HI5020 Corporate Accounting: Detailed Analysis of Galaxy Resources

VerifiedAdded on 2023/06/11

|15

|2981

|120

Report

AI Summary

This report provides a financial analysis of Galaxy Resources Limited, an Australian mining company listed on the ASX. It examines the company's cash flow statement, highlighting changes in operating, investing, and financing activities between 2016 and 2017. The analysis includes a discussion of items reported under other comprehensive income, such as foreign currency transactions and revaluation of assets. Furthermore, the report delves into the company's accounting for corporate income tax, including deferred tax assets and reconciliation of income tax expenses. The report concludes with insights into the company's financial position based on the analyzed data.

Audit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 22nd May 2018.

[Type here]

By student name

Professor

University

Date: 22nd May 2018.

[Type here]

2

Executive Summary

Audit report is an essential record that the company is required to submit and hence it is essential all

that is stated and related to the company must be accurate and there should not be any avoidance

within it. Required topics that the auditor is required to intimate has been mentioned in this assignment

with appropriate analysis and conclusion. Portion from the annual reports of 2 companies have been

adopted and checked to look as to the way, they have been reporting important topics in their audit

report.

[Type here]

Executive Summary

Audit report is an essential record that the company is required to submit and hence it is essential all

that is stated and related to the company must be accurate and there should not be any avoidance

within it. Required topics that the auditor is required to intimate has been mentioned in this assignment

with appropriate analysis and conclusion. Portion from the annual reports of 2 companies have been

adopted and checked to look as to the way, they have been reporting important topics in their audit

report.

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTENTS:

Introduction...........…………………………………………………………………..........…...4

Analysis.......................………………........................................................................................6

Conclusion.......................………………...................................................................................10

References......................……………….....................................................................................11

[Type here]

CONTENTS:

Introduction...........…………………………………………………………………..........…...4

Analysis.......................………………........................................................................................6

Conclusion.......................………………...................................................................................10

References......................……………….....................................................................................11

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Galaxy Resources Limited

Introduction

In this assignment the financial statements of galaxy resources limited has been discussed and

important matters is analysed and presented. There are various elements in the financial statements the

users do not have follow knowledge of that, so they need expert help who can guide them and tell them

who needs what. In this case also the experts have extracted certain elements from the financial

statements and have presented it in a brief manner so that users can relate to it and can decide whether

they want to invest in the company or not. The cash flow statement and other items that might affect

the financial position of the company has been extracted and presented below. Formulas and

judgement has been applied to reach to a conclusion on whether the management should invest in this

company or not. Galaxy resource Limited is an Australian company that works in the mining industry and

is also present in the ASX list of top 100 companies (Alexander, 2016). The overall revenue of the

company runs into millions and the stocks of the company are listed in the Australian Stock Exchange. It

begun its operations in 2009 and has been operating since then. The financials of the company have

been extracted and analysed below, with proper recommendations and conclusion being given below –

[Type here]

Galaxy Resources Limited

Introduction

In this assignment the financial statements of galaxy resources limited has been discussed and

important matters is analysed and presented. There are various elements in the financial statements the

users do not have follow knowledge of that, so they need expert help who can guide them and tell them

who needs what. In this case also the experts have extracted certain elements from the financial

statements and have presented it in a brief manner so that users can relate to it and can decide whether

they want to invest in the company or not. The cash flow statement and other items that might affect

the financial position of the company has been extracted and presented below. Formulas and

judgement has been applied to reach to a conclusion on whether the management should invest in this

company or not. Galaxy resource Limited is an Australian company that works in the mining industry and

is also present in the ASX list of top 100 companies (Alexander, 2016). The overall revenue of the

company runs into millions and the stocks of the company are listed in the Australian Stock Exchange. It

begun its operations in 2009 and has been operating since then. The financials of the company have

been extracted and analysed below, with proper recommendations and conclusion being given below –

[Type here]

5

Analysis

[Type here]

