Accounting Report: Financial Statement Preparation and Analysis

VerifiedAdded on 2023/06/04

|11

|2404

|363

Report

AI Summary

This report details the step-by-step preparation of financial statements for Mr. Paul, starting with the initial trial balance and progressing through adjustment and closing entries. It includes a detailed analysis of the trial balance, adjusted trial balance, profit and loss account, statement of changes in equity, and the balance sheet. The report also addresses key accounting concepts such as the purpose of a trial balance, the importance of adjustment journal entries, and the differences between adjustment and closing entries. The analysis reveals that Mr. Paul's business is profitable, with a net profit of $86,757.5, and showcases the increase in his capital due to the business's profitability. The adjusted trial balance confirms the accuracy and balance of the accounts, ensuring a reliable foundation for the financial statements.

BUSINESS ACCOUNTING

EXECUTIVE SUMMARY

The report has been prepared with an intention to detail out various steps involved in the

preparation of Financial Statement of Mr. Paul. The report consist of 7 steps and has been

presented here-in-below:

EXECUTIVE SUMMARY

The report has been prepared with an intention to detail out various steps involved in the

preparation of Financial Statement of Mr. Paul. The report consist of 7 steps and has been

presented here-in-below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step -1

The same has been carried out and the question has been allotted. The question that has been

allocated on the basis of above has been detailed here-in-below:

Trial Balance of Paul

For June ended, 2016

Account No Account Name Debit Credit

101 Cash at Bank 55120

105 Accounts Receivable 18370

115 Supplies 1550

120 Prepaid Insurance 3100

135 Office Furniture 38800

137 Acc. Depreciation. - Furniture 0

140 Office Equipment 77600

141 Acc. Depreciation - Equipment 0

145 Store Equipment 116400

146 Acc. Depreciation - Equipment 0

170 Automobile 155200

171 Acc. Depreciation - Automobile 0

201 Accounts Payable 36740

201 Interest Payable 55110

201 Unearned revenue 19400

201 Loan Payable 7760

201 Mortgage Payable 155200

201 Paul's Capital 49865

201 Paul's Drawings 155

201 Revenue 155000

201 Advertising Expense 1100

201 Automobile Expense 5775

201 Depreciation Expense - Furniture

201 Depreciation Expense - Equipment

201 Depreciation Expense - Store Equipment

201 Depreciation Expense - Automobile

201 Insurance Expense 900

201 Maintenance Expense 3850

201 Miscellaneous Expense 1155

201 Rent Expense

201 Supplies Expense

201 Utilities Expense

201 Interest Expense

479075 479075

The same has been carried out and the question has been allotted. The question that has been

allocated on the basis of above has been detailed here-in-below:

Trial Balance of Paul

For June ended, 2016

Account No Account Name Debit Credit

101 Cash at Bank 55120

105 Accounts Receivable 18370

115 Supplies 1550

120 Prepaid Insurance 3100

135 Office Furniture 38800

137 Acc. Depreciation. - Furniture 0

140 Office Equipment 77600

141 Acc. Depreciation - Equipment 0

145 Store Equipment 116400

146 Acc. Depreciation - Equipment 0

170 Automobile 155200

171 Acc. Depreciation - Automobile 0

201 Accounts Payable 36740

201 Interest Payable 55110

201 Unearned revenue 19400

201 Loan Payable 7760

201 Mortgage Payable 155200

201 Paul's Capital 49865

201 Paul's Drawings 155

201 Revenue 155000

201 Advertising Expense 1100

201 Automobile Expense 5775

201 Depreciation Expense - Furniture

201 Depreciation Expense - Equipment

201 Depreciation Expense - Store Equipment

201 Depreciation Expense - Automobile

201 Insurance Expense 900

201 Maintenance Expense 3850

201 Miscellaneous Expense 1155

201 Rent Expense

201 Supplies Expense

201 Utilities Expense

201 Interest Expense

479075 479075

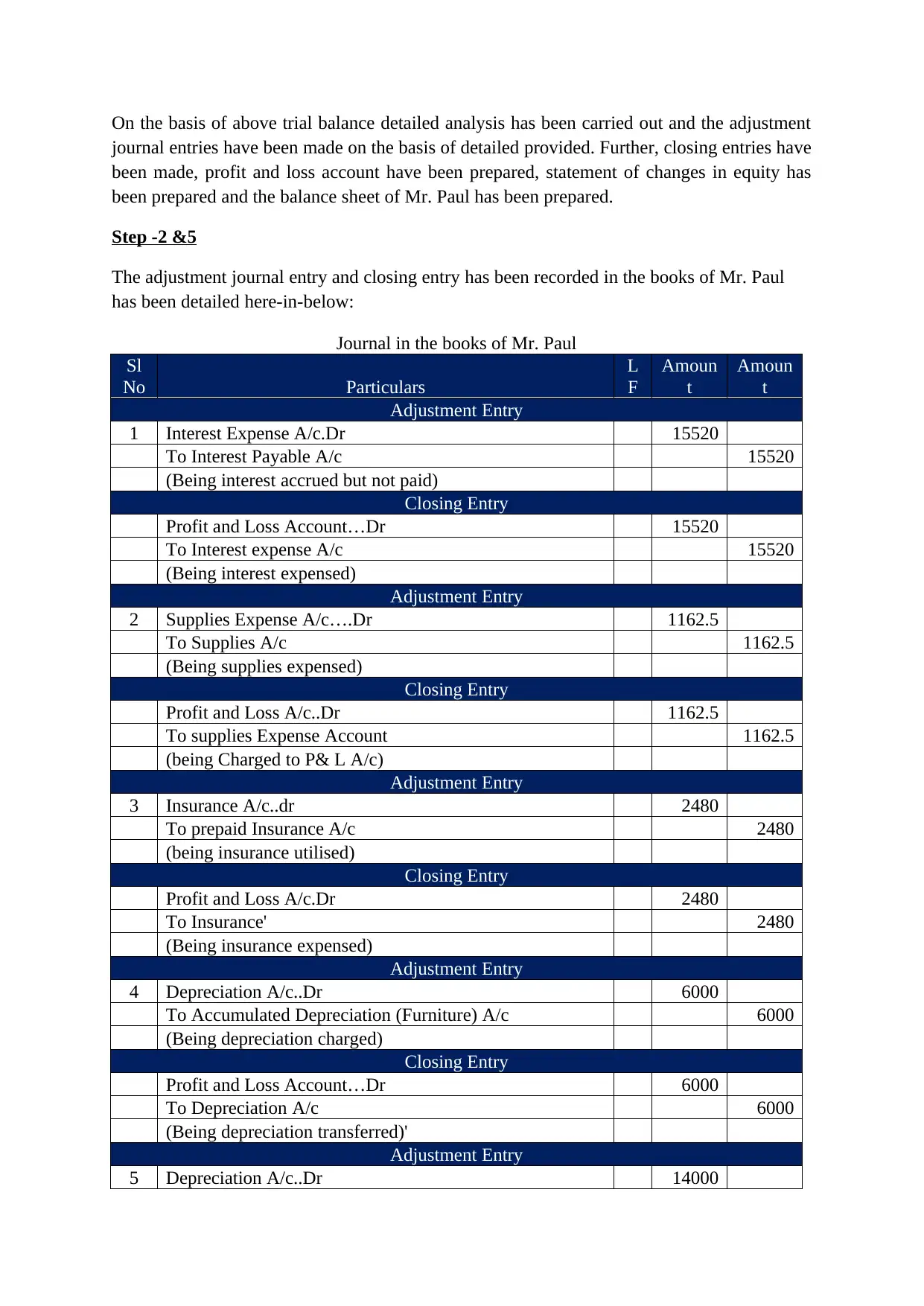

On the basis of above trial balance detailed analysis has been carried out and the adjustment

journal entries have been made on the basis of detailed provided. Further, closing entries have

been made, profit and loss account have been prepared, statement of changes in equity has

been prepared and the balance sheet of Mr. Paul has been prepared.

Step -2 &5

The adjustment journal entry and closing entry has been recorded in the books of Mr. Paul

has been detailed here-in-below:

Journal in the books of Mr. Paul

Sl

No Particulars

L

F

Amoun

t

Amoun

t

Adjustment Entry

1 Interest Expense A/c.Dr 15520

To Interest Payable A/c 15520

(Being interest accrued but not paid)

Closing Entry

Profit and Loss Account…Dr 15520

To Interest expense A/c 15520

(Being interest expensed)

Adjustment Entry

2 Supplies Expense A/c….Dr 1162.5

To Supplies A/c 1162.5

(Being supplies expensed)

Closing Entry

Profit and Loss A/c..Dr 1162.5

To supplies Expense Account 1162.5

(being Charged to P& L A/c)

Adjustment Entry

3 Insurance A/c..dr 2480

To prepaid Insurance A/c 2480

(being insurance utilised)

Closing Entry

Profit and Loss A/c.Dr 2480

To Insurance' 2480

(Being insurance expensed)

Adjustment Entry

4 Depreciation A/c..Dr 6000

To Accumulated Depreciation (Furniture) A/c 6000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 6000

To Depreciation A/c 6000

(Being depreciation transferred)'

Adjustment Entry

5 Depreciation A/c..Dr 14000

journal entries have been made on the basis of detailed provided. Further, closing entries have

been made, profit and loss account have been prepared, statement of changes in equity has

been prepared and the balance sheet of Mr. Paul has been prepared.

Step -2 &5

The adjustment journal entry and closing entry has been recorded in the books of Mr. Paul

has been detailed here-in-below:

Journal in the books of Mr. Paul

Sl

No Particulars

L

F

Amoun

t

Amoun

t

Adjustment Entry

1 Interest Expense A/c.Dr 15520

To Interest Payable A/c 15520

(Being interest accrued but not paid)

Closing Entry

Profit and Loss Account…Dr 15520

To Interest expense A/c 15520

(Being interest expensed)

Adjustment Entry

2 Supplies Expense A/c….Dr 1162.5

To Supplies A/c 1162.5

(Being supplies expensed)

Closing Entry

Profit and Loss A/c..Dr 1162.5

To supplies Expense Account 1162.5

(being Charged to P& L A/c)

Adjustment Entry

3 Insurance A/c..dr 2480

To prepaid Insurance A/c 2480

(being insurance utilised)

Closing Entry

Profit and Loss A/c.Dr 2480

To Insurance' 2480

(Being insurance expensed)

Adjustment Entry

4 Depreciation A/c..Dr 6000

To Accumulated Depreciation (Furniture) A/c 6000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 6000

To Depreciation A/c 6000

(Being depreciation transferred)'

