Codan Ltd: An Analysis of Corporate Accounting and Financials

VerifiedAdded on 2021/05/31

|12

|3021

|256

Report

AI Summary

This report provides a detailed analysis of Codan Ltd's financial statements, focusing on corporate accounting principles. The analysis begins with an examination of the cash flow statement, highlighting trends in cash receipts, employee payments, interest paid, and investments in intangible assets. The report then delves into the financing activities, including share issuances and dividend payments. Part 2 breaks down the cash flow statement into operating, investing, and financing activities, and provides a graphical comparison over a three-year period, while Part 3 looks at the other comprehensive income statement. Part 4 discusses foreign currency translation reserves, cash flow hedge reserves, and retained earnings. Part 5 highlights the significance of the other comprehensive income statement. Parts 6 and 7 focus on the calculation and analysis of tax expenses, comparing current tax expenses with book tax and cash tax. Parts 8 and 9 examine deferred tax assets and liabilities, and the reasons behind the differences between income tax expense and income tax payable. Part 10 addresses the discrepancy between income tax expense in the income statement and the tax paid as per the cash flow statement. The report utilizes financial data from Codan Ltd's annual reports, offering valuable insights into the company's financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author note

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Cash flow Statement:

Part 1:

Codan Limited is a long time manufacturer as well as supplier of communications

equipment’s, mining equipment’s and metal detection accessories. It earns an annual revenue

of 132 million dollars. It is engaged in the business the supply of communications

equipment’s. The cash flow statement is one of the most important tools of analysing the

financial functioning of the company and all the stakeholders give their undue preference in

the cash flow statement for taking their investing decisions. On careful analysis of the cash

flow statements of the past three years from 2017 to 2015, some important aspects have been

revealed. The cash receipts are one of the most important aspects of any company’s cash

flow, it has increased from 175,300 to 230,959 million in 2017. The cash paid to the

employees have also increased, from 125,369 to 153,060, indicating the recruitment of new

employees. There has also been a decrease in the amount of interest paid by the Codan,

signifying a decrease of dependence on credit. The payments for intellectual property has also

increased from 1569 to 2905 million, signifying the company’s increased protection of its

patent and trademarks against competitors. The acquisition of various kinds of intangible

assets like computer software’s and various other licenses have also increased from 222

million to 277 million dollars. For a company, which is actively engaged in radio

communications and producing communications and metal detectors, usage of intangibles

like software’s are necessary.

The financing activity denotes the fiscal activities of the company. The fiscal activities of any

company form the most important activities of the company. Issuing of shares such as

preference shares and equity shares, payments of dividend form some of the most important

aspects of the financial activities of any company. It includes payment of dividends, issuing

Cash flow Statement:

Part 1:

Codan Limited is a long time manufacturer as well as supplier of communications

equipment’s, mining equipment’s and metal detection accessories. It earns an annual revenue

of 132 million dollars. It is engaged in the business the supply of communications

equipment’s. The cash flow statement is one of the most important tools of analysing the

financial functioning of the company and all the stakeholders give their undue preference in

the cash flow statement for taking their investing decisions. On careful analysis of the cash

flow statements of the past three years from 2017 to 2015, some important aspects have been

revealed. The cash receipts are one of the most important aspects of any company’s cash

flow, it has increased from 175,300 to 230,959 million in 2017. The cash paid to the

employees have also increased, from 125,369 to 153,060, indicating the recruitment of new

employees. There has also been a decrease in the amount of interest paid by the Codan,

signifying a decrease of dependence on credit. The payments for intellectual property has also

increased from 1569 to 2905 million, signifying the company’s increased protection of its

patent and trademarks against competitors. The acquisition of various kinds of intangible

assets like computer software’s and various other licenses have also increased from 222

million to 277 million dollars. For a company, which is actively engaged in radio

communications and producing communications and metal detectors, usage of intangibles

like software’s are necessary.

The financing activity denotes the fiscal activities of the company. The fiscal activities of any

company form the most important activities of the company. Issuing of shares such as

preference shares and equity shares, payments of dividend form some of the most important

aspects of the financial activities of any company. It includes payment of dividends, issuing

2CORPORATE ACCOUNTING

shares for raising capital for expansion purposes or addressing the expenses of the company.

