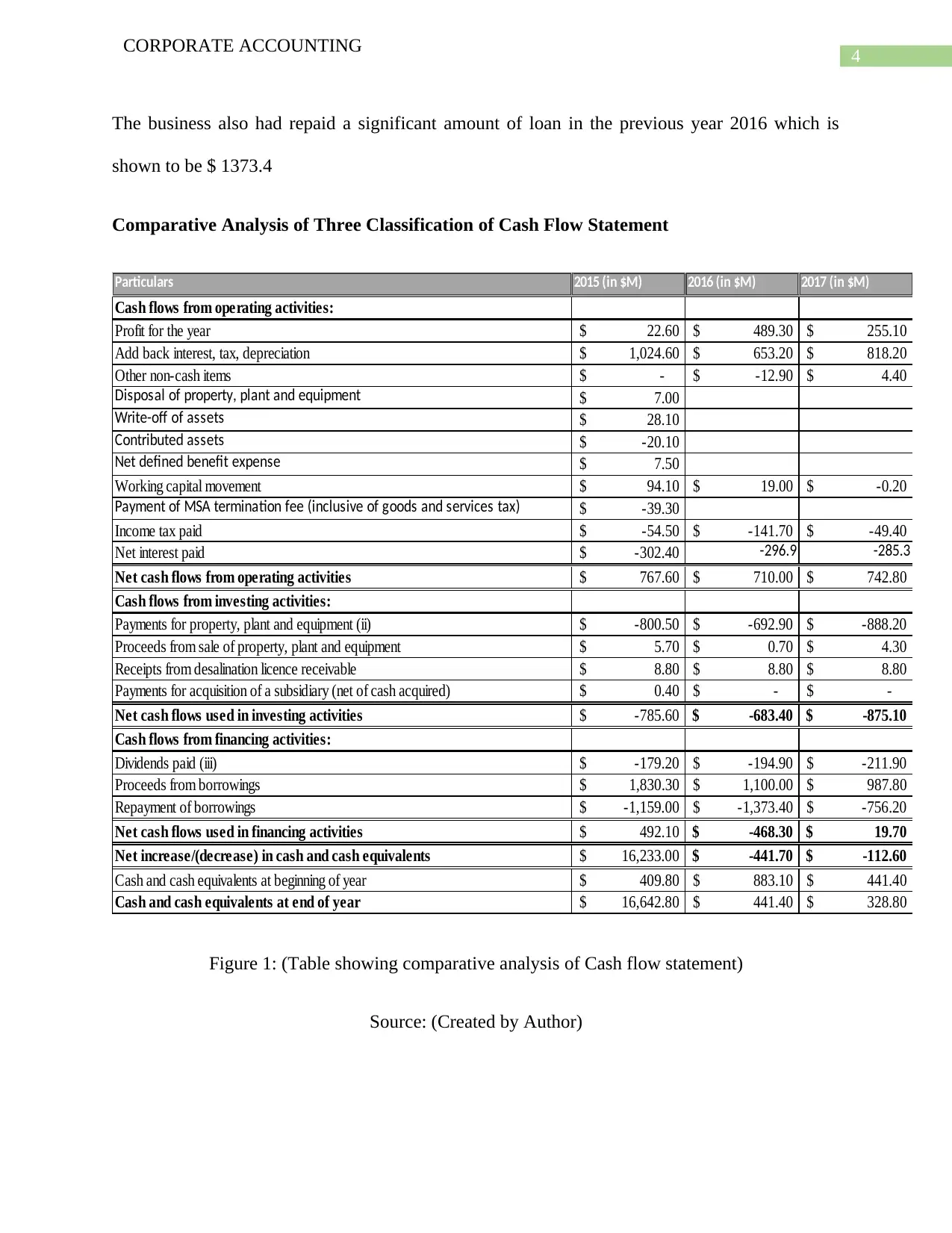

Comparative Analysis of Three Classification of Cash Flow Statement

Particulars 2015 (in $M) 2016 (in $M) 2017 (in $M)

Cash flows from operating activities:

Profit for the year 22.60$ 489.30$ 255.10$

Add back interest, tax, depreciation 1,024.60$ 653.20$ 818.20$

Other non-cash items -$ -12.90$ 4.40$

Disposal of property, plant and equipment 7.00$

Write-off of assets 28.10$

Contributed assets -20.10$

Net defined benefit expense 7.50$

Working capital movement 94.10$ 19.00$ -0.20$

Payment of MSA termination fee (inclusive of goods and services tax) -39.30$

Income tax paid -54.50$ -141.70$ -49.40$

Net interest paid -302.40$ -296.9 -285.3

Net cash flows from operating activities 767.60$ 710.00$ 742.80$

Cash flows from investing activities:

Payments for property, plant and equipment (ii) -800.50$ -692.90$ -888.20$

Proceeds from sale of property, plant and equipment 5.70$ 0.70$ 4.30$

Receipts from desalination licence receivable 8.80$ 8.80$ 8.80$

Payments for acquisition of a subsidiary (net of cash acquired) 0.40$ -$ -$

Net cash flows used in investing activities -785.60$ -683.40$ -875.10$

Cash flows from financing activities:

Dividends paid (iii) -179.20$ -194.90$ -211.90$

Proceeds from borrowings 1,830.30$ 1,100.00$ 987.80$

Repayment of borrowings -1,159.00$ -1,373.40$ -756.20$

Net cash flows used in financing activities 492.10$ -468.30$ 19.70$

Net increase/(decrease) in cash and cash equivalents 16,233.00$ -441.70$ -112.60$

Cash and cash equivalents at beginning of year 409.80$ 883.10$ 441.40$

Cash and cash equivalents at end of year 16,642.80$ 441.40$ 328.80$

Figure 1: (Table showing comparative analysis of Cash flow statement)

Source: (Created by Author)

CORPORATE ACCOUNTING

The business also had repaid a significant amount of loan in the previous year 2016 which is

shown to be $ 1373.4

Comparative Analysis of Three Classification of Cash Flow Statement

Particulars 2015 (in $M) 2016 (in $M) 2017 (in $M)

Cash flows from operating activities:

Profit for the year 22.60$ 489.30$ 255.10$

Add back interest, tax, depreciation 1,024.60$ 653.20$ 818.20$

Other non-cash items -$ -12.90$ 4.40$

Disposal of property, plant and equipment 7.00$

Write-off of assets 28.10$

Contributed assets -20.10$

Net defined benefit expense 7.50$

Working capital movement 94.10$ 19.00$ -0.20$

Payment of MSA termination fee (inclusive of goods and services tax) -39.30$

Income tax paid -54.50$ -141.70$ -49.40$

Net interest paid -302.40$ -296.9 -285.3

Net cash flows from operating activities 767.60$ 710.00$ 742.80$

Cash flows from investing activities:

Payments for property, plant and equipment (ii) -800.50$ -692.90$ -888.20$

Proceeds from sale of property, plant and equipment 5.70$ 0.70$ 4.30$

Receipts from desalination licence receivable 8.80$ 8.80$ 8.80$

Payments for acquisition of a subsidiary (net of cash acquired) 0.40$ -$ -$

Net cash flows used in investing activities -785.60$ -683.40$ -875.10$

Cash flows from financing activities:

Dividends paid (iii) -179.20$ -194.90$ -211.90$

Proceeds from borrowings 1,830.30$ 1,100.00$ 987.80$

Repayment of borrowings -1,159.00$ -1,373.40$ -756.20$

Net cash flows used in financing activities 492.10$ -468.30$ 19.70$

Net increase/(decrease) in cash and cash equivalents 16,233.00$ -441.70$ -112.60$

Cash and cash equivalents at beginning of year 409.80$ 883.10$ 441.40$

Cash and cash equivalents at end of year 16,642.80$ 441.40$ 328.80$

Figure 1: (Table showing comparative analysis of Cash flow statement)

Source: (Created by Author)