Adjustment Entry

5 Depreciation A/c..Dr 14000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

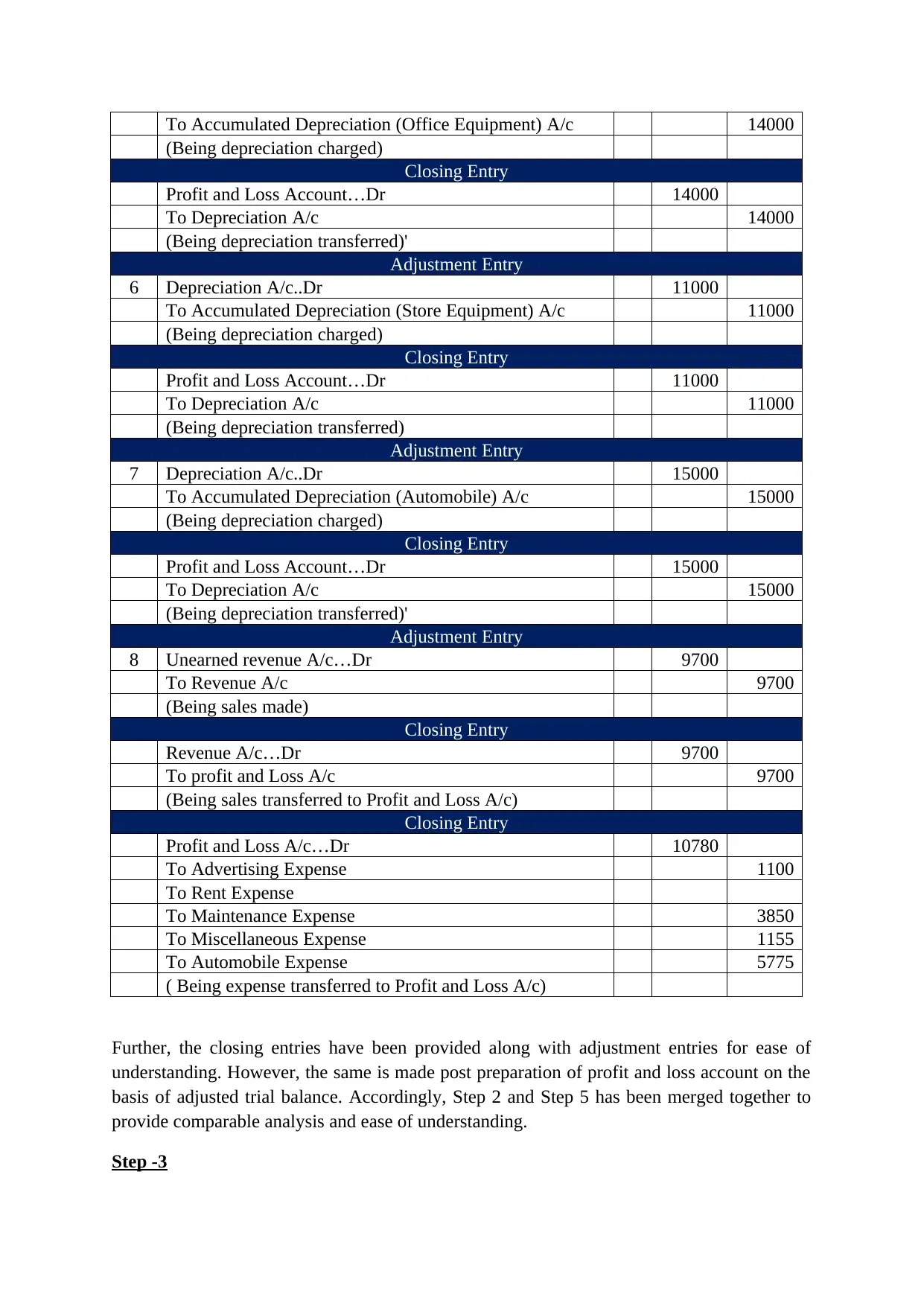

To Accumulated Depreciation (Office Equipment) A/c 14000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 14000

To Depreciation A/c 14000

(Being depreciation transferred)'

Adjustment Entry

6 Depreciation A/c..Dr 11000

To Accumulated Depreciation (Store Equipment) A/c 11000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 11000

To Depreciation A/c 11000

(Being depreciation transferred)

Adjustment Entry

7 Depreciation A/c..Dr 15000

To Accumulated Depreciation (Automobile) A/c 15000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 15000

To Depreciation A/c 15000

(Being depreciation transferred)'

Adjustment Entry

8 Unearned revenue A/c…Dr 9700

To Revenue A/c 9700

(Being sales made)

Closing Entry

Revenue A/c…Dr 9700

To profit and Loss A/c 9700

(Being sales transferred to Profit and Loss A/c)

Closing Entry

Profit and Loss A/c…Dr 10780

To Advertising Expense 1100

To Rent Expense

To Maintenance Expense 3850

To Miscellaneous Expense 1155

To Automobile Expense 5775

( Being expense transferred to Profit and Loss A/c)

Further, the closing entries have been provided along with adjustment entries for ease of

understanding. However, the same is made post preparation of profit and loss account on the

basis of adjusted trial balance. Accordingly, Step 2 and Step 5 has been merged together to

provide comparable analysis and ease of understanding.

Step -3

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 14000

To Depreciation A/c 14000

(Being depreciation transferred)'

Adjustment Entry

6 Depreciation A/c..Dr 11000

To Accumulated Depreciation (Store Equipment) A/c 11000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 11000

To Depreciation A/c 11000

(Being depreciation transferred)

Adjustment Entry

7 Depreciation A/c..Dr 15000

To Accumulated Depreciation (Automobile) A/c 15000

(Being depreciation charged)

Closing Entry

Profit and Loss Account…Dr 15000

To Depreciation A/c 15000

(Being depreciation transferred)'

Adjustment Entry

8 Unearned revenue A/c…Dr 9700

To Revenue A/c 9700

(Being sales made)

Closing Entry

Revenue A/c…Dr 9700

To profit and Loss A/c 9700

(Being sales transferred to Profit and Loss A/c)

Closing Entry

Profit and Loss A/c…Dr 10780

To Advertising Expense 1100

To Rent Expense

To Maintenance Expense 3850

To Miscellaneous Expense 1155

To Automobile Expense 5775

( Being expense transferred to Profit and Loss A/c)

Further, the closing entries have been provided along with adjustment entries for ease of

understanding. However, the same is made post preparation of profit and loss account on the

basis of adjusted trial balance. Accordingly, Step 2 and Step 5 has been merged together to

provide comparable analysis and ease of understanding.

