Financial Statement Analysis Report: Nick Scali Limited (Finance)

VerifiedAdded on 2022/09/10

|10

|2050

|21

Report

AI Summary

This report provides a financial statement analysis of Nick Scali Limited, focusing on the company's accounting practices and their impact on financial performance. The analysis, based on the 2018 and 2019 annual reports, examines key accounting policies, including those related to revenue recognition, inventories, depreciation, and lease accounting. The report evaluates the accounting flexibility and strategy employed by the company, assessing the quality of disclosures and identifying potential earning management techniques. The analysis also considers potential red flags, such as credit and liquidity risks, and evaluates the impact of accounting distortions on reported profits. The report concludes with an overview of the company's financial health and the effectiveness of its accounting policies in reflecting the underlying business reality. The report also includes a table that explains the accounting techniques used by the company.

Running Head: FINANCIAL STATEMENT ANALYSIS

FINANCIAL STATEMENT ANALYSIS

Name of the Student

Name of the University

Author Note

FINANCIAL STATEMENT ANALYSIS

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STATEMENT ANALYSIS

Executive Summary

The main purpose of this research is to do an analysis on the accounting system adopted by

Nick Scali Limited. The study is supported by doing an analysis of the company's annual

reports for the financial year 2018 and 2019. It has been found that the accounting technique

used by the company, has helped them to sustain as a good financial performer in the market.

Executive Summary

The main purpose of this research is to do an analysis on the accounting system adopted by

Nick Scali Limited. The study is supported by doing an analysis of the company's annual

reports for the financial year 2018 and 2019. It has been found that the accounting technique

used by the company, has helped them to sustain as a good financial performer in the market.

2FINANCIAL STATEMENT ANALYSIS

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Accounting Analysis..............................................................................................................3

Step-1 Accounting Policies adopted by Nick Scali Limited..................................................3

Step 2: Accounting Flexibility...............................................................................................4

Step 3: Accounting Strategy...................................................................................................5

Step 4: Disclosure Quality.....................................................................................................5

Step 5: Earning Management of the Company......................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Accounting Analysis..............................................................................................................3

Step-1 Accounting Policies adopted by Nick Scali Limited..................................................3

Step 2: Accounting Flexibility...............................................................................................4

Step 3: Accounting Strategy...................................................................................................5

Step 4: Disclosure Quality.....................................................................................................5

Step 5: Earning Management of the Company......................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL STATEMENT ANALYSIS

Introduction

Nick Scali Limited is a leading importer of furniture across New Zealand, Hamilton

and Australia. The company has gained a substantial growth of sales in the FY 2019. The first

part of this paper has discussed on the accounting policies adopted by Nick Scali Ltd. The

next part is on the accounting policies and strategy implemented by the organisation. The last

part is an emphasis on the earning management technique implemented by the management.

The intense of this paper is to do an accounting analysis of Nick Scali Limited.

Discussions

Accounting Analysis

Accounting analysis is the process that is carried out by the professionals of a

company in order to facilitate subsequent decision-making. Accounting analysis is done to

maintain the profitability & liquidity position of a business in order to sustain itself in the

long run. The professionals include management, auditors & financial managers of the

company. They estimate the future financial performance of a company by improving the

quality of the financial reports.

Step-1 Accounting Policies adopted by Nick Scali Limited

Nick Scali Limited is an importer of furniture, having nearly 30 stores at June 2018

and added five more stores in Australia. Income from the contacts with the customers is the

main revenue for the company (Openbriefing.com.au, 2019). The inventories are valued

according to the net realisable value and weighted average cost method. Net realisable value

is calculated by estimating the selling price of the business, less the cost estimated to make

the sale. Sales margin are used for identifying the historical measure of the inventories.

Depreciation is charged for proper, plant and equipment. The land is not depreciated. It is

Introduction

Nick Scali Limited is a leading importer of furniture across New Zealand, Hamilton

and Australia. The company has gained a substantial growth of sales in the FY 2019. The first

part of this paper has discussed on the accounting policies adopted by Nick Scali Ltd. The

next part is on the accounting policies and strategy implemented by the organisation. The last

part is an emphasis on the earning management technique implemented by the management.

