Financial Statement Analysis for Business FIN 924 Assignment

VerifiedAdded on 2023/06/18

|11

|2229

|141

Homework Assignment

AI Summary

This document presents a solved assignment for the course FIN 924, Financial Statement Analysis for Business. It covers various aspects of financial analysis including the calculation of abnormal earnings growth, long-term growth rate, intrinsic value, effective tax rate, and free cash flow using different methods. The assignment also delves into the interpretation of financial ratios like P/E, P/B, and ROE, and their implications for a company's financial health. Furthermore, it analyzes the return on capital employed and return on net assets for Everest Ltd, evaluating the company's financial performance and competitive advantage based on provided data. The solution includes detailed calculations, explanations, and references to support the analysis.

Financial Statement Analysis

For Business FIN 924

For Business FIN 924

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................3

C..................................................................................................................................................3

D..................................................................................................................................................3

QUESTION 2...................................................................................................................................4

a...................................................................................................................................................4

b...................................................................................................................................................4

c...................................................................................................................................................5

QUESTION 3...................................................................................................................................6

Calculation of free cash flow......................................................................................................6

QUESTION 4...................................................................................................................................7

a...................................................................................................................................................7

b...................................................................................................................................................7

c...................................................................................................................................................7

d...................................................................................................................................................8

e...................................................................................................................................................8

QUESTION 5...................................................................................................................................8

A..................................................................................................................................................8

B..................................................................................................................................................9

C..................................................................................................................................................9

D................................................................................................................................................10

E................................................................................................................................................10

REFERENCES..............................................................................................................................11

QUESTION 1...................................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................3

C..................................................................................................................................................3

D..................................................................................................................................................3

QUESTION 2...................................................................................................................................4

a...................................................................................................................................................4

b...................................................................................................................................................4

c...................................................................................................................................................5

QUESTION 3...................................................................................................................................6

Calculation of free cash flow......................................................................................................6

QUESTION 4...................................................................................................................................7

a...................................................................................................................................................7

b...................................................................................................................................................7

c...................................................................................................................................................7

d...................................................................................................................................................8

e...................................................................................................................................................8

QUESTION 5...................................................................................................................................8

A..................................................................................................................................................8

B..................................................................................................................................................9

C..................................................................................................................................................9

D................................................................................................................................................10

E................................................................................................................................................10

REFERENCES..............................................................................................................................11

QUESTION 1

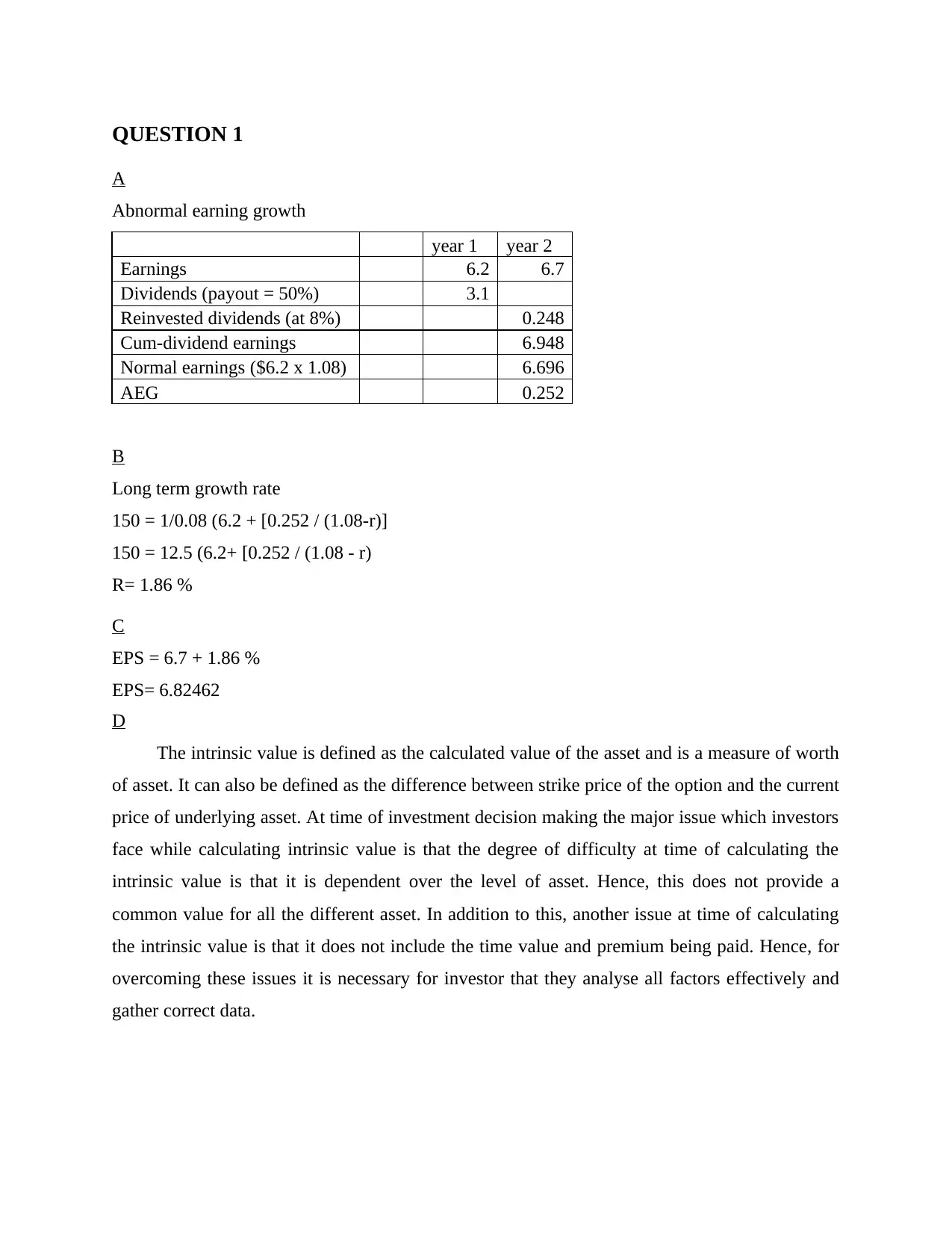

A

Abnormal earning growth

year 1 year 2

Earnings 6.2 6.7

Dividends (payout = 50%) 3.1

Reinvested dividends (at 8%) 0.248

Cum-dividend earnings 6.948

Normal earnings ($6.2 x 1.08) 6.696

AEG 0.252

B

Long term growth rate

150 = 1/0.08 (6.2 + [0.252 / (1.08-r)]

