Comprehensive Financial Statement Analysis of Sony Corporation

VerifiedAdded on 2023/06/10

|10

|1830

|311

Report

AI Summary

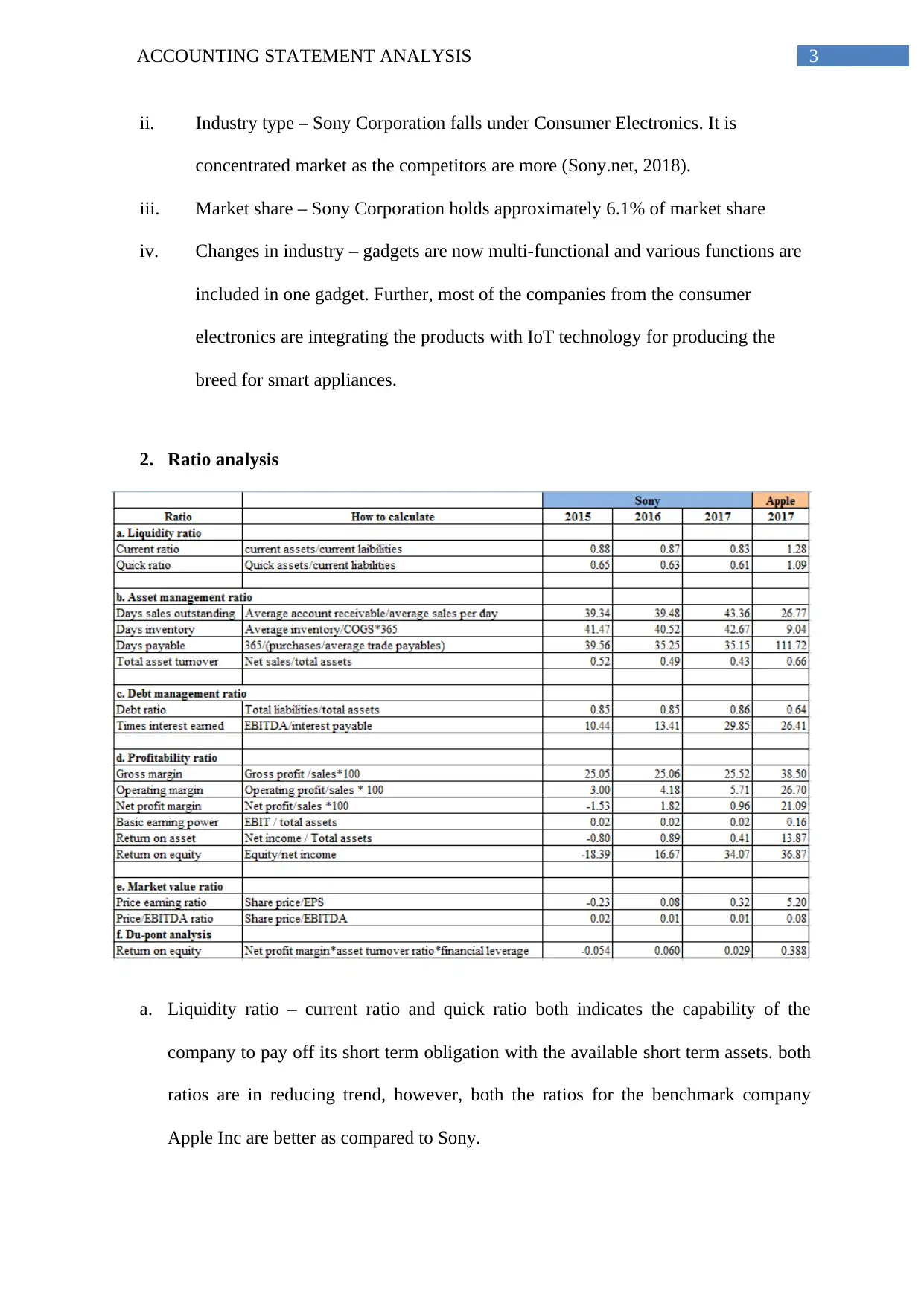

This report provides a comprehensive financial analysis of Sony Corporation, comparing it against a benchmark company (Apple Inc.) within the Consumer Electronics industry. The analysis includes ratio analysis (liquidity, asset management, debt management, profitability, and market value), WACC calculation, free cash flow analysis, and a valuation of operations. The report concludes with a recommendation against investing in Sony's stock due to deteriorating financial performance and negative free cash flow. Additionally, the report touches upon accounting practices, referencing the Enron scandal and emphasizing the importance of ethical accounting. The analysis uses formulas and calculations to provide a detailed financial overview, highlighting strengths and weaknesses in Sony's financial position. Desklib provides solved assignments and past papers for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.