A company cannot receive all the funds from its owners, as a result of which they issue

shares to the general public. In return, the company is required to pay adequate dividends,

which is actually the returns, provided by the company to the shareholders, who have

invested their money into the company. In the case of Codan, repayments of the various kinds

of borrowings have increased from 15,536 to 26,935 in 2017. This states that the company

had taken a lot of borrowings for conducting its operations. Dividends are also an important

aspect .of any company’s financial activities, as it signifies the amount of returns provided to

the shareholder of the company in lieu of investing their money in the company. In case of

Codan, the dividend payment has increased from 7082 in 2016 to 17,724 in the year 2017.

This proves the fact the company has increased the amount of dividend payments to its

existing shareholders.

Part 2:

The cash flow statements of any business entity is mainly categorised in three

different kinds of segments or activities. They are the operating, investing and the financial

activities. Each of these activities form the crux of the financial health of the company. For a

detailed analysis of each of these activities, a comprehensive graphical presentation of the

comparison has been provided below for the three year period from 2015 to 2017:

shares for raising capital for expansion purposes or addressing the expenses of the company.

A company cannot receive all the funds from its owners, as a result of which they issue

shares to the general public. In return, the company is required to pay adequate dividends,

which is actually the returns, provided by the company to the shareholders, who have

invested their money into the company. In the case of Codan, repayments of the various kinds

of borrowings have increased from 15,536 to 26,935 in 2017. This states that the company

had taken a lot of borrowings for conducting its operations. Dividends are also an important

aspect .of any company’s financial activities, as it signifies the amount of returns provided to

the shareholder of the company in lieu of investing their money in the company. In case of

Codan, the dividend payment has increased from 7082 in 2016 to 17,724 in the year 2017.

This proves the fact the company has increased the amount of dividend payments to its

existing shareholders.

Part 2:

The cash flow statements of any business entity is mainly categorised in three

different kinds of segments or activities. They are the operating, investing and the financial

activities. Each of these activities form the crux of the financial health of the company. For a

detailed analysis of each of these activities, a comprehensive graphical presentation of the

comparison has been provided below for the three year period from 2015 to 2017:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

