Auditing: Financial Statement Analysis of Great Gift Inc. Report

VerifiedAdded on 2022/11/28

|10

|2089

|371

Report

AI Summary

This report provides an in-depth analysis of the auditing process, focusing on the financial statements of Great Gift Inc., a gift product manufacturer. The report examines the company's internal controls, identifies material misstatements in accounts like inventory and sales, and assesses associated risks such as fraud and accounting estimates. The auditor's considerations regarding completeness and accuracy assertions are detailed, along with recommendations to enhance the audit scope, plan materiality, and improve internal control analysis. The conclusion emphasizes the auditor's role in evaluating financial statements and providing an opinion based on the examination of the company's operations and financial reporting, ultimately aiming to assist financial statement users in making informed decisions. The report also includes references to relevant academic sources.

Running head: Auditing

Auditing

Name of the Student

Name of the University

Author Note

Auditing

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Auditing

Executive Summary

The report conclude about how the auditing process is been carried by the auditor to give its

opinion upon the financial statement of the company. It show about the company Great Gift,

Inc which is a manufacture of gift products and sale its product to wholesaler and retailer.

The report about the internal control of the company that how the company is been managing

its internal control, it show about the account in which material misstatement are there and

what are the assertion which the auditor have taken consideration in regards of those

accounts.

Auditing

Executive Summary

The report conclude about how the auditing process is been carried by the auditor to give its

opinion upon the financial statement of the company. It show about the company Great Gift,

Inc which is a manufacture of gift products and sale its product to wholesaler and retailer.

The report about the internal control of the company that how the company is been managing

its internal control, it show about the account in which material misstatement are there and

what are the assertion which the auditor have taken consideration in regards of those

accounts.

2

Auditing

Table of Contents

Introduction................................................................................................................................3

Overview of the company..........................................................................................................3

Internal control of company.......................................................................................................3

Material Misstatement in company............................................................................................4

Recommendation in regards of Risk..........................................................................................6

Conclusion..................................................................................................................................7

Reference....................................................................................................................................8

Auditing

Table of Contents

Introduction................................................................................................................................3

Overview of the company..........................................................................................................3

Internal control of company.......................................................................................................3

Material Misstatement in company............................................................................................4

Recommendation in regards of Risk..........................................................................................6

Conclusion..................................................................................................................................7

Reference....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Auditing

Introduction

. Auditing is the process from which the auditor check whether the company financial

statement is showing true and fair or not. It check the company financial statement as whether

the company is able to follow all the rules and regulation (Balsam, Jiang and Lu 2014). It

check that the company is able to have proper disclosure in the annual report about the

accounting entry and estimate which they have taken in the preparation of financial

statement. It check the internal control of the company as how the company is able to manage

the business risk and how they are able to manage the business operation internally. The

report show about the company Great Gift Inc, it show about the various aspects of the

company (De Simone, Ege and Stomberg 2014). It show about the internal control of the

company and different aspects which is been concern by the auditor.

Overview of the company

The assessment is based upon the company name Great Gift Inc which is a

manufacture of gift item for all the necessary occasion. It operate its business in both

wholesaler as well as retailer, it sale it product to big wholesaler, small chain group of

business and also to individual owner of the company.

Internal control of company

Internal control shows how the company is able to manage their business operation

internally and effectively (DeFond and Zhang 2014). It show how the company is able to

manage its activities and able to achieve their business goals and objective. As per the

previous analysis of the auditor it can be said that the company is not having proper internal

control as the auditor have checked the sale and purchase and it does not able to get sufficient

amount of document which can support that the company is having problem in the internal

Auditing

Introduction

. Auditing is the process from which the auditor check whether the company financial

statement is showing true and fair or not. It check the company financial statement as whether

the company is able to follow all the rules and regulation (Balsam, Jiang and Lu 2014). It

check that the company is able to have proper disclosure in the annual report about the

accounting entry and estimate which they have taken in the preparation of financial

statement. It check the internal control of the company as how the company is able to manage

the business risk and how they are able to manage the business operation internally. The

report show about the company Great Gift Inc, it show about the various aspects of the

company (De Simone, Ege and Stomberg 2014). It show about the internal control of the

company and different aspects which is been concern by the auditor.

