Auditing Report: Fandango Enterprises' Financial Statement Analysis

VerifiedAdded on 2020/12/09

|10

|1994

|388

Report

AI Summary

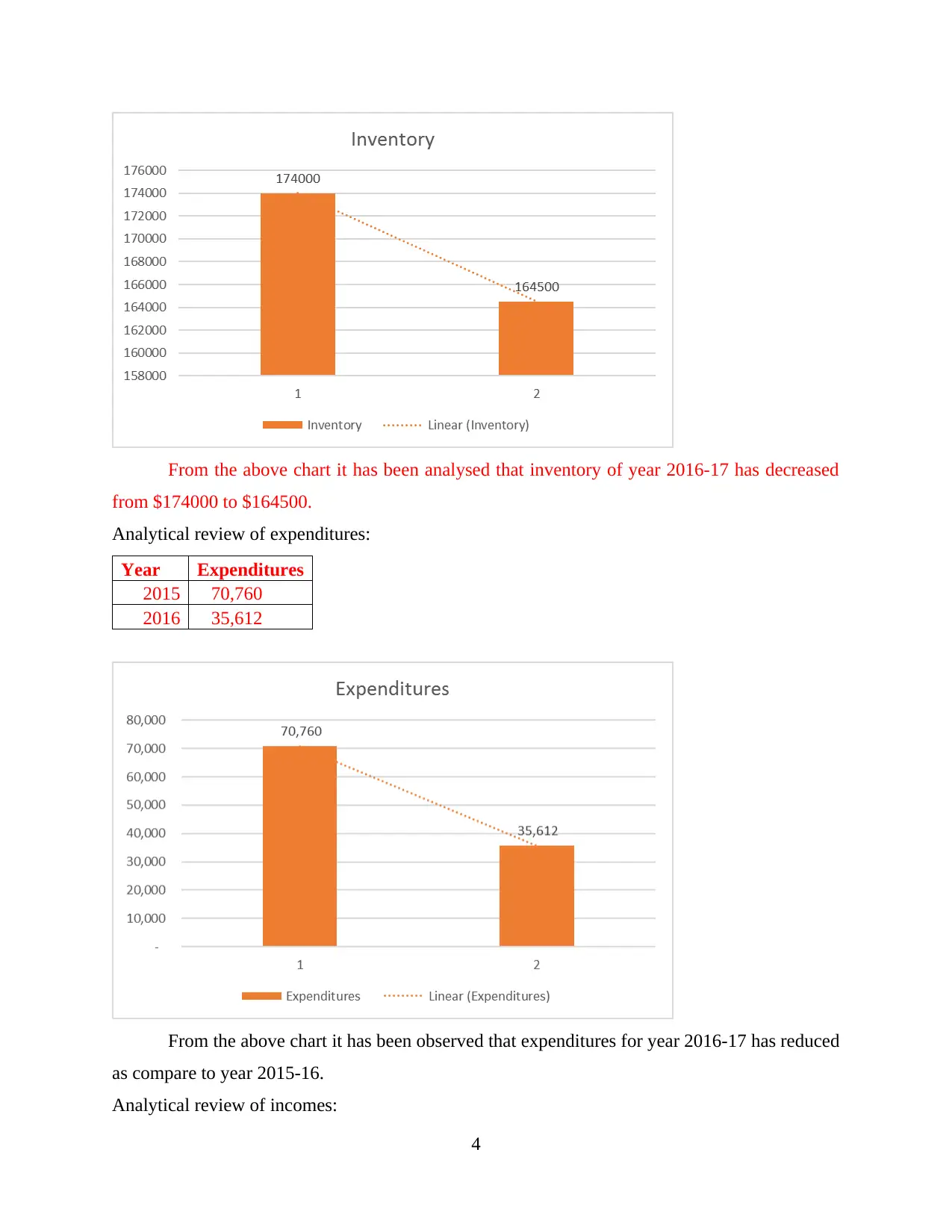

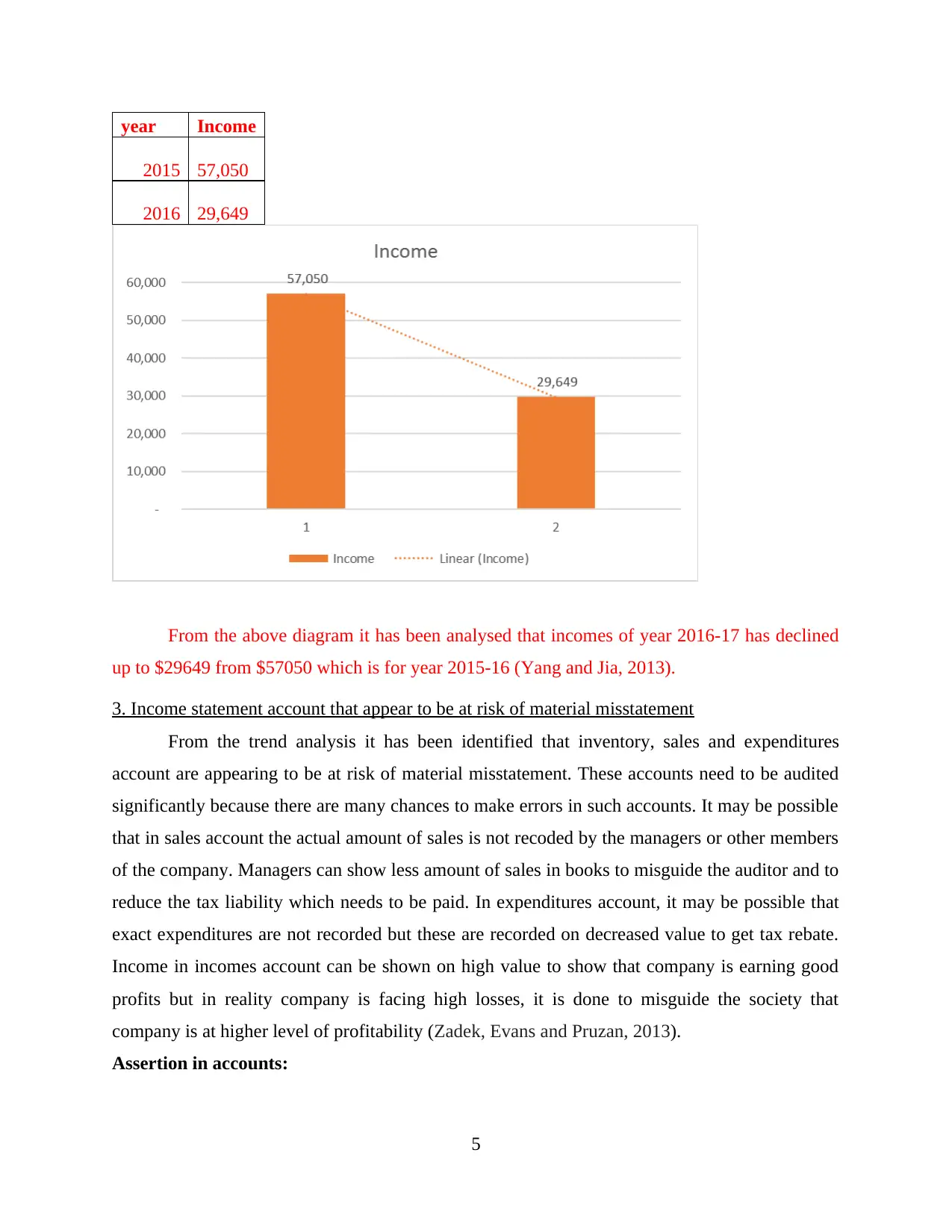

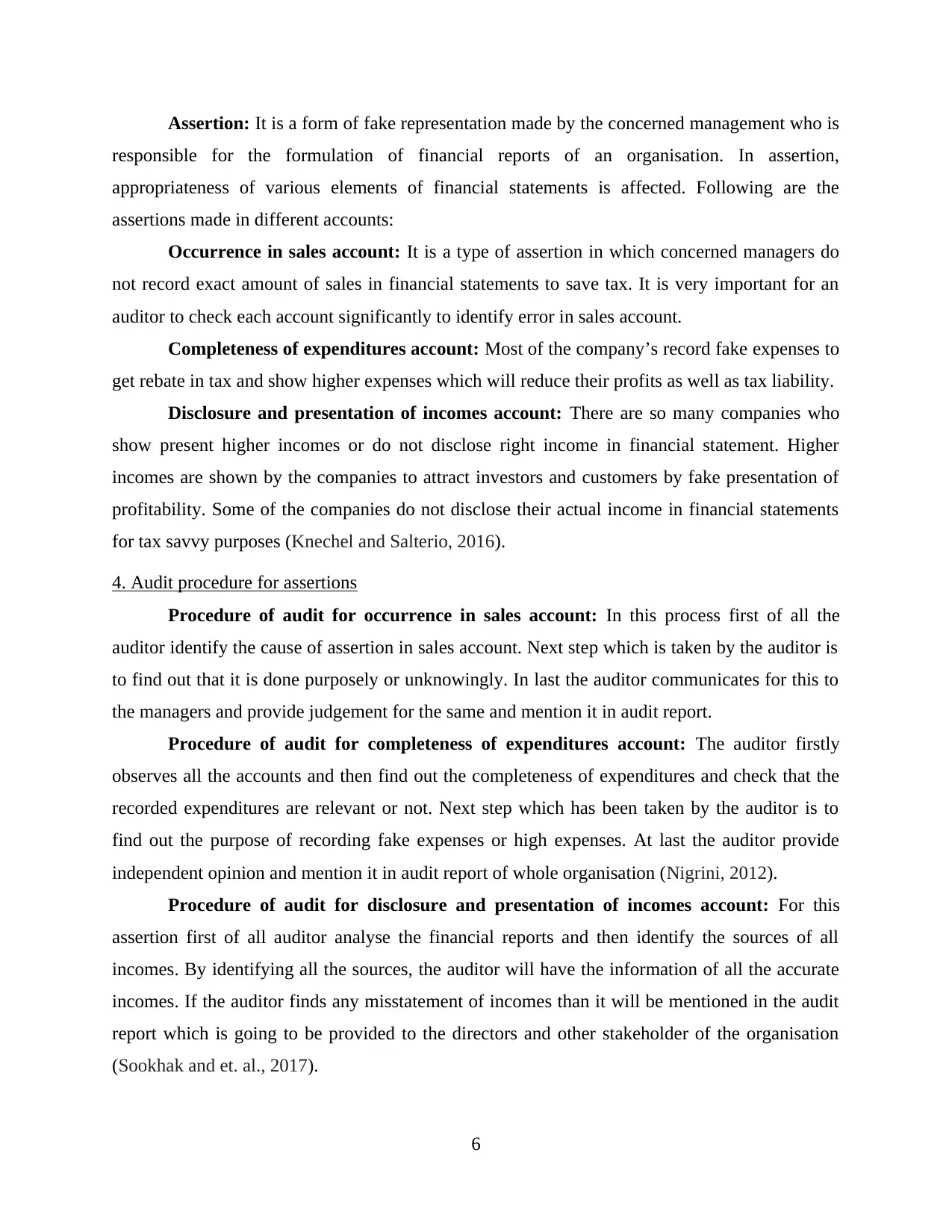

This report provides a comprehensive overview of the auditing process, focusing on the financial statements of Fandango Enterprises. The report begins with a preliminary assessment of materiality, outlining the budget and procedures involved. It then moves into an analytical review of income statement items, including sales, cost of sales, inventory, and expenditures, using trend analysis to identify potential misstatements. The report identifies specific income statement accounts at risk of material misstatement, such as sales, expenditures, and incomes, and discusses relevant assertions like occurrence, completeness, and disclosure. It details audit procedures for these assertions, including procedures for occurrence in sales, completeness of expenditures, and disclosure and presentation of incomes. Finally, the report critiques an audit partner's suggestion regarding fraud risk, concluding that the suggestion is inappropriate due to the non-matching trial balance and identified errors in the client's financial records.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.