Corporate Accounting: Detailed Analysis of Nufarm's Financial Reports

VerifiedAdded on 2024/06/03

|17

|3163

|272

Report

AI Summary

This report provides an in-depth analysis of Nufarm's financial statements, focusing on the cash flow statement, other comprehensive income statement, and accounting for corporate income tax. It examines each item reported in the cash flow statement, providing a comparative analysis of operating, investing, and financing activities over three years (2015-2017). The report also discusses items reported in the other comprehensive income statement, explaining why these items are not included in the income statement. Furthermore, it analyzes Nufarm's tax expense, deferred tax assets/liabilities, and the differences between income tax expense and income tax paid. The analysis includes observations and insights gained about the company's tax treatment, offering a comprehensive view of Nufarm's financial accounting practices. Desklib provides access to similar solved assignments and resources for students.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

CASH FLOWS STATEMENT.......................................................................................................5

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and write your understanding of each item. Discuss any changes in each item

of CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for

the change....................................................................................................................................5

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.............................................................................................................7

OTHER COMPREHENSIVE INCOME STATEMENT................................................................8

(iii) What items have been reported in the other comprehensive income statement?.................8

(iv) Explain your understanding of each item reported in the other comprehensive income

statement......................................................................................................................................9

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.10

ACCOUNTING FOR CORPORATE INCOME TAX.................................................................11

(vi)What is your firm’s tax expense in its latest financial statements?.....................................11

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.................................................................12

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded................................................13

2

Introduction......................................................................................................................................4

CASH FLOWS STATEMENT.......................................................................................................5

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and write your understanding of each item. Discuss any changes in each item

of CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for

the change....................................................................................................................................5

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.............................................................................................................7

OTHER COMPREHENSIVE INCOME STATEMENT................................................................8

(iii) What items have been reported in the other comprehensive income statement?.................8

(iv) Explain your understanding of each item reported in the other comprehensive income

statement......................................................................................................................................9

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.10

ACCOUNTING FOR CORPORATE INCOME TAX.................................................................11

(vi)What is your firm’s tax expense in its latest financial statements?.....................................11

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.................................................................12

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded................................................13

2

(ix)Is there any a current tax asset or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?...................................................13

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..............................................14

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?.............................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

the income tax payable not the same as income tax expense?...................................................13

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..............................................14

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?.............................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report is divided in to different parts of financial statements. It analyses the financial

statements of Nufarm which is global agricultural inputs company. It supplies the better

standard quality products and services and also maintains the better relations with

customers. The objective of the Nufarm is to grow the better tomorrow by providing the

services and products. It discusses the profit and loss account that shows the income and

expenses of the company. It also evaluates the cash flow statements that denote the cash

inflow and cash outflow. Cash flow statements help the company to ascertain the

profitability and liquidity of the firm.

4

This report is divided in to different parts of financial statements. It analyses the financial

statements of Nufarm which is global agricultural inputs company. It supplies the better

standard quality products and services and also maintains the better relations with

customers. The objective of the Nufarm is to grow the better tomorrow by providing the

services and products. It discusses the profit and loss account that shows the income and

expenses of the company. It also evaluates the cash flow statements that denote the cash

inflow and cash outflow. Cash flow statements help the company to ascertain the

profitability and liquidity of the firm.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASH FLOWS STATEMENT

(i) From your firm’s financial statement, list each item reported in the CASH

FLOWS STATEMENT and write your understanding of each item. Discuss any

changes in each item of CASH FLOWS STATEMENT for your firm over the

past year articulating the reasons for the change.

Cash flow statements show the changes in income that affects the cash and cash equivalents and

carries out the operating, investing and financing activities.

Operating Activities:

Depreciation and amortisation: It is the expenditure on the fixed assets over the life. It can be

defined as the decrease in the value of fixed assets. Amortisation is the decrease in the value of

intangible assets it can be defined as the method off paying debt over time.

Non-cash materials: Non-cash current assets are consumed by the firm and they are not

converted in to cash. For example, depreciation, amortisation.

