Arden University - FIN4001 Financial Statement Analysis Report

VerifiedAdded on 2023/06/04

|17

|3736

|173

Report

AI Summary

This report provides a comprehensive financial analysis, including ratio calculations for 2018 and 2019, assessing profitability, efficiency, and liquidity. It includes a discussion on the significance of financial statement analysis for stakeholders. The report features an opening statement of financial position and a six-month cash budget, along with explanations of additional expenditures. Furthermore, the analysis calculates the break-even point (BEP) and margin of safety (MOS) for 2019 and 2020, discussing a new business strategy. Finally, the report evaluates investment appraisal techniques, including payback period, net present value (NPV), and average rate of return, to determine the best investment option. This student-contributed document is available on Desklib, a platform offering a wealth of study resources.

Introduction to Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Calculation of ratios for year 2019 and year 2018 ......................................................................1

Significance of financial statements analysis .............................................................................3

Question 2........................................................................................................................................3

a) opening statement of financial position .................................................................................3

b ) monthly cash budget for 6 months ........................................................................................4

c ) Explanation of additional expenditures..................................................................................4

Question 3 .......................................................................................................................................5

a ) Calculation of Break even point (BEP)..................................................................................5

b) Margin of safety ( MOS ) for the year ended 2019 and 2020.................................................6

c) Discussion of the new strategy that has been formed by Jessica.............................................6

Question 4........................................................................................................................................7

(a) calculation of pay back period, Net present value and average rate of return........................7

Discuss the best method of appraisal technique..........................................................................9

Capital investment appraisal techniques....................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Calculation of ratios for year 2019 and year 2018 ......................................................................1

Significance of financial statements analysis .............................................................................3

Question 2........................................................................................................................................3

a) opening statement of financial position .................................................................................3

b ) monthly cash budget for 6 months ........................................................................................4

c ) Explanation of additional expenditures..................................................................................4

Question 3 .......................................................................................................................................5

a ) Calculation of Break even point (BEP)..................................................................................5

b) Margin of safety ( MOS ) for the year ended 2019 and 2020.................................................6

c) Discussion of the new strategy that has been formed by Jessica.............................................6

Question 4........................................................................................................................................7

(a) calculation of pay back period, Net present value and average rate of return........................7

Discuss the best method of appraisal technique..........................................................................9

Capital investment appraisal techniques....................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is general term which tells about various activities attached like banking services,

leverage debt or credit, money market, and other monetary investments. It represents

management of money and the procedure to required necessary funds. Finance word is used in

day to day operating life of any enterprise which should be managed with financial statement. It

are written document which signifies different economic activities and financial performance of

an organisation. They are usually audited by group of professional and government agencies to

ensure optimum reliability and utilize for many purposes by organisation (Elijido‐Ten and

Dumay, 2019). Financial statement most often consists of statement of profit and loss, statement

of financial position and statement of cash flow. This written report includes calculation of few

ratios and their analysis, NPV analysis which implies to choose most profitable project and it

also consider cash budget which analyse their cost which would occur in future.

Question 1

Calculation of ratios for year 2019 and year 2018

1. Gross profit margin = ( sales - COGS ) * 100 / sales

= ( 3495 – 2182 ) * 100 / 3495

= ( 1313 / 3495 ) * 100

= 37.57 %

Interpretation: It generally categorized into profitability ratio which makes comparison in gross

profit of an enterprise against with sales revenue. In the given question, gross profit comes out

37.57 % which is equivalent to 38 % that implies good as a growing sector company this is get

only after deducting the cost of these goods.

2. Assets usage ratio = total sales / average total assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

Interpretation : It categorized into efficiency ratio which assists every organisation to obtain

sales income from their held assets in terms of monetary value through using net revenue with

average total assets. In this ratio, it signifies higher the ratio better the organisation's efficiency.

When it comes to ideal ratio it is 2.5 times or more. In the given question, the assets usage ratio

1

Finance is general term which tells about various activities attached like banking services,

leverage debt or credit, money market, and other monetary investments. It represents

management of money and the procedure to required necessary funds. Finance word is used in

day to day operating life of any enterprise which should be managed with financial statement. It

are written document which signifies different economic activities and financial performance of

an organisation. They are usually audited by group of professional and government agencies to

ensure optimum reliability and utilize for many purposes by organisation (Elijido‐Ten and

Dumay, 2019). Financial statement most often consists of statement of profit and loss, statement

of financial position and statement of cash flow. This written report includes calculation of few

ratios and their analysis, NPV analysis which implies to choose most profitable project and it

also consider cash budget which analyse their cost which would occur in future.

Question 1

Calculation of ratios for year 2019 and year 2018

1. Gross profit margin = ( sales - COGS ) * 100 / sales

= ( 3495 – 2182 ) * 100 / 3495

= ( 1313 / 3495 ) * 100

= 37.57 %

Interpretation: It generally categorized into profitability ratio which makes comparison in gross

profit of an enterprise against with sales revenue. In the given question, gross profit comes out

37.57 % which is equivalent to 38 % that implies good as a growing sector company this is get

only after deducting the cost of these goods.

