Comprehensive Financial Decision Making Report: Roast Ltd. Analysis

VerifiedAdded on 2023/01/17

|17

|4611

|35

Report

AI Summary

This report provides a comprehensive financial analysis of Roast Ltd., an independent coffee house chain operating in the UK. The analysis begins with an industry review of the UK beverage sector, highlighting key players and market trends. The core of the report focuses on the analysis of financial statements, including the statement of profit or loss, statement of financial position (balance sheet), and statement of cash flows for the years 2017 and 2018. Various financial ratios, such as gross profit ratio, net profit ratio, operating profit ratio, current ratio, quick ratio, debt-to-equity ratio, and return on capital employed, are calculated and interpreted to assess the company's performance, profitability, and financial stability. Furthermore, the report explores investment appraisal techniques and discusses potential sources of funding for Roast Ltd., offering insights into its financial decision-making processes and strategic planning. The analysis reveals the company's growth and profitability trends, providing valuable information for stakeholders and decision-makers.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Industry Review..........................................................................................................................1

PART 2............................................................................................................................................2

2.1 Statement of profit or loss.....................................................................................................2

2.2 Statement of financial position..............................................................................................4

2.3 Statement of cash Flows........................................................................................................6

PART 3............................................................................................................................................9

3.1 Investment appraisal..............................................................................................................9

3.2 Sources of fund...................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Industry Review..........................................................................................................................1

PART 2............................................................................................................................................2

2.1 Statement of profit or loss.....................................................................................................2

2.2 Statement of financial position..............................................................................................4

2.3 Statement of cash Flows........................................................................................................6

PART 3............................................................................................................................................9

3.1 Investment appraisal..............................................................................................................9

3.2 Sources of fund...................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making includes the process which is related to the formulation of

future strategies that help the organisation in attainment of sustainable growth opportunities. It is

the duty of the management of each organisation to formulate the strategies that are optimum in

nature for the attainment of development in business operations. After the formulation of

effective decisions, attention is provided by the management towards the analysis of financial

situation and position. The different documents upon which focus is provided in this process

includes balance sheet, P&L account and cash flow statements. There effective analysis help to

ascertain the actual status of an organisation along with their presence in market. This is report

is based upon Roast Ltd. It is an independent coffee house chain and having its operations in UK.

This organisation is founded in year 2008. The main aim of this report is about consideration of

different financial documents to build effective decision making (Bond, Edmans and Goldstein,

2012).

This report covers various topics such as industry review, analysis of financial statements

along with their attached balance sheet, cash flow and profit and loss account. Also, analysis is

done in respect to the investment appraisal techniques along sources of funds.

PART 1

Industry Review

The beverage industry of UK is very big in nature and having significant contribution in

the economy of UK. The different aspects along with information that contributes in the

determination of industry situation are presented below in different points:

The overall contribution of this industry in the GDP of UK is around 3.7 billion pound in

the year 2017.

In the year 2018 noticed that the overall development in beverage industry is around

7.9%.

The main organisations that have significant operations in this industry includes Costa

Coffee, Starbucks, Cafe Nero, Cafe2U, Soho Coffee, AMT Coffee, Coffee republic etc

(Major players in coffee house industry of UK. 2019).

The best opportunity present in this industry is about expansion of business over such

locations where still have no operations are established related to coffee business. This

1

Financial decision making includes the process which is related to the formulation of

future strategies that help the organisation in attainment of sustainable growth opportunities. It is

the duty of the management of each organisation to formulate the strategies that are optimum in

nature for the attainment of development in business operations. After the formulation of

effective decisions, attention is provided by the management towards the analysis of financial

situation and position. The different documents upon which focus is provided in this process

includes balance sheet, P&L account and cash flow statements. There effective analysis help to

ascertain the actual status of an organisation along with their presence in market. This is report

is based upon Roast Ltd. It is an independent coffee house chain and having its operations in UK.

This organisation is founded in year 2008. The main aim of this report is about consideration of

different financial documents to build effective decision making (Bond, Edmans and Goldstein,

2012).

This report covers various topics such as industry review, analysis of financial statements

along with their attached balance sheet, cash flow and profit and loss account. Also, analysis is

done in respect to the investment appraisal techniques along sources of funds.

PART 1

Industry Review

The beverage industry of UK is very big in nature and having significant contribution in

the economy of UK. The different aspects along with information that contributes in the

determination of industry situation are presented below in different points:

The overall contribution of this industry in the GDP of UK is around 3.7 billion pound in

the year 2017.

In the year 2018 noticed that the overall development in beverage industry is around

7.9%.

The main organisations that have significant operations in this industry includes Costa

Coffee, Starbucks, Cafe Nero, Cafe2U, Soho Coffee, AMT Coffee, Coffee republic etc

(Major players in coffee house industry of UK. 2019).

The best opportunity present in this industry is about expansion of business over such

locations where still have no operations are established related to coffee business. This

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will provides an option to all the existing businesses in this sector to expand their

operations and grab the opportunities present in market.

Lot of challenges are present in the beverage industry that has to be faced by the

organisation operating in this sector. The first challenge about inclusion of different type

of drinks in market that have direct impact over the business and market share. Secondly,

the perception of consumers where they focus over consumption of healthy drinks. In this

case, this will have direct impact over their operations (Carraher and Van Auken, 2013).

PART 2

2.1 Statement of profit or loss

Profit and loss statement is prepared by the organisation for the determination of the

amount of profit and loss at the end of year. This is the part of final accounts and presented in

front of the internal external stakeholders. This will have huge contribution in respect to the

ascertain of actual and real information related to the profitability and position of organisation in

market. This is majorly used by the different kind of personnels includes creditors, suppliers,

customers, investors. It help in building their decision making ability more profound. The

different respective in respect to which decision is taken includes providence of credit,

investment, supply and buy of goods etc. Roast Ltd. is the coffee house that having its operations

in UK. From the analysis of the profit and loss account of the organisation ascertained that the

sales attained in the year 2017 is 2022 but the figure is increased in the year 2018 and attained

the figure of 2534. This represented that organisation is in growing stage and able to generate

higher amount of sales in the year 2018. The direct impact of the same is ascertained over the

cost of goods sold which is also increased and attain the mark of 1990 in 2018 which is just 1505

in the year 2017. The amount of gross profit is also increased in year 2018. This is determined

with the help of its comparative analysis of the accounts of the year 2017. The amount of gross

profit in year 2017 is 517 whereas in the year 2018 is 544. At end, profit and loss determined for

2017 and 2018 is as 36 and 81. This depicts that the profitability of organisation is high in year

2018 in comparison to 2017 (Hershey, Austin and Gutierrez, H. 2015). The different ratios are

calculated for the purpose of analysing the performance of organisation. All these ratios are

presented below:

2

operations and grab the opportunities present in market.

