ACC306 Report: Investment Analysis of Qantas Airways Financials

VerifiedAdded on 2023/06/07

|20

|4490

|470

Report

AI Summary

This report provides a comprehensive financial analysis of Qantas Airways, focusing on its long-term solvency and liquidity over the past three years. It assesses various financial ratios, including solvency ratios (debt to equity, total debt to total assets, interest coverage ratio, and return on financial leverage) and liquidity ratios (current ratio, quick ratio, working capital, operating cash flow with current liabilities and capital expenditures, and free cash flow). The analysis indicates that while Qantas Airways has performed satisfactorily, there are areas of concern, such as decreasing return on equity and increasing debt to equity ratio in 2017. The report also discusses the qualitative aspects of the company's financial statements, providing insights into its overall financial health. Desklib provides similar past papers and solved assignments for students.

Running Head: FINANCE 0

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 1

Table of Contents

Introduction................................................................................................................................2

Financial Performance Analysis................................................................................................4

Solvency and Liquidity...........................................................................................................5

Solvency ratios.......................................................................................................................5

Debt to equity......................................................................................................................6

Total debt to Total assets....................................................................................................7

Interest coverage Ratio.......................................................................................................8

Return on Financial leverage..............................................................................................9

Liquidity ratios.....................................................................................................................10

Current Ratio.....................................................................................................................11

Quick Ratio.......................................................................................................................11

Working capital.................................................................................................................13

Operating cash flow with the current liabilities................................................................14

Operating cash flow with the capital expenditures...........................................................14

Free cash flow...................................................................................................................14

Quality of the financial statements...........................................................................................15

References................................................................................................................................17

Table of Contents

Introduction................................................................................................................................2

Financial Performance Analysis................................................................................................4

Solvency and Liquidity...........................................................................................................5

Solvency ratios.......................................................................................................................5

Debt to equity......................................................................................................................6

Total debt to Total assets....................................................................................................7

Interest coverage Ratio.......................................................................................................8

Return on Financial leverage..............................................................................................9

Liquidity ratios.....................................................................................................................10

Current Ratio.....................................................................................................................11

Quick Ratio.......................................................................................................................11

Working capital.................................................................................................................13

Operating cash flow with the current liabilities................................................................14

Operating cash flow with the capital expenditures...........................................................14

Free cash flow...................................................................................................................14

Quality of the financial statements...........................................................................................15

References................................................................................................................................17

FINANCE 2

Introduction

Qantas is the one of the famous Airline service industry in the Australia. It is one of the

largest airlines in the Australia and the Qantas Airways is the largest company by the fleet

size, flights and the destinations it operates at. The Qantas Airways is the old brand and the

airline and the third largest among the other airlines in the world. The major competitors of

the Qantas are KLMM and Avianca. The total operating income of the company is A$1.59

billion and the revenue of the company is A$16.1 billion in the financial year 2017 (Qantas,

2018). This report performs the analysis of the long term solvency of the company over the

last three years and also assesses the liquidity position of the company as at the latest

financial year. Apart from this the qualitative nature of the company is also discussed in

detail.

Year End (3 years)

Ratios and Other Analysis Measures 2015 2016 2017

ROE and DuPont Ratios

ROE (NI / OEavg) 31.6% 24.1% 24.8%

ROA 6.2% 5.0% 6.2%

Profitability (NI / Sales ) 6.5% 5.4% 5.9%

Efficiency (Turnover = Sales / Assets avg) 1.20 1.15 2.24

Leverage (Leverage = Assets avg / OEavg) 0.44 0.43 0.46

Additional Profitability Ratios

Gross Profit Margin % [(net Rev - COGS) / net Revenue] 58% 59% 59%

Selling General andAdministration % (SGandA expense / net

Revenue)

34% 34% 33%

Introduction

Qantas is the one of the famous Airline service industry in the Australia. It is one of the

largest airlines in the Australia and the Qantas Airways is the largest company by the fleet

size, flights and the destinations it operates at. The Qantas Airways is the old brand and the

airline and the third largest among the other airlines in the world. The major competitors of

the Qantas are KLMM and Avianca. The total operating income of the company is A$1.59

billion and the revenue of the company is A$16.1 billion in the financial year 2017 (Qantas,

2018). This report performs the analysis of the long term solvency of the company over the

last three years and also assesses the liquidity position of the company as at the latest

financial year. Apart from this the qualitative nature of the company is also discussed in

detail.

Year End (3 years)

Ratios and Other Analysis Measures 2015 2016 2017

ROE and DuPont Ratios

ROE (NI / OEavg) 31.6% 24.1% 24.8%

ROA 6.2% 5.0% 6.2%

Profitability (NI / Sales ) 6.5% 5.4% 5.9%

Efficiency (Turnover = Sales / Assets avg) 1.20 1.15 2.24

Leverage (Leverage = Assets avg / OEavg) 0.44 0.43 0.46

Additional Profitability Ratios

Gross Profit Margin % [(net Rev - COGS) / net Revenue] 58% 59% 59%

Selling General andAdministration % (SGandA expense / net

Revenue)

34% 34% 33%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 3

Important Expense Percentage* (Important Expense / net

Revenue)