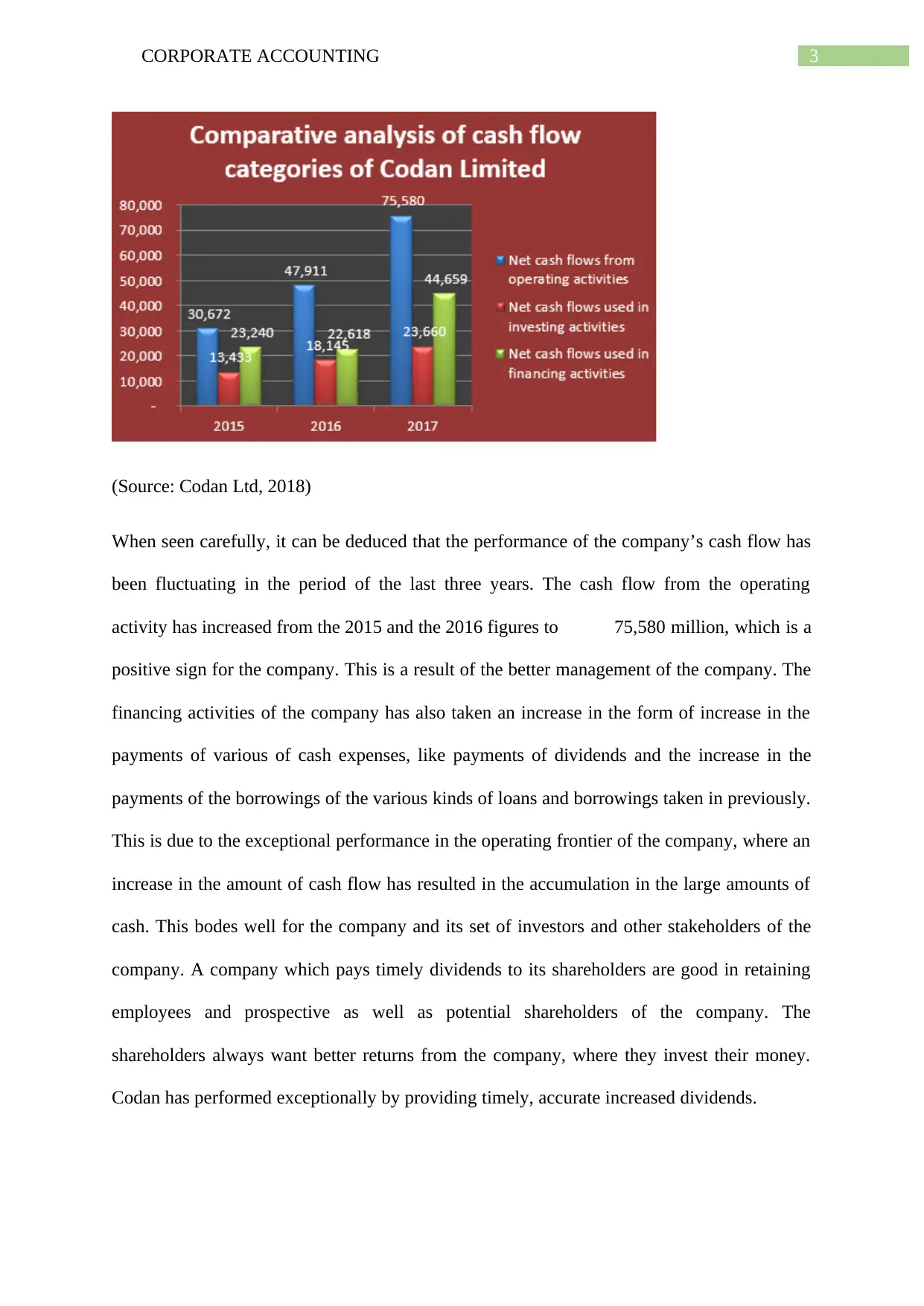

(Source: Codan Ltd, 2018)

When seen carefully, it can be deduced that the performance of the company’s cash flow has

been fluctuating in the period of the last three years. The cash flow from the operating

activity has increased from the 2015 and the 2016 figures to 75,580 million, which is a

positive sign for the company. This is a result of the better management of the company. The

financing activities of the company has also taken an increase in the form of increase in the

payments of various of cash expenses, like payments of dividends and the increase in the

payments of the borrowings of the various kinds of loans and borrowings taken in previously.

This is due to the exceptional performance in the operating frontier of the company, where an

increase in the amount of cash flow has resulted in the accumulation in the large amounts of

cash. This bodes well for the company and its set of investors and other stakeholders of the

company. A company which pays timely dividends to its shareholders are good in retaining

employees and prospective as well as potential shareholders of the company. The

shareholders always want better returns from the company, where they invest their money.

Codan has performed exceptionally by providing timely, accurate increased dividends.

(Source: Codan Ltd, 2018)

When seen carefully, it can be deduced that the performance of the company’s cash flow has

been fluctuating in the period of the last three years. The cash flow from the operating

activity has increased from the 2015 and the 2016 figures to 75,580 million, which is a

positive sign for the company. This is a result of the better management of the company. The

financing activities of the company has also taken an increase in the form of increase in the

payments of various of cash expenses, like payments of dividends and the increase in the

payments of the borrowings of the various kinds of loans and borrowings taken in previously.

This is due to the exceptional performance in the operating frontier of the company, where an

increase in the amount of cash flow has resulted in the accumulation in the large amounts of

cash. This bodes well for the company and its set of investors and other stakeholders of the

company. A company which pays timely dividends to its shareholders are good in retaining

employees and prospective as well as potential shareholders of the company. The

shareholders always want better returns from the company, where they invest their money.

