FIN921 - Financial Statement Analysis: Predicting Corporate Bankruptcy

VerifiedAdded on 2023/06/11

|12

|3570

|423

Essay

AI Summary

This essay provides a comprehensive analysis of financial statement analysis as a tool for predicting corporate bankruptcy. It discusses the limitations of relying solely on financial statements due to corporate scandals and emphasizes the importance of incorporating non-financial information and alternative financial ratios. The essay explores various financial analysis tools, such as ratio analysis and capital budgeting, and highlights the significance of solvency, profitability, and effective management in preventing bankruptcy. It also touches upon credit risk models and the Z score approach for assessing financial risk. The research emphasizes that the proper use of financial details and tools can help in evaluating future financial performance and detecting financial frauds. Desklib provides students access to similar solved assignments and resources for academic support.

Financial Statement analysis

FINANCIAL STATEMENT ANALYSIS

Financial analysis

Name of Author

University Name

FINANCIAL STATEMENT ANALYSIS

Financial analysis

Name of Author

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

There are several financial factors which have been affecting the business growth and

development. There are several financial analysis tools such as ratio analysis, bottom up

analysis, top down analysis and capital budgeting tools which are used to assess the financial

performance of company. The financial statement analysis is used to evaluate the financial

performance of company and how it could be used to evaluate the past and future trend of

company in long run. It is further observed that various financial scandals have shown that

analysis the financial statements are not the adequate source to evaluate the present and future

performance of company. In this essay, it is inferred that if analysis uses the proper financial

details and tools then they could easily evaluate how well they could evaluate the future

financial performance at large. The objective of the paper is to stress the imperativeness of

the detecting the financial frauds in the business failures and evaluating how financial tools

could be used to assess the future financial performance in long run.

There are several financial factors which have been affecting the business growth and

development. There are several financial analysis tools such as ratio analysis, bottom up

analysis, top down analysis and capital budgeting tools which are used to assess the financial

performance of company. The financial statement analysis is used to evaluate the financial

performance of company and how it could be used to evaluate the past and future trend of

company in long run. It is further observed that various financial scandals have shown that

analysis the financial statements are not the adequate source to evaluate the present and future

performance of company. In this essay, it is inferred that if analysis uses the proper financial

details and tools then they could easily evaluate how well they could evaluate the future

financial performance at large. The objective of the paper is to stress the imperativeness of

the detecting the financial frauds in the business failures and evaluating how financial tools

could be used to assess the future financial performance in long run.

Table of Contents

EXECUTIVE SUMMARY........................................................................................................1

INTRODUTION........................................................................................................................1

OBJECTIVE..............................................................................................................................2

METHODOLOGIES..................................................................................................................2

Carroll’s Pyramid...................................................................................................................2

Wartick and Cochrane’s Typology.........................................................................................3

INFORMATION ANALYSIS...................................................................................................3

FINDINGS.................................................................................................................................4

RECOMMENDATIONS...........................................................................................................5

Conclusion..................................................................................................................................6

References..................................................................................................................................7

EXECUTIVE SUMMARY........................................................................................................1

INTRODUTION........................................................................................................................1

OBJECTIVE..............................................................................................................................2

METHODOLOGIES..................................................................................................................2

Carroll’s Pyramid...................................................................................................................2

Wartick and Cochrane’s Typology.........................................................................................3

INFORMATION ANALYSIS...................................................................................................3

FINDINGS.................................................................................................................................4

RECOMMENDATIONS...........................................................................................................5

Conclusion..................................................................................................................................6

References..................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUTION

Predicting the bankruptcy was an on-going concern of the researchers and lately it has

become subject extensively studied the process and controversial discussion. Financial

analysis is the process to evaluate the past and future performance of company. If person

wants to evaluate the financial performance of company then they will have to use the

financial statements such as balance sheet, profit and loss statements and other details. After

that financial analysis tools will be used to evaluate the profitability, efficiency, solvency and

market ratio to identify the past and future performance of company. Sign of the business

failure are the main usual evident long before bankruptcy. It is analyzed that if investors use

proper analysis tools then they could easily determine whether company has been facing any

financial leverage in its business or not. Ideally, bank faces bankruptcy when it has higher

solvency ratio or the profitability of company is not adequate enough to cover its fixed

charges and expenses. There are number of methods and financial tools which are used to

assess whether the bank will be sustainable in the long run or not.