150 = 12.5 (6.2+ [0.252 / (1.08 - r)

R= 1.86 %

C

EPS = 6.7 + 1.86 %

EPS= 6.82462

D

The intrinsic value is defined as the calculated value of the asset and is a measure of worth

of asset. It can also be defined as the difference between strike price of the option and the current

price of underlying asset. At time of investment decision making the major issue which investors

face while calculating intrinsic value is that the degree of difficulty at time of calculating the

intrinsic value is that it is dependent over the level of asset. Hence, this does not provide a

common value for all the different asset. In addition to this, another issue at time of calculating

the intrinsic value is that it does not include the time value and premium being paid. Hence, for

overcoming these issues it is necessary for investor that they analyse all factors effectively and

gather correct data.

A

Abnormal earning growth

year 1 year 2

Earnings 6.2 6.7

Dividends (payout = 50%) 3.1

Reinvested dividends (at 8%) 0.248

Cum-dividend earnings 6.948

Normal earnings ($6.2 x 1.08) 6.696

AEG 0.252

B

Long term growth rate

150 = 1/0.08 (6.2 + [0.252 / (1.08-r)]

150 = 12.5 (6.2+ [0.252 / (1.08 - r)

R= 1.86 %

C

EPS = 6.7 + 1.86 %

EPS= 6.82462

D

The intrinsic value is defined as the calculated value of the asset and is a measure of worth

of asset. It can also be defined as the difference between strike price of the option and the current

price of underlying asset. At time of investment decision making the major issue which investors

face while calculating intrinsic value is that the degree of difficulty at time of calculating the

intrinsic value is that it is dependent over the level of asset. Hence, this does not provide a

common value for all the different asset. In addition to this, another issue at time of calculating

the intrinsic value is that it does not include the time value and premium being paid. Hence, for

overcoming these issues it is necessary for investor that they analyse all factors effectively and