2. Assets usage ratio = total sales / average total assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

Interpretation : It categorized into efficiency ratio which assists every organisation to obtain

sales income from their held assets in terms of monetary value through using net revenue with

average total assets. In this ratio, it signifies higher the ratio better the organisation's efficiency.

When it comes to ideal ratio it is 2.5 times or more. In the given question, the assets usage ratio

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of an organisation has 1.10 which is quite low than ideal one. They need to improve their

revenue generation ability and need to optimum utilize their assets in proper manner.

33 Current ratio = current assets / current liabilities

= 1687 / 744

= 2.27 times

Interpretation : In this ratio, it measures the capacity of a firm to meet their short term obligation

in lesser time period. It analyses short term liquidity of firm. It has ideal ratio of 2 : 1 but the

given company has 2.27 which is above than ideal one. This is the most appropriate situation for

any firm where they has more current assets.

33 Acid test ratio = ( Current asset – stock ) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation: In this acid test ratio, it makes the comparison of highly liquidated assets of the

organisation with their current liabilities. The ideal one for this is 1times. In this question, it

comes out to 2.06 time which signifies more secured and adequate capacity to meet short term

obligations.

33 Inventory holding period = ( average inventory / cost of goods sold ) * 365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Interpretation: Inventory Holding Period is a ratio that depicts the quantity of days for which an

company holds stock earlier than sales. It suggests what number of days it takes for stock to

rotate within side the enterprise.

6. Debt to equity ratio = total debts / total equity

= 170 / 2898

= 0.058 times

Interpretation: In this ratio, when there is high debt equity ratio which indicates that an

enterprise having more borrowed fund from capital market in their operations. Whereas low debt

equity ratio indicates assets utilised at its optimum and have less borrowed fund outside market.

2

revenue generation ability and need to optimum utilize their assets in proper manner.

33 Current ratio = current assets / current liabilities

= 1687 / 744

= 2.27 times

Interpretation : In this ratio, it measures the capacity of a firm to meet their short term obligation

in lesser time period. It analyses short term liquidity of firm. It has ideal ratio of 2 : 1 but the

given company has 2.27 which is above than ideal one. This is the most appropriate situation for

any firm where they has more current assets.

33 Acid test ratio = ( Current asset – stock ) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation: In this acid test ratio, it makes the comparison of highly liquidated assets of the

organisation with their current liabilities. The ideal one for this is 1times. In this question, it

comes out to 2.06 time which signifies more secured and adequate capacity to meet short term

obligations.

33 Inventory holding period = ( average inventory / cost of goods sold ) * 365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Interpretation: Inventory Holding Period is a ratio that depicts the quantity of days for which an

company holds stock earlier than sales. It suggests what number of days it takes for stock to

rotate within side the enterprise.

6. Debt to equity ratio = total debts / total equity

= 170 / 2898

= 0.058 times

Interpretation: In this ratio, when there is high debt equity ratio which indicates that an

enterprise having more borrowed fund from capital market in their operations. Whereas low debt

equity ratio indicates assets utilised at its optimum and have less borrowed fund outside market.

2

In this given question, it have 0.058 which denotes they have less borrowed fund and less risk at

hand.