Analysis

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

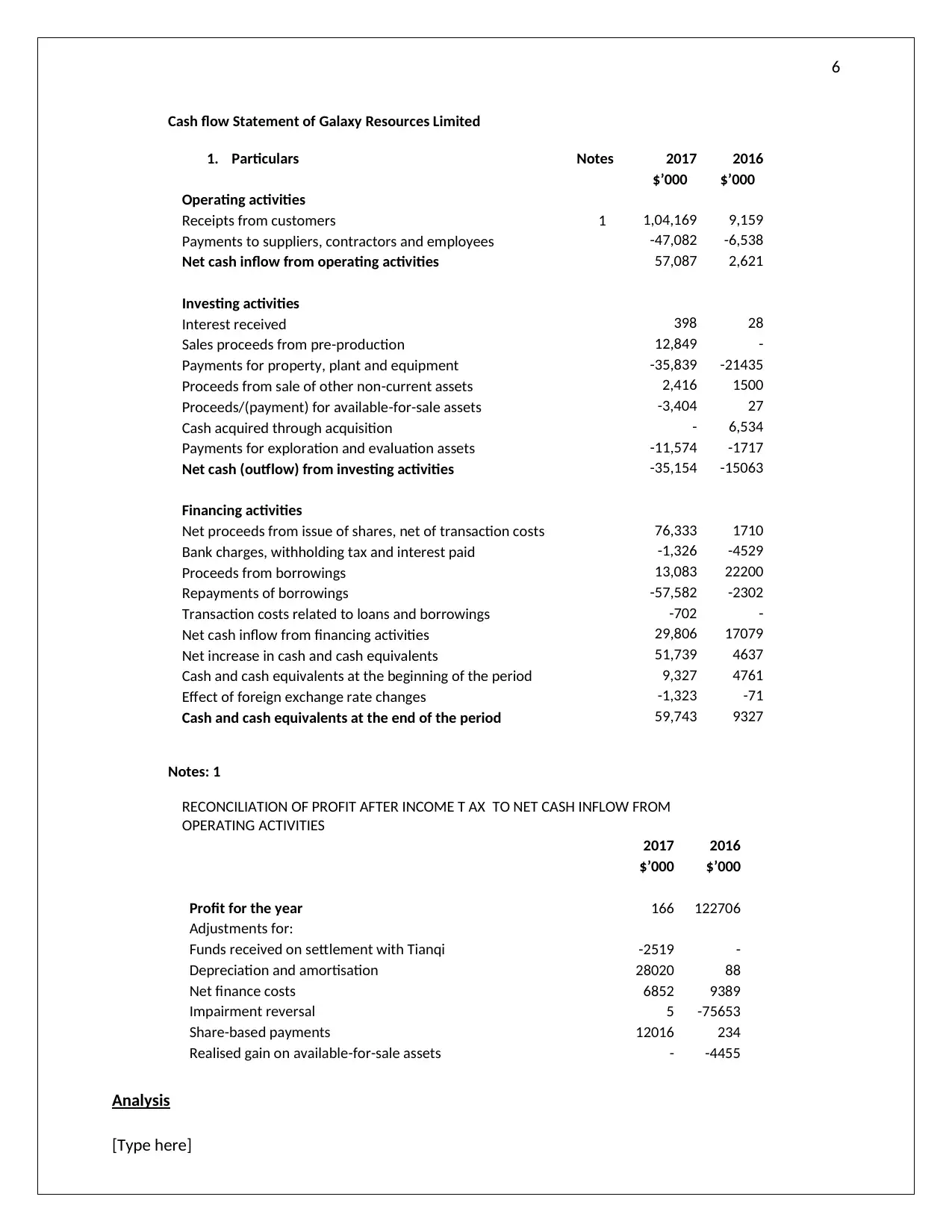

Cash flow Statement of Galaxy Resources Limited

1. Particulars Notes 2017 2016

$’000 $’000

Operating activities

Receipts from customers 1 1,04,169 9,159

Payments to suppliers, contractors and employees -47,082 -6,538

Net cash inflow from operating activities 57,087 2,621

Investing activities

Interest received 398 28

Sales proceeds from pre-production 12,849 -

Payments for property, plant and equipment -35,839 -21435

Proceeds from sale of other non-current assets 2,416 1500

Proceeds/(payment) for available-for-sale assets -3,404 27

Cash acquired through acquisition - 6,534

Payments for exploration and evaluation assets -11,574 -1717

Net cash (outflow) from investing activities -35,154 -15063

Financing activities

Net proceeds from issue of shares, net of transaction costs 76,333 1710

Bank charges, withholding tax and interest paid -1,326 -4529

Proceeds from borrowings 13,083 22200

Repayments of borrowings -57,582 -2302

Transaction costs related to loans and borrowings -702 -

Net cash inflow from financing activities 29,806 17079

Net increase in cash and cash equivalents 51,739 4637

Cash and cash equivalents at the beginning of the period 9,327 4761

Effect of foreign exchange rate changes -1,323 -71

Cash and cash equivalents at the end of the period 59,743 9327

Notes: 1

RECONCILIATION OF PROFIT AFTER INCOME T AX TO NET CASH INFLOW FROM

OPERATING ACTIVITIES

2017 2016

$’000 $’000

Profit for the year 166 122706

Adjustments for:

Funds received on settlement with Tianqi -2519 -

Depreciation and amortisation 28020 88

Net finance costs 6852 9389

Impairment reversal 5 -75653

Share-based payments 12016 234

Realised gain on available-for-sale assets - -4455

Analysis

[Type here]

Cash flow Statement of Galaxy Resources Limited

1. Particulars Notes 2017 2016

$’000 $’000

Operating activities

Receipts from customers 1 1,04,169 9,159

Payments to suppliers, contractors and employees -47,082 -6,538

Net cash inflow from operating activities 57,087 2,621

Investing activities

Interest received 398 28

Sales proceeds from pre-production 12,849 -

Payments for property, plant and equipment -35,839 -21435

Proceeds from sale of other non-current assets 2,416 1500

Proceeds/(payment) for available-for-sale assets -3,404 27

Cash acquired through acquisition - 6,534

Payments for exploration and evaluation assets -11,574 -1717