8% 9% 9%

Additional Efficiency Ratios

AR Turnover (Sales / ARavg) 11.49 11.17 23.69

Days Receivables Outstanding (DRO) [ARavg / (Sales /365)] 18.26 19.69 9.97

Inventory Turnover (COGS / Inventoryavg) 4.81 4.61 9.73

Days Inventory (DI) [Inventoryavg / (COGS/365)] 18.55 19.79 18.76

AP Turnover (Purchases / APavg) 0.82 0.74 1.49

Days Payables Outstanding (DPO) [365 / (Purchases / Accts

Payableavg)]

447.4

7

491.7

8

245.3

6

CASH CONVERSION CYCLE (DI - DPO + DRO)

-

410.6

7

-

452.3

0

-

216.6

4

PPE Turnover (Sales / Net PPEavg) 0.16 0.20 0.65

Additional Leverage Ratios

Debt-to-Equity (total Liabilities / total OE) 0.94 0.89 1.10

Times Interest Earned (Earnings before Interest Expense and

Taxes / Interest Exp)

5.01 5.03 6.05

Return on Financial Leverage (ROE - ROA) 25.5% 19.2% 18.5%

LT Debt-to-Assets (LT Debt, including current portion / total

Assets )

0.60 0.59 0.76

Cash Liquidity and Cash Sources and Uses

Working Capital (CA - CL) - - -

Important Expense Percentage* (Important Expense / net

Revenue)

8% 9% 9%

Additional Efficiency Ratios

AR Turnover (Sales / ARavg) 11.49 11.17 23.69

Days Receivables Outstanding (DRO) [ARavg / (Sales /365)] 18.26 19.69 9.97

Inventory Turnover (COGS / Inventoryavg) 4.81 4.61 9.73

Days Inventory (DI) [Inventoryavg / (COGS/365)] 18.55 19.79 18.76

AP Turnover (Purchases / APavg) 0.82 0.74 1.49

Days Payables Outstanding (DPO) [365 / (Purchases / Accts

Payableavg)]

447.4

7

491.7

8

245.3

6

CASH CONVERSION CYCLE (DI - DPO + DRO)

-

410.6

7

-

452.3

0

-

216.6

4

PPE Turnover (Sales / Net PPEavg) 0.16 0.20 0.65

Additional Leverage Ratios

Debt-to-Equity (total Liabilities / total OE) 0.94 0.89 1.10

Times Interest Earned (Earnings before Interest Expense and

Taxes / Interest Exp)

5.01 5.03 6.05

Return on Financial Leverage (ROE - ROA) 25.5% 19.2% 18.5%

LT Debt-to-Assets (LT Debt, including current portion / total

Assets )

0.60 0.59 0.76

Cash Liquidity and Cash Sources and Uses

Working Capital (CA - CL) - - -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 4

