Financial Statement Overstatement: An Auditing Report on Woolworths

VerifiedAdded on 2021/02/20

|6

|587

|65

Report

AI Summary

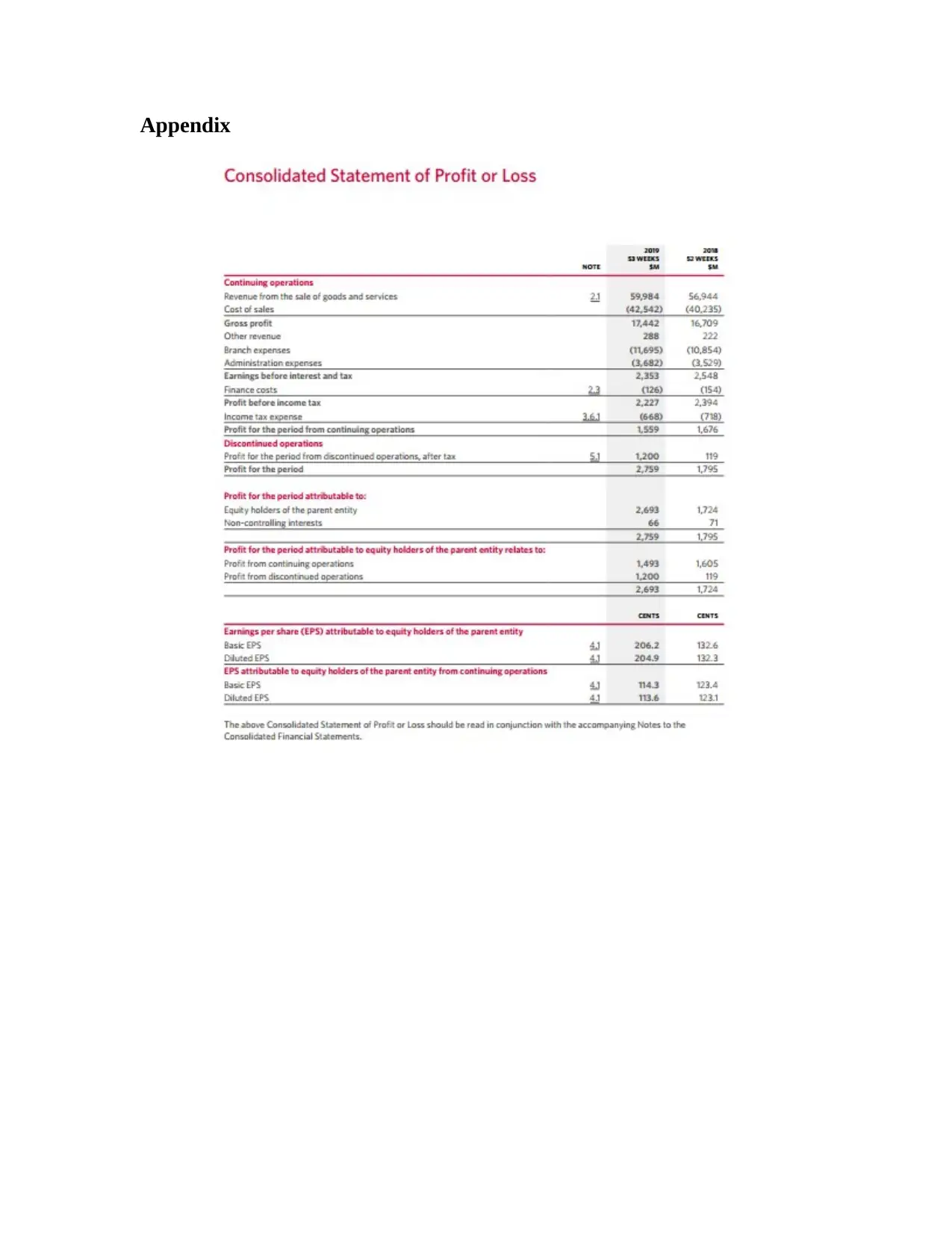

This report examines the overstatement of financial statements, specifically focusing on a case study involving Woolworths. The analysis delves into the misstatement of income and expenses, highlighting how the company overstated both revenues and expenses by equal amounts, ultimately nullifying the net effect on profits. The auditor identified that personal expenses were improperly included in branch expenses, and the company overstated revenues from other sources to offset these expenses. The report discusses the auditor's findings, the materiality of the misstatement, and the implications for the audit opinion. The auditor is expected to give an adverse opinion on the overstatement of revenues and expenses. The report also touches upon the relevant auditing standards (ASA 705) and the potential consequences of these misstatements, including the influence on investor decisions and potential scrutiny from tax authorities. The conclusion emphasizes the auditor's duty to provide an opinion based on the findings and not to seek personal interest by giving unqualified opinion on misstated financial statements.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.