Overview of the company

The assessment is based upon the company name Great Gift Inc which is a

manufacture of gift item for all the necessary occasion. It operate its business in both

wholesaler as well as retailer, it sale it product to big wholesaler, small chain group of

business and also to individual owner of the company.

Internal control of company

Internal control shows how the company is able to manage their business operation

internally and effectively (DeFond and Zhang 2014). It show how the company is able to

manage its activities and able to achieve their business goals and objective. As per the

previous analysis of the auditor it can be said that the company is not having proper internal

control as the auditor have checked the sale and purchase and it does not able to get sufficient

amount of document which can support that the company is having problem in the internal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Auditing

control. So it is the duty of the auditor to make change in the internal control so that it will

help the company to manage the business risk more easily in the company operation.

Material Misstatement in company

Material misstatement is happen when the company is not able to record proper

transaction in the financial statement (Furnham and Gunter 2015). It happen that the company

is have omitted or error has happen while recording the transaction so due to these the

company is having some material misstatement so the financial account will not show proper

valuation and as a result the financial user will not able to take proper decision in regards of

the company performance. As per the company is been seen it can be said that the company is

having less control in inventory as it does not able to have as in 2016 it recorded the useful

inventory as waste which afterward realise to be worth of $200000 so it can be said that the

there can be material misstatement in the same (Griffiths 2016). As the risk which are been

associated in material misstatement is that it can able to affect it will over or undervalued the

company asset and liabilities so it will directly affect the financial user decision as the user

will not able to take proper amount of decision in regards of the financial statement of the

company. The risk which are associated are fraud, going concern, Accounting estimates.

As per the financial statement it can be seen that the company is having no proper

estimates in regards of the accounting policy as it does not able to have proper estimates in

regards of the inventory so this show that there is material misstatement in company financial

statement so it is the duty auditor to carry different audit process in company so that it can

able to know the affect of material misstatement and able to judge the financial statement

more properly so that it can able to give proper recommendation in regards of the financial

statement of the company (Groomer and Murthy 2018).

