University Company Accounting: Consolidation and Financial Statements

VerifiedAdded on 2022/09/14

|9

|758

|16

Practical Assignment

AI Summary

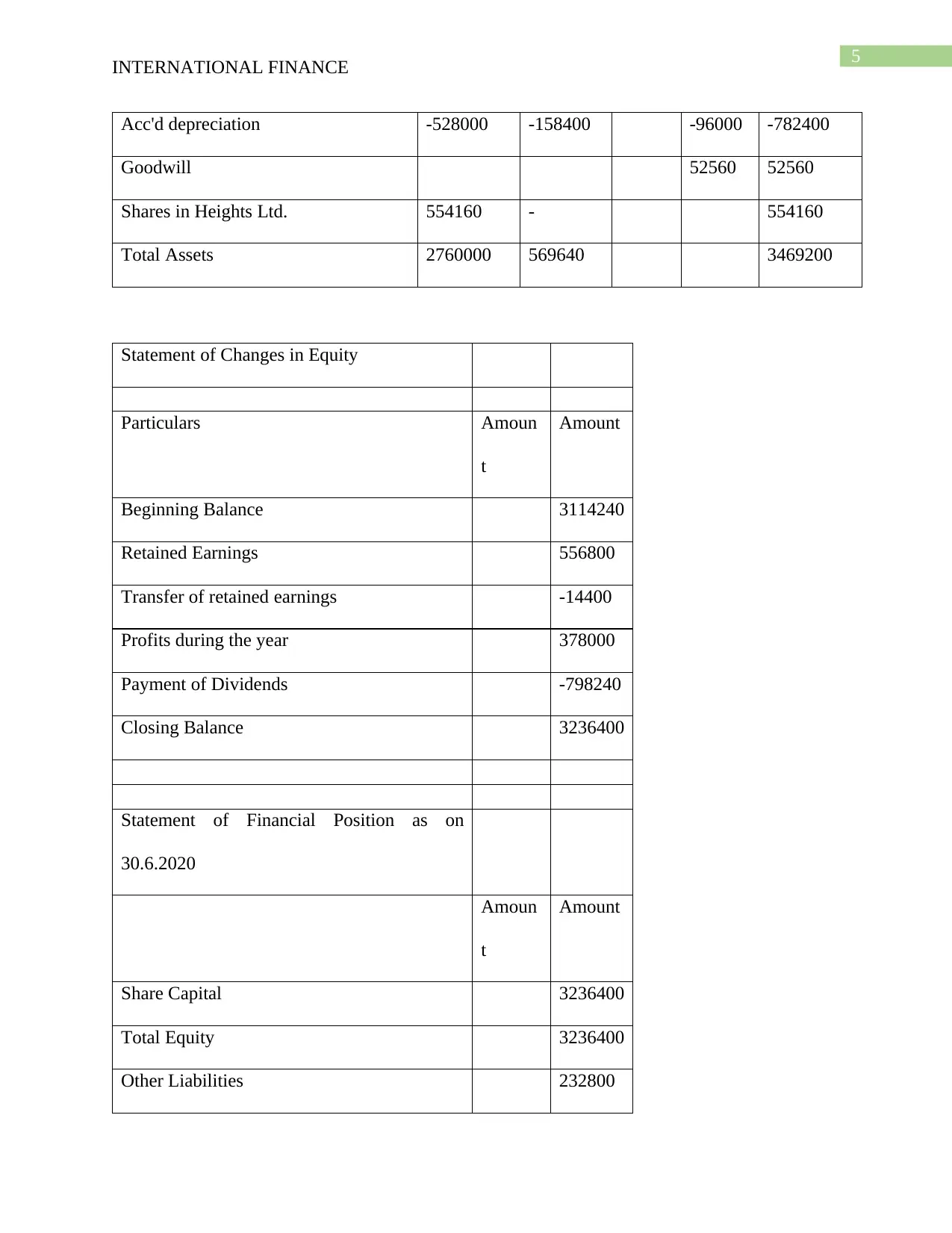

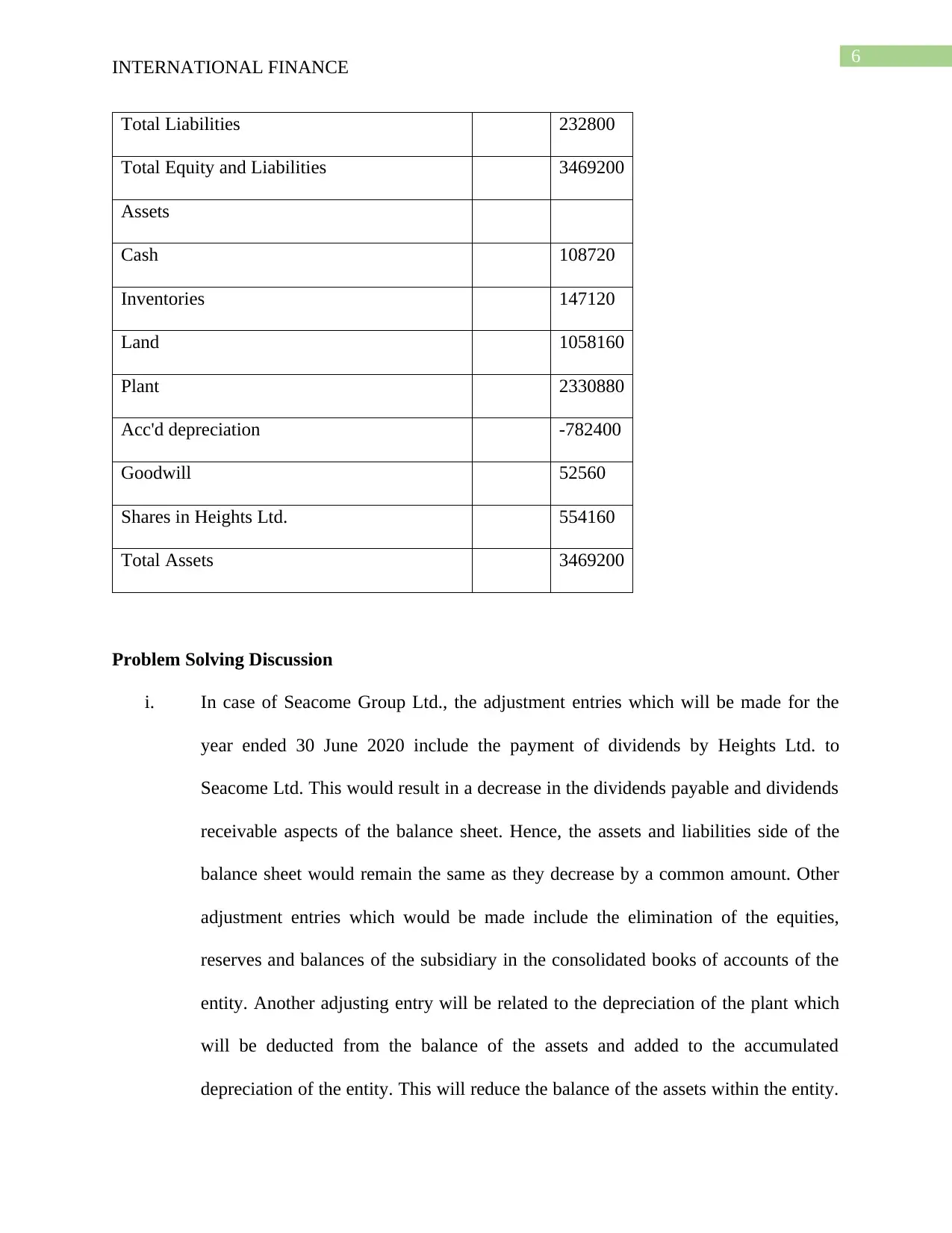

This assignment provides a detailed solution to a Company Accounting case study focusing on the consolidation of financial statements. It includes a practical application of accounting principles, specifically addressing the preparation of consolidated financial statements, acquisition analysis, and consolidation journal entries. The solution demonstrates the creation of a consolidation worksheet, incorporating adjustments for fair value differences, goodwill calculation, and the elimination of intercompany transactions. Furthermore, the assignment covers the treatment of deferred tax liabilities, business combination valuation reserves, and the impact of dividends on the consolidated financial position. The document also features a discussion section explaining the rationale behind the accounting entries and adjustments made in the consolidation process, providing a comprehensive understanding of the topic.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.