The intense of this paper is to do an accounting analysis of Nick Scali Limited.

Discussions

Accounting Analysis

Accounting analysis is the process that is carried out by the professionals of a

company in order to facilitate subsequent decision-making. Accounting analysis is done to

maintain the profitability & liquidity position of a business in order to sustain itself in the

long run. The professionals include management, auditors & financial managers of the

company. They estimate the future financial performance of a company by improving the

quality of the financial reports.

Step-1 Accounting Policies adopted by Nick Scali Limited

Nick Scali Limited is an importer of furniture, having nearly 30 stores at June 2018

and added five more stores in Australia. Income from the contacts with the customers is the

main revenue for the company (Openbriefing.com.au, 2019). The inventories are valued

according to the net realisable value and weighted average cost method. Net realisable value

is calculated by estimating the selling price of the business, less the cost estimated to make

the sale. Sales margin are used for identifying the historical measure of the inventories.

Depreciation is charged for proper, plant and equipment. The land is not depreciated. It is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STATEMENT ANALYSIS

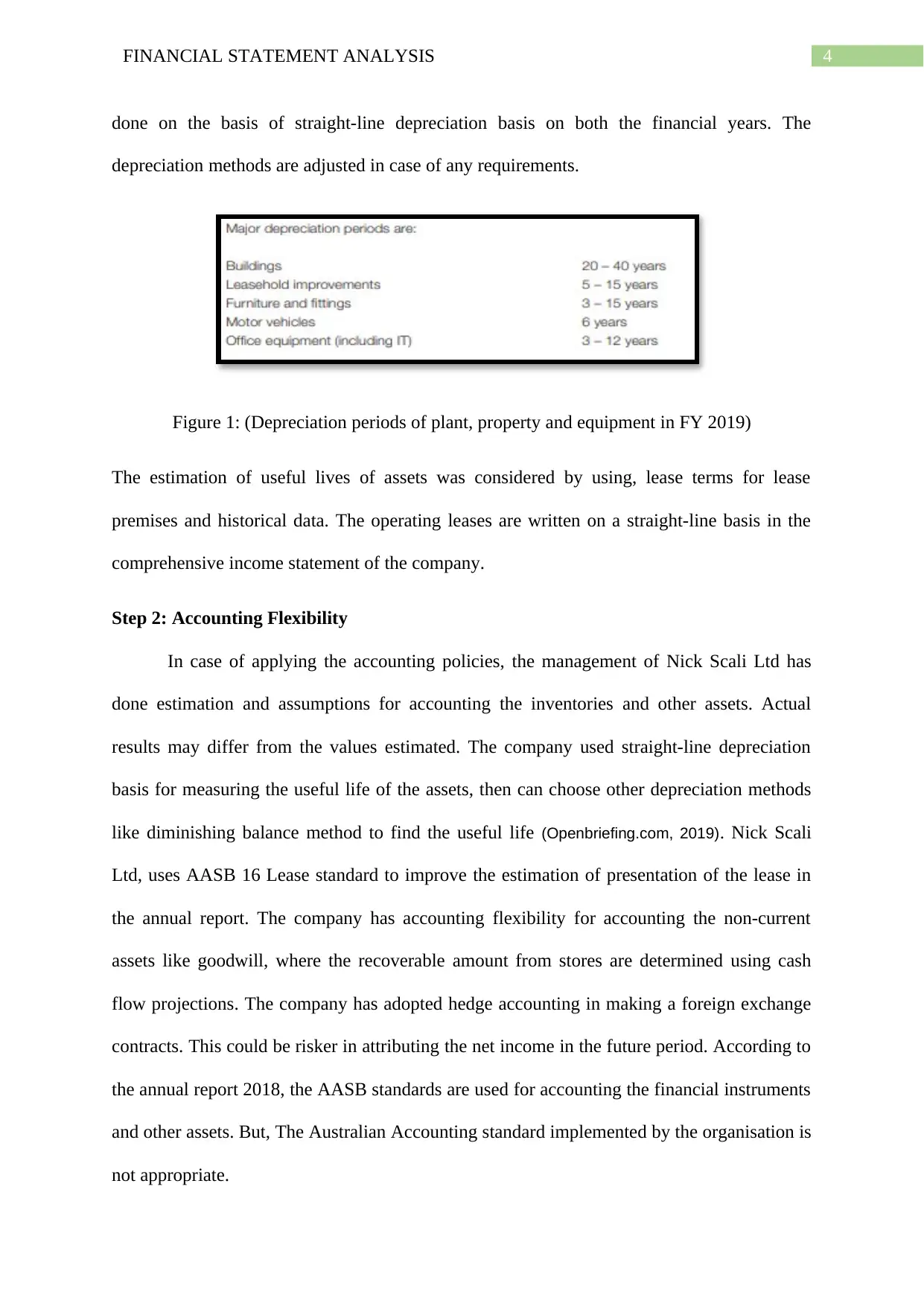

done on the basis of straight-line depreciation basis on both the financial years. The

depreciation methods are adjusted in case of any requirements.

Figure 1: (Depreciation periods of plant, property and equipment in FY 2019)

The estimation of useful lives of assets was considered by using, lease terms for lease

premises and historical data. The operating leases are written on a straight-line basis in the

comprehensive income statement of the company.

Step 2: Accounting Flexibility

In case of applying the accounting policies, the management of Nick Scali Ltd has

done estimation and assumptions for accounting the inventories and other assets. Actual

results may differ from the values estimated. The company used straight-line depreciation

basis for measuring the useful life of the assets, then can choose other depreciation methods

like diminishing balance method to find the useful life (Openbriefing.com, 2019). Nick Scali

Ltd, uses AASB 16 Lease standard to improve the estimation of presentation of the lease in

the annual report. The company has accounting flexibility for accounting the non-current

assets like goodwill, where the recoverable amount from stores are determined using cash

flow projections. The company has adopted hedge accounting in making a foreign exchange

contracts. This could be risker in attributing the net income in the future period. According to

the annual report 2018, the AASB standards are used for accounting the financial instruments

and other assets. But, The Australian Accounting standard implemented by the organisation is

not appropriate.

