AASB, IFRS, and Financial Statement Analysis Report

VerifiedAdded on 2023/06/05

|13

|3243

|386

Report

AI Summary

This report provides a comprehensive overview of financial statement regulations, highlighting the importance of their enforcement and the consequences of non-compliance. It details the contributions of the Australian Accounting Standards Board (AASB) to International Financial Reporting Standards (IFRS) and explains why IFRS is not mandatory for all members. The report then analyzes the equity and debt positions of four listed companies in the mineral industry over a four-year period, examining key financial metrics such as share capital, retained earnings, reserves, and debt-to-equity ratios. The analysis includes detailed breakdowns of equity components and debt positions, offering insights into the financial performance and capital structure of each company, with specific focus on Amani Gold and Anova Metal. The report also explains key financial terms and definitions to aid in the understanding of the financial data presented.

TABLE OF CONTENT

TABLE OF CONTENT................................................................1

EXECUTIVE SUMMARY............................................................2

INTRODUCTION........................................................................3

Annexure-1(i)..............................................................................4

Annexure-1(ii).............................................................................5

Annexure-3.................................................................................6

References:..............................................................................12

TABLE OF CONTENT................................................................1

EXECUTIVE SUMMARY............................................................2

INTRODUCTION........................................................................3

Annexure-1(i)..............................................................................4

Annexure-1(ii).............................................................................5

Annexure-3.................................................................................6

References:..............................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report highlights the importance of regulation of financial statements along with the drawback of

not regulating the same. The report further set out to deal in length about how AASB contributes to

IFRS and the rationale behind IFRS not being declared mandatory for members.

In the second half of the report, the analysis deals with the equity and debt position of 4 listed entities

dealing in mineral industry. Further, the analysis has been carried out over a period of 4 years.

The report highlights the importance of regulation of financial statements along with the drawback of

not regulating the same. The report further set out to deal in length about how AASB contributes to

IFRS and the rationale behind IFRS not being declared mandatory for members.

In the second half of the report, the analysis deals with the equity and debt position of 4 listed entities

dealing in mineral industry. Further, the analysis has been carried out over a period of 4 years.

INTRODUCTION

This report shows the requirement of the preparation of financial statement along with the

shortcomings of not preparing the financial statement. This report shows the contribution of AASB to

IFRS and reason IFRS not being made mandatory to members.

The other part of the report deals about four listed companies in mineral industry and there debt and

equity position over a period of four years.

This report shows the requirement of the preparation of financial statement along with the

shortcomings of not preparing the financial statement. This report shows the contribution of AASB to

IFRS and reason IFRS not being made mandatory to members.

The other part of the report deals about four listed companies in mineral industry and there debt and

equity position over a period of four years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Annexure-1(i)

Expanding of corporate scandal like Enron and WorldCom lead to the emergence of regulation of

accounting system and a fair and transparency reporting so that all the books of the company is

maintained in such a way that it depicts a true picture of the company without any hidden transaction.

All the bodies and regulators have thereby requested for the reporting pattern which should be

transparent in nature and improvement in standards of accounting and rules thereof.

(Uniassignment.com, 2018) It is very mush necessary to set the standards on accounting as on the

basis of this the auditors can easily form there opinion about the companies and provide justification

on the report on basis of such standard which enhance the value of their professionalism.

The accounting regulation and set of standard also ease the users of financial statement to make

comparison easily and judge the future prospects of the company and their investment decision. It

also helps in saving of cost if certain information is easily available from the disclosures.

The disclosure and setting of standard in accounting helps the investors to easily make their

investment decision so helping the entity to maximise their value and achieve high value.

The error of non-reporting can hide many material facts from the users to financial statements and the

investors will be at risk so a need to regulate the accounting system is required. The disclosures in

financials of the company solve the gap of information between the directors of the company and the

outsiders such as shareholders, suppliers, customers, government and others; it makes the user

group to easily compare the financials of the company with the other company within the same

industry. The accounting method to choose from must be reliable, easily understandable and

comparable with other company in same industry. Through regulation in accounting scam such as

WorldCom can be prevented.

Expanding of corporate scandal like Enron and WorldCom lead to the emergence of regulation of

accounting system and a fair and transparency reporting so that all the books of the company is

maintained in such a way that it depicts a true picture of the company without any hidden transaction.

All the bodies and regulators have thereby requested for the reporting pattern which should be

transparent in nature and improvement in standards of accounting and rules thereof.

(Uniassignment.com, 2018) It is very mush necessary to set the standards on accounting as on the

basis of this the auditors can easily form there opinion about the companies and provide justification

on the report on basis of such standard which enhance the value of their professionalism.

The accounting regulation and set of standard also ease the users of financial statement to make

comparison easily and judge the future prospects of the company and their investment decision. It

also helps in saving of cost if certain information is easily available from the disclosures.

The disclosure and setting of standard in accounting helps the investors to easily make their

investment decision so helping the entity to maximise their value and achieve high value.