5

CORPORATE ACCOUNTING

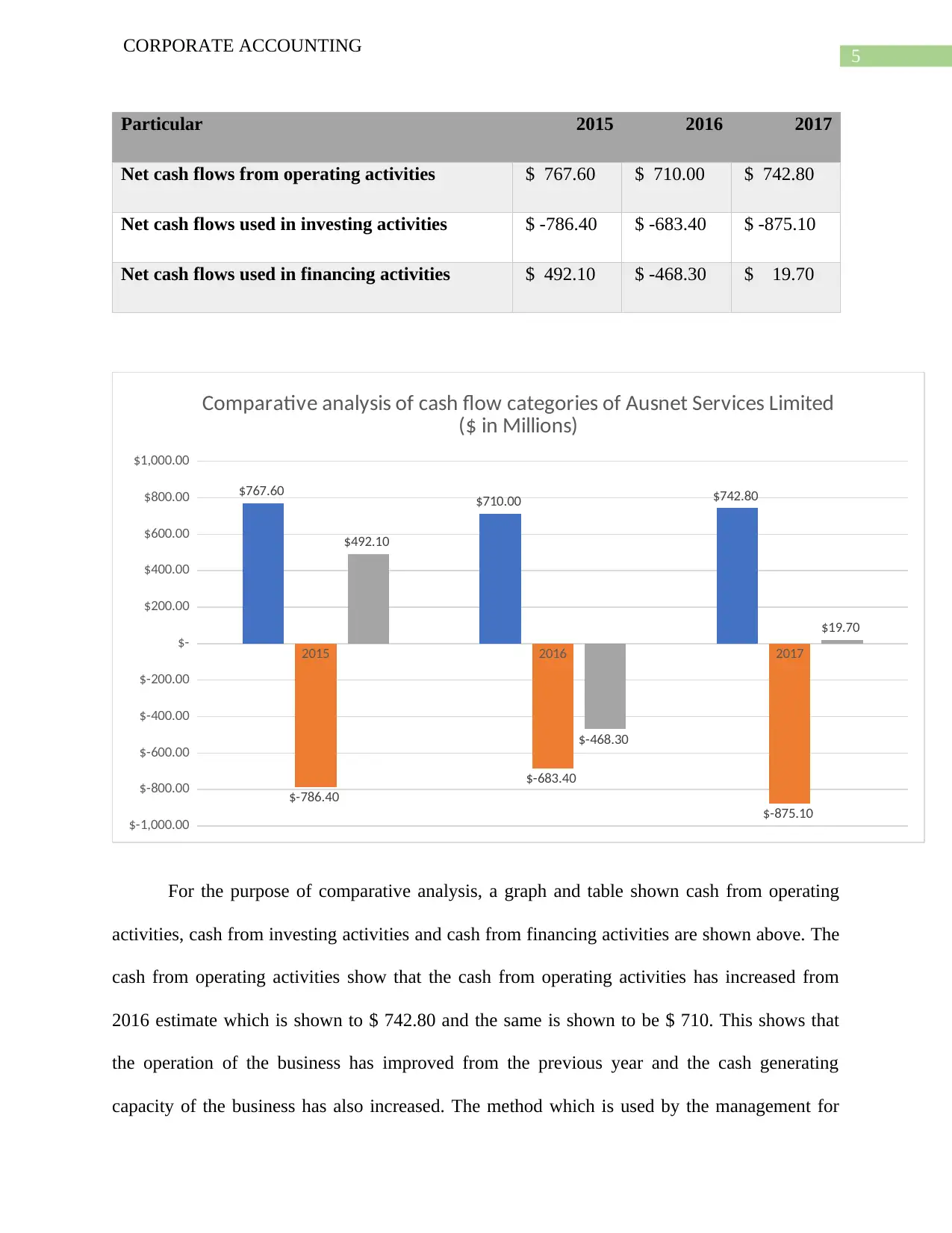

Particular 2015 2016 2017

Net cash flows from operating activities $ 767.60 $ 710.00 $ 742.80

Net cash flows used in investing activities $ -786.40 $ -683.40 $ -875.10

Net cash flows used in financing activities $ 492.10 $ -468.30 $ 19.70

2015 2016 2017

$-1,000.00

$-800.00

$-600.00

$-400.00

$-200.00

$-

$200.00

$400.00

$600.00

$800.00

$1,000.00

$767.60 $710.00 $742.80

$-786.40

$-683.40

$-875.10

$492.10

$-468.30

$19.70

Comparative analysis of cash flow categories of Ausnet Services Limited

($ in Millions)