35700

00

39760

00

38840

00

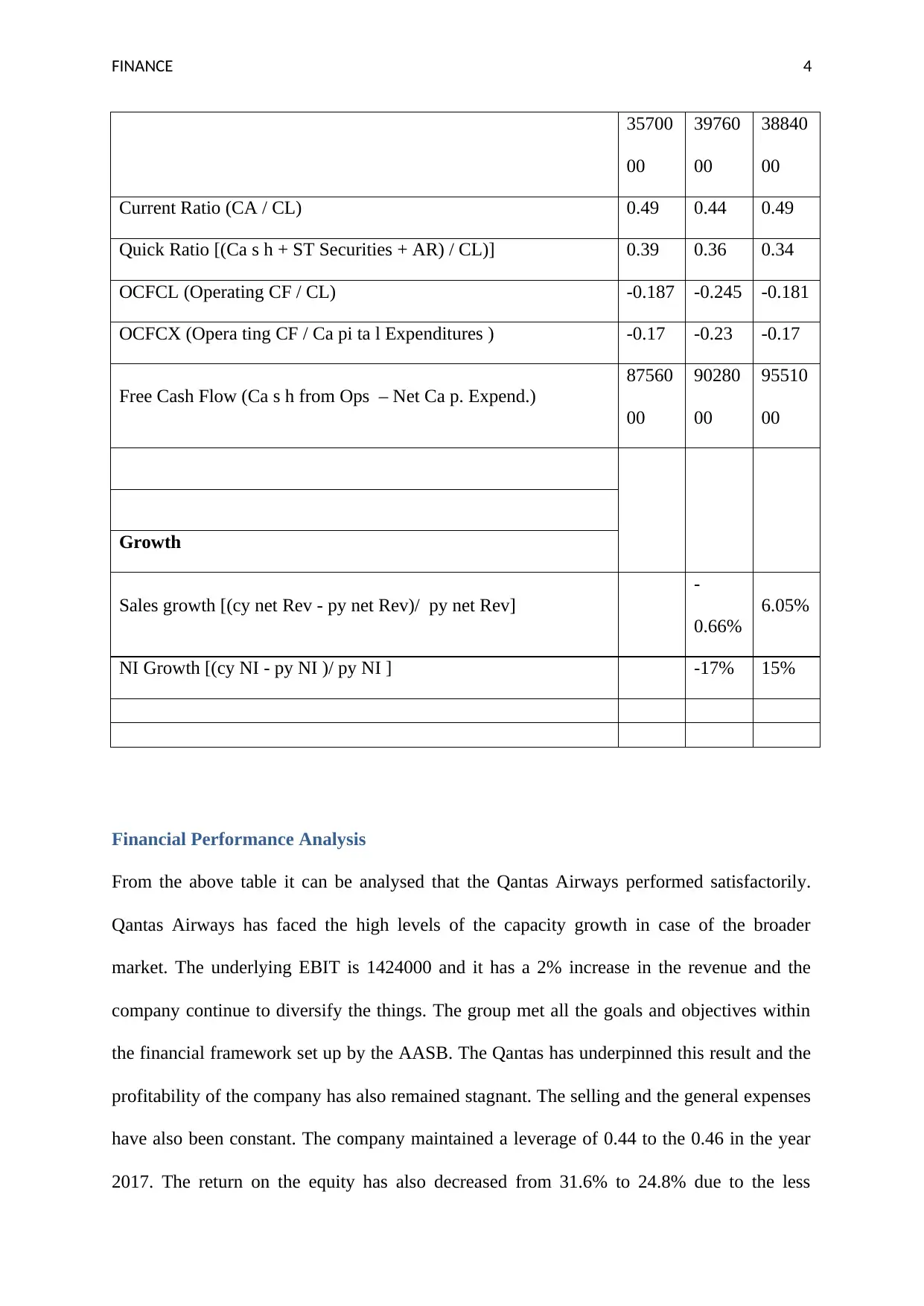

Current Ratio (CA / CL) 0.49 0.44 0.49

Quick Ratio [(Ca s h + ST Securities + AR) / CL)] 0.39 0.36 0.34

OCFCL (Operating CF / CL) -0.187 -0.245 -0.181

OCFCX (Opera ting CF / Ca pi ta l Expenditures ) -0.17 -0.23 -0.17

Free Cash Flow (Ca s h from Ops – Net Ca p. Expend.)

87560

00

90280

00

95510

00

Growth

Sales growth [(cy net Rev - py net Rev)/ py net Rev]

-

0.66%

6.05%

NI Growth [(cy NI - py NI )/ py NI ] -17% 15%

Financial Performance Analysis

From the above table it can be analysed that the Qantas Airways performed satisfactorily.

Qantas Airways has faced the high levels of the capacity growth in case of the broader

market. The underlying EBIT is 1424000 and it has a 2% increase in the revenue and the

company continue to diversify the things. The group met all the goals and objectives within

the financial framework set up by the AASB. The Qantas has underpinned this result and the

profitability of the company has also remained stagnant. The selling and the general expenses

have also been constant. The company maintained a leverage of 0.44 to the 0.46 in the year

2017. The return on the equity has also decreased from 31.6% to 24.8% due to the less

35700

00

39760

00

38840

00

Current Ratio (CA / CL) 0.49 0.44 0.49

Quick Ratio [(Ca s h + ST Securities + AR) / CL)] 0.39 0.36 0.34

OCFCL (Operating CF / CL) -0.187 -0.245 -0.181

OCFCX (Opera ting CF / Ca pi ta l Expenditures ) -0.17 -0.23 -0.17

Free Cash Flow (Ca s h from Ops – Net Ca p. Expend.)

87560

00

90280

00

95510

00

Growth

Sales growth [(cy net Rev - py net Rev)/ py net Rev]

-

0.66%

6.05%

NI Growth [(cy NI - py NI )/ py NI ] -17% 15%

Financial Performance Analysis

From the above table it can be analysed that the Qantas Airways performed satisfactorily.

Qantas Airways has faced the high levels of the capacity growth in case of the broader

market. The underlying EBIT is 1424000 and it has a 2% increase in the revenue and the

company continue to diversify the things. The group met all the goals and objectives within

the financial framework set up by the AASB. The Qantas has underpinned this result and the

profitability of the company has also remained stagnant. The selling and the general expenses

have also been constant. The company maintained a leverage of 0.44 to the 0.46 in the year

2017. The return on the equity has also decreased from 31.6% to 24.8% due to the less

FINANCE 5

number of the equity investors (News Corp Australia Network, 2017). The cash decreased by

286000 in the year 2017 in a period of last three years and therefore after the analysis of the

financial statements of the last three years.

Solvency and Liquidity

The long term solvency analysis includes the financial analysis of the Solvency and the

liquidity ratios. Solvency ratio is one of the key metrics that is used to analyse the ability of

the company, whether it can meet the obligations and pay off the current liabilities. The

solvency ratio basically determines the cash flow of the company and decodes whether the

current liabilities are payable or not (Venkatesh and Gugloth, 2017). The basic notation for

the company is that, the lower the solvency ratio of the company, the higher is risk of the

default on the debt obligations. The formula for calculating the ratio is

Solvency Ratio Net income (After tax) + Depreciation

Short term liabilities + Long term

liabilities

Solvency ratios

The solvency ratio is the comprehensive measure of the cash flow rather than its income by

including the depreciation to make the clear assessment of the capacity of the company.

There are different forms of the solvency ratio such as Debt to equity ratio, times earned

ratio, Return on financial leverage and long term debt to assets. The solvency ratio higher

than the 20% is an ideal ratio is considered as the benchmark (Zainudin, Zainudin, Hashim

and Hashim, 2016). This ratio is not assessed in the isolation; rather it is compared with the

other companies operating in the similar industry.

number of the equity investors (News Corp Australia Network, 2017). The cash decreased by

286000 in the year 2017 in a period of last three years and therefore after the analysis of the

financial statements of the last three years.

