Financial Statement Analysis Report: Comparative Study of T&L and DCG

VerifiedAdded on 2020/06/05

|22

|3808

|37

Report

AI Summary

This report presents a comprehensive financial statement analysis of Tate & Lyle Plc (T&L) and Dairy Crest Group (DCG) PLC, both operating in the Consumer Goods Food & Beverages sector. The analysis employs ratio analysis, including profitability, efficiency, liquidity, solvency, and investment ratios, to evaluate the companies' financial performance over a three-year period (2016-2017, including interim results for 2017). The report also incorporates SWOT and Porter's Five Forces analyses to provide a broader context. Key findings highlight trends in Return on Equity (ROE), Net Profit margin, Fixed Asset Turnover, Inventory Turnover, Current Ratio, Debt-Equity Ratio, and Earnings Per Share (EPS). The analysis reveals insights into each company's strengths, weaknesses, opportunities, and threats, offering a comparative assessment of their financial health and market position. Common size financial statement analysis and trend analysis are also included to support the financial evaluations.

Financial Statement Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. INTRODUCTION.......................................................................................................................1

1.1 Background of the company..................................................................................................1

1.2 Analysis of company’s position in the industry....................................................................1

1.3 Scope of the report.................................................................................................................2

1.4 Methodology..........................................................................................................................2

2. FINANCIAL STATEMENT ANALYSIS..................................................................................2

2.1 Background............................................................................................................................2

2.2 Business analysis...................................................................................................................3

2.3 Analysis of financial performance.........................................................................................4

Common size financial statement analysis................................................................................10

Trend analysis............................................................................................................................11

Altman Z score..........................................................................................................................13

CONCLUSION..............................................................................................................................14

RECOMMENDATIONS...............................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................18

1. Ratio analysis of Dairy Crest Group PLC.............................................................................18

2. Ratio analysis of Tate & Lyle Plc..........................................................................................19

1. INTRODUCTION.......................................................................................................................1

1.1 Background of the company..................................................................................................1

1.2 Analysis of company’s position in the industry....................................................................1

1.3 Scope of the report.................................................................................................................2

1.4 Methodology..........................................................................................................................2

2. FINANCIAL STATEMENT ANALYSIS..................................................................................2

2.1 Background............................................................................................................................2

2.2 Business analysis...................................................................................................................3

2.3 Analysis of financial performance.........................................................................................4

Common size financial statement analysis................................................................................10

Trend analysis............................................................................................................................11

Altman Z score..........................................................................................................................13

CONCLUSION..............................................................................................................................14

RECOMMENDATIONS...............................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................18

1. Ratio analysis of Dairy Crest Group PLC.............................................................................18

2. Ratio analysis of Tate & Lyle Plc..........................................................................................19

1. INTRODUCTION

1.1 Background of the company

On the basis of given case situation, two business units have been selected namely Tate &

Lyle Plc (T&L) and Dairy Crest Group (DCG) PLC. Both the companies are operating in the

sector of Consumer Goods Food & Beverages. Brief introduction of both such companies are

enumerated below:

T&L: It is none of the leading British based multinational agribusiness that lays high

level of emphasis on using innovative technology. By using unique technologies firm turns raw

material like corn, tapioca and oats into ingredients (Tate & Lyle plc (TATE), 2017). T&L is the

main constituent of FTSE 250 index and listed on recognized stock exchange of London.

DCG Plc: Such business unit provides customers with wide range of dairy products and

brands like cheese, Country life butter, Vitalite, Clover etc (Dairy Crest Group plc - Company

Profile, 2017). DCG also listed on London stock exchange and recognized as main element of

FTSE 250.

1.2 Analysis of company’s position in the industry

Bargaining power of buyers

Under F&B sector, bargaining power of buyers are

high because they prefer to purchase products or

services from the retailer who charges lower prices

and maintains better quality.

Bargaining power of suppliers

It is low due to the availability of large number of

suppliers. Hence, by purchasing quality product

from the suitable supplier business unit can

generate high margin.

Threat from substitutes

Company is facing threat from the companies

which are offering similar kind of products or

services. Hence, by making focus on the actual

need of customers T&T can cope with such issue

(Tate & Lyle Plc Porter Five Forces Analysis,

2017).

Threat from new entrants

Moderate level of threat exists in F&B sector in

relation to new entrants. Moreover, innovation and

stiff competition imposes threat in front of new

entrants.

1.1 Background of the company

On the basis of given case situation, two business units have been selected namely Tate &

Lyle Plc (T&L) and Dairy Crest Group (DCG) PLC. Both the companies are operating in the

sector of Consumer Goods Food & Beverages. Brief introduction of both such companies are

enumerated below:

T&L: It is none of the leading British based multinational agribusiness that lays high

level of emphasis on using innovative technology. By using unique technologies firm turns raw

material like corn, tapioca and oats into ingredients (Tate & Lyle plc (TATE), 2017). T&L is the

main constituent of FTSE 250 index and listed on recognized stock exchange of London.

DCG Plc: Such business unit provides customers with wide range of dairy products and

brands like cheese, Country life butter, Vitalite, Clover etc (Dairy Crest Group plc - Company

Profile, 2017). DCG also listed on London stock exchange and recognized as main element of

FTSE 250.

1.2 Analysis of company’s position in the industry

Bargaining power of buyers

Under F&B sector, bargaining power of buyers are

high because they prefer to purchase products or

services from the retailer who charges lower prices

and maintains better quality.

Bargaining power of suppliers

It is low due to the availability of large number of

suppliers. Hence, by purchasing quality product

from the suitable supplier business unit can

generate high margin.

Threat from substitutes

Company is facing threat from the companies

which are offering similar kind of products or

services. Hence, by making focus on the actual

need of customers T&T can cope with such issue

(Tate & Lyle Plc Porter Five Forces Analysis,

2017).

Threat from new entrants

Moderate level of threat exists in F&B sector in

relation to new entrants. Moreover, innovation and

stiff competition imposes threat in front of new

entrants.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Competitive rivalry

Intensity of rivalry is high under F&B sector which in turn directly impacts the profit margin of firm.

Moreover, for dealing with the highly competitive situation business unit has to decrease the level of

profit margin.

1.3 Scope of the report

Scope of the present report is wide which in turn provides information to the investors

about the extent to which monetary position of the concerned companies recognized as sound.

As it includes financial evaluation of T&L and DCG Plc for the latest 3 years period which

clearly shows the company prove to be fruitful from investment perspective.

1.4 Methodology

To evaluate financial position and performance of T&L and DCG Plc ratio analysis tool

has been selected as well as employed. It is one of the most effectual tools which help in

summarizing financial statements under different categories such as profitability, liquidity,

solvency, efficiency and investment. Along with this, tool of internal and external environmental

analysis such as Porter five forces & SWOT has also been undertaken to support the financial

evaluation of results. Hence, from the below mentioned sources data has been gathered by the

researcher.