The error of non-reporting can hide many material facts from the users to financial statements and the

investors will be at risk so a need to regulate the accounting system is required. The disclosures in

financials of the company solve the gap of information between the directors of the company and the

outsiders such as shareholders, suppliers, customers, government and others; it makes the user

group to easily compare the financials of the company with the other company within the same

industry. The accounting method to choose from must be reliable, easily understandable and

comparable with other company in same industry. Through regulation in accounting scam such as

WorldCom can be prevented.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Annexure-1(ii)

AASB is a government control entity manged by the Australian government .It the body who manages

and regulate the financial reporting framework and look after how the financial statement to be

presented.AASB report to the Australian parliament.IASB (International Accounting standard Board) is

an international organisation who looks after the private companies.The accounting board contributes

to International Financial Reporting standard in following ways:

(a) AASB provides funds for the regular activities of IASB.

(b) Coordination on matters relating to preparation of books of accounts of the company with

IASB.

(c) Providing feedback on draft sent by IASB through comment.

(d) Issues to be raised if any came across by AASB.

(e) Accounting standard’s alignment with IFRS.

(f) To adopt IFRS.

The IFRS compliance has not been mandatory for the members due to following reasons:-

(a) IFRS is complex and not easy to adopt;

(b) IFRS has got its own drawback shortcomings ;

(c) Since members are from different countries they have a varied accounting system making

IFRS compulsory may be cumbersome.

.

(a)

AASB is a government control entity manged by the Australian government .It the body who manages

and regulate the financial reporting framework and look after how the financial statement to be

presented.AASB report to the Australian parliament.IASB (International Accounting standard Board) is

an international organisation who looks after the private companies.The accounting board contributes

to International Financial Reporting standard in following ways:

(a) AASB provides funds for the regular activities of IASB.

(b) Coordination on matters relating to preparation of books of accounts of the company with

IASB.

(c) Providing feedback on draft sent by IASB through comment.

(d) Issues to be raised if any came across by AASB.

(e) Accounting standard’s alignment with IFRS.

(f) To adopt IFRS.

The IFRS compliance has not been mandatory for the members due to following reasons:-

(a) IFRS is complex and not easy to adopt;

(b) IFRS has got its own drawback shortcomings ;

(c) Since members are from different countries they have a varied accounting system making

IFRS compulsory may be cumbersome.

.

(a)

Annexure-2

In the third part of the analysis, attention has been paid to understand the different elements of

statement of financial position along with detailed focus in equity part of the balance sheet along with

non-current liability. The companies that have been chosen for the aforesaid analysis includes the

entities that have been listed on Australian Securities Exchange and is engaged in basic materials.

The name of the companied have been detailed here-in-below:

(a) Amani Gold;

(b) Anova Metal;

(c) Energia Minerals;

(d) Alloy Resources.

About the Company

Amani Gold Limited, an entity listed on Australian stock exchange is engaged in exploration of

minerals. The company marks its presence in South Africa and has interest in Giro Gold project. The

traded price of the stock on 26-09-2018 is 0.01 AUD. (Reuters.com, 2018)

Before analysing the equity portion of the company, it shall be important to understand the key terms

in the balance sheet and the assumption undertaken for analysing the equity have been enumerated

here-in-below:

(a) Debt bearing interest has been considered while computing debt equity ratio and capital

gearing ratio;

(b) Debt that has been falling under the category of non-current liability has been considered;

(c) Balance sheet and notes to accounts have been considered for the purpose of analysis.

Further, details have been considered for past 4 years;

(d) Cash and cash equivalent has not been considered and net debt has been considered on the

basis of balance sheet balance;

(e) Many balance sheet have been reinstated for year 2016 and the reinstated figure has been

considered.

Key Definitions

Before analysing the equity portion of balance sheet, it shall be important to understand the key terms

in the equity portion of balance sheet of the aforesaid four companies:

(a) Issued Capital: These shares are issued by the company at its inception and increased by time

to time to meet the requirements of funds of the company. These share carry voting rights and

the holder of these shares are the owners of the company. Further, these shares are paid at

last at the time winding of the company.

(b) Preference shares of different classes: These shareholders are next to equity shareholders and

have less influence on the company. They are entitled to a fixed rate of return. Further, many a

times preference share come with a feature of convertibility.

(c) Non-current liability: The liability which shall be paid in period greater than 12 months;

(d) Current Liability: The liability which shall be paid in a period of 12 months are known as current

liability;

In the third part of the analysis, attention has been paid to understand the different elements of

statement of financial position along with detailed focus in equity part of the balance sheet along with

non-current liability. The companies that have been chosen for the aforesaid analysis includes the

entities that have been listed on Australian Securities Exchange and is engaged in basic materials.

The name of the companied have been detailed here-in-below:

(a) Amani Gold;

(b) Anova Metal;

(c) Energia Minerals;

(d) Alloy Resources.

About the Company

Amani Gold Limited, an entity listed on Australian stock exchange is engaged in exploration of

minerals. The company marks its presence in South Africa and has interest in Giro Gold project. The

traded price of the stock on 26-09-2018 is 0.01 AUD. (Reuters.com, 2018)

Before analysing the equity portion of the company, it shall be important to understand the key terms

in the balance sheet and the assumption undertaken for analysing the equity have been enumerated

here-in-below:

(a) Debt bearing interest has been considered while computing debt equity ratio and capital

gearing ratio;

(b) Debt that has been falling under the category of non-current liability has been considered;

(c) Balance sheet and notes to accounts have been considered for the purpose of analysis.