Lot of challenges are present in the beverage industry that has to be faced by the

organisation operating in this sector. The first challenge about inclusion of different type

of drinks in market that have direct impact over the business and market share. Secondly,

the perception of consumers where they focus over consumption of healthy drinks. In this

case, this will have direct impact over their operations (Carraher and Van Auken, 2013).

PART 2

2.1 Statement of profit or loss

Profit and loss statement is prepared by the organisation for the determination of the

amount of profit and loss at the end of year. This is the part of final accounts and presented in

front of the internal external stakeholders. This will have huge contribution in respect to the

ascertain of actual and real information related to the profitability and position of organisation in

market. This is majorly used by the different kind of personnels includes creditors, suppliers,

customers, investors. It help in building their decision making ability more profound. The

different respective in respect to which decision is taken includes providence of credit,

investment, supply and buy of goods etc. Roast Ltd. is the coffee house that having its operations

in UK. From the analysis of the profit and loss account of the organisation ascertained that the

sales attained in the year 2017 is 2022 but the figure is increased in the year 2018 and attained

the figure of 2534. This represented that organisation is in growing stage and able to generate

higher amount of sales in the year 2018. The direct impact of the same is ascertained over the

cost of goods sold which is also increased and attain the mark of 1990 in 2018 which is just 1505

in the year 2017. The amount of gross profit is also increased in year 2018. This is determined

with the help of its comparative analysis of the accounts of the year 2017. The amount of gross

profit in year 2017 is 517 whereas in the year 2018 is 544. At end, profit and loss determined for

2017 and 2018 is as 36 and 81. This depicts that the profitability of organisation is high in year

2018 in comparison to 2017 (Hershey, Austin and Gutierrez, H. 2015). The different ratios are

calculated for the purpose of analysing the performance of organisation. All these ratios are

presented below:

2

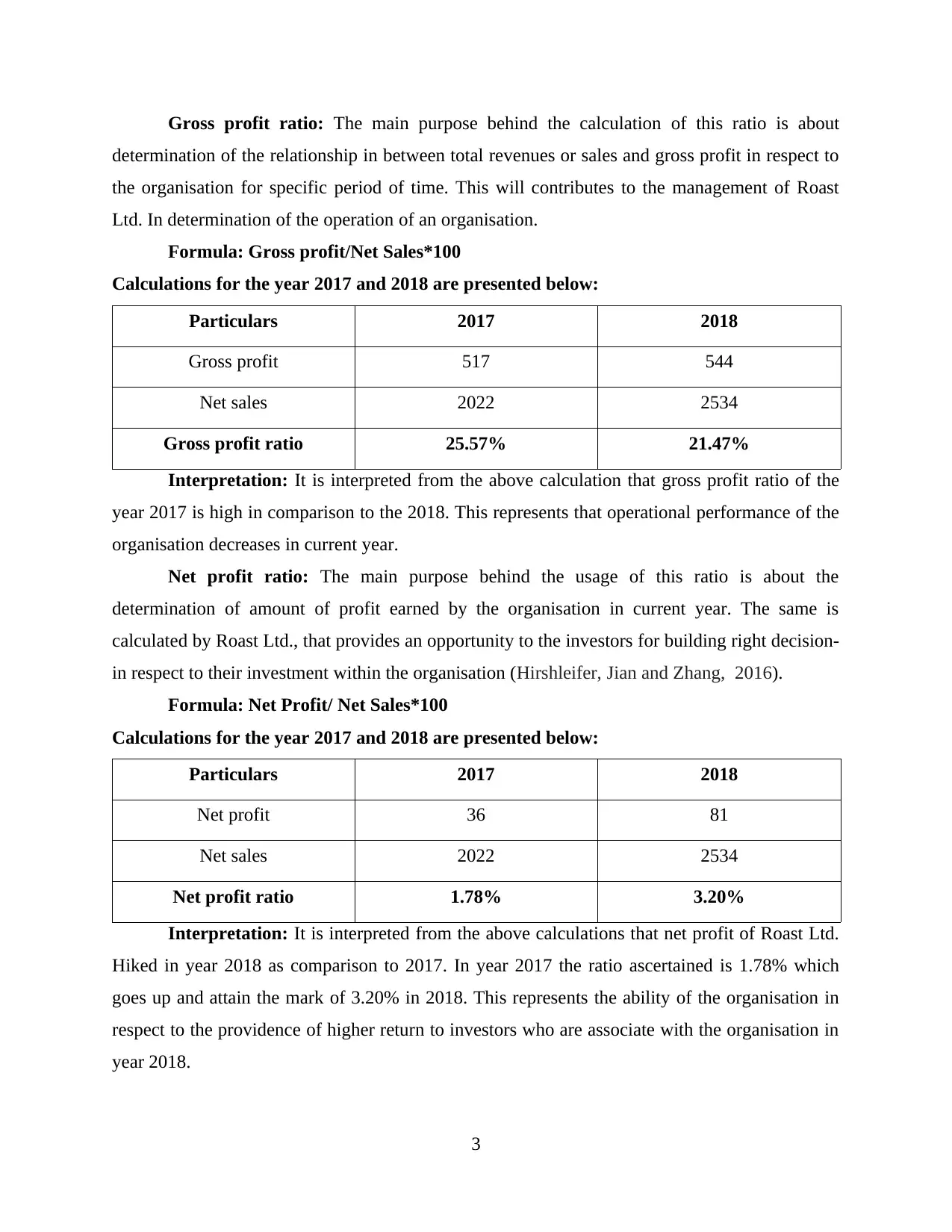

Gross profit ratio: The main purpose behind the calculation of this ratio is about

determination of the relationship in between total revenues or sales and gross profit in respect to

the organisation for specific period of time. This will contributes to the management of Roast

Ltd. In determination of the operation of an organisation.

Formula: Gross profit/Net Sales*100

Calculations for the year 2017 and 2018 are presented below:

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit ratio 25.57% 21.47%

Interpretation: It is interpreted from the above calculation that gross profit ratio of the

year 2017 is high in comparison to the 2018. This represents that operational performance of the

organisation decreases in current year.

