Financial Statement Presentation for Non-reporting Entities Report

VerifiedAdded on 2023/05/31

|12

|600

|344

Report

AI Summary

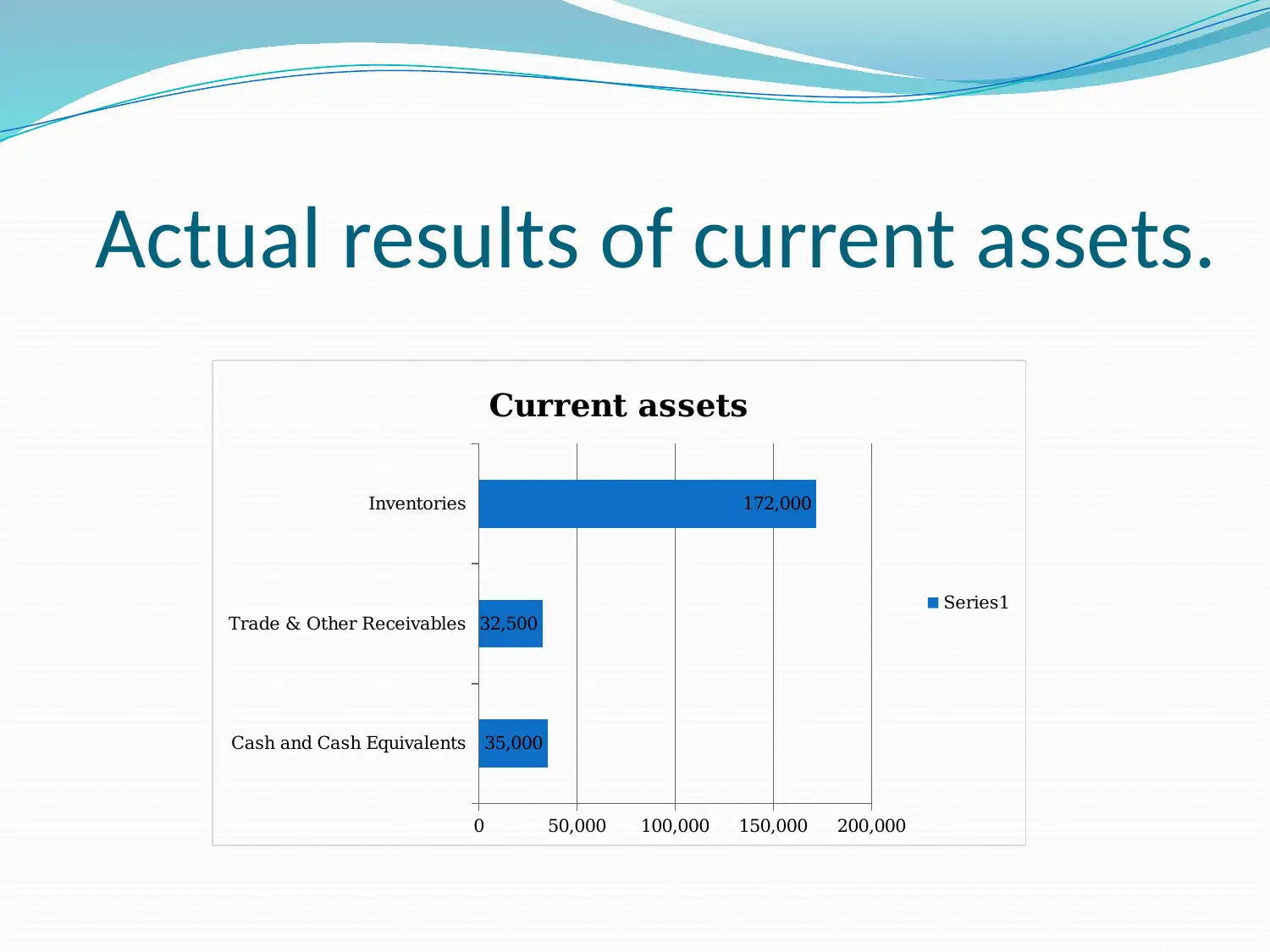

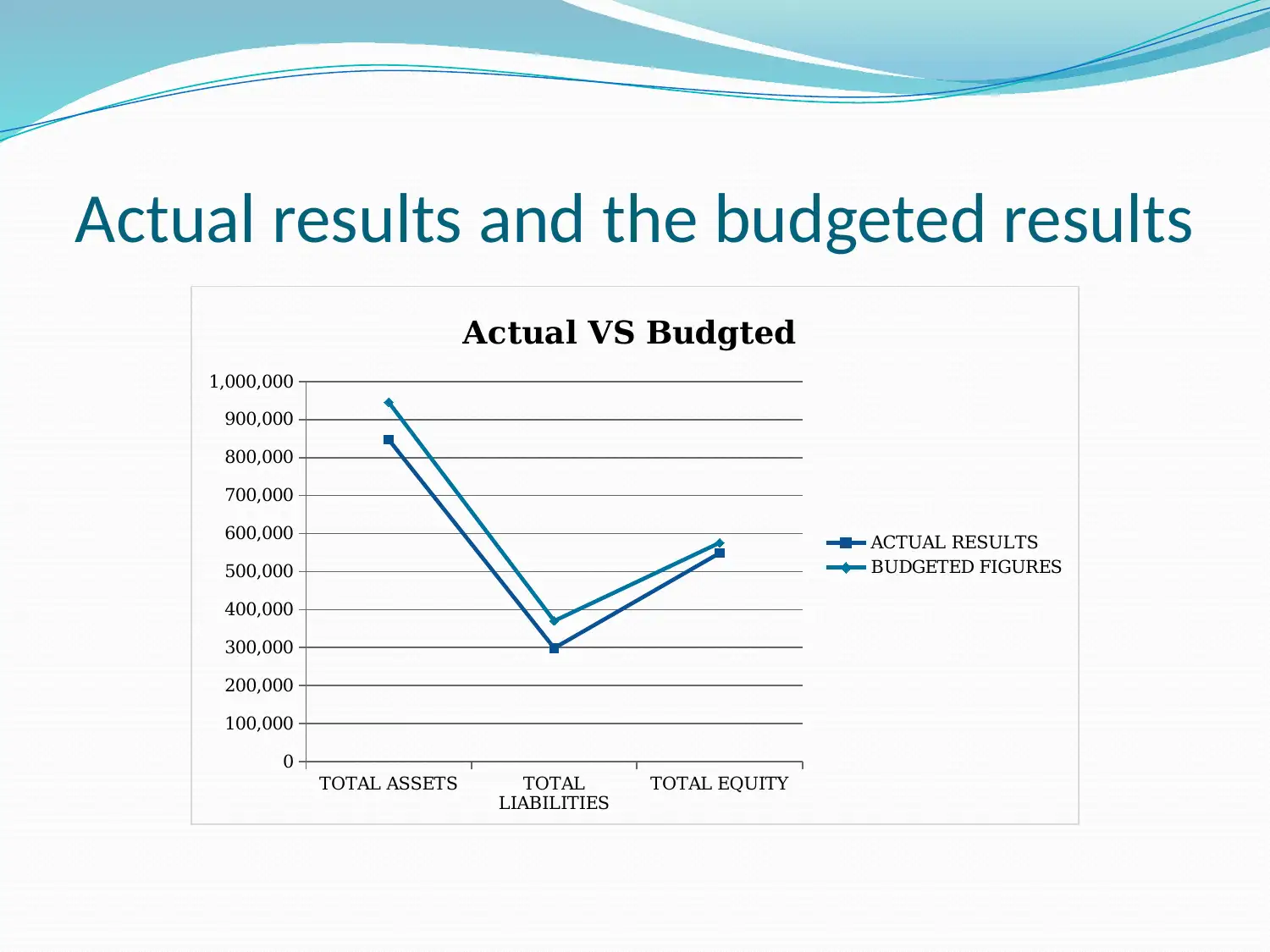