Net cash (outflow) from investing activities -35,154 -15063

Financing activities

Net proceeds from issue of shares, net of transaction costs 76,333 1710

Bank charges, withholding tax and interest paid -1,326 -4529

Proceeds from borrowings 13,083 22200

Repayments of borrowings -57,582 -2302

Transaction costs related to loans and borrowings -702 -

Net cash inflow from financing activities 29,806 17079

Net increase in cash and cash equivalents 51,739 4637

Cash and cash equivalents at the beginning of the period 9,327 4761

Effect of foreign exchange rate changes -1,323 -71

Cash and cash equivalents at the end of the period 59,743 9327

Notes: 1

RECONCILIATION OF PROFIT AFTER INCOME T AX TO NET CASH INFLOW FROM

OPERATING ACTIVITIES

2017 2016

$’000 $’000

Profit for the year 166 122706

Adjustments for:

Funds received on settlement with Tianqi -2519 -

Depreciation and amortisation 28020 88

Net finance costs 6852 9389

Impairment reversal 5 -75653

Share-based payments 12016 234

Realised gain on available-for-sale assets - -4455

Analysis

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

1. Effect from Changes and Comparative analysis of the cash flow of Galaxy Resources Limited are

discussed below: -

There are following changes in cash flow since last year 2016: -

1. Receipt from customer increase in 2017 because revenue increases of the company will rise.

Further profit of last year 2016 is very high in compare to profit in 2017 but there are various

changes which result the increase in income of cash flow from operating activity of the

company. Item that effect the cash flow is Depreciation and amortisation, Impairment reversal,

Share-based payments, Profit on sale of those assets which are available for sale, Transaction

costs on acquisition of company, Net inventory movement, Deferred tax on available for sale

assets, Deferred income to investing activities, Adjustment to rehabilitation provision, Change in

Debtor and other receivables in two years, Change in value of Creditors and other payable,

Change in value of inventories, Change in value of prepayments, Change in amount of provisions

and employee benefits, and Difference in deferred tax assets of the company. Further what

amount of changes made is already mentioned in above table of Cash flow from operating

activities. Cash flow will increase to $57087000 in the year 2017 because of change in above

item during the year of the company.