Codan has performed exceptionally by providing timely, accurate increased dividends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

On analysing the investing activities of the company it can be seen that the expenses in the

investment activities of the company has increased significantly. The company has

significantly increased its expenses in the acquisition of plant and equipment, properties and

various kinds of intellectual properties in terms of patents and trademarks. In addition to this,

the company has also increased the acquisition and purchase of intangible goods. This

suggests that the company wants to increase its scale of operations in order to expand the

business in new areas. Codan wants to explore new areas of market for its communications

and radio communications services.

Other Comprehensive Income Statement:

Part 3:

Many important and vital aspects of the company have been mentioned in the other

comprehensive income of the company. The profit for the period has been provided in the

statement. The fair value of the cash flow hedges have been mentioned also, exchange

differences regarding the translation loss on the foreign operations involving foreign

currencies, have also been mentioned here. The total comprehensive income of the period of

the Codan has also been mentioned. The attribution of the income towards the equity

shareholders of the company as well as the non-controlling interests has also been provided.

Part 4:

According to Damodaran (2016), foreign currency translation reserve main purpose

remains the conversion of the financial results of the different subsidiary companies of any

parent business organisation into the reporting currency of the parent company. It is one of

the most significant aspect of the entire process of consolidation procedure of the financial

statements. The conversion into the currencies of the parent company’s country is imperative

in this regard. After the completion of this conversion procedure, the financial statements of

On analysing the investing activities of the company it can be seen that the expenses in the

investment activities of the company has increased significantly. The company has

significantly increased its expenses in the acquisition of plant and equipment, properties and

various kinds of intellectual properties in terms of patents and trademarks. In addition to this,

the company has also increased the acquisition and purchase of intangible goods. This

suggests that the company wants to increase its scale of operations in order to expand the

business in new areas. Codan wants to explore new areas of market for its communications

and radio communications services.

Other Comprehensive Income Statement:

Part 3:

Many important and vital aspects of the company have been mentioned in the other

comprehensive income of the company. The profit for the period has been provided in the

statement. The fair value of the cash flow hedges have been mentioned also, exchange

differences regarding the translation loss on the foreign operations involving foreign

currencies, have also been mentioned here. The total comprehensive income of the period of

the Codan has also been mentioned. The attribution of the income towards the equity

shareholders of the company as well as the non-controlling interests has also been provided.

Part 4:

According to Damodaran (2016), foreign currency translation reserve main purpose

remains the conversion of the financial results of the different subsidiary companies of any

parent business organisation into the reporting currency of the parent company. It is one of

the most significant aspect of the entire process of consolidation procedure of the financial

statements. The conversion into the currencies of the parent company’s country is imperative

in this regard. After the completion of this conversion procedure, the financial statements of

5CORPORATE ACCOUNTING

the subsidiary of the foreign country are again measured into the currency of the parent

company. After the termination of all these procedures, the profits and losses of the foreign

company are recorded in the currency translation.

Cash flow hedge reserve primary purpose is protection of the company’s financial

health, due to sudden changes in the cash flows of the company. It is mainly used at the time

when a business entity plans to reduce or diminish the various kinds of ill-effect, ascending

from changes in cash flows of any particular liability or asset because of the different kinds of

changes in a particular risk like rate of interest on various kinds of debt instruments of

floating rate (Gohet al. 2016). Whereas, when the focus shifts to the area of retained earnings,

it refers to that portion of the profits of the company, which is preserved, protected and kept

aside for expansion purposes of the business and for any other kinds of jobs which are of

contingency purposes. It is not distributed to the shareholders; it is on the other hand retained

for meeting any kind of emergency purposes or for paying debt.

Part 5:

In accordance with the research paper conducted and formulated by Graham et

al. (2017), other comprehensive income is very often viewed as an external part of the net

profit of any business organisation. During the early 90s, the differences in the profits of any

business entity were meant to be completely different of its central functions or even the

capricious items of the financial statements were transferred to the portion of the

shareholders’ equity. Nevertheless, Codan utilizes the other comprehensive income statement

in order to provide imperative details about the above mentioned figures and items. Thus it

can be said that comprehensive income is a combination of other comprehensive income and

net standard income. All these fiscal items are presented in the other comprehensive income

statement of the company, as it helps in providing an inclusive view of the various important

the subsidiary of the foreign country are again measured into the currency of the parent

company. After the termination of all these procedures, the profits and losses of the foreign

company are recorded in the currency translation.