Financial statements of T&L and DCG for the period of 3 years (2016, 2017, interim

results of 2017)

Books, journals and scholarly articles

2. FINANCIAL STATEMENT ANALYSIS

2.1 Background

In order to get quick indication about the financial position and performance of T&L in

against to the competitor such as DCG Plc ratio analysis tool has been employed. This in turn

helps in getting deeper insight about the level to which profitability, liquidity and solvency

position of T&L Plc is sound over others.

Intensity of rivalry is high under F&B sector which in turn directly impacts the profit margin of firm.

Moreover, for dealing with the highly competitive situation business unit has to decrease the level of

profit margin.

1.3 Scope of the report

Scope of the present report is wide which in turn provides information to the investors

about the extent to which monetary position of the concerned companies recognized as sound.

As it includes financial evaluation of T&L and DCG Plc for the latest 3 years period which

clearly shows the company prove to be fruitful from investment perspective.

1.4 Methodology

To evaluate financial position and performance of T&L and DCG Plc ratio analysis tool

has been selected as well as employed. It is one of the most effectual tools which help in

summarizing financial statements under different categories such as profitability, liquidity,

solvency, efficiency and investment. Along with this, tool of internal and external environmental

analysis such as Porter five forces & SWOT has also been undertaken to support the financial

evaluation of results. Hence, from the below mentioned sources data has been gathered by the

researcher.

Financial statements of T&L and DCG for the period of 3 years (2016, 2017, interim

results of 2017)

Books, journals and scholarly articles

2. FINANCIAL STATEMENT ANALYSIS

2.1 Background

In order to get quick indication about the financial position and performance of T&L in

against to the competitor such as DCG Plc ratio analysis tool has been employed. This in turn

helps in getting deeper insight about the level to which profitability, liquidity and solvency

position of T&L Plc is sound over others.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

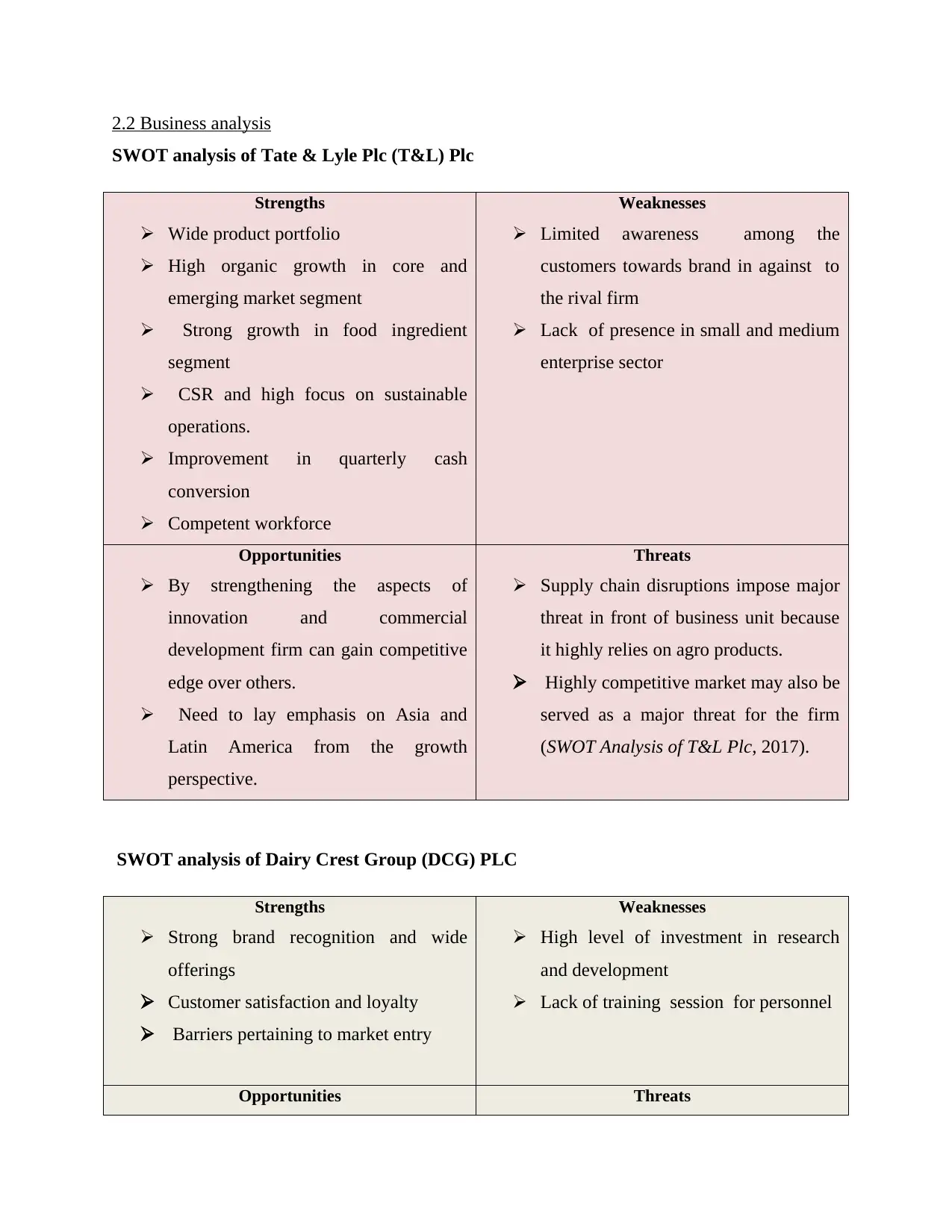

2.2 Business analysis

SWOT analysis of Tate & Lyle Plc (T&L) Plc

Strengths

Wide product portfolio

High organic growth in core and

emerging market segment

Strong growth in food ingredient

segment

CSR and high focus on sustainable

operations.

Improvement in quarterly cash

conversion

Competent workforce

Weaknesses

Limited awareness among the

customers towards brand in against to

the rival firm

Lack of presence in small and medium

enterprise sector

Opportunities

By strengthening the aspects of

innovation and commercial

development firm can gain competitive

edge over others.

Need to lay emphasis on Asia and

Latin America from the growth

perspective.

Threats

Supply chain disruptions impose major

threat in front of business unit because

it highly relies on agro products.

Highly competitive market may also be

served as a major threat for the firm

(SWOT Analysis of T&L Plc, 2017).

SWOT analysis of Dairy Crest Group (DCG) PLC

Strengths

Strong brand recognition and wide

offerings

Customer satisfaction and loyalty

Barriers pertaining to market entry

Weaknesses

High level of investment in research

and development

Lack of training session for personnel

Opportunities Threats

SWOT analysis of Tate & Lyle Plc (T&L) Plc

Strengths

Wide product portfolio

High organic growth in core and

emerging market segment

Strong growth in food ingredient

segment

CSR and high focus on sustainable

operations.