For the purpose of comparative analysis, a graph and table shown cash from operating

activities, cash from investing activities and cash from financing activities are shown above. The

cash from operating activities show that the cash from operating activities has increased from

2016 estimate which is shown to $ 742.80 and the same is shown to be $ 710. This shows that

the operation of the business has improved from the previous year and the cash generating

capacity of the business has also increased. The method which is used by the management for

CORPORATE ACCOUNTING

Particular 2015 2016 2017

Net cash flows from operating activities $ 767.60 $ 710.00 $ 742.80

Net cash flows used in investing activities $ -786.40 $ -683.40 $ -875.10

Net cash flows used in financing activities $ 492.10 $ -468.30 $ 19.70

2015 2016 2017

$-1,000.00

$-800.00

$-600.00

$-400.00

$-200.00

$-

$200.00

$400.00

$600.00

$800.00

$1,000.00

$767.60 $710.00 $742.80

$-786.40

$-683.40

$-875.10

$492.10

$-468.30

$19.70

Comparative analysis of cash flow categories of Ausnet Services Limited

($ in Millions)

For the purpose of comparative analysis, a graph and table shown cash from operating

activities, cash from investing activities and cash from financing activities are shown above. The

cash from operating activities show that the cash from operating activities has increased from

2016 estimate which is shown to $ 742.80 and the same is shown to be $ 710. This shows that

the operation of the business has improved from the previous year and the cash generating

capacity of the business has also increased. The method which is used by the management for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

preparing the cash flow statement is using indirect method as shown in Figure 1. The non-cash

items such as depreciation have been added back as shown in the above figure. The cash flow

from operating activity for the current year has improved which suggests that the cost of

operations of the business has reduced.

The cash which is generated from investing activities show that the expenses has

increased from the previous year which can be attributed to the purchase of property, plant and

equipment during the year and the amount for purchase is significant and the same is shown to

be $ 888.2 and the same affects the cash from investing activities of the business. The business

also has sold property, plant and equipment during the year for which the cash proceeds are

shown in the cash flow statement.

The cash from financing activities of the business has improved from previous year’s

estimate which shows the business has tremendously improved. The company has repaid a

significant amount of loans and also has taken loan in 2017 as shown in the table above

Comprehensive Income Statement

The comprehensive income statement which is shown in the annual reports of the

business depict those items which are extraordinary in nature and affect the profits of the

business. As per the financial statement of Ausnet ltd, the company has prepared a separate

comprehensive income statement which is shown below the statement of profit and loss of the

business Eaton, T.V., (Easterday and Rhodes 2013).

CORPORATE ACCOUNTING

preparing the cash flow statement is using indirect method as shown in Figure 1. The non-cash

items such as depreciation have been added back as shown in the above figure. The cash flow

from operating activity for the current year has improved which suggests that the cost of

operations of the business has reduced.

The cash which is generated from investing activities show that the expenses has

increased from the previous year which can be attributed to the purchase of property, plant and

equipment during the year and the amount for purchase is significant and the same is shown to

be $ 888.2 and the same affects the cash from investing activities of the business. The business

also has sold property, plant and equipment during the year for which the cash proceeds are

shown in the cash flow statement.

The cash from financing activities of the business has improved from previous year’s

estimate which shows the business has tremendously improved. The company has repaid a

significant amount of loans and also has taken loan in 2017 as shown in the table above

Comprehensive Income Statement

The comprehensive income statement which is shown in the annual reports of the

business depict those items which are extraordinary in nature and affect the profits of the

business. As per the financial statement of Ausnet ltd, the company has prepared a separate

comprehensive income statement which is shown below the statement of profit and loss of the

business Eaton, T.V., (Easterday and Rhodes 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

Items which are included in Other Comprehensive Income

The comprehensive income items which are shown in the financial statements of the

business are movements in hedge reserves, income tax charged on hedge reserve, movement and

tax which is charged on defined benefit fund. The items are shown in a separate statement

showing comprehensive income which is prepared by the business of Ausnet Service ltd.

