Corporate Accounting: Financial Statement Analysis of Two Companies

VerifiedAdded on 2023/06/05

|34

|3747

|150

Report

AI Summary

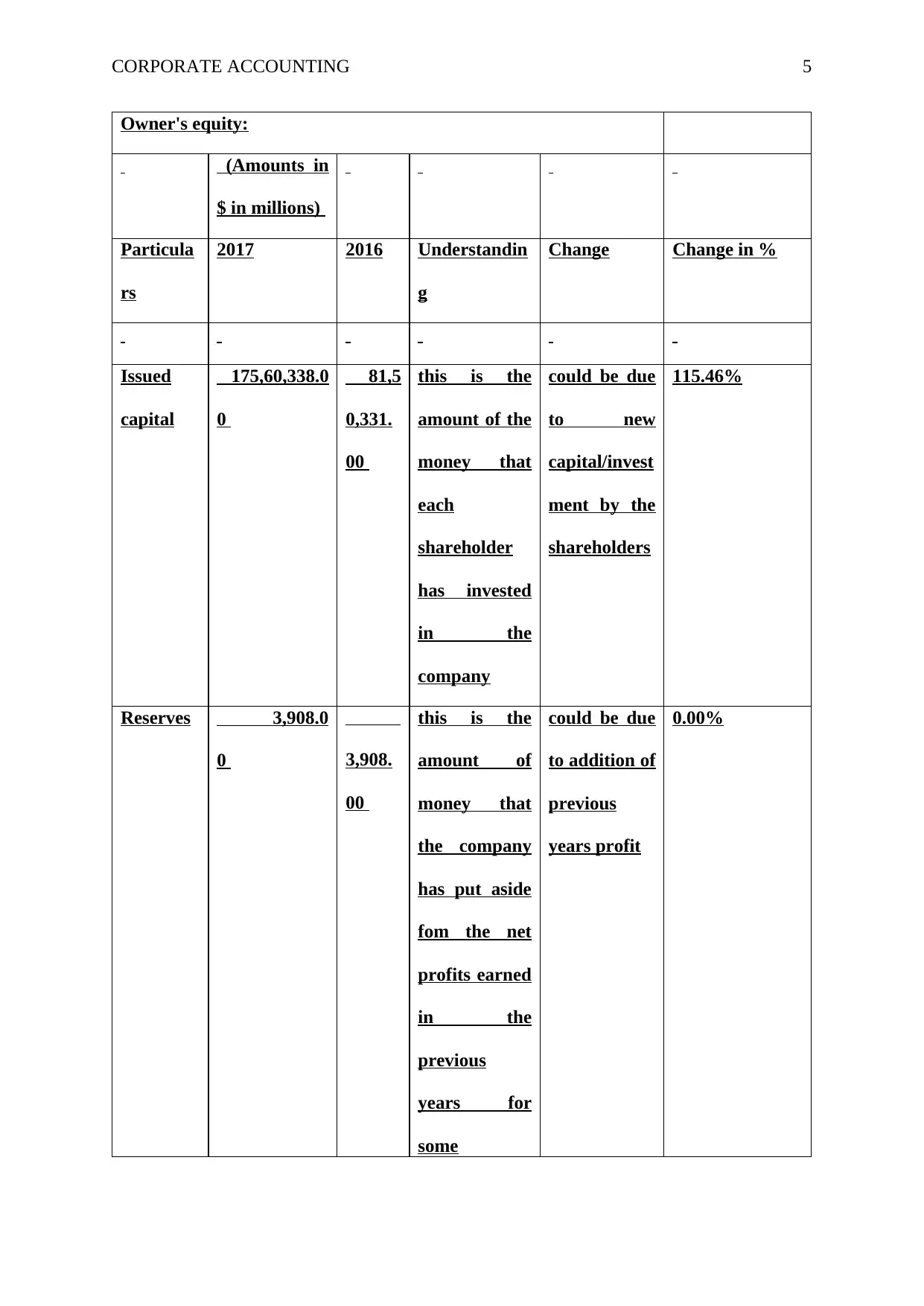

