Financial Statement Analysis Assignment - HC1010 Accounting

VerifiedAdded on 2023/01/10

|9

|1296

|71

Homework Assignment

AI Summary

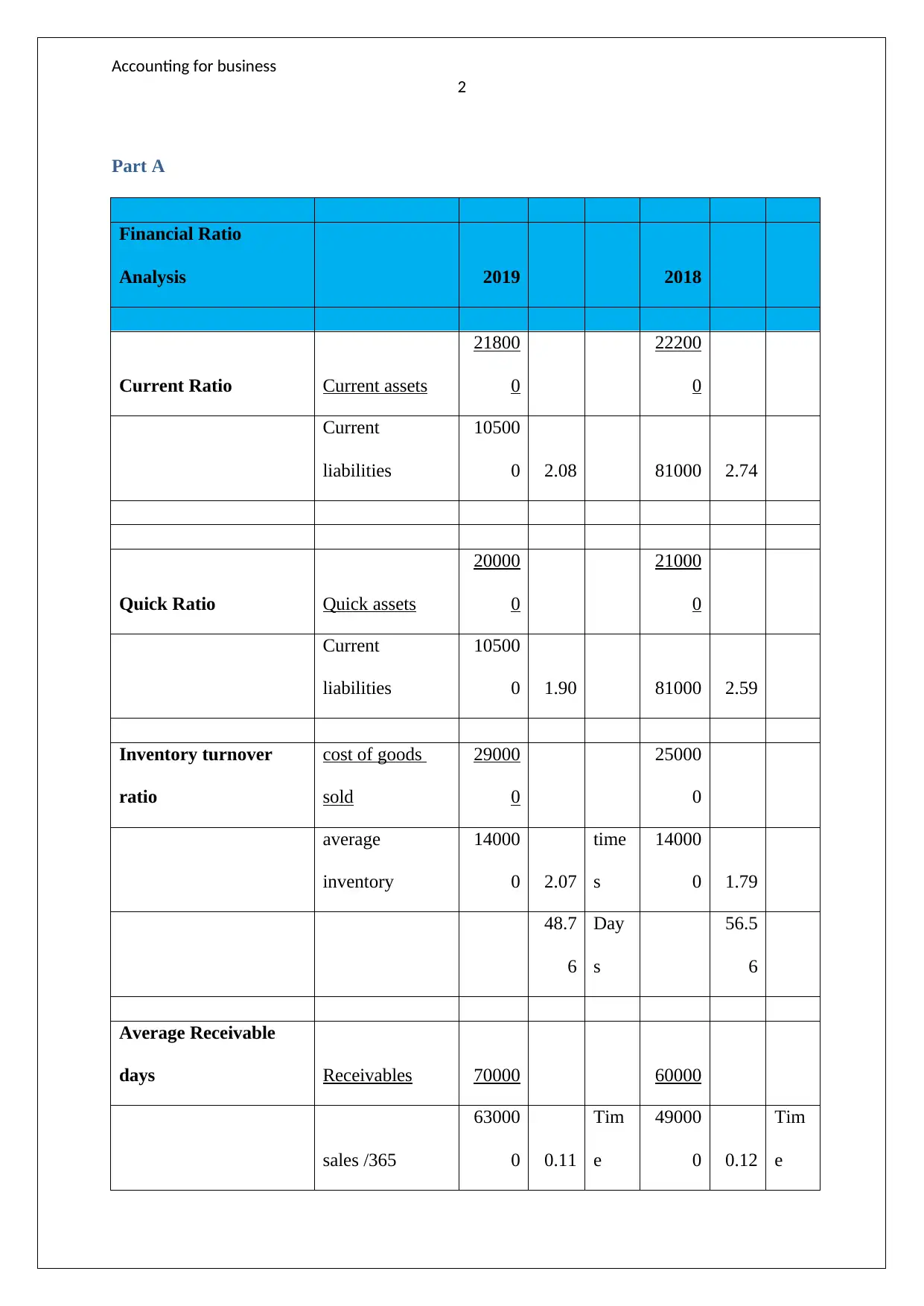

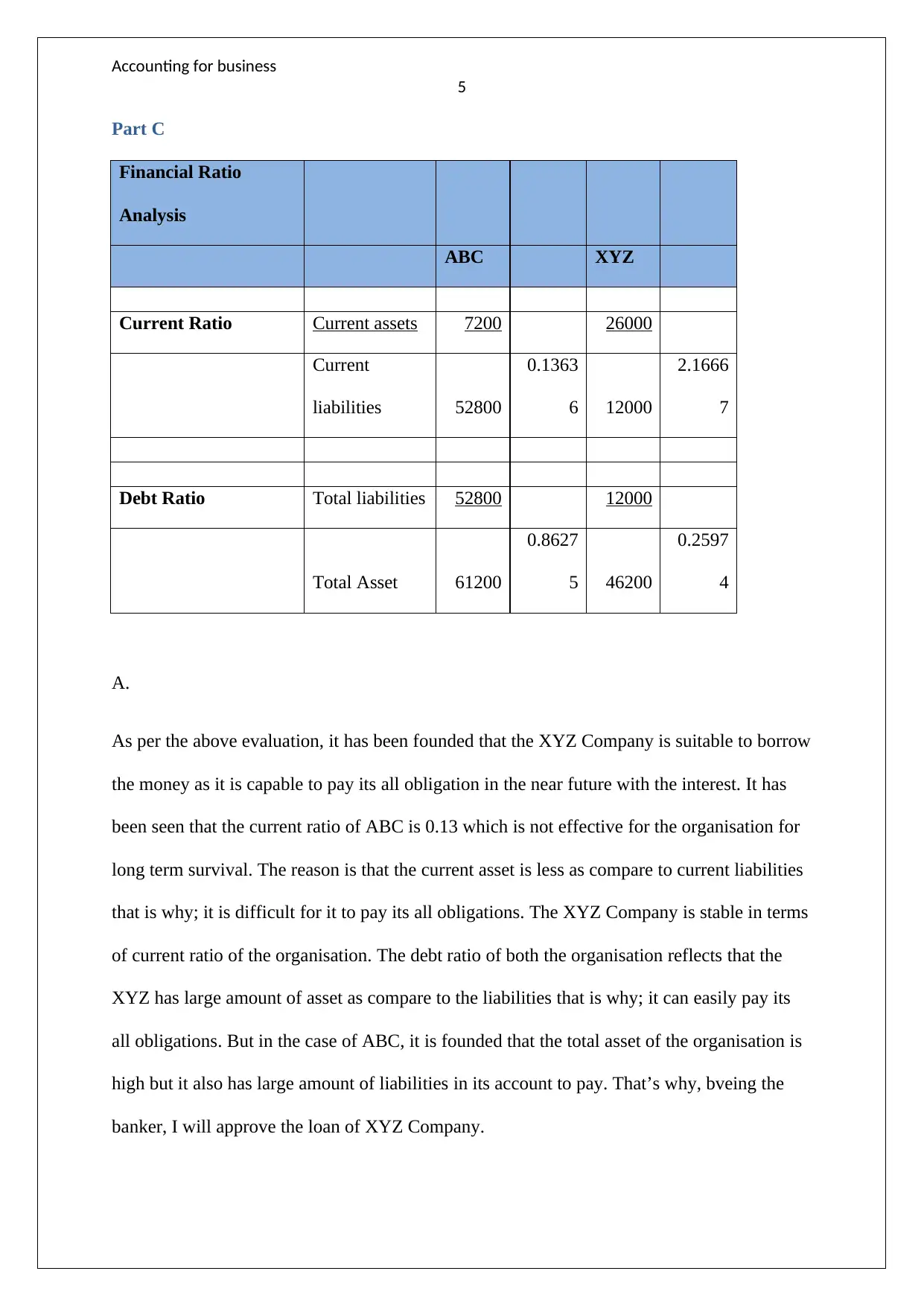

This assignment provides a detailed analysis of financial statements and ratios, including current, quick, inventory turnover, and debt ratios. Part A focuses on financial ratio analysis for 2018 and 2019, evaluating liquidity and efficiency. Part B defines income and revenue according to Australian Accounting Standards, applying these concepts to a case study. Part C analyzes financial ratios for two companies, ABC and XYZ, to determine which is suitable for a loan and investment, considering their financial positions and debt levels. The assignment demonstrates the application of accounting principles to assess business performance and make informed decisions. References from accounting resources and standards are included to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.