2. Income from investing activities of Galaxy Resources Limited in the year 2017 net outflow from

investing activity will increase to ($35154000) due to increase in interest received, Sales

proceeds from pre-production and Proceeds from sale of other non-current asset during this

year. And also increase in outflow of Payments for property, plant and equipment,

Proceeds/(payment) for sale of assets which are available for sale and any Payments for

revaluation of assets. These items will result to increase the net outflow from last year 2016.

3. Cash flow from financing Activity will increase in the year 2017 due to changes in following item.

Like: - change in value of Net proceeds from issue of shares, Transaction costs on issue of share,

Amount of Bank charges paid, Amount of withholding tax paid and interest paid, Proceeds from

borrowings, Repayments of borrowings, Transaction costs related to loans and borrowings and

Effect of foreign exchange rate changes. These items will result to increase the cash flow from

financing activity in the year 2017 amounting to $ 59743000.

4. Further apart from the above item cash and cash equivalent will also increase in the year 2017.

This is also factoring to change in cash flow activity of the company. Increase in cash flow means

[Type here]

1. Effect from Changes and Comparative analysis of the cash flow of Galaxy Resources Limited are

discussed below: -

There are following changes in cash flow since last year 2016: -

1. Receipt from customer increase in 2017 because revenue increases of the company will rise.

Further profit of last year 2016 is very high in compare to profit in 2017 but there are various

changes which result the increase in income of cash flow from operating activity of the

company. Item that effect the cash flow is Depreciation and amortisation, Impairment reversal,

Share-based payments, Profit on sale of those assets which are available for sale, Transaction

costs on acquisition of company, Net inventory movement, Deferred tax on available for sale

assets, Deferred income to investing activities, Adjustment to rehabilitation provision, Change in

Debtor and other receivables in two years, Change in value of Creditors and other payable,

Change in value of inventories, Change in value of prepayments, Change in amount of provisions

and employee benefits, and Difference in deferred tax assets of the company. Further what

amount of changes made is already mentioned in above table of Cash flow from operating

activities. Cash flow will increase to $57087000 in the year 2017 because of change in above

item during the year of the company.

2. Income from investing activities of Galaxy Resources Limited in the year 2017 net outflow from

investing activity will increase to ($35154000) due to increase in interest received, Sales

proceeds from pre-production and Proceeds from sale of other non-current asset during this

year. And also increase in outflow of Payments for property, plant and equipment,

Proceeds/(payment) for sale of assets which are available for sale and any Payments for

revaluation of assets. These items will result to increase the net outflow from last year 2016.

3. Cash flow from financing Activity will increase in the year 2017 due to changes in following item.

Like: - change in value of Net proceeds from issue of shares, Transaction costs on issue of share,

Amount of Bank charges paid, Amount of withholding tax paid and interest paid, Proceeds from

borrowings, Repayments of borrowings, Transaction costs related to loans and borrowings and

Effect of foreign exchange rate changes. These items will result to increase the cash flow from

financing activity in the year 2017 amounting to $ 59743000.

4. Further apart from the above item cash and cash equivalent will also increase in the year 2017.

This is also factoring to change in cash flow activity of the company. Increase in cash flow means

[Type here]

8

Galaxy Resources Limited will have more Liquid cash in hand to run the day to day operation of

the company.