Solvency and Liquidity

The long term solvency analysis includes the financial analysis of the Solvency and the

liquidity ratios. Solvency ratio is one of the key metrics that is used to analyse the ability of

the company, whether it can meet the obligations and pay off the current liabilities. The

solvency ratio basically determines the cash flow of the company and decodes whether the

current liabilities are payable or not (Venkatesh and Gugloth, 2017). The basic notation for

the company is that, the lower the solvency ratio of the company, the higher is risk of the

default on the debt obligations. The formula for calculating the ratio is

Solvency Ratio Net income (After tax) + Depreciation

Short term liabilities + Long term

liabilities

Solvency ratios

The solvency ratio is the comprehensive measure of the cash flow rather than its income by

including the depreciation to make the clear assessment of the capacity of the company.

There are different forms of the solvency ratio such as Debt to equity ratio, times earned

ratio, Return on financial leverage and long term debt to assets. The solvency ratio higher

than the 20% is an ideal ratio is considered as the benchmark (Zainudin, Zainudin, Hashim

and Hashim, 2016). This ratio is not assessed in the isolation; rather it is compared with the

other companies operating in the similar industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 6

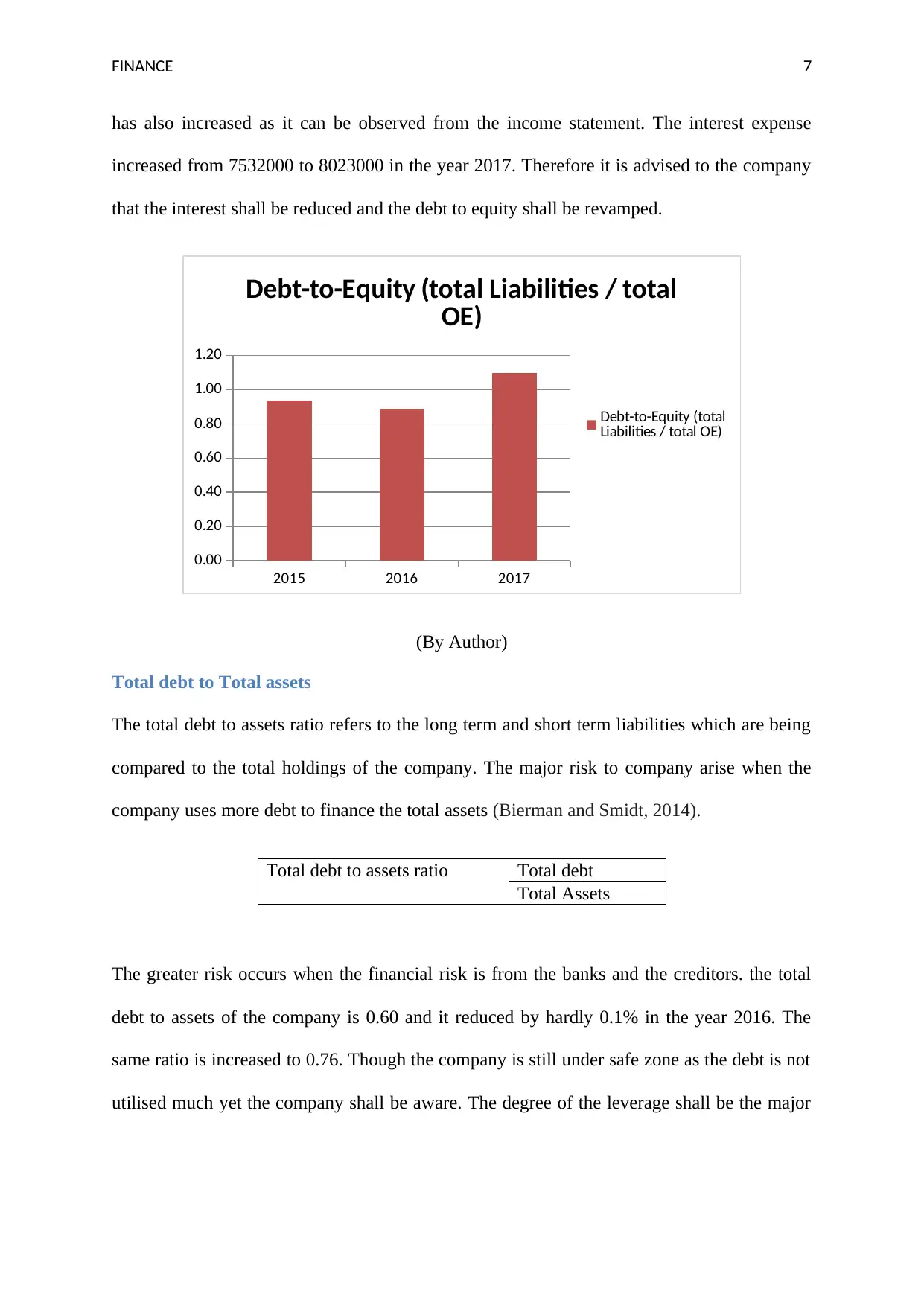

Debt-to-Equity (total Liabilities / total OE) 0.94 0.89 1.10

Times Interest Earned (Earnings before Interest Expense and

Taxes / Interest Exp)

5.01 5.03 6.05

Return on Financial Leverage (ROE - ROA)

25.5

%

19.2

%

18.5

%

LT Debt-to-Assets (LT Debt, including current portion / total

Assets )

0.60 0.59 0.76

Debt to equity

Debt to Equity ratio determines the total liabilities by the stakeholders. The Debt to Equity

ratio indicates how much debt the company is maintaining to finance the assets which are

relative to the value of the shareholder’s equity.