Net profit ratio: The main purpose behind the usage of this ratio is about the

determination of amount of profit earned by the organisation in current year. The same is

calculated by Roast Ltd., that provides an opportunity to the investors for building right decision-

in respect to their investment within the organisation (Hirshleifer, Jian and Zhang, 2016).

Formula: Net Profit/ Net Sales*100

Calculations for the year 2017 and 2018 are presented below:

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

Interpretation: It is interpreted from the above calculations that net profit of Roast Ltd.

Hiked in year 2018 as comparison to 2017. In year 2017 the ratio ascertained is 1.78% which

goes up and attain the mark of 3.20% in 2018. This represents the ability of the organisation in

respect to the providence of higher return to investors who are associate with the organisation in

year 2018.

3

determination of the relationship in between total revenues or sales and gross profit in respect to

the organisation for specific period of time. This will contributes to the management of Roast

Ltd. In determination of the operation of an organisation.

Formula: Gross profit/Net Sales*100

Calculations for the year 2017 and 2018 are presented below:

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit ratio 25.57% 21.47%

Interpretation: It is interpreted from the above calculation that gross profit ratio of the

year 2017 is high in comparison to the 2018. This represents that operational performance of the

organisation decreases in current year.

Net profit ratio: The main purpose behind the usage of this ratio is about the

determination of amount of profit earned by the organisation in current year. The same is

calculated by Roast Ltd., that provides an opportunity to the investors for building right decision-

in respect to their investment within the organisation (Hirshleifer, Jian and Zhang, 2016).

Formula: Net Profit/ Net Sales*100

Calculations for the year 2017 and 2018 are presented below:

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

Interpretation: It is interpreted from the above calculations that net profit of Roast Ltd.

Hiked in year 2018 as comparison to 2017. In year 2017 the ratio ascertained is 1.78% which

goes up and attain the mark of 3.20% in 2018. This represents the ability of the organisation in

respect to the providence of higher return to investors who are associate with the organisation in

year 2018.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

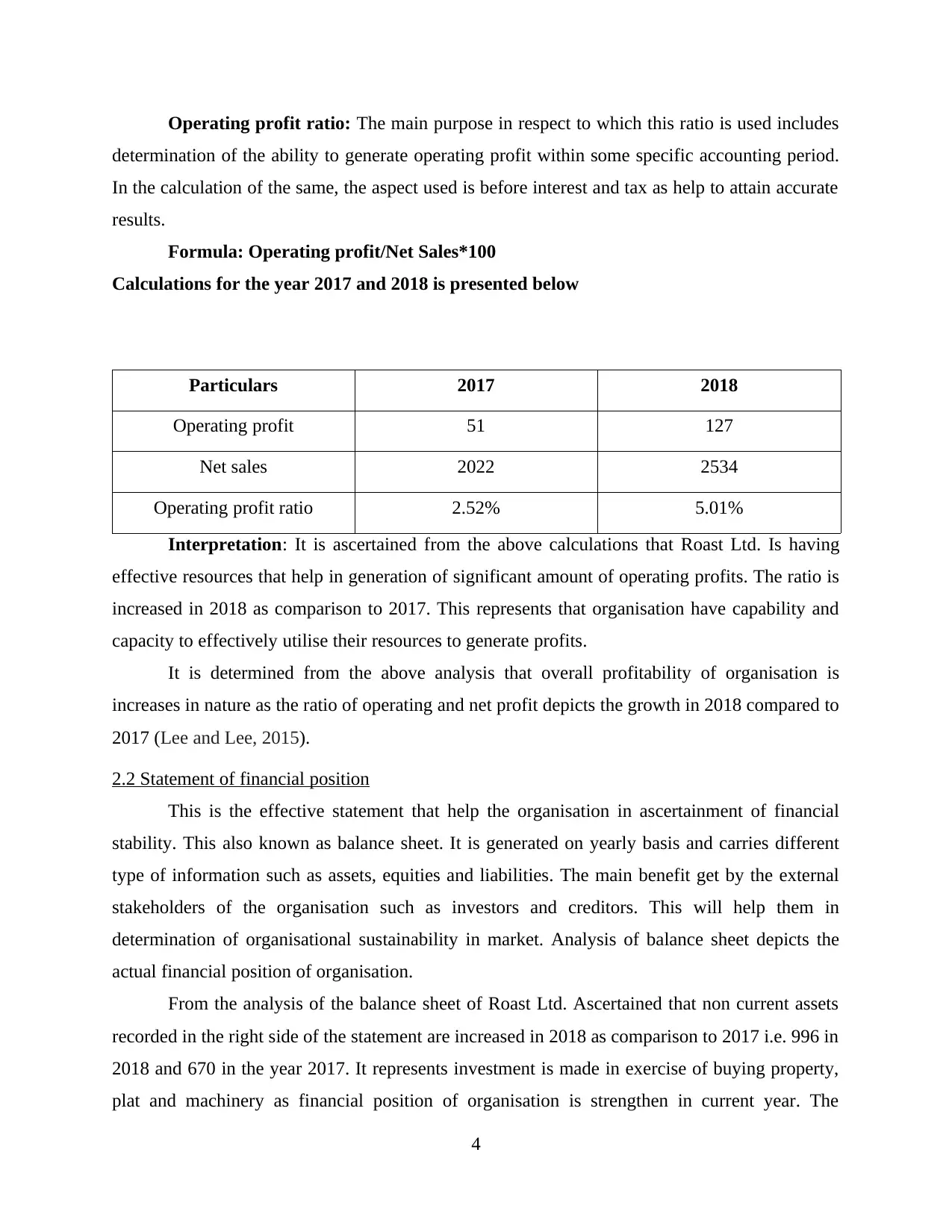

Operating profit ratio: The main purpose in respect to which this ratio is used includes

determination of the ability to generate operating profit within some specific accounting period.

In the calculation of the same, the aspect used is before interest and tax as help to attain accurate

results.

Formula: Operating profit/Net Sales*100

Calculations for the year 2017 and 2018 is presented below

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

Interpretation: It is ascertained from the above calculations that Roast Ltd. Is having

effective resources that help in generation of significant amount of operating profits. The ratio is

increased in 2018 as comparison to 2017. This represents that organisation have capability and

capacity to effectively utilise their resources to generate profits.