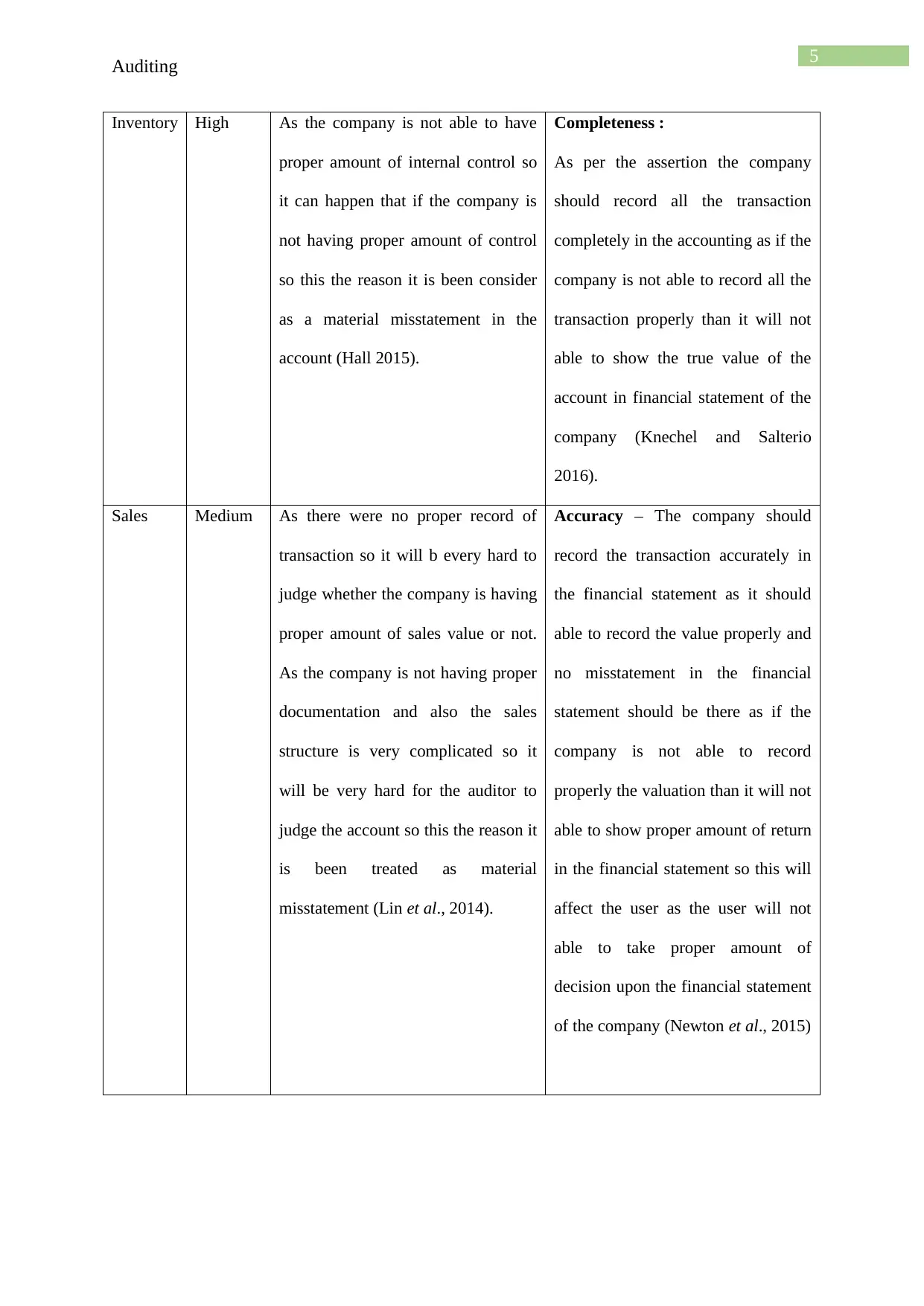

Account Grading Justification Assertion

Auditing

control. So it is the duty of the auditor to make change in the internal control so that it will

help the company to manage the business risk more easily in the company operation.

Material Misstatement in company

Material misstatement is happen when the company is not able to record proper

transaction in the financial statement (Furnham and Gunter 2015). It happen that the company

is have omitted or error has happen while recording the transaction so due to these the

company is having some material misstatement so the financial account will not show proper

valuation and as a result the financial user will not able to take proper decision in regards of

the company performance. As per the company is been seen it can be said that the company is

having less control in inventory as it does not able to have as in 2016 it recorded the useful

inventory as waste which afterward realise to be worth of $200000 so it can be said that the

there can be material misstatement in the same (Griffiths 2016). As the risk which are been

associated in material misstatement is that it can able to affect it will over or undervalued the

company asset and liabilities so it will directly affect the financial user decision as the user

will not able to take proper amount of decision in regards of the financial statement of the

company. The risk which are associated are fraud, going concern, Accounting estimates.

As per the financial statement it can be seen that the company is having no proper

estimates in regards of the accounting policy as it does not able to have proper estimates in

regards of the inventory so this show that there is material misstatement in company financial

statement so it is the duty auditor to carry different audit process in company so that it can

able to know the affect of material misstatement and able to judge the financial statement

more properly so that it can able to give proper recommendation in regards of the financial

statement of the company (Groomer and Murthy 2018).

Account Grading Justification Assertion

5

Auditing

Inventory High As the company is not able to have

proper amount of internal control so

it can happen that if the company is

not having proper amount of control

so this the reason it is been consider

as a material misstatement in the

account (Hall 2015).