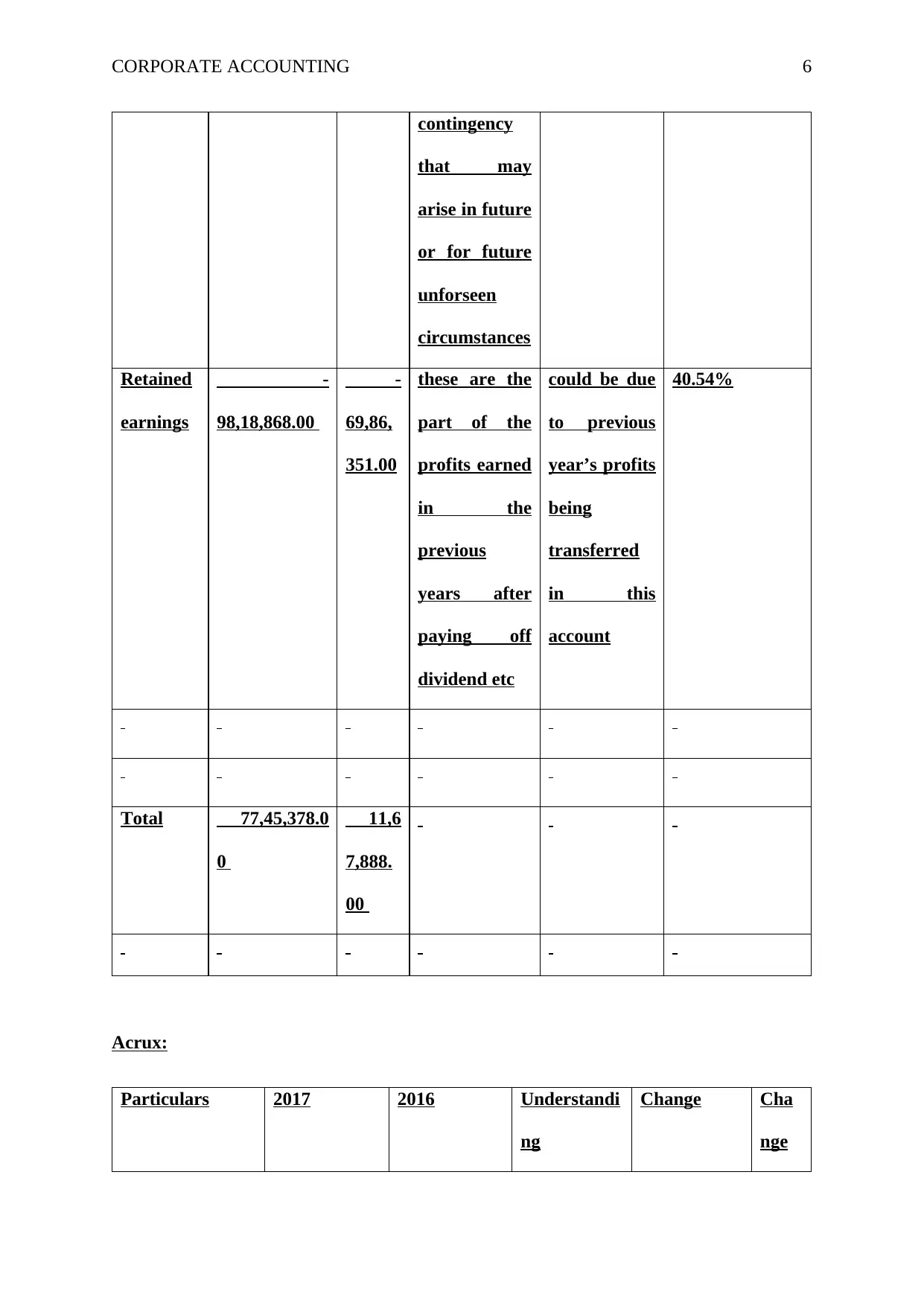

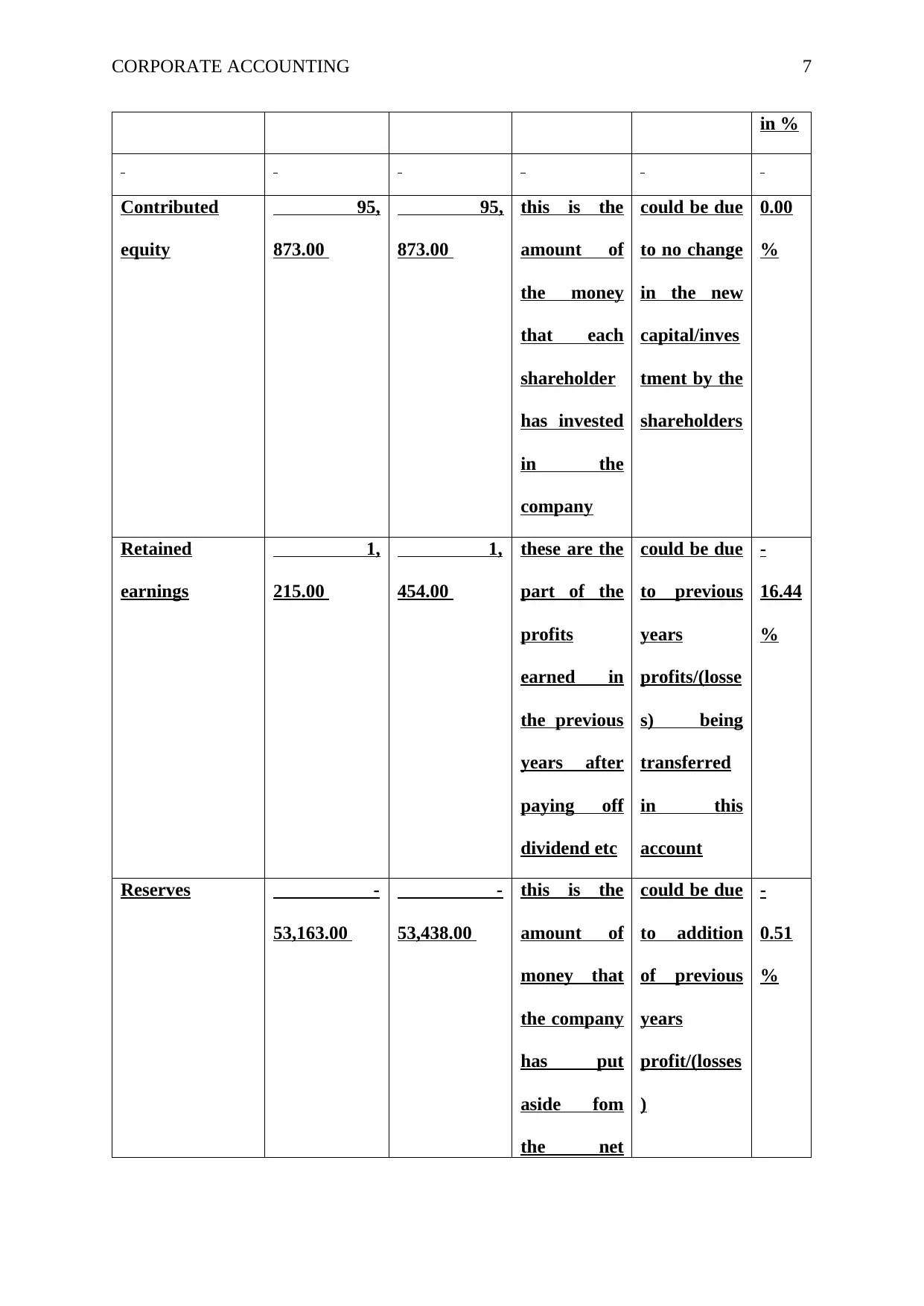

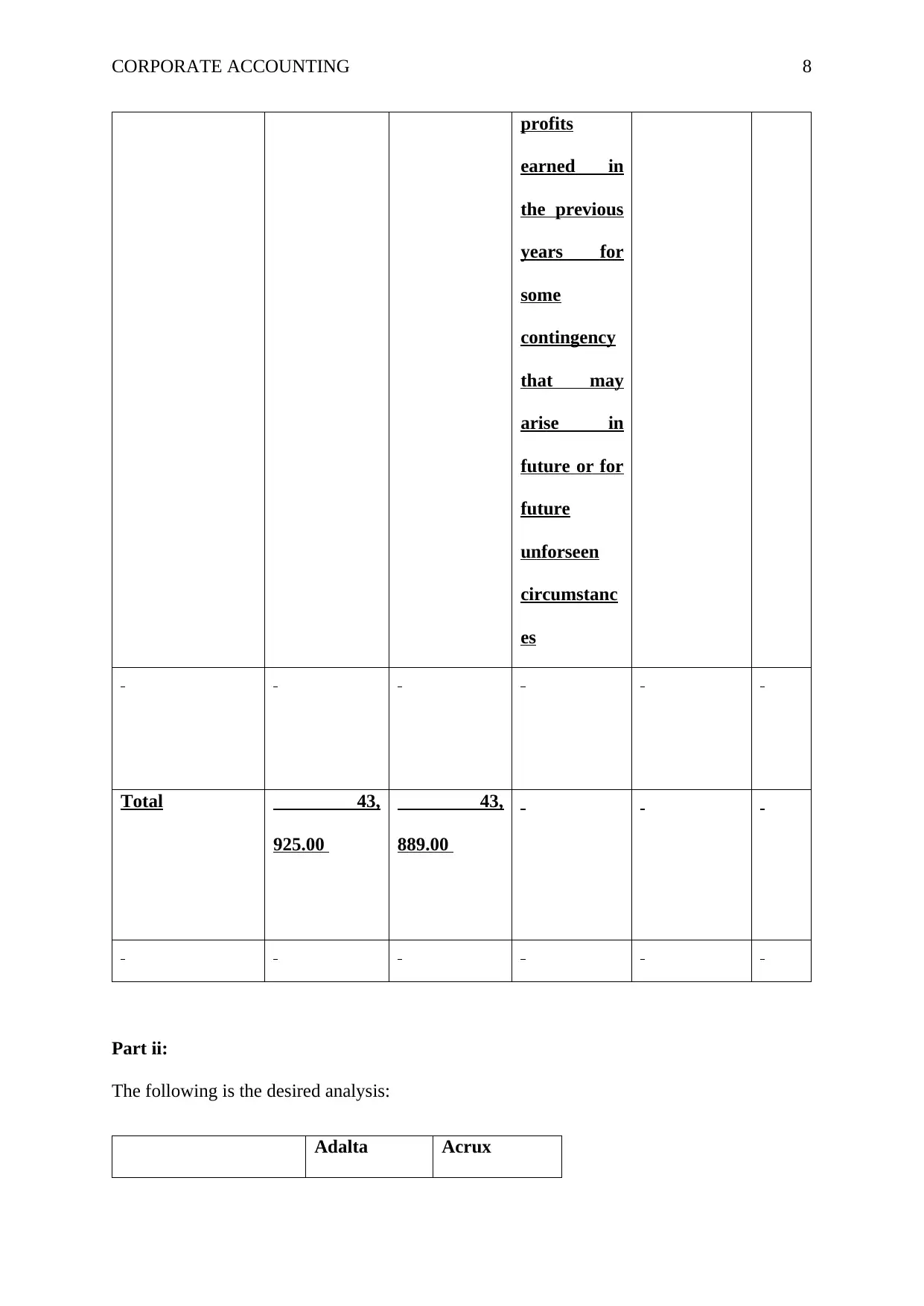

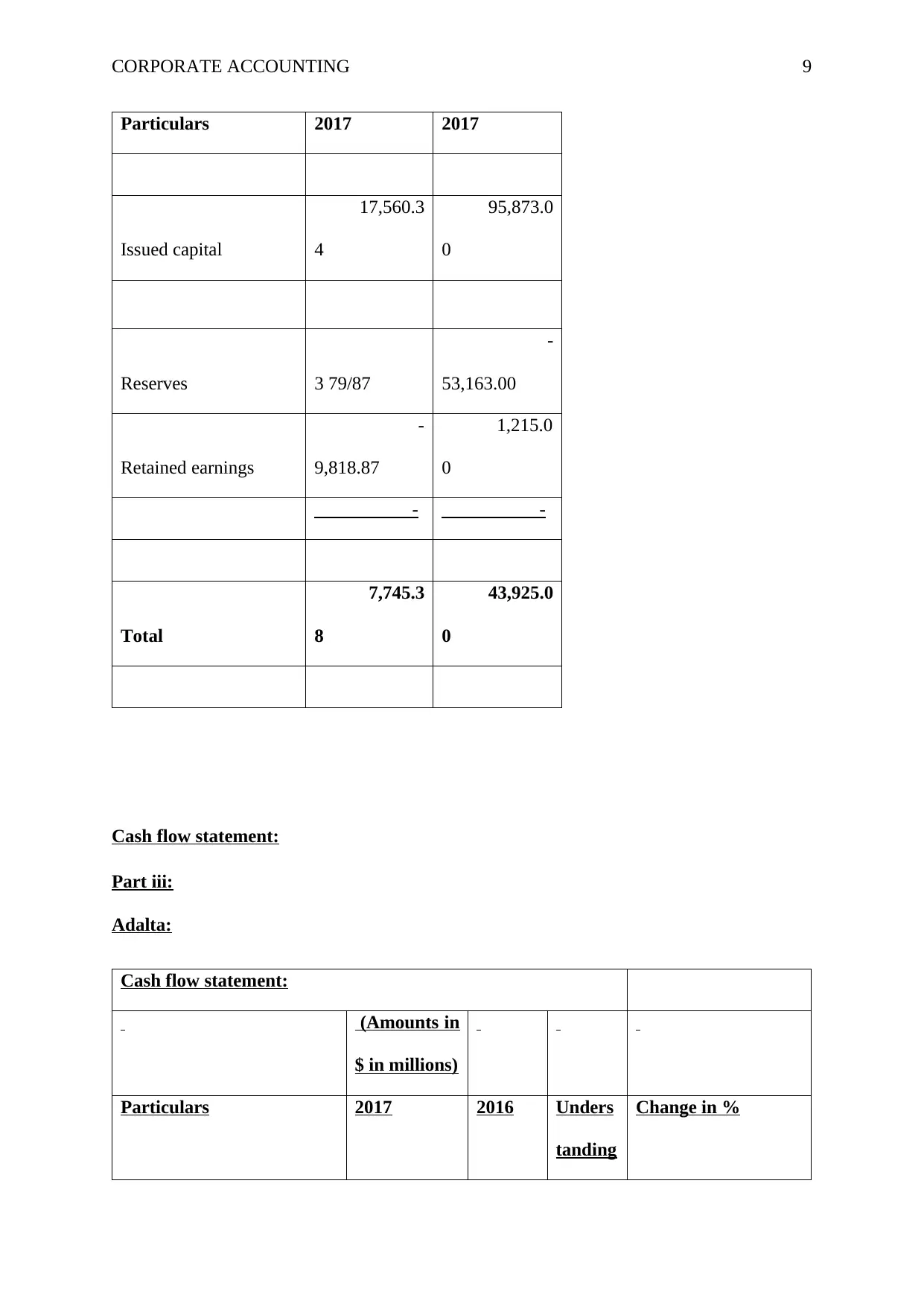