It is determined from the above analysis that overall profitability of organisation is

increases in nature as the ratio of operating and net profit depicts the growth in 2018 compared to

2017 (Lee and Lee, 2015).

2.2 Statement of financial position

This is the effective statement that help the organisation in ascertainment of financial

stability. This also known as balance sheet. It is generated on yearly basis and carries different

type of information such as assets, equities and liabilities. The main benefit get by the external

stakeholders of the organisation such as investors and creditors. This will help them in

determination of organisational sustainability in market. Analysis of balance sheet depicts the

actual financial position of organisation.

From the analysis of the balance sheet of Roast Ltd. Ascertained that non current assets

recorded in the right side of the statement are increased in 2018 as comparison to 2017 i.e. 996 in

2018 and 670 in the year 2017. It represents investment is made in exercise of buying property,

plat and machinery as financial position of organisation is strengthen in current year. The

4

determination of the ability to generate operating profit within some specific accounting period.

In the calculation of the same, the aspect used is before interest and tax as help to attain accurate

results.

Formula: Operating profit/Net Sales*100

Calculations for the year 2017 and 2018 is presented below

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

Interpretation: It is ascertained from the above calculations that Roast Ltd. Is having

effective resources that help in generation of significant amount of operating profits. The ratio is

increased in 2018 as comparison to 2017. This represents that organisation have capability and

capacity to effectively utilise their resources to generate profits.

It is determined from the above analysis that overall profitability of organisation is

increases in nature as the ratio of operating and net profit depicts the growth in 2018 compared to

2017 (Lee and Lee, 2015).

2.2 Statement of financial position

This is the effective statement that help the organisation in ascertainment of financial

stability. This also known as balance sheet. It is generated on yearly basis and carries different

type of information such as assets, equities and liabilities. The main benefit get by the external

stakeholders of the organisation such as investors and creditors. This will help them in

determination of organisational sustainability in market. Analysis of balance sheet depicts the

actual financial position of organisation.

From the analysis of the balance sheet of Roast Ltd. Ascertained that non current assets

recorded in the right side of the statement are increased in 2018 as comparison to 2017 i.e. 996 in

2018 and 670 in the year 2017. It represents investment is made in exercise of buying property,

plat and machinery as financial position of organisation is strengthen in current year. The

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

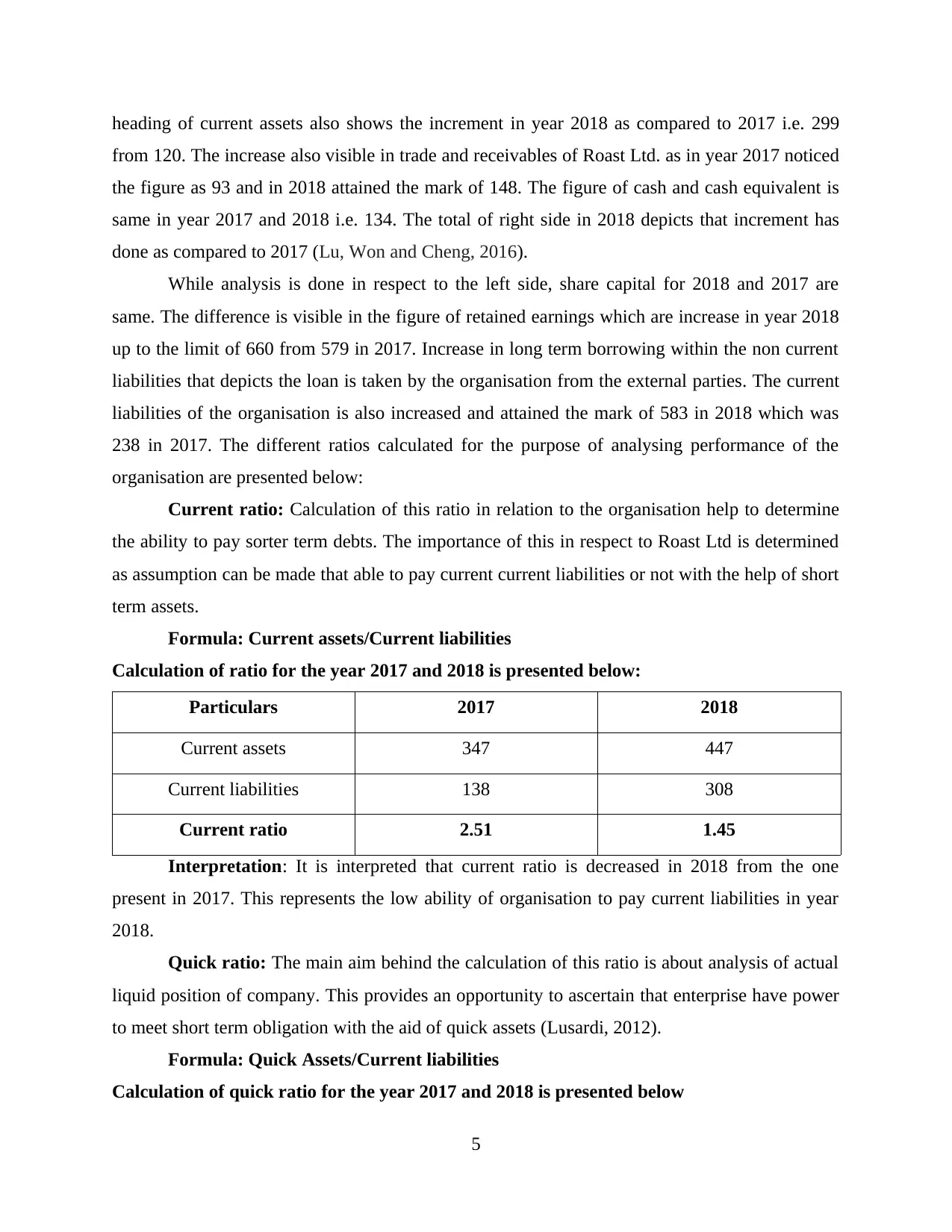

heading of current assets also shows the increment in year 2018 as compared to 2017 i.e. 299

from 120. The increase also visible in trade and receivables of Roast Ltd. as in year 2017 noticed

the figure as 93 and in 2018 attained the mark of 148. The figure of cash and cash equivalent is

same in year 2017 and 2018 i.e. 134. The total of right side in 2018 depicts that increment has

done as compared to 2017 (Lu, Won and Cheng, 2016).