Understanding of Items shown under Comprehensive Income

As per the comprehensive income statement which is shown by the business in the

financial statements of the company, defined benefit fund which is shown in the statement as $

46.5 million on which tax is charged which is about $ 14 million. Defined benefit fund refers to

the fund of the business which the business has created for a specific purpose and the fund will

be used for that specific purpose only. The comprehensive income statement shows that the

company has also engaged in Hedge transactions for which hedge reserves are created by the

business (Schaberl and Victoravich 2015). The hedge reserve represents the profit which the

business makes from hedge transactions. The hedge accounts refer to the activities of the

business which tends to make profits from fluctuations of prices in home and foreign currency.

Reporting for Comprehensive Items

The items which are shown in the comprehensive income statement are not recorded in

the profit and loss account due to the fact that such items are of extraordinary nature and are

quite different from day to day activities of the business. The primary reason for recording such

transaction in the financial statements is due to the fact that the company wants to follow the full

disclosure principle of the business. The comprehensive income items of the business disclose

extraordinary items to the users of the financial statements of the company.

CORPORATE ACCOUNTING

Items which are included in Other Comprehensive Income

The comprehensive income items which are shown in the financial statements of the

business are movements in hedge reserves, income tax charged on hedge reserve, movement and

tax which is charged on defined benefit fund. The items are shown in a separate statement

showing comprehensive income which is prepared by the business of Ausnet Service ltd.

Understanding of Items shown under Comprehensive Income

As per the comprehensive income statement which is shown by the business in the

financial statements of the company, defined benefit fund which is shown in the statement as $

46.5 million on which tax is charged which is about $ 14 million. Defined benefit fund refers to

the fund of the business which the business has created for a specific purpose and the fund will

be used for that specific purpose only. The comprehensive income statement shows that the

company has also engaged in Hedge transactions for which hedge reserves are created by the

business (Schaberl and Victoravich 2015). The hedge reserve represents the profit which the

business makes from hedge transactions. The hedge accounts refer to the activities of the

business which tends to make profits from fluctuations of prices in home and foreign currency.

Reporting for Comprehensive Items

The items which are shown in the comprehensive income statement are not recorded in

the profit and loss account due to the fact that such items are of extraordinary nature and are

quite different from day to day activities of the business. The primary reason for recording such

transaction in the financial statements is due to the fact that the company wants to follow the full

disclosure principle of the business. The comprehensive income items of the business disclose

extraordinary items to the users of the financial statements of the company.

8

CORPORATE ACCOUNTING

Tax items of the Business

Current Tax Paid

The current tax expenses which is shown in the financial statements of Ausnet ltd is

shown to be $ 108.2 million. In 2016 the company received a tax benefit which is shown to be $

31.4 million as per the profit and loss statement of the business. The company may have paid

extra tax therefore the business has received tax benefits in 2016.

Tax rate Charged by the business

The tax which is charged by the business is according to the relevant tax laws and

provisions which are applicable in Australia. The tax is charged on the profits which are made by

the business during the year. The tax which is actually applicable to the business considering the

tax rate and tax provision which are prevalent in Australia and the tax expense which is shown in

the profit and loss statement of the business is slightly different which suggest that there must be

certain setoff and exemptions which are applicable to the business. The tax rate of the business

and which is applicable in Australia is 30%. This suggest that there are certain deferred tax assets

and deferred tax liabilities which are present in the financial statement of the company. The

items which are included in the comprehensive income statement of the business are also

applicable to tax such as tax which is charged defined benefit fund and hedge reserve which the

business has maintained. The taxes are also included in the total tax which is to be paid by the

business.

