Financial Statement Analysis of Barclays PLC: A Detailed Report

VerifiedAdded on 2020/02/05

|27

|6309

|474

Report

AI Summary

This report provides a comprehensive financial statement analysis of Barclays PLC. It begins with an overview of the company, including its history, services, and reasons for selection, followed by an identification of key announcements and financial trends influenced by internal and external environmental factors. The core of the report involves a detailed computation of Barclays' financial health, evaluating liquidity, efficiency, gearing, and profitability ratios, along with an analysis of the cash flow statement. The analysis includes interpretations of operational performance, financial performance, and investor perspectives. Finally, the report concludes with a summary of financial strengths and weaknesses, along with recommendations for improvement. The assignment utilizes financial data and industry knowledge to assess the financial position and performance of Barclays PLC. The report also provides insights into the factors affecting the company's financial health, making it a valuable resource for understanding financial statement analysis.

STUDENT NAME:

STUDENT ID:

SUBJECT CODE:

ASSIGNMENT TITLE: FINANCIAL STTAEEMT ANALYSIS

STUDENT ID:

SUBJECT CODE:

ASSIGNMENT TITLE: FINANCIAL STTAEEMT ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of content

Introduction......................................................................................................................................3

Part A...............................................................................................................................................4

1) Overview of Barclays PLC and the reason for selecting the company.......................................4

2) Identification of different key announcements............................................................................5

3) Identification of key financial trends of the company with internal and external environmental

factors..............................................................................................................................................5

Part B Computation of financial health of the company.................................................................8

1) Evaluation of liquidity ratios.....................................................................................................11

2) Interpretation of operational performance of the company through efficiency ratios...............13

3) Gearing ratios for evaluating financial performance.................................................................14

4) Evaluation of profitability ratios...............................................................................................15

5) Ratios on Investors analysis......................................................................................................17

6) Analysis of cash flow statement................................................................................................18

Part C Findings and recommendations..........................................................................................20

1) Financial strengths and weaknesses..........................................................................................20

2) Conclusion and recommendations.............................................................................................20

Reference list.................................................................................................................................22

Appendices:...................................................................................................................................24

Appendix 1.....................................................................................................................................24

Appendix 2.....................................................................................................................................24

Introduction......................................................................................................................................3

Part A...............................................................................................................................................4

1) Overview of Barclays PLC and the reason for selecting the company.......................................4

2) Identification of different key announcements............................................................................5

3) Identification of key financial trends of the company with internal and external environmental

factors..............................................................................................................................................5

Part B Computation of financial health of the company.................................................................8

1) Evaluation of liquidity ratios.....................................................................................................11

2) Interpretation of operational performance of the company through efficiency ratios...............13

3) Gearing ratios for evaluating financial performance.................................................................14

4) Evaluation of profitability ratios...............................................................................................15

5) Ratios on Investors analysis......................................................................................................17

6) Analysis of cash flow statement................................................................................................18

Part C Findings and recommendations..........................................................................................20

1) Financial strengths and weaknesses..........................................................................................20

2) Conclusion and recommendations.............................................................................................20

Reference list.................................................................................................................................22

Appendices:...................................................................................................................................24

Appendix 1.....................................................................................................................................24

Appendix 2.....................................................................................................................................24

Introduction

Financial position signifies financial and accounting status of a respective business organisation.

Financial position and its statements of a respective company include the profits, loss,

investments, capitals etc. which are evident and help business analyzers and professionals to get

all the information regarding financial status and statements of the company as well. In this

respect, it should be highly identified that researchers need to choose a significant company in

order to represent its current financial status and position in its marketplace. Moreover, the

researchers also try to represent and calculate the final ratio of the company as well ( Weil et al.

2013, p.111). Other than this, it is also formulated that financial status also verifies and compares

the company’s past and present status of financial and accounting management. Along with the

comparison, accountant managers and financial managers try to evaluate the financial status and

position so that the company can be able to improve financial position and statement of the

company so that the respective company acquire a significant and reputed position in its

marketplace (Hirsa and Neftci, 2013, p.101).

The thesis statement of this assignment study is to analyze a company’s financial and accounting

position by representing its current ratios and also the evaluation of the ratios as well. In this

respect, researchers need to collect and gather more information and data regarding that specific

selected company so that the research analysis of this assignment may provide all the ratio

analysis, financial strengths and weaknesses, key financial trends of the company with internal

and external environmental factors, evaluation of profitability ratios and so on to the readers and

other business professionals and analysers, who will go through the assignment (Davies and

Green, 2013, p.100).

Financial position signifies financial and accounting status of a respective business organisation.

Financial position and its statements of a respective company include the profits, loss,

investments, capitals etc. which are evident and help business analyzers and professionals to get

all the information regarding financial status and statements of the company as well. In this

respect, it should be highly identified that researchers need to choose a significant company in

order to represent its current financial status and position in its marketplace. Moreover, the

researchers also try to represent and calculate the final ratio of the company as well ( Weil et al.