Step -3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

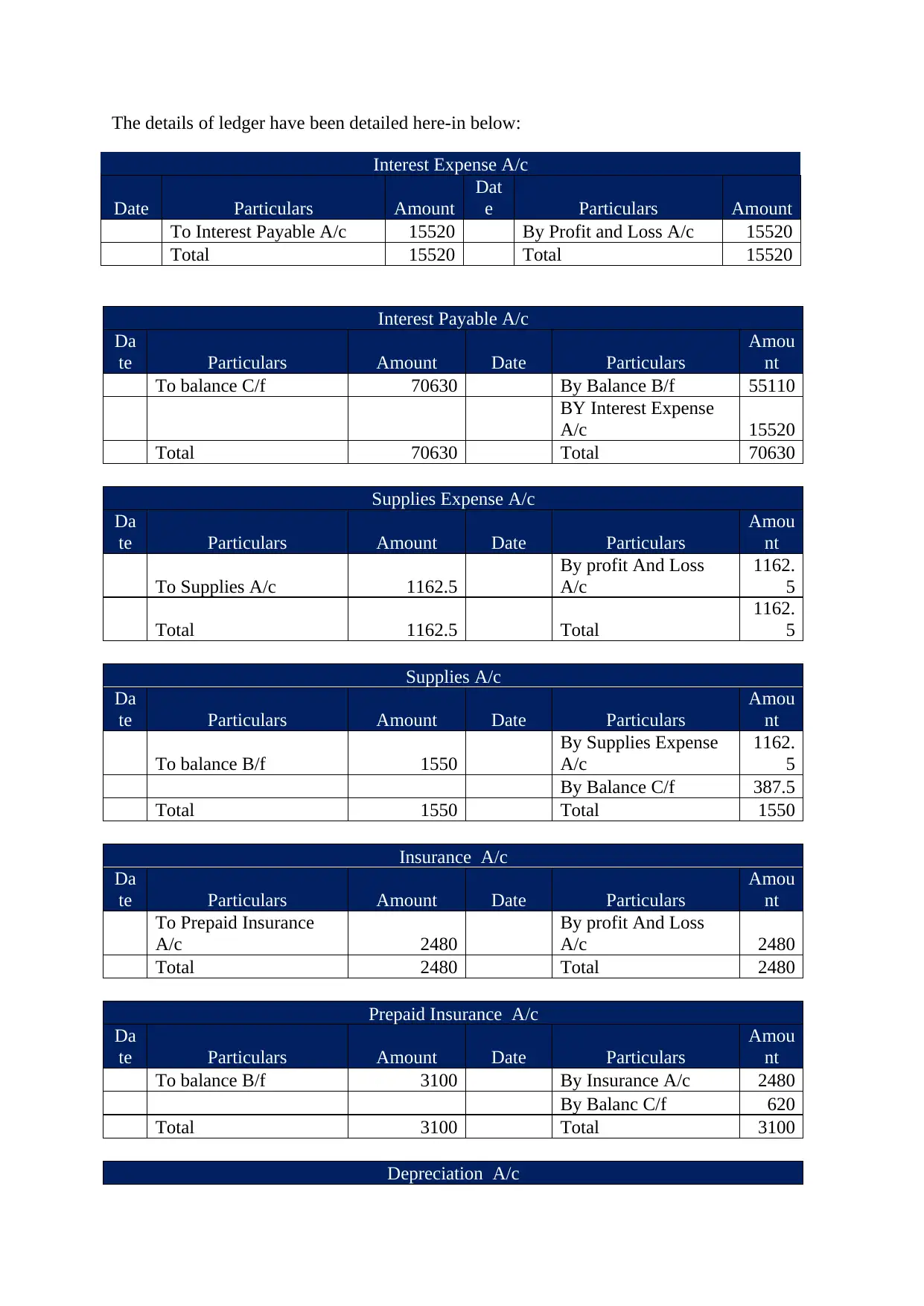

The details of ledger have been detailed here-in below:

Interest Expense A/c

Date Particulars Amount

Dat

e Particulars Amount

To Interest Payable A/c 15520 By Profit and Loss A/c 15520

Total 15520 Total 15520

Interest Payable A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance C/f 70630 By Balance B/f 55110

BY Interest Expense

A/c 15520

Total 70630 Total 70630

Supplies Expense A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To Supplies A/c 1162.5

By profit And Loss

A/c

1162.

5

Total 1162.5 Total

1162.

5

Supplies A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance B/f 1550

By Supplies Expense

A/c

1162.

5

By Balance C/f 387.5

Total 1550 Total 1550

Insurance A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To Prepaid Insurance

A/c 2480

By profit And Loss

A/c 2480

Total 2480 Total 2480

Prepaid Insurance A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance B/f 3100 By Insurance A/c 2480