done on the basis of straight-line depreciation basis on both the financial years. The

depreciation methods are adjusted in case of any requirements.

Figure 1: (Depreciation periods of plant, property and equipment in FY 2019)

The estimation of useful lives of assets was considered by using, lease terms for lease

premises and historical data. The operating leases are written on a straight-line basis in the

comprehensive income statement of the company.

Step 2: Accounting Flexibility

In case of applying the accounting policies, the management of Nick Scali Ltd has

done estimation and assumptions for accounting the inventories and other assets. Actual

results may differ from the values estimated. The company used straight-line depreciation

basis for measuring the useful life of the assets, then can choose other depreciation methods

like diminishing balance method to find the useful life (Openbriefing.com, 2019). Nick Scali

Ltd, uses AASB 16 Lease standard to improve the estimation of presentation of the lease in

the annual report. The company has accounting flexibility for accounting the non-current

assets like goodwill, where the recoverable amount from stores are determined using cash

flow projections. The company has adopted hedge accounting in making a foreign exchange

contracts. This could be risker in attributing the net income in the future period. According to

the annual report 2018, the AASB standards are used for accounting the financial instruments

and other assets. But, The Australian Accounting standard implemented by the organisation is

not appropriate.

5FINANCIAL STATEMENT ANALYSIS

Step 3: Evaluating the Accounting Strategy

The organisation is compiled with Australian Accounting Standard and Corporation

Act 2001 to improve the standard of the annual report for better decision-making. But, the

company has done adjustments in preparing the financial statement. The company used

weighted average method for valuation of inventories. This method is easy and better for

asset valuation (Hsieh and Novoselov 2018). The value of financial instrument is the fair

value that is calculated according to the accounting standard, whereas, the values of other

particulars are just on the basis of assumptions from the historical data. The straight-line

method used for calculating the depreciation is a simpler way to find the useful life value of

the assets. But, the some of the equipments like office equipments, fittings and lease

improvements cannot be performed with the same amount. This accounting strategy may not

provide an appropriate figure of depreciation. Qantas Ltd also calculates its depreciation

value on a straight-line method for property, plants and equipments. The depreciation value

are on the basis of estimation of residual value of the assets. Accounting strategy of using

AASB 16 will be replaced with AASB 117 for recognition of lease requirements, where the

lease expenses will be recognised as expense on the basis of the straight-line method.