2013, p.111). Other than this, it is also formulated that financial status also verifies and compares

the company’s past and present status of financial and accounting management. Along with the

comparison, accountant managers and financial managers try to evaluate the financial status and

position so that the company can be able to improve financial position and statement of the

company so that the respective company acquire a significant and reputed position in its

marketplace (Hirsa and Neftci, 2013, p.101).

The thesis statement of this assignment study is to analyze a company’s financial and accounting

position by representing its current ratios and also the evaluation of the ratios as well. In this

respect, researchers need to collect and gather more information and data regarding that specific

selected company so that the research analysis of this assignment may provide all the ratio

analysis, financial strengths and weaknesses, key financial trends of the company with internal

and external environmental factors, evaluation of profitability ratios and so on to the readers and

other business professionals and analysers, who will go through the assignment (Davies and

Green, 2013, p.100).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part A

1) Overview of Barclays PLC and the reason for selecting the company

Overview of the company: In order to represent current ratios and evaluation of profitability

ratios and other respective financial reports, one has chosen Barclays PLC respectively. This

company has been founded on 17th November, 1690 in the city of London, United Kingdom.

Headquarter of this company is also situated in One Churchill Place, Canary Wharf, London,

UK.

Barclays is a banking and financial organisation which provides every positive and significant

functions to its customers regarding accounting and financial systems as well (Foulds et al. 2015,

p.371). All these financial systems may include savings of finance, investment, mortgage and

other services related to finance. In this respect, it should be mentioned that Barclays PLC is a

universal bank and it provides its services to the customers throughout the world. In order to

provide some significant information regarding this company, one should highlight that it has

nearly 48 million customers and it performs its operations in 50 countries and territories

reflectively. Moreover, its key people are John McFarlane, the chairman and Jes Staley, Group

Chief Executive (Barclays.co.uk. 2017). This bank includes retail banking, commercial banking,

investment banking and investment management as its services, for which its customers get

highlighted and high quality services regarding their finance and accounting management.

However, the total revenue of this bank is $25.454 billion. Total operating income of this

company is $2.073 billion.

Reason for selecting the company: This Company has been selected for the analysis of this

assignment study of financial position for specific and evaluative reason as well. Some reasons

are highly evaluative and important in order to present financial position and statement of this

company as well (Sahoo and Vidyadhar Reddy, 2014, p.99). It is to be highly signified that as

this is a banking and financial company, people can be able to get more data and information

regarding current and past ratios, profit, loss etc. In this respect, it should be designated that this

company was facing some troubles regarding financial and accounting analysis and ratios from

recent past years. But, in the most recent days, the business analysers and accounting managers

are trying to evaluate and improve their services so that the financial position and statements of

this company can be able to highlight its management and marketplace as well. However, it is to

1) Overview of Barclays PLC and the reason for selecting the company

Overview of the company: In order to represent current ratios and evaluation of profitability

ratios and other respective financial reports, one has chosen Barclays PLC respectively. This

company has been founded on 17th November, 1690 in the city of London, United Kingdom.

Headquarter of this company is also situated in One Churchill Place, Canary Wharf, London,

UK.

Barclays is a banking and financial organisation which provides every positive and significant

functions to its customers regarding accounting and financial systems as well (Foulds et al. 2015,

p.371). All these financial systems may include savings of finance, investment, mortgage and

other services related to finance. In this respect, it should be mentioned that Barclays PLC is a

universal bank and it provides its services to the customers throughout the world. In order to

provide some significant information regarding this company, one should highlight that it has

nearly 48 million customers and it performs its operations in 50 countries and territories

reflectively. Moreover, its key people are John McFarlane, the chairman and Jes Staley, Group

Chief Executive (Barclays.co.uk. 2017). This bank includes retail banking, commercial banking,

investment banking and investment management as its services, for which its customers get

highlighted and high quality services regarding their finance and accounting management.

However, the total revenue of this bank is $25.454 billion. Total operating income of this

company is $2.073 billion.

Reason for selecting the company: This Company has been selected for the analysis of this

assignment study of financial position for specific and evaluative reason as well. Some reasons

are highly evaluative and important in order to present financial position and statement of this

company as well (Sahoo and Vidyadhar Reddy, 2014, p.99). It is to be highly signified that as

this is a banking and financial company, people can be able to get more data and information

regarding current and past ratios, profit, loss etc. In this respect, it should be designated that this

company was facing some troubles regarding financial and accounting analysis and ratios from

recent past years. But, in the most recent days, the business analysers and accounting managers

are trying to evaluate and improve their services so that the financial position and statements of

this company can be able to highlight its management and marketplace as well. However, it is to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be informed that researchers have chose this company for this assignment study so that they can

be able to get financial reports and annual reports of finance and accounting definitely and

significantly. If researchers get exact and sufficient data of financial reports and background,

improving and evaluating and also creating a significant data chart and providing information

regarding financial currency and statements to the customers are very easy for them to manage

(Crook, 2014, p.38). Therefore, this company has been selected by the researchers for this

assignment study as well.