Debt to Equity Ratio Debt

Equity

If a lot of the debt option is used is to finance and increase the financial operations. The

major reason for the company is that it could generate more earnings as it would have done

without the help of the company to outsource the finance (Baker, Jabbouri and Dyaz, 2017).

If the earnings are increased by the greater amount than the shareholders will have the most

benefit, on the other hand if the cost of debt is more than the company may also lead to the

bankruptcy. The debt to equity ratio of the Qantas Airways is 0.94 in the year 2012 and it

decreased to the figure to the 0.89. The fall in the debt to equity ratio is that debt is less than

the equity. However, the company has again increased the ratio to 1.10 in the year 2017

(Australian Government, 2018). A high debt to equity ratio suggests that the company has

over utilized debt to support the growth of the company. The interest level of the company

Debt-to-Equity (total Liabilities / total OE) 0.94 0.89 1.10

Times Interest Earned (Earnings before Interest Expense and

Taxes / Interest Exp)

5.01 5.03 6.05

Return on Financial Leverage (ROE - ROA)

25.5

%

19.2

%

18.5

%

LT Debt-to-Assets (LT Debt, including current portion / total

Assets )

0.60 0.59 0.76

Debt to equity

Debt to Equity ratio determines the total liabilities by the stakeholders. The Debt to Equity

ratio indicates how much debt the company is maintaining to finance the assets which are

relative to the value of the shareholder’s equity.

Debt to Equity Ratio Debt

Equity

If a lot of the debt option is used is to finance and increase the financial operations. The

major reason for the company is that it could generate more earnings as it would have done

without the help of the company to outsource the finance (Baker, Jabbouri and Dyaz, 2017).

If the earnings are increased by the greater amount than the shareholders will have the most

benefit, on the other hand if the cost of debt is more than the company may also lead to the

bankruptcy. The debt to equity ratio of the Qantas Airways is 0.94 in the year 2012 and it

decreased to the figure to the 0.89. The fall in the debt to equity ratio is that debt is less than

the equity. However, the company has again increased the ratio to 1.10 in the year 2017

(Australian Government, 2018). A high debt to equity ratio suggests that the company has

over utilized debt to support the growth of the company. The interest level of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 7

has also increased as it can be observed from the income statement. The interest expense

increased from 7532000 to 8023000 in the year 2017. Therefore it is advised to the company

that the interest shall be reduced and the debt to equity shall be revamped.

2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Debt-to-Equity (total Liabilities / total

OE)

Debt-to-Equity (total

Liabilities / total OE)

(By Author)

Total debt to Total assets

The total debt to assets ratio refers to the long term and short term liabilities which are being

compared to the total holdings of the company. The major risk to company arise when the

company uses more debt to finance the total assets (Bierman and Smidt, 2014).

Total debt to assets ratio Total debt

Total Assets

The greater risk occurs when the financial risk is from the banks and the creditors. the total

debt to assets of the company is 0.60 and it reduced by hardly 0.1% in the year 2016. The

same ratio is increased to 0.76. Though the company is still under safe zone as the debt is not

utilised much yet the company shall be aware. The degree of the leverage shall be the major

has also increased as it can be observed from the income statement. The interest expense

increased from 7532000 to 8023000 in the year 2017. Therefore it is advised to the company

that the interest shall be reduced and the debt to equity shall be revamped.

2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Debt-to-Equity (total Liabilities / total

OE)

Debt-to-Equity (total

Liabilities / total OE)

(By Author)

Total debt to Total assets

The total debt to assets ratio refers to the long term and short term liabilities which are being

compared to the total holdings of the company. The major risk to company arise when the

company uses more debt to finance the total assets (Bierman and Smidt, 2014).

Total debt to assets ratio Total debt

Total Assets

The greater risk occurs when the financial risk is from the banks and the creditors. the total

debt to assets of the company is 0.60 and it reduced by hardly 0.1% in the year 2016. The

same ratio is increased to 0.76. Though the company is still under safe zone as the debt is not

utilised much yet the company shall be aware. The degree of the leverage shall be the major

FINANCE 8

concern for the Qantas Airways and therefore the value of the current assets shall be

increased (Gurufocus, 2018).

Interest coverage Ratio

The interest coverage ratio is the metric which keeps the record of the interest payments

which arise parallel with the outstanding debt. The business owner the Earnings before

interest and tax shall be divided by the interest expenses (Borgonovo, 2017).

Interest Coverage Ratio EBIT

Interest Expense

The interest coverage ratio is basically a source to the public which can be a clear indicator of

the fact that how much interest expenses the company is under the fact to pay to the debt

holders. After the payment of the interest and the taxes the final income is given to the

shareholders therefore, the company will be requiring to keep the interest income low so the

income can be distributed to the shareholders (Colloquy, 2015). The lower the interest

coverage ratio, the more its debt expense is going to affect the going concern of the company

and it will create a burden for the company. The company with the interest coverage ratio of

1.5 or less is considered to be unstable (Shapiro, 2008).

concern for the Qantas Airways and therefore the value of the current assets shall be

increased (Gurufocus, 2018).

Interest coverage Ratio

The interest coverage ratio is the metric which keeps the record of the interest payments

which arise parallel with the outstanding debt. The business owner the Earnings before

interest and tax shall be divided by the interest expenses (Borgonovo, 2017).