Improvement in quarterly cash

conversion

Competent workforce

Weaknesses

Limited awareness among the

customers towards brand in against to

the rival firm

Lack of presence in small and medium

enterprise sector

Opportunities

By strengthening the aspects of

innovation and commercial

development firm can gain competitive

edge over others.

Need to lay emphasis on Asia and

Latin America from the growth

perspective.

Threats

Supply chain disruptions impose major

threat in front of business unit because

it highly relies on agro products.

Highly competitive market may also be

served as a major threat for the firm

(SWOT Analysis of T&L Plc, 2017).

SWOT analysis of Dairy Crest Group (DCG) PLC

Strengths

Strong brand recognition and wide

offerings

Customer satisfaction and loyalty

Barriers pertaining to market entry

Weaknesses

High level of investment in research

and development

Lack of training session for personnel

Opportunities Threats

It needs to enter in global and new

markets through the means of

acquisition strategy

Growing economical aspect exhibits

growth opportunities in front of DCG

plc

Availability of competitors

Fluctuations in pricing and packaging

policy (Dairy Crest Group plc SWOT

Analysis, 2017)

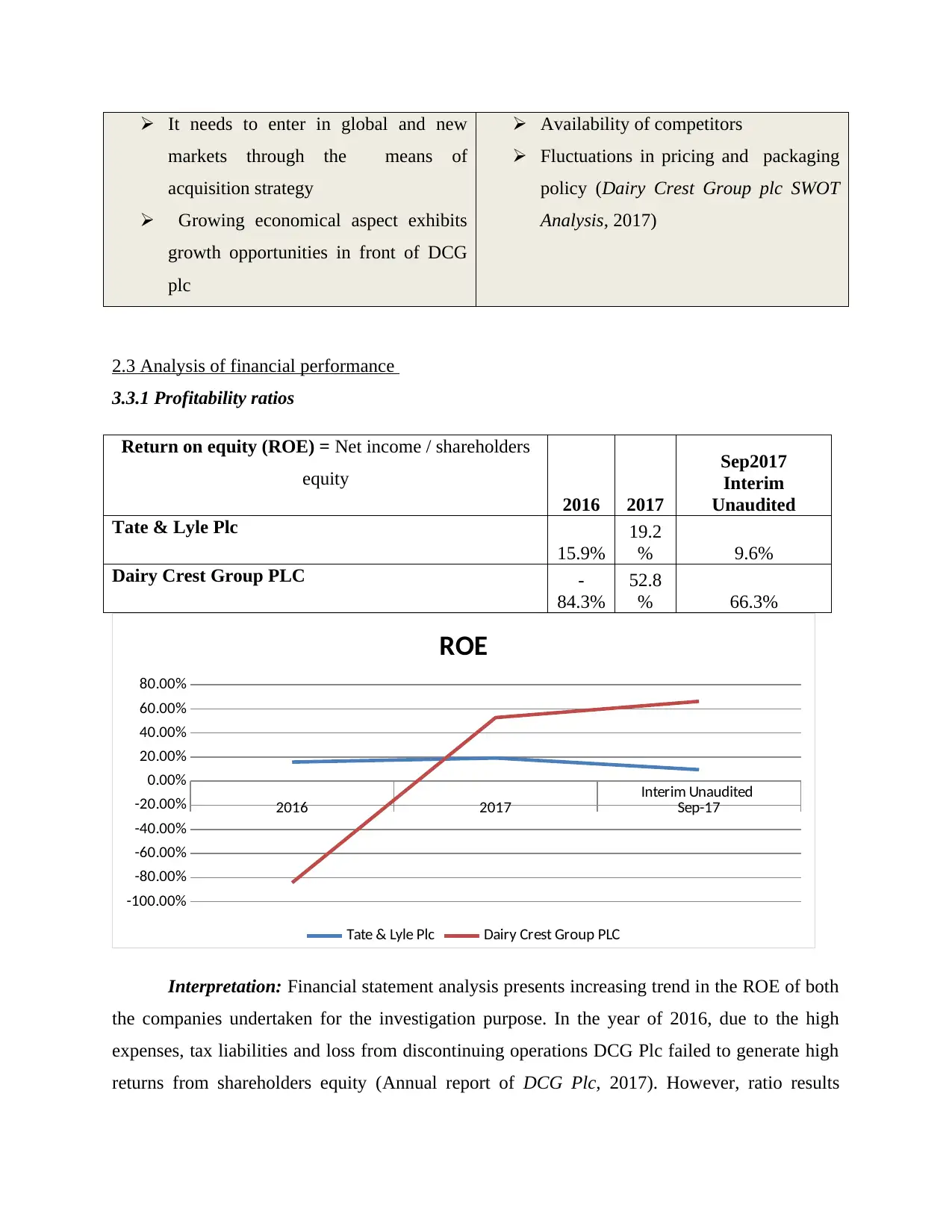

2.3 Analysis of financial performance

3.3.1 Profitability ratios

Return on equity (ROE) = Net income / shareholders

equity

2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc

15.9%

19.2

% 9.6%

Dairy Crest Group PLC -

84.3%

52.8

% 66.3%

Interim Unaudited

2016 2017 Sep-17

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

ROE

Tate & Lyle Plc Dairy Crest Group PLC

Interpretation: Financial statement analysis presents increasing trend in the ROE of both

the companies undertaken for the investigation purpose. In the year of 2016, due to the high

expenses, tax liabilities and loss from discontinuing operations DCG Plc failed to generate high

returns from shareholders equity (Annual report of DCG Plc, 2017). However, ratio results

markets through the means of

acquisition strategy

Growing economical aspect exhibits

growth opportunities in front of DCG

plc

Availability of competitors

Fluctuations in pricing and packaging

policy (Dairy Crest Group plc SWOT

Analysis, 2017)

2.3 Analysis of financial performance

3.3.1 Profitability ratios

Return on equity (ROE) = Net income / shareholders

equity

2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc

15.9%

19.2

% 9.6%

Dairy Crest Group PLC -

84.3%

52.8

% 66.3%

Interim Unaudited

2016 2017 Sep-17

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

ROE

Tate & Lyle Plc Dairy Crest Group PLC

Interpretation: Financial statement analysis presents increasing trend in the ROE of both

the companies undertaken for the investigation purpose. In the year of 2016, due to the high

expenses, tax liabilities and loss from discontinuing operations DCG Plc failed to generate high

returns from shareholders equity (Annual report of DCG Plc, 2017). However, ratio results

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pertaining to the year 2017 and interim period outcome shows that DCG Plc has used

shareholders fund in a prominent way as compared to T&L. Such financial results can clearly be

linked with SWOT analysis section which in turn exhibits that customers are highly aware from

the products of T&L Plc. Thus, it is one of the main reasons due to which T&L failed to generate

higher returns from funds invested by shareholders.