gather correct data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

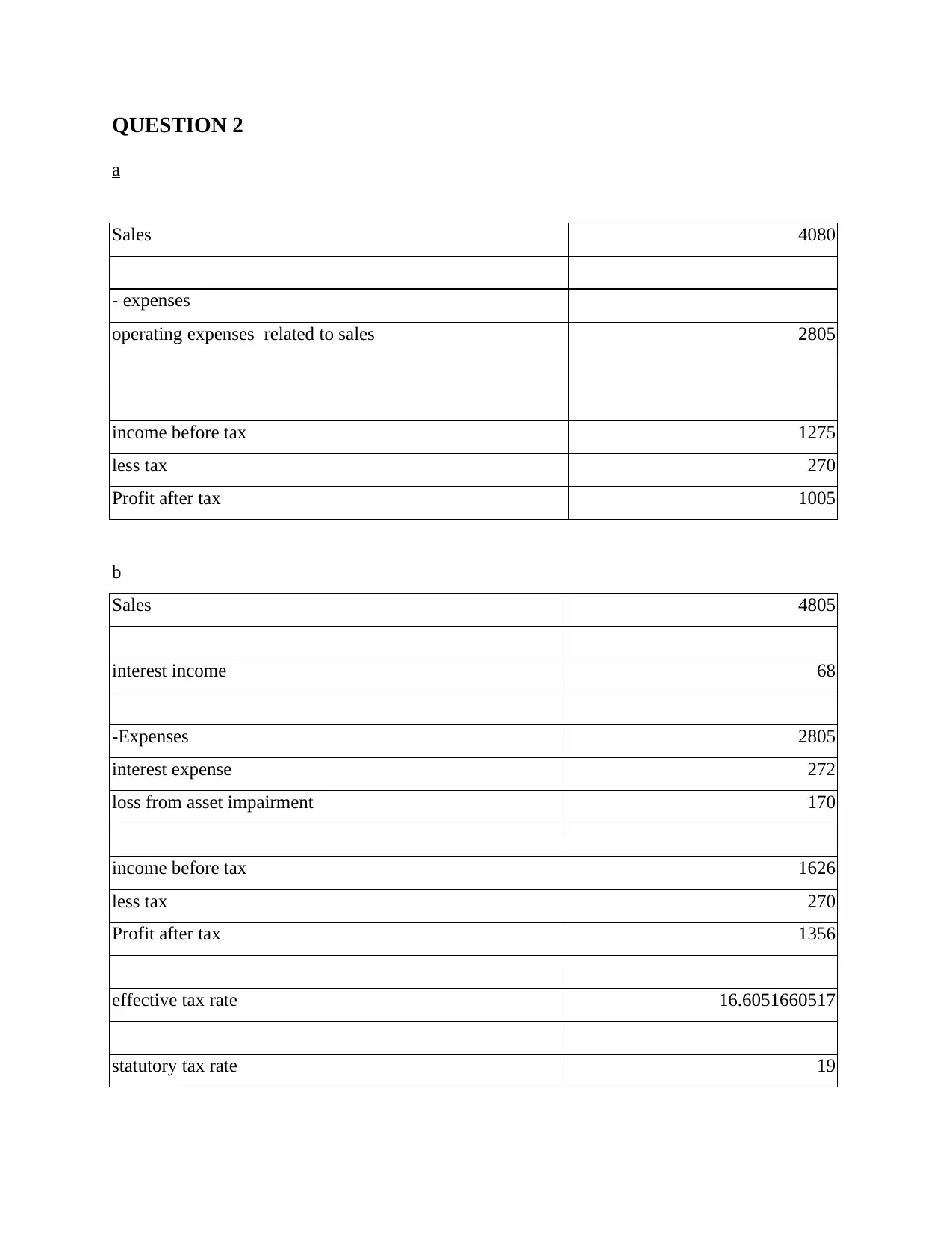

a

Sales 4080

- expenses

operating expenses related to sales 2805

income before tax 1275

less tax 270

Profit after tax 1005

b

Sales 4805

interest income 68

-Expenses 2805

interest expense 272

loss from asset impairment 170

income before tax 1626

less tax 270

Profit after tax 1356

effective tax rate 16.6051660517

statutory tax rate 19

a

Sales 4080

- expenses

operating expenses related to sales 2805

income before tax 1275

less tax 270

Profit after tax 1005

b

Sales 4805

interest income 68

-Expenses 2805

interest expense 272

loss from asset impairment 170

income before tax 1626

less tax 270

Profit after tax 1356

effective tax rate 16.6051660517

statutory tax rate 19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

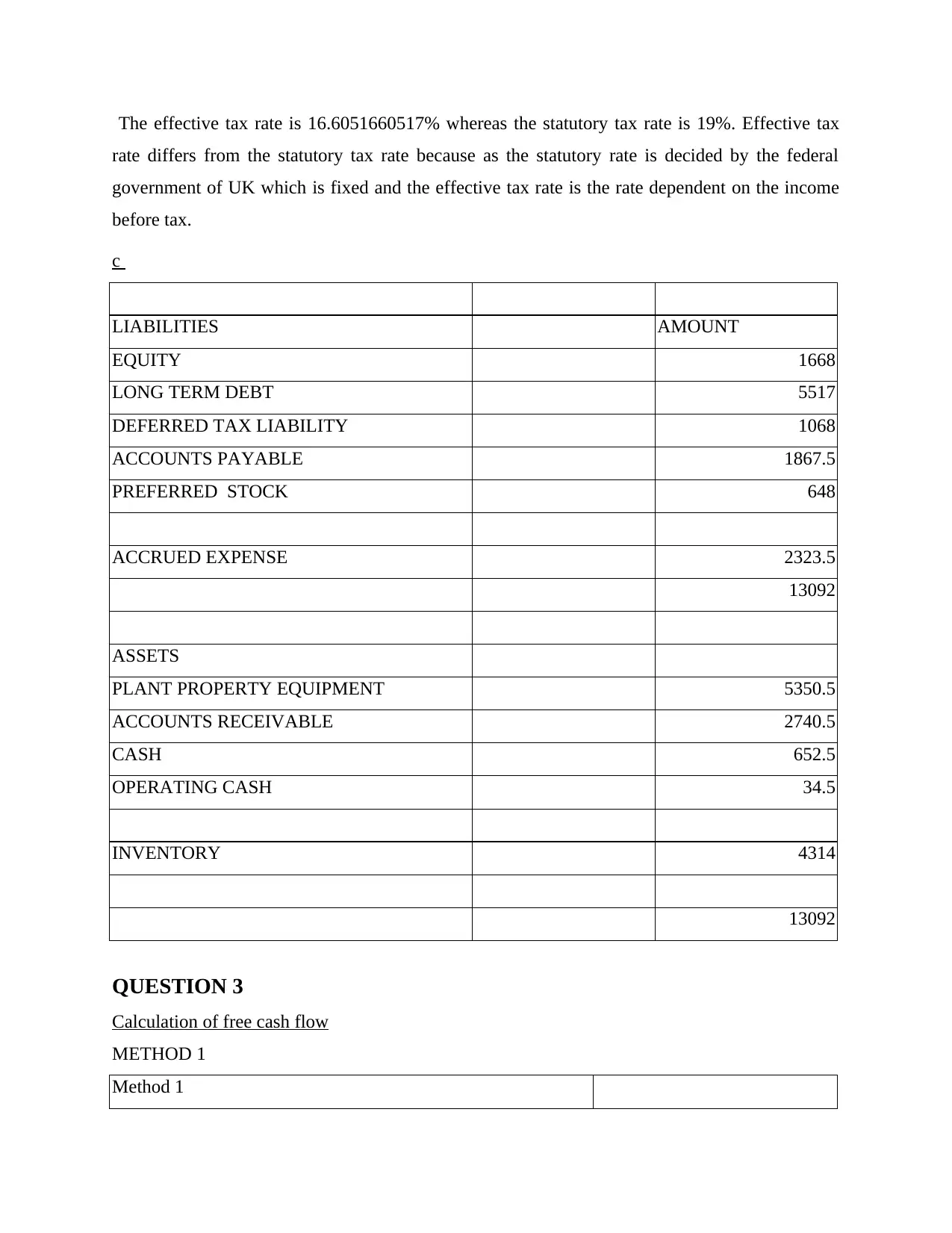

The effective tax rate is 16.6051660517% whereas the statutory tax rate is 19%. Effective tax

rate differs from the statutory tax rate because as the statutory rate is decided by the federal

government of UK which is fixed and the effective tax rate is the rate dependent on the income

before tax.

c

LIABILITIES AMOUNT

EQUITY 1668

LONG TERM DEBT 5517

DEFERRED TAX LIABILITY 1068

ACCOUNTS PAYABLE 1867.5

PREFERRED STOCK 648

ACCRUED EXPENSE 2323.5

13092

ASSETS

PLANT PROPERTY EQUIPMENT 5350.5

ACCOUNTS RECEIVABLE 2740.5

CASH 652.5

OPERATING CASH 34.5

INVENTORY 4314

13092

QUESTION 3

Calculation of free cash flow

METHOD 1

Method 1

rate differs from the statutory tax rate because as the statutory rate is decided by the federal

government of UK which is fixed and the effective tax rate is the rate dependent on the income

before tax.