Other comprehensive income statement of Galaxy Resources Limited

2. There are following item which reported under other comprehensive income statement

Profit or loss Foreign Currency Transaction which arise due to change in price of the

currency – foreign operations

Revaluation of available for sale financial assets

Income tax relating to sale of those assets which are available for sale

Change in fair value of assets and liability

Revaluation of Fixed assets

Revaluation of financial instrument

Retirement Benefits

Actuary gain

Actuary loss

Pension prior period service cost or credit (Goldmann, 2016).

3. Other comprehensive income statement is providing an overview of company's financial

statements in a more comprehensive way, which helps to understand the current financial

position of the company very easily.

Item which may be reclassified during the year is mentioned in the other comprehensive

income statement. These items are classified in other comprehensive income statement of

the company because this is not a part of normal income statement. Further Reporting of

such item in (OCI) other comprehensive income is provided by the (IFRS) international

financial reporting Standards. Treatment of the entire above items is done provided as

the manner prescribed by international financial reporting Standards. Further

reclassification of assets and liabilities are done from fair value change through Other

comprehensive income to fair value through Profit and Loss account are consider in OCI of

the company. There are 3 methods through which we can done the accounting the method

[Type here]

Galaxy Resources Limited will have more Liquid cash in hand to run the day to day operation of

the company.

Other comprehensive income statement of Galaxy Resources Limited

2. There are following item which reported under other comprehensive income statement

Profit or loss Foreign Currency Transaction which arise due to change in price of the

currency – foreign operations

Revaluation of available for sale financial assets

Income tax relating to sale of those assets which are available for sale

Change in fair value of assets and liability

Revaluation of Fixed assets

Revaluation of financial instrument

Retirement Benefits

Actuary gain

Actuary loss

Pension prior period service cost or credit (Goldmann, 2016).

3. Other comprehensive income statement is providing an overview of company's financial

statements in a more comprehensive way, which helps to understand the current financial

position of the company very easily.

Item which may be reclassified during the year is mentioned in the other comprehensive

income statement. These items are classified in other comprehensive income statement of

the company because this is not a part of normal income statement. Further Reporting of

such item in (OCI) other comprehensive income is provided by the (IFRS) international

financial reporting Standards. Treatment of the entire above items is done provided as

the manner prescribed by international financial reporting Standards. Further

reclassification of assets and liabilities are done from fair value change through Other

comprehensive income to fair value through Profit and Loss account are consider in OCI of

the company. There are 3 methods through which we can done the accounting the method

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

is Fair value change through profit and loss account method, Fair value change through

other comprehensive income and Amortisation method is followed to value any change in

financial instrument, Such revaluation recorded in other comprehensive income statement

of the company (Alexander, 2016).

4. Other comprehensive income statement of company includes revenues, expenses, gains, and

losses which are prescribed under the Generally Accepted Accounting

Principles and International Financial Reporting Standards. Other comprehensive incomes are

not a part of normal income of the company. Normal income is different from other

comprehensive income statement. Further Revenues, expenses, gains and losses appear in

other comprehensive income which is not realized yet. Further some are realized when the

underlying transaction has been completed. For example, if a company has invested in Security,

and the value of such Security changes, then we recognize the difference of such Security as a

gain or loss and recorded in other comprehensive income. At the time of selling of such security,

company earn profit or loss from such security, and then company record above gain or loss

which arises on sale of security is recorded in other comprehensive income. Further we consider

the treatment which is prescribe by (Belton, 2017)

International financial reporting Standards we do not consider the above item in Normal

income statement of the company.

Accounting for Corporate Income tax

5. The tax expenses of Galaxy Resources Limited is as per the latest financial expenses is

($5999000).

Further Income tax relating to revaluation of those assets which are available for sale of Galaxy

Resources Limited is ($5070000)

6. No, Amount of income tax of company and rate of income tax charged on company are not

same. A reconciliation of income tax benefit applicable to accounting profit/(loss) before income

tax at the statutory income tax rate to income tax expense at the Group’s effective income tax

rate for the years ended 31 December 2017 and 31 December 2016 is as follows:

[Type here]

is Fair value change through profit and loss account method, Fair value change through

other comprehensive income and Amortisation method is followed to value any change in

financial instrument, Such revaluation recorded in other comprehensive income statement

of the company (Alexander, 2016).