CORPORATE ACCOUNTING

Tax items of the Business

Current Tax Paid

The current tax expenses which is shown in the financial statements of Ausnet ltd is

shown to be $ 108.2 million. In 2016 the company received a tax benefit which is shown to be $

31.4 million as per the profit and loss statement of the business. The company may have paid

extra tax therefore the business has received tax benefits in 2016.

Tax rate Charged by the business

The tax which is charged by the business is according to the relevant tax laws and

provisions which are applicable in Australia. The tax is charged on the profits which are made by

the business during the year. The tax which is actually applicable to the business considering the

tax rate and tax provision which are prevalent in Australia and the tax expense which is shown in

the profit and loss statement of the business is slightly different which suggest that there must be

certain setoff and exemptions which are applicable to the business. The tax rate of the business

and which is applicable in Australia is 30%. This suggest that there are certain deferred tax assets

and deferred tax liabilities which are present in the financial statement of the company. The

items which are included in the comprehensive income statement of the business are also

applicable to tax such as tax which is charged defined benefit fund and hedge reserve which the

business has maintained. The taxes are also included in the total tax which is to be paid by the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Deferred Tax Assets and Liabilities

Deferred tax assets are components of tax which is included in the financial statements

represents the excess tax which is paid by the individual and companies and such acts as assets

of the business. On the other hand, deferred tax liabilities represent the amount paid by the

individual or the company is less than what actually should be paid to the tax authorities of the

business (Laux 2013). As per the financial statements of Ausnet ltd, the company has deferred

tax liabilities which is shown in the balance sheet of the company. The deferred tax liabilities of

the business is shown to be $ 586.4 million which has increased from previous year’s estimate

which is shown to be $ 465.8 million as per the balance sheet of the company (Chytis 2015). The

primary reason for such items to arise is due to the temporary difference which exist in the

timing of the transaction. In some cases, such deferred tax liability is carried forward from

previous years and therefore the same is shown in the financial statement of the business

(Hanlon, Navissi and Soepriyanto 2014).

Deferred tax liabilities and assets are shown in the financial statements are shown in the

financial statements so that the business can set off the same in the future years. The financial

statement of Ausnet ltd shows that all the relevant provisions for tax is followed by the company.

Current Tax Assets and Liabilities

The current assets of the business are shown to be $ 25.9 million and the current tax

liabilities of the business is zero for the year 2017. The current tax liabilities of the business

which is shown in the balance sheet reflect for the current year’s tax liability of the business. The

company also has income tax receivable which represents that the business has certain tax

benefits which accrue to the current year. The figure of income tax payable is not same as

CORPORATE ACCOUNTING

Deferred Tax Assets and Liabilities

Deferred tax assets are components of tax which is included in the financial statements

represents the excess tax which is paid by the individual and companies and such acts as assets

of the business. On the other hand, deferred tax liabilities represent the amount paid by the

individual or the company is less than what actually should be paid to the tax authorities of the

business (Laux 2013). As per the financial statements of Ausnet ltd, the company has deferred

tax liabilities which is shown in the balance sheet of the company. The deferred tax liabilities of

the business is shown to be $ 586.4 million which has increased from previous year’s estimate

which is shown to be $ 465.8 million as per the balance sheet of the company (Chytis 2015). The

primary reason for such items to arise is due to the temporary difference which exist in the

timing of the transaction. In some cases, such deferred tax liability is carried forward from

previous years and therefore the same is shown in the financial statement of the business

(Hanlon, Navissi and Soepriyanto 2014).

Deferred tax liabilities and assets are shown in the financial statements are shown in the

financial statements so that the business can set off the same in the future years. The financial

statement of Ausnet ltd shows that all the relevant provisions for tax is followed by the company.

Current Tax Assets and Liabilities

The current assets of the business are shown to be $ 25.9 million and the current tax

liabilities of the business is zero for the year 2017. The current tax liabilities of the business

which is shown in the balance sheet reflect for the current year’s tax liability of the business. The

company also has income tax receivable which represents that the business has certain tax

benefits which accrue to the current year. The figure of income tax payable is not same as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

income tax expenses because income tax payable also contains taxes which are carried forward

from previous year and also due to deferred tax assets and liabilities which are recorded in the

financial statements of the business.