Interest Coverage Ratio EBIT

Interest Expense

The interest coverage ratio is basically a source to the public which can be a clear indicator of

the fact that how much interest expenses the company is under the fact to pay to the debt

holders. After the payment of the interest and the taxes the final income is given to the

shareholders therefore, the company will be requiring to keep the interest income low so the

income can be distributed to the shareholders (Colloquy, 2015). The lower the interest

coverage ratio, the more its debt expense is going to affect the going concern of the company

and it will create a burden for the company. The company with the interest coverage ratio of

1.5 or less is considered to be unstable (Shapiro, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

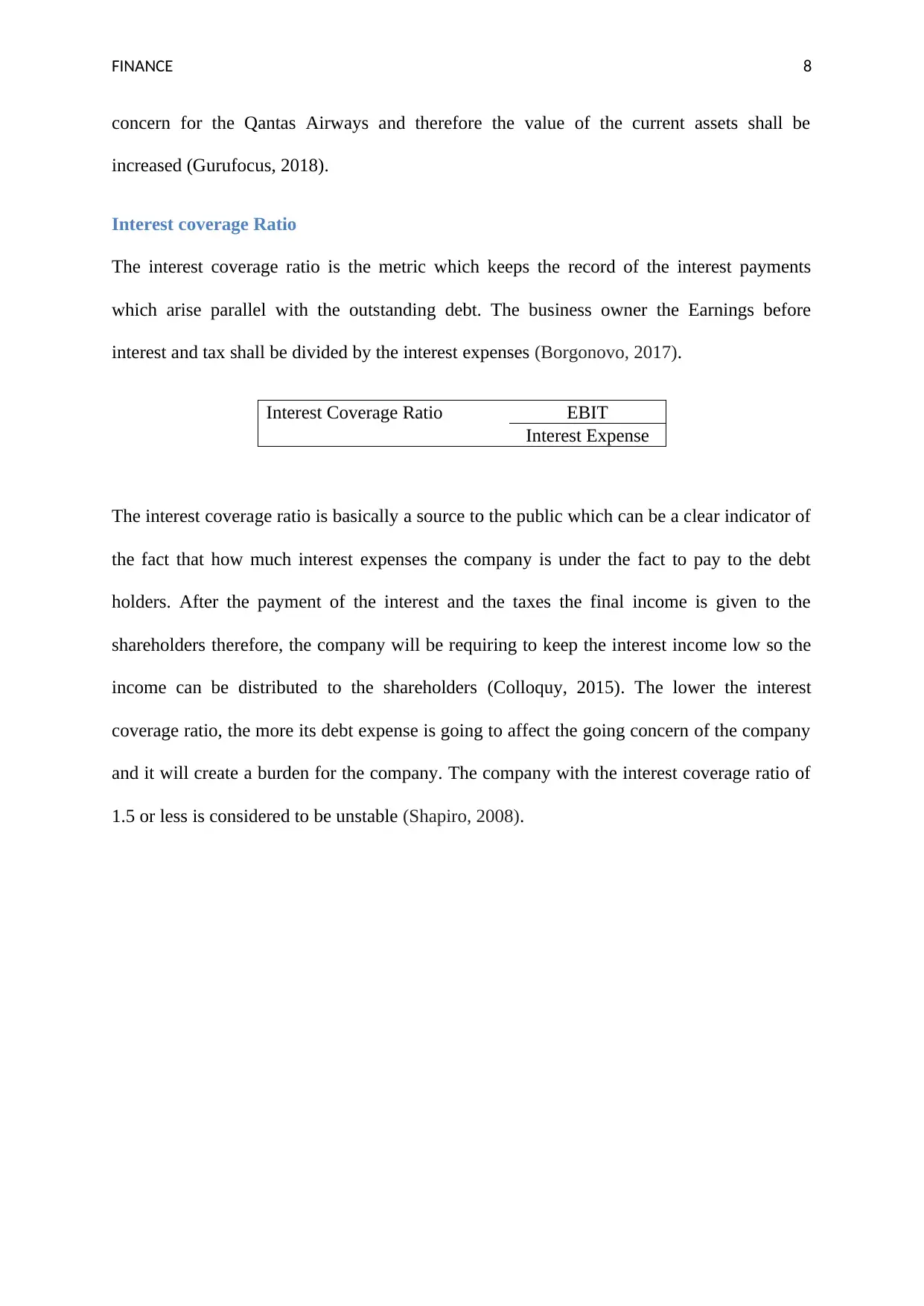

FINANCE 9

2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Times Interest Earned (Earnings

before Interest Expense and Taxes /

Interest Exp)

Times Interest Earned

(Earnings before Interest

Expense and Taxes /

Interest Exp)

(By Author)

From the above graph it can be analysed that the times interest ratio of the company is sound

and the company is performing better (Daunfeldt and Hartwig, 2014). The interest coverage

ratio of the company in the year 2015 was 5.01 and it increased to 5.03 and finally increased

to 6.05 in the year 2017. The interest coverage ratio can be improved if the interest expense

can be improved. Moreover the interest coverage ratio below 1 is considered as a highly

danger situation and in comparison to the benchmark the Qantas Airways performed

extremely well (Bragg, 2012).