2) Identification of different key announcements

In this assignment in order to analyse financial statement it should have to evaluate the different

announcements that the company have been made that can affect company’s financial

performance and financial position. Barclays plc in order to increase their efficiency level and

performance have implemented certain steps regarding investment and mortgage securities if the

company. The management team of the company have signed an agreement with the UK trust

organisation that can lead to increase the sales pattern and increase in growth level is possible.

It has been evaluated from the annual report of Barclays that the company have simplified their

strategies that can help to measure financial performance level and strengthening the base of

capital and control cost effectively and efficiently.

3) Identification of key financial trends of the company with internal and

external environmental factors

In order to evaluate financial statement analysis identification of the key financial trends of the

company should have to be done in an efficient manner by the management team of the

company. Preparation of financial statement depending on the key financial trends and

environmental factors affecting business operations of a company should have to be considered

effectively and efficiently for smooth flow of operations is considered as an important factor in

this regard. In this assignment of financial statement analysis the selected company is Barclays

PLC, a public limited company listed in the London stock exchange is the largest banking

organisation in the World providing services relating to investment banking, wealth management

and financial services appropriately in an efficient manner. Barclays bank of London, UK

operates in the Whole World and the operations and performance are affected by the economic

be able to get financial reports and annual reports of finance and accounting definitely and

significantly. If researchers get exact and sufficient data of financial reports and background,

improving and evaluating and also creating a significant data chart and providing information

regarding financial currency and statements to the customers are very easy for them to manage

(Crook, 2014, p.38). Therefore, this company has been selected by the researchers for this

assignment study as well.

2) Identification of different key announcements

In this assignment in order to analyse financial statement it should have to evaluate the different

announcements that the company have been made that can affect company’s financial

performance and financial position. Barclays plc in order to increase their efficiency level and

performance have implemented certain steps regarding investment and mortgage securities if the

company. The management team of the company have signed an agreement with the UK trust

organisation that can lead to increase the sales pattern and increase in growth level is possible.

It has been evaluated from the annual report of Barclays that the company have simplified their

strategies that can help to measure financial performance level and strengthening the base of

capital and control cost effectively and efficiently.

3) Identification of key financial trends of the company with internal and

external environmental factors

In order to evaluate financial statement analysis identification of the key financial trends of the

company should have to be done in an efficient manner by the management team of the

company. Preparation of financial statement depending on the key financial trends and

environmental factors affecting business operations of a company should have to be considered

effectively and efficiently for smooth flow of operations is considered as an important factor in

this regard. In this assignment of financial statement analysis the selected company is Barclays

PLC, a public limited company listed in the London stock exchange is the largest banking

organisation in the World providing services relating to investment banking, wealth management

and financial services appropriately in an efficient manner. Barclays bank of London, UK

operates in the Whole World and the operations and performance are affected by the economic

and changes conditions and it can be evaluated through PESTLE analysis effectively. In these

context environmental factors such as the internal and external factors impacting the financial

operations and performance of the company should have to be evaluated as follows:

External factors-

Political factors: Political factors can directly affect the financial performance and operations of

a company. Political factors such as welfare and social policies and regulations, taxation policies

and their changes that ca directly affect the production capacity of a company (Bekaert et al.

2016, p.22). Barclays plc also affected by the taxation policies. Government stability is another

political factor that can help the operation and production functions such as Barclays to expand

their business operations.

Economic factors: Economic factors such as interest rates, business cycle of the company,

money supply in the economy, level of lifestyle and consumerism rate can directly impact on the

performance level of the company (Roncalli and Weisang, 2016, p.377). Depending on these

factors the management team of Barclays have to decide productivity planning and operations to

manufacture products and services according to the requirements of the customers such as

investment and wealth management services.

Social factors: Social factors impact on the productivity of Barclays that according to a survey it

has been found that the business transactions in 2014 has increased from 59% to 75% effectively

and efficiently that lead the company to higher profitability and revenue (Sharma and Crossler,

2014, p.305).

Technological factors: Technological factors that affect the business operations of Barclays

PLC are mainly the government spending, technological changes, speed of transfer of

infrastructural and technological affect the business operations that lead the company to increase

productivity and returns.

Legal factors: Product safety and services, different employment laws, regulations and

legislations of monopolies and accounting laws and policies should have to be followed by the

directors and management team of the Barclays plc in order to prepare financial statements that

can reveal true and fair view of the annual reports effectively and efficiently in this regard.

Environmental factors: In order to evaluate the financial report of the Barclays PLC, banking

organisation of London, external factors affecting the financial position and operations of the

company should have to be interpreted appropriately to view effectiveness on business (Epstein

context environmental factors such as the internal and external factors impacting the financial

operations and performance of the company should have to be evaluated as follows:

External factors-

Political factors: Political factors can directly affect the financial performance and operations of

a company. Political factors such as welfare and social policies and regulations, taxation policies

and their changes that ca directly affect the production capacity of a company (Bekaert et al.

2016, p.22). Barclays plc also affected by the taxation policies. Government stability is another

political factor that can help the operation and production functions such as Barclays to expand

their business operations.