By Balanc C/f 620

Total 3100 Total 3100

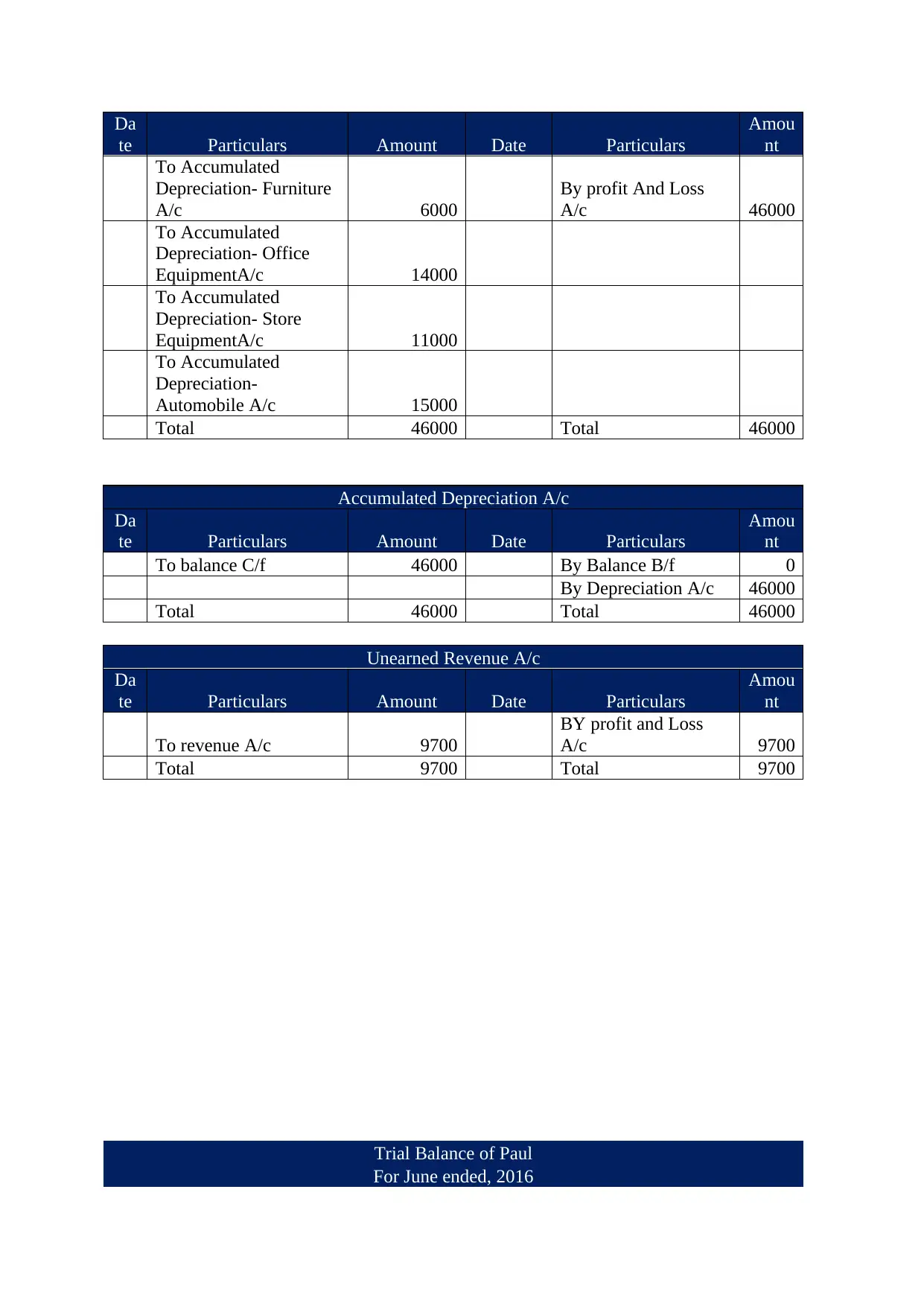

Depreciation A/c

Interest Expense A/c

Date Particulars Amount

Dat

e Particulars Amount

To Interest Payable A/c 15520 By Profit and Loss A/c 15520

Total 15520 Total 15520

Interest Payable A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance C/f 70630 By Balance B/f 55110

BY Interest Expense

A/c 15520

Total 70630 Total 70630

Supplies Expense A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To Supplies A/c 1162.5

By profit And Loss

A/c

1162.

5

Total 1162.5 Total

1162.

5

Supplies A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance B/f 1550

By Supplies Expense

A/c

1162.

5

By Balance C/f 387.5

Total 1550 Total 1550

Insurance A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To Prepaid Insurance

A/c 2480

By profit And Loss

A/c 2480

Total 2480 Total 2480

Prepaid Insurance A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance B/f 3100 By Insurance A/c 2480

By Balanc C/f 620

Total 3100 Total 3100

Depreciation A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To Accumulated

Depreciation- Furniture

A/c 6000

By profit And Loss

A/c 46000

To Accumulated

Depreciation- Office

EquipmentA/c 14000

To Accumulated

Depreciation- Store

EquipmentA/c 11000

To Accumulated

Depreciation-

Automobile A/c 15000

Total 46000 Total 46000

Accumulated Depreciation A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance C/f 46000 By Balance B/f 0

By Depreciation A/c 46000

Total 46000 Total 46000

Unearned Revenue A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To revenue A/c 9700

BY profit and Loss

A/c 9700

Total 9700 Total 9700

Trial Balance of Paul

For June ended, 2016

te Particulars Amount Date Particulars

Amou

nt

To Accumulated

Depreciation- Furniture

A/c 6000

By profit And Loss

A/c 46000

To Accumulated

Depreciation- Office

EquipmentA/c 14000

To Accumulated

Depreciation- Store

EquipmentA/c 11000

To Accumulated

Depreciation-

Automobile A/c 15000

Total 46000 Total 46000

Accumulated Depreciation A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To balance C/f 46000 By Balance B/f 0