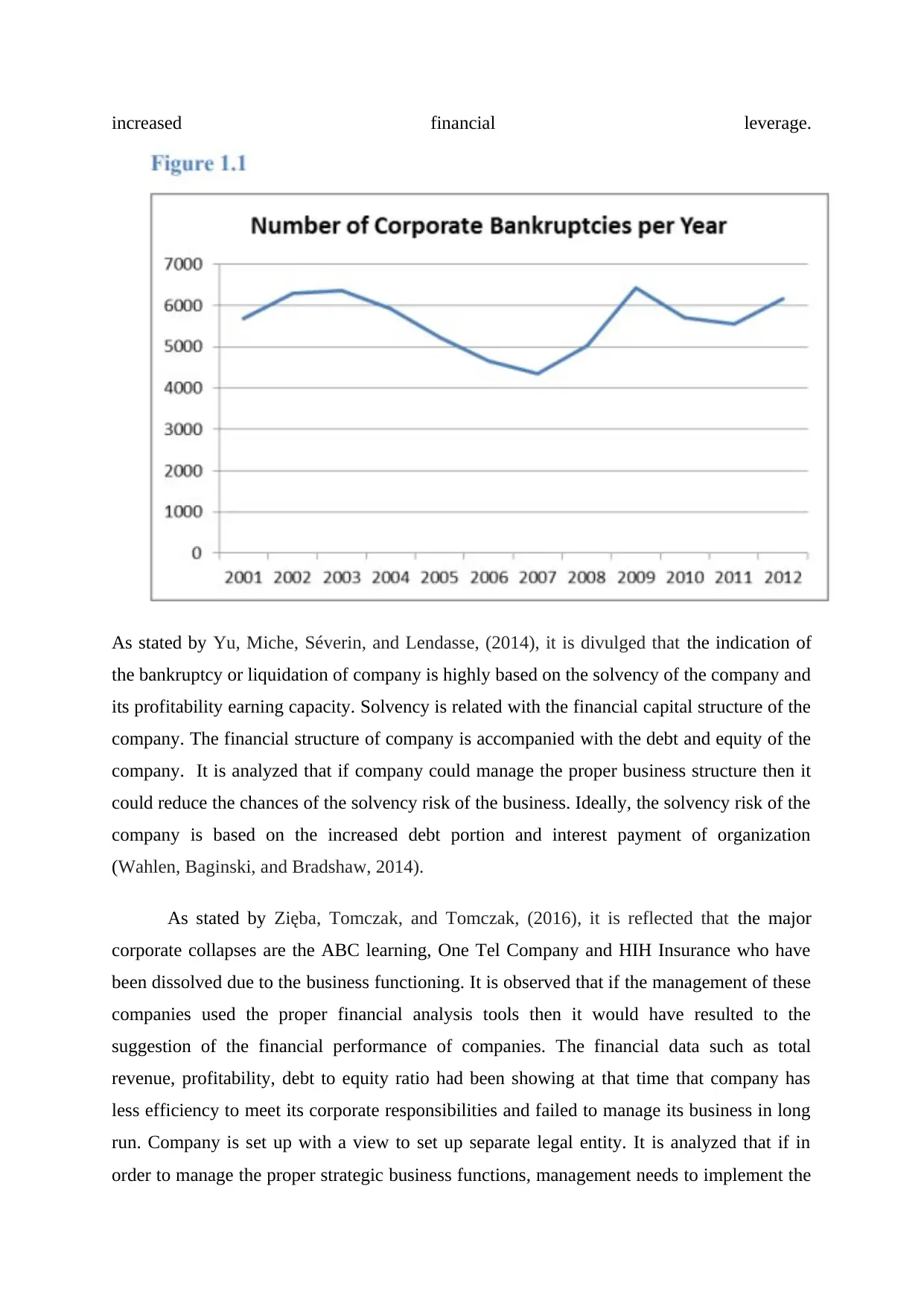

There are thousands of companies have been facing the financial distress and

difficulties which in many cases lead to bankruptcy. After analysing the cases of the

corporates scandals, it could be inferred that these numbers have increased due to the

Predicting the bankruptcy was an on-going concern of the researchers and lately it has

become subject extensively studied the process and controversial discussion. Financial

analysis is the process to evaluate the past and future performance of company. If person

wants to evaluate the financial performance of company then they will have to use the

financial statements such as balance sheet, profit and loss statements and other details. After

that financial analysis tools will be used to evaluate the profitability, efficiency, solvency and

market ratio to identify the past and future performance of company. Sign of the business

failure are the main usual evident long before bankruptcy. It is analyzed that if investors use

proper analysis tools then they could easily determine whether company has been facing any

financial leverage in its business or not. Ideally, bank faces bankruptcy when it has higher

solvency ratio or the profitability of company is not adequate enough to cover its fixed

charges and expenses. There are number of methods and financial tools which are used to

assess whether the bank will be sustainable in the long run or not.

There are thousands of companies have been facing the financial distress and

difficulties which in many cases lead to bankruptcy. After analysing the cases of the

corporates scandals, it could be inferred that these numbers have increased due to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increased financial leverage.