Net finance expense: It is the adjusted finance expense that arises from the operating activities.

Interest received: It is the amounts of interest that can be earned form the operating activities.

Dividends received: It is the amount that can be received on the purchase and sale of shares.

Interest paid: Interest is the payment from the borrower or deposit –taking to a depositor and

lender of an amount of sum.

Taxes paid: This expense for the company as they have to pay certain amount of tax.

Investing Activities:

Proceeds from sale of plant, equipment and property: It is the amount which can be earned by

the sale of plant and machinery and the company proceeds the activities from that amount.

5

(i) From your firm’s financial statement, list each item reported in the CASH

FLOWS STATEMENT and write your understanding of each item. Discuss any

changes in each item of CASH FLOWS STATEMENT for your firm over the

past year articulating the reasons for the change.

Cash flow statements show the changes in income that affects the cash and cash equivalents and

carries out the operating, investing and financing activities.

Operating Activities:

Depreciation and amortisation: It is the expenditure on the fixed assets over the life. It can be

defined as the decrease in the value of fixed assets. Amortisation is the decrease in the value of

intangible assets it can be defined as the method off paying debt over time.

Non-cash materials: Non-cash current assets are consumed by the firm and they are not

converted in to cash. For example, depreciation, amortisation.

Net finance expense: It is the adjusted finance expense that arises from the operating activities.

Interest received: It is the amounts of interest that can be earned form the operating activities.

Dividends received: It is the amount that can be received on the purchase and sale of shares.

Interest paid: Interest is the payment from the borrower or deposit –taking to a depositor and

lender of an amount of sum.

Taxes paid: This expense for the company as they have to pay certain amount of tax.

Investing Activities:

Proceeds from sale of plant, equipment and property: It is the amount which can be earned by

the sale of plant and machinery and the company proceeds the activities from that amount.

5

Proceeds from sales of investments and business: In this the company earned the money by

selling the investments and business.

Payments for equipment’s and plant: To invest the assets in company, they have to make

payments for the plant and machinery

Payments of business: The Company purchase the business to run their operations. For this they

have to make certain payment to that business.

Payments for acquired intangibles and development of product expenditure: To purchase the

intangibles and to develop the services and products the company has to make certain payments

(Allen and Seaman, 2017).

Financing Activities:

Debt establishment transaction costs: It includes that cost that can be spending at the time of

establishing company such as preliminary cost.

Proceeds from borrowings: It is the amount which can be established in exchange for a duty to

pay back something.

Repayment of borrowings: It is the situation in which money can be paid back and that can be

hired from a lender.

6

selling the investments and business.

Payments for equipment’s and plant: To invest the assets in company, they have to make

payments for the plant and machinery

Payments of business: The Company purchase the business to run their operations. For this they

have to make certain payment to that business.

Payments for acquired intangibles and development of product expenditure: To purchase the

intangibles and to develop the services and products the company has to make certain payments

(Allen and Seaman, 2017).

Financing Activities:

Debt establishment transaction costs: It includes that cost that can be spending at the time of

establishing company such as preliminary cost.

Proceeds from borrowings: It is the amount which can be established in exchange for a duty to

pay back something.

Repayment of borrowings: It is the situation in which money can be paid back and that can be