Completeness :

As per the assertion the company

should record all the transaction

completely in the accounting as if the

company is not able to record all the

transaction properly than it will not

able to show the true value of the

account in financial statement of the

company (Knechel and Salterio

2016).

Sales Medium As there were no proper record of

transaction so it will b every hard to

judge whether the company is having

proper amount of sales value or not.

As the company is not having proper

documentation and also the sales

structure is very complicated so it

will be very hard for the auditor to

judge the account so this the reason it

is been treated as material

misstatement (Lin et al., 2014).

Accuracy – The company should

record the transaction accurately in

the financial statement as it should

able to record the value properly and

no misstatement in the financial

statement should be there as if the

company is not able to record

properly the valuation than it will not

able to show proper amount of return

in the financial statement so this will

affect the user as the user will not

able to take proper amount of

decision upon the financial statement

of the company (Newton et al., 2015)

Auditing

Inventory High As the company is not able to have

proper amount of internal control so

it can happen that if the company is

not having proper amount of control

so this the reason it is been consider

as a material misstatement in the

account (Hall 2015).

Completeness :

As per the assertion the company

should record all the transaction

completely in the accounting as if the

company is not able to record all the

transaction properly than it will not

able to show the true value of the

account in financial statement of the

company (Knechel and Salterio

2016).

Sales Medium As there were no proper record of

transaction so it will b every hard to

judge whether the company is having

proper amount of sales value or not.

As the company is not having proper

documentation and also the sales

structure is very complicated so it

will be very hard for the auditor to

judge the account so this the reason it

is been treated as material

misstatement (Lin et al., 2014).

Accuracy – The company should

record the transaction accurately in

the financial statement as it should

able to record the value properly and

no misstatement in the financial

statement should be there as if the

company is not able to record

properly the valuation than it will not

able to show proper amount of return

in the financial statement so this will

affect the user as the user will not

able to take proper amount of

decision upon the financial statement

of the company (Newton et al., 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Auditing

Recommendation in regards of Risk

As the risk is been concern it can be said that the auditor have to take many steps so

taht it can able to eliminate the risk and able to carry the audit more properly in the company.

The steps which is to be taken by the auditor are:

1. Increase in scope of Audit – It should increase the scope the audit process so that it

can able to judge the financial statement more properly, as if it increase the scope of

audit than it will able to judge each account more properly as it will to evaluate the

financial statement more properly (Sandvig et al., 2014). As the auditor is able to

increase the audit process in the company so it will help it to make more proper

opinion upon the financial statement of the company.

2. Planning Materiality – It should judge the business and should plan the materiality

which should be there in the financial statement of the company (Wang, Li and Li

2014). As if the auditor able to judge the financial statement materiality in planning

stage than it will help him to judge the company account more easily as it will able to

match the materiality with the budgeted and able to give its opinion upon how the

company is able to have materiality in the financial statement of the company.

3. Increase in Internal Control Analysis – As per the company is been concern it can

be said that the company is not having proper amount of internal control so due to this

there is material misstatement in company financial statement so to overcome that it

should have proper internal control which will help the company to overcome the

problem which they are facing while carrying the internal control so if the company

will have proper amount of internal control than it will able to achieve the business

goals easily and effectively in the company.

Auditing

Recommendation in regards of Risk

As the risk is been concern it can be said that the auditor have to take many steps so

taht it can able to eliminate the risk and able to carry the audit more properly in the company.

The steps which is to be taken by the auditor are:

1. Increase in scope of Audit – It should increase the scope the audit process so that it

can able to judge the financial statement more properly, as if it increase the scope of

audit than it will able to judge each account more properly as it will to evaluate the

financial statement more properly (Sandvig et al., 2014). As the auditor is able to

increase the audit process in the company so it will help it to make more proper

opinion upon the financial statement of the company.