As stated by Yu, Miche, Séverin, and Lendasse, (2014), it is divulged that the indication of

the bankruptcy or liquidation of company is highly based on the solvency of the company and

its profitability earning capacity. Solvency is related with the financial capital structure of the

company. The financial structure of company is accompanied with the debt and equity of the

company. It is analyzed that if company could manage the proper business structure then it

could reduce the chances of the solvency risk of the business. Ideally, the solvency risk of the

company is based on the increased debt portion and interest payment of organization

(Wahlen, Baginski, and Bradshaw, 2014).

As stated by Zięba, Tomczak, and Tomczak, (2016), it is reflected that the major

corporate collapses are the ABC learning, One Tel Company and HIH Insurance who have

been dissolved due to the business functioning. It is observed that if the management of these

companies used the proper financial analysis tools then it would have resulted to the

suggestion of the financial performance of companies. The financial data such as total

revenue, profitability, debt to equity ratio had been showing at that time that company has

less efficiency to meet its corporate responsibilities and failed to manage its business in long

run. Company is set up with a view to set up separate legal entity. It is analyzed that if in

order to manage the proper strategic business functions, management needs to implement the

As stated by Yu, Miche, Séverin, and Lendasse, (2014), it is divulged that the indication of

the bankruptcy or liquidation of company is highly based on the solvency of the company and

its profitability earning capacity. Solvency is related with the financial capital structure of the

company. The financial structure of company is accompanied with the debt and equity of the

company. It is analyzed that if company could manage the proper business structure then it

could reduce the chances of the solvency risk of the business. Ideally, the solvency risk of the

company is based on the increased debt portion and interest payment of organization

(Wahlen, Baginski, and Bradshaw, 2014).

As stated by Zięba, Tomczak, and Tomczak, (2016), it is reflected that the major

corporate collapses are the ABC learning, One Tel Company and HIH Insurance who have

been dissolved due to the business functioning. It is observed that if the management of these

companies used the proper financial analysis tools then it would have resulted to the

suggestion of the financial performance of companies. The financial data such as total

revenue, profitability, debt to equity ratio had been showing at that time that company has

less efficiency to meet its corporate responsibilities and failed to manage its business in long

run. Company is set up with a view to set up separate legal entity. It is analyzed that if in

order to manage the proper strategic business functions, management needs to implement the

proper strategic program. As per the views of Altman, Iwanicz-Drozdowska, Laitinen, and

Suvas, (2015), it is reflected that the Capital budgeting tools is another method to evaluate

how the investment in the particular project will give more return to company. In one Tel

company, management had to face high loss due to the less transparency and non-effective

reporting frameworks. It will not only resulted to the dissolution of company but also lower

down the outcomes of the business. It is further observed that financial statements of

company could only divulge the possible financial information which could be qualified and

non-qualified information. If investors want to assess the present and future financial

performance then they will have to consider the share price performance, solvency and

profitability of company. However, ratio analysis is the basic tool which is used to assess the

financial performance and future business practice of company. For instance, the current ratio

of company divulges the ability of company to pay off its short term and long term debts out

of the available current assets. In addition to this, profitability ratio shows the company’s

ability to earn profit from its turnover. It shows the return on capital employed, return on

assets, return on share capital (Liang, et al., 2016). After that, investors and management

department could assess the efficiency of company to run the business. As stated by Gupta,

Gregoriou, and Healy, 2015. It is divulged that it will not only showcase the efficiency of

company to deploy the cash funds but also reflects how well Particular Corporation has used

its capital. Ideally, corporate scandals and liquidating cases have emerged due to the less

transparent business functions and complex business structure. Each and every company

needs to establish the proper harmonization in its domestic and international reporting

framework to strengthen its transparency of the business. It is analyzed that the financial

diagnosis by the bankruptcy risk rate analysis and risk assessment considers the primarily on

three important dimensions of firm: profitability, liquidity and financial structure.

As stated by Lakshmi, Martin, and Venkatesan, (2016), it is reflected that the failure

of the business in the market and increased financial distress has happened due to the less

effective business functions and non-efficient management program of company. Managers

are the key persons of the company who takes all the strategic decisions. If they fail to take

effective decisions then it will not only impact the business but also increase the financial risk

of company in long run. Ideally, the financial risk of company is highly dependent upon debt

capital and profitability of company. For instance, if company is having high profitability

then it could have higher financial leverage in its business. Ideally, financial scandals arise

when company fails to meet its short term and long term responsibilities. It is evaluated that

Suvas, (2015), it is reflected that the Capital budgeting tools is another method to evaluate

how the investment in the particular project will give more return to company. In one Tel

company, management had to face high loss due to the less transparency and non-effective

reporting frameworks. It will not only resulted to the dissolution of company but also lower

down the outcomes of the business. It is further observed that financial statements of

company could only divulge the possible financial information which could be qualified and

non-qualified information. If investors want to assess the present and future financial

performance then they will have to consider the share price performance, solvency and

profitability of company. However, ratio analysis is the basic tool which is used to assess the

financial performance and future business practice of company. For instance, the current ratio

of company divulges the ability of company to pay off its short term and long term debts out

of the available current assets. In addition to this, profitability ratio shows the company’s

ability to earn profit from its turnover. It shows the return on capital employed, return on

assets, return on share capital (Liang, et al., 2016). After that, investors and management

department could assess the efficiency of company to run the business. As stated by Gupta,