4. Other comprehensive income statement of company includes revenues, expenses, gains, and

losses which are prescribed under the Generally Accepted Accounting

Principles and International Financial Reporting Standards. Other comprehensive incomes are

not a part of normal income of the company. Normal income is different from other

comprehensive income statement. Further Revenues, expenses, gains and losses appear in

other comprehensive income which is not realized yet. Further some are realized when the

underlying transaction has been completed. For example, if a company has invested in Security,

and the value of such Security changes, then we recognize the difference of such Security as a

gain or loss and recorded in other comprehensive income. At the time of selling of such security,

company earn profit or loss from such security, and then company record above gain or loss

which arises on sale of security is recorded in other comprehensive income. Further we consider

the treatment which is prescribe by (Belton, 2017)

International financial reporting Standards we do not consider the above item in Normal

income statement of the company.

Accounting for Corporate Income tax

5. The tax expenses of Galaxy Resources Limited is as per the latest financial expenses is

($5999000).

Further Income tax relating to revaluation of those assets which are available for sale of Galaxy

Resources Limited is ($5070000)

6. No, Amount of income tax of company and rate of income tax charged on company are not

same. A reconciliation of income tax benefit applicable to accounting profit/(loss) before income

tax at the statutory income tax rate to income tax expense at the Group’s effective income tax

rate for the years ended 31 December 2017 and 31 December 2016 is as follows:

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

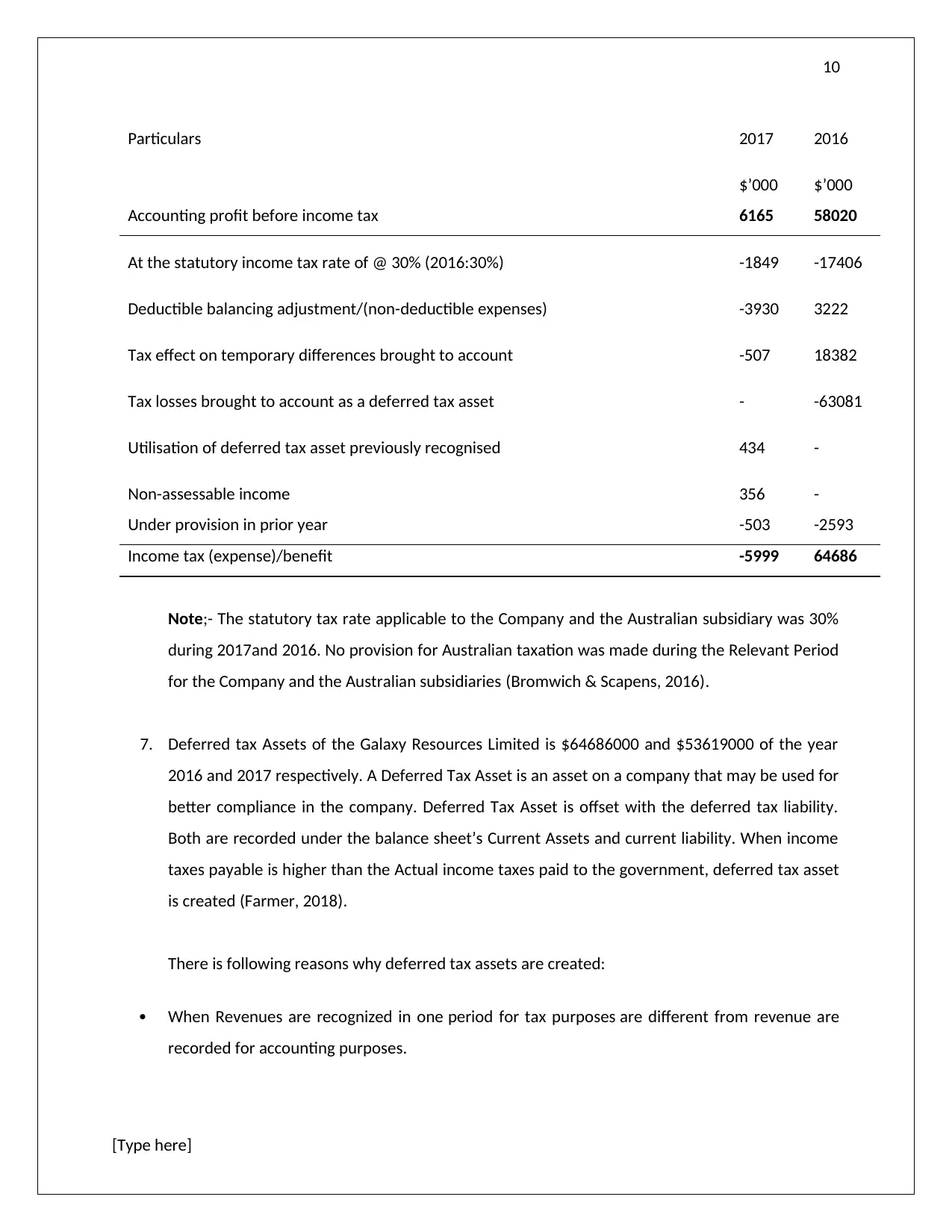

Particulars 2017 2016

$’000 $’000

Accounting profit before income tax 6165 58020

At the statutory income tax rate of @ 30% (2016:30%) -1849 -17406

Deductible balancing adjustment/(non-deductible expenses) -3930 3222

Tax effect on temporary differences brought to account -507 18382

Tax losses brought to account as a deferred tax asset - -63081

Utilisation of deferred tax asset previously recognised 434 -

Non-assessable income 356 -

Under provision in prior year -503 -2593

Income tax (expense)/benefit -5999 64686

Note;- The statutory tax rate applicable to the Company and the Australian subsidiary was 30%

during 2017and 2016. No provision for Australian taxation was made during the Relevant Period

for the Company and the Australian subsidiaries (Bromwich & Scapens, 2016).

7. Deferred tax Assets of the Galaxy Resources Limited is $64686000 and $53619000 of the year

2016 and 2017 respectively. A Deferred Tax Asset is an asset on a company that may be used for

better compliance in the company. Deferred Tax Asset is offset with the deferred tax liability.

Both are recorded under the balance sheet’s Current Assets and current liability. When income

taxes payable is higher than the Actual income taxes paid to the government, deferred tax asset

is created (Farmer, 2018).

There is following reasons why deferred tax assets are created:

When Revenues are recognized in one period for tax purposes are different from revenue are

recorded for accounting purposes.

[Type here]

Particulars 2017 2016

$’000 $’000

Accounting profit before income tax 6165 58020

At the statutory income tax rate of @ 30% (2016:30%) -1849 -17406

Deductible balancing adjustment/(non-deductible expenses) -3930 3222

Tax effect on temporary differences brought to account -507 18382

Tax losses brought to account as a deferred tax asset - -63081

Utilisation of deferred tax asset previously recognised 434 -

Non-assessable income 356 -

Under provision in prior year -503 -2593

Income tax (expense)/benefit -5999 64686

Note;- The statutory tax rate applicable to the Company and the Australian subsidiary was 30%

during 2017and 2016. No provision for Australian taxation was made during the Relevant Period

for the Company and the Australian subsidiaries (Bromwich & Scapens, 2016).

7. Deferred tax Assets of the Galaxy Resources Limited is $64686000 and $53619000 of the year

2016 and 2017 respectively. A Deferred Tax Asset is an asset on a company that may be used for

better compliance in the company. Deferred Tax Asset is offset with the deferred tax liability.