Further, details have been considered for past 4 years;

(d) Cash and cash equivalent has not been considered and net debt has been considered on the

basis of balance sheet balance;

(e) Many balance sheet have been reinstated for year 2016 and the reinstated figure has been

considered.

Key Definitions

Before analysing the equity portion of balance sheet, it shall be important to understand the key terms

in the equity portion of balance sheet of the aforesaid four companies:

(a) Issued Capital: These shares are issued by the company at its inception and increased by time

to time to meet the requirements of funds of the company. These share carry voting rights and

the holder of these shares are the owners of the company. Further, these shares are paid at

last at the time winding of the company.

(b) Preference shares of different classes: These shareholders are next to equity shareholders and

have less influence on the company. They are entitled to a fixed rate of return. Further, many a

times preference share come with a feature of convertibility.

(c) Non-current liability: The liability which shall be paid in period greater than 12 months;

(d) Current Liability: The liability which shall be paid in a period of 12 months are known as current

liability;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(e) Options: Options are the rights which are issued by the company which entitles its holders right

to receive shares at a particular date.

(f) Reserves: Reserve are the saved portion of the company to meet any future contingency.

These are created by the company to meet future needs.

(g) Foreign Currency translation Reserve: This is one type of reserve which are created at the time

of consolidation of accounts of subsidiary in the books of parent in terms of requirement of

AASB and IFRS. Further, the method of consolidating accounts include temporal and current

method.

(h) Available for Sale Investment Reserve These are the reserve created by the company in

compliance with AASB and IFRS to mark the investments at fair value.

(i) Option Reserve: Options reserves are created by the company to meet the requirement of

vesting when the option holders exercise their right. These reserve are created in terms of

compliance with IFRS and AASB;

(j) Cash flow hedging reserve: The reserves are created to meet cash flow requirement in case

the management estimate does not match the actual outcome and is essential to meet the

working capital requirement of the company;

(k) Non-Controlling interest: Non-controlling interest represent claim of minority investor who hold

shares in the company and do not exercise any significant control in the board of director and

decision making of the company.

(l) Treasury Shares: Treasury share also known as bought back shares represent those shares

that have been called back by the company with an intention to cancel the same.

(m) Dividend reinvestment: These are the dividend which have been reinvested in the company and

increases the wealth of the shareholders.

(n) Retained earnings: This represents the profit or loss of the company accumulated over the

years.

Analysis of Equity

The detailed break of equity of Amani Gold has been presented here-in-below:

Amani Gold formerly known as Burey Gold $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 47.883 36.719 30.722 23.82

2 Retained Earnings -30.445 -30.69 -18.31 -17.104

3 Reserves 7.852 9.681 5.266 2.467

4 Non-Controlling interest 0.384 0.365 0.477

5 Total Equity 25.674 16.075 18.155 9.183

(BDO Audit (WA) Pty Ltd, 2017) (BDO Audit (WA) Pty Ltd, 2017)

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company. The non-controlling

interest of the company has also been falling down on account of the afore-stated reason. The

reserves of the company include foreign currency translation reserve and option reserve. The

to receive shares at a particular date.

(f) Reserves: Reserve are the saved portion of the company to meet any future contingency.

These are created by the company to meet future needs.

(g) Foreign Currency translation Reserve: This is one type of reserve which are created at the time

of consolidation of accounts of subsidiary in the books of parent in terms of requirement of

AASB and IFRS. Further, the method of consolidating accounts include temporal and current

method.

(h) Available for Sale Investment Reserve These are the reserve created by the company in

compliance with AASB and IFRS to mark the investments at fair value.

(i) Option Reserve: Options reserves are created by the company to meet the requirement of

vesting when the option holders exercise their right. These reserve are created in terms of

compliance with IFRS and AASB;

(j) Cash flow hedging reserve: The reserves are created to meet cash flow requirement in case

the management estimate does not match the actual outcome and is essential to meet the

working capital requirement of the company;

(k) Non-Controlling interest: Non-controlling interest represent claim of minority investor who hold

shares in the company and do not exercise any significant control in the board of director and

decision making of the company.

(l) Treasury Shares: Treasury share also known as bought back shares represent those shares

that have been called back by the company with an intention to cancel the same.

(m) Dividend reinvestment: These are the dividend which have been reinvested in the company and

increases the wealth of the shareholders.

(n) Retained earnings: This represents the profit or loss of the company accumulated over the

years.

Analysis of Equity

The detailed break of equity of Amani Gold has been presented here-in-below:

Amani Gold formerly known as Burey Gold $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 47.883 36.719 30.722 23.82

2 Retained Earnings -30.445 -30.69 -18.31 -17.104

3 Reserves 7.852 9.681 5.266 2.467

4 Non-Controlling interest 0.384 0.365 0.477

5 Total Equity 25.674 16.075 18.155 9.183

(BDO Audit (WA) Pty Ltd, 2017) (BDO Audit (WA) Pty Ltd, 2017)

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company. The non-controlling

interest of the company has also been falling down on account of the afore-stated reason. The

reserves of the company include foreign currency translation reserve and option reserve. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

aforesaid reserve have already been detailed above. The detail break up of share Capital of the

company has been presented here-in-below:

Contributed Equity

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 36.719 30.722 23.821 23.142

2 Capital Raising Costs -0.66 -0.43 -0.314 -0.011

3 Capital Raised 11.824 6.427 7.215 0.69

4 Total Contributed Equity 47.883 36.719 30.722 23.821

On perusal of the above, it may be seen that company has issued equity from time to time to meet the

fund requirement as the company has been incurring losses.

