Comprehensive Financial Statement Analysis: Maine's 2018 Report

VerifiedAdded on 2023/01/17

|9

|1932

|57

Report

AI Summary

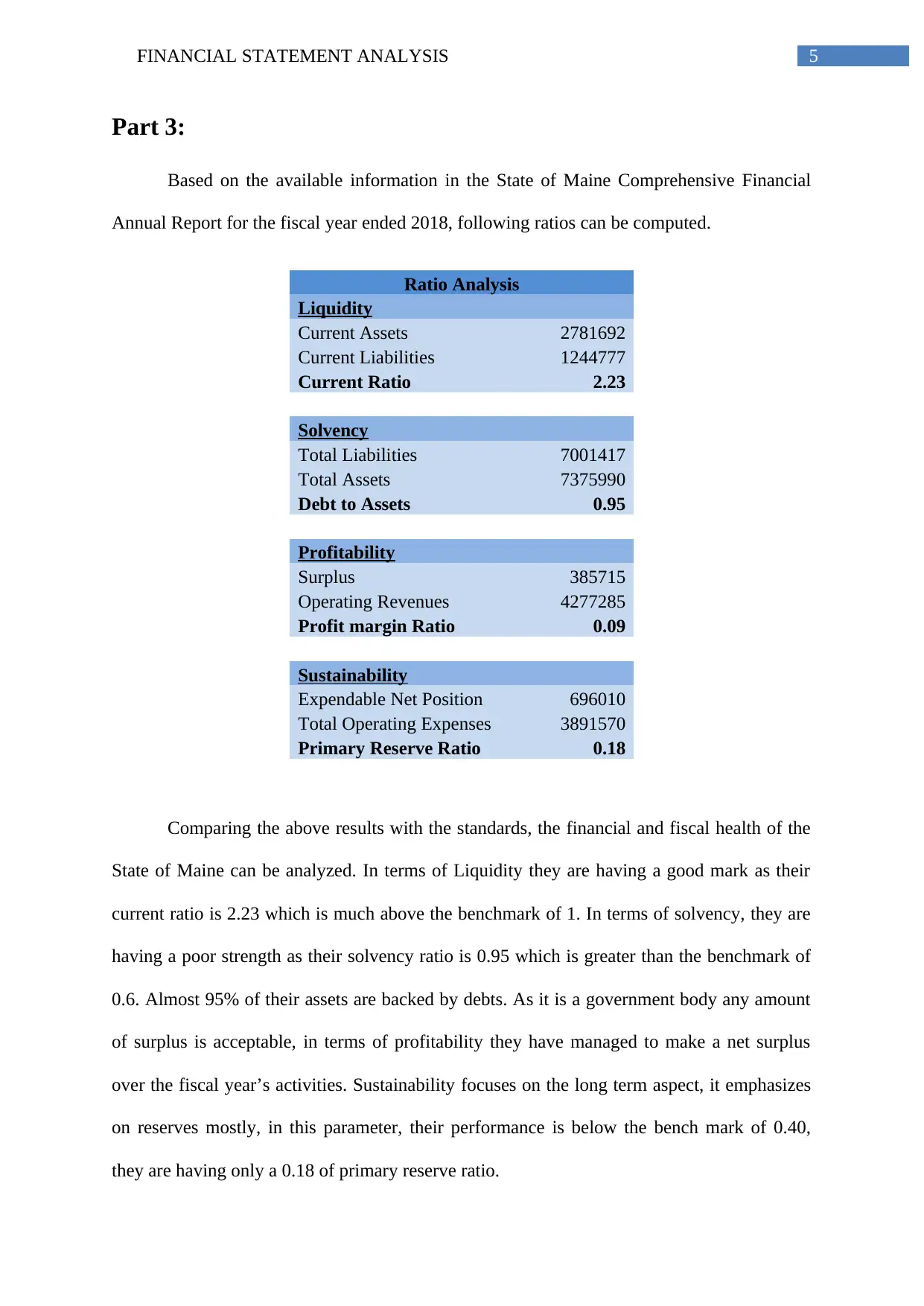

This report conducts a detailed financial statement analysis of the State of Maine's Comprehensive Annual Report for the fiscal year 2018. It begins with an executive summary and then examines the auditor's opinion, accounting treatments, and management's discussion. The report delves into the notes to the financial statements, highlighting key accounting principles and policies, and provides a ratio analysis to assess the state's liquidity, solvency, profitability, and sustainability. The analysis compares these ratios to benchmarks to gauge the state's fiscal health. Furthermore, the report explores the management's discussion section, outlining the state's financial performance across governmental and business-type activities. The report concludes with a reflective overview of the financial statement analysis process, emphasizing the importance of financial statements in expressing an organization's fiscal position and performance, particularly in the context of governmental entities.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.