Economic factors: Economic factors such as interest rates, business cycle of the company,

money supply in the economy, level of lifestyle and consumerism rate can directly impact on the

performance level of the company (Roncalli and Weisang, 2016, p.377). Depending on these

factors the management team of Barclays have to decide productivity planning and operations to

manufacture products and services according to the requirements of the customers such as

investment and wealth management services.

Social factors: Social factors impact on the productivity of Barclays that according to a survey it

has been found that the business transactions in 2014 has increased from 59% to 75% effectively

and efficiently that lead the company to higher profitability and revenue (Sharma and Crossler,

2014, p.305).

Technological factors: Technological factors that affect the business operations of Barclays

PLC are mainly the government spending, technological changes, speed of transfer of

infrastructural and technological affect the business operations that lead the company to increase

productivity and returns.

Legal factors: Product safety and services, different employment laws, regulations and

legislations of monopolies and accounting laws and policies should have to be followed by the

directors and management team of the Barclays plc in order to prepare financial statements that

can reveal true and fair view of the annual reports effectively and efficiently in this regard.

Environmental factors: In order to evaluate the financial report of the Barclays PLC, banking

organisation of London, external factors affecting the financial position and operations of the

company should have to be interpreted appropriately to view effectiveness on business (Epstein

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Buhovac, 2014, p.112). The company should have to follow certain laws relating

environment such as waste disposal law and energy consumption that directly impact financial

performance.

Internal factors- Internal factors such as organisational structures, relationship[ between

managers, workers and employees among the company, objectives and aims, business strategies

of the company are considered as the main internal factors that can influence business operations

effectively and efficiently.

Organisational structures: Organisational structure and strategy of this company is to focus on

the customers of UK in order enhance their business scale with investment banking, wealth

management and personal banking (Bies et al. 2016, p.245). Such organisational strategy helps

the business to enhance their operations to international market in order to gain competitive

advantage and marketing capabilities.

Objectives and aims: Barclays plc’s objectives and aims is to serve people to help them achieve

their objectives such as investment banking and wealth management that can affect on the

balance scorecard of the company effectively. Standardised and quality financial services should

have to provide that can lead to create brand loyalty of the company and increase in the

profitability level.

environment such as waste disposal law and energy consumption that directly impact financial

performance.

Internal factors- Internal factors such as organisational structures, relationship[ between

managers, workers and employees among the company, objectives and aims, business strategies

of the company are considered as the main internal factors that can influence business operations

effectively and efficiently.

Organisational structures: Organisational structure and strategy of this company is to focus on

the customers of UK in order enhance their business scale with investment banking, wealth

management and personal banking (Bies et al. 2016, p.245). Such organisational strategy helps

the business to enhance their operations to international market in order to gain competitive

advantage and marketing capabilities.

Objectives and aims: Barclays plc’s objectives and aims is to serve people to help them achieve

their objectives such as investment banking and wealth management that can affect on the

balance scorecard of the company effectively. Standardised and quality financial services should

have to provide that can lead to create brand loyalty of the company and increase in the

profitability level.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B Computation of financial health of the company

Every business organisation should have to analyse their financial reports and statements for

evaluating the financial ratios of the company effectively that can reflect on the financial

positions, strengths and weaknesses of the organisation for a financial year effectively and

efficiently. In this regard the selected company is Barclays PLC, largest banking company of UK

for which ratio analysis should have to be done through liquidity ratio, efficiency ratio, gearing

ratio, profitability and dividend ratio (Freund and Mustaro, 2016, p.206). Depending on these

ratios the organisational management team can make operational decisions and planning

regarding expansion of business operations and profitability that can help to create brand loyalty

appropriately.

Ratio analysis: Accounting tools and techniques include the ratio analysis process as an

important aspect of the financial statement in order to find financial position and strengths and

weakness of a company for particular financial year effectively by the management team that can

help them to make financial decisions regarding investment. It is also considered that effective

planning is the main key of ratio analysis in order to understand and evaluate financial statement

appropriately (Tsai et al. 2016, p.3314). In order to analyse the financial statement of Barclays

plc it is also important to interpret ratios.

Importance of ratio analysis can be evaluated that it can help to judge the operational efficiency

for a particular time period for formulating plans and policies. In order to grow ad increase

performance level of the organisation comparative analysis can be done which can lead to

manage the operations and productivity level (Camin et al. 2016, p.870).

Every business organisation should have to analyse their financial reports and statements for

evaluating the financial ratios of the company effectively that can reflect on the financial

positions, strengths and weaknesses of the organisation for a financial year effectively and

efficiently. In this regard the selected company is Barclays PLC, largest banking company of UK

for which ratio analysis should have to be done through liquidity ratio, efficiency ratio, gearing

ratio, profitability and dividend ratio (Freund and Mustaro, 2016, p.206). Depending on these

ratios the organisational management team can make operational decisions and planning

regarding expansion of business operations and profitability that can help to create brand loyalty

appropriately.

Ratio analysis: Accounting tools and techniques include the ratio analysis process as an

important aspect of the financial statement in order to find financial position and strengths and

weakness of a company for particular financial year effectively by the management team that can

help them to make financial decisions regarding investment. It is also considered that effective

planning is the main key of ratio analysis in order to understand and evaluate financial statement

appropriately (Tsai et al. 2016, p.3314). In order to analyse the financial statement of Barclays

plc it is also important to interpret ratios.