Difference in Income tax expenses and Income Tax paid.

The income tax expenses which is shown in the profit and loss statement reflects the

actual amount which the business is liable to pay during the current year and the income tax

expenses which is shown in the cash flow statement of the company signifies that the tax

expense which is actually paid by the business. The reason for such a difference may be due to

the difference in accounting treatments such as cash flow statement follows cash basis while

profit and loss account is prepared on the basis of accrual basis. There might also be other

reasons for such difference such as difference in timing for recording the transaction.

Tax policy of the Company

The analysis of the financial statement of company reveals that the company has made all

the necessary adjustments which is related to the tax expense which the company incurs during

the period. The tax liability of the business which the business is not able to pay is shown in the

balance sheet of the business as current tax liability of the business. The company follows all the

relevant standards for preparation of the financial statements of the company.

CORPORATE ACCOUNTING

income tax expenses because income tax payable also contains taxes which are carried forward

from previous year and also due to deferred tax assets and liabilities which are recorded in the

financial statements of the business.

Difference in Income tax expenses and Income Tax paid.

The income tax expenses which is shown in the profit and loss statement reflects the

actual amount which the business is liable to pay during the current year and the income tax

expenses which is shown in the cash flow statement of the company signifies that the tax

expense which is actually paid by the business. The reason for such a difference may be due to

the difference in accounting treatments such as cash flow statement follows cash basis while

profit and loss account is prepared on the basis of accrual basis. There might also be other

reasons for such difference such as difference in timing for recording the transaction.

Tax policy of the Company

The analysis of the financial statement of company reveals that the company has made all

the necessary adjustments which is related to the tax expense which the company incurs during

the period. The tax liability of the business which the business is not able to pay is shown in the

balance sheet of the business as current tax liability of the business. The company follows all the

relevant standards for preparation of the financial statements of the company.

11

CORPORATE ACCOUNTING

Reference

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax attributed

to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2), pp.87-99.

Chang, X., Dasgupta, S., Wong, G. and Yao, J., 2014. Cash-flow sensitivities and the allocation

of internal cash flow. The Review of Financial Studies, 27(12), pp.3628-3657.

Ausnetservices.com.au. (2018). Home. [online] Available at: https://www.ausnetservices.com.au/

[Accessed 23 May 2018].

Kaspina, R.G., Molotov, L.A. and Kaspin, L.E., 2015. Cash flow forecasting as an element of

integrated reporting: an empirical study. Asian social science, 11(11), p.89.

Radhakrishnan, S. and Wu, S.L., 2014. Analysts' cash flow forecasts and accrual

mispricing. Contemporary Accounting Research, 31(4), pp.1191-1219.

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Schaberl, P.D. and Victoravich, L.M., 2015. Reporting location and the value relevance of

accounting information: The case of other comprehensive income. Advances in

Accounting, 31(2), pp.239-246.

CORPORATE ACCOUNTING

Reference

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax attributed

to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2), pp.87-99.

Chang, X., Dasgupta, S., Wong, G. and Yao, J., 2014. Cash-flow sensitivities and the allocation

of internal cash flow. The Review of Financial Studies, 27(12), pp.3628-3657.

Ausnetservices.com.au. (2018). Home. [online] Available at: https://www.ausnetservices.com.au/

[Accessed 23 May 2018].

Kaspina, R.G., Molotov, L.A. and Kaspin, L.E., 2015. Cash flow forecasting as an element of

integrated reporting: an empirical study. Asian social science, 11(11), p.89.

Radhakrishnan, S. and Wu, S.L., 2014. Analysts' cash flow forecasts and accrual

mispricing. Contemporary Accounting Research, 31(4), pp.1191-1219.

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Schaberl, P.D. and Victoravich, L.M., 2015. Reporting location and the value relevance of

accounting information: The case of other comprehensive income. Advances in

Accounting, 31(2), pp.239-246.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.