Financial Statement Analysis for General Mills and Kimberly-Clark

VerifiedAdded on 2020/05/28

|6

|632

|80

Homework Assignment

AI Summary

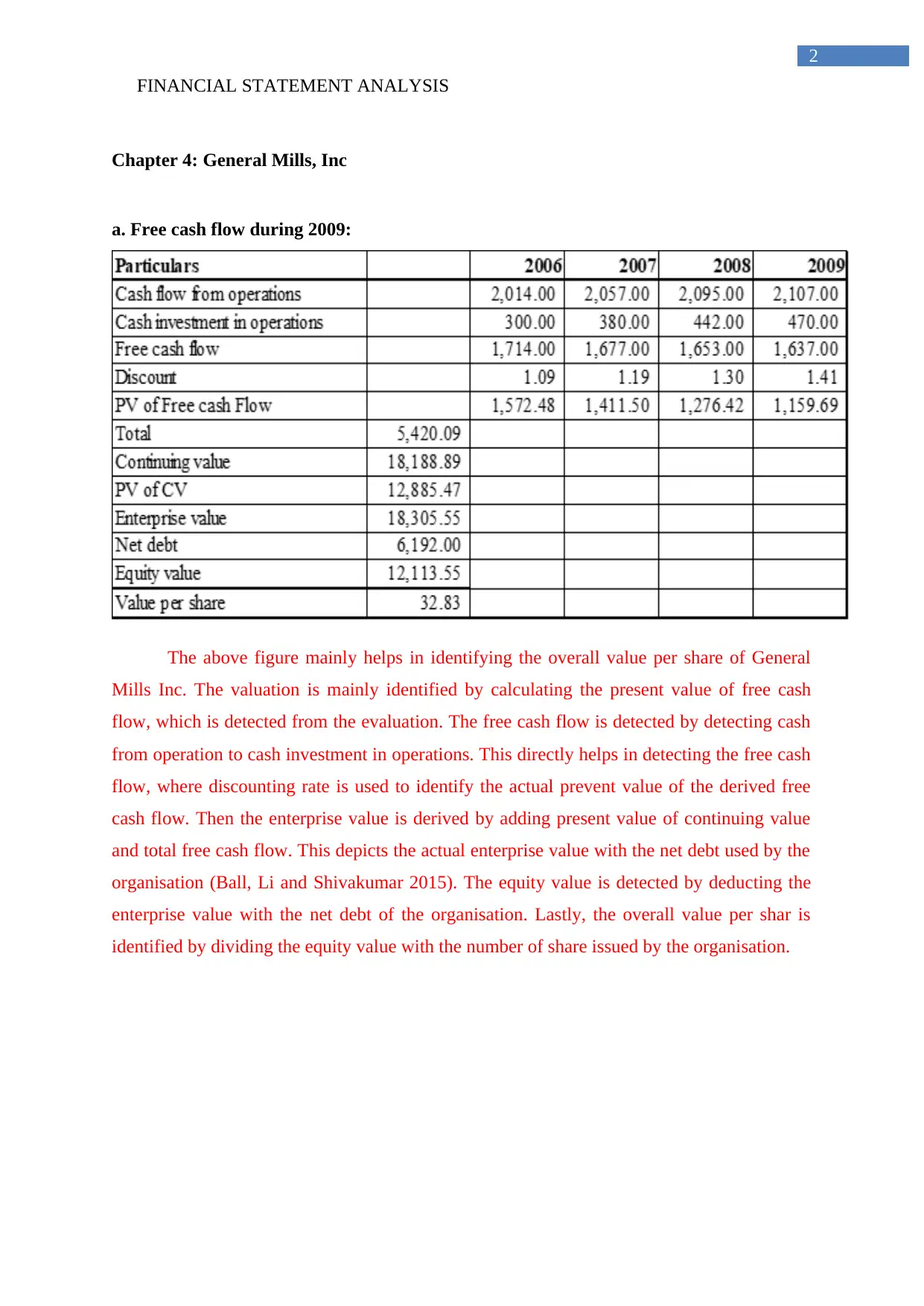

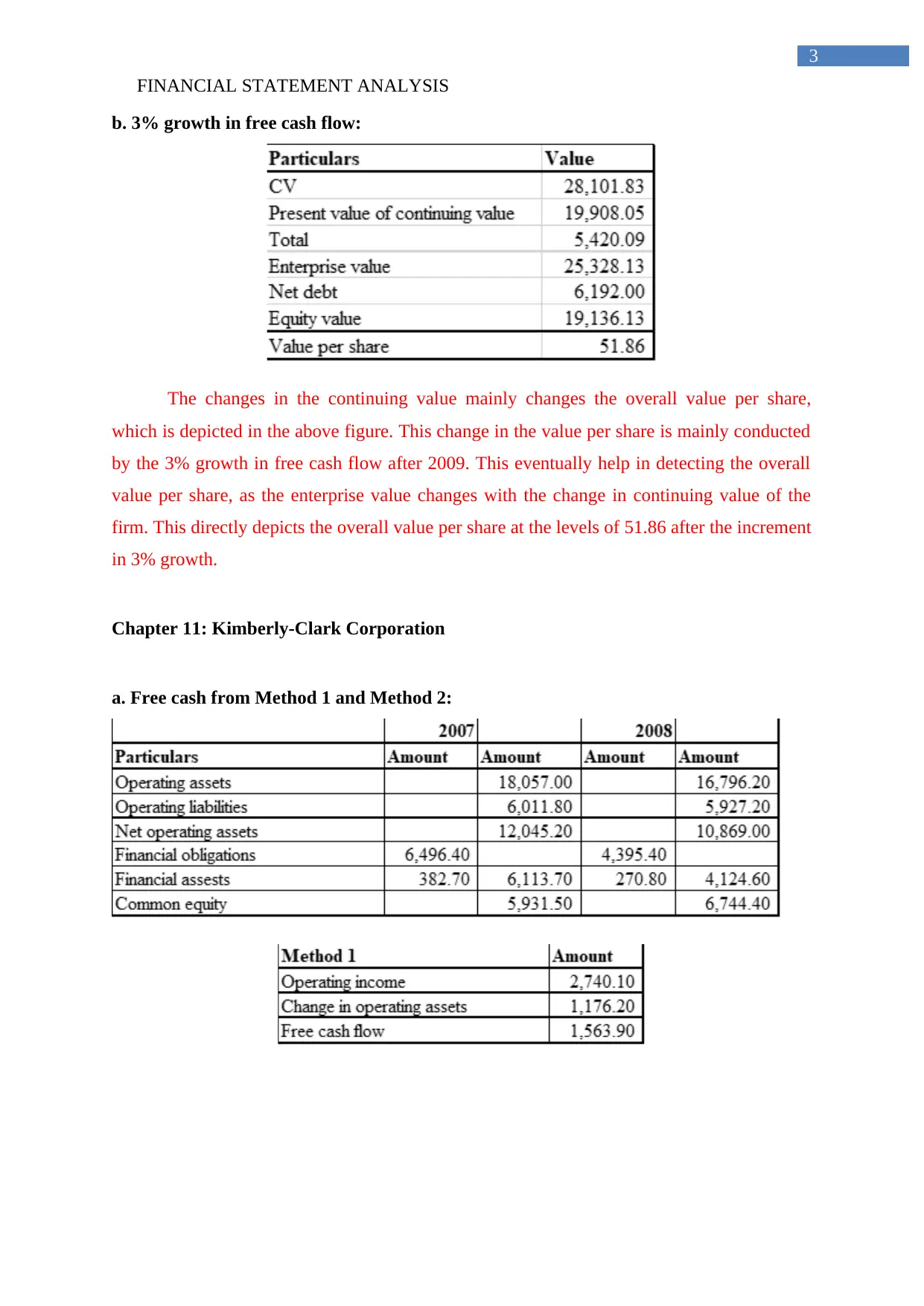

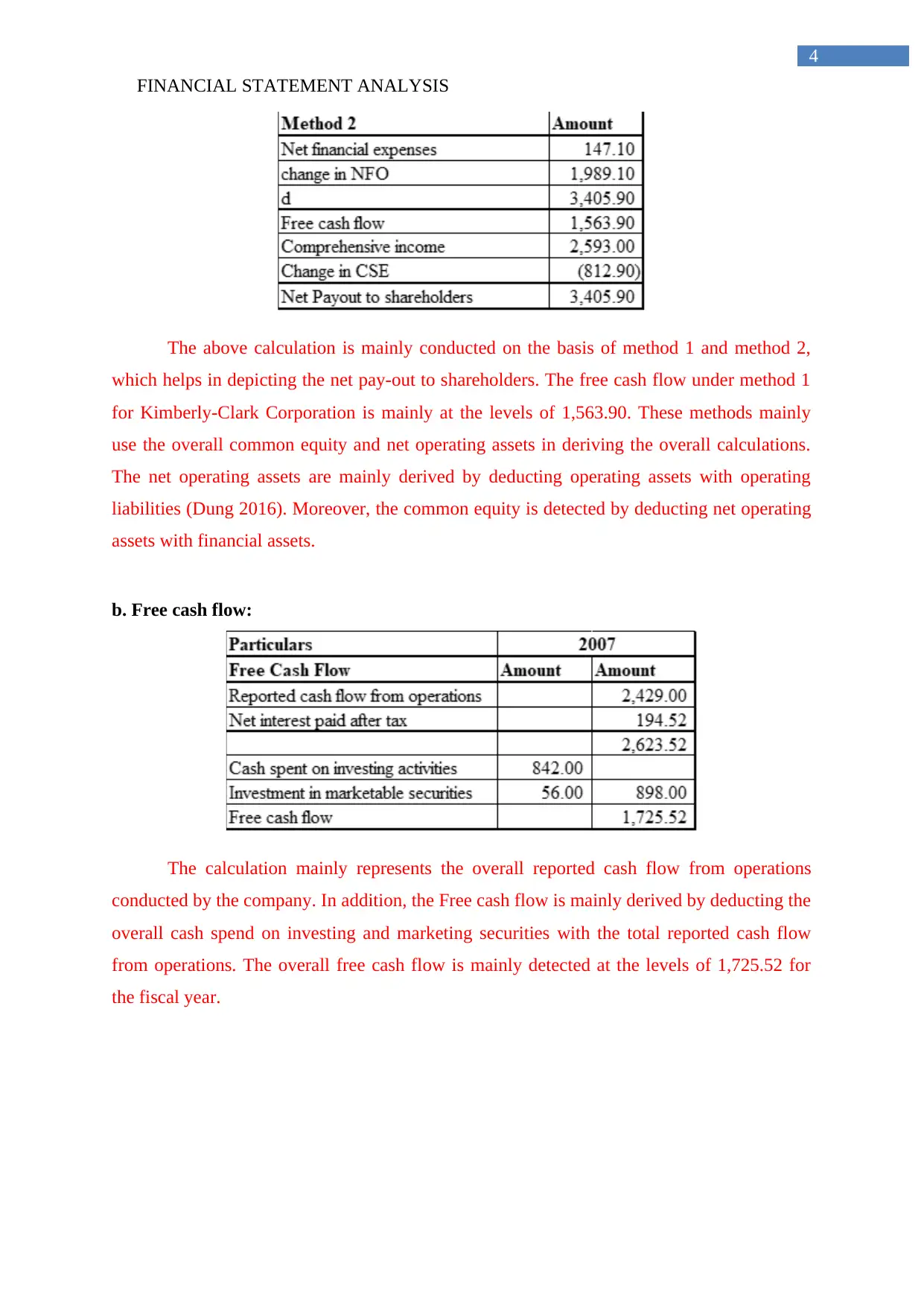

The assignment involves a detailed analysis of financial statements from two corporations, General Mills, Inc. and Kimberly-Clark Corporation. It emphasizes calculating free cash flow during 2009 for General Mills using the present value method to determine enterprise value and subsequently identify the overall value per share. A subsequent section examines how a projected 3% growth in free cash flow influences the company's valuation metrics. For Kimberly-Clark, the assignment includes calculations of free cash flow using two different methods—Method 1 and Method 2—and evaluating the net payout to shareholders. The report concludes with an analysis of reported operating cash flows and the deduction of investing and financing activities to determine overall free cash flow for the fiscal year.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.