Importance of ratio analysis can be evaluated that it can help to judge the operational efficiency

for a particular time period for formulating plans and policies. In order to grow ad increase

performance level of the organisation comparative analysis can be done which can lead to

manage the operations and productivity level (Camin et al. 2016, p.870).

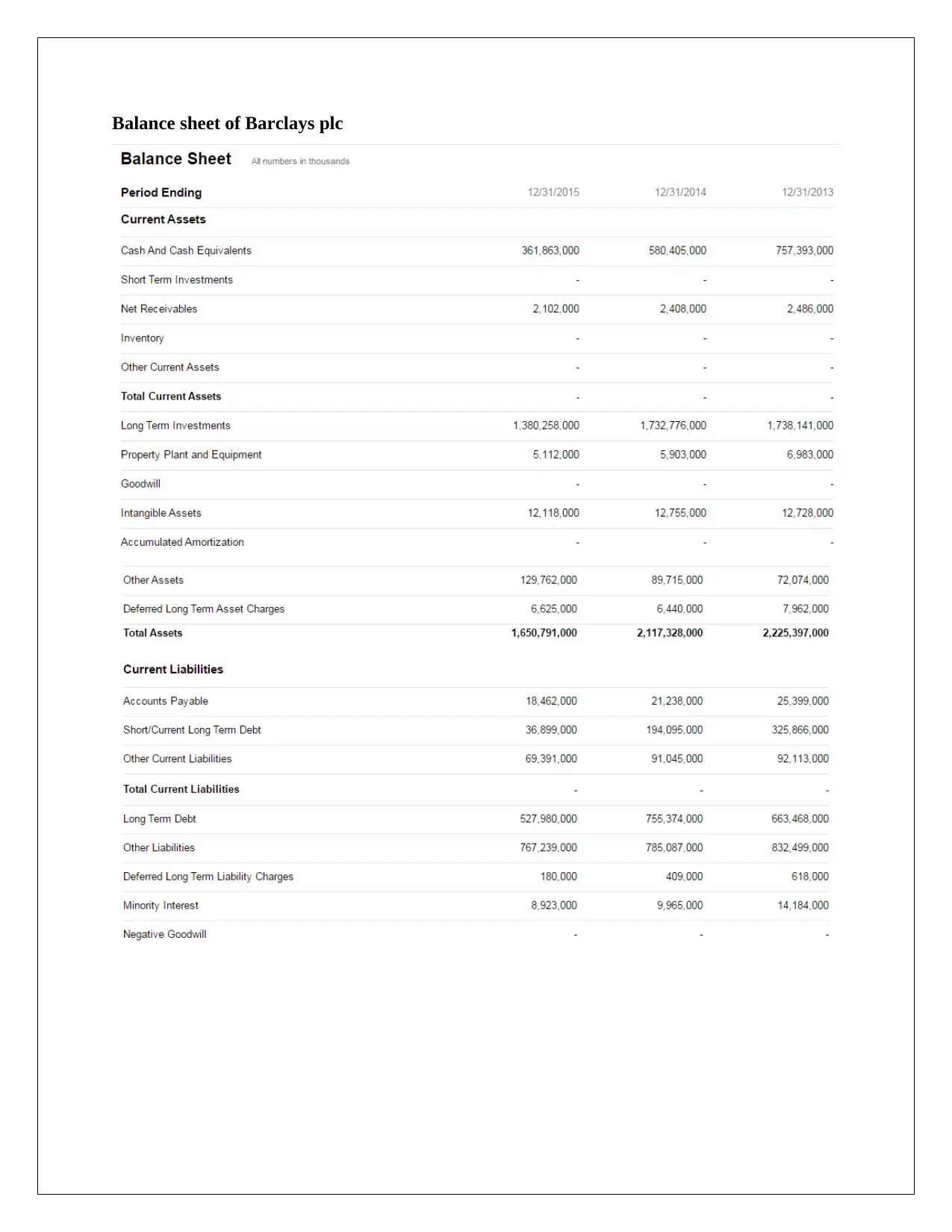

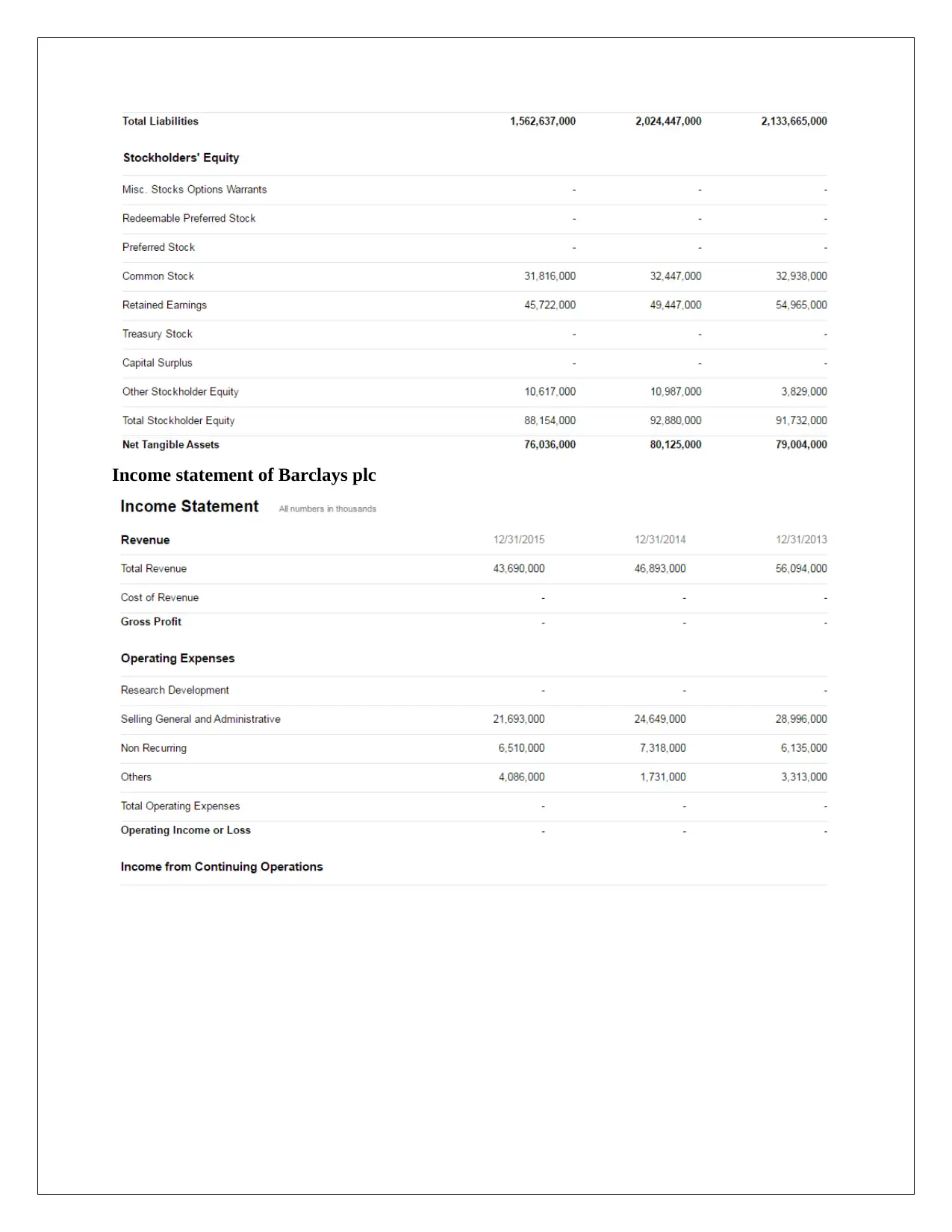

Balance sheet of Barclays plc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

