Financial Statement Analysis and Ratio Analysis Report - MBA504

VerifiedAdded on 2022/09/30

|4

|736

|84

Report

AI Summary

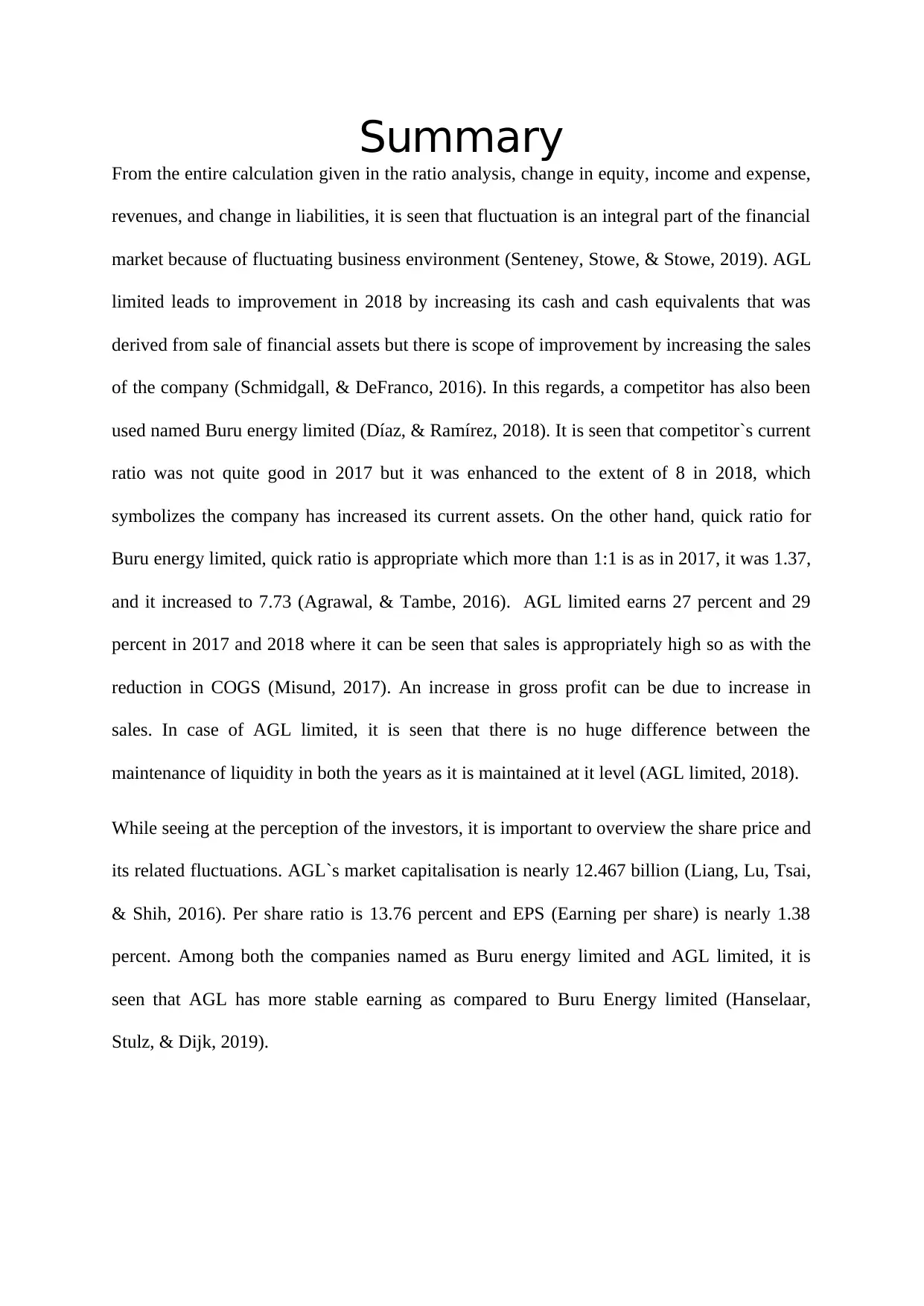

This report presents a financial analysis of AGL Limited and Buru Energy Limited, examining their financial performance through ratio analysis and comparison. The analysis covers key financial statements, including balance sheets, income statements, and cash flow statements. The report highlights fluctuations in the financial market and evaluates the companies' liquidity, profitability, and investor perceptions. It compares the current and quick ratios of both companies, assessing their ability to meet short-term obligations. The report also analyzes the gross profit margins and sales performance of AGL Limited, while considering market capitalization and earnings per share (EPS) to assess the stability of earnings. The references provided support the findings and analysis presented in the report.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.