By Depreciation A/c 46000

Total 46000 Total 46000

Unearned Revenue A/c

Da

te Particulars Amount Date Particulars

Amou

nt

To revenue A/c 9700

BY profit and Loss

A/c 9700

Total 9700 Total 9700

Trial Balance of Paul

For June ended, 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

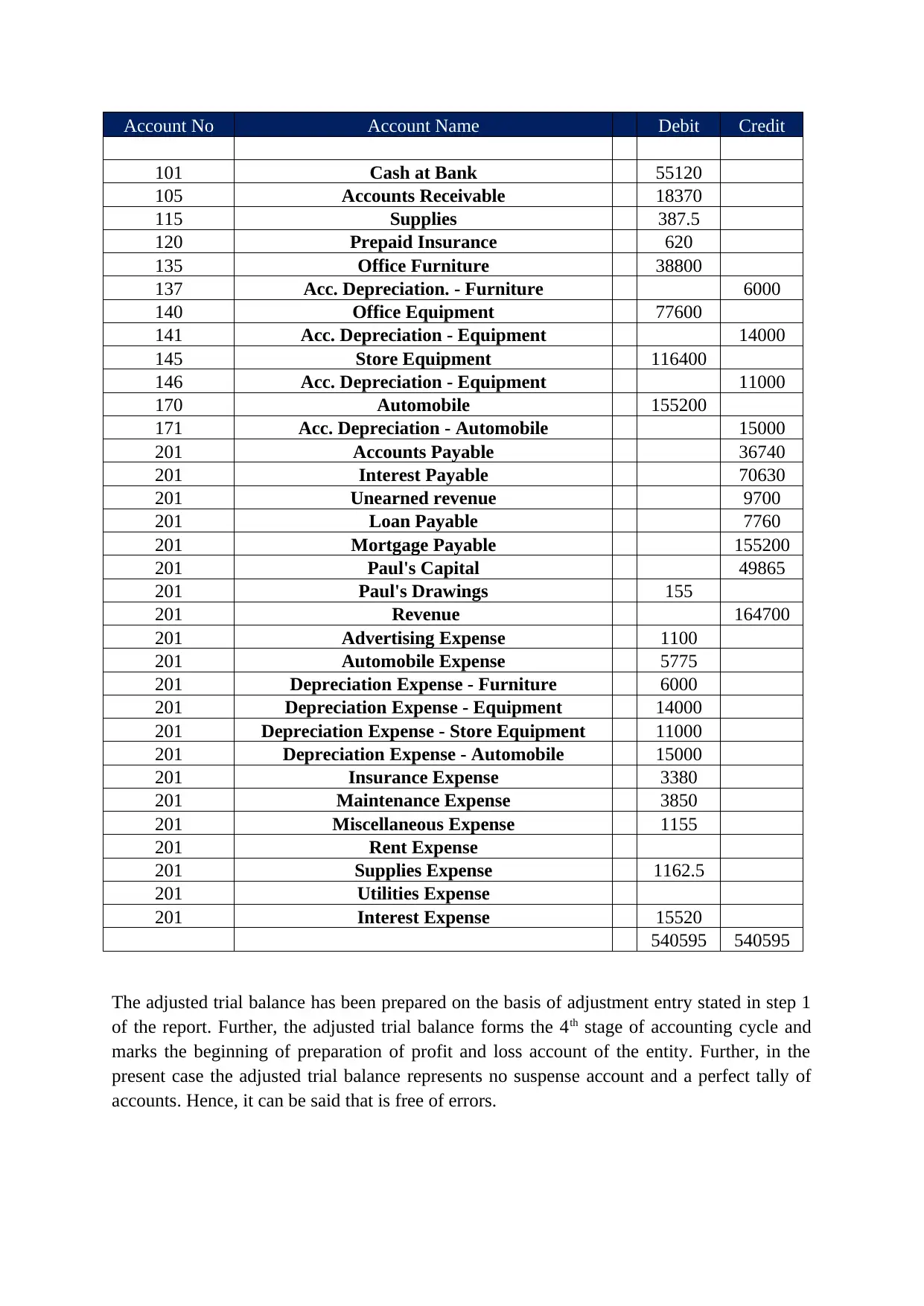

Account No Account Name Debit Credit

101 Cash at Bank 55120

105 Accounts Receivable 18370

115 Supplies 387.5

120 Prepaid Insurance 620

135 Office Furniture 38800

137 Acc. Depreciation. - Furniture 6000

140 Office Equipment 77600

141 Acc. Depreciation - Equipment 14000

145 Store Equipment 116400

146 Acc. Depreciation - Equipment 11000

170 Automobile 155200

171 Acc. Depreciation - Automobile 15000

201 Accounts Payable 36740

201 Interest Payable 70630

201 Unearned revenue 9700

201 Loan Payable 7760

201 Mortgage Payable 155200

201 Paul's Capital 49865

201 Paul's Drawings 155

201 Revenue 164700

201 Advertising Expense 1100

201 Automobile Expense 5775

201 Depreciation Expense - Furniture 6000

201 Depreciation Expense - Equipment 14000

201 Depreciation Expense - Store Equipment 11000

201 Depreciation Expense - Automobile 15000

201 Insurance Expense 3380

201 Maintenance Expense 3850

201 Miscellaneous Expense 1155

201 Rent Expense

201 Supplies Expense 1162.5

201 Utilities Expense

201 Interest Expense 15520

540595 540595

The adjusted trial balance has been prepared on the basis of adjustment entry stated in step 1

of the report. Further, the adjusted trial balance forms the 4th stage of accounting cycle and

marks the beginning of preparation of profit and loss account of the entity. Further, in the

present case the adjusted trial balance represents no suspense account and a perfect tally of

accounts. Hence, it can be said that is free of errors.

101 Cash at Bank 55120

105 Accounts Receivable 18370

115 Supplies 387.5

120 Prepaid Insurance 620

135 Office Furniture 38800

137 Acc. Depreciation. - Furniture 6000

140 Office Equipment 77600

141 Acc. Depreciation - Equipment 14000

145 Store Equipment 116400

146 Acc. Depreciation - Equipment 11000

170 Automobile 155200

171 Acc. Depreciation - Automobile 15000

201 Accounts Payable 36740

201 Interest Payable 70630

201 Unearned revenue 9700

201 Loan Payable 7760

201 Mortgage Payable 155200

201 Paul's Capital 49865

201 Paul's Drawings 155

201 Revenue 164700

201 Advertising Expense 1100

201 Automobile Expense 5775

201 Depreciation Expense - Furniture 6000

201 Depreciation Expense - Equipment 14000

201 Depreciation Expense - Store Equipment 11000

201 Depreciation Expense - Automobile 15000

201 Insurance Expense 3380

201 Maintenance Expense 3850

201 Miscellaneous Expense 1155

201 Rent Expense

201 Supplies Expense 1162.5

201 Utilities Expense

201 Interest Expense 15520

540595 540595

The adjusted trial balance has been prepared on the basis of adjustment entry stated in step 1

of the report. Further, the adjusted trial balance forms the 4th stage of accounting cycle and

marks the beginning of preparation of profit and loss account of the entity. Further, in the

present case the adjusted trial balance represents no suspense account and a perfect tally of

accounts. Hence, it can be said that is free of errors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