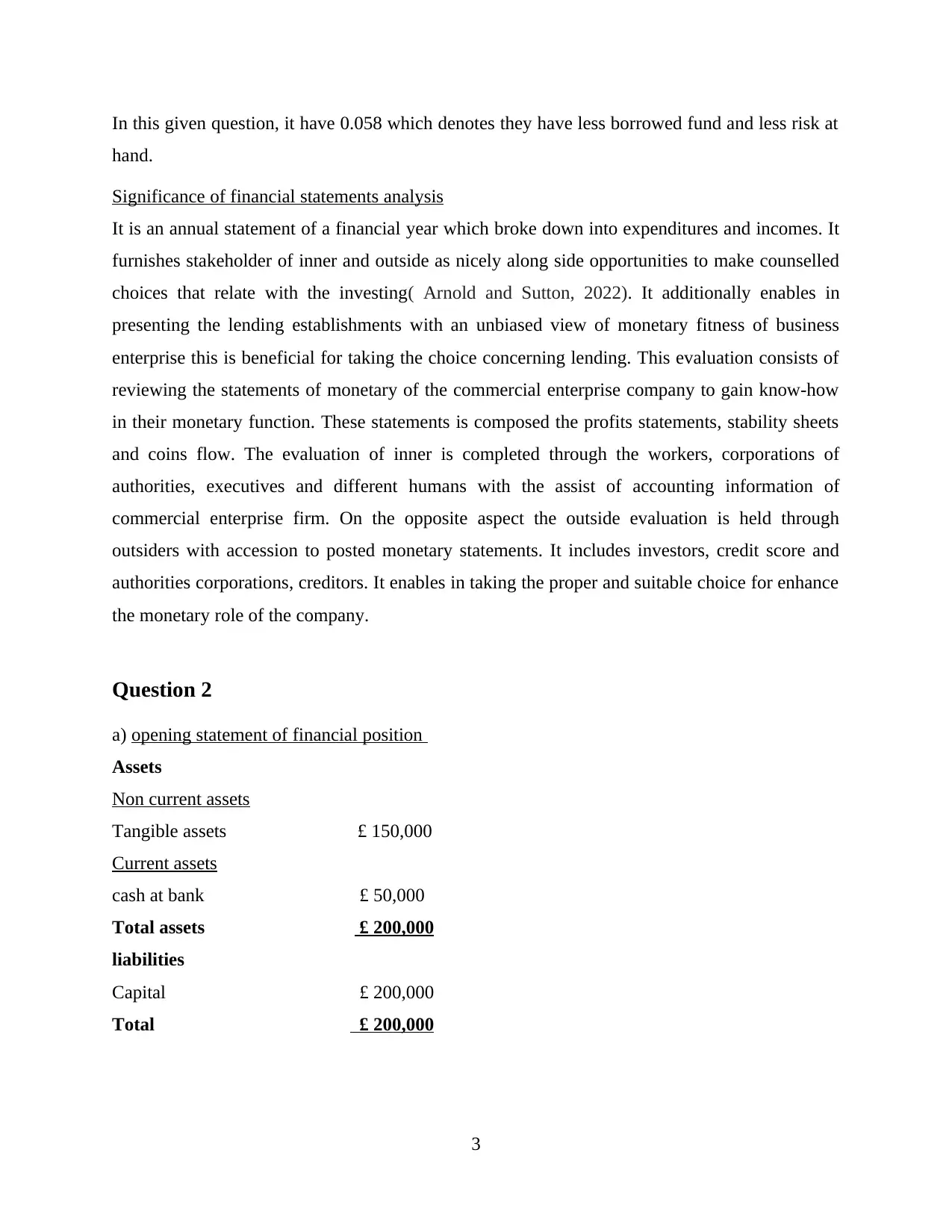

Significance of financial statements analysis

It is an annual statement of a financial year which broke down into expenditures and incomes. It

furnishes stakeholder of inner and outside as nicely along side opportunities to make counselled

choices that relate with the investing( Arnold and Sutton, 2022). It additionally enables in

presenting the lending establishments with an unbiased view of monetary fitness of business

enterprise this is beneficial for taking the choice concerning lending. This evaluation consists of

reviewing the statements of monetary of the commercial enterprise company to gain know-how

in their monetary function. These statements is composed the profits statements, stability sheets

and coins flow. The evaluation of inner is completed through the workers, corporations of

authorities, executives and different humans with the assist of accounting information of

commercial enterprise firm. On the opposite aspect the outside evaluation is held through

outsiders with accession to posted monetary statements. It includes investors, credit score and

authorities corporations, creditors. It enables in taking the proper and suitable choice for enhance

the monetary role of the company.

Question 2

a) opening statement of financial position

Assets

Non current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

Total £ 200,000

3

hand.

Significance of financial statements analysis

It is an annual statement of a financial year which broke down into expenditures and incomes. It

furnishes stakeholder of inner and outside as nicely along side opportunities to make counselled

choices that relate with the investing( Arnold and Sutton, 2022). It additionally enables in

presenting the lending establishments with an unbiased view of monetary fitness of business

enterprise this is beneficial for taking the choice concerning lending. This evaluation consists of

reviewing the statements of monetary of the commercial enterprise company to gain know-how

in their monetary function. These statements is composed the profits statements, stability sheets

and coins flow. The evaluation of inner is completed through the workers, corporations of

authorities, executives and different humans with the assist of accounting information of

commercial enterprise firm. On the opposite aspect the outside evaluation is held through

outsiders with accession to posted monetary statements. It includes investors, credit score and

authorities corporations, creditors. It enables in taking the proper and suitable choice for enhance

the monetary role of the company.