hired from a lender.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

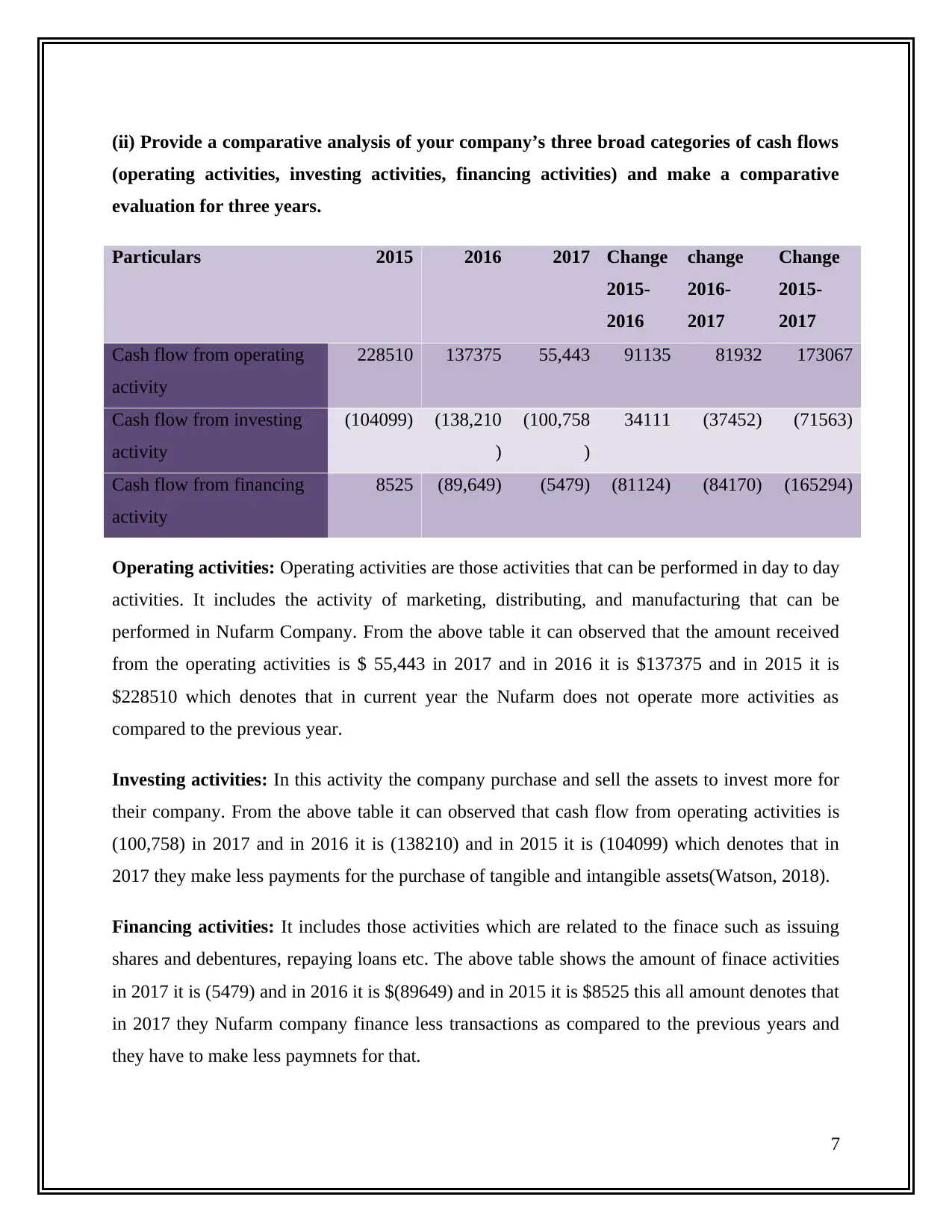

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.

Particulars 2015 2016 2017 Change

2015-

2016

change

2016-

2017

Change

2015-

2017

Cash flow from operating

activity

228510 137375 55,443 91135 81932 173067

Cash flow from investing

activity

(104099) (138,210

)

(100,758

)

34111 (37452) (71563)

Cash flow from financing

activity

8525 (89,649) (5479) (81124) (84170) (165294)

Operating activities: Operating activities are those activities that can be performed in day to day

activities. It includes the activity of marketing, distributing, and manufacturing that can be

performed in Nufarm Company. From the above table it can observed that the amount received

from the operating activities is $ 55,443 in 2017 and in 2016 it is $137375 and in 2015 it is

$228510 which denotes that in current year the Nufarm does not operate more activities as

compared to the previous year.