Gregoriou, and Healy, 2015. It is divulged that it will not only showcase the efficiency of

company to deploy the cash funds but also reflects how well Particular Corporation has used

its capital. Ideally, corporate scandals and liquidating cases have emerged due to the less

transparent business functions and complex business structure. Each and every company

needs to establish the proper harmonization in its domestic and international reporting

framework to strengthen its transparency of the business. It is analyzed that the financial

diagnosis by the bankruptcy risk rate analysis and risk assessment considers the primarily on

three important dimensions of firm: profitability, liquidity and financial structure.

As stated by Lakshmi, Martin, and Venkatesan, (2016), it is reflected that the failure

of the business in the market and increased financial distress has happened due to the less

effective business functions and non-efficient management program of company. Managers

are the key persons of the company who takes all the strategic decisions. If they fail to take

effective decisions then it will not only impact the business but also increase the financial risk

of company in long run. Ideally, the financial risk of company is highly dependent upon debt

capital and profitability of company. For instance, if company is having high profitability

then it could have higher financial leverage in its business. Ideally, financial scandals arise

when company fails to meet its short term and long term responsibilities. It is evaluated that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

mangers need to have proper financial information about the company to make the strategic

financial decisions (Iturriaga, and Sanz, 2015). It is analyzed that the ratio analysis is ideally

used by the managers to establish the relation between the two financial factors and evaluate

whether the implemented decisions will add value to the clients satisfaction or not. It is

further observed capital budgeting tools such as NPV, IRR and profitability index are the key

to analysis whether company should invest their capital in particular project or not. In

addition to this, company also needs to analysis whether investing capital in the particular

project will have more output or not. Managers need to only accept those projects which

gives higher project benefits to the organization. All the financial information shown in the

annual report or financial statement of company needs to be analyzed whether investing

capital in the particular project will create value on the investment or not. All the financial

and non-financial information such as employee turnover, market share, profitability and

financial leverage of company are the key indicator to determine whether company has strong

financial position in the market or not. This research has reflected that how financial ratio

could have different bankruptcy- indicating abilities across industries and time. The main

goal of this research is to estimate models in such a way whether it could prevent company

from happening of negative outcomes (Altman, et al. 2014). Corporate default and failure is

often associated with the potential negative events in the particular situation when credit risk

is present. According to the Finance and Banking (Oxford Reference, 2012), default could be

defined as failure to make the required payment. Ideally, a bank goes into liquidation when

company fails to make the proper payment to its creditors. This liquidation and dissolving

problems arise due to the distress of the work process system of organization. Management

could use this financial and non-financial information as indication for their business failure.

For instance, if company fails to meet its set targets in the given time manner or having the

deficiency of the resources then it will showcase the negative indicator for the future growth

of the business. Therefore, mangers should use this information to prepare the proactive

strategic plan which will further add value for the better work satisfaction of the organization

(Abdullah,., 2016).

As stated by Calabrese, Marra, and Osmetti, (2016), it is divulged that the analysis of the

financial data and non-financial data is based on the two important factors such as rate of

return of business and economic rate of return. The rate of return of company shows the

return earned by company from its business and on the other hand, economic rate of return

divulges the allocation of the capital for the productive activity of the enterprise and are

financial decisions (Iturriaga, and Sanz, 2015). It is analyzed that the ratio analysis is ideally

used by the managers to establish the relation between the two financial factors and evaluate

whether the implemented decisions will add value to the clients satisfaction or not. It is

further observed capital budgeting tools such as NPV, IRR and profitability index are the key

to analysis whether company should invest their capital in particular project or not. In

addition to this, company also needs to analysis whether investing capital in the particular

project will have more output or not. Managers need to only accept those projects which

gives higher project benefits to the organization. All the financial information shown in the

annual report or financial statement of company needs to be analyzed whether investing

capital in the particular project will create value on the investment or not. All the financial

and non-financial information such as employee turnover, market share, profitability and

financial leverage of company are the key indicator to determine whether company has strong

financial position in the market or not. This research has reflected that how financial ratio

could have different bankruptcy- indicating abilities across industries and time. The main

goal of this research is to estimate models in such a way whether it could prevent company

from happening of negative outcomes (Altman, et al. 2014). Corporate default and failure is

often associated with the potential negative events in the particular situation when credit risk

is present. According to the Finance and Banking (Oxford Reference, 2012), default could be

defined as failure to make the required payment. Ideally, a bank goes into liquidation when

company fails to make the proper payment to its creditors. This liquidation and dissolving

problems arise due to the distress of the work process system of organization. Management

could use this financial and non-financial information as indication for their business failure.