Cash flow hedge reserve primary purpose is protection of the company’s financial

health, due to sudden changes in the cash flows of the company. It is mainly used at the time

when a business entity plans to reduce or diminish the various kinds of ill-effect, ascending

from changes in cash flows of any particular liability or asset because of the different kinds of

changes in a particular risk like rate of interest on various kinds of debt instruments of

floating rate (Gohet al. 2016). Whereas, when the focus shifts to the area of retained earnings,

it refers to that portion of the profits of the company, which is preserved, protected and kept

aside for expansion purposes of the business and for any other kinds of jobs which are of

contingency purposes. It is not distributed to the shareholders; it is on the other hand retained

for meeting any kind of emergency purposes or for paying debt.

Part 5:

In accordance with the research paper conducted and formulated by Graham et

al. (2017), other comprehensive income is very often viewed as an external part of the net

profit of any business organisation. During the early 90s, the differences in the profits of any

business entity were meant to be completely different of its central functions or even the

capricious items of the financial statements were transferred to the portion of the

shareholders’ equity. Nevertheless, Codan utilizes the other comprehensive income statement

in order to provide imperative details about the above mentioned figures and items. Thus it

can be said that comprehensive income is a combination of other comprehensive income and

net standard income. All these fiscal items are presented in the other comprehensive income

statement of the company, as it helps in providing an inclusive view of the various important

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

items of the business firms and entities, which otherwise could not be provided in the income

statement of the company.

Accounting for Corporate Income:

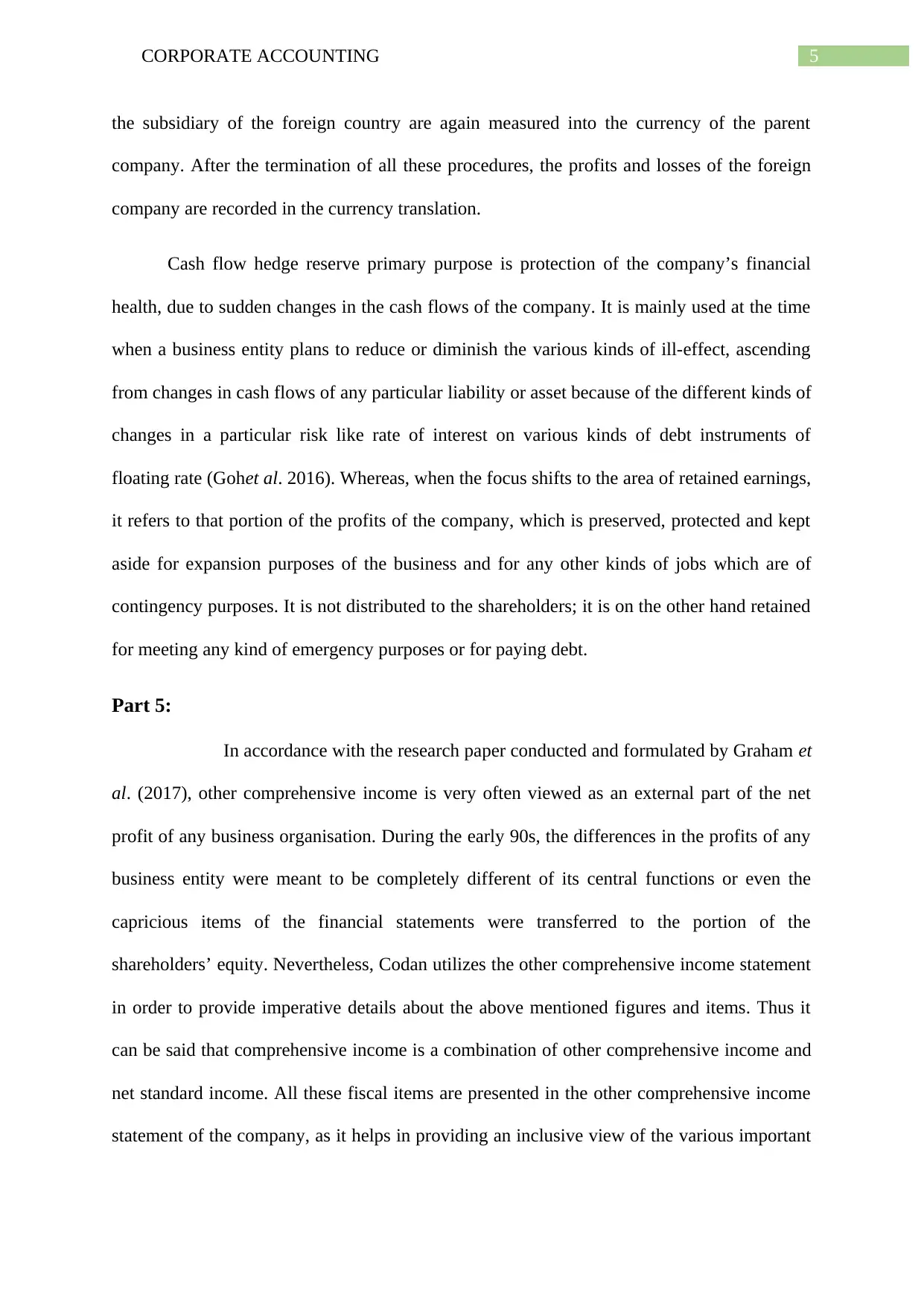

Part 6:

Any business entity incurs different kinds of expenditures. Some of the prominent

ones are, R&D expenses, marketing expenses, operating expenses, selling expenses etc. Tax

expense is a prominent one out of all those expenses (Khan, Srinivasan and Tan 2016). It is

calculated by multiplying the profit before tax which is also known as PAT with the current

tax rate. The current tax expenses of the company are 18970 million for the year 2017. An

excerpt has been attached below:

(Source: Codan annual report, 2017)

Part 7:

On analysis of the financial statements of Codan for the year 2017, it could be seen

that, the profit before tax of the company has been $15,970 million, which was $1219 million

in 2016. The tax rate used by Codan, as analysed from its financial statements is 30%.

While using this rate, it is seen that the tax expense of Codan for the year 2017 should have

been $17,952 million ($59,843 x 30%) and $582.7 million ($19,426 million x 30%) in 2016.

Thus it could be seen that there indeed was a difference in the taxes paid. There could be a

items of the business firms and entities, which otherwise could not be provided in the income

statement of the company.

Accounting for Corporate Income:

Part 6:

Any business entity incurs different kinds of expenditures. Some of the prominent

ones are, R&D expenses, marketing expenses, operating expenses, selling expenses etc. Tax

expense is a prominent one out of all those expenses (Khan, Srinivasan and Tan 2016). It is

calculated by multiplying the profit before tax which is also known as PAT with the current

tax rate. The current tax expenses of the company are 18970 million for the year 2017. An

excerpt has been attached below:

(Source: Codan annual report, 2017)

Part 7:

On analysis of the financial statements of Codan for the year 2017, it could be seen

that, the profit before tax of the company has been $15,970 million, which was $1219 million

in 2016. The tax rate used by Codan, as analysed from its financial statements is 30%.

While using this rate, it is seen that the tax expense of Codan for the year 2017 should have

been $17,952 million ($59,843 x 30%) and $582.7 million ($19,426 million x 30%) in 2016.

Thus it could be seen that there indeed was a difference in the taxes paid. There could be a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

variety of reasons for this but the most prominent one is the presence of book tax and cash

tax. Cash tax refers to the amount of tax which is payable to the government departments,

which is the legal norm of the country, where the business entity operates. On the other hand,

book tax refers to the amount of tax which is recorded on the financial statements in the

annual reports of the company. Moreover, Codan has made some exclusion in the items while

calculating the overall taxable expense, which have added to the difference. Different tax

rates across various countries, deferred tax assets and the case of non assessable income has

also contributed in the differences.

