Finance: Accounting and Management Decisions - Week 10 Analysis

VerifiedAdded on 2023/04/20

|11

|1735

|88

Homework Assignment

AI Summary

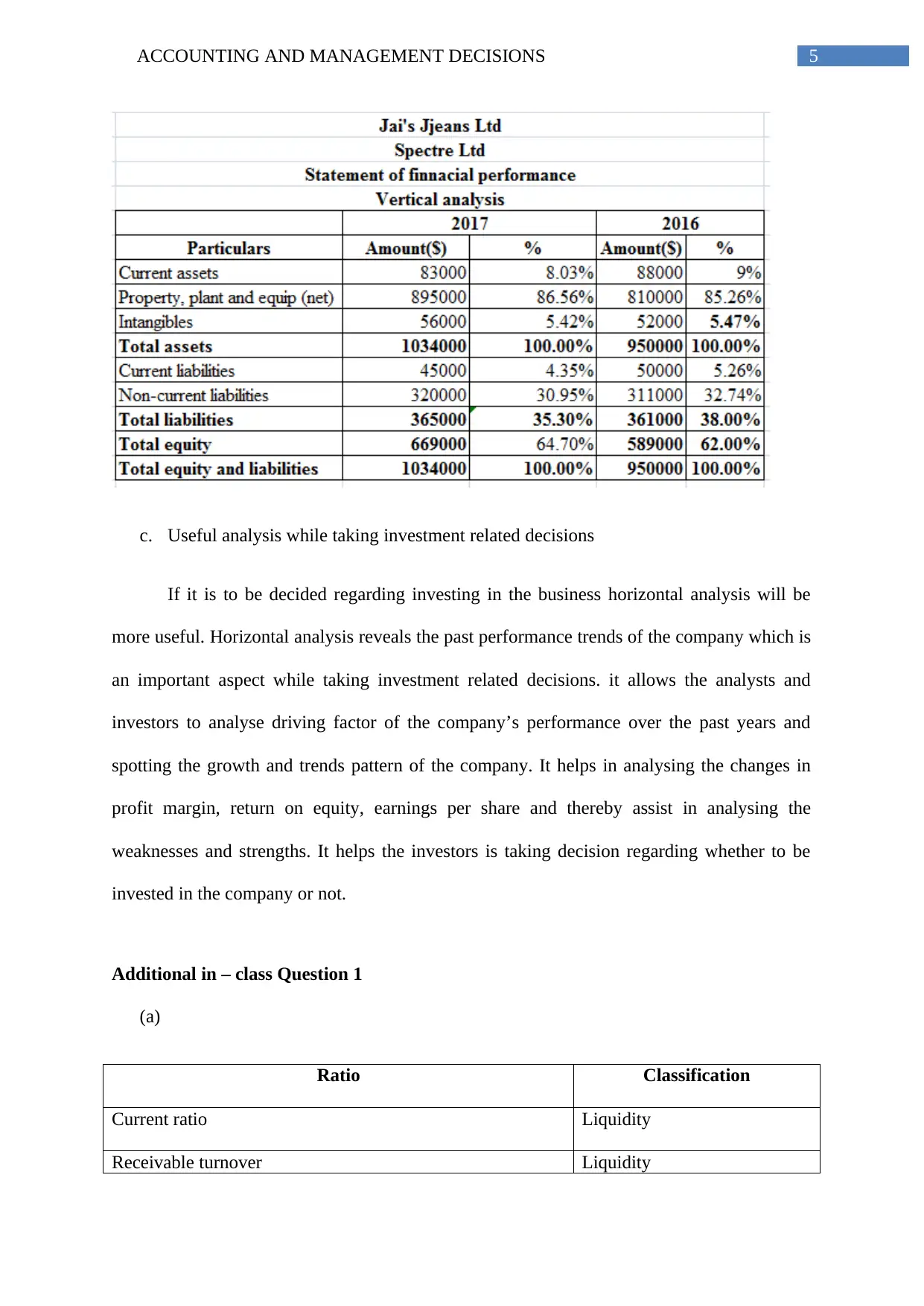

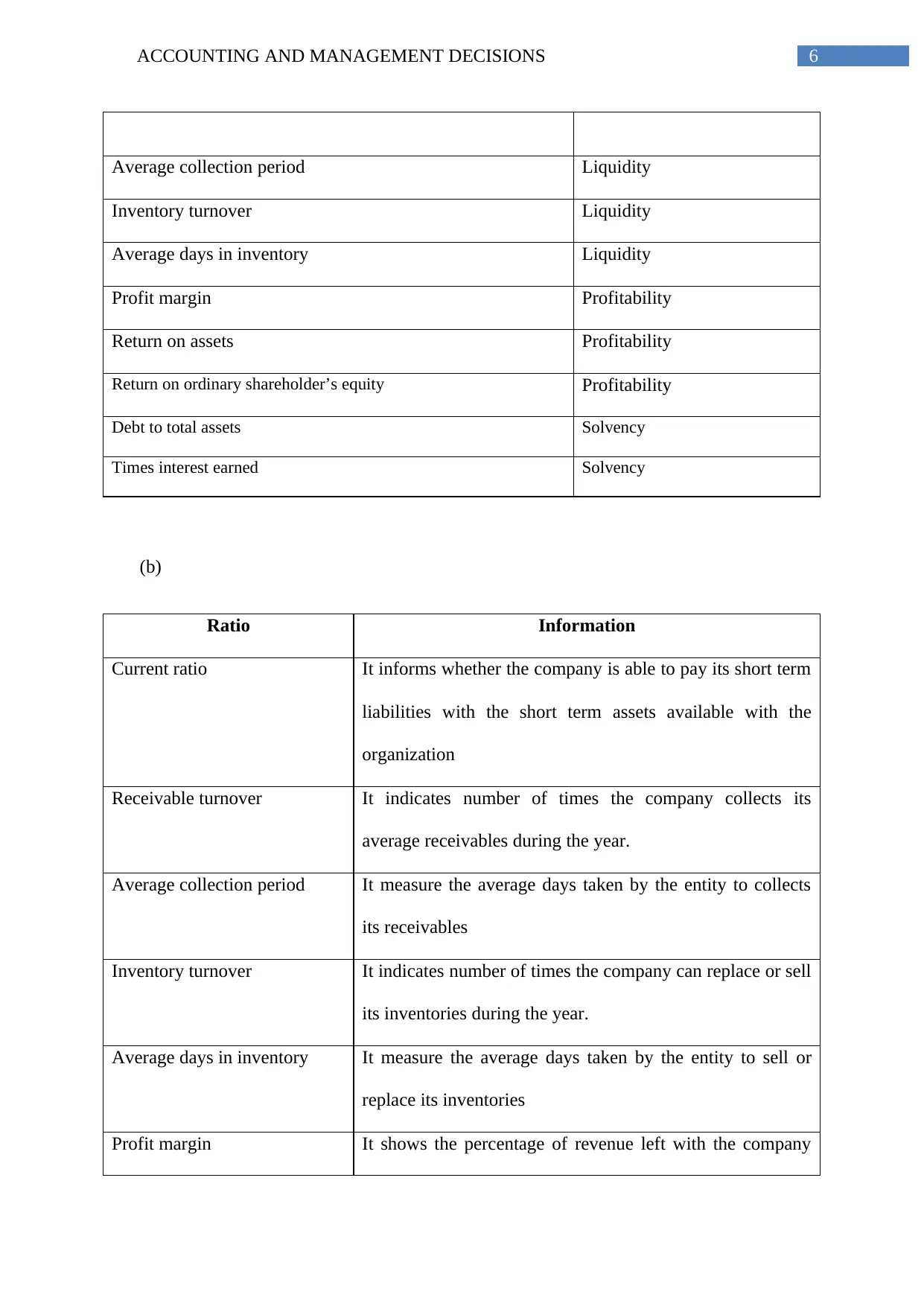

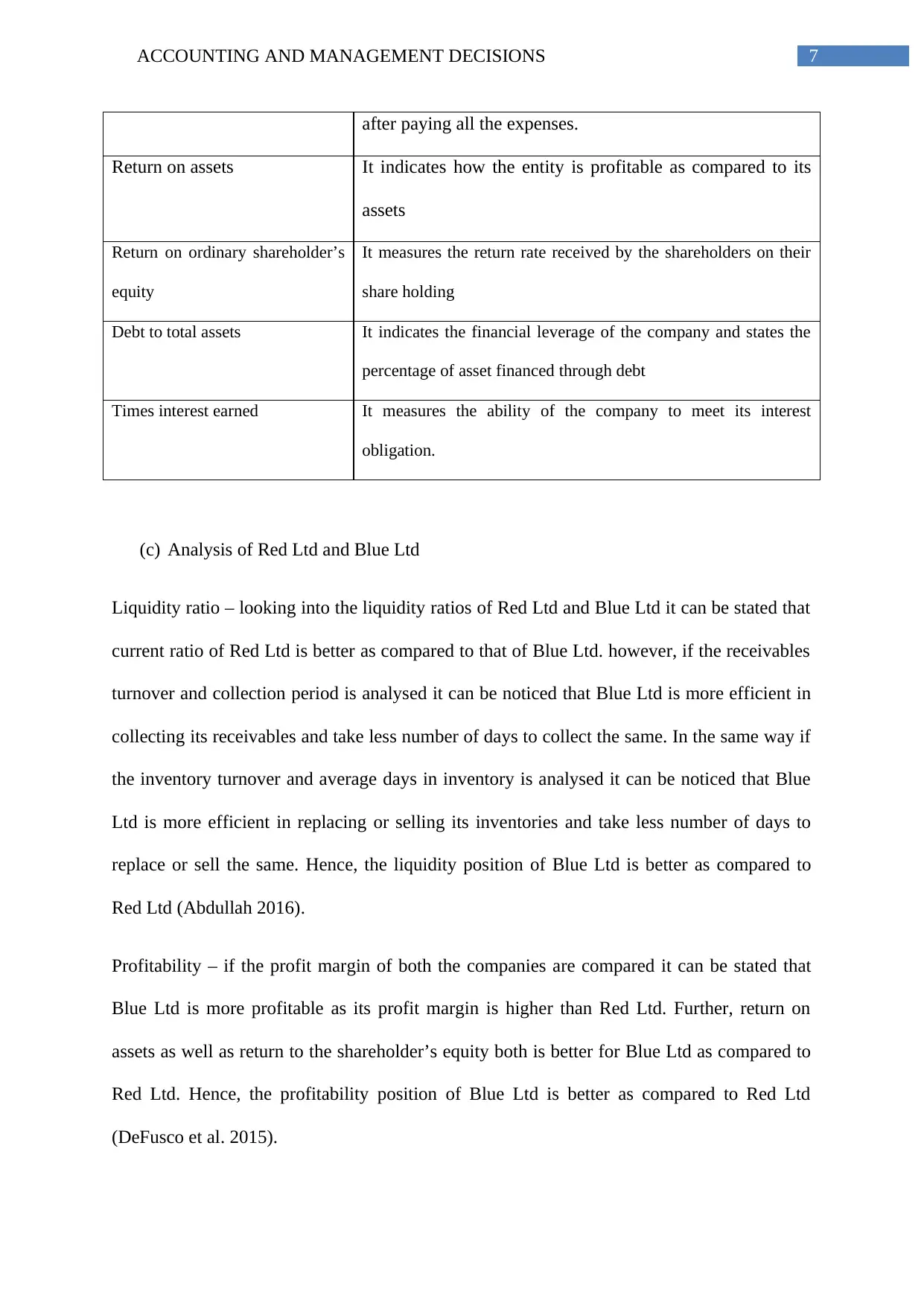

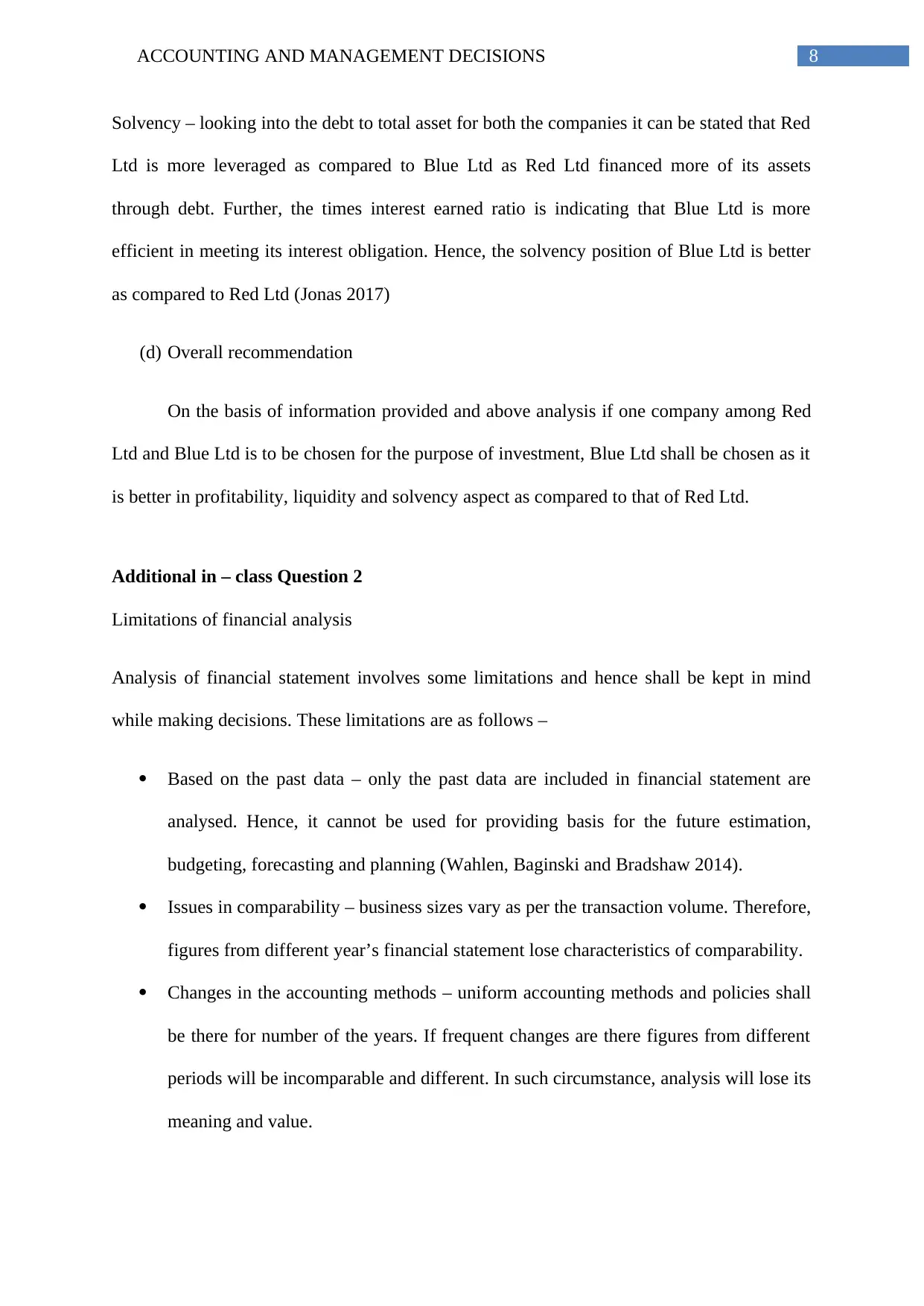

This assignment solution focuses on accounting and management decisions, providing a detailed analysis of financial statements. It includes horizontal and vertical analysis of Forrester’s Ltd's financial position, explaining changes in assets, liabilities, and equity. The solution also covers ratio analysis, classifying and interpreting various ratios like current ratio, receivable turnover, profit margin, and debt to total assets for Red Ltd and Blue Ltd, comparing their liquidity, profitability, and solvency. Furthermore, the assignment explores the usefulness of horizontal analysis in investment-related decisions and discusses the limitations of financial statement analysis, such as reliance on past data, comparability issues, and changes in accounting methods. The document concludes with a recommendation on which company to invest in based on the analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.