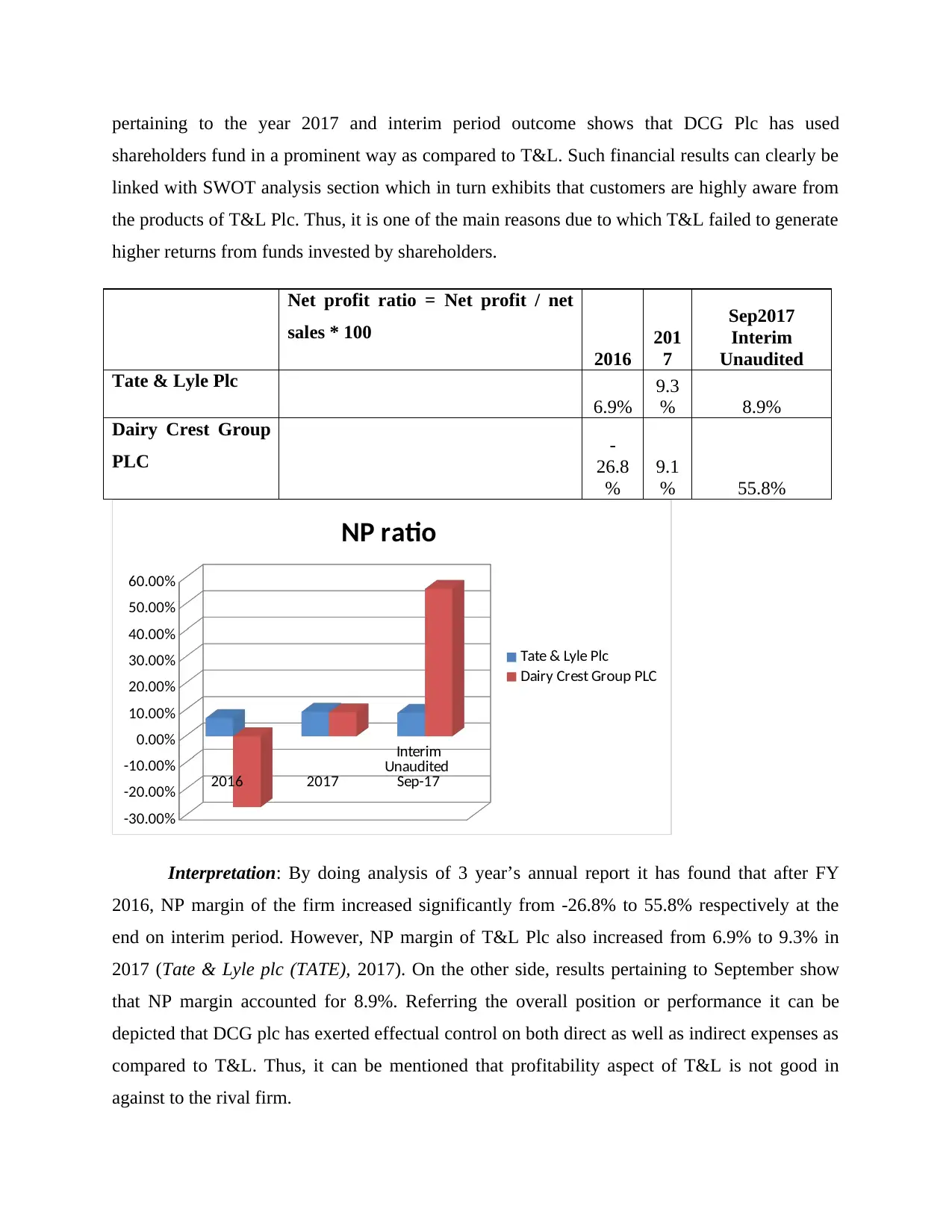

Net profit ratio = Net profit / net

sales * 100

2016

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc

6.9%

9.3

% 8.9%

Dairy Crest Group

PLC -

26.8

%

9.1

% 55.8%

Interim

Unaudited

2016 2017 Sep-17

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

NP ratio

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: By doing analysis of 3 year’s annual report it has found that after FY

2016, NP margin of the firm increased significantly from -26.8% to 55.8% respectively at the

end on interim period. However, NP margin of T&L Plc also increased from 6.9% to 9.3% in

2017 (Tate & Lyle plc (TATE), 2017). On the other side, results pertaining to September show

that NP margin accounted for 8.9%. Referring the overall position or performance it can be

depicted that DCG plc has exerted effectual control on both direct as well as indirect expenses as

compared to T&L. Thus, it can be mentioned that profitability aspect of T&L is not good in

against to the rival firm.

shareholders fund in a prominent way as compared to T&L. Such financial results can clearly be

linked with SWOT analysis section which in turn exhibits that customers are highly aware from

the products of T&L Plc. Thus, it is one of the main reasons due to which T&L failed to generate

higher returns from funds invested by shareholders.

Net profit ratio = Net profit / net

sales * 100

2016

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc

6.9%

9.3

% 8.9%

Dairy Crest Group

PLC -

26.8

%

9.1

% 55.8%

Interim

Unaudited

2016 2017 Sep-17

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

NP ratio

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: By doing analysis of 3 year’s annual report it has found that after FY

2016, NP margin of the firm increased significantly from -26.8% to 55.8% respectively at the

end on interim period. However, NP margin of T&L Plc also increased from 6.9% to 9.3% in

2017 (Tate & Lyle plc (TATE), 2017). On the other side, results pertaining to September show

that NP margin accounted for 8.9%. Referring the overall position or performance it can be

depicted that DCG plc has exerted effectual control on both direct as well as indirect expenses as

compared to T&L. Thus, it can be mentioned that profitability aspect of T&L is not good in