Part 8:

Deferred tax assets refer to those assets where the entities have either paid higher

taxes or have paid the taxes in advance (Klassen, Lisowsky and Mescall, 2015). For Codan,

deferred tax liabilities have been $7237 million in 2017, which was $6808 million in 2016.

Deferred tax liabilities are documented and recorded because of the presence of some sought

of temporary variations differences in business profits, on which lower taxes have been paid

in the previous year, which is 2017 in the present case.

Part 9:

There is a presence of current income tax payable in the section of current of tax

liabilities, which is $16,089 for the year 2017. The possible reason of difference between the

income tax payable and the income tax expense is deferred tax assets (Qamar et al., 2016).

The payment of this additional tax causes the difference. Moreover, the treatment of

depreciation is another reason which can cause a possible difference between the two.

variety of reasons for this but the most prominent one is the presence of book tax and cash

tax. Cash tax refers to the amount of tax which is payable to the government departments,

which is the legal norm of the country, where the business entity operates. On the other hand,

book tax refers to the amount of tax which is recorded on the financial statements in the

annual reports of the company. Moreover, Codan has made some exclusion in the items while

calculating the overall taxable expense, which have added to the difference. Different tax

rates across various countries, deferred tax assets and the case of non assessable income has

also contributed in the differences.

Part 8:

Deferred tax assets refer to those assets where the entities have either paid higher

taxes or have paid the taxes in advance (Klassen, Lisowsky and Mescall, 2015). For Codan,

deferred tax liabilities have been $7237 million in 2017, which was $6808 million in 2016.

Deferred tax liabilities are documented and recorded because of the presence of some sought

of temporary variations differences in business profits, on which lower taxes have been paid

in the previous year, which is 2017 in the present case.

Part 9:

There is a presence of current income tax payable in the section of current of tax

liabilities, which is $16,089 for the year 2017. The possible reason of difference between the

income tax payable and the income tax expense is deferred tax assets (Qamar et al., 2016).

The payment of this additional tax causes the difference. Moreover, the treatment of

depreciation is another reason which can cause a possible difference between the two.

8CORPORATE ACCOUNTING

Part 10:

There exists a difference between the income tax expense in the income statement of

Codan and its balance sheet. In the income tax statement of the company, the tax expense

comes to $15,970million in the year 2017, whereas, the income tax paid as per the cash flow

statement of the company stood at $874 million. There exists a stark difference between the

two figures. One of the most prominent reasons for this mis-match is the treatment of tax in

the income statement and the cash flow statement is the presence of many sundry items,

while calculating income tax expense in the income statement such as depreciation,

amortisation, interest, asset revaluation, asset disposal and dividend payment.

Part 11:

On the assessment of the tax treatment at Codan Ltd, no surprising or confusing

elements were found. All the set of laws of the Australian Tax Office or ATO are strictly

followed. Additionally it was found, that Codan has provided necessary reasons for

supporting the different aspects of taxation like tax rate, income tax payable, tax liabilities

and deferred assets and liabilities.

Along with this, the essential working notes to the financial statements have been

provided for backing the treatment of various items. All these aspects of tax treatment,

dealing with items like deferred liabilities and assets have been intriguing and a novel one.

This has helped in recuperating the appreciative knowledge of business taxation. Thus it can

be said that this assessment would go a long way in teaching the intricacies of business

taxation to any individual.

Part 10:

There exists a difference between the income tax expense in the income statement of

Codan and its balance sheet. In the income tax statement of the company, the tax expense

comes to $15,970million in the year 2017, whereas, the income tax paid as per the cash flow

statement of the company stood at $874 million. There exists a stark difference between the

two figures. One of the most prominent reasons for this mis-match is the treatment of tax in

the income statement and the cash flow statement is the presence of many sundry items,

while calculating income tax expense in the income statement such as depreciation,

amortisation, interest, asset revaluation, asset disposal and dividend payment.

Part 11:

On the assessment of the tax treatment at Codan Ltd, no surprising or confusing

elements were found. All the set of laws of the Australian Tax Office or ATO are strictly

followed. Additionally it was found, that Codan has provided necessary reasons for

supporting the different aspects of taxation like tax rate, income tax payable, tax liabilities

and deferred assets and liabilities.