c

LIABILITIES AMOUNT

EQUITY 1668

LONG TERM DEBT 5517

DEFERRED TAX LIABILITY 1068

ACCOUNTS PAYABLE 1867.5

PREFERRED STOCK 648

ACCRUED EXPENSE 2323.5

13092

ASSETS

PLANT PROPERTY EQUIPMENT 5350.5

ACCOUNTS RECEIVABLE 2740.5

CASH 652.5

OPERATING CASH 34.5

INVENTORY 4314

13092

QUESTION 3

Calculation of free cash flow

METHOD 1

Method 1

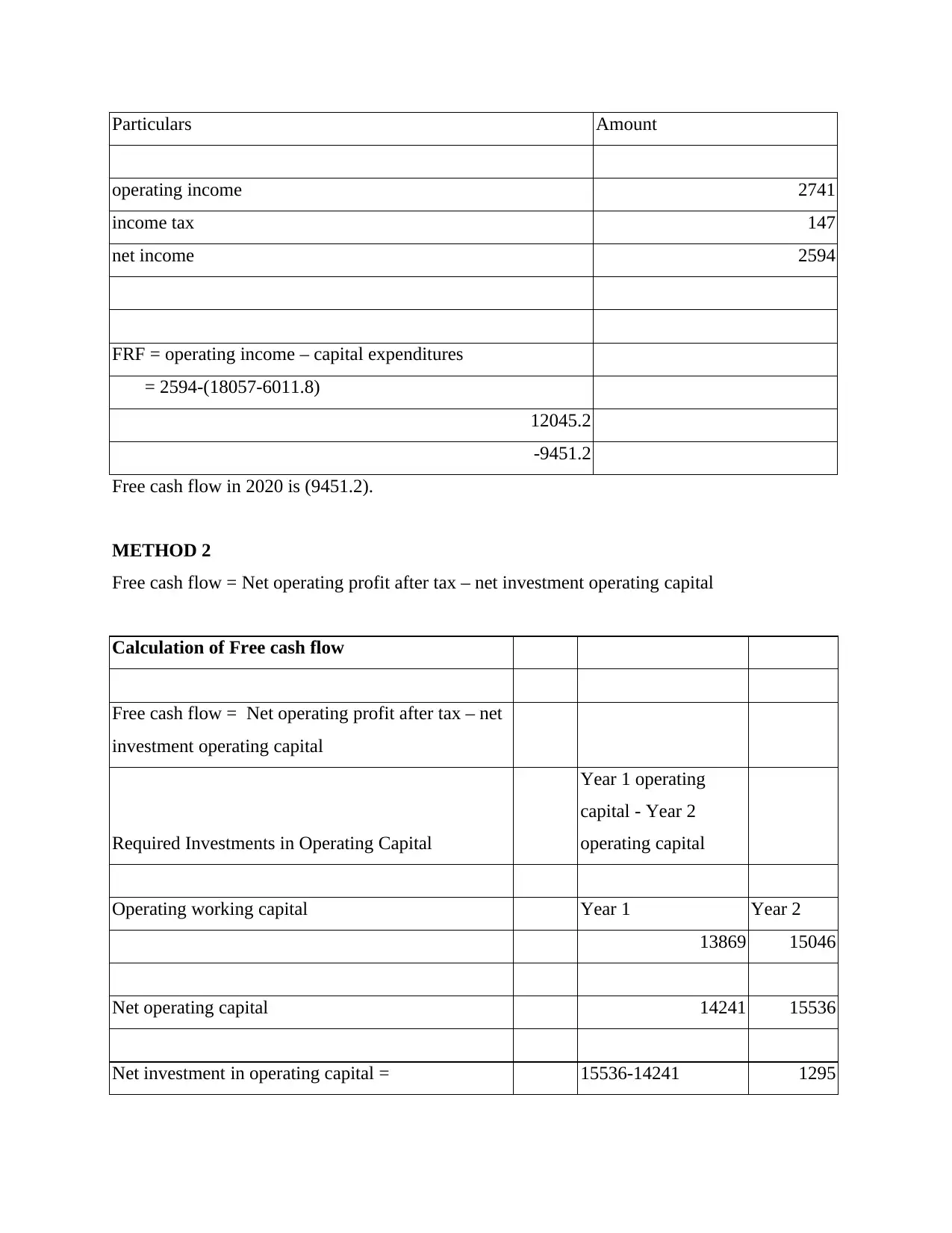

Particulars Amount

operating income 2741

income tax 147

net income 2594

FRF = operating income – capital expenditures

= 2594-(18057-6011.8)

12045.2

-9451.2

Free cash flow in 2020 is (9451.2).

METHOD 2

Free cash flow = Net operating profit after tax – net investment operating capital

Calculation of Free cash flow

Free cash flow = Net operating profit after tax – net

investment operating capital

Required Investments in Operating Capital

Year 1 operating

capital - Year 2

operating capital

Operating working capital Year 1 Year 2

13869 15046

Net operating capital 14241 15536

Net investment in operating capital = 15536-14241 1295

operating income 2741

income tax 147

net income 2594

FRF = operating income – capital expenditures

= 2594-(18057-6011.8)

12045.2

-9451.2

Free cash flow in 2020 is (9451.2).

METHOD 2

Free cash flow = Net operating profit after tax – net investment operating capital