Question 2

a) opening statement of financial position

Assets

Non current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

Total £ 200,000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

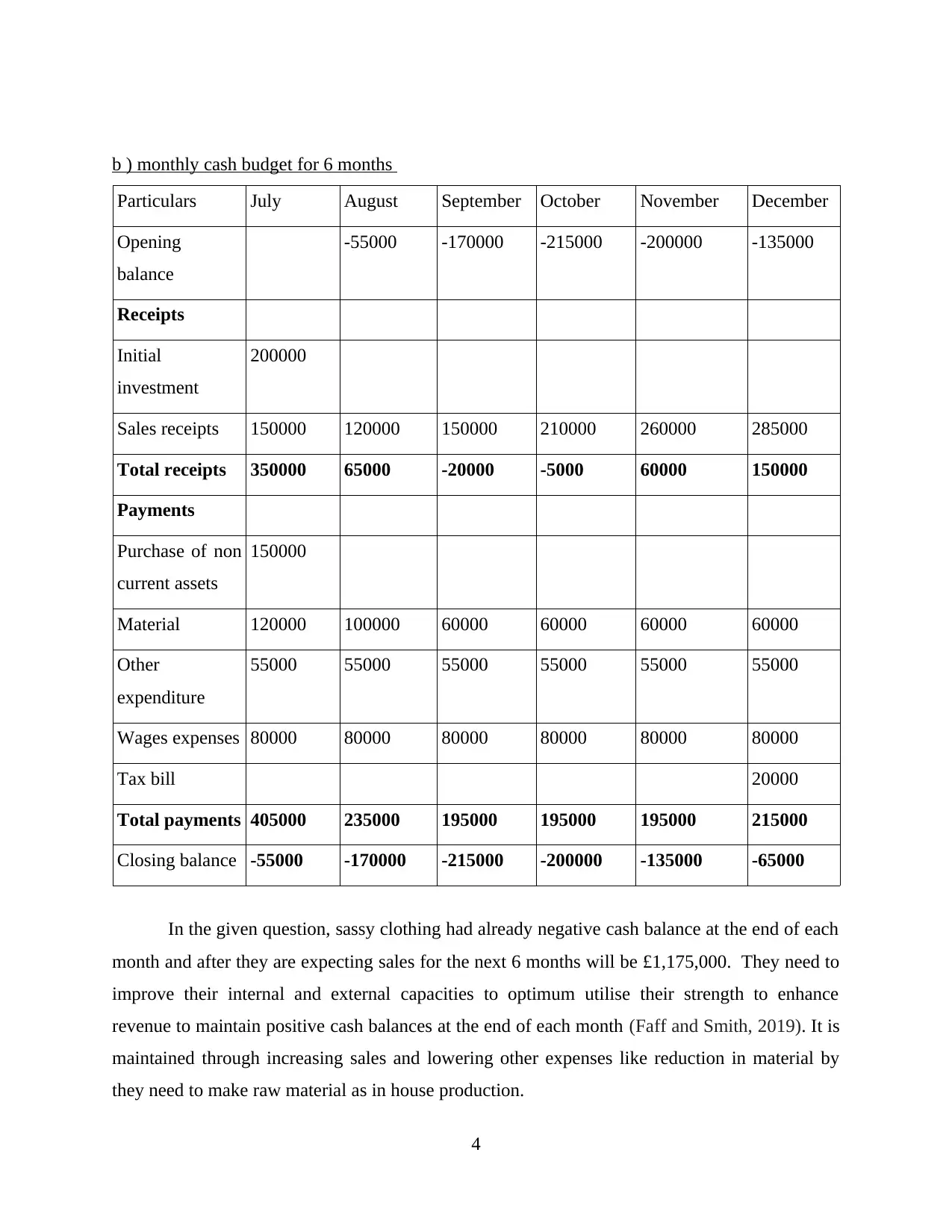

b ) monthly cash budget for 6 months

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, sassy clothing had already negative cash balance at the end of each

month and after they are expecting sales for the next 6 months will be £1,175,000. They need to

improve their internal and external capacities to optimum utilise their strength to enhance

revenue to maintain positive cash balances at the end of each month (Faff and Smith, 2019). It is

maintained through increasing sales and lowering other expenses like reduction in material by

they need to make raw material as in house production.

4

Particulars July August September October November December

Opening

balance

-55000 -170000 -215000 -200000 -135000

Receipts

Initial

investment

200000

Sales receipts 150000 120000 150000 210000 260000 285000

Total receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of non

current assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

expenditure

55000 55000 55000 55000 55000 55000

Wages expenses 80000 80000 80000 80000 80000 80000

Tax bill 20000

Total payments 405000 235000 195000 195000 195000 215000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, sassy clothing had already negative cash balance at the end of each

month and after they are expecting sales for the next 6 months will be £1,175,000. They need to

improve their internal and external capacities to optimum utilise their strength to enhance

revenue to maintain positive cash balances at the end of each month (Faff and Smith, 2019). It is

maintained through increasing sales and lowering other expenses like reduction in material by

they need to make raw material as in house production.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