against to the rival firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

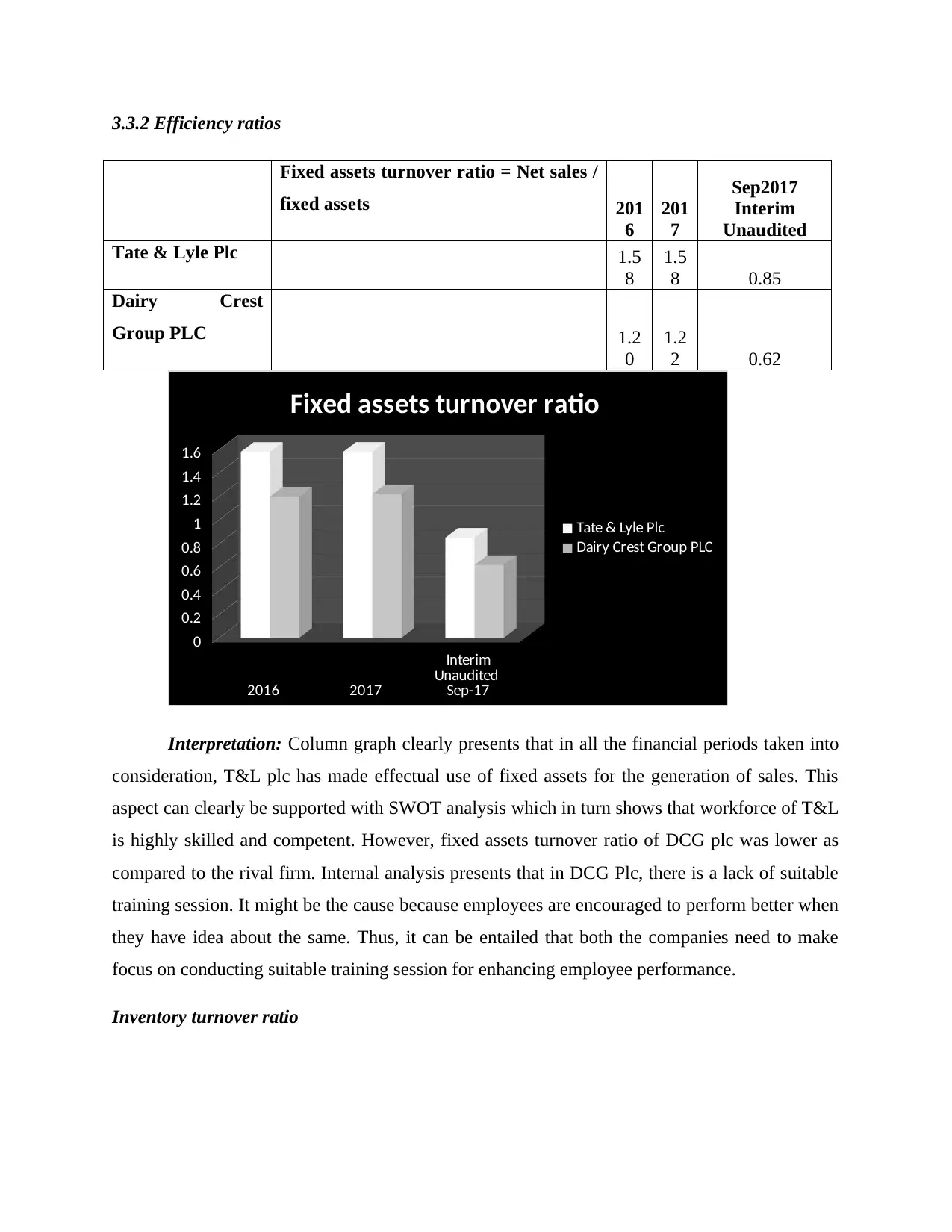

3.3.2 Efficiency ratios

Fixed assets turnover ratio = Net sales /

fixed assets 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 1.5

8

1.5

8 0.85

Dairy Crest

Group PLC 1.2

0

1.2

2 0.62

Interim

Unaudited

2016 2017 Sep-17

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Fixed assets turnover ratio

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: Column graph clearly presents that in all the financial periods taken into

consideration, T&L plc has made effectual use of fixed assets for the generation of sales. This

aspect can clearly be supported with SWOT analysis which in turn shows that workforce of T&L

is highly skilled and competent. However, fixed assets turnover ratio of DCG plc was lower as

compared to the rival firm. Internal analysis presents that in DCG Plc, there is a lack of suitable

training session. It might be the cause because employees are encouraged to perform better when

they have idea about the same. Thus, it can be entailed that both the companies need to make

focus on conducting suitable training session for enhancing employee performance.

Inventory turnover ratio

Fixed assets turnover ratio = Net sales /

fixed assets 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 1.5

8

1.5

8 0.85

Dairy Crest

Group PLC 1.2

0

1.2

2 0.62

Interim

Unaudited

2016 2017 Sep-17

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Fixed assets turnover ratio

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: Column graph clearly presents that in all the financial periods taken into

consideration, T&L plc has made effectual use of fixed assets for the generation of sales. This

aspect can clearly be supported with SWOT analysis which in turn shows that workforce of T&L

is highly skilled and competent. However, fixed assets turnover ratio of DCG plc was lower as

compared to the rival firm. Internal analysis presents that in DCG Plc, there is a lack of suitable

training session. It might be the cause because employees are encouraged to perform better when

they have idea about the same. Thus, it can be entailed that both the companies need to make

focus on conducting suitable training session for enhancing employee performance.