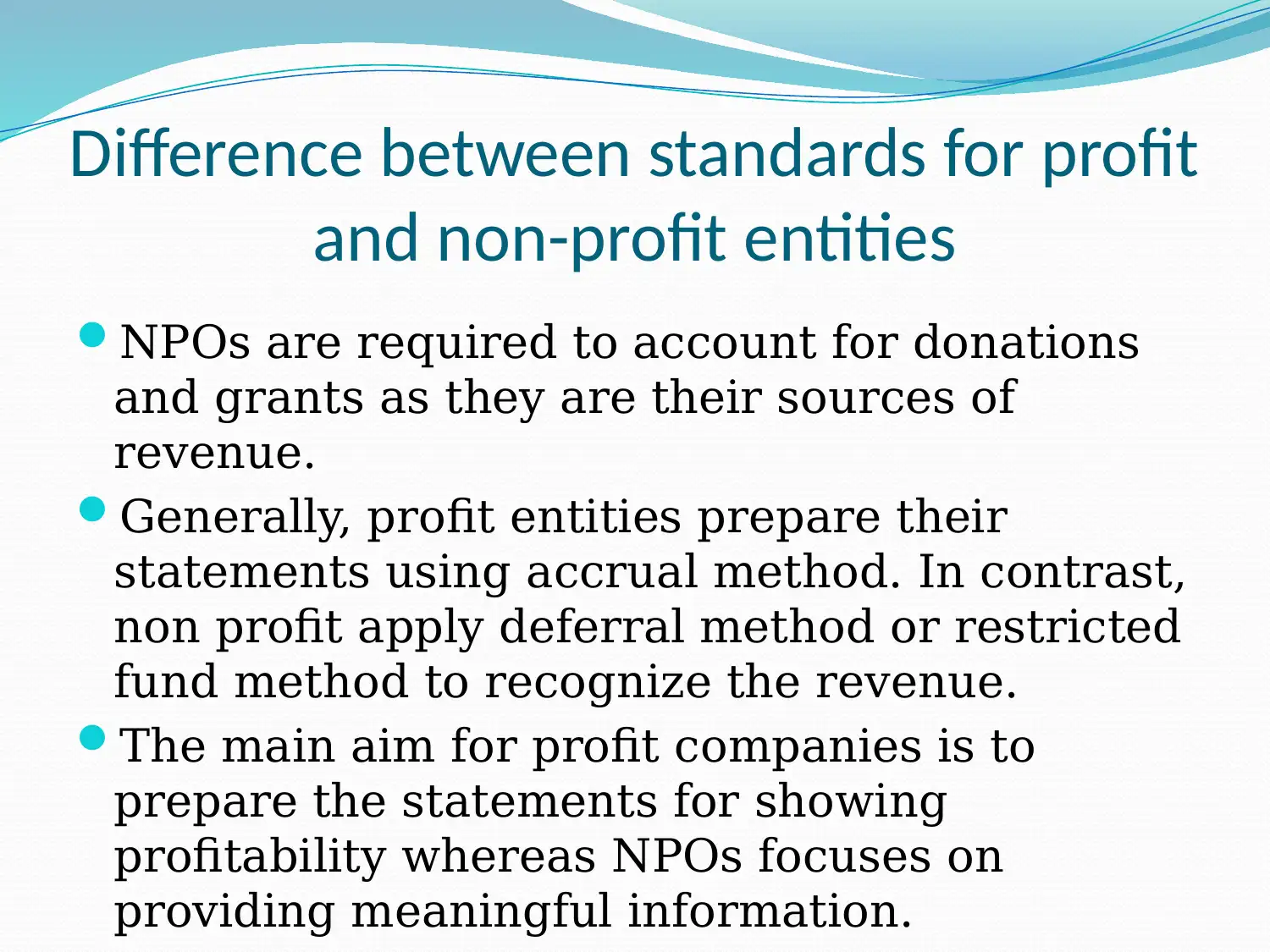

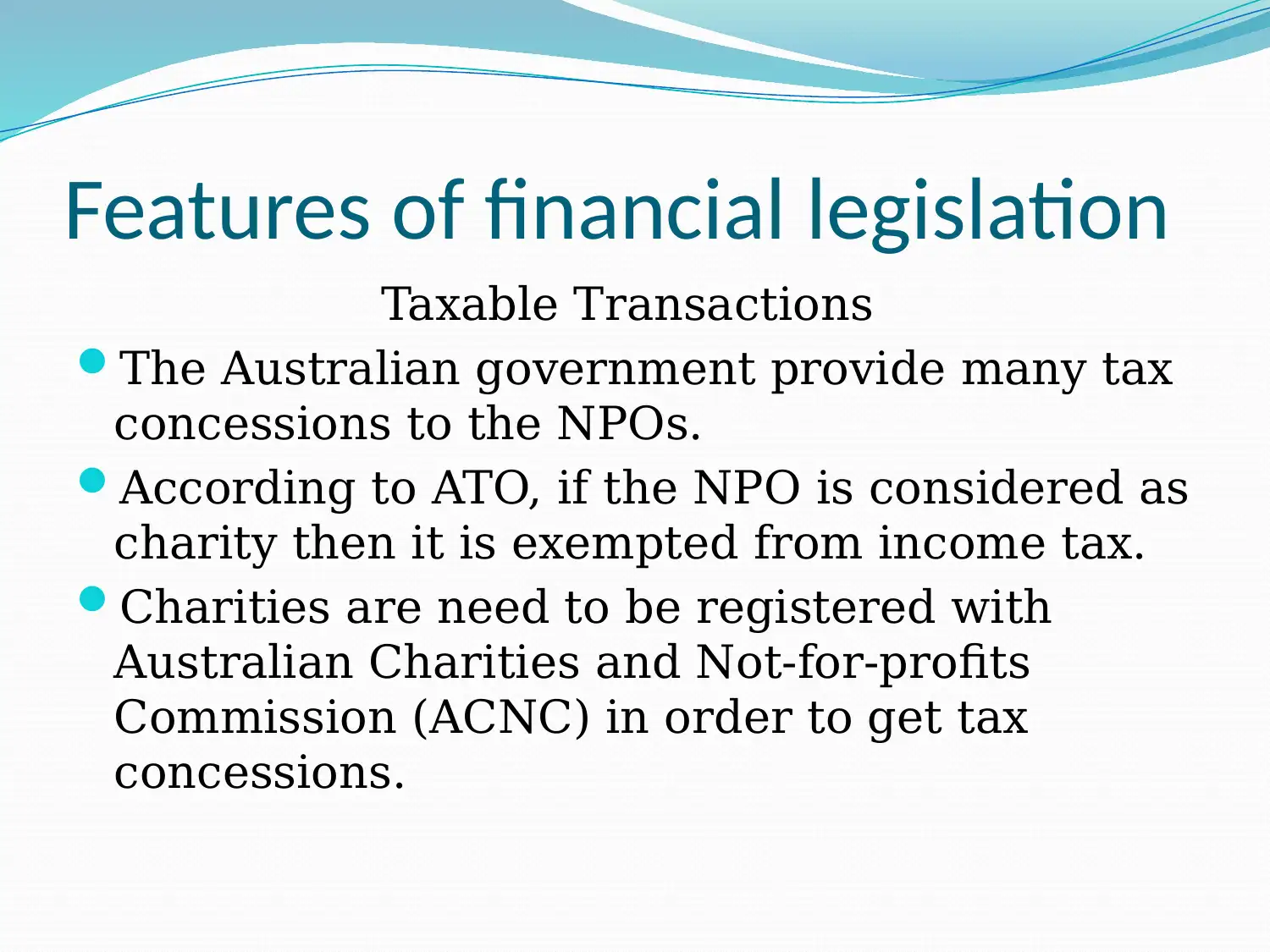

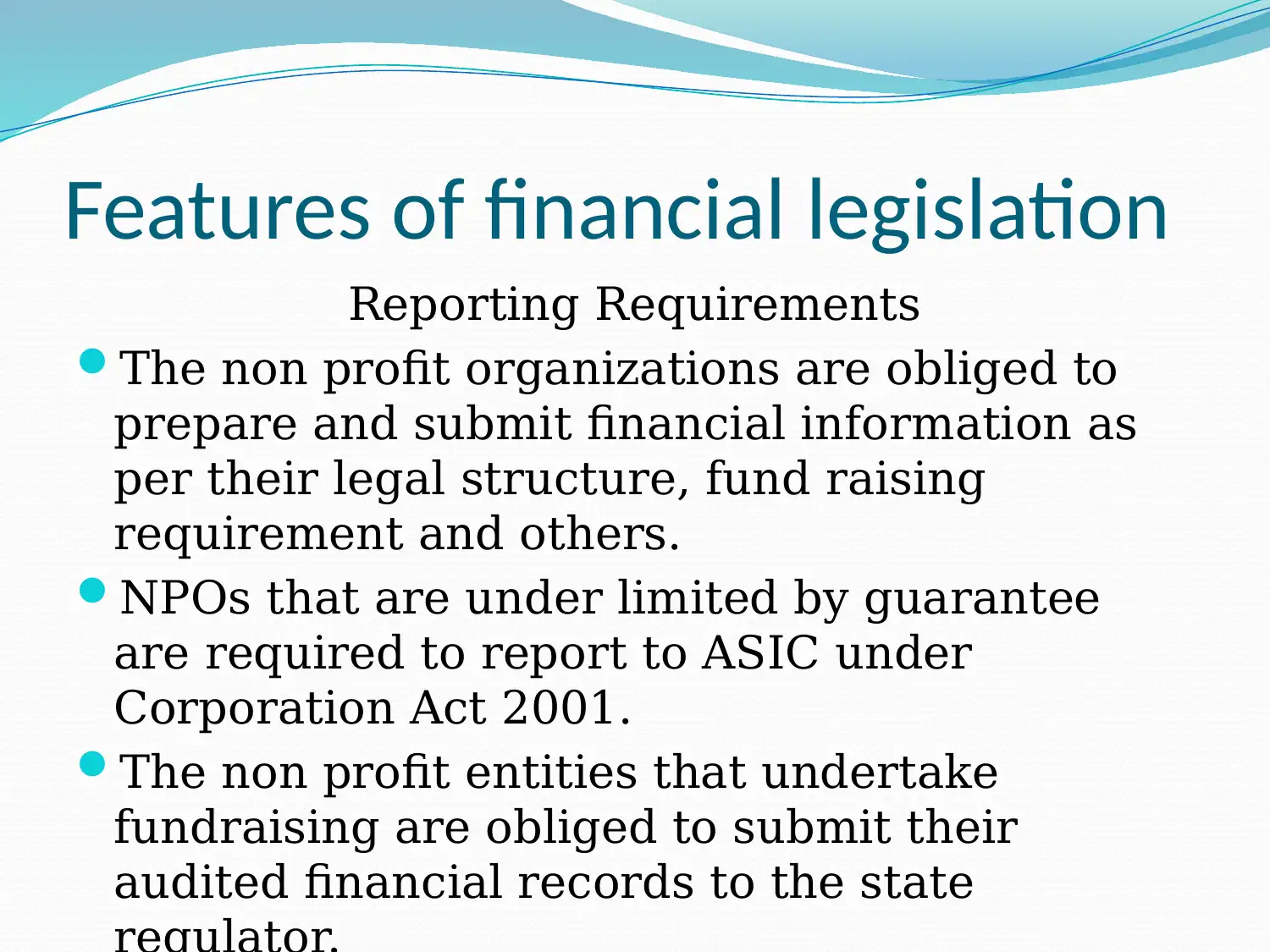

This report provides an analysis of financial statement presentation, focusing on actual versus budgeted results, variance analysis, and differences in accounting standards between for-profit and non-profit entities. It highlights the importance of understanding financial legislation, including taxable transactions and reporting requirements for non-profit organizations in Australia, referencing sources like the Council on Foundations, AIC, and ATO. The report includes data on assets, liabilities, and equity, illustrating the variance between actual and budgeted figures, and emphasizes the need for non-profit organizations to adhere to specific accounting practices and reporting obligations.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.