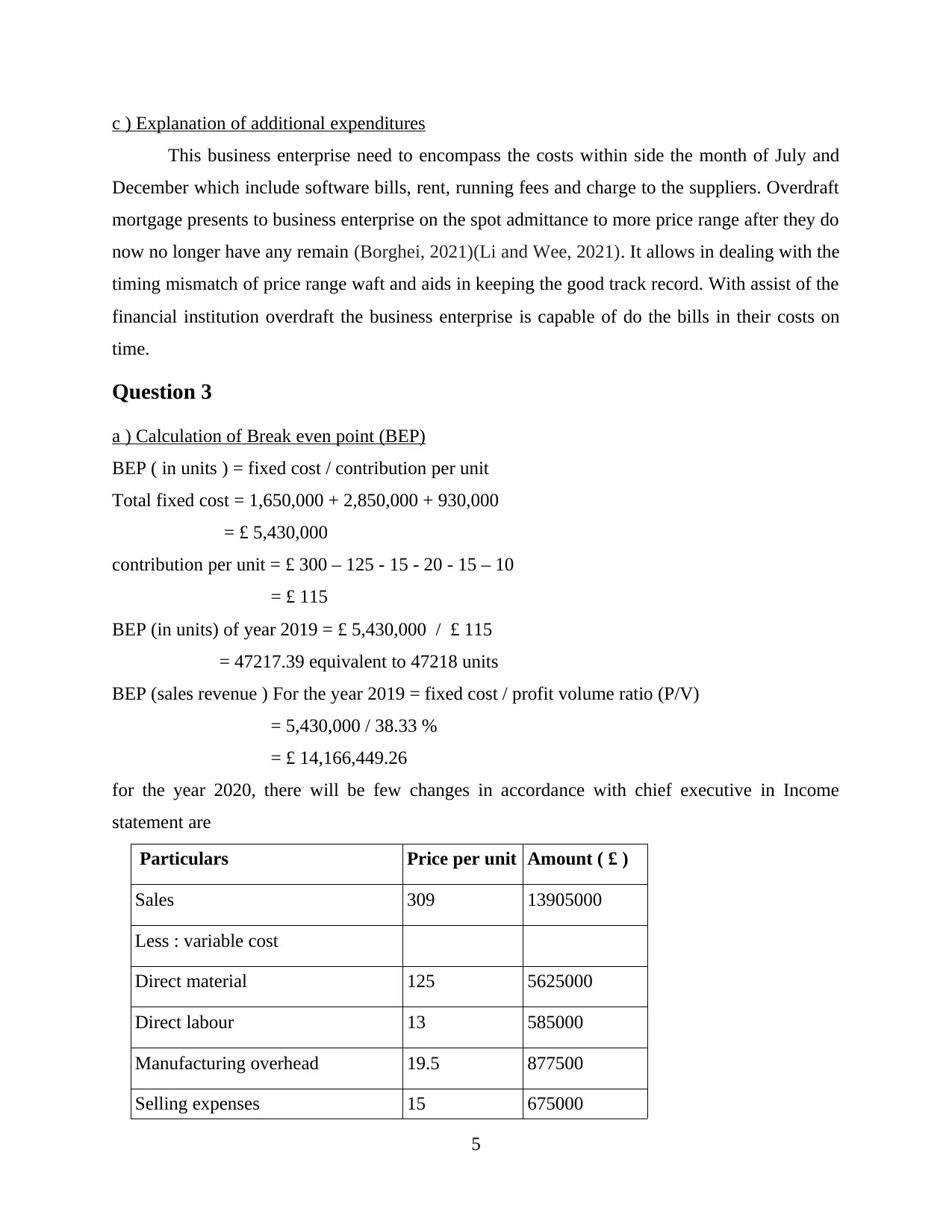

c ) Explanation of additional expenditures

This business enterprise need to encompass the costs within side the month of July and

December which include software bills, rent, running fees and charge to the suppliers. Overdraft

mortgage presents to business enterprise on the spot admittance to more price range after they do

now no longer have any remain (Borghei, 2021)(Li and Wee, 2021). It allows in dealing with the

timing mismatch of price range waft and aids in keeping the good track record. With assist of the

financial institution overdraft the business enterprise is capable of do the bills in their costs on

time.

Question 3

a ) Calculation of Break even point (BEP)

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (sales revenue ) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

5

This business enterprise need to encompass the costs within side the month of July and

December which include software bills, rent, running fees and charge to the suppliers. Overdraft

mortgage presents to business enterprise on the spot admittance to more price range after they do

now no longer have any remain (Borghei, 2021)(Li and Wee, 2021). It allows in dealing with the

timing mismatch of price range waft and aids in keeping the good track record. With assist of the

financial institution overdraft the business enterprise is capable of do the bills in their costs on

time.

Question 3

a ) Calculation of Break even point (BEP)

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (sales revenue ) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

