Financial Statement Analysis: Holmes Institute HC1010 Assignment

VerifiedAdded on 2022/11/11

|5

|1177

|69

Homework Assignment

AI Summary

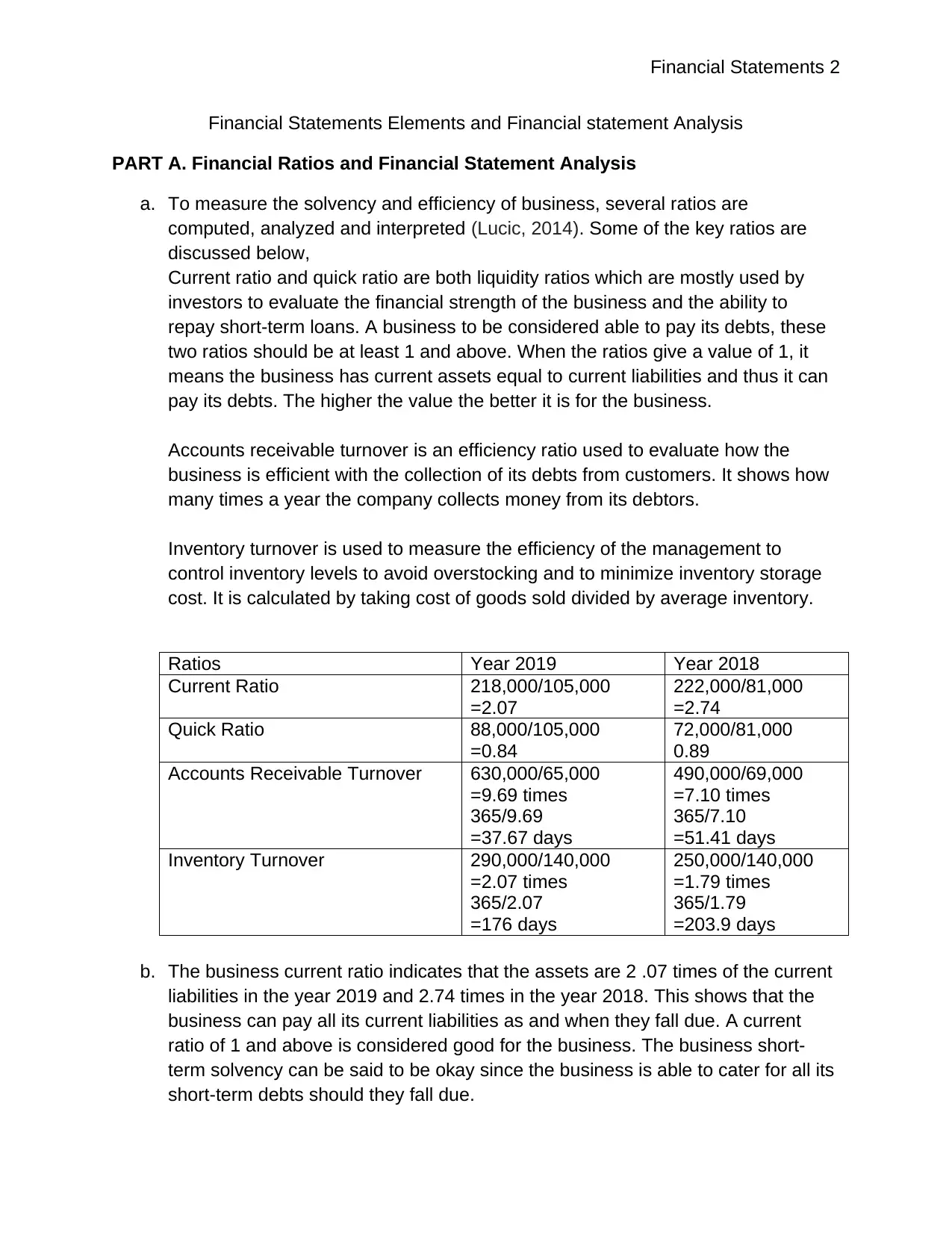

This assignment analyzes financial statements, focusing on key financial ratios such as current ratio, quick ratio, accounts receivable turnover, and inventory turnover to assess a business's solvency and efficiency. The document compares these ratios for two different years, providing insights into the business's financial health and identifying areas for improvement. Furthermore, the assignment distinguishes between income and revenue, clarifying their definitions and applications within a business context. It also compares the balance sheets of two companies, using the data to determine which business is more suitable for a short-term loan and investment based on their financial positions. The assignment utilizes the provided financial data to make informed decisions, demonstrating an understanding of financial statement analysis and its practical implications.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.