Along with this, the essential working notes to the financial statements have been

provided for backing the treatment of various items. All these aspects of tax treatment,

dealing with items like deferred liabilities and assets have been intriguing and a novel one.

This has helped in recuperating the appreciative knowledge of business taxation. Thus it can

be said that this assessment would go a long way in teaching the intricacies of business

taxation to any individual.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

References:

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Doran, C.M., Byrnes, J.M., Cobiac, L.J., Vandenberg, B. and Vos, T., 2013. Estimated

impacts of alternative Australian alcohol taxation structures on consumption, public health

and government revenues. Med J Aust, 199(9), pp.619-622.

Goh, B.W., Lee, J., Lim, C.Y. and Shevlin, T., 2016. The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), pp.1647-1670.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate

Decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Khan, M., Srinivasan, S. and Tan, L., 2016. Institutional ownership and corporate tax

avoidance: New evidence. The Accounting Review, 92(2), pp.101-122.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2015. The role of auditors, non-auditors, and

internal tax departments in corporate tax aggressiveness. The Accounting Review, 91(1),

pp.179-205.

Liu, Y., Li, X., Zeng, H. and An, Y., 2016. Political connections, auditor choice and

corporate accounting transparency: evidence from private sector firms in China. Accounting

& Finance.

References:

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Doran, C.M., Byrnes, J.M., Cobiac, L.J., Vandenberg, B. and Vos, T., 2013. Estimated

impacts of alternative Australian alcohol taxation structures on consumption, public health

and government revenues. Med J Aust, 199(9), pp.619-622.

Goh, B.W., Lee, J., Lim, C.Y. and Shevlin, T., 2016. The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), pp.1647-1670.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate

Decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Khan, M., Srinivasan, S. and Tan, L., 2016. Institutional ownership and corporate tax

avoidance: New evidence. The Accounting Review, 92(2), pp.101-122.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2015. The role of auditors, non-auditors, and

internal tax departments in corporate tax aggressiveness. The Accounting Review, 91(1),

pp.179-205.

Liu, Y., Li, X., Zeng, H. and An, Y., 2016. Political connections, auditor choice and

corporate accounting transparency: evidence from private sector firms in China. Accounting

& Finance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Qamar, M.A.J., Khalil, F. and Akhtar, W., 2016. Corporate Governance Culture

Transmission in Mutual Funds: Directors as Vector of Transmission. International Journal of

Academic Research in Accounting, Finance and Management Sciences, 6(2), pp.175-183.

Ramanna, K., 2014. Political standards: Accounting for legitimacy.

Richardson, G., Taylor, G. and Lanis, R., 2013. Determinants of transfer pricing

aggressiveness: Empirical evidence from Australian firms. Journal of Contemporary

Accounting & Economics, 9(2), pp.136-150.

Christensen, D.M., Dhaliwal, D.S., Boivie, S. and Graffin, S.D., 2015. Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), pp.1918-

1938.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2),

pp.113-122.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Elsevier.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), pp.12-25.

Wesfarmers.com.au., 2018., [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed 6 May 2018].

Qamar, M.A.J., Khalil, F. and Akhtar, W., 2016. Corporate Governance Culture

Transmission in Mutual Funds: Directors as Vector of Transmission. International Journal of

Academic Research in Accounting, Finance and Management Sciences, 6(2), pp.175-183.

Ramanna, K., 2014. Political standards: Accounting for legitimacy.

Richardson, G., Taylor, G. and Lanis, R., 2013. Determinants of transfer pricing

aggressiveness: Empirical evidence from Australian firms. Journal of Contemporary

Accounting & Economics, 9(2), pp.136-150.

Christensen, D.M., Dhaliwal, D.S., Boivie, S. and Graffin, S.D., 2015. Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), pp.1918-

1938.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating Corporate Accounting and

Reporting for Sustainability–Attributes and Challenges. Sustainable Development, 25(2),

pp.113-122.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Elsevier.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), pp.12-25.

Wesfarmers.com.au., 2018., [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed 6 May 2018].

11CORPORATE ACCOUNTING

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.