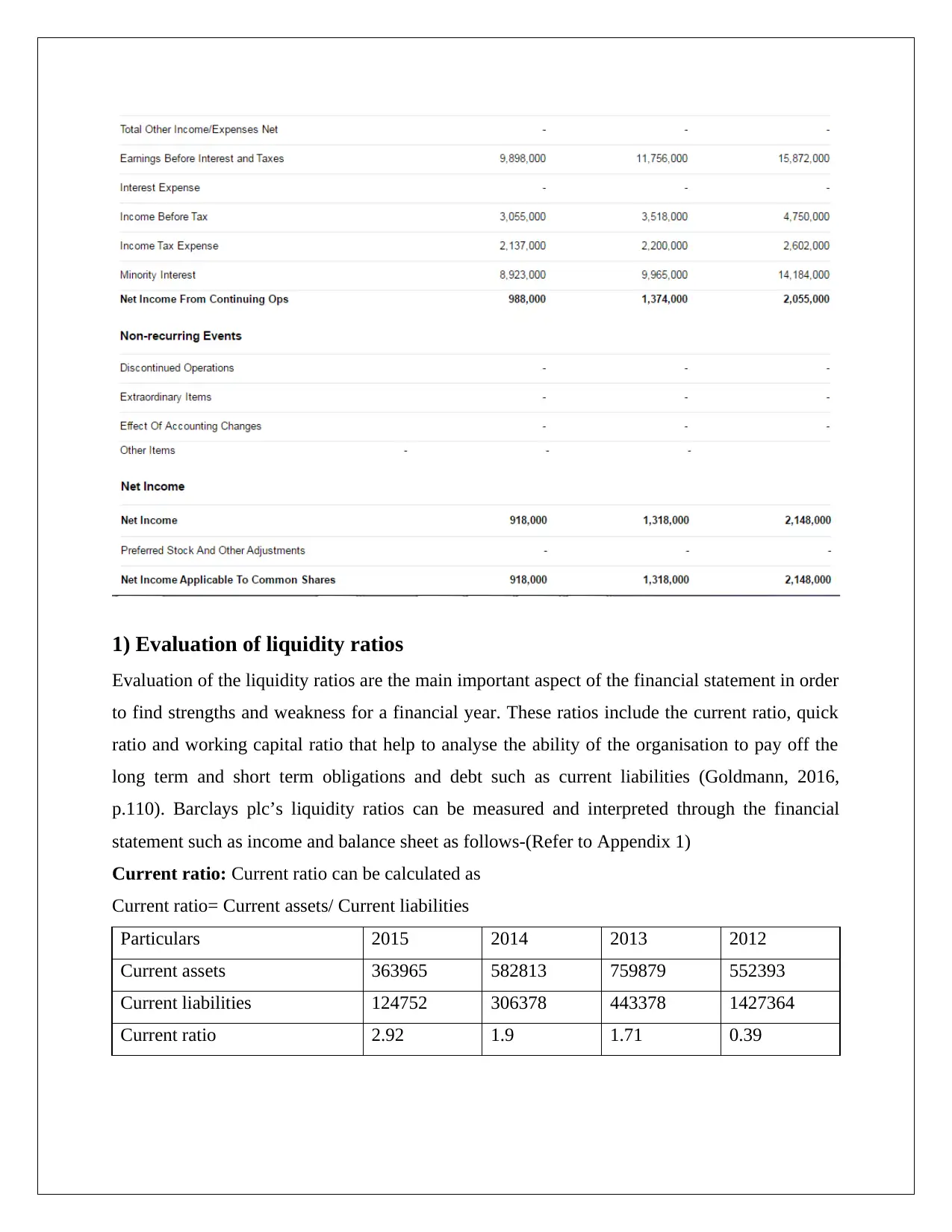

Income statement of Barclays plc

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

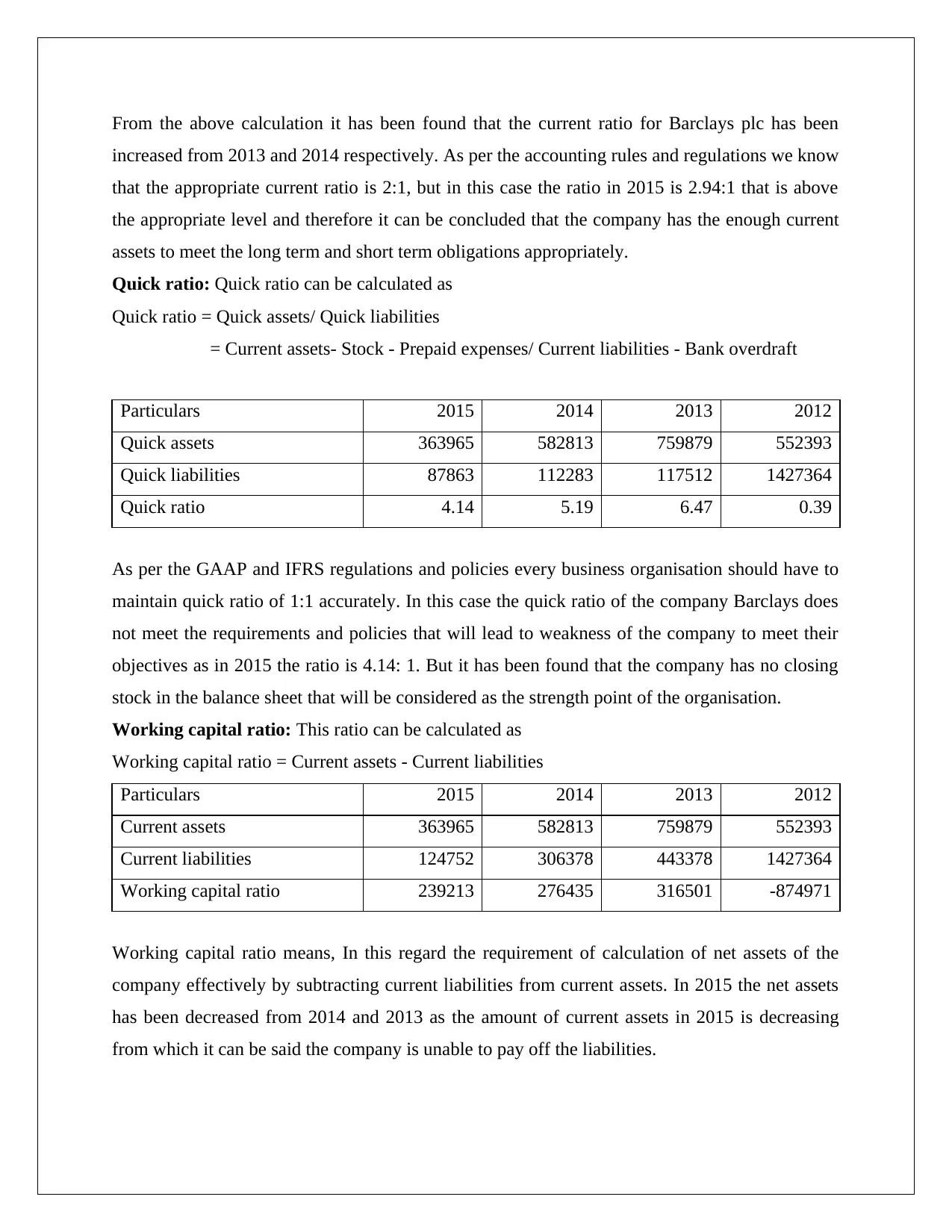

1) Evaluation of liquidity ratios

Evaluation of the liquidity ratios are the main important aspect of the financial statement in order

to find strengths and weakness for a financial year. These ratios include the current ratio, quick

ratio and working capital ratio that help to analyse the ability of the organisation to pay off the

long term and short term obligations and debt such as current liabilities (Goldmann, 2016,

p.110). Barclays plc’s liquidity ratios can be measured and interpreted through the financial

statement such as income and balance sheet as follows-(Refer to Appendix 1)