Calculation of Free cash flow

Free cash flow = Net operating profit after tax – net

investment operating capital

Required Investments in Operating Capital

Year 1 operating

capital - Year 2

operating capital

Operating working capital Year 1 Year 2

13869 15046

Net operating capital 14241 15536

Net investment in operating capital = 15536-14241 1295

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

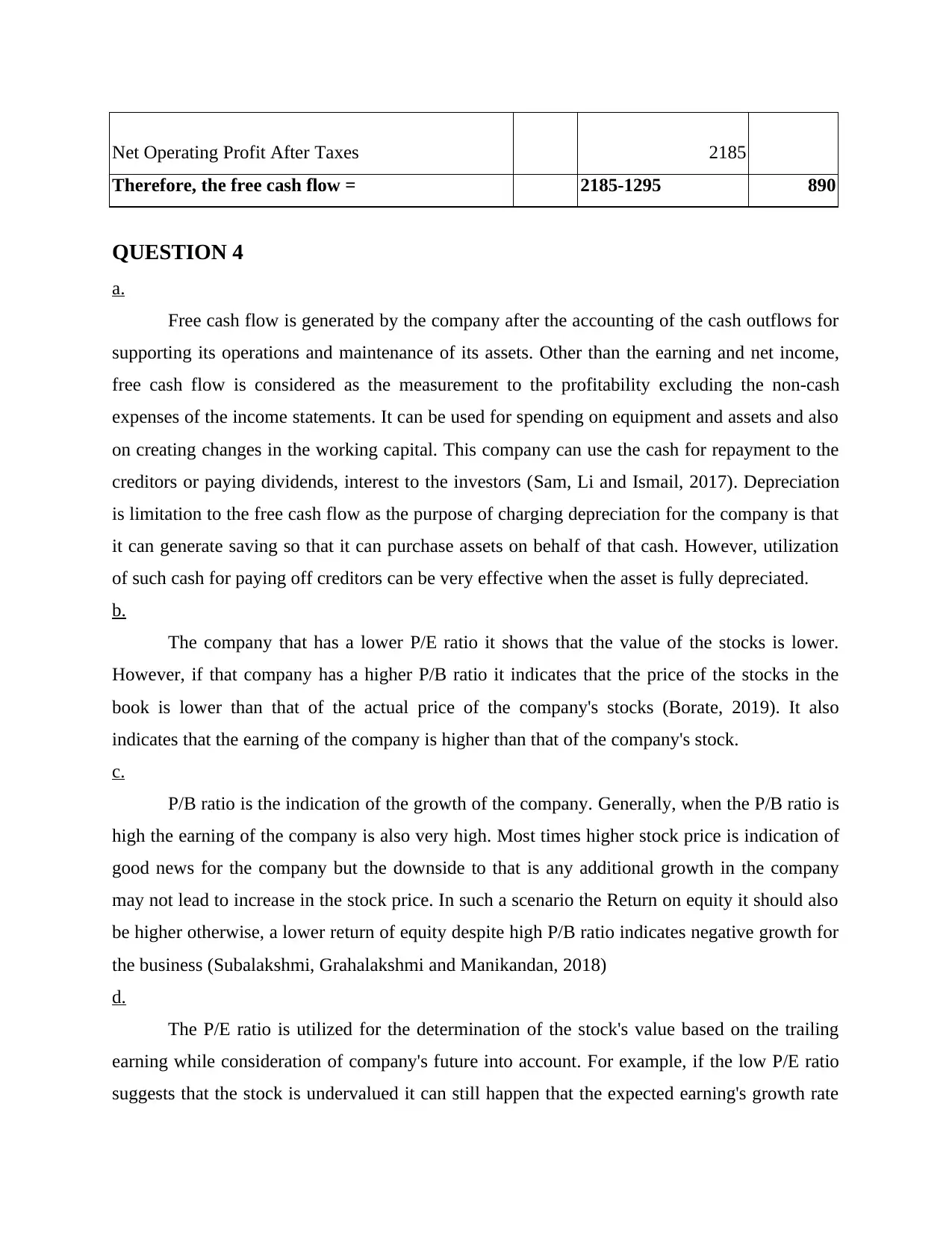

Net Operating Profit After Taxes 2185

Therefore, the free cash flow = 2185-1295 890

QUESTION 4

a.

Free cash flow is generated by the company after the accounting of the cash outflows for

supporting its operations and maintenance of its assets. Other than the earning and net income,

free cash flow is considered as the measurement to the profitability excluding the non-cash

expenses of the income statements. It can be used for spending on equipment and assets and also

on creating changes in the working capital. This company can use the cash for repayment to the

creditors or paying dividends, interest to the investors (Sam, Li and Ismail, 2017). Depreciation

is limitation to the free cash flow as the purpose of charging depreciation for the company is that

it can generate saving so that it can purchase assets on behalf of that cash. However, utilization

of such cash for paying off creditors can be very effective when the asset is fully depreciated.

b.

The company that has a lower P/E ratio it shows that the value of the stocks is lower.

However, if that company has a higher P/B ratio it indicates that the price of the stocks in the

book is lower than that of the actual price of the company's stocks (Borate, 2019). It also

indicates that the earning of the company is higher than that of the company's stock.

c.

P/B ratio is the indication of the growth of the company. Generally, when the P/B ratio is

high the earning of the company is also very high. Most times higher stock price is indication of

good news for the company but the downside to that is any additional growth in the company

may not lead to increase in the stock price. In such a scenario the Return on equity it should also

be higher otherwise, a lower return of equity despite high P/B ratio indicates negative growth for

the business (Subalakshmi, Grahalakshmi and Manikandan, 2018)

d.

The P/E ratio is utilized for the determination of the stock's value based on the trailing

earning while consideration of company's future into account. For example, if the low P/E ratio

suggests that the stock is undervalued it can still happen that the expected earning's growth rate

Therefore, the free cash flow = 2185-1295 890

QUESTION 4

a.

Free cash flow is generated by the company after the accounting of the cash outflows for

supporting its operations and maintenance of its assets. Other than the earning and net income,

free cash flow is considered as the measurement to the profitability excluding the non-cash

expenses of the income statements. It can be used for spending on equipment and assets and also

on creating changes in the working capital. This company can use the cash for repayment to the

creditors or paying dividends, interest to the investors (Sam, Li and Ismail, 2017). Depreciation

is limitation to the free cash flow as the purpose of charging depreciation for the company is that

it can generate saving so that it can purchase assets on behalf of that cash. However, utilization

of such cash for paying off creditors can be very effective when the asset is fully depreciated.

b.

The company that has a lower P/E ratio it shows that the value of the stocks is lower.

However, if that company has a higher P/B ratio it indicates that the price of the stocks in the

book is lower than that of the actual price of the company's stocks (Borate, 2019). It also

indicates that the earning of the company is higher than that of the company's stock.

c.

P/B ratio is the indication of the growth of the company. Generally, when the P/B ratio is

high the earning of the company is also very high. Most times higher stock price is indication of

good news for the company but the downside to that is any additional growth in the company

may not lead to increase in the stock price. In such a scenario the Return on equity it should also

be higher otherwise, a lower return of equity despite high P/B ratio indicates negative growth for

the business (Subalakshmi, Grahalakshmi and Manikandan, 2018)

d.

The P/E ratio is utilized for the determination of the stock's value based on the trailing

earning while consideration of company's future into account. For example, if the low P/E ratio

suggests that the stock is undervalued it can still happen that the expected earning's growth rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the future increases. This happens as PEG ratio is considered to be good when it is at 1 or

lower which suggests that the stock is fairly priced or is undervalued.

e.