Step 4: Quality of Disclosure

The Annual report of Nick Scali Ltd of both the financial years has shown; the

auditor’s independence report, various financial statements, director’s report, shareholders

information and corporate information. But, the corporate governance statement is not

presented by the management (Fisman, Schulz and Vig 2016). The directors have not

disclosed the premium paid to the directors and other officers during the contract. The report

has clearly mentioned about the total number of employees working in the organisation. Total

employees in 2019 is 515 and in 2018 were 468 in numbers. Statutory remuneration report is

not disclosed. According to the FY 2019 report, the sales of goods were increased by 6.9%

Step 3: Evaluating the Accounting Strategy

The organisation is compiled with Australian Accounting Standard and Corporation

Act 2001 to improve the standard of the annual report for better decision-making. But, the

company has done adjustments in preparing the financial statement. The company used

weighted average method for valuation of inventories. This method is easy and better for

asset valuation (Hsieh and Novoselov 2018). The value of financial instrument is the fair

value that is calculated according to the accounting standard, whereas, the values of other

particulars are just on the basis of assumptions from the historical data. The straight-line

method used for calculating the depreciation is a simpler way to find the useful life value of

the assets. But, the some of the equipments like office equipments, fittings and lease

improvements cannot be performed with the same amount. This accounting strategy may not

provide an appropriate figure of depreciation. Qantas Ltd also calculates its depreciation

value on a straight-line method for property, plants and equipments. The depreciation value

are on the basis of estimation of residual value of the assets. Accounting strategy of using

AASB 16 will be replaced with AASB 117 for recognition of lease requirements, where the

lease expenses will be recognised as expense on the basis of the straight-line method.

Step 4: Quality of Disclosure

The Annual report of Nick Scali Ltd of both the financial years has shown; the

auditor’s independence report, various financial statements, director’s report, shareholders

information and corporate information. But, the corporate governance statement is not

presented by the management (Fisman, Schulz and Vig 2016). The directors have not

disclosed the premium paid to the directors and other officers during the contract. The report

has clearly mentioned about the total number of employees working in the organisation. Total

employees in 2019 is 515 and in 2018 were 468 in numbers. Statutory remuneration report is

not disclosed. According to the FY 2019 report, the sales of goods were increased by 6.9%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL STATEMENT ANALYSIS

from $250.8 to $268.0, but the net profit after tax did not show a larger variation. It only

increased by 1% in the current year. The information from the historical data does not show a

correct measurement of the figure. Therefore, the financial performance from the historical

data does not provide a clear review of the data. The company mainly focuses on the

underlying profit for making a fair presented in the annual report.

Step 5: Potential Red Flags

The management of the company has been using this accounting policy since past

years. In the annual report, the maximum credit risk of the company includes the receivables,

cash & cash equivalents. It was also found that, the company will not able to meet the

liquidity risks due to insufficient fund. The annual report is audited by a qualified auditor,

therefore, they have successfully audited the report in a qualified way. They have

successfully implemented the earning management techniques to hide the changes in

accounting system. There is unexpected write-offs in depreciation amount, sale expenses,

inventory expenses, administration expenses and other market expenses. The accumulated

depreciation value of the asset is adjusted and is normally written off as the depreciation

expense for property, plants and equipment. The greater value of depreciation expense was

shown in the current year as compared to the previous year 2018. Even the estimation of the

useful life of some assets is shorter than the actual physical life of assets (Swlearning.com,

2019). Hence, the management is engaged with large earning management technique to show

a good appearance of company’s financial statement. There is a large increase in gap of

taxable income in the income statement of FY 2018 and 2019. This could cause a problem for

the company. (Sajjad et al. 2019). There is a weak audit committee in the organisation. There

are total four audit committee in the organisation.