5

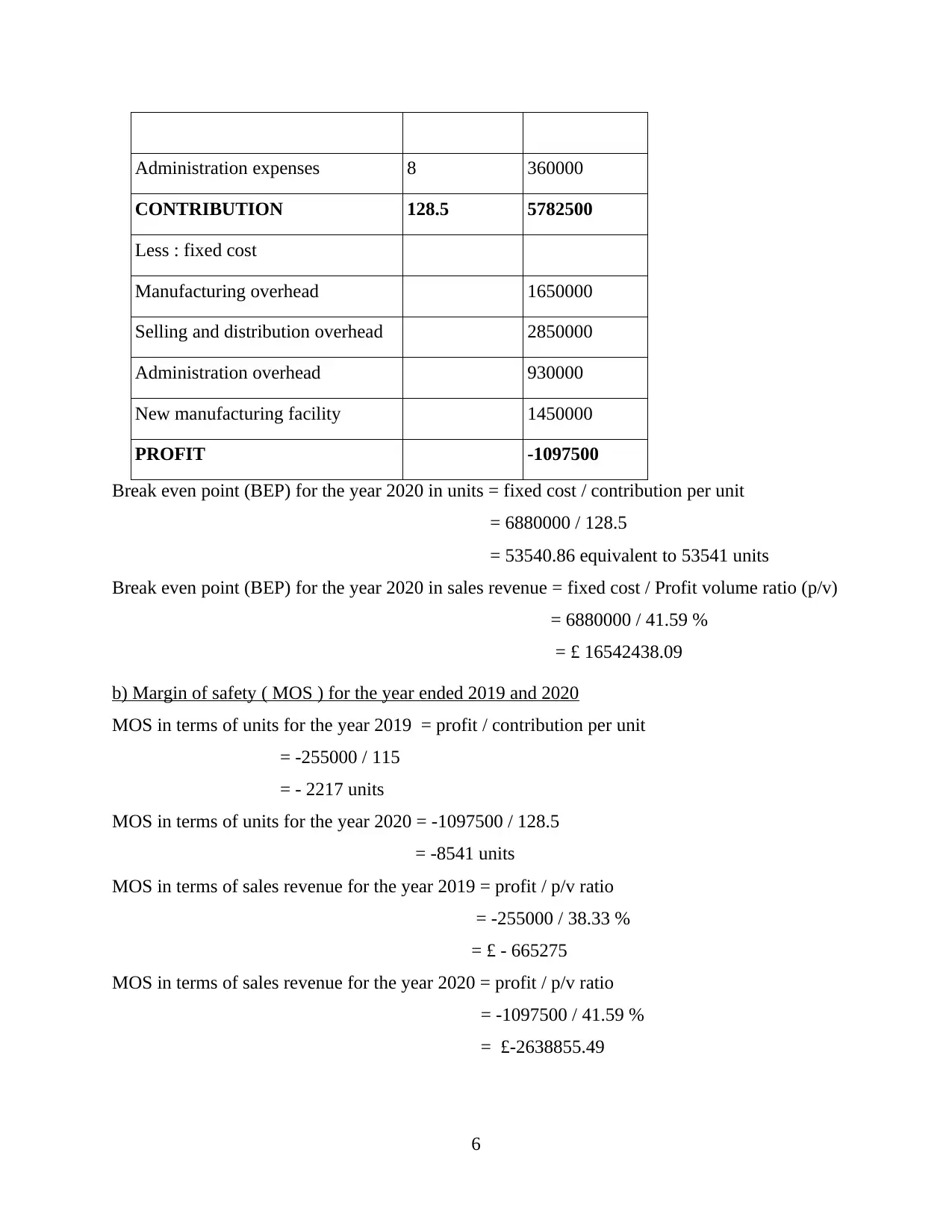

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

b) Margin of safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

= £-2638855.49

6

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

b) Margin of safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

= £-2638855.49

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

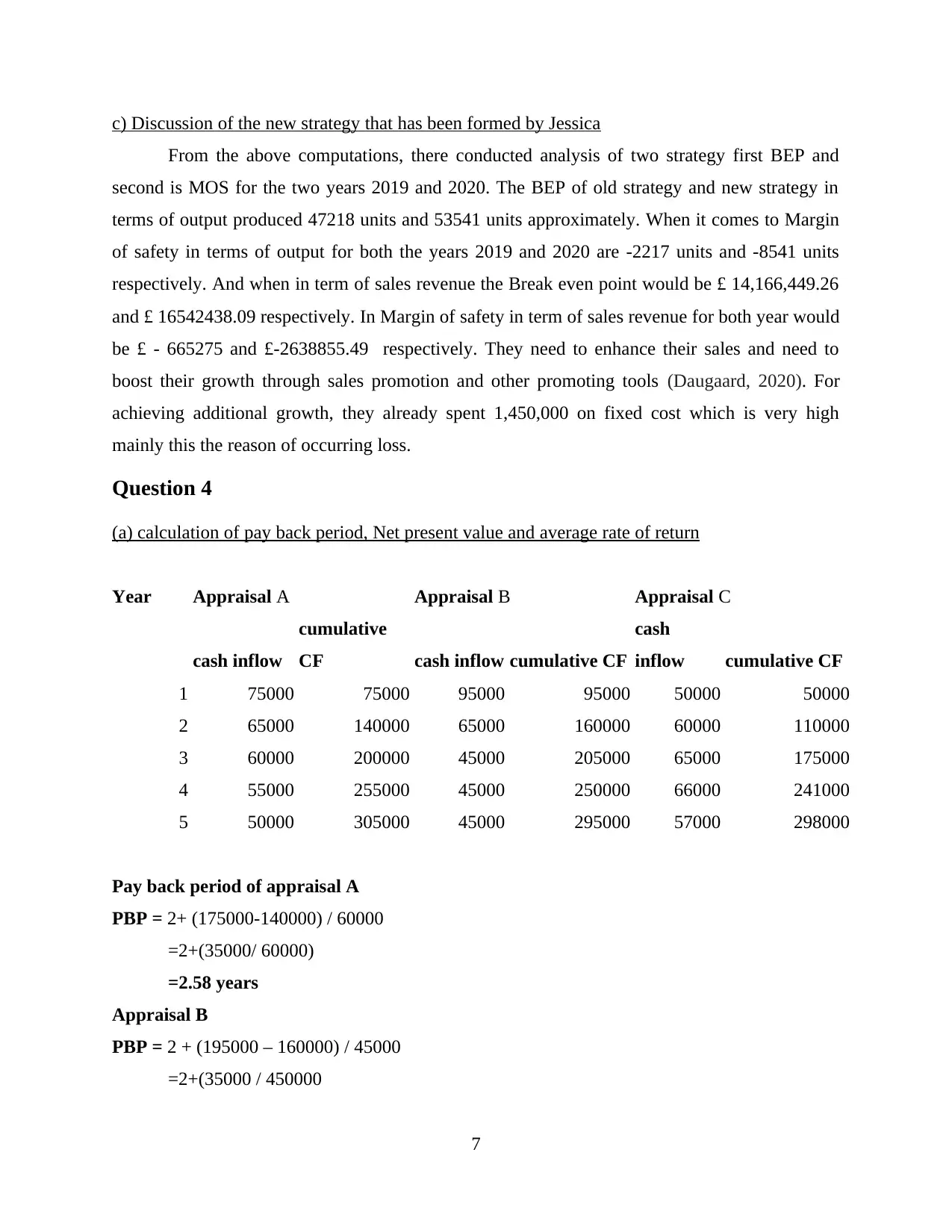

c) Discussion of the new strategy that has been formed by Jessica

From the above computations, there conducted analysis of two strategy first BEP and

second is MOS for the two years 2019 and 2020. The BEP of old strategy and new strategy in

terms of output produced 47218 units and 53541 units approximately. When it comes to Margin

of safety in terms of output for both the years 2019 and 2020 are -2217 units and -8541 units

respectively. And when in term of sales revenue the Break even point would be £ 14,166,449.26

and £ 16542438.09 respectively. In Margin of safety in term of sales revenue for both year would

be £ - 665275 and £-2638855.49 respectively. They need to enhance their sales and need to

boost their growth through sales promotion and other promoting tools (Daugaard, 2020). For

achieving additional growth, they already spent 1,450,000 on fixed cost which is very high

mainly this the reason of occurring loss.

Question 4

(a) calculation of pay back period, Net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

7

From the above computations, there conducted analysis of two strategy first BEP and

second is MOS for the two years 2019 and 2020. The BEP of old strategy and new strategy in

terms of output produced 47218 units and 53541 units approximately. When it comes to Margin

of safety in terms of output for both the years 2019 and 2020 are -2217 units and -8541 units

respectively. And when in term of sales revenue the Break even point would be £ 14,166,449.26

and £ 16542438.09 respectively. In Margin of safety in term of sales revenue for both year would

be £ - 665275 and £-2638855.49 respectively. They need to enhance their sales and need to

boost their growth through sales promotion and other promoting tools (Daugaard, 2020). For

achieving additional growth, they already spent 1,450,000 on fixed cost which is very high

mainly this the reason of occurring loss.

Question 4

(a) calculation of pay back period, Net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.77 years