For instance, if company fails to meet its set targets in the given time manner or having the

deficiency of the resources then it will showcase the negative indicator for the future growth

of the business. Therefore, mangers should use this information to prepare the proactive

strategic plan which will further add value for the better work satisfaction of the organization

(Abdullah,., 2016).

As stated by Calabrese, Marra, and Osmetti, (2016), it is divulged that the analysis of the

financial data and non-financial data is based on the two important factors such as rate of

return of business and economic rate of return. The rate of return of company shows the

return earned by company from its business and on the other hand, economic rate of return

divulges the allocation of the capital for the productive activity of the enterprise and are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

commonly used for analysis between firms in the same sector or different sectors irrespective

of the size and invested capital.

As per the views of Zainudin, and Hashim, (2016) it is analyzed that in order to

determine the bankrupt company and at what condition company goes into liquidation, it is

first required to read the bankruptcy rule and regulations. These rules and regulations are

used to assess the failure of companies, its negative outcomes on the business and restricted

business practices in the business. If company does not take into account the proper methods

and work process system then it will lead to liquidation of company. In case of the

bankruptcy and liquidation of company, it is analyzed that company fails to pay off its debts

and creditors are filling case against the company for their debt funding. It is observed that if

managers could know their future expectation and responsibilities in long run then they could

easily set up proper work functions program to arrange capital for their business.

As stated by Aris, et al, (2015) it is reflected that the Z score approach is used to analysis the

methods of measuring and interpretation of the risk to which investors who invested capital

and enterprises exposed.

This measurement is used for development of value judgments that linear combine a group of

financial ratios or of significant variables.

The score functions are accompanied with the following details

: Z = a1*X1 + a2*X2 + a3*X3 + … + an*Xn

(Almamy, Aston, and Ngwa, 2016).

Credit risk models

As per the views of the Kim,. Kang,. and Kim, (2015) it is reflected that there are

ideally two credit risk models which could be used to assess the financial performance and

future outlook of the business in long run. The first group consists of accounting based

models which predict the corporate failure estimation of the reason of the failure of these

companies. The other model group consists of the market based model in which the market

entries and future perspective of the future will be undertaken for the better handling of the

of the size and invested capital.

As per the views of Zainudin, and Hashim, (2016) it is analyzed that in order to

determine the bankrupt company and at what condition company goes into liquidation, it is

first required to read the bankruptcy rule and regulations. These rules and regulations are

used to assess the failure of companies, its negative outcomes on the business and restricted

business practices in the business. If company does not take into account the proper methods

and work process system then it will lead to liquidation of company. In case of the

bankruptcy and liquidation of company, it is analyzed that company fails to pay off its debts

and creditors are filling case against the company for their debt funding. It is observed that if

managers could know their future expectation and responsibilities in long run then they could

easily set up proper work functions program to arrange capital for their business.

As stated by Aris, et al, (2015) it is reflected that the Z score approach is used to analysis the

methods of measuring and interpretation of the risk to which investors who invested capital

and enterprises exposed.

This measurement is used for development of value judgments that linear combine a group of

financial ratios or of significant variables.

The score functions are accompanied with the following details

: Z = a1*X1 + a2*X2 + a3*X3 + … + an*Xn

(Almamy, Aston, and Ngwa, 2016).

Credit risk models

As per the views of the Kim,. Kang,. and Kim, (2015) it is reflected that there are

ideally two credit risk models which could be used to assess the financial performance and

future outlook of the business in long run. The first group consists of accounting based

models which predict the corporate failure estimation of the reason of the failure of these

companies. The other model group consists of the market based model in which the market

entries and future perspective of the future will be undertaken for the better handling of the

cases. As per the views of Mohammed, (2016), it is divulged that the credit risk models are

used to assess the whether the existing resources of the company will be enough to meet the

future responsibility of the company. If managers identify the issues and problems faced by

company then it will add value for the handling the financial distress issues and also prepare

company for the financial management in determined approach (Ballings, Van den Poel,

Hespeels, and Gryp, 2015).