But, the management is implementing the earning management technique from past

years. The company has maintained a substantial growth in sales revenue from the past years.

from $250.8 to $268.0, but the net profit after tax did not show a larger variation. It only

increased by 1% in the current year. The information from the historical data does not show a

correct measurement of the figure. Therefore, the financial performance from the historical

data does not provide a clear review of the data. The company mainly focuses on the

underlying profit for making a fair presented in the annual report.

Step 5: Potential Red Flags

The management of the company has been using this accounting policy since past

years. In the annual report, the maximum credit risk of the company includes the receivables,

cash & cash equivalents. It was also found that, the company will not able to meet the

liquidity risks due to insufficient fund. The annual report is audited by a qualified auditor,

therefore, they have successfully audited the report in a qualified way. They have

successfully implemented the earning management techniques to hide the changes in

accounting system. There is unexpected write-offs in depreciation amount, sale expenses,

inventory expenses, administration expenses and other market expenses. The accumulated

depreciation value of the asset is adjusted and is normally written off as the depreciation

expense for property, plants and equipment. The greater value of depreciation expense was

shown in the current year as compared to the previous year 2018. Even the estimation of the

useful life of some assets is shorter than the actual physical life of assets (Swlearning.com,

2019). Hence, the management is engaged with large earning management technique to show

a good appearance of company’s financial statement. There is a large increase in gap of

taxable income in the income statement of FY 2018 and 2019. This could cause a problem for

the company. (Sajjad et al. 2019). There is a weak audit committee in the organisation. There

are total four audit committee in the organisation.

But, the management is implementing the earning management technique from past

years. The company has maintained a substantial growth in sales revenue from the past years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENT ANALYSIS

The firm is well placed to grow its capital and take advantages from the investment

opportunities. Therefore, this method has not been a threat for the company. Hence, no such

major adjustments are required in this case.

Step 6: undo Accounting Distortions

Items Over five years Accounting flexibility Adjustments

Inventory Valued on weighted

average cost method

and net realisable

value.

Regulation

AASB 102 inventories, section 334 of

corporation act (Aasb.gov.au, 2018)

Net realisable value is done by

estimation of the selling price, and the

weighted average cost formula is used

for valuation of inventories. No

adjustments are required. Overstating

of inventories is not done.

Depreciation The useful life of the

assets are recognised

using the straight-line

method

Regulation

Australian Accounting standard AAS

4 ‘depreciation” section 5.5.11

(Aasb.gov.au, 2019).

Recognition of the depreciable

amount can be done by the straight-

line method.

Adjustments can be done by using

reducing-balance method for

increasing the expected yield from

certain equipment.

In-tangible

assets

The recoverable

amount of goodwill

is determined on the

basis of cash flow

projections

Regulation

According to the AASB 1338

Intangibles, the carrying amount will

be recognised by using the cost model.

(Cpaaustralia.com.au, 2019)

No adjustment is required. No impact

on the income

Table 2: (Explanation of accounting techniques used by this company)

Conclusion

Therefore, it can be deferred from the annual report of Nick Scali, that the company

has acquired a reasonable increase in the sale revenue over the past five years. In the current

The firm is well placed to grow its capital and take advantages from the investment

opportunities. Therefore, this method has not been a threat for the company. Hence, no such

major adjustments are required in this case.

Step 6: undo Accounting Distortions

Items Over five years Accounting flexibility Adjustments

Inventory Valued on weighted

average cost method

and net realisable

value.

Regulation

AASB 102 inventories, section 334 of

corporation act (Aasb.gov.au, 2018)

Net realisable value is done by

estimation of the selling price, and the

weighted average cost formula is used

for valuation of inventories. No

adjustments are required. Overstating

of inventories is not done.

Depreciation The useful life of the

assets are recognised

using the straight-line

method

Regulation

Australian Accounting standard AAS

4 ‘depreciation” section 5.5.11

(Aasb.gov.au, 2019).