Both are recorded under the balance sheet’s Current Assets and current liability. When income

taxes payable is higher than the Actual income taxes paid to the government, deferred tax asset

is created (Farmer, 2018).

There is following reasons why deferred tax assets are created:

When Revenues are recognized in one period for tax purposes are different from revenue are

recorded for accounting purposes.

[Type here]

11

When assets have a different tax base for the purpose of income tax and for the purpose of

accounting than deferred tax assets is recorded in the books.

When The Company paid excess tax, and refund is taken in future.

When Losses or expenses are recognized in the income statement but which are not recognising

by respective tax authority than differed tax is created (Chron, 2017).

Further Deferred tax is reported in the balance sheet because it is a reporting requirement of

both Generally Accepted Accounting Principles and International Financial Reporting Standards.

8. Yes the current income tax payable of Galaxy Resources Limited is ($17406000) and ($1849000)

for the year 2016 and 2017 respectively. Income tax payable are not the income tax expenses of

the company because income tax payable is an amount which is charged on profit as per the

applicable tax rate on the company, but the income tax actually paid are not same because we

should consider the differed tax before making the payment of tax to the government. After

taking the effect of differed tax whatever amount is left such amount is income tax expenses of

the company. This is the reason the income tax expenses and income tax payable are not same

of any company. Income tax is a amount what company owes in tax based on standard business

accounting rule (Das, 2017).

9. No, Income tax expenses which appear in income statement are different from cash flow’s tax

amount. Because the income tax expense which shown in income statement are the actual tax

amount which is payable by the company, the income tax expenses which reflect in cash flow

statement are the Actual tax amount which is paid by the company to the government during

the year. In cash flow we record the actual outflow of cash which is paid as a tax expenses

(Heminway, 2017). Further In cash flow statement we record the actual change of deferred tax

during the year. Further Accounting method followed by the company when reporting financial

results are often different from the method that followed for calculation of income taxes for the

company, As a result, the amount of tax calculated "should" pay based on its reported profit will

be different from its actual income tax expense. This disparity shows up in company’s financial

statements as a difference between "income tax expense" and "income tax payable (Kuhn &

Morris, 2016)."

[Type here]

When assets have a different tax base for the purpose of income tax and for the purpose of

accounting than deferred tax assets is recorded in the books.

When The Company paid excess tax, and refund is taken in future.

When Losses or expenses are recognized in the income statement but which are not recognising

by respective tax authority than differed tax is created (Chron, 2017).

Further Deferred tax is reported in the balance sheet because it is a reporting requirement of

both Generally Accepted Accounting Principles and International Financial Reporting Standards.

8. Yes the current income tax payable of Galaxy Resources Limited is ($17406000) and ($1849000)

for the year 2016 and 2017 respectively. Income tax payable are not the income tax expenses of

the company because income tax payable is an amount which is charged on profit as per the

applicable tax rate on the company, but the income tax actually paid are not same because we

should consider the differed tax before making the payment of tax to the government. After

taking the effect of differed tax whatever amount is left such amount is income tax expenses of

the company. This is the reason the income tax expenses and income tax payable are not same

of any company. Income tax is a amount what company owes in tax based on standard business

accounting rule (Das, 2017).

9. No, Income tax expenses which appear in income statement are different from cash flow’s tax

amount. Because the income tax expense which shown in income statement are the actual tax

amount which is payable by the company, the income tax expenses which reflect in cash flow

statement are the Actual tax amount which is paid by the company to the government during

the year. In cash flow we record the actual outflow of cash which is paid as a tax expenses

(Heminway, 2017). Further In cash flow statement we record the actual change of deferred tax

during the year. Further Accounting method followed by the company when reporting financial

results are often different from the method that followed for calculation of income taxes for the

company, As a result, the amount of tax calculated "should" pay based on its reported profit will

be different from its actual income tax expense. This disparity shows up in company’s financial

statements as a difference between "income tax expense" and "income tax payable (Kuhn &

Morris, 2016)."

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.