Further detail of debt position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 25.674 16.075 18.155 9.183

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

Anova Metal Limited

Anova Metal Limited is an entity listed on Australian Stock exchange and primarily engaged in

exploration of minerals The Company has interest in big spring project in Nevada. The price of the

share of the company on 26-09-2018 is 0.02 AUD. (Reuters, 2018)

An analysis of the equity of the company has been presented here-in-below:

Anova Metal $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 44.747 34.947 32.895 29.315

2 Retained Earnings -28.157 -24.98 -22.774 -19.118

3 Reserves 1.863 2.425 2.176 1.897

4 Non-Controlling interest 0

5 Total Equity 18.453 12.392 12.297 12.094

(Judd, 2017) (Judd, 2017)

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company. The non-controlling

interest of the company is zero and does not have any minority liability. The reserves of the company

include foreign currency translation reserve and option reserve. The aforesaid reserve have already

been detailed above. The detail break up of share Capital of the company has been presented here-

in-below:

company has been presented here-in-below:

Contributed Equity

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 36.719 30.722 23.821 23.142

2 Capital Raising Costs -0.66 -0.43 -0.314 -0.011

3 Capital Raised 11.824 6.427 7.215 0.69

4 Total Contributed Equity 47.883 36.719 30.722 23.821

On perusal of the above, it may be seen that company has issued equity from time to time to meet the

fund requirement as the company has been incurring losses.

Further detail of debt position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 25.674 16.075 18.155 9.183

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

Anova Metal Limited

Anova Metal Limited is an entity listed on Australian Stock exchange and primarily engaged in

exploration of minerals The Company has interest in big spring project in Nevada. The price of the

share of the company on 26-09-2018 is 0.02 AUD. (Reuters, 2018)

An analysis of the equity of the company has been presented here-in-below:

Anova Metal $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 44.747 34.947 32.895 29.315

2 Retained Earnings -28.157 -24.98 -22.774 -19.118

3 Reserves 1.863 2.425 2.176 1.897

4 Non-Controlling interest 0

5 Total Equity 18.453 12.392 12.297 12.094

(Judd, 2017) (Judd, 2017)

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company. The non-controlling

interest of the company is zero and does not have any minority liability. The reserves of the company

include foreign currency translation reserve and option reserve. The aforesaid reserve have already

been detailed above. The detail break up of share Capital of the company has been presented here-

in-below:

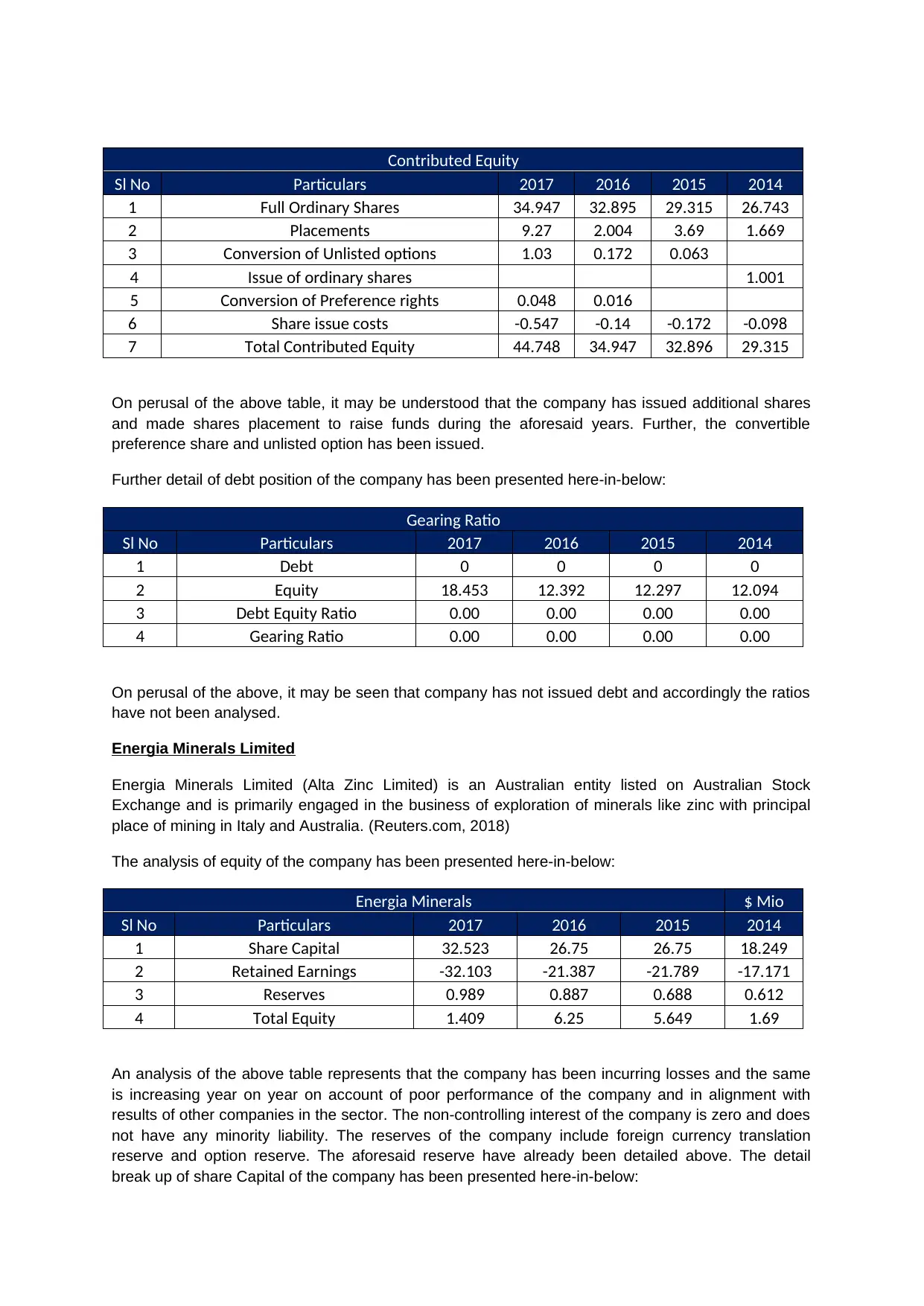

Contributed Equity

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 34.947 32.895 29.315 26.743

2 Placements 9.27 2.004 3.69 1.669

3 Conversion of Unlisted options 1.03 0.172 0.063

4 Issue of ordinary shares 1.001

5 Conversion of Preference rights 0.048 0.016

6 Share issue costs -0.547 -0.14 -0.172 -0.098

7 Total Contributed Equity 44.748 34.947 32.896 29.315

On perusal of the above table, it may be understood that the company has issued additional shares

and made shares placement to raise funds during the aforesaid years. Further, the convertible

preference share and unlisted option has been issued.

Further detail of debt position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 18.453 12.392 12.297 12.094

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

Energia Minerals Limited

Energia Minerals Limited (Alta Zinc Limited) is an Australian entity listed on Australian Stock

Exchange and is primarily engaged in the business of exploration of minerals like zinc with principal

place of mining in Italy and Australia. (Reuters.com, 2018)

The analysis of equity of the company has been presented here-in-below:

Energia Minerals $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 32.523 26.75 26.75 18.249

2 Retained Earnings -32.103 -21.387 -21.789 -17.171

3 Reserves 0.989 0.887 0.688 0.612

4 Total Equity 1.409 6.25 5.649 1.69

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company and in alignment with

results of other companies in the sector. The non-controlling interest of the company is zero and does

not have any minority liability. The reserves of the company include foreign currency translation

reserve and option reserve. The aforesaid reserve have already been detailed above. The detail

break up of share Capital of the company has been presented here-in-below:

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 34.947 32.895 29.315 26.743

2 Placements 9.27 2.004 3.69 1.669

3 Conversion of Unlisted options 1.03 0.172 0.063

4 Issue of ordinary shares 1.001

5 Conversion of Preference rights 0.048 0.016

6 Share issue costs -0.547 -0.14 -0.172 -0.098

7 Total Contributed Equity 44.748 34.947 32.896 29.315

On perusal of the above table, it may be understood that the company has issued additional shares

and made shares placement to raise funds during the aforesaid years. Further, the convertible

preference share and unlisted option has been issued.

Further detail of debt position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 18.453 12.392 12.297 12.094

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

Energia Minerals Limited

Energia Minerals Limited (Alta Zinc Limited) is an Australian entity listed on Australian Stock

Exchange and is primarily engaged in the business of exploration of minerals like zinc with principal

place of mining in Italy and Australia. (Reuters.com, 2018)

The analysis of equity of the company has been presented here-in-below:

Energia Minerals $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 32.523 26.75 26.75 18.249

2 Retained Earnings -32.103 -21.387 -21.789 -17.171

3 Reserves 0.989 0.887 0.688 0.612

4 Total Equity 1.409 6.25 5.649 1.69

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company and in alignment with

results of other companies in the sector. The non-controlling interest of the company is zero and does

not have any minority liability. The reserves of the company include foreign currency translation

reserve and option reserve. The aforesaid reserve have already been detailed above. The detail

break up of share Capital of the company has been presented here-in-below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