Return on Financial leverage

When a business realises the financial leverage which means the Qantas Airways will be

earnings more profit. The Return on the financial leverage is the difference between the

return on equity and the return on assets (Gotze, Northcott and Schuster, 2016). The ROA is

the useful ratio and it is used in interpreting the profit. The return on financial leverage of the

company is 25.5% and it reduced to 18.5% in the year 2017. Every investor wants to get a

higher return on the investment and if the return on financial leverage is going to decrease

this will ultimately hamper the performance of the company and the count of the number of

2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Times Interest Earned (Earnings

before Interest Expense and Taxes /

Interest Exp)

Times Interest Earned

(Earnings before Interest

Expense and Taxes /

Interest Exp)

(By Author)

From the above graph it can be analysed that the times interest ratio of the company is sound

and the company is performing better (Daunfeldt and Hartwig, 2014). The interest coverage

ratio of the company in the year 2015 was 5.01 and it increased to 5.03 and finally increased

to 6.05 in the year 2017. The interest coverage ratio can be improved if the interest expense

can be improved. Moreover the interest coverage ratio below 1 is considered as a highly

danger situation and in comparison to the benchmark the Qantas Airways performed

extremely well (Bragg, 2012).

Return on Financial leverage

When a business realises the financial leverage which means the Qantas Airways will be

earnings more profit. The Return on the financial leverage is the difference between the

return on equity and the return on assets (Gotze, Northcott and Schuster, 2016). The ROA is

the useful ratio and it is used in interpreting the profit. The return on financial leverage of the

company is 25.5% and it reduced to 18.5% in the year 2017. Every investor wants to get a

higher return on the investment and if the return on financial leverage is going to decrease

this will ultimately hamper the performance of the company and the count of the number of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 10

the investors is low. Henceforth it is advised to the company that the return on financial

leverage shall be improved (Gibson, 2011).

Return on Financial Leverage ROE-ROA

Liquidity ratios

Liquidity ratios are another type of the financial ratios that are used by the investors and

determine the ability of the debtor to pay off the current debt of the company without taking

the assistance of the external capital. Liquidity ratios are basically the metrics that measures

the current ratio, quick ratio, operating cash flow (Godwin and Alderman, 2012). Current

liabilities are analysed in relation to the liquid assets to assess the time period of the short

term debts. The analysts as well as the mortgage holders use the liquidity ratios more to make

the valuation of the going concern issues. This ratio also helps to indicate the cash flow

positioning of the company. This information is also used to measure the strategic strength of

the company in comparison to its competitors.

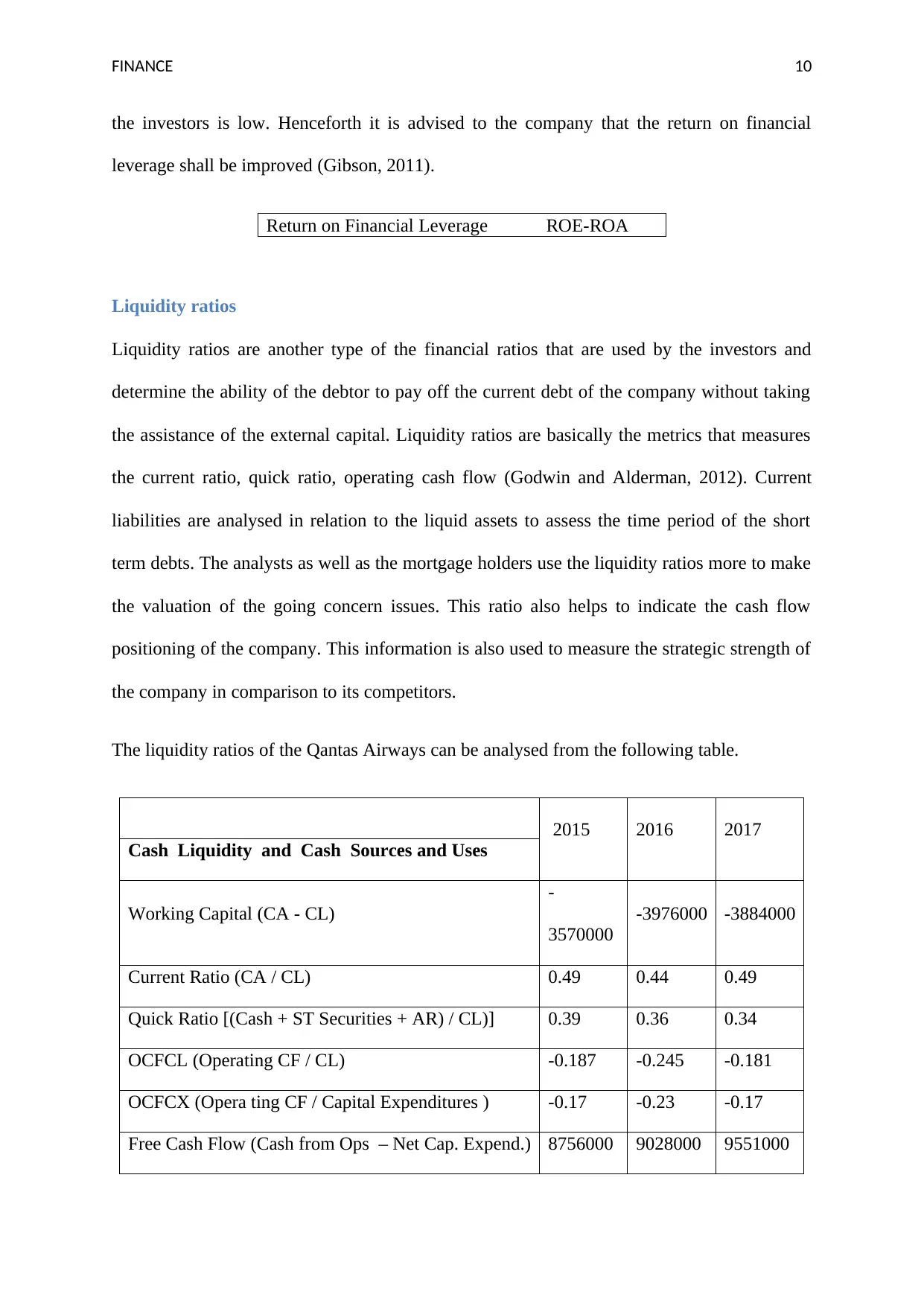

The liquidity ratios of the Qantas Airways can be analysed from the following table.

2015 2016 2017

Cash Liquidity and Cash Sources and Uses

Working Capital (CA - CL)

-

3570000

-3976000 -3884000

Current Ratio (CA / CL) 0.49 0.44 0.49

Quick Ratio [(Cash + ST Securities + AR) / CL)] 0.39 0.36 0.34

OCFCL (Operating CF / CL) -0.187 -0.245 -0.181

OCFCX (Opera ting CF / Capital Expenditures ) -0.17 -0.23 -0.17

Free Cash Flow (Cash from Ops – Net Cap. Expend.) 8756000 9028000 9551000

the investors is low. Henceforth it is advised to the company that the return on financial

leverage shall be improved (Gibson, 2011).

Return on Financial Leverage ROE-ROA

Liquidity ratios

Liquidity ratios are another type of the financial ratios that are used by the investors and

determine the ability of the debtor to pay off the current debt of the company without taking

the assistance of the external capital. Liquidity ratios are basically the metrics that measures

the current ratio, quick ratio, operating cash flow (Godwin and Alderman, 2012). Current

liabilities are analysed in relation to the liquid assets to assess the time period of the short

term debts. The analysts as well as the mortgage holders use the liquidity ratios more to make

the valuation of the going concern issues. This ratio also helps to indicate the cash flow

positioning of the company. This information is also used to measure the strategic strength of

the company in comparison to its competitors.

The liquidity ratios of the Qantas Airways can be analysed from the following table.

2015 2016 2017

Cash Liquidity and Cash Sources and Uses

Working Capital (CA - CL)

-

3570000

-3976000 -3884000

Current Ratio (CA / CL) 0.49 0.44 0.49

Quick Ratio [(Cash + ST Securities + AR) / CL)] 0.39 0.36 0.34

OCFCL (Operating CF / CL) -0.187 -0.245 -0.181

OCFCX (Opera ting CF / Capital Expenditures ) -0.17 -0.23 -0.17

Free Cash Flow (Cash from Ops – Net Cap. Expend.) 8756000 9028000 9551000

FINANCE 11

Current Ratio

Current ratio is the kind of the liquidity ratio which is used to measure the ability of the

company to pay short term liabilities as well as the long term liabilities. To cover this kind of

the liability the current ratios takes into the consideration that the total assets of the company

and its relation to the current liabilities of the company. From the table below it can be

analysed that the company is maintaining its current ratio from 0.48 to 0.50 consistently or

the past three years (Higgins, 2012). The company shall increase its ratio to 2:1 which is also

considered as the ideal ratio as per the standards of the industry. It is advised to the company

to get rid of the useless assets that are not beneficial to the company, and also the company

shall also control the overhead expenses to which the major cost cutting is possible.

Current Ratio Current Assets

Current Liabilities

Quick Ratio

The quick ratio also known as the liquid ratio or the acid test ratio is used to determine the

ability of the fir to generate the cash to pay back to the current liabilities and the obligations.

The quick ratio is basically the tester that determines the value of how much cash the

company can generate within the stipulated period of the 90 days. The assets and the

marketable securities are the quick generator of the cash and therefore this ratio reflects the

ideology of the quick sources of the cash (Jenter and Lewellen, 2015). The major difference

between the quick ratio and the current ratio is that not all the current assets are convertible

into cash within the given time frame. For example inventories.

Current Ratio

Current ratio is the kind of the liquidity ratio which is used to measure the ability of the

company to pay short term liabilities as well as the long term liabilities. To cover this kind of

the liability the current ratios takes into the consideration that the total assets of the company

and its relation to the current liabilities of the company. From the table below it can be

analysed that the company is maintaining its current ratio from 0.48 to 0.50 consistently or

the past three years (Higgins, 2012). The company shall increase its ratio to 2:1 which is also

considered as the ideal ratio as per the standards of the industry. It is advised to the company

to get rid of the useless assets that are not beneficial to the company, and also the company

shall also control the overhead expenses to which the major cost cutting is possible.

Current Ratio Current Assets

Current Liabilities

Quick Ratio

The quick ratio also known as the liquid ratio or the acid test ratio is used to determine the

ability of the fir to generate the cash to pay back to the current liabilities and the obligations.

The quick ratio is basically the tester that determines the value of how much cash the

company can generate within the stipulated period of the 90 days. The assets and the

marketable securities are the quick generator of the cash and therefore this ratio reflects the

ideology of the quick sources of the cash (Jenter and Lewellen, 2015). The major difference

between the quick ratio and the current ratio is that not all the current assets are convertible

into cash within the given time frame. For example inventories.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.