While analysis is done in respect to the left side, share capital for 2018 and 2017 are

same. The difference is visible in the figure of retained earnings which are increase in year 2018

up to the limit of 660 from 579 in 2017. Increase in long term borrowing within the non current

liabilities that depicts the loan is taken by the organisation from the external parties. The current

liabilities of the organisation is also increased and attained the mark of 583 in 2018 which was

238 in 2017. The different ratios calculated for the purpose of analysing performance of the

organisation are presented below:

Current ratio: Calculation of this ratio in relation to the organisation help to determine

the ability to pay sorter term debts. The importance of this in respect to Roast Ltd is determined

as assumption can be made that able to pay current current liabilities or not with the help of short

term assets.

Formula: Current assets/Current liabilities

Calculation of ratio for the year 2017 and 2018 is presented below:

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 1.45

Interpretation: It is interpreted that current ratio is decreased in 2018 from the one

present in 2017. This represents the low ability of organisation to pay current liabilities in year

2018.

Quick ratio: The main aim behind the calculation of this ratio is about analysis of actual

liquid position of company. This provides an opportunity to ascertain that enterprise have power

to meet short term obligation with the aid of quick assets (Lusardi, 2012).

Formula: Quick Assets/Current liabilities

Calculation of quick ratio for the year 2017 and 2018 is presented below

5

from 120. The increase also visible in trade and receivables of Roast Ltd. as in year 2017 noticed

the figure as 93 and in 2018 attained the mark of 148. The figure of cash and cash equivalent is

same in year 2017 and 2018 i.e. 134. The total of right side in 2018 depicts that increment has

done as compared to 2017 (Lu, Won and Cheng, 2016).

While analysis is done in respect to the left side, share capital for 2018 and 2017 are

same. The difference is visible in the figure of retained earnings which are increase in year 2018

up to the limit of 660 from 579 in 2017. Increase in long term borrowing within the non current

liabilities that depicts the loan is taken by the organisation from the external parties. The current

liabilities of the organisation is also increased and attained the mark of 583 in 2018 which was

238 in 2017. The different ratios calculated for the purpose of analysing performance of the

organisation are presented below:

Current ratio: Calculation of this ratio in relation to the organisation help to determine

the ability to pay sorter term debts. The importance of this in respect to Roast Ltd is determined

as assumption can be made that able to pay current current liabilities or not with the help of short

term assets.

Formula: Current assets/Current liabilities

Calculation of ratio for the year 2017 and 2018 is presented below:

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 1.45

Interpretation: It is interpreted that current ratio is decreased in 2018 from the one

present in 2017. This represents the low ability of organisation to pay current liabilities in year

2018.

Quick ratio: The main aim behind the calculation of this ratio is about analysis of actual

liquid position of company. This provides an opportunity to ascertain that enterprise have power

to meet short term obligation with the aid of quick assets (Lusardi, 2012).

Formula: Quick Assets/Current liabilities

Calculation of quick ratio for the year 2017 and 2018 is presented below

5

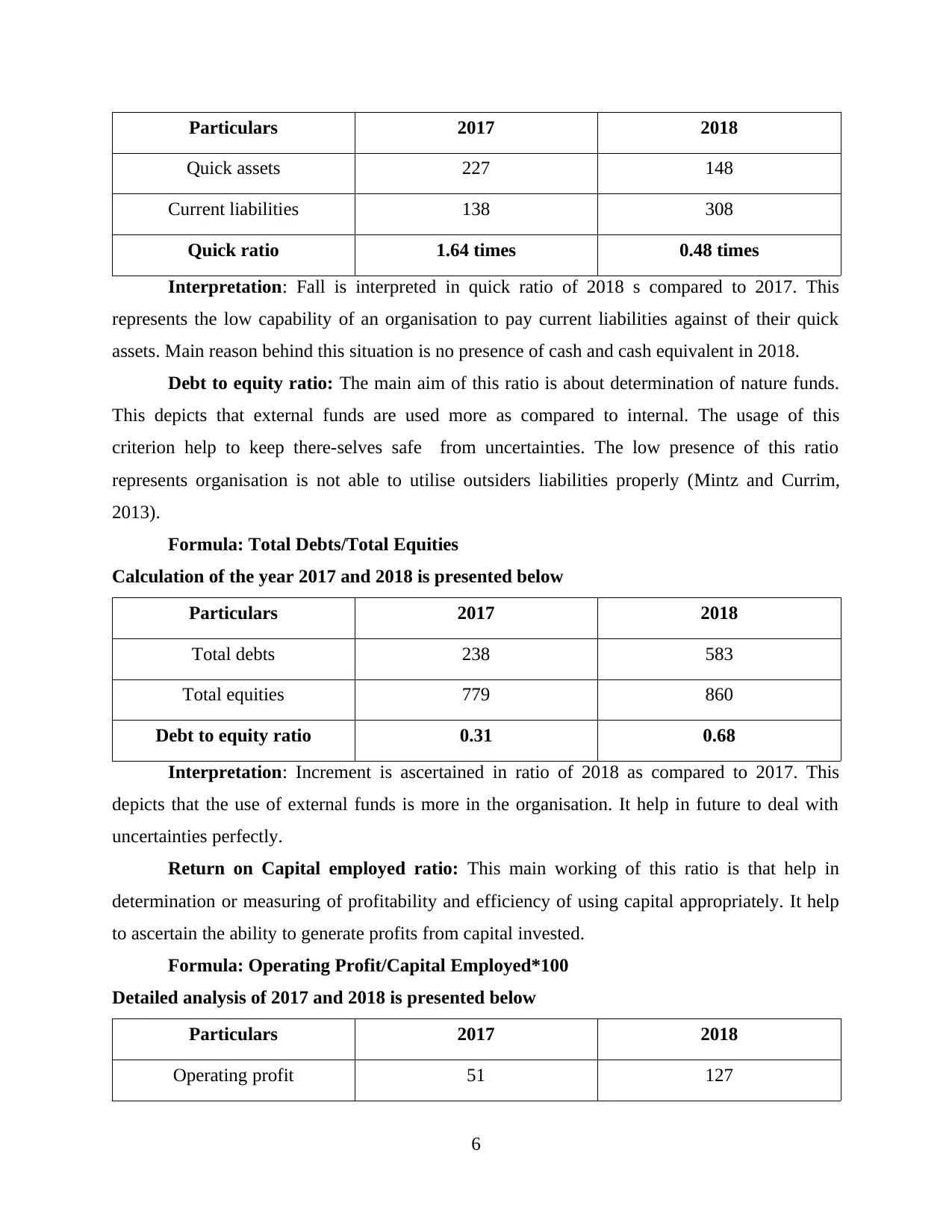

Particulars 2017 2018

Quick assets 227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

Interpretation: Fall is interpreted in quick ratio of 2018 s compared to 2017. This

represents the low capability of an organisation to pay current liabilities against of their quick

assets. Main reason behind this situation is no presence of cash and cash equivalent in 2018.