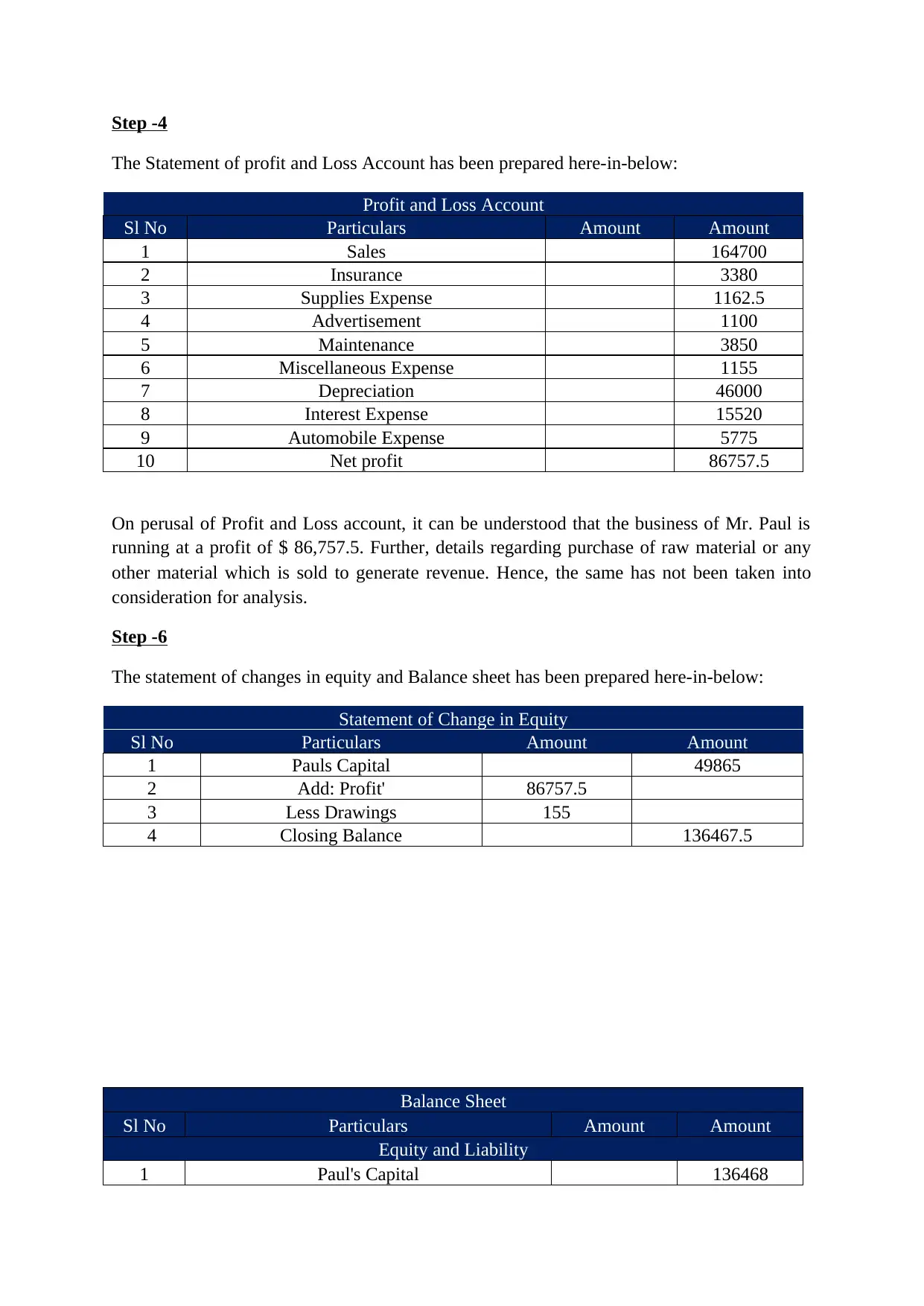

Step -4

The Statement of profit and Loss Account has been prepared here-in-below:

Profit and Loss Account

Sl No Particulars Amount Amount

1 Sales 164700

2 Insurance 3380

3 Supplies Expense 1162.5

4 Advertisement 1100

5 Maintenance 3850

6 Miscellaneous Expense 1155

7 Depreciation 46000

8 Interest Expense 15520

9 Automobile Expense 5775

10 Net profit 86757.5

On perusal of Profit and Loss account, it can be understood that the business of Mr. Paul is

running at a profit of $ 86,757.5. Further, details regarding purchase of raw material or any

other material which is sold to generate revenue. Hence, the same has not been taken into

consideration for analysis.

Step -6

The statement of changes in equity and Balance sheet has been prepared here-in-below:

Statement of Change in Equity

Sl No Particulars Amount Amount

1 Pauls Capital 49865

2 Add: Profit' 86757.5

3 Less Drawings 155

4 Closing Balance 136467.5

Balance Sheet

Sl No Particulars Amount Amount

Equity and Liability

1 Paul's Capital 136468

The Statement of profit and Loss Account has been prepared here-in-below:

Profit and Loss Account

Sl No Particulars Amount Amount

1 Sales 164700

2 Insurance 3380

3 Supplies Expense 1162.5

4 Advertisement 1100

5 Maintenance 3850

6 Miscellaneous Expense 1155

7 Depreciation 46000

8 Interest Expense 15520

9 Automobile Expense 5775

10 Net profit 86757.5

On perusal of Profit and Loss account, it can be understood that the business of Mr. Paul is

running at a profit of $ 86,757.5. Further, details regarding purchase of raw material or any

other material which is sold to generate revenue. Hence, the same has not been taken into

consideration for analysis.

Step -6

The statement of changes in equity and Balance sheet has been prepared here-in-below:

Statement of Change in Equity

Sl No Particulars Amount Amount

1 Pauls Capital 49865

2 Add: Profit' 86757.5

3 Less Drawings 155

4 Closing Balance 136467.5

Balance Sheet

Sl No Particulars Amount Amount

Equity and Liability

1 Paul's Capital 136468

2 Mortgage Payable 155200

3 Interest Payable 70630

4 Accounts Payable 36740

5 Unearned Revenue 9700

6 Loan Payable 7760

7 Accumulated Depreciation 46000

Total 462498

Asset

1 Cash at Bank 55120

2 Accounts Receivable 18370

3 Supplies 387.5

4 Prepaid Insurance A/c 620

5 Office Furniture 38800

6 Office Equipment 77600

7 Store Equipment 116400

8 Automobile 155200

Total 462498

On perusal of balance sheet of the company, one can understand that the capital of Mr. Paul

has increased over the period on account of profitability of business.

Step -7

Question -1

What is a trial balance and why do we create it?

Answer -1

It is a statement of ending balances of a company, individual etc. The trial balance is prepared

at the end of the reporting period to aid in preparation of Profit and Loss Accounts and

Balance Sheet. The ledger balances are segregated into debit and credit accounts with bot

side tallying. Further under trial balance on the debit side appears expense and asset while on

the credit side both liability and income shall appear.(Accounting-Simplified.com, 2017)

The purpose of creation of Trial Balance has been summarised here-in-below:

(a) It assists in the preparation of financial statement and marks the inception towards the

same;

(b) Identification and Rectification of errors while journalising and posting;

(c) Ensuring correct and accurate Financial Statement;

Question -2

What are adjustment journal entries? Why do we record the adjustment journal entries?

3 Interest Payable 70630

4 Accounts Payable 36740

5 Unearned Revenue 9700

6 Loan Payable 7760

7 Accumulated Depreciation 46000

Total 462498

Asset

1 Cash at Bank 55120

2 Accounts Receivable 18370

3 Supplies 387.5

4 Prepaid Insurance A/c 620

5 Office Furniture 38800

6 Office Equipment 77600

7 Store Equipment 116400

8 Automobile 155200

Total 462498

On perusal of balance sheet of the company, one can understand that the capital of Mr. Paul

has increased over the period on account of profitability of business.

Step -7

Question -1

What is a trial balance and why do we create it?

Answer -1

It is a statement of ending balances of a company, individual etc. The trial balance is prepared

at the end of the reporting period to aid in preparation of Profit and Loss Accounts and

Balance Sheet. The ledger balances are segregated into debit and credit accounts with bot

side tallying. Further under trial balance on the debit side appears expense and asset while on

the credit side both liability and income shall appear.(Accounting-Simplified.com, 2017)

The purpose of creation of Trial Balance has been summarised here-in-below:

(a) It assists in the preparation of financial statement and marks the inception towards the

same;

(b) Identification and Rectification of errors while journalising and posting;

(c) Ensuring correct and accurate Financial Statement;

Question -2

What are adjustment journal entries? Why do we record the adjustment journal entries?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer -2

Adjustment Journal entries are generally done in the books of accounts at the end of financial

year. The intention of such entry at the end of the period is to allocate income and expense of

a particular period to that reporting period based on matching principle and accrual basis.