Inventory turnover ratio

Inventory turnover ratio = Net sales /

fixed assets 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.0

0

0.5

8 0.00

Dairy Crest Group

PLC 2.0

5

1.9

9 1.16

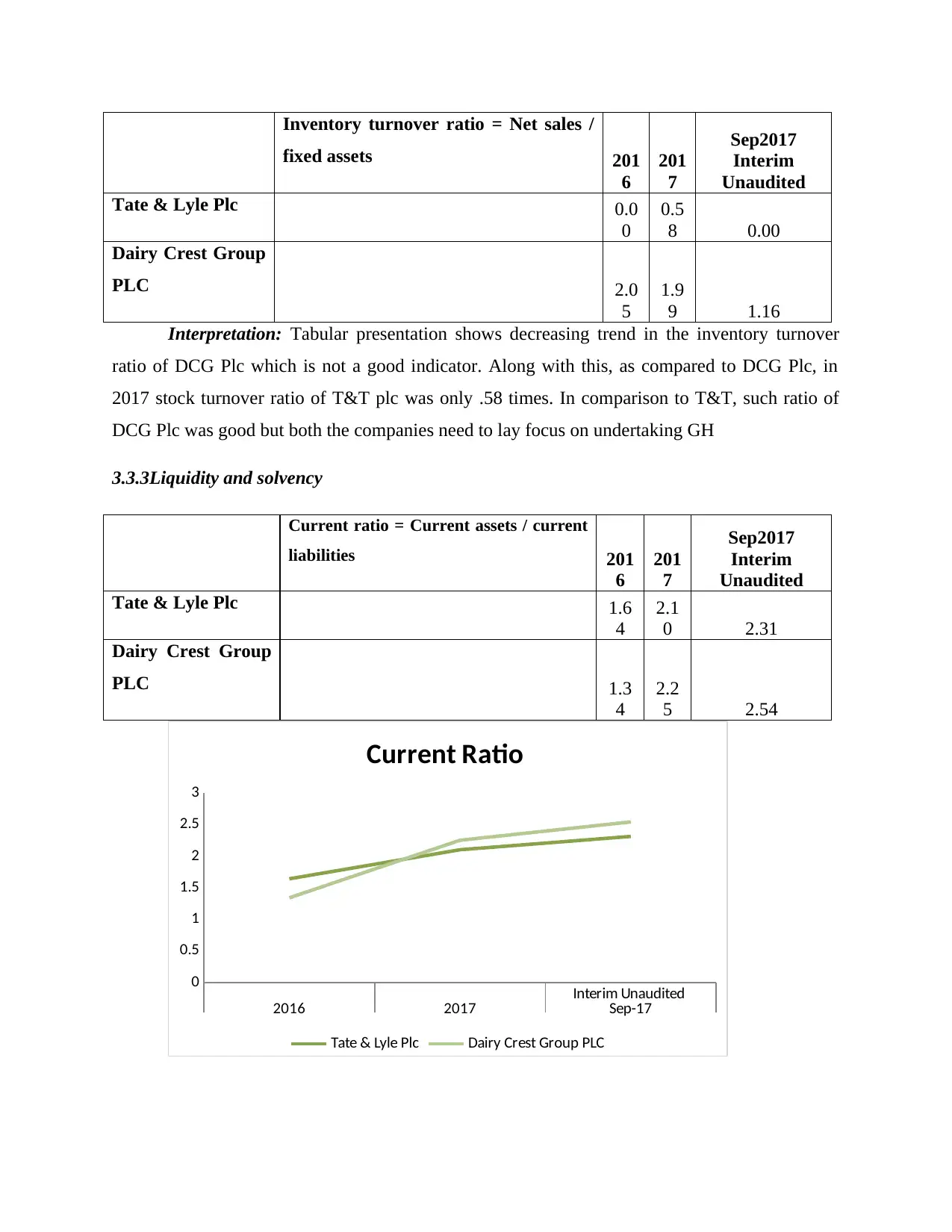

Interpretation: Tabular presentation shows decreasing trend in the inventory turnover

ratio of DCG Plc which is not a good indicator. Along with this, as compared to DCG Plc, in

2017 stock turnover ratio of T&T plc was only .58 times. In comparison to T&T, such ratio of

DCG Plc was good but both the companies need to lay focus on undertaking GH

3.3.3Liquidity and solvency

Current ratio = Current assets / current

liabilities 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 1.6

4

2.1

0 2.31

Dairy Crest Group

PLC 1.3

4

2.2

5 2.54

Interim Unaudited

2016 2017 Sep-17

0

0.5

1

1.5

2

2.5

3

Current Ratio

Tate & Lyle Plc Dairy Crest Group PLC

fixed assets 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.0

0

0.5

8 0.00

Dairy Crest Group

PLC 2.0

5

1.9

9 1.16

Interpretation: Tabular presentation shows decreasing trend in the inventory turnover

ratio of DCG Plc which is not a good indicator. Along with this, as compared to DCG Plc, in

2017 stock turnover ratio of T&T plc was only .58 times. In comparison to T&T, such ratio of

DCG Plc was good but both the companies need to lay focus on undertaking GH

3.3.3Liquidity and solvency

Current ratio = Current assets / current

liabilities 201

6

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 1.6

4

2.1

0 2.31

Dairy Crest Group

PLC 1.3

4

2.2

5 2.54

Interim Unaudited

2016 2017 Sep-17

0

0.5

1

1.5

2

2.5

3

Current Ratio

Tate & Lyle Plc Dairy Crest Group PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

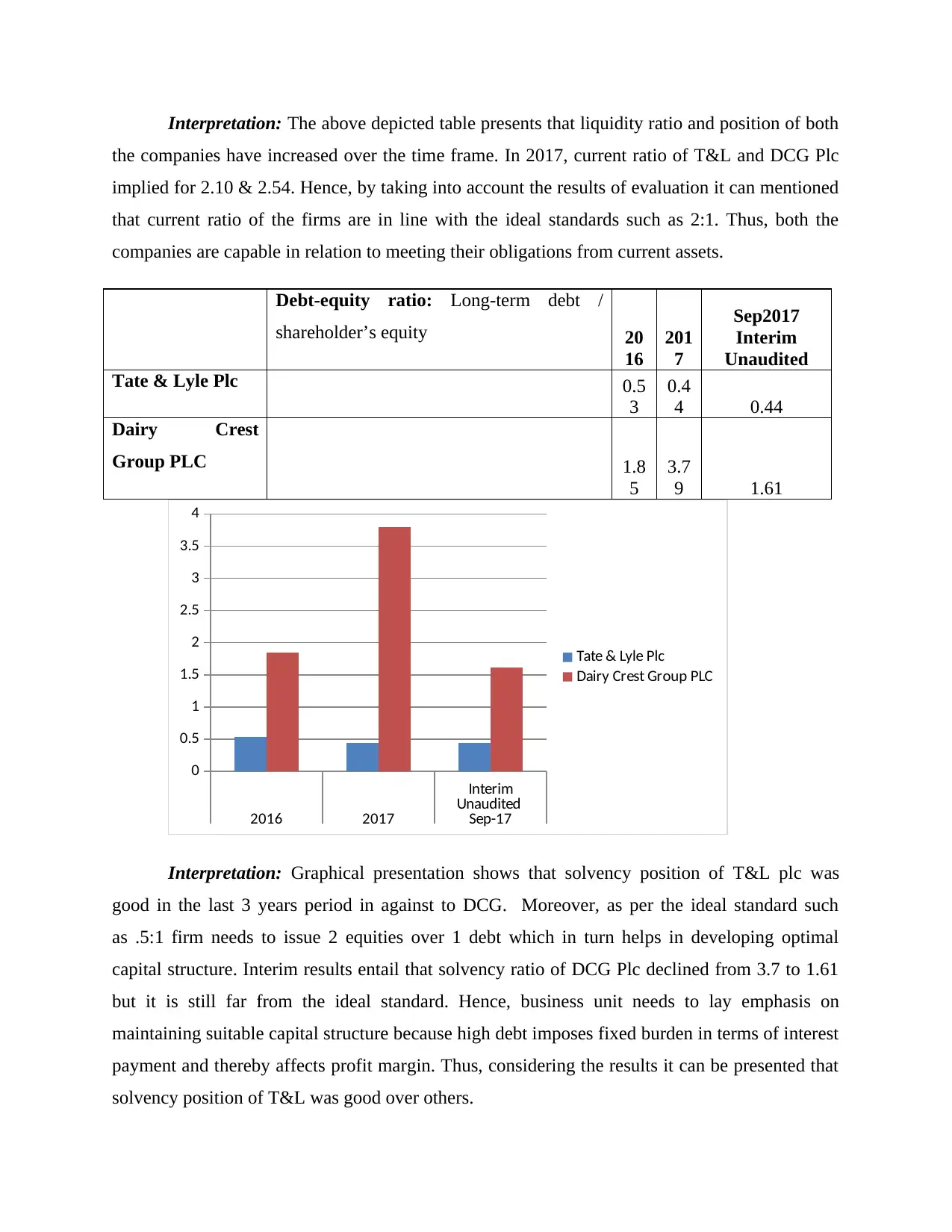

Interpretation: The above depicted table presents that liquidity ratio and position of both

the companies have increased over the time frame. In 2017, current ratio of T&L and DCG Plc

implied for 2.10 & 2.54. Hence, by taking into account the results of evaluation it can mentioned

that current ratio of the firms are in line with the ideal standards such as 2:1. Thus, both the

companies are capable in relation to meeting their obligations from current assets.