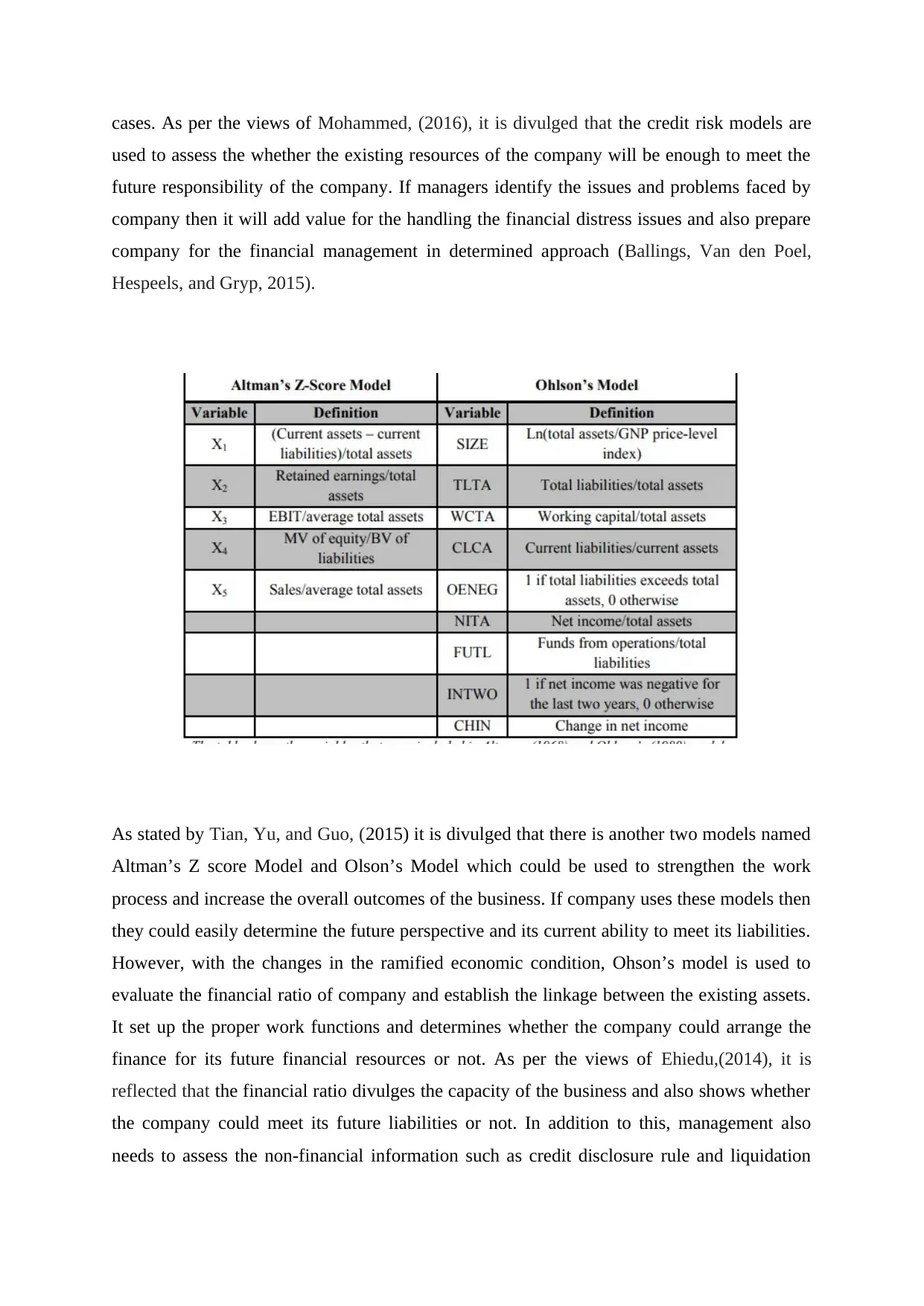

As stated by Tian, Yu, and Guo, (2015) it is divulged that there is another two models named

Altman’s Z score Model and Olson’s Model which could be used to strengthen the work

process and increase the overall outcomes of the business. If company uses these models then

they could easily determine the future perspective and its current ability to meet its liabilities.

However, with the changes in the ramified economic condition, Ohson’s model is used to

evaluate the financial ratio of company and establish the linkage between the existing assets.

It set up the proper work functions and determines whether the company could arrange the

finance for its future financial resources or not. As per the views of Ehiedu,(2014), it is

reflected that the financial ratio divulges the capacity of the business and also shows whether

the company could meet its future liabilities or not. In addition to this, management also

needs to assess the non-financial information such as credit disclosure rule and liquidation

used to assess the whether the existing resources of the company will be enough to meet the

future responsibility of the company. If managers identify the issues and problems faced by

company then it will add value for the handling the financial distress issues and also prepare

company for the financial management in determined approach (Ballings, Van den Poel,

Hespeels, and Gryp, 2015).

As stated by Tian, Yu, and Guo, (2015) it is divulged that there is another two models named

Altman’s Z score Model and Olson’s Model which could be used to strengthen the work

process and increase the overall outcomes of the business. If company uses these models then

they could easily determine the future perspective and its current ability to meet its liabilities.

However, with the changes in the ramified economic condition, Ohson’s model is used to

evaluate the financial ratio of company and establish the linkage between the existing assets.

It set up the proper work functions and determines whether the company could arrange the

finance for its future financial resources or not. As per the views of Ehiedu,(2014), it is

reflected that the financial ratio divulges the capacity of the business and also shows whether

the company could meet its future liabilities or not. In addition to this, management also

needs to assess the non-financial information such as credit disclosure rule and liquidation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

rules and regulation. Managers need to evaluate when and how company goes in the

liquidation. These are the main factors which make managers more proactive towards

restricting the situation of the liquidation.