(Shultz, 2018)

The intention of adjustment journal entry is detailed here-in-below:

(a) It ensures allocation of prepaid expenditure to the period it is incurred;

(b) Revenue which are unearned are to allocated in the year in which it is realised.

(c) Expenses which are accrued are to be allocated in the year in which it is spend.

(d) Revenue earned but not realised during the current year.

(e) Rectification of errors;

(f) Omission of entries etc.

(g) To allign with the concept of accrual the adjusting journal entries are passed

(h) It is a way to ensure that all the revenue and expenses are properly recorded in the

books of accounts.

(i) A company cannot record few of its income earned at the mid of the year but will

record the same at the end of the year by doing adjustment for the same.

Question -3

What is the purpose of writing an adjusted trial balance?

Answer-3

The motive behind preparation of adjusted trial balance has been detailed here-in-below:

(a) It is the last step in the accounting cycle before preparation of financial statement;

(b) It aids in preparation of financial statement;(MyAccountingCourse.com, 2018)

(c) It helps in presenting true and accurate figure;

(d) It assists in correct revenue recognition;

(e) It is in alignment with accounting principles;

(f) It eases the preparation of financial statement;

(g) It is also prepared to confirm that all the ledger accounts are properly balanced.

(h) All the end balances of the ledger is shown..

(i) The sum total of debit should match with the credit total.

Question -4

How adjustment journal entries are different from the closing entries?

Answer-4

Adjustment Journal entries are generally done in the books of accounts at the end of financial

year. The intention of such entry at the end of the period is to allocate income and expense of

a particular period to that reporting period based on matching principle and accrual basis.

(Shultz, 2018)

The intention of adjustment journal entry is detailed here-in-below:

(a) It ensures allocation of prepaid expenditure to the period it is incurred;

(b) Revenue which are unearned are to allocated in the year in which it is realised.

(c) Expenses which are accrued are to be allocated in the year in which it is spend.

(d) Revenue earned but not realised during the current year.

(e) Rectification of errors;

(f) Omission of entries etc.

(g) To allign with the concept of accrual the adjusting journal entries are passed

(h) It is a way to ensure that all the revenue and expenses are properly recorded in the

books of accounts.

(i) A company cannot record few of its income earned at the mid of the year but will

record the same at the end of the year by doing adjustment for the same.

Question -3

What is the purpose of writing an adjusted trial balance?

Answer-3

The motive behind preparation of adjusted trial balance has been detailed here-in-below:

(a) It is the last step in the accounting cycle before preparation of financial statement;

(b) It aids in preparation of financial statement;(MyAccountingCourse.com, 2018)

(c) It helps in presenting true and accurate figure;

(d) It assists in correct revenue recognition;

(e) It is in alignment with accounting principles;

(f) It eases the preparation of financial statement;

(g) It is also prepared to confirm that all the ledger accounts are properly balanced.

(h) All the end balances of the ledger is shown..

(i) The sum total of debit should match with the credit total.

Question -4

How adjustment journal entries are different from the closing entries?

Answer-4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adjustment entries are made in books of account before preparation of financial statement

and aids in recording accounts up-to-date on the basis of accrual basis of accounting. The

adjustment entries are passed due to following reasons:The adjustment entries are passed due

to following reasons:

(a) It ensures allocation of prepaid expenditure to the period it is incurred;

(b) Revenue which are unearned are to be allocated in the year in which it is realised.

(c) Expenses which are accrued are to be allocated in the year in which it is spend.

(d) Revenue earned but not realised during the current year.

Closing entries are posted in the books of accounts on the last day of the company financial

year. Generally all the closing entries relate to the profit and loss account of the company .

The intention of passing such an entry is to sell all revenue and expense account to zero.

Thus, it shall ensure fresh start of all account at the beginning of each financial year.(Lofoya

Pvt Ltd., 2018) The balances of profit and loss account are transferred to retained earnings at

the end of reporting period.

References:

Accounting-Simplified.com, 2017. What is a Trial Balance?. [Online]

Available at: https://accounting-simplified.com/trial-balance.html

[Accessed 23 September 2018].

Lofoya Pvt Ltd., 2018. Permutation-Combination. [Online]

Available at: http://www.lofoya.com/Aptitude-Questions-and-Answers/Permutation-and-Combination/

l3p1

[Accessed 23 September 2018].

MyAccountingCourse.com, 2018. Adjusted Trial Balance. [Online]

Available at: https://www.myaccountingcourse.com/accounting-cycle/adjusted-trial-balance

[Accessed 23 September 2018].

Shultz, M., 2018. What Are Adjusting Journal Entries. [Online]

Available at: https://www.blackline.com/blog/account-reconciliations/adjusting-journal-entries/

[Accessed 23 September 2018].

and aids in recording accounts up-to-date on the basis of accrual basis of accounting. The

adjustment entries are passed due to following reasons:The adjustment entries are passed due

to following reasons:

(a) It ensures allocation of prepaid expenditure to the period it is incurred;

(b) Revenue which are unearned are to be allocated in the year in which it is realised.

(c) Expenses which are accrued are to be allocated in the year in which it is spend.

(d) Revenue earned but not realised during the current year.

Closing entries are posted in the books of accounts on the last day of the company financial

year. Generally all the closing entries relate to the profit and loss account of the company .

The intention of passing such an entry is to sell all revenue and expense account to zero.

Thus, it shall ensure fresh start of all account at the beginning of each financial year.(Lofoya

Pvt Ltd., 2018) The balances of profit and loss account are transferred to retained earnings at

the end of reporting period.

References:

Accounting-Simplified.com, 2017. What is a Trial Balance?. [Online]

Available at: https://accounting-simplified.com/trial-balance.html

[Accessed 23 September 2018].

Lofoya Pvt Ltd., 2018. Permutation-Combination. [Online]

Available at: http://www.lofoya.com/Aptitude-Questions-and-Answers/Permutation-and-Combination/

l3p1

[Accessed 23 September 2018].

MyAccountingCourse.com, 2018. Adjusted Trial Balance. [Online]

Available at: https://www.myaccountingcourse.com/accounting-cycle/adjusted-trial-balance

[Accessed 23 September 2018].

Shultz, M., 2018. What Are Adjusting Journal Entries. [Online]

Available at: https://www.blackline.com/blog/account-reconciliations/adjusting-journal-entries/

[Accessed 23 September 2018].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.