Debt-equity ratio: Long-term debt /

shareholder’s equity 20

16

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.5

3

0.4

4 0.44

Dairy Crest

Group PLC 1.8

5

3.7

9 1.61

Interim

Unaudited

2016 2017 Sep-17

0

0.5

1

1.5

2

2.5

3

3.5

4

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: Graphical presentation shows that solvency position of T&L plc was

good in the last 3 years period in against to DCG. Moreover, as per the ideal standard such

as .5:1 firm needs to issue 2 equities over 1 debt which in turn helps in developing optimal

capital structure. Interim results entail that solvency ratio of DCG Plc declined from 3.7 to 1.61

but it is still far from the ideal standard. Hence, business unit needs to lay emphasis on

maintaining suitable capital structure because high debt imposes fixed burden in terms of interest

payment and thereby affects profit margin. Thus, considering the results it can be presented that

solvency position of T&L was good over others.

the companies have increased over the time frame. In 2017, current ratio of T&L and DCG Plc

implied for 2.10 & 2.54. Hence, by taking into account the results of evaluation it can mentioned

that current ratio of the firms are in line with the ideal standards such as 2:1. Thus, both the

companies are capable in relation to meeting their obligations from current assets.

Debt-equity ratio: Long-term debt /

shareholder’s equity 20

16

201

7

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.5

3

0.4

4 0.44

Dairy Crest

Group PLC 1.8

5

3.7

9 1.61

Interim

Unaudited

2016 2017 Sep-17

0

0.5

1

1.5

2

2.5

3

3.5

4

Tate & Lyle Plc

Dairy Crest Group PLC

Interpretation: Graphical presentation shows that solvency position of T&L plc was

good in the last 3 years period in against to DCG. Moreover, as per the ideal standard such

as .5:1 firm needs to issue 2 equities over 1 debt which in turn helps in developing optimal

capital structure. Interim results entail that solvency ratio of DCG Plc declined from 3.7 to 1.61

but it is still far from the ideal standard. Hence, business unit needs to lay emphasis on

maintaining suitable capital structure because high debt imposes fixed burden in terms of interest

payment and thereby affects profit margin. Thus, considering the results it can be presented that

solvency position of T&L was good over others.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

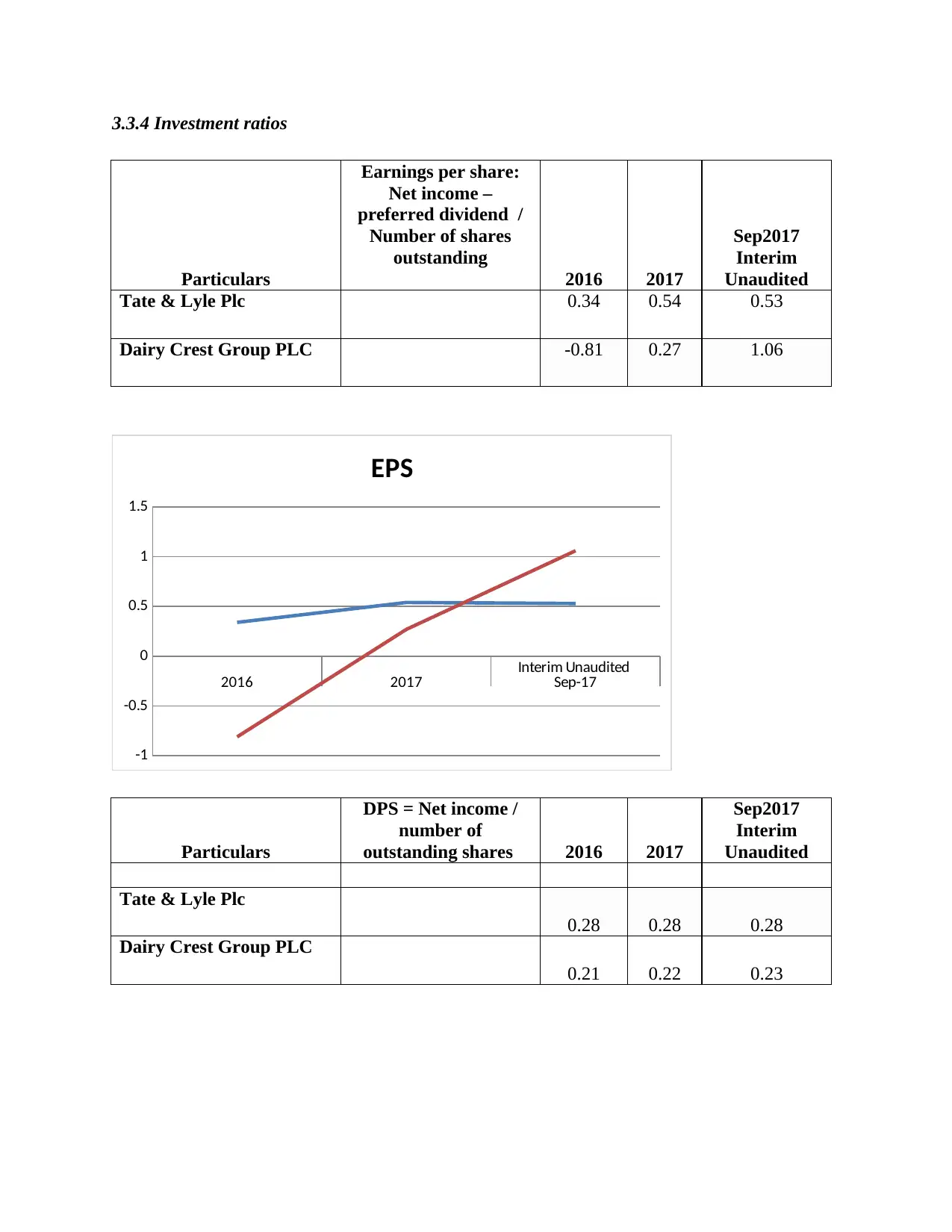

3.3.4 Investment ratios

Particulars

Earnings per share:

Net income –

preferred dividend /

Number of shares

outstanding

2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.34 0.54 0.53

Dairy Crest Group PLC -0.81 0.27 1.06

Interim Unaudited

2016 2017 Sep-17

-1

-0.5

0

0.5

1

1.5

EPS

Particulars

DPS = Net income /

number of

outstanding shares 2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc

0.28 0.28 0.28

Dairy Crest Group PLC

0.21 0.22 0.23

Particulars

Earnings per share:

Net income –

preferred dividend /

Number of shares

outstanding

2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc 0.34 0.54 0.53

Dairy Crest Group PLC -0.81 0.27 1.06

Interim Unaudited

2016 2017 Sep-17

-1

-0.5

0

0.5

1

1.5

EPS

Particulars

DPS = Net income /

number of

outstanding shares 2016 2017

Sep2017

Interim

Unaudited

Tate & Lyle Plc

0.28 0.28 0.28

Dairy Crest Group PLC

0.21 0.22 0.23

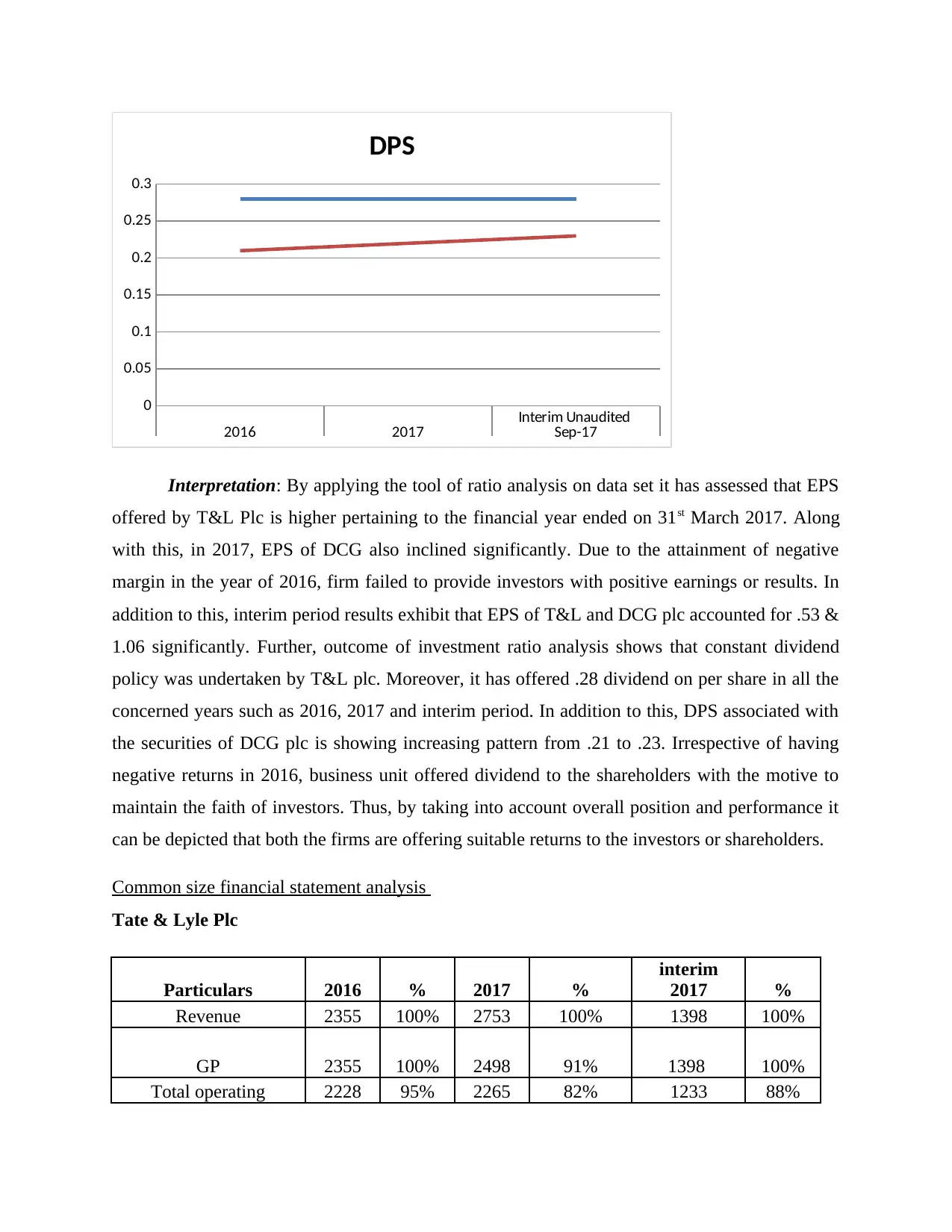

Interim Unaudited

2016 2017 Sep-17

0

0.05

0.1

0.15

0.2

0.25

0.3

DPS

Interpretation: By applying the tool of ratio analysis on data set it has assessed that EPS

offered by T&L Plc is higher pertaining to the financial year ended on 31st March 2017. Along

with this, in 2017, EPS of DCG also inclined significantly. Due to the attainment of negative

margin in the year of 2016, firm failed to provide investors with positive earnings or results. In

addition to this, interim period results exhibit that EPS of T&L and DCG plc accounted for .53 &

1.06 significantly. Further, outcome of investment ratio analysis shows that constant dividend

policy was undertaken by T&L plc. Moreover, it has offered .28 dividend on per share in all the

concerned years such as 2016, 2017 and interim period. In addition to this, DPS associated with

the securities of DCG plc is showing increasing pattern from .21 to .23. Irrespective of having

negative returns in 2016, business unit offered dividend to the shareholders with the motive to

maintain the faith of investors. Thus, by taking into account overall position and performance it

can be depicted that both the firms are offering suitable returns to the investors or shareholders.

Common size financial statement analysis

Tate & Lyle Plc

Particulars 2016 % 2017 %

interim

2017 %

Revenue 2355 100% 2753 100% 1398 100%

GP 2355 100% 2498 91% 1398 100%

Total operating 2228 95% 2265 82% 1233 88%

2016 2017 Sep-17

0

0.05

0.1

0.15

0.2

0.25

0.3

DPS

Interpretation: By applying the tool of ratio analysis on data set it has assessed that EPS

offered by T&L Plc is higher pertaining to the financial year ended on 31st March 2017. Along

with this, in 2017, EPS of DCG also inclined significantly. Due to the attainment of negative

margin in the year of 2016, firm failed to provide investors with positive earnings or results. In

addition to this, interim period results exhibit that EPS of T&L and DCG plc accounted for .53 &

1.06 significantly. Further, outcome of investment ratio analysis shows that constant dividend

policy was undertaken by T&L plc. Moreover, it has offered .28 dividend on per share in all the

concerned years such as 2016, 2017 and interim period. In addition to this, DPS associated with

the securities of DCG plc is showing increasing pattern from .21 to .23. Irrespective of having

negative returns in 2016, business unit offered dividend to the shareholders with the motive to

maintain the faith of investors. Thus, by taking into account overall position and performance it

can be depicted that both the firms are offering suitable returns to the investors or shareholders.

Common size financial statement analysis

Tate & Lyle Plc

Particulars 2016 % 2017 %

interim

2017 %

Revenue 2355 100% 2753 100% 1398 100%

GP 2355 100% 2498 91% 1398 100%

Total operating 2228 95% 2265 82% 1233 88%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.