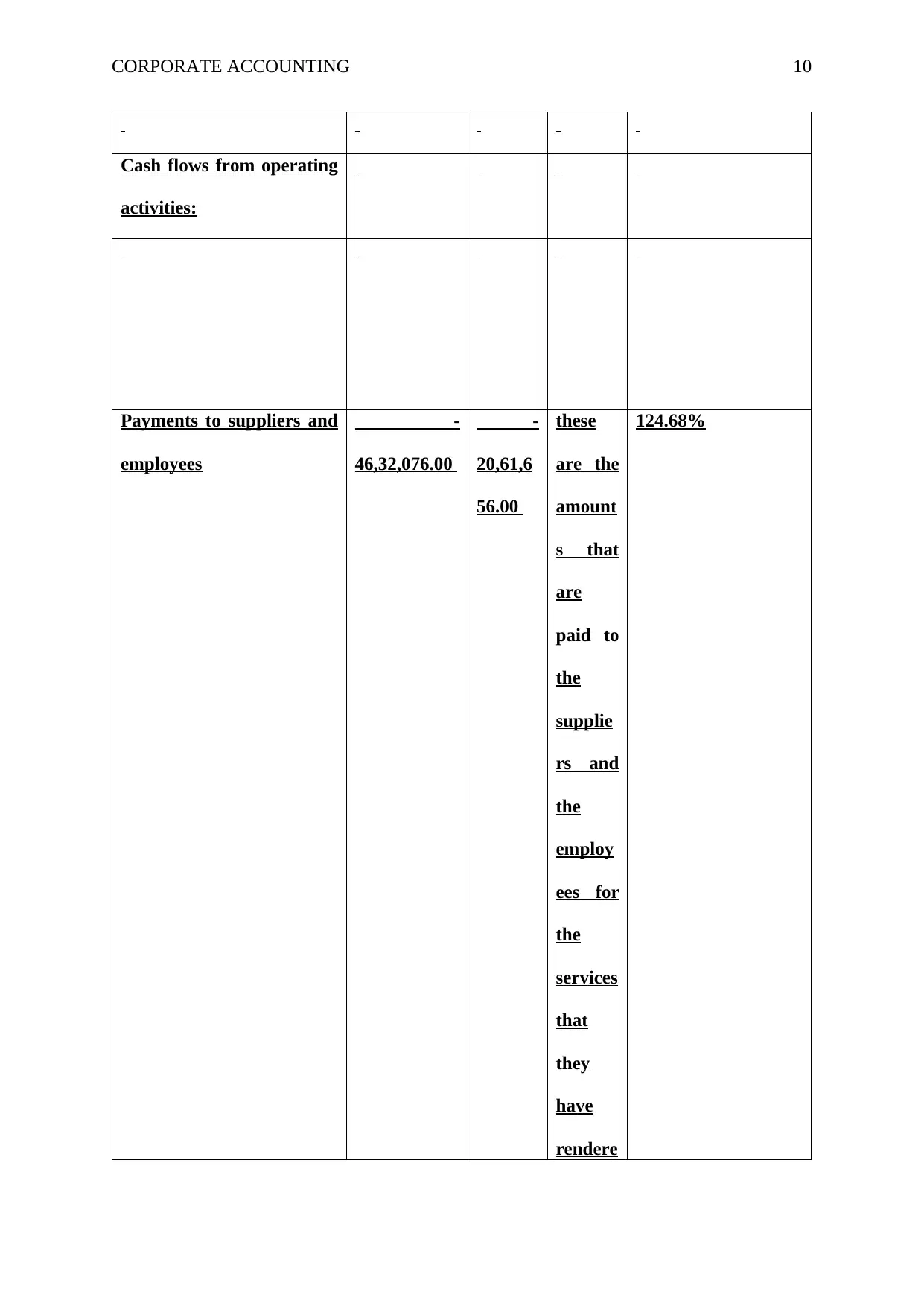

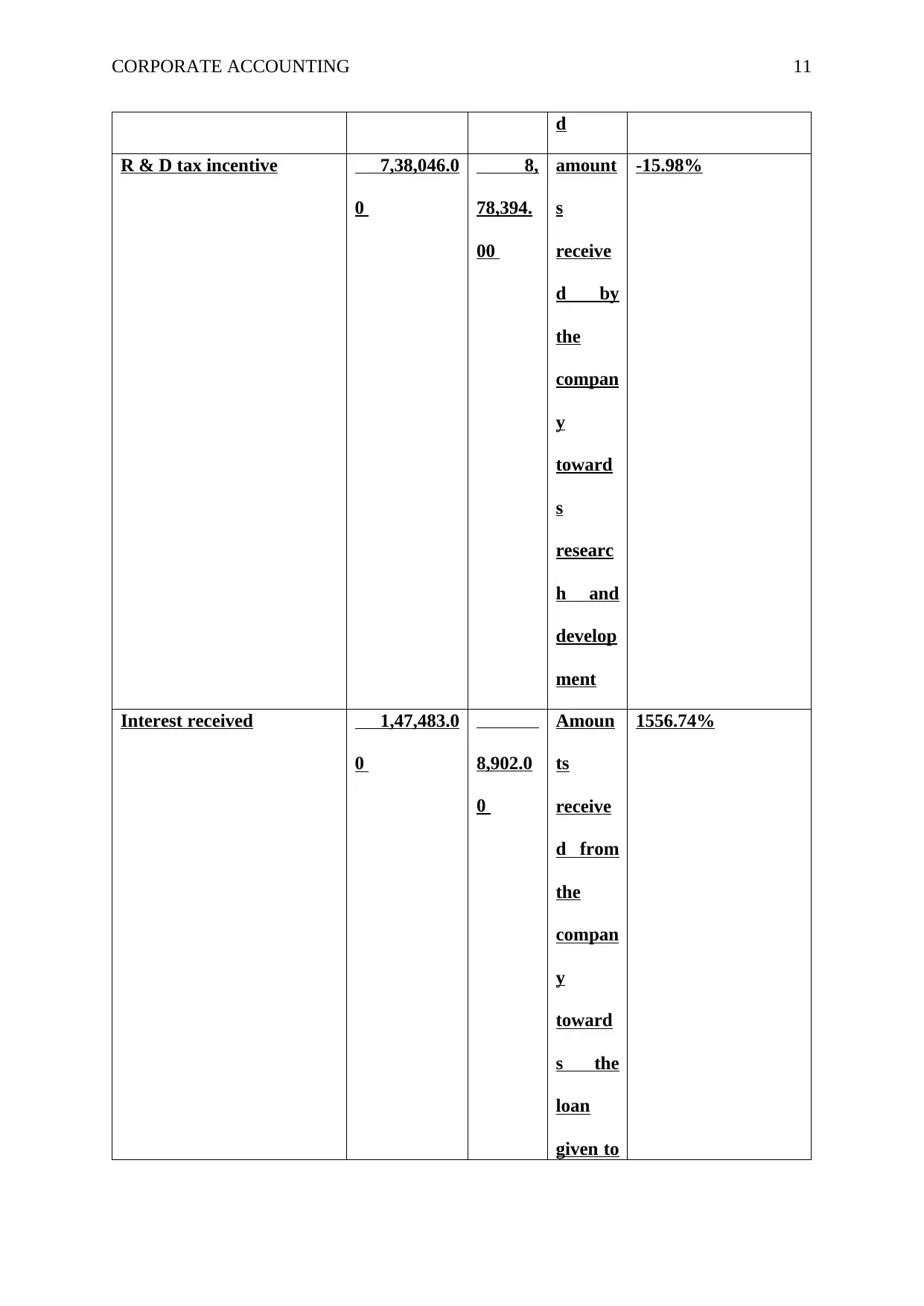

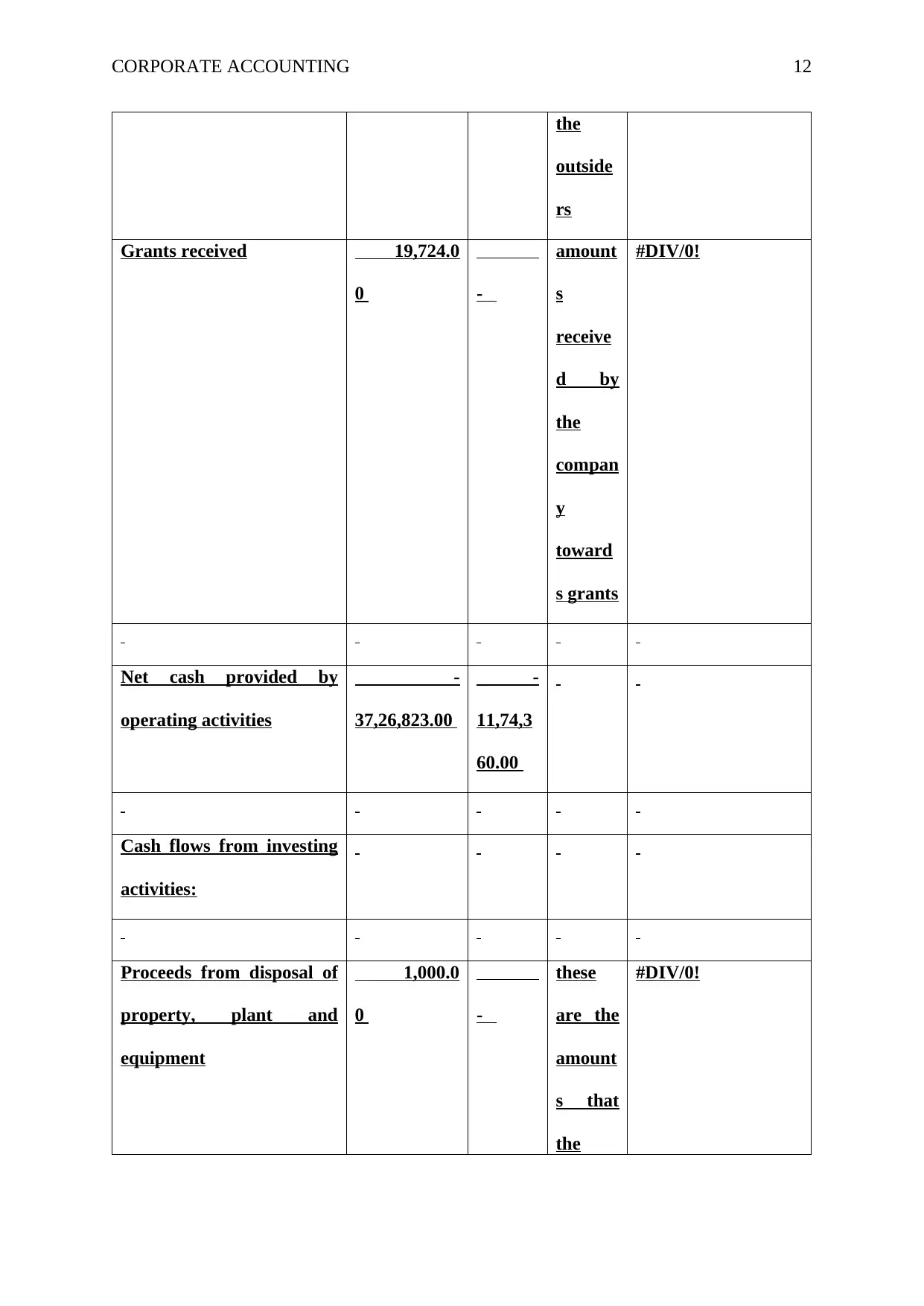

This report presents a comprehensive analysis of the financial statements of two pharmaceutical companies, Adalta Limited and Acrux Limited. The analysis covers various aspects of the companies' financial positions, including the break-up of owners' equity, other comprehensive income statements, and cash flow statements. The report provides detailed comparisons between the two companies, examining their financial performance over specific periods. It also delves into the accounting treatment of corporate income tax, including deferred tax assets and liabilities, and the differences between effective and cash tax rates. Furthermore, the report highlights the significance of these financial statements in understanding the companies' overall financial health and performance. The analysis provides a clear understanding of the financial position of each company.

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.