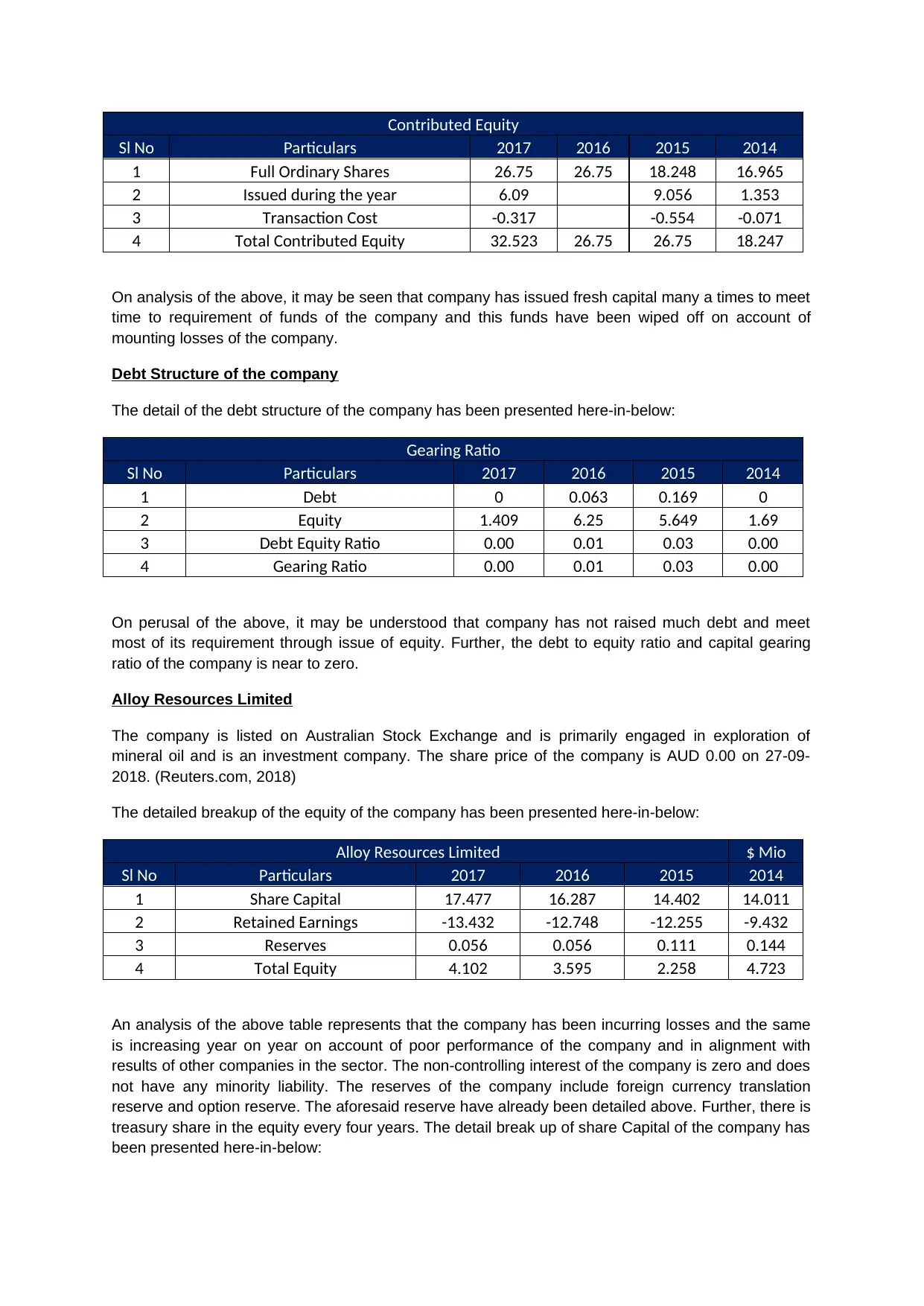

Contributed Equity

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 26.75 26.75 18.248 16.965

2 Issued during the year 6.09 9.056 1.353

3 Transaction Cost -0.317 -0.554 -0.071

4 Total Contributed Equity 32.523 26.75 26.75 18.247

On analysis of the above, it may be seen that company has issued fresh capital many a times to meet

time to requirement of funds of the company and this funds have been wiped off on account of

mounting losses of the company.

Debt Structure of the company

The detail of the debt structure of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0.063 0.169 0

2 Equity 1.409 6.25 5.649 1.69

3 Debt Equity Ratio 0.00 0.01 0.03 0.00

4 Gearing Ratio 0.00 0.01 0.03 0.00

On perusal of the above, it may be understood that company has not raised much debt and meet

most of its requirement through issue of equity. Further, the debt to equity ratio and capital gearing

ratio of the company is near to zero.

