Presentation: Financial Statement Analysis and Audit of ABC Learning

VerifiedAdded on 2023/06/10

|12

|1212

|165

Presentation

AI Summary

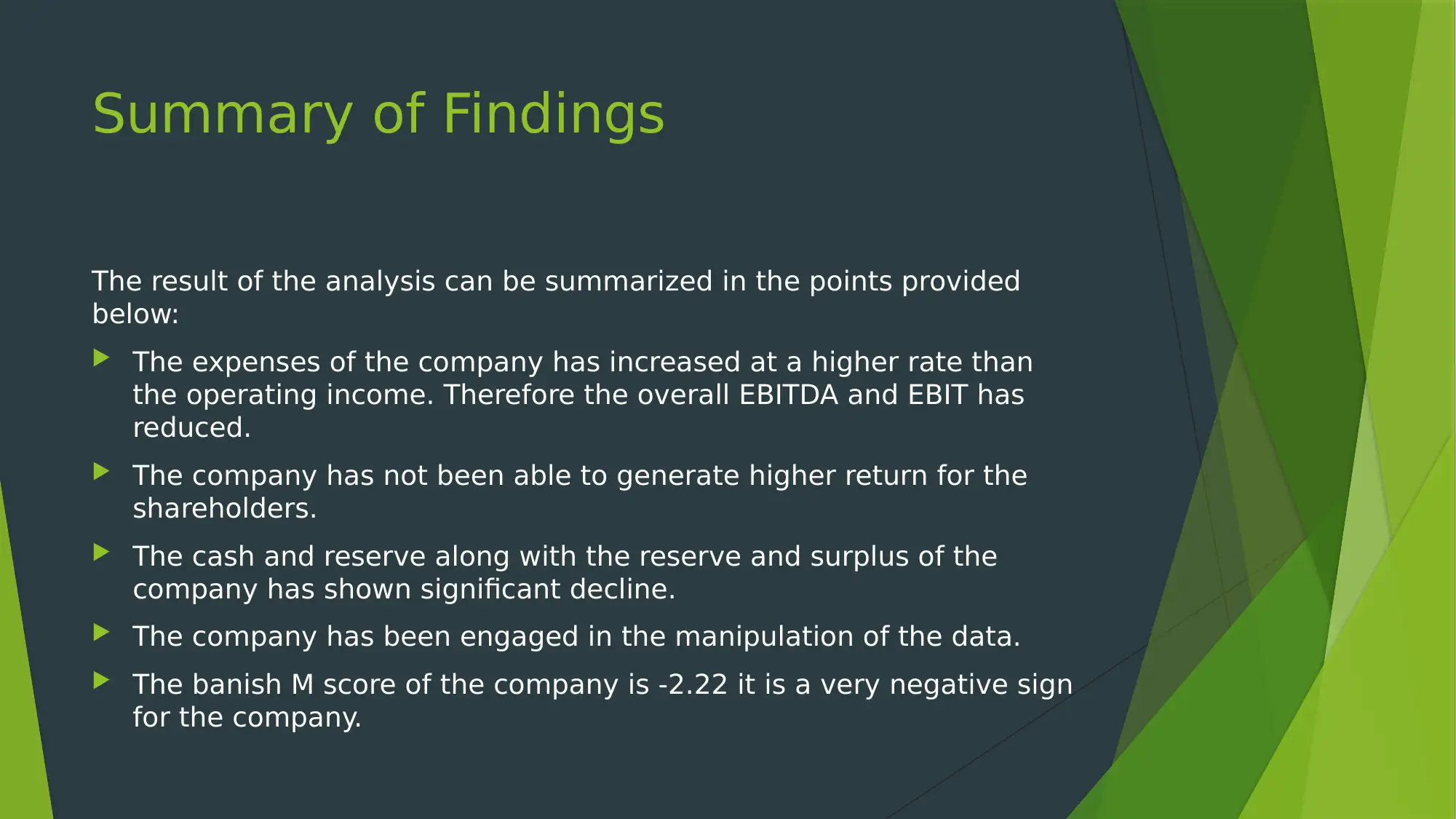

This presentation offers a comprehensive audit of ABC Learning's financial statements. It begins with an introduction outlining the purpose of the analysis, which is to assess the financial health of the company and evaluate the auditor's role in ensuring a true and fair view of the financial position. The presentation then delves into a literature review, highlighting relevant auditing standards such as ASA 200, ASA 220, ASA 230, ASA 315, ASA 500, and ASA 240. The analysis employs various tools including trend analysis, Beneish M-score, DuPont analysis, and common size statements to scrutinize the financial data. The findings reveal a decline in EBITDA and EBIT, shareholder returns, and cash reserves. Furthermore, the analysis suggests data manipulation and a negative Beneish M-score. Recommendations include cost reduction, avoidance of account manipulation, and improved capital utilization. The presentation concludes with a summary of key points and emphasizes the importance of adhering to laws and regulations in business operations.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.