Investing activities: In this activity the company purchase and sell the assets to invest more for

their company. From the above table it can observed that cash flow from operating activities is

(100,758) in 2017 and in 2016 it is (138210) and in 2015 it is (104099) which denotes that in

2017 they make less payments for the purchase of tangible and intangible assets(Watson, 2018).

Financing activities: It includes those activities which are related to the finace such as issuing

shares and debentures, repaying loans etc. The above table shows the amount of finace activities

in 2017 it is (5479) and in 2016 it is $(89649) and in 2015 it is $8525 this all amount denotes that

in 2017 they Nufarm company finance less transactions as compared to the previous years and

they have to make less paymnets for that.

7

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years.

Particulars 2015 2016 2017 Change

2015-

2016

change

2016-

2017

Change

2015-

2017

Cash flow from operating

activity

228510 137375 55,443 91135 81932 173067

Cash flow from investing

activity

(104099) (138,210

)

(100,758

)

34111 (37452) (71563)

Cash flow from financing

activity

8525 (89,649) (5479) (81124) (84170) (165294)

Operating activities: Operating activities are those activities that can be performed in day to day

activities. It includes the activity of marketing, distributing, and manufacturing that can be

performed in Nufarm Company. From the above table it can observed that the amount received

from the operating activities is $ 55,443 in 2017 and in 2016 it is $137375 and in 2015 it is

$228510 which denotes that in current year the Nufarm does not operate more activities as

compared to the previous year.

Investing activities: In this activity the company purchase and sell the assets to invest more for

their company. From the above table it can observed that cash flow from operating activities is

(100,758) in 2017 and in 2016 it is (138210) and in 2015 it is (104099) which denotes that in

2017 they make less payments for the purchase of tangible and intangible assets(Watson, 2018).

Financing activities: It includes those activities which are related to the finace such as issuing

shares and debentures, repaying loans etc. The above table shows the amount of finace activities

in 2017 it is (5479) and in 2016 it is $(89649) and in 2015 it is $8525 this all amount denotes that

in 2017 they Nufarm company finance less transactions as compared to the previous years and

they have to make less paymnets for that.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) What items have been reported in the other comprehensive income statement?

Comprehensive income is that income that can be bypass from the income statements, as the

items of these statements are not realised and they have the losses and gains that can be available

from the foreign currency and sale of securities. The Nufarm Company has divided

comprehensive income in to two parts that is certain items that are reclassified in to profit and

loss account and other items which are not reclassified to profit and loss account. It includes the

foreign exchange translation and their differences to the operations of foreign. It also includes

the value of cash flow hedges and value of net investment hedges. Amount not reclassified to the

profit and loss account that is Actuarial gains on the benefit plans and income tax on the payment

transactions.

8

(iii) What items have been reported in the other comprehensive income statement?

Comprehensive income is that income that can be bypass from the income statements, as the

items of these statements are not realised and they have the losses and gains that can be available

from the foreign currency and sale of securities. The Nufarm Company has divided

comprehensive income in to two parts that is certain items that are reclassified in to profit and

loss account and other items which are not reclassified to profit and loss account. It includes the

foreign exchange translation and their differences to the operations of foreign. It also includes

the value of cash flow hedges and value of net investment hedges. Amount not reclassified to the

profit and loss account that is Actuarial gains on the benefit plans and income tax on the payment

transactions.

