Accounting for Business: Financial Statement and Ratio Analysis

VerifiedAdded on 2022/11/24

|10

|1625

|255

Homework Assignment

AI Summary

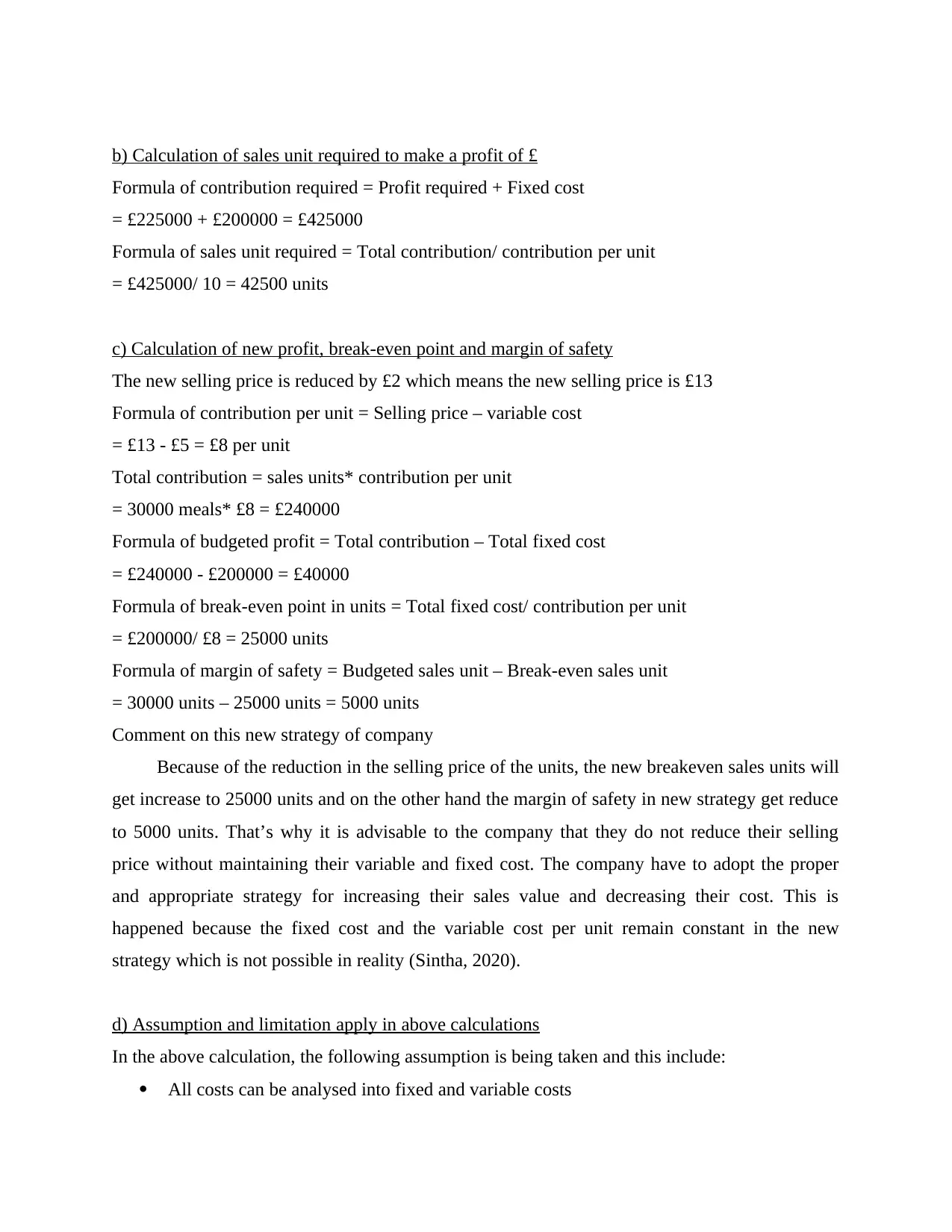

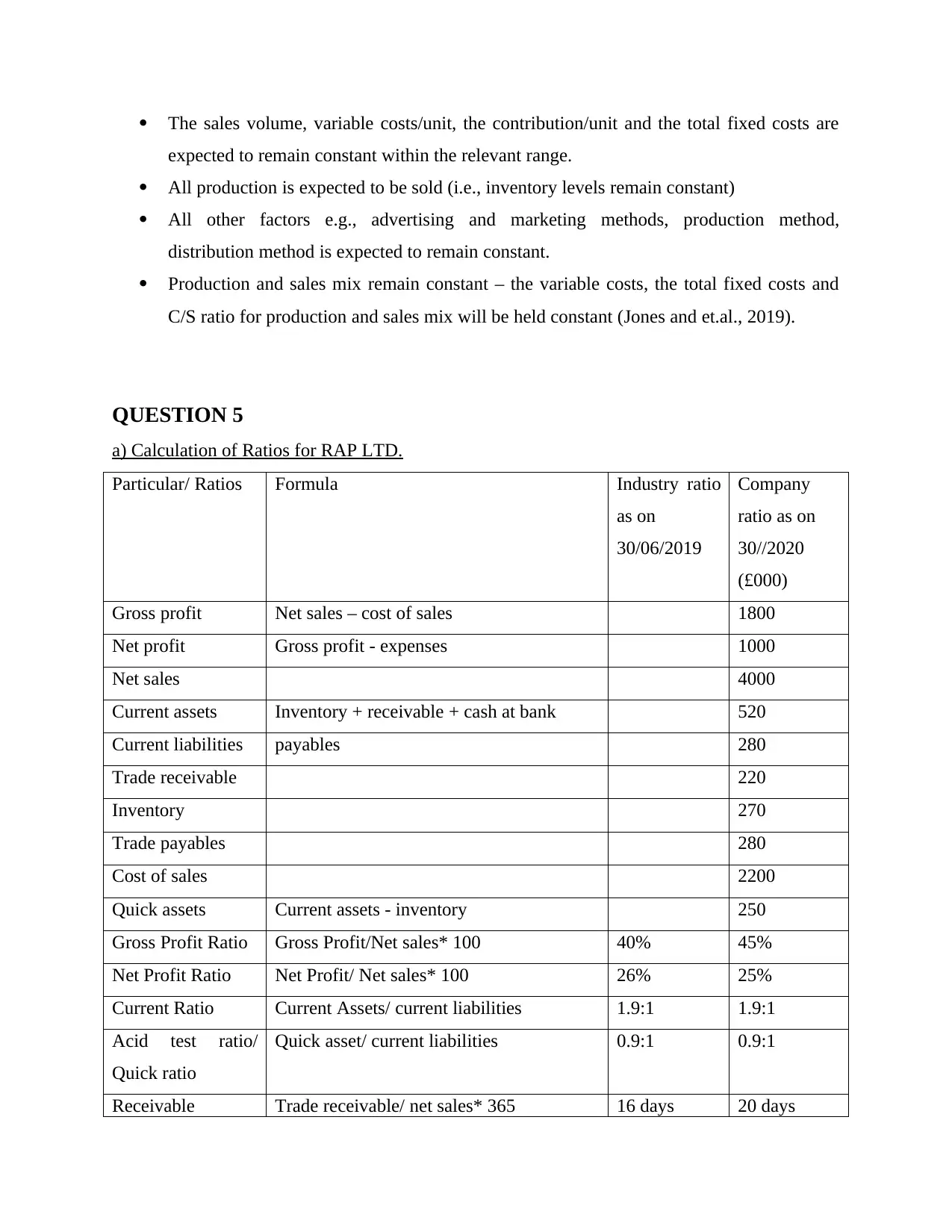

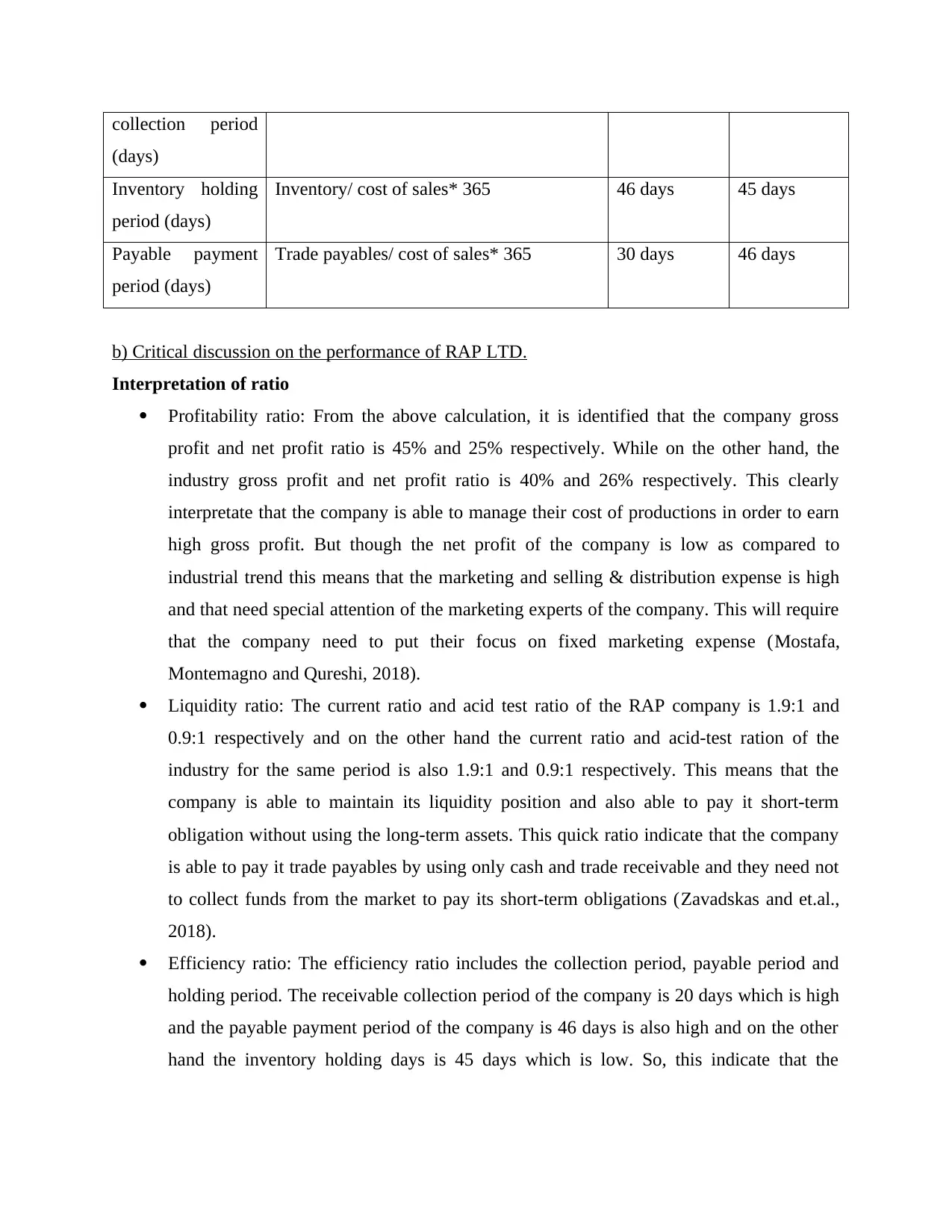

This accounting assignment delves into comprehensive financial analysis, encompassing the creation of income statements and statements of financial position. It presents detailed calculations of profitability ratios, including gross profit and net profit margins, and liquidity ratios like current and acid-test ratios, applied to the case of RAP LTD. Furthermore, the assignment explores break-even analysis, margin of safety calculations, and the impact of changes in selling prices on a company's financial performance, demonstrated through the analysis of MS LTD. Critical discussions on company performance based on calculated ratios are included, along with assumptions, limitations and recommendations for improvement. The assignment provides a practical application of accounting principles to assess financial health and make informed business decisions, supported by relevant references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.