Return on equity is the measurement of the financial performance of the company which

is calculated by the division of net income with the shareholder's equity (Haralayya, 2021). It

measures the corporation's profitability in relation to stockholder's equity. Increasing the debt, a

company increases its total assets which can be cash, or any kind of asset. The equity in ROE, is

equal to the assets minus the total debt. The company as a result decreases its equity by

increasing its debt or in other words increasing the borrowing effects the return on equity. In the

increase in debt shrinks the equity and as the formula of ROE has equity as the denominator, the

Return on equity increases.

QUESTION 5

A

The return on capital employed is the return which company is providing to its

shareholders. With the analysis of the data provided by Everest Ltd, it is clear that return on

capital equity has increased in comparison to last year (Murtala and et.al., 2018). This is

particularly due to the changes within the financing and operating activities. with respect to the

operating activity the sales of company have increased by 23.25 % and as a result of this profits

also increased. On the basis of operating income after tax it is evident that there is 18.60 %

increase in profit after tax. With this it can be implied that due to increase in profits the return on

capital employed has increased. Further with reference to financing activity both financial

obligation and average common shareholder equity has increased. With this it can be assumed

that with increase in shareholders and debt obligation the company will invest money in

operations and as a result of this profitability will be increased and will be provided to the

shareholders as return.

B

The return on net asset is a measure which assist the company in evaluating the financial

performance of the company based on the fixed assets. With the evaluation of Everest Ltd, data it

is clearly visible that return on net asset has reduced from 13.87 % to 12.86 %. With respect to

profit margin it is clear that profit has increased in comparison to last year and this will be

lower which suggests that the stock is fairly priced or is undervalued.

e.

Return on equity is the measurement of the financial performance of the company which

is calculated by the division of net income with the shareholder's equity (Haralayya, 2021). It

measures the corporation's profitability in relation to stockholder's equity. Increasing the debt, a

company increases its total assets which can be cash, or any kind of asset. The equity in ROE, is

equal to the assets minus the total debt. The company as a result decreases its equity by

increasing its debt or in other words increasing the borrowing effects the return on equity. In the

increase in debt shrinks the equity and as the formula of ROE has equity as the denominator, the

Return on equity increases.

QUESTION 5

A

The return on capital employed is the return which company is providing to its

shareholders. With the analysis of the data provided by Everest Ltd, it is clear that return on

capital equity has increased in comparison to last year (Murtala and et.al., 2018). This is

particularly due to the changes within the financing and operating activities. with respect to the

operating activity the sales of company have increased by 23.25 % and as a result of this profits

also increased. On the basis of operating income after tax it is evident that there is 18.60 %

increase in profit after tax. With this it can be implied that due to increase in profits the return on

capital employed has increased. Further with reference to financing activity both financial

obligation and average common shareholder equity has increased. With this it can be assumed

that with increase in shareholders and debt obligation the company will invest money in

operations and as a result of this profitability will be increased and will be provided to the

shareholders as return.

B

The return on net asset is a measure which assist the company in evaluating the financial

performance of the company based on the fixed assets. With the evaluation of Everest Ltd, data it

is clearly visible that return on net asset has reduced from 13.87 % to 12.86 %. With respect to

profit margin it is clear that profit has increased in comparison to last year and this will be