8

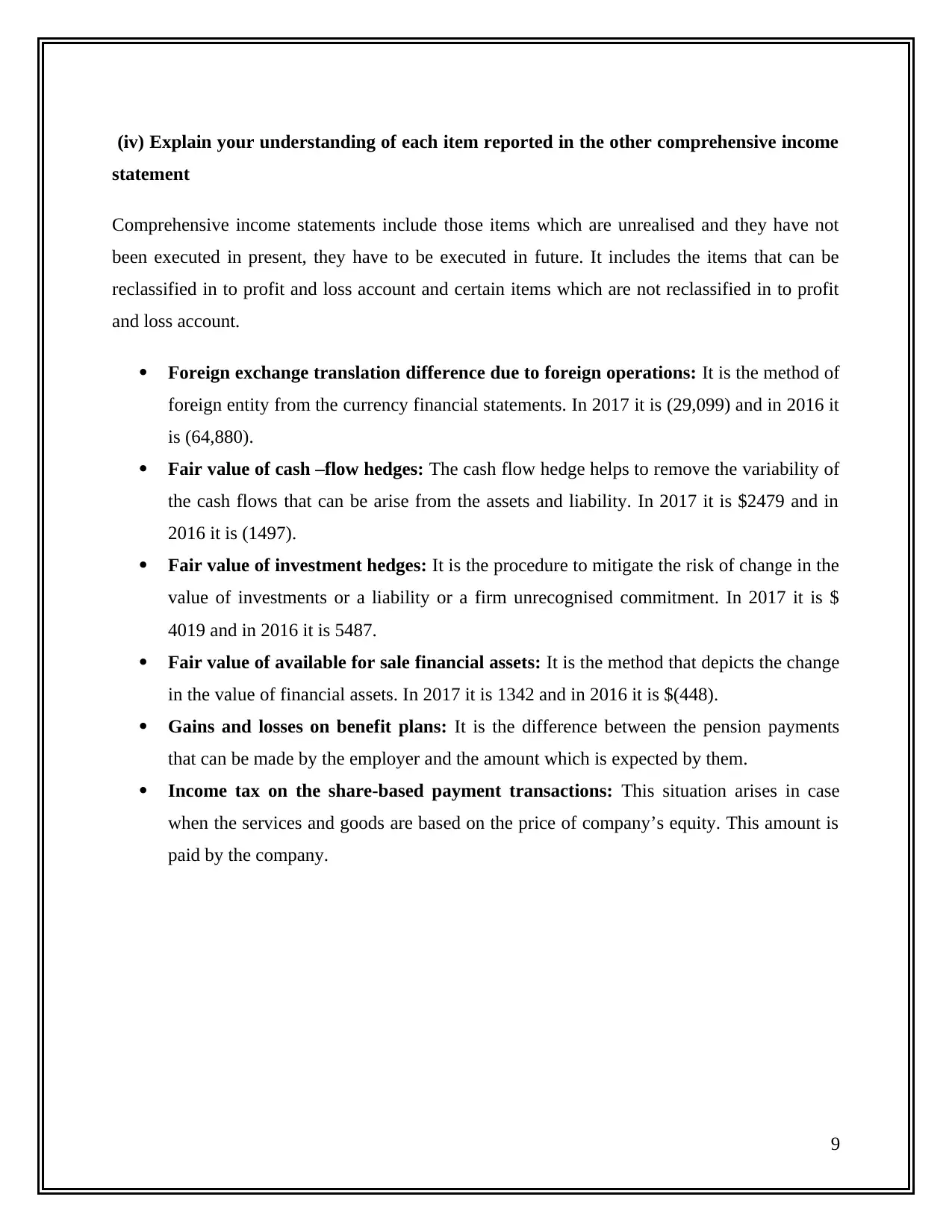

(iv) Explain your understanding of each item reported in the other comprehensive income

statement

Comprehensive income statements include those items which are unrealised and they have not

been executed in present, they have to be executed in future. It includes the items that can be

reclassified in to profit and loss account and certain items which are not reclassified in to profit

and loss account.

Foreign exchange translation difference due to foreign operations: It is the method of

foreign entity from the currency financial statements. In 2017 it is (29,099) and in 2016 it

is (64,880).

Fair value of cash –flow hedges: The cash flow hedge helps to remove the variability of

the cash flows that can be arise from the assets and liability. In 2017 it is $2479 and in

2016 it is (1497).

Fair value of investment hedges: It is the procedure to mitigate the risk of change in the

value of investments or a liability or a firm unrecognised commitment. In 2017 it is $

4019 and in 2016 it is 5487.