As per the views of Jan, and Marimuthu, (2015) it is divulged that managers are the key

managerial persons who take all the key imperative decisions. It is analyzed that proper

management strategies and strategic programs to maintain the effective work structure in

determined approach. The bankruptcy and liquidation of the organization is dependent upon

the management strategies and financial strategic planning. If company could manage the

proper financial strategic planning in its business then it will add value for the sustainable

business strategies.

As stated by Ishibashi, et al. (2017) this could be illustrated with the given example that in

One Tel Company, managers could have identified the financial risk of the business which

company faced due to the non-efficient business functioning. They could have used the debt

to equity structure and profitability ratio of business. The financial statement of One Tel

Company reflected only thorough information regarding the financial and non-financial

information of the business. The financial statement could only divulge the present and

future outcomes of the business. However, managers could have used the financial analysis

tools such as ratio analysis, capital budgeting, du Pont analysis and top down analysis to

evaluate the deficiency and possibility of the non-effective business functioning.

liquidation. These are the main factors which make managers more proactive towards

restricting the situation of the liquidation.

As per the views of Jan, and Marimuthu, (2015) it is divulged that managers are the key

managerial persons who take all the key imperative decisions. It is analyzed that proper

management strategies and strategic programs to maintain the effective work structure in

determined approach. The bankruptcy and liquidation of the organization is dependent upon

the management strategies and financial strategic planning. If company could manage the

proper financial strategic planning in its business then it will add value for the sustainable

business strategies.

As stated by Ishibashi, et al. (2017) this could be illustrated with the given example that in

One Tel Company, managers could have identified the financial risk of the business which

company faced due to the non-efficient business functioning. They could have used the debt

to equity structure and profitability ratio of business. The financial statement of One Tel

Company reflected only thorough information regarding the financial and non-financial

information of the business. The financial statement could only divulge the present and

future outcomes of the business. However, managers could have used the financial analysis

tools such as ratio analysis, capital budgeting, du Pont analysis and top down analysis to

evaluate the deficiency and possibility of the non-effective business functioning.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Abdullah, A.A., 2016. Financial Statement Analysis for Kier Group PLC. Global Journal of

Management And Business Research.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the

UK. Journal of Corporate Finance, 36, pp.278-285.

Altman, E., Iwanicz-Drozdowska, M., Laitinen, E. and Suvas, A., 2014. Distressed Firm and

Bankruptcy Prediction in an International Context: A Review and Empirical Analysis of

Altman's Z-Score Model.

Altman, E.I., Iwanicz-Drozdowska, M., Laitinen, E.K. and Suvas, A., 2015. Financial and

non-financial variables as long-horizon predictors of bankruptcy.

Aris, N.A., Arif, S.M.M., Othman, R. and Zain, M.M., 2015. Fraudulent financial statement

detection using statistical techniques: The case of small medium automotive

enterprise. Journal of Applied Business Research, 31(4), p.1469.

Ballings, M., Van den Poel, D., Hespeels, N. and Gryp, R., 2015. Evaluating multiple

classifiers for stock price direction prediction. Expert Systems with Applications, 42(20),

pp.7046-7056.

Calabrese, R., Marra, G. and Osmetti, S.A., 2016. Bankruptcy prediction of small and

medium enterprises using a flexible binary generalized extreme value model. Journal of the

Operational Research Society, 67(4), pp.604-615.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), pp.81-90.

Gupta, J., Gregoriou, A. and Healy, J., 2015. Forecasting bankruptcy for SMEs using hazard

function: To what extent does size matter?. Review of Quantitative Finance and

Accounting, 45(4), pp.845-869.

Ishibashi, K., Iwasaki, T., Otomasa, S. and Yada, K., 2017, October. Model selection for

financial statement analysis: Comparison of models developed by using data mining

technique. In Systems, Man, and Cybernetics (SMC), 2017 IEEE International Conference

on (pp. 81-86). IEEE.

Iturriaga, F.J.L. and Sanz, I.P., 2015. Bankruptcy visualization and prediction using neural

networks: A study of US commercial banks. Expert Systems with applications, 42(6),

pp.2857-2869.

Jan, A. and Marimuthu, M., 2015. Altman model and bankruptcy profile of islamic banking

industry: A comparative analysis on financial performance. International Journal of Business

and Management, 10(7), p.110.

Kim, M.J., Kang, D.K. and Kim, H.B., 2015. Geometric mean based boosting algorithm with

over-sampling to resolve data imbalance problem for bankruptcy prediction. Expert Systems

with Applications, 42(3), pp.1074-1082.

Abdullah, A.A., 2016. Financial Statement Analysis for Kier Group PLC. Global Journal of

Management And Business Research.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the

UK. Journal of Corporate Finance, 36, pp.278-285.