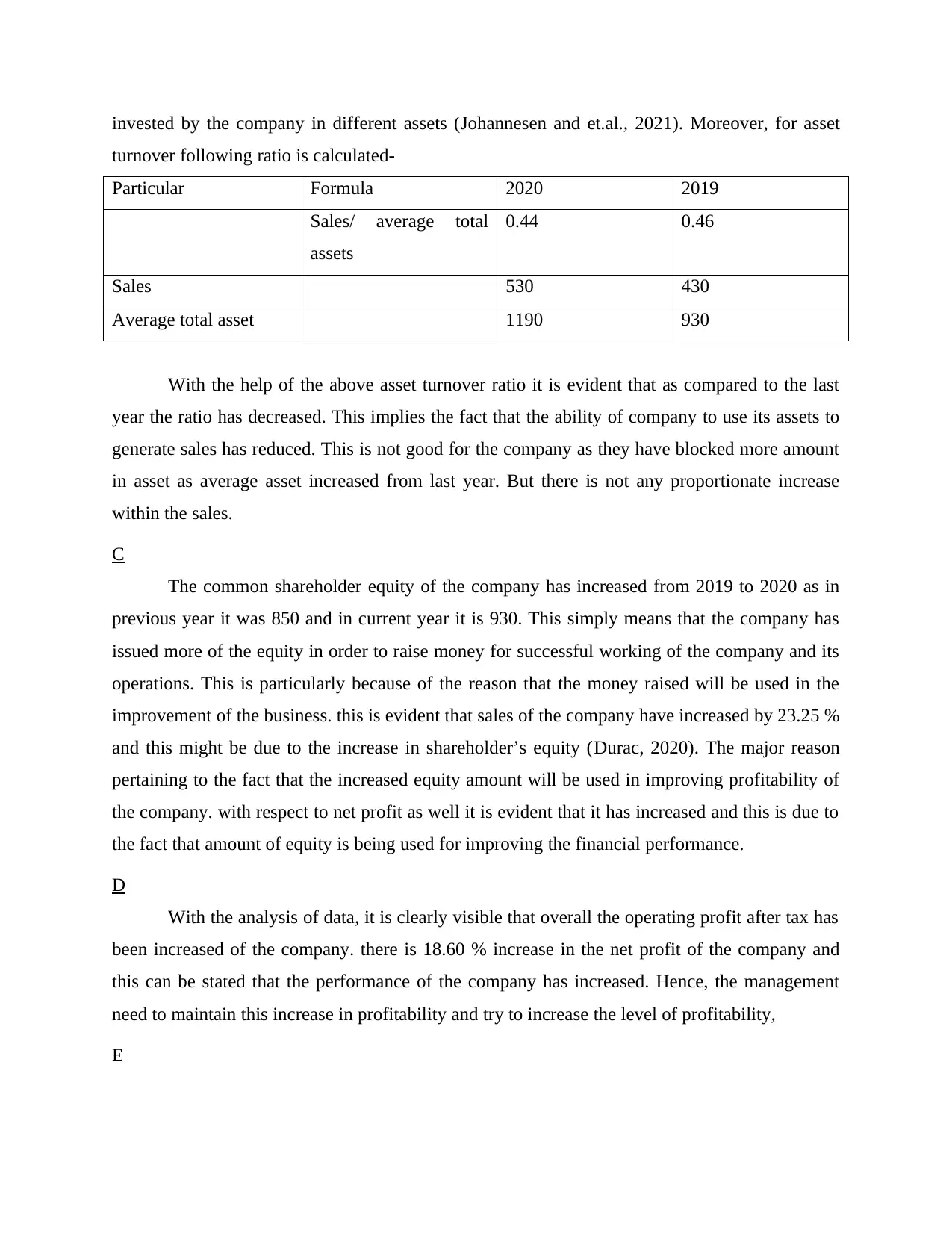

invested by the company in different assets (Johannesen and et.al., 2021). Moreover, for asset

turnover following ratio is calculated-

Particular Formula 2020 2019

Sales/ average total

assets

0.44 0.46

Sales 530 430

Average total asset 1190 930

With the help of the above asset turnover ratio it is evident that as compared to the last

year the ratio has decreased. This implies the fact that the ability of company to use its assets to

generate sales has reduced. This is not good for the company as they have blocked more amount

in asset as average asset increased from last year. But there is not any proportionate increase

within the sales.

C

The common shareholder equity of the company has increased from 2019 to 2020 as in

previous year it was 850 and in current year it is 930. This simply means that the company has

issued more of the equity in order to raise money for successful working of the company and its

operations. This is particularly because of the reason that the money raised will be used in the

improvement of the business. this is evident that sales of the company have increased by 23.25 %

and this might be due to the increase in shareholder’s equity (Durac, 2020). The major reason

pertaining to the fact that the increased equity amount will be used in improving profitability of

the company. with respect to net profit as well it is evident that it has increased and this is due to

the fact that amount of equity is being used for improving the financial performance.

D

With the analysis of data, it is clearly visible that overall the operating profit after tax has

been increased of the company. there is 18.60 % increase in the net profit of the company and

this can be stated that the performance of the company has increased. Hence, the management

need to maintain this increase in profitability and try to increase the level of profitability,

E

turnover following ratio is calculated-

Particular Formula 2020 2019

Sales/ average total

assets

0.44 0.46

Sales 530 430

Average total asset 1190 930

With the help of the above asset turnover ratio it is evident that as compared to the last

year the ratio has decreased. This implies the fact that the ability of company to use its assets to

generate sales has reduced. This is not good for the company as they have blocked more amount

in asset as average asset increased from last year. But there is not any proportionate increase

within the sales.

C

The common shareholder equity of the company has increased from 2019 to 2020 as in

previous year it was 850 and in current year it is 930. This simply means that the company has

issued more of the equity in order to raise money for successful working of the company and its

operations. This is particularly because of the reason that the money raised will be used in the

improvement of the business. this is evident that sales of the company have increased by 23.25 %

and this might be due to the increase in shareholder’s equity (Durac, 2020). The major reason

pertaining to the fact that the increased equity amount will be used in improving profitability of

the company. with respect to net profit as well it is evident that it has increased and this is due to

the fact that amount of equity is being used for improving the financial performance.

D

With the analysis of data, it is clearly visible that overall the operating profit after tax has

been increased of the company. there is 18.60 % increase in the net profit of the company and

this can be stated that the performance of the company has increased. Hence, the management

need to maintain this increase in profitability and try to increase the level of profitability,

E

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With help of the above calculation it is clear that the company is having a competitive

advantage. This is particularly because of the reason that the net profit of company has increased

and this implies that company is performing in proper manner (Tondok, Pahlevi and Aswan,

2019). In addition to this, ROCE of company is also good which implies that company is

providing good returns to the shareholders. Hence, this will attract more of the people to invest in

equity of company which will provide a competitive advantage to the company.

advantage. This is particularly because of the reason that the net profit of company has increased

and this implies that company is performing in proper manner (Tondok, Pahlevi and Aswan,

2019). In addition to this, ROCE of company is also good which implies that company is

providing good returns to the shareholders. Hence, this will attract more of the people to invest in

equity of company which will provide a competitive advantage to the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