Fair value of available for sale financial assets: It is the method that depicts the change

in the value of financial assets. In 2017 it is 1342 and in 2016 it is $(448).

Gains and losses on benefit plans: It is the difference between the pension payments

that can be made by the employer and the amount which is expected by them.

Income tax on the share-based payment transactions: This situation arises in case

when the services and goods are based on the price of company’s equity. This amount is

paid by the company.

9

statement

Comprehensive income statements include those items which are unrealised and they have not

been executed in present, they have to be executed in future. It includes the items that can be

reclassified in to profit and loss account and certain items which are not reclassified in to profit

and loss account.

Foreign exchange translation difference due to foreign operations: It is the method of

foreign entity from the currency financial statements. In 2017 it is (29,099) and in 2016 it

is (64,880).

Fair value of cash –flow hedges: The cash flow hedge helps to remove the variability of

the cash flows that can be arise from the assets and liability. In 2017 it is $2479 and in

2016 it is (1497).

Fair value of investment hedges: It is the procedure to mitigate the risk of change in the

value of investments or a liability or a firm unrecognised commitment. In 2017 it is $

4019 and in 2016 it is 5487.

Fair value of available for sale financial assets: It is the method that depicts the change

in the value of financial assets. In 2017 it is 1342 and in 2016 it is $(448).

Gains and losses on benefit plans: It is the difference between the pension payments

that can be made by the employer and the amount which is expected by them.

Income tax on the share-based payment transactions: This situation arises in case

when the services and goods are based on the price of company’s equity. This amount is

paid by the company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(v) Why these items have not been reported in Income Statement/Profit and Loss

Statement

It can be stated that the income statements consists the realised items and the comprehensive

income statements includes the unrealised items that can be executed in future. The profit and

loss account and income statements includes all the expenditure and incomes and on the

comprehensive statements includes the losses and gains that can be arise due to the foreign

currency, hedging business, pension plans and fair value of tangible and intangible assets.

It can be observed that these items are not recorded under the profit and loss account as they are

not realized and they are recorded below the profit and loss account so that stakeholder or

shareholder can determine the amount of equity(Cuccia, 2018).

10

Statement

It can be stated that the income statements consists the realised items and the comprehensive

income statements includes the unrealised items that can be executed in future. The profit and

loss account and income statements includes all the expenditure and incomes and on the

comprehensive statements includes the losses and gains that can be arise due to the foreign

currency, hedging business, pension plans and fair value of tangible and intangible assets.

It can be observed that these items are not recorded under the profit and loss account as they are

not realized and they are recorded below the profit and loss account so that stakeholder or

shareholder can determine the amount of equity(Cuccia, 2018).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR CORPORATE INCOME TAX