Altman, E., Iwanicz-Drozdowska, M., Laitinen, E. and Suvas, A., 2014. Distressed Firm and

Bankruptcy Prediction in an International Context: A Review and Empirical Analysis of

Altman's Z-Score Model.

Altman, E.I., Iwanicz-Drozdowska, M., Laitinen, E.K. and Suvas, A., 2015. Financial and

non-financial variables as long-horizon predictors of bankruptcy.

Aris, N.A., Arif, S.M.M., Othman, R. and Zain, M.M., 2015. Fraudulent financial statement

detection using statistical techniques: The case of small medium automotive

enterprise. Journal of Applied Business Research, 31(4), p.1469.

Ballings, M., Van den Poel, D., Hespeels, N. and Gryp, R., 2015. Evaluating multiple

classifiers for stock price direction prediction. Expert Systems with Applications, 42(20),

pp.7046-7056.

Calabrese, R., Marra, G. and Osmetti, S.A., 2016. Bankruptcy prediction of small and

medium enterprises using a flexible binary generalized extreme value model. Journal of the

Operational Research Society, 67(4), pp.604-615.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), pp.81-90.

Gupta, J., Gregoriou, A. and Healy, J., 2015. Forecasting bankruptcy for SMEs using hazard

function: To what extent does size matter?. Review of Quantitative Finance and

Accounting, 45(4), pp.845-869.

Ishibashi, K., Iwasaki, T., Otomasa, S. and Yada, K., 2017, October. Model selection for

financial statement analysis: Comparison of models developed by using data mining

technique. In Systems, Man, and Cybernetics (SMC), 2017 IEEE International Conference

on (pp. 81-86). IEEE.

Iturriaga, F.J.L. and Sanz, I.P., 2015. Bankruptcy visualization and prediction using neural

networks: A study of US commercial banks. Expert Systems with applications, 42(6),

pp.2857-2869.

Jan, A. and Marimuthu, M., 2015. Altman model and bankruptcy profile of islamic banking

industry: A comparative analysis on financial performance. International Journal of Business

and Management, 10(7), p.110.

Kim, M.J., Kang, D.K. and Kim, H.B., 2015. Geometric mean based boosting algorithm with

over-sampling to resolve data imbalance problem for bankruptcy prediction. Expert Systems

with Applications, 42(3), pp.1074-1082.

Lakshmi, T.M., Martin, A. and Venkatesan, V.P., 2016. A genetic bankrupt ratio analysis tool

using a genetic algorithm to identify influencing financial ratios. IEEE Transactions on

Evolutionary Computation, 20(1), pp.38-51.

Liang, D., Lu, C.C., Tsai, C.F. and Shih, G.A., 2016. Financial ratios and corporate

governance indicators in bankruptcy prediction: A comprehensive study. European Journal

of Operational Research, 252(2), pp.561-572.

Mohammed, S., 2016. Bankruptcy Prediction Using the Altman Z-score Model in Oman: A

Case Study of Raysut Cement Company SAOG and its subsidiaries. Australasian Accounting

Business & Finance Journal, 10(4), p.70.

Tian, S., Yu, Y. and Guo, H., 2015. Variable selection and corporate bankruptcy

forecasts. Journal of Banking & Finance, 52, pp.89-100.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Yu, Q., Miche, Y., Séverin, E. and Lendasse, A., 2014. Bankruptcy prediction using extreme

learning machine and financial expertise. Neurocomputing, 128, pp.296-302.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using

financial ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Zięba, M., Tomczak, S.K. and Tomczak, J.M., 2016. Ensemble boosted trees with synthetic

features generation in application to bankruptcy prediction. Expert Systems with

Applications, 58, pp.93-101.

using a genetic algorithm to identify influencing financial ratios. IEEE Transactions on

Evolutionary Computation, 20(1), pp.38-51.

Liang, D., Lu, C.C., Tsai, C.F. and Shih, G.A., 2016. Financial ratios and corporate

governance indicators in bankruptcy prediction: A comprehensive study. European Journal

of Operational Research, 252(2), pp.561-572.

Mohammed, S., 2016. Bankruptcy Prediction Using the Altman Z-score Model in Oman: A

Case Study of Raysut Cement Company SAOG and its subsidiaries. Australasian Accounting

Business & Finance Journal, 10(4), p.70.

Tian, S., Yu, Y. and Guo, H., 2015. Variable selection and corporate bankruptcy

forecasts. Journal of Banking & Finance, 52, pp.89-100.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Yu, Q., Miche, Y., Séverin, E. and Lendasse, A., 2014. Bankruptcy prediction using extreme

learning machine and financial expertise. Neurocomputing, 128, pp.296-302.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using

financial ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Zięba, M., Tomczak, S.K. and Tomczak, J.M., 2016. Ensemble boosted trees with synthetic

features generation in application to bankruptcy prediction. Expert Systems with

Applications, 58, pp.93-101.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.