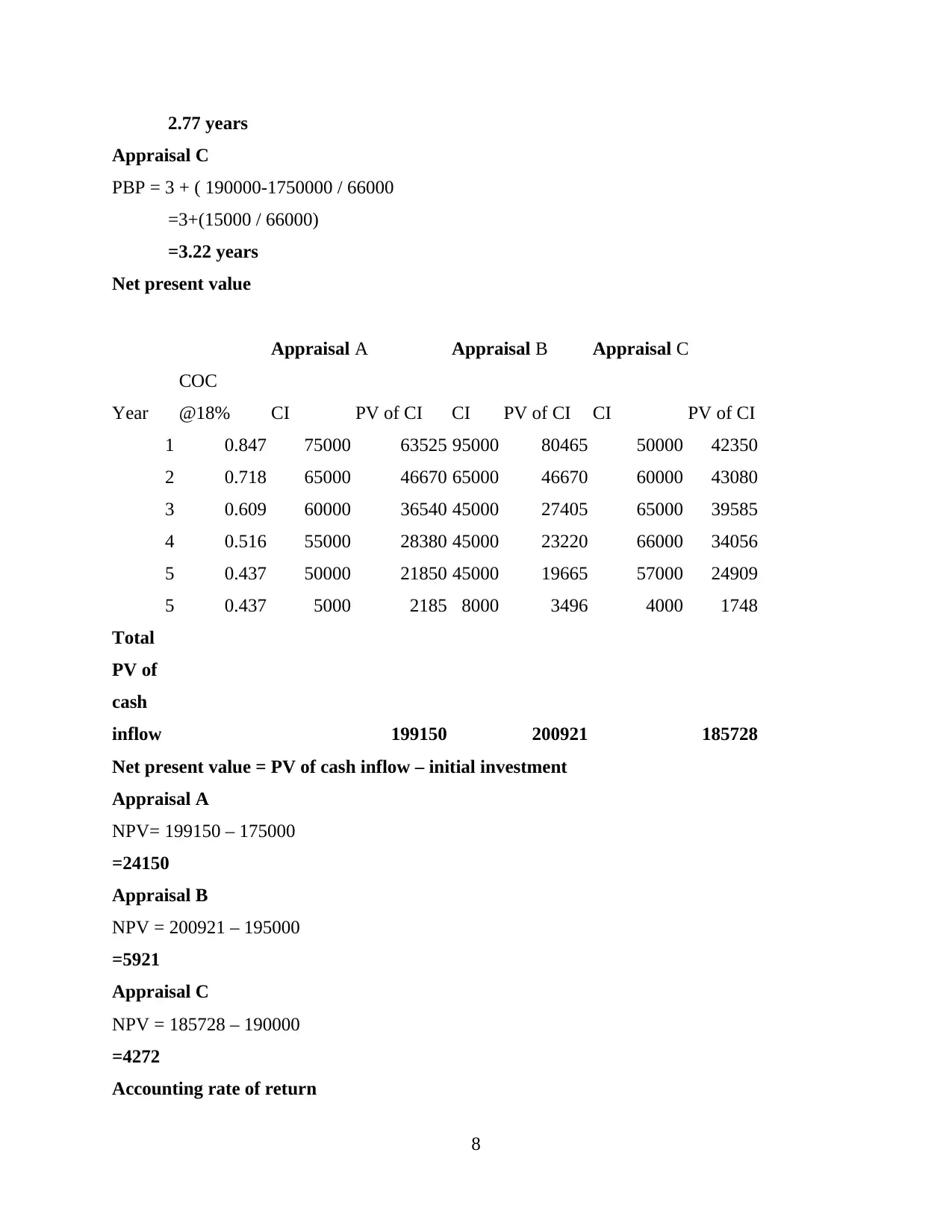

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

8

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

8

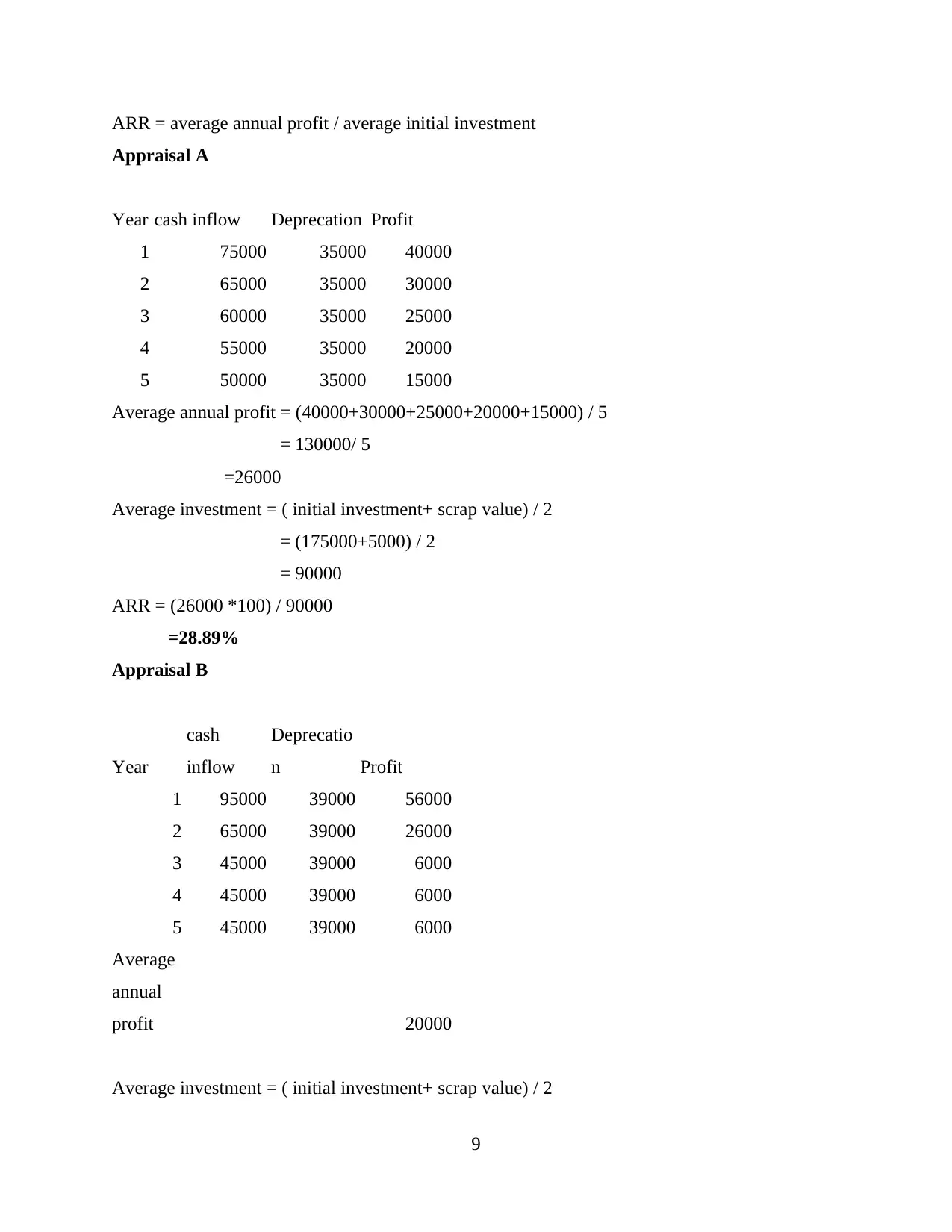

ARR = average annual profit / average initial investment

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Average investment = ( initial investment+ scrap value) / 2

9

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Average investment = ( initial investment+ scrap value) / 2

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.