2. Planning Materiality – It should judge the business and should plan the materiality

which should be there in the financial statement of the company (Wang, Li and Li

2014). As if the auditor able to judge the financial statement materiality in planning

stage than it will help him to judge the company account more easily as it will able to

match the materiality with the budgeted and able to give its opinion upon how the

company is able to have materiality in the financial statement of the company.

3. Increase in Internal Control Analysis – As per the company is been concern it can

be said that the company is not having proper amount of internal control so due to this

there is material misstatement in company financial statement so to overcome that it

should have proper internal control which will help the company to overcome the

problem which they are facing while carrying the internal control so if the company

will have proper amount of internal control than it will able to achieve the business

goals easily and effectively in the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Auditing

Conclusion

The report can be conclude as auditing is the process which help the auditor to carry

audit process in the company. The auditor carry audit process in the company financial

statement so that it can able to have proper details about how the company has made the

financial statement and able to give proper opinion upon the financial statement of the

company. It also check the internal control of the company as whether the company is having

proper amount of internal control or not as if the company is not having proper amount of

internal control than there is a high chance that the company will able to have material

misstatement in the company account which will directly affect the financial user to take

necessary decision in regards of the financial statement of the company.

It conclude about the company Great Gifts, Inc which is an manufacture of gift and

sale its gift to different wholesaler, retailer and also to individual store owner. The report

show about the different aspects which is been taken care by the auditor while carrying the

audit process in the company. It show different problem which the company faces internal

control as how the company internal control is working. It also show the material

misstatement which is been there in the company financial statement and which two account

which are been affected by the material misstatement. Lastly it show the assertion which the

auditor have to take while carrying the audit process of the company accounts.

Auditing

Conclusion

The report can be conclude as auditing is the process which help the auditor to carry

audit process in the company. The auditor carry audit process in the company financial

statement so that it can able to have proper details about how the company has made the

financial statement and able to give proper opinion upon the financial statement of the

company. It also check the internal control of the company as whether the company is having

proper amount of internal control or not as if the company is not having proper amount of

internal control than there is a high chance that the company will able to have material

misstatement in the company account which will directly affect the financial user to take

necessary decision in regards of the financial statement of the company.

It conclude about the company Great Gifts, Inc which is an manufacture of gift and

sale its gift to different wholesaler, retailer and also to individual store owner. The report

show about the different aspects which is been taken care by the auditor while carrying the

audit process in the company. It show different problem which the company faces internal

control as how the company internal control is working. It also show the material

misstatement which is been there in the company financial statement and which two account

which are been affected by the material misstatement. Lastly it show the assertion which the

auditor have to take while carrying the audit process of the company accounts.

8

Auditing

Reference

Balsam, S., Jiang, W. and Lu, B., 2014. Equity incentives and internal control

weaknesses. Contemporary Accounting Research, 31(1), pp.178-201.

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lin, Y.C., Wang, Y.C., Chiou, J.R. and Huang, H.W., 2014. CEO characteristics and internal

control quality. Corporate Governance: An International Review, 22(1), pp.24-42.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Auditing

Reference

Balsam, S., Jiang, W. and Lu, B., 2014. Equity incentives and internal control

weaknesses. Contemporary Accounting Research, 31(1), pp.178-201.

De Simone, L., Ege, M.S. and Stomberg, B., 2014. Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), pp.1469-1496.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hall, J.A., 2015. Information technology auditing. Cengage Learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Lin, Y.C., Wang, Y.C., Chiou, J.R. and Huang, H.W., 2014. CEO characteristics and internal

control quality. Corporate Governance: An International Review, 22(1), pp.24-42.

Newton, N.J., Persellin, J.S., Wang, D. and Wilkins, M.S., 2015. Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), pp.603-623.

Sandvig, C., Hamilton, K., Karahalios, K. and Langbort, C., 2014. Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Auditing

Wang, B., Li, B. and Li, H., 2014. Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), pp.43-56.

Auditing

Wang, B., Li, B. and Li, H., 2014. Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), pp.43-56.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.