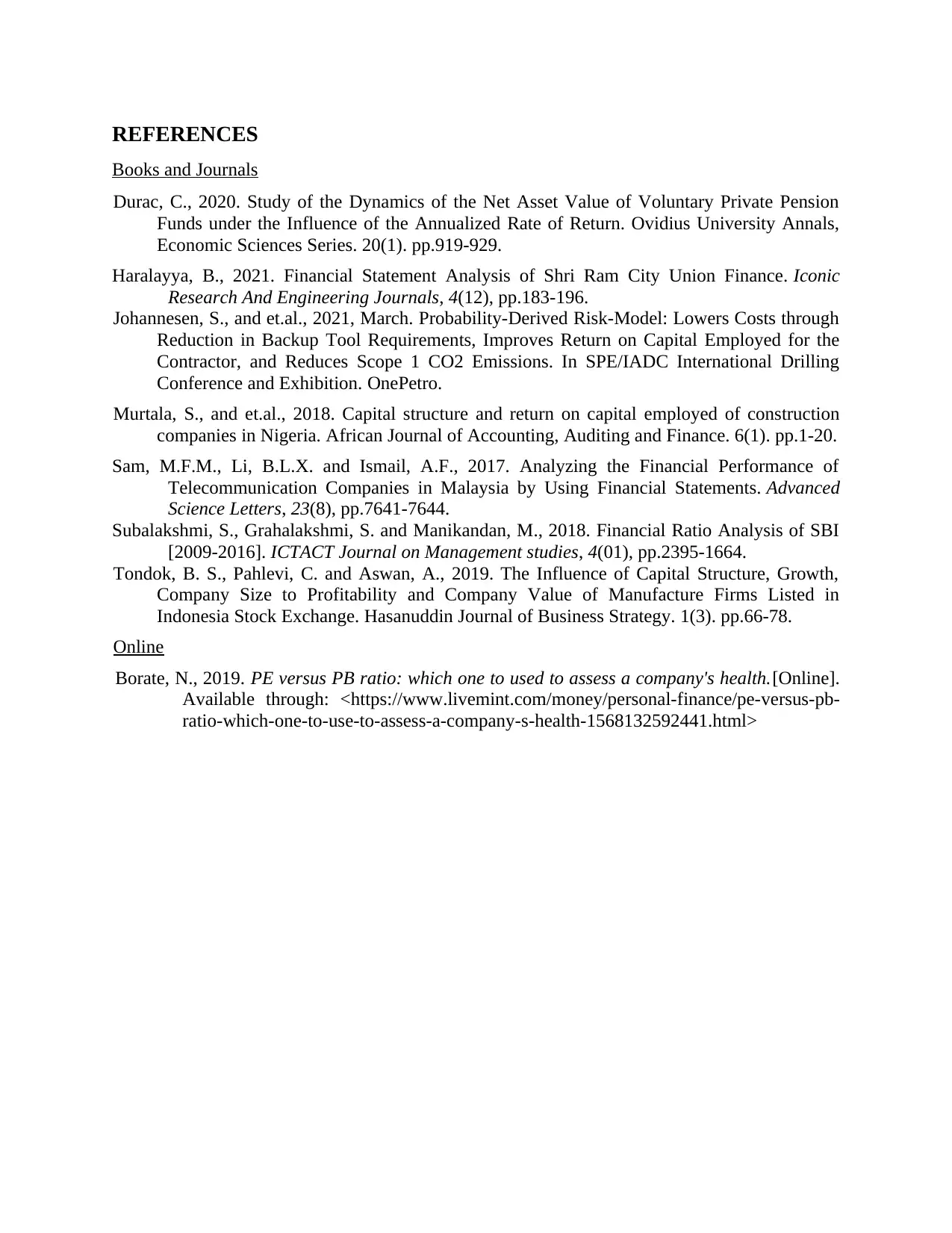

REFERENCES

Books and Journals

Durac, C., 2020. Study of the Dynamics of the Net Asset Value of Voluntary Private Pension

Funds under the Influence of the Annualized Rate of Return. Ovidius University Annals,

Economic Sciences Series. 20(1). pp.919-929.

Haralayya, B., 2021. Financial Statement Analysis of Shri Ram City Union Finance. Iconic

Research And Engineering Journals, 4(12), pp.183-196.

Johannesen, S., and et.al., 2021, March. Probability-Derived Risk-Model: Lowers Costs through

Reduction in Backup Tool Requirements, Improves Return on Capital Employed for the

Contractor, and Reduces Scope 1 CO2 Emissions. In SPE/IADC International Drilling

Conference and Exhibition. OnePetro.

Murtala, S., and et.al., 2018. Capital structure and return on capital employed of construction

companies in Nigeria. African Journal of Accounting, Auditing and Finance. 6(1). pp.1-20.

Sam, M.F.M., Li, B.L.X. and Ismail, A.F., 2017. Analyzing the Financial Performance of

Telecommunication Companies in Malaysia by Using Financial Statements. Advanced

Science Letters, 23(8), pp.7641-7644.

Subalakshmi, S., Grahalakshmi, S. and Manikandan, M., 2018. Financial Ratio Analysis of SBI

[2009-2016]. ICTACT Journal on Management studies, 4(01), pp.2395-1664.

Tondok, B. S., Pahlevi, C. and Aswan, A., 2019. The Influence of Capital Structure, Growth,

Company Size to Profitability and Company Value of Manufacture Firms Listed in

Indonesia Stock Exchange. Hasanuddin Journal of Business Strategy. 1(3). pp.66-78.

Online

Borate, N., 2019. PE versus PB ratio: which one to used to assess a company's health.[Online].

Available through: <https://www.livemint.com/money/personal-finance/pe-versus-pb-

ratio-which-one-to-use-to-assess-a-company-s-health-1568132592441.html>

Books and Journals

Durac, C., 2020. Study of the Dynamics of the Net Asset Value of Voluntary Private Pension

Funds under the Influence of the Annualized Rate of Return. Ovidius University Annals,

Economic Sciences Series. 20(1). pp.919-929.

Haralayya, B., 2021. Financial Statement Analysis of Shri Ram City Union Finance. Iconic

Research And Engineering Journals, 4(12), pp.183-196.

Johannesen, S., and et.al., 2021, March. Probability-Derived Risk-Model: Lowers Costs through

Reduction in Backup Tool Requirements, Improves Return on Capital Employed for the

Contractor, and Reduces Scope 1 CO2 Emissions. In SPE/IADC International Drilling

Conference and Exhibition. OnePetro.

Murtala, S., and et.al., 2018. Capital structure and return on capital employed of construction

companies in Nigeria. African Journal of Accounting, Auditing and Finance. 6(1). pp.1-20.

Sam, M.F.M., Li, B.L.X. and Ismail, A.F., 2017. Analyzing the Financial Performance of

Telecommunication Companies in Malaysia by Using Financial Statements. Advanced

Science Letters, 23(8), pp.7641-7644.

Subalakshmi, S., Grahalakshmi, S. and Manikandan, M., 2018. Financial Ratio Analysis of SBI

[2009-2016]. ICTACT Journal on Management studies, 4(01), pp.2395-1664.

Tondok, B. S., Pahlevi, C. and Aswan, A., 2019. The Influence of Capital Structure, Growth,

Company Size to Profitability and Company Value of Manufacture Firms Listed in

Indonesia Stock Exchange. Hasanuddin Journal of Business Strategy. 1(3). pp.66-78.

Online

Borate, N., 2019. PE versus PB ratio: which one to used to assess a company's health.[Online].

Available through: <https://www.livemint.com/money/personal-finance/pe-versus-pb-

ratio-which-one-to-use-to-assess-a-company-s-health-1568132592441.html>

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.