Debt to equity ratio: The main aim of this ratio is about determination of nature funds.

This depicts that external funds are used more as compared to internal. The usage of this

criterion help to keep there-selves safe from uncertainties. The low presence of this ratio

represents organisation is not able to utilise outsiders liabilities properly (Mintz and Currim,

2013).

Formula: Total Debts/Total Equities

Calculation of the year 2017 and 2018 is presented below

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt to equity ratio 0.31 0.68

Interpretation: Increment is ascertained in ratio of 2018 as compared to 2017. This

depicts that the use of external funds is more in the organisation. It help in future to deal with

uncertainties perfectly.

Return on Capital employed ratio: This main working of this ratio is that help in

determination or measuring of profitability and efficiency of using capital appropriately. It help

to ascertain the ability to generate profits from capital invested.

Formula: Operating Profit/Capital Employed*100

Detailed analysis of 2017 and 2018 is presented below

Particulars 2017 2018

Operating profit 51 127

6

Quick assets 227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

Interpretation: Fall is interpreted in quick ratio of 2018 s compared to 2017. This

represents the low capability of an organisation to pay current liabilities against of their quick

assets. Main reason behind this situation is no presence of cash and cash equivalent in 2018.

Debt to equity ratio: The main aim of this ratio is about determination of nature funds.

This depicts that external funds are used more as compared to internal. The usage of this

criterion help to keep there-selves safe from uncertainties. The low presence of this ratio

represents organisation is not able to utilise outsiders liabilities properly (Mintz and Currim,

2013).

Formula: Total Debts/Total Equities

Calculation of the year 2017 and 2018 is presented below

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt to equity ratio 0.31 0.68

Interpretation: Increment is ascertained in ratio of 2018 as compared to 2017. This

depicts that the use of external funds is more in the organisation. It help in future to deal with

uncertainties perfectly.

Return on Capital employed ratio: This main working of this ratio is that help in

determination or measuring of profitability and efficiency of using capital appropriately. It help

to ascertain the ability to generate profits from capital invested.

Formula: Operating Profit/Capital Employed*100

Detailed analysis of 2017 and 2018 is presented below

Particulars 2017 2018

Operating profit 51 127

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

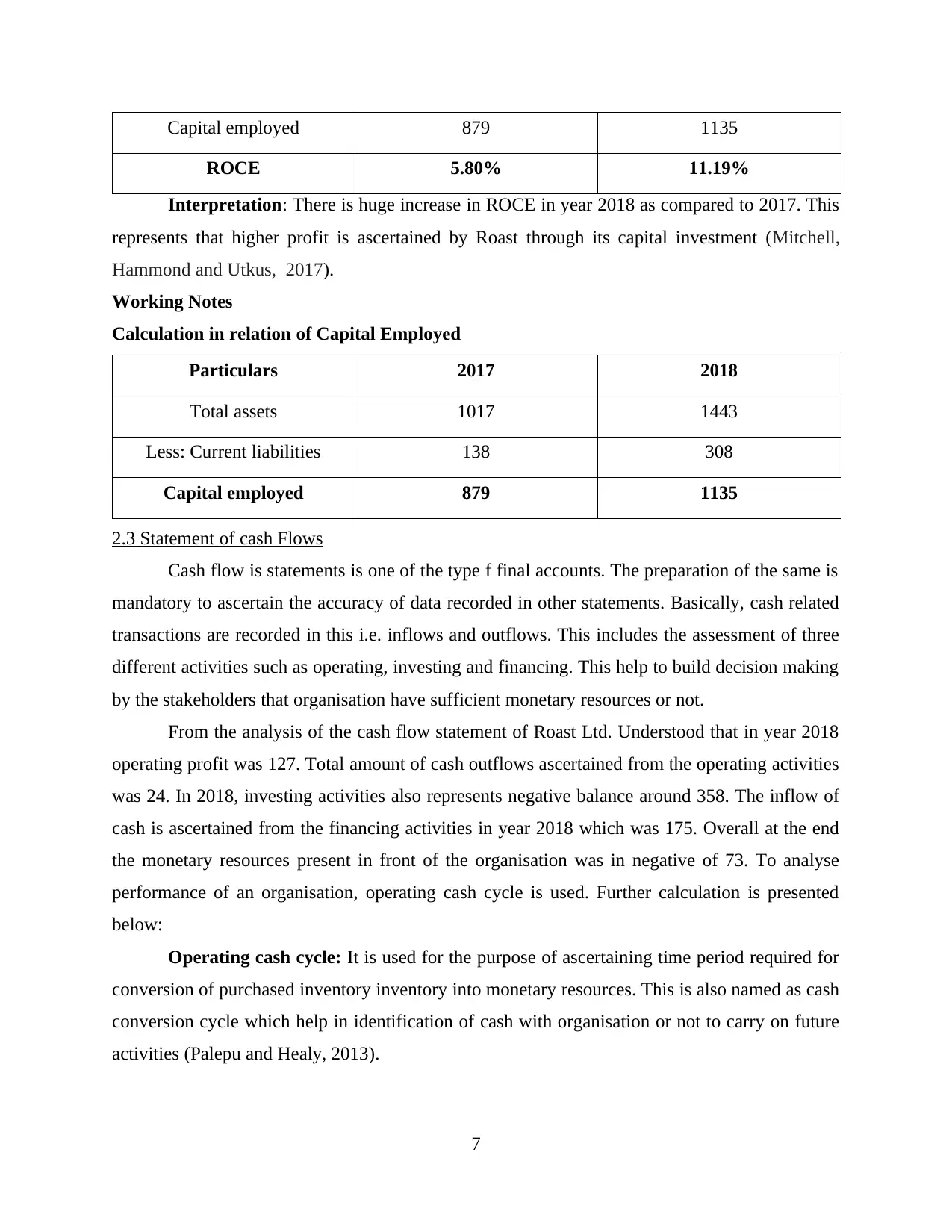

Capital employed 879 1135

ROCE 5.80% 11.19%

Interpretation: There is huge increase in ROCE in year 2018 as compared to 2017. This

represents that higher profit is ascertained by Roast through its capital investment (Mitchell,

Hammond and Utkus, 2017).