Recognition of the depreciable

amount can be done by the straight-

line method.

Adjustments can be done by using

reducing-balance method for

increasing the expected yield from

certain equipment.

In-tangible

assets

The recoverable

amount of goodwill

is determined on the

basis of cash flow

projections

Regulation

According to the AASB 1338

Intangibles, the carrying amount will

be recognised by using the cost model.

(Cpaaustralia.com.au, 2019)

No adjustment is required. No impact

on the income

Table 2: (Explanation of accounting techniques used by this company)

Conclusion

Therefore, it can be deferred from the annual report of Nick Scali, that the company

has acquired a reasonable increase in the sale revenue over the past five years. In the current

8FINANCIAL STATEMENT ANALYSIS

year, the sales revenue was increased by 6.9%, which is quite for the company. The

accounting policy used by the management has helped the company to maintain a position in

the market. The current strategy has helped the business to sustain and face challenges in the

market. Earning management technique is implemented by the management for appearing a

good financial statement of the firm.

year, the sales revenue was increased by 6.9%, which is quite for the company. The

accounting policy used by the management has helped the company to maintain a position in

the market. The current strategy has helped the business to sustain and face challenges in the

market. Earning management technique is implemented by the management for appearing a

good financial statement of the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL STATEMENT ANALYSIS

References

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-15.pdf [Accessed 12 Dec. 2019].

Aasb.gov.au (2018). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-15.pdf [Accessed 12 Dec. 2018].

Cpaaustralia.com.au. (2019). [online] Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-

resources/public-sector/guide-to-valuation-and-depreciation [Accessed 12 Dec.

2019].

Fisman, R., Schulz, F. and Vig, V., 2016. Financial disclosure and political selection:

Evidence from India. Unpublished manuscript, Boston Univ.

Hsieh, C.C., Ma, Z. and Novoselov, K.E., 2018. Accounting conservatism, business strategy,

and ambiguity. Accounting, OrganisationsOrganisations and Society, 30, p.1e15.

Openbriefing.com.au (2019). [online] Openbriefing.com.au. Available at:

http://openbriefing.com.au/AsxDownload.aspx?pdfUrl=Report%2FComNews

%2F20180921%2F02024908.pdf [Accessed 12 Dec. 2019].

Sajjad, T., Abbas, N., Hussain, S. and Waheed, A., 2019. The impact of Corporate

Governance, Product Market Competition on Earning Management Practices. Journal of

Managerial Sciences, 13(2).

Swlearning.com (2019). [online] Swlearning.com. Available at:

http://www.swlearning.com/pdfs/chapter/0324223250_2.PDF [Accessed 12 Dec. 2019].

References

Aasb.gov.au (2019). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-15.pdf [Accessed 12 Dec. 2019].

Aasb.gov.au (2018). [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-15.pdf [Accessed 12 Dec. 2018].

Cpaaustralia.com.au. (2019). [online] Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-

resources/public-sector/guide-to-valuation-and-depreciation [Accessed 12 Dec.

2019].

Fisman, R., Schulz, F. and Vig, V., 2016. Financial disclosure and political selection:

Evidence from India. Unpublished manuscript, Boston Univ.

Hsieh, C.C., Ma, Z. and Novoselov, K.E., 2018. Accounting conservatism, business strategy,

and ambiguity. Accounting, OrganisationsOrganisations and Society, 30, p.1e15.

Openbriefing.com.au (2019). [online] Openbriefing.com.au. Available at:

http://openbriefing.com.au/AsxDownload.aspx?pdfUrl=Report%2FComNews

%2F20180921%2F02024908.pdf [Accessed 12 Dec. 2019].

Sajjad, T., Abbas, N., Hussain, S. and Waheed, A., 2019. The impact of Corporate

Governance, Product Market Competition on Earning Management Practices. Journal of

Managerial Sciences, 13(2).

Swlearning.com (2019). [online] Swlearning.com. Available at:

http://www.swlearning.com/pdfs/chapter/0324223250_2.PDF [Accessed 12 Dec. 2019].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.