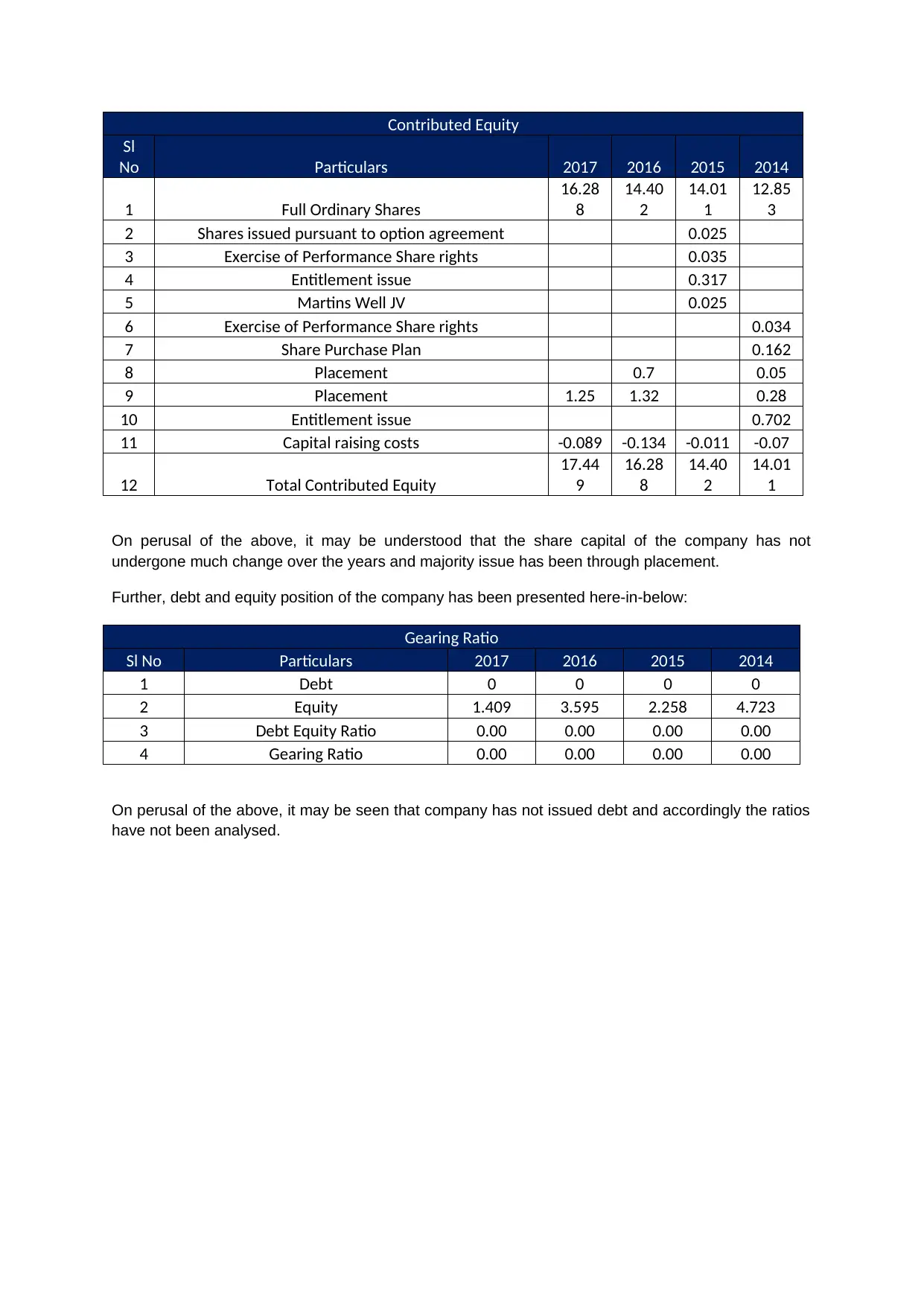

Alloy Resources Limited

The company is listed on Australian Stock Exchange and is primarily engaged in exploration of

mineral oil and is an investment company. The share price of the company is AUD 0.00 on 27-09-

2018. (Reuters.com, 2018)

The detailed breakup of the equity of the company has been presented here-in-below:

Alloy Resources Limited $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 17.477 16.287 14.402 14.011

2 Retained Earnings -13.432 -12.748 -12.255 -9.432

3 Reserves 0.056 0.056 0.111 0.144

4 Total Equity 4.102 3.595 2.258 4.723

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company and in alignment with

results of other companies in the sector. The non-controlling interest of the company is zero and does

not have any minority liability. The reserves of the company include foreign currency translation

reserve and option reserve. The aforesaid reserve have already been detailed above. Further, there is

treasury share in the equity every four years. The detail break up of share Capital of the company has

been presented here-in-below:

Sl No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares 26.75 26.75 18.248 16.965

2 Issued during the year 6.09 9.056 1.353

3 Transaction Cost -0.317 -0.554 -0.071

4 Total Contributed Equity 32.523 26.75 26.75 18.247

On analysis of the above, it may be seen that company has issued fresh capital many a times to meet

time to requirement of funds of the company and this funds have been wiped off on account of

mounting losses of the company.

Debt Structure of the company

The detail of the debt structure of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0.063 0.169 0

2 Equity 1.409 6.25 5.649 1.69

3 Debt Equity Ratio 0.00 0.01 0.03 0.00

4 Gearing Ratio 0.00 0.01 0.03 0.00

On perusal of the above, it may be understood that company has not raised much debt and meet

most of its requirement through issue of equity. Further, the debt to equity ratio and capital gearing

ratio of the company is near to zero.

Alloy Resources Limited

The company is listed on Australian Stock Exchange and is primarily engaged in exploration of

mineral oil and is an investment company. The share price of the company is AUD 0.00 on 27-09-

2018. (Reuters.com, 2018)

The detailed breakup of the equity of the company has been presented here-in-below:

Alloy Resources Limited $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 17.477 16.287 14.402 14.011

2 Retained Earnings -13.432 -12.748 -12.255 -9.432

3 Reserves 0.056 0.056 0.111 0.144

4 Total Equity 4.102 3.595 2.258 4.723

An analysis of the above table represents that the company has been incurring losses and the same

is increasing year on year on account of poor performance of the company and in alignment with

results of other companies in the sector. The non-controlling interest of the company is zero and does

not have any minority liability. The reserves of the company include foreign currency translation

reserve and option reserve. The aforesaid reserve have already been detailed above. Further, there is

treasury share in the equity every four years. The detail break up of share Capital of the company has

been presented here-in-below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contributed Equity