Working Notes

Calculation in relation of Capital Employed

Particulars 2017 2018

Total assets 1017 1443

Less: Current liabilities 138 308

Capital employed 879 1135

2.3 Statement of cash Flows

Cash flow is statements is one of the type f final accounts. The preparation of the same is

mandatory to ascertain the accuracy of data recorded in other statements. Basically, cash related

transactions are recorded in this i.e. inflows and outflows. This includes the assessment of three

different activities such as operating, investing and financing. This help to build decision making

by the stakeholders that organisation have sufficient monetary resources or not.

From the analysis of the cash flow statement of Roast Ltd. Understood that in year 2018

operating profit was 127. Total amount of cash outflows ascertained from the operating activities

was 24. In 2018, investing activities also represents negative balance around 358. The inflow of

cash is ascertained from the financing activities in year 2018 which was 175. Overall at the end

the monetary resources present in front of the organisation was in negative of 73. To analyse

performance of an organisation, operating cash cycle is used. Further calculation is presented

below:

Operating cash cycle: It is used for the purpose of ascertaining time period required for

conversion of purchased inventory inventory into monetary resources. This is also named as cash

conversion cycle which help in identification of cash with organisation or not to carry on future

activities (Palepu and Healy, 2013).

7

ROCE 5.80% 11.19%

Interpretation: There is huge increase in ROCE in year 2018 as compared to 2017. This

represents that higher profit is ascertained by Roast through its capital investment (Mitchell,

Hammond and Utkus, 2017).

Working Notes

Calculation in relation of Capital Employed

Particulars 2017 2018

Total assets 1017 1443

Less: Current liabilities 138 308

Capital employed 879 1135

2.3 Statement of cash Flows

Cash flow is statements is one of the type f final accounts. The preparation of the same is

mandatory to ascertain the accuracy of data recorded in other statements. Basically, cash related

transactions are recorded in this i.e. inflows and outflows. This includes the assessment of three

different activities such as operating, investing and financing. This help to build decision making

by the stakeholders that organisation have sufficient monetary resources or not.

From the analysis of the cash flow statement of Roast Ltd. Understood that in year 2018

operating profit was 127. Total amount of cash outflows ascertained from the operating activities

was 24. In 2018, investing activities also represents negative balance around 358. The inflow of

cash is ascertained from the financing activities in year 2018 which was 175. Overall at the end

the monetary resources present in front of the organisation was in negative of 73. To analyse

performance of an organisation, operating cash cycle is used. Further calculation is presented

below:

Operating cash cycle: It is used for the purpose of ascertaining time period required for

conversion of purchased inventory inventory into monetary resources. This is also named as cash

conversion cycle which help in identification of cash with organisation or not to carry on future

activities (Palepu and Healy, 2013).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

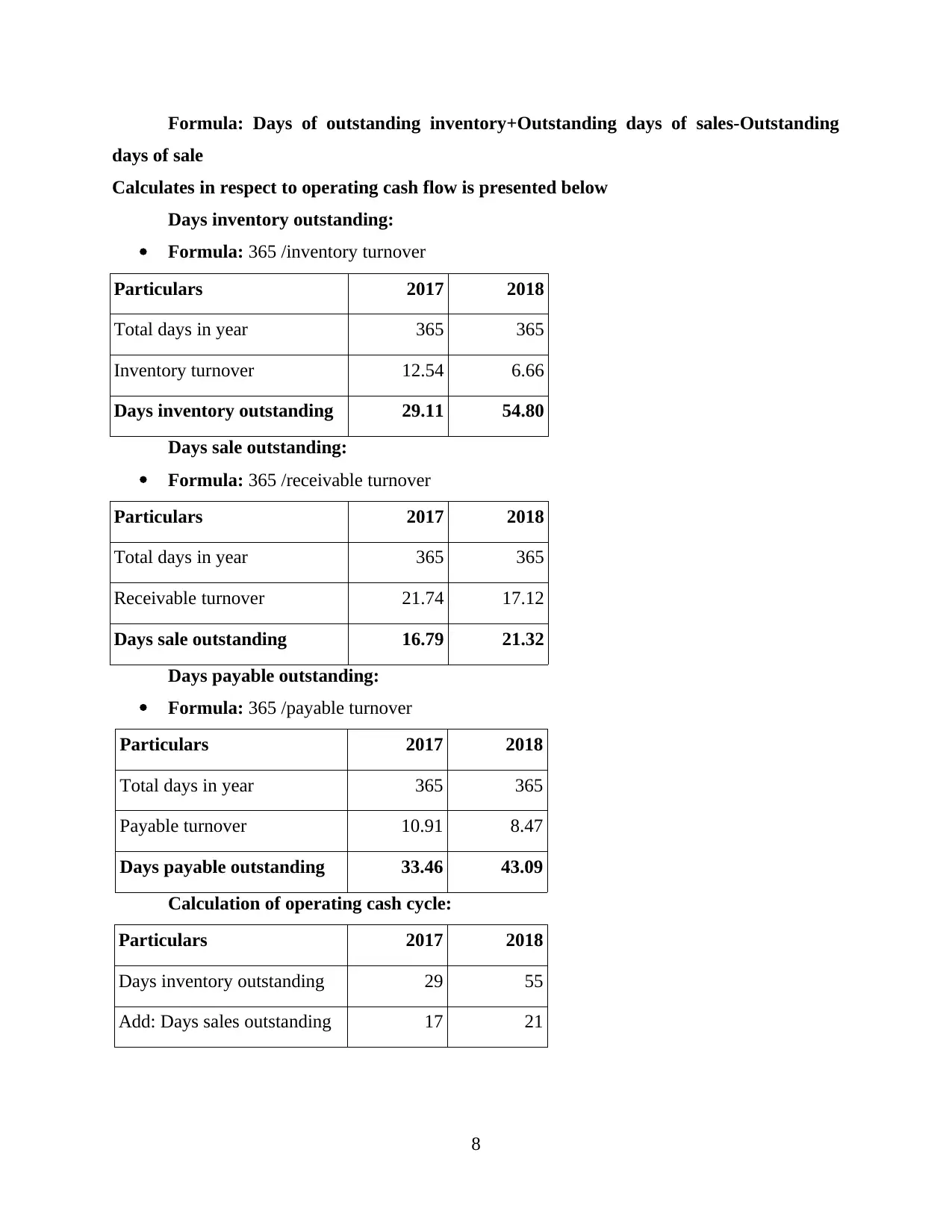

Formula: Days of outstanding inventory+Outstanding days of sales-Outstanding

days of sale

Calculates in respect to operating cash flow is presented below

Days inventory outstanding:

Formula: 365 /inventory turnover

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Days inventory outstanding 29.11 54.80

Days sale outstanding:

Formula: 365 /receivable turnover

Particulars 2017 2018

Total days in year 365 365

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

Formula: 365 /payable turnover

Particulars 2017 2018

Total days in year 365 365

Payable turnover 10.91 8.47

Days payable outstanding 33.46 43.09

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

8

days of sale

Calculates in respect to operating cash flow is presented below

Days inventory outstanding:

Formula: 365 /inventory turnover

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Days inventory outstanding 29.11 54.80

Days sale outstanding:

Formula: 365 /receivable turnover

Particulars 2017 2018

Total days in year 365 365

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

Formula: 365 /payable turnover

Particulars 2017 2018

Total days in year 365 365

Payable turnover 10.91 8.47

Days payable outstanding 33.46 43.09

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

8

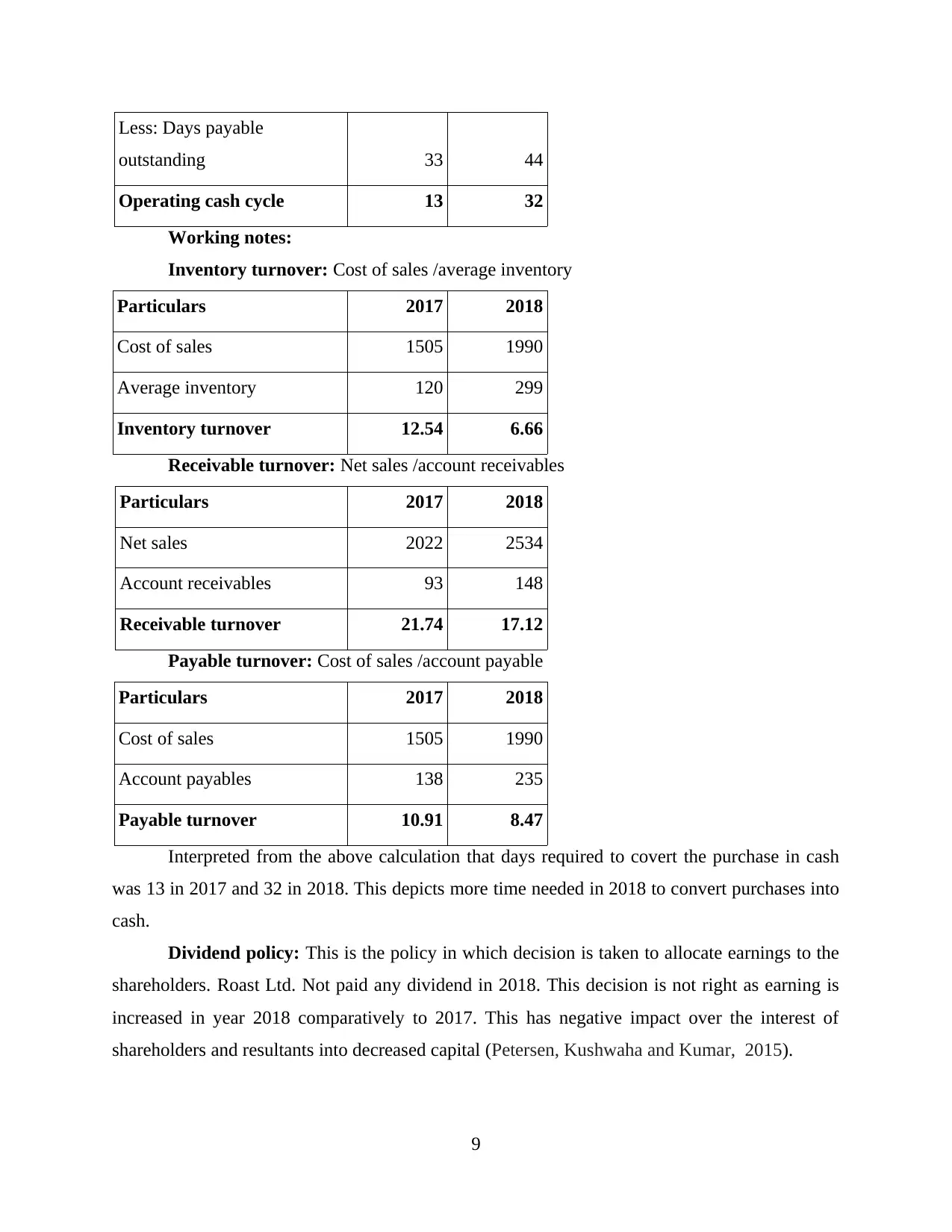

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

Working notes:

Inventory turnover: Cost of sales /average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales /account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales /account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

Interpreted from the above calculation that days required to covert the purchase in cash

was 13 in 2017 and 32 in 2018. This depicts more time needed in 2018 to convert purchases into

cash.

Dividend policy: This is the policy in which decision is taken to allocate earnings to the

shareholders. Roast Ltd. Not paid any dividend in 2018. This decision is not right as earning is

increased in year 2018 comparatively to 2017. This has negative impact over the interest of

shareholders and resultants into decreased capital (Petersen, Kushwaha and Kumar, 2015).

9

outstanding 33 44

Operating cash cycle 13 32

Working notes:

Inventory turnover: Cost of sales /average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales /account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales /account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

Interpreted from the above calculation that days required to covert the purchase in cash

was 13 in 2017 and 32 in 2018. This depicts more time needed in 2018 to convert purchases into

cash.

Dividend policy: This is the policy in which decision is taken to allocate earnings to the

shareholders. Roast Ltd. Not paid any dividend in 2018. This decision is not right as earning is

increased in year 2018 comparatively to 2017. This has negative impact over the interest of

shareholders and resultants into decreased capital (Petersen, Kushwaha and Kumar, 2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.