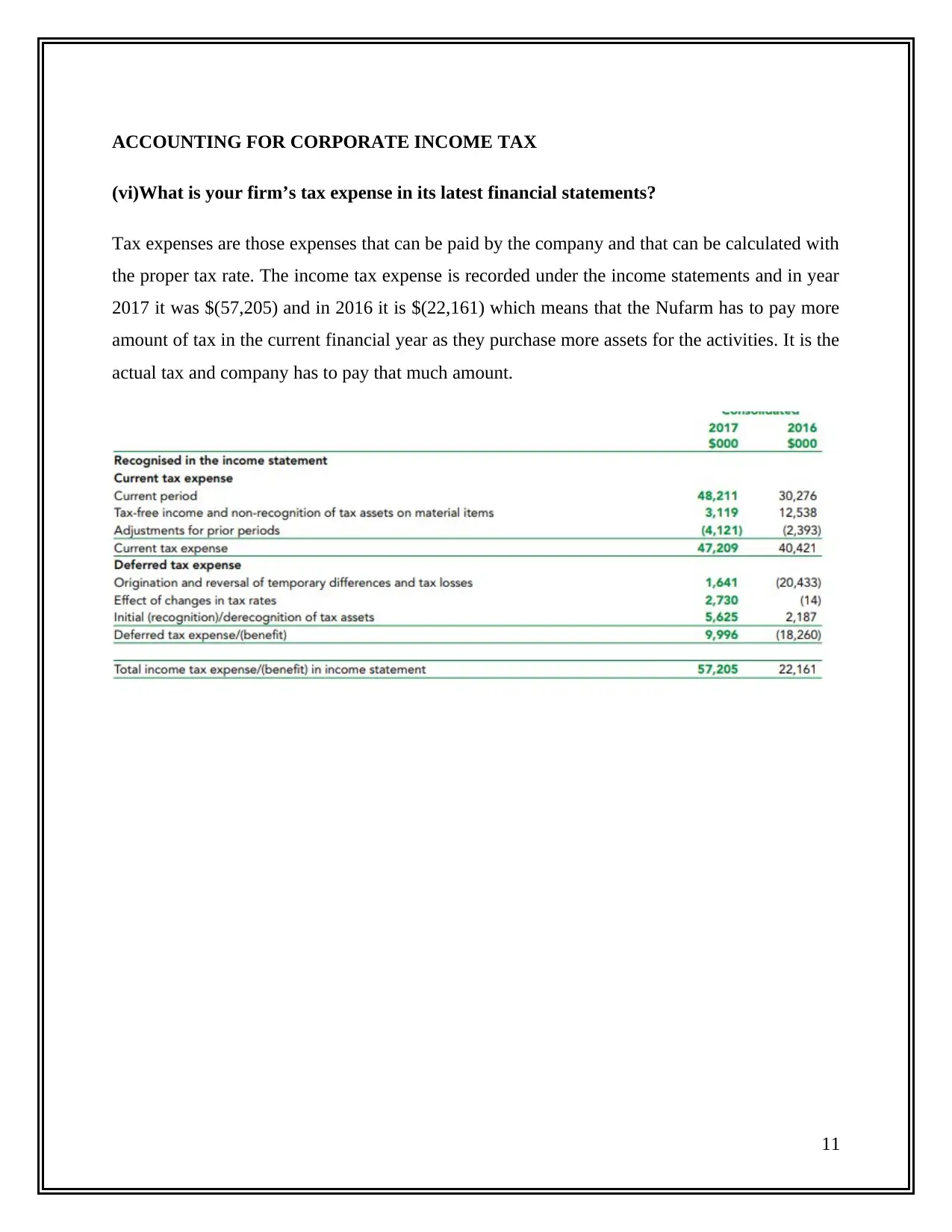

(vi)What is your firm’s tax expense in its latest financial statements?

Tax expenses are those expenses that can be paid by the company and that can be calculated with

the proper tax rate. The income tax expense is recorded under the income statements and in year

2017 it was $(57,205) and in 2016 it is $(22,161) which means that the Nufarm has to pay more

amount of tax in the current financial year as they purchase more assets for the activities. It is the

actual tax and company has to pay that much amount.

11

(vi)What is your firm’s tax expense in its latest financial statements?

Tax expenses are those expenses that can be paid by the company and that can be calculated with

the proper tax rate. The income tax expense is recorded under the income statements and in year

2017 it was $(57,205) and in 2016 it is $(22,161) which means that the Nufarm has to pay more

amount of tax in the current financial year as they purchase more assets for the activities. It is the

actual tax and company has to pay that much amount.

11

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

From the financial statements of Nufarm Company, it can be analyse that the amount of tax

expense is not similar to the profit of the company. The income tax rate is 30% and it is based on

the Australian tax laws. It can be stated that the tax expense does not consist the income or

losses, amortisation and depreciation. But to calculate the company has to consider these all

items (Annual report, 2017).

12

Explain why this is, or is not, the case for your firm.

From the financial statements of Nufarm Company, it can be analyse that the amount of tax

expense is not similar to the profit of the company. The income tax rate is 30% and it is based on

the Australian tax laws. It can be stated that the tax expense does not consist the income or

losses, amortisation and depreciation. But to calculate the company has to consider these all

items (Annual report, 2017).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.