Current ratio: Current ratio can be calculated as

Current ratio= Current assets/ Current liabilities

Particulars 2015 2014 2013 2012

Current assets 363965 582813 759879 552393

Current liabilities 124752 306378 443378 1427364

Current ratio 2.92 1.9 1.71 0.39

Evaluation of the liquidity ratios are the main important aspect of the financial statement in order

to find strengths and weakness for a financial year. These ratios include the current ratio, quick

ratio and working capital ratio that help to analyse the ability of the organisation to pay off the

long term and short term obligations and debt such as current liabilities (Goldmann, 2016,

p.110). Barclays plc’s liquidity ratios can be measured and interpreted through the financial

statement such as income and balance sheet as follows-(Refer to Appendix 1)

Current ratio: Current ratio can be calculated as

Current ratio= Current assets/ Current liabilities

Particulars 2015 2014 2013 2012

Current assets 363965 582813 759879 552393

Current liabilities 124752 306378 443378 1427364

Current ratio 2.92 1.9 1.71 0.39

From the above calculation it has been found that the current ratio for Barclays plc has been

increased from 2013 and 2014 respectively. As per the accounting rules and regulations we know

that the appropriate current ratio is 2:1, but in this case the ratio in 2015 is 2.94:1 that is above

the appropriate level and therefore it can be concluded that the company has the enough current

assets to meet the long term and short term obligations appropriately.

Quick ratio: Quick ratio can be calculated as

Quick ratio = Quick assets/ Quick liabilities

= Current assets- Stock - Prepaid expenses/ Current liabilities - Bank overdraft

Particulars 2015 2014 2013 2012

Quick assets 363965 582813 759879 552393

Quick liabilities 87863 112283 117512 1427364

Quick ratio 4.14 5.19 6.47 0.39

As per the GAAP and IFRS regulations and policies every business organisation should have to

maintain quick ratio of 1:1 accurately. In this case the quick ratio of the company Barclays does

not meet the requirements and policies that will lead to weakness of the company to meet their

objectives as in 2015 the ratio is 4.14: 1. But it has been found that the company has no closing

stock in the balance sheet that will be considered as the strength point of the organisation.

Working capital ratio: This ratio can be calculated as

Working capital ratio = Current assets - Current liabilities

Particulars 2015 2014 2013 2012

Current assets 363965 582813 759879 552393

Current liabilities 124752 306378 443378 1427364

Working capital ratio 239213 276435 316501 -874971

Working capital ratio means, In this regard the requirement of calculation of net assets of the

company effectively by subtracting current liabilities from current assets. In 2015 the net assets

has been decreased from 2014 and 2013 as the amount of current assets in 2015 is decreasing

from which it can be said the company is unable to pay off the liabilities.

increased from 2013 and 2014 respectively. As per the accounting rules and regulations we know

that the appropriate current ratio is 2:1, but in this case the ratio in 2015 is 2.94:1 that is above

the appropriate level and therefore it can be concluded that the company has the enough current

assets to meet the long term and short term obligations appropriately.

Quick ratio: Quick ratio can be calculated as

Quick ratio = Quick assets/ Quick liabilities

= Current assets- Stock - Prepaid expenses/ Current liabilities - Bank overdraft

Particulars 2015 2014 2013 2012

Quick assets 363965 582813 759879 552393

Quick liabilities 87863 112283 117512 1427364

Quick ratio 4.14 5.19 6.47 0.39

As per the GAAP and IFRS regulations and policies every business organisation should have to

maintain quick ratio of 1:1 accurately. In this case the quick ratio of the company Barclays does

not meet the requirements and policies that will lead to weakness of the company to meet their

objectives as in 2015 the ratio is 4.14: 1. But it has been found that the company has no closing

stock in the balance sheet that will be considered as the strength point of the organisation.

Working capital ratio: This ratio can be calculated as

Working capital ratio = Current assets - Current liabilities

Particulars 2015 2014 2013 2012

Current assets 363965 582813 759879 552393

Current liabilities 124752 306378 443378 1427364

Working capital ratio 239213 276435 316501 -874971

Working capital ratio means, In this regard the requirement of calculation of net assets of the

company effectively by subtracting current liabilities from current assets. In 2015 the net assets

has been decreased from 2014 and 2013 as the amount of current assets in 2015 is decreasing

from which it can be said the company is unable to pay off the liabilities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.