Sl

No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares

16.28

8

14.40

2

14.01

1

12.85

3

2 Shares issued pursuant to option agreement 0.025

3 Exercise of Performance Share rights 0.035

4 Entitlement issue 0.317

5 Martins Well JV 0.025

6 Exercise of Performance Share rights 0.034

7 Share Purchase Plan 0.162

8 Placement 0.7 0.05

9 Placement 1.25 1.32 0.28

10 Entitlement issue 0.702

11 Capital raising costs -0.089 -0.134 -0.011 -0.07

12 Total Contributed Equity

17.44

9

16.28

8

14.40

2

14.01

1

On perusal of the above, it may be understood that the share capital of the company has not

undergone much change over the years and majority issue has been through placement.

Further, debt and equity position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 1.409 3.595 2.258 4.723

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

Sl

No Particulars 2017 2016 2015 2014

1 Full Ordinary Shares

16.28

8

14.40

2

14.01

1

12.85

3

2 Shares issued pursuant to option agreement 0.025

3 Exercise of Performance Share rights 0.035

4 Entitlement issue 0.317

5 Martins Well JV 0.025

6 Exercise of Performance Share rights 0.034

7 Share Purchase Plan 0.162

8 Placement 0.7 0.05

9 Placement 1.25 1.32 0.28

10 Entitlement issue 0.702

11 Capital raising costs -0.089 -0.134 -0.011 -0.07

12 Total Contributed Equity

17.44

9

16.28

8

14.40

2

14.01

1

On perusal of the above, it may be understood that the share capital of the company has not

undergone much change over the years and majority issue has been through placement.

Further, debt and equity position of the company has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 1.409 3.595 2.258 4.723

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above, it may be seen that company has not issued debt and accordingly the ratios

have not been analysed.

References:

Australian Accounting Standard Board. (n.d.). The Standard-Setting Process. Retrieved September

21, 2018, from www.aasb.gov.au: https://www.aasb.gov.au/About-the-AASB/The-standard-

setting-process.aspx

BDO Audit (WA) Pty Ltd. (2017). Annual Report. Retrieved September 28, 2018, from

www.amanigold.com: https://www.amanigold.com/wp-content/uploads/2018/07/2017-Annual-

Report.pdf

Judd, H. M. (2017). Annual Report. Retrieved September 28, 2018, from anovametals.com.a:

anovametals.com.au/wp-content/uploads/2017/10/Anova-AR-2017.pdf

Reuters. (2018). Anova Metals Ltd (AWV.AX). Retrieved September 28, 2018, from www.reuters.com:

https://www.reuters.com/finance/stocks/overview/AWV.AX

Reuters.com. (2018). Alloy Resources Ltd (AYR.AX). Retrieved September 28, 2018, from

www.reuters.com: https://www.reuters.com/finance/stocks/overview/AYR.AX

Reuters.com. (2018). Alta Zinc Ltd. Retrieved September 28, 2018, from www.reuters.com:

https://www.reuters.com/finance/stocks/overview/EMXXX.AX

Reuters.com. (2018). Amani Gold Ltd (ANL.AX). Retrieved September 28, 2018, from

www.reuters.com: https://www.reuters.com/finance/stocks/overview/ANL.AX

Uniassignment.com. (2018). What Are The Arguments For And Against Regulations Accounting

Essay. Retrieved September 28, 2018, from https://www.uniassignment.com/essay-

samples/accounting/what-are-the-arguments-for-and-against-regulations-accounting-

essay.php

Australian Accounting Standard Board. (n.d.). The Standard-Setting Process. Retrieved September

21, 2018, from www.aasb.gov.au: https://www.aasb.gov.au/About-the-AASB/The-standard-

setting-process.aspx

BDO Audit (WA) Pty Ltd. (2017). Annual Report. Retrieved September 28, 2018, from

www.amanigold.com: https://www.amanigold.com/wp-content/uploads/2018/07/2017-Annual-

Report.pdf

Judd, H. M. (2017). Annual Report. Retrieved September 28, 2018, from anovametals.com.a:

anovametals.com.au/wp-content/uploads/2017/10/Anova-AR-2017.pdf

Reuters. (2018). Anova Metals Ltd (AWV.AX). Retrieved September 28, 2018, from www.reuters.com:

https://www.reuters.com/finance/stocks/overview/AWV.AX

Reuters.com. (2018). Alloy Resources Ltd (AYR.AX). Retrieved September 28, 2018, from

www.reuters.com: https://www.reuters.com/finance/stocks/overview/AYR.AX

Reuters.com. (2018). Alta Zinc Ltd. Retrieved September 28, 2018, from www.reuters.com:

https://www.reuters.com/finance/stocks/overview/EMXXX.AX

Reuters.com. (2018). Amani Gold Ltd (ANL.AX). Retrieved September 28, 2018, from

www.reuters.com: https://www.reuters.com/finance/stocks/overview/ANL.AX

Uniassignment.com. (2018). What Are The Arguments For And Against Regulations Accounting

Essay. Retrieved September 28, 2018, from https://www.uniassignment.com/essay-

samples/accounting/what-are-the-arguments-for-and-against-regulations-accounting-

essay.php

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.