University Financial Analysis Report: Crystal Hotel Decision Making

VerifiedAdded on 2022/09/25

|14

|2532

|15

Report

AI Summary

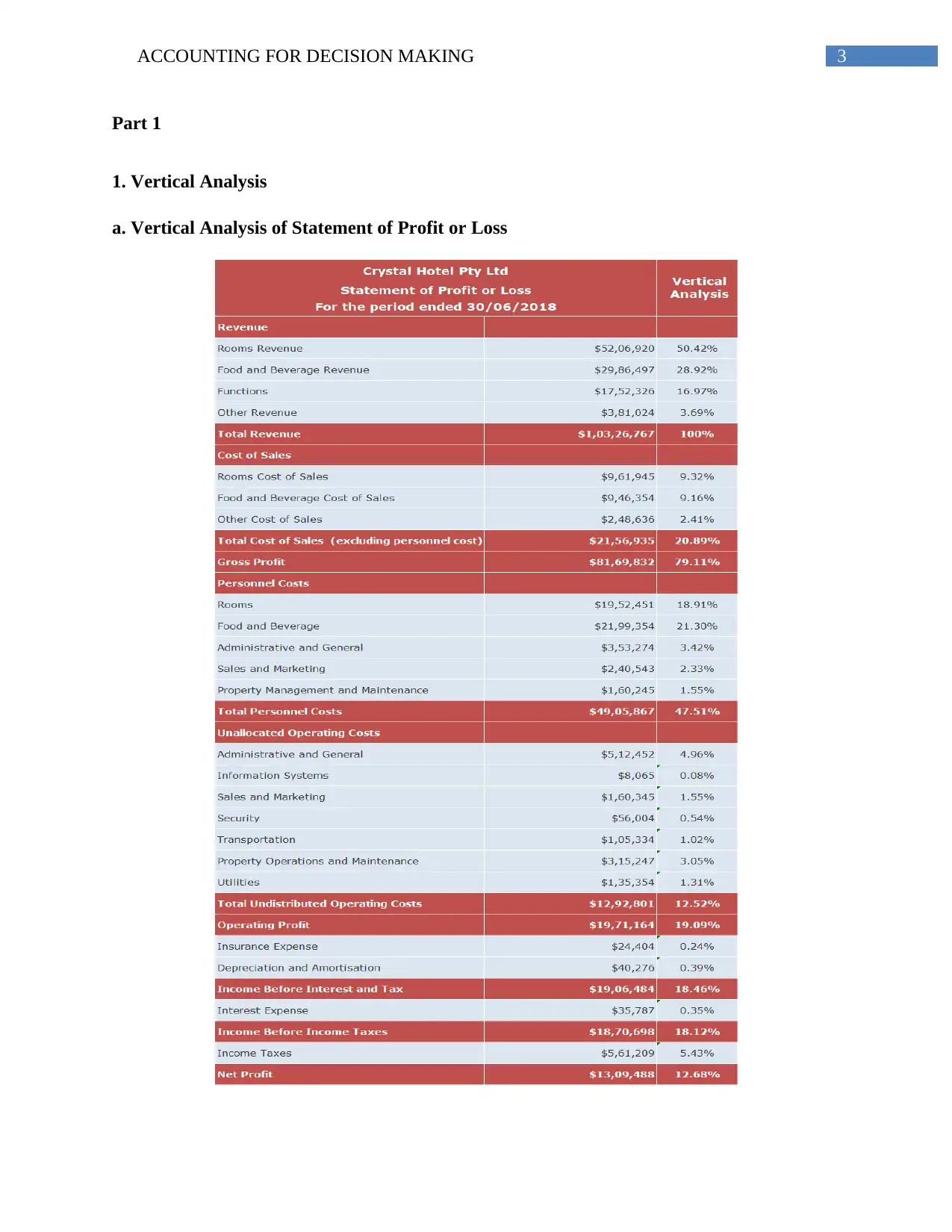

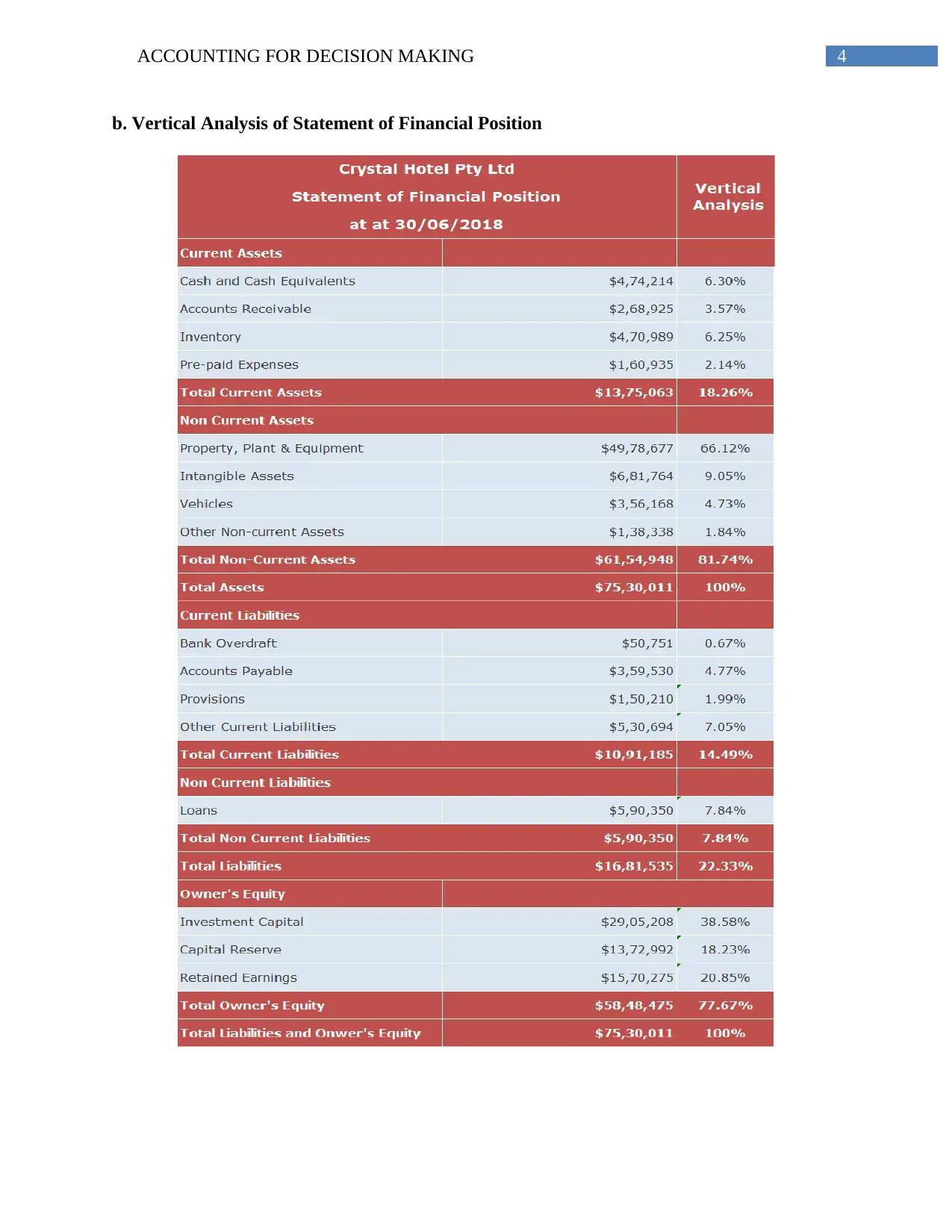

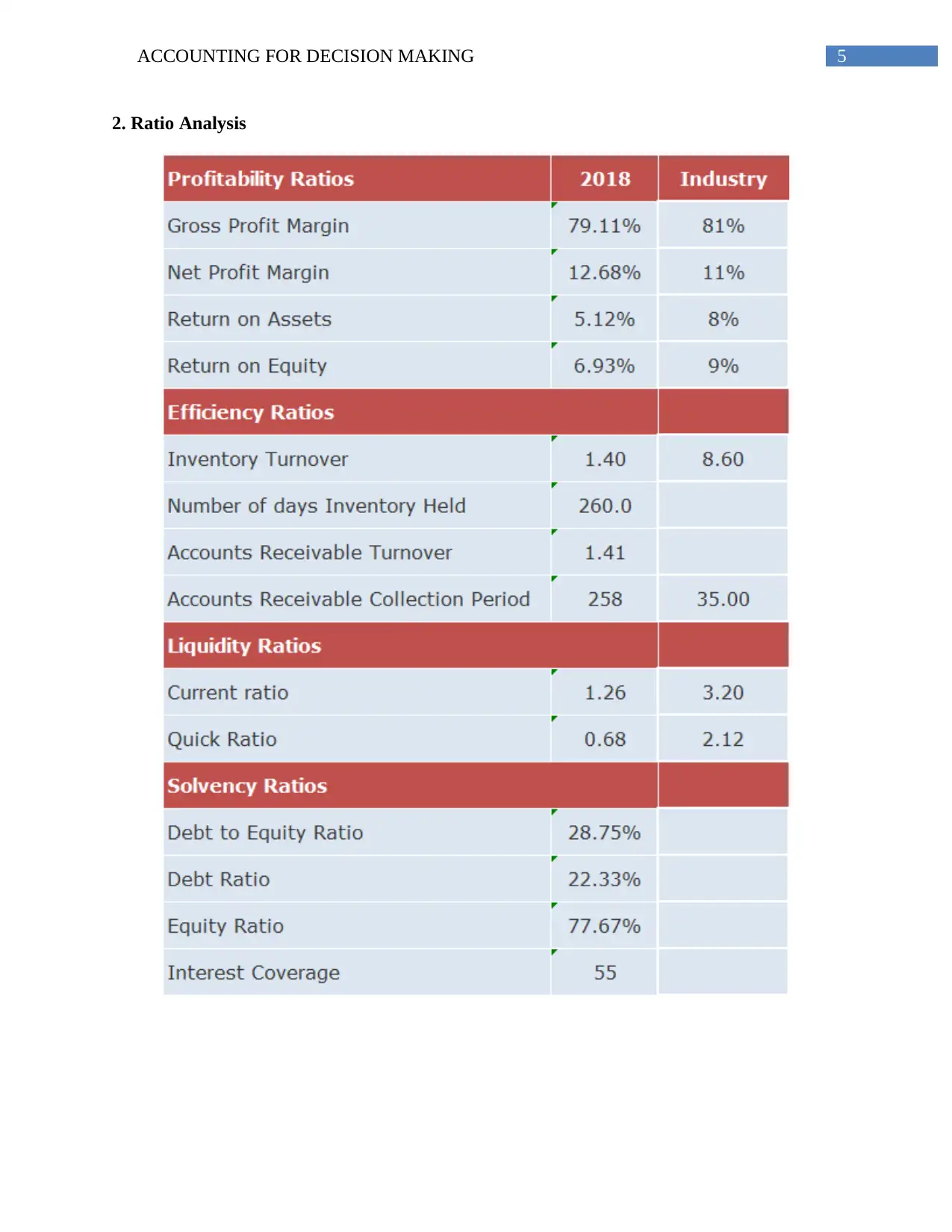

This report provides a comprehensive financial analysis of Crystal Hotel Pty Ltd, assessing its current financial standing to aid management in expansion planning. The analysis involves a vertical analysis of the statements of profit or loss and financial position, along with an examination of profitability, efficiency, liquidity, and solvency ratios. The analysis reveals that Crystal Hotel has struggled to generate sufficient revenue from rooms and food and beverage sales compared to industry standards, with associated costs also being higher. The report highlights inefficiencies in asset and equity utilization, slow inventory turnover, and delayed receivables collection, impacting overall efficiency. Furthermore, the analysis indicates liquidity issues due to inadequate current and quick assets. Despite these challenges, Crystal Hotel maintains a lower reliance on debt due to its significant equity capital. The report concludes with recommendations for improvement in revenue generation, cost reduction, and efficiency enhancement, along with suggestions for additional industry-specific benchmarks like ADR, RevPAR, and